presentations on sustainability - shopsplusproject.org · the impact of nhif accreditation on...

TRANSCRIPT

Presentations on Sustainability

• Global Workshop for Social Franchising in Health – Jeanna Holtz, Abt Associates

• Strategic Purchasing of Quality Health Services from Private Providers in Myanmar –Han Win

Htat, PSI

• Linking Social Franchising Clinics to Health Financing Mechanisms – Joyce Wanderi-Maina, PSI

• The Impact of NHIF Accreditation on Sustainability and Contraceptive Uptake – MSK

• Vouchers in Uganda: An Accelerator of Access to Quality FP Services

• Masterclass: The Essentials of Contracting to Provide Family Planning and Reproductive

Health Services – Jeanna Holtz, Abt Associates

• Growing Businesses to Grow Health Impact – Sylvia Wamuhu, PSI

• Improving Business Skills – Miguel Antonio S. Lindo, PSPI

• Social Franchising in Lima: Expanding the Value Proposition

• Sustainability and Affordability in Low-Income Countries – Alexis Aimé Miharimanana, MSI

• Enhancing Sustainability of Social Franchising Supervision through Decentralization –Genet

Mengistu, IPPF

• Sustaining Sun Quality Health Network through Linkage with Health Financing Schemes –

Socheat Chi, PSI

• The Philippines’ Evolving Health Financing Landscape - Miguel Antonio S. Lindo, PSPI

Unlocking Sustainability

Understanding expectations and tradeoffs

Linking social franchising into broader health financing

mechanisms

Linking social franchising into broader

health financing mechanisms:

Overview of health financing

Jeanna Holtz

Abt Associates

28 September 2017

Global Workshop on Social Franchising

Accra, Ghana

5

We need a common language

mCPR

Method-

mix

Unmet

need

Risk

pooling

Purchasing

Mobilizing

resources

Health Financing Family Planning

6

Universal health coverage

Definition: People can access the care they

need without financial hardship

• UHC is an aspiration,

and not:

– a program

– insurance

7

Health financing is part of HSS

8

Health financing functions

Revenue

collection

Pooling

Purchasing• What will be purchased? (benefits)?; Who to

purchase from (public, private)? What payment mechanism to use?

• The accumulation of pre-paid revenues on behalf

enrolled members, whether privately or publically…to

enable transfer of risks between healthy and sick,

and wealthy and poor.

• Need source of funds, collection mechanism and collector. Examples:

– Government collects taxes from citizens

– Employer pays premiums to an insurer on behalf of employees

9

Financing UHC

• Countries pursue UHC using a mix of financing mechanisms

– Publicly financed services

– Insurance

Publicly-financed: social health insurance, national health insurance, government-sponsored insurance

Privately-financed:

– Products for the wealthy/formal sector

– Products for low income households/informal sector: community-based (mutuelles), microinsurance

• Majority of population in many LMICs relies on out of pocket spending

– Result: financial hardship/forgo care

Strategic Purchasing of Quality Health Services

From Private Providers In MyanmarHan Win Htat, National Director

Sun Quality Health Network, Population Services International Myanmar

12

3.8 Achieve universal health coverage, including financial risk

protection, access to quality essential health-care services and

access to safe, effective, quality and affordable essential medicines

and vaccines for all

2

13

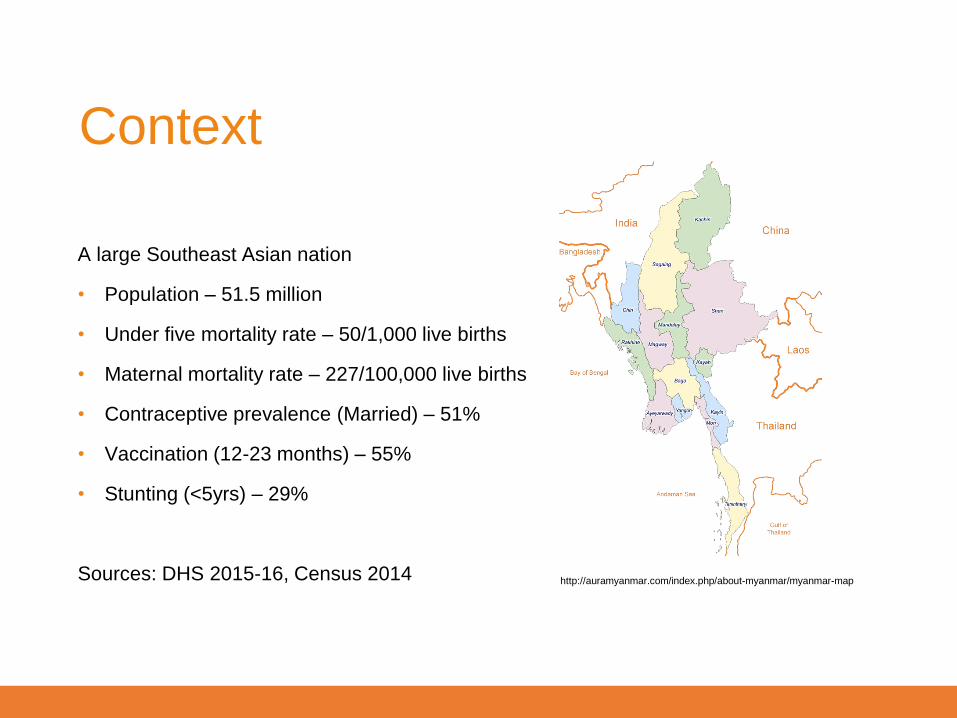

A large Southeast Asian nation

• Population – 51.5 million

• Under five mortality rate – 50/1,000 live births

• Maternal mortality rate – 227/100,000 live births

• Contraceptive prevalence (Married) – 51%

• Vaccination (12-23 months) – 55%

• Stunting (<5yrs) – 29%

Sources: DHS 2015-16, Census 2014 http://auramyanmar.com/index.php/about-myanmar/myanmar-map

Context

14

Myanmar’s UHC 2030 Vision

15

NHP Conceptual Framework

16

• Sun Quality Health Network: A social franchise network of 1,200+ general practitioners

• Mainly urban and peri-urban

• Focuses on reproductive health, HIV, malaria, tuberculosis, and maternal and child health

• Sun offers the government of Myanmar the opportunity and mechanism to commission services from private sector providers to compliment the public sector at predictable costs and quality

Sun Quality Health

17

Being at the table consistently is

important

18

Strategic

Purchasing Pilot

19

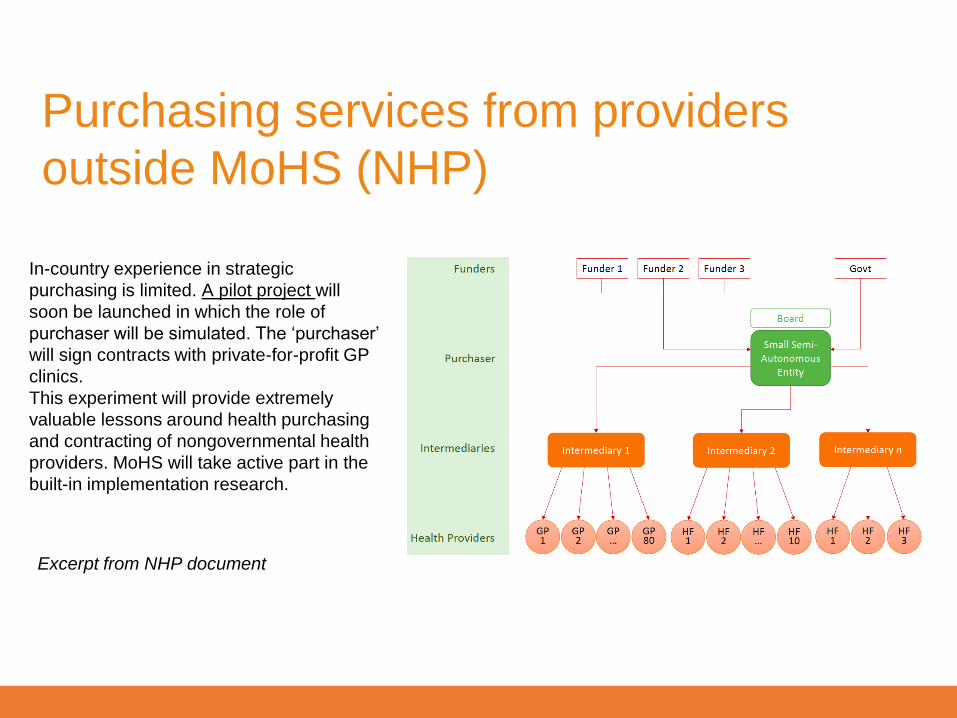

Purchasing services from providers

outside MoHS (NHP)

Excerpt from NHP document

In-country experience in strategic

purchasing is limited. A pilot project will

soon be launched in which the role of

purchaser will be simulated. The ‘purchaser’

will sign contracts with private-for-profit GP

clinics.

This experiment will provide extremely

valuable lessons around health purchasing

and contracting of nongovernmental health

providers. MoHS will take active part in the

built-in implementation research.

20

Under strategic purchasing arrangements, this model of care can increase access by

low-income consumers and achieve good value for money for public subsidy.

Project Objectives

In particular the project aims to:

• Increase the range of services

provided

• Decrease out of pocket payments

• Decrease the time to seek

treatment at a qualified provider

from the start of signs and

symptoms

21

Package of services

Inclusion criteria for

beneficiaries

Monthly capitation amount

Pay for performance

targets

Medical records

Critical Planning Steps

http://www.jointlearningnetwork.org/uploads/files/resources/UHC_Learning_Brief_Series_-_No1_Package_of_Services_FINAL_(1).pdf

http://www.jointlearningnetwork.org/uploads/files/resources/UHC_Learning_Brief_Series_-_No2_Strategic_Purchasing_FINAL_(1).pdf

22

• 2-year longitudinal study

• Base-line, mid-line and end-line

• 2 sites in peri-urban Yangon

• 11,000 study population

• 5 Sun Quality Health providers

• MOHS joined the project as the

Co-investigator.

Methodology

2,797 Potential

households

Screened

291 households

rejected

2,506 households registered

(10,881 eligible beneficiaries )

1,049 households eligible for

health surveys (41.9%)

1,334 individuals reported

seeking health

1,108 women reported

seeking health for FP or

fertility reasons

23

Five Categories

• Child health – IMCI approach, nutrition, immunization

• Reproductive health – short-term and long-term family planning methods, AN care, PN care, delivery support, ARH, Gender-based violence screening

• Communicable diseases – HIV, TB, Malaria

• Non-communicable diseases – Hypertension, Diabetes, Cervical cancer

• General illnesses - Minor Injuries (Abscess, Stitch), Aches and Pains, Alcoholism, Mental illness, Fever, Neuropathy, General weakness, Abdominal pain, Cough and URTI, Dengue (Grade I), Eyes (Conjunctivitis), Asthma, COPD (Primary Care Level), Fits, Epilepsy

The Package

24

Socio-economic Profiles

0%

15%

30%

45%

60%

Poorestquintile

2nd quintile Middlequintile

4th quintile Best-offquintile

Socio-Economic Profile_DB (N=1243)

(Reference: Yangon Population)

0%

15%

30%

45%

60%

Poorestquintile

2nd quintile Middlequintile

4th quintile Best-offquintile

Socio-Economic Profile_SPT (N=1263)

(Reference: Yangon Population)

25

Project Status (As of August 2017)

5 SQH doctors signed the provider contracts 7,287 beneficiaries received medical check-up

Each beneficiary received a health card MoHS team visited project clinics

UNiD generated by iris scan

Scale-up Management met 2 times

So what exactly does this look like for Su Su?

Access to low cost quality health care

• at a clinic of her choice

• close to her community

• for a wide range of FP options and illnesses

• from a friendly provider

• without financial hardship

27

• Negotiation with general practitioners to join the program

and accept the capitation model

• Lengthy identification process for poor households

• Prolonged baseline study due to temporary migrant

households

• Higher research cost due to higher burden of diseases

• Only 64% of eligible beneficiaries came to clinics for

medical screening (March-June 2017)

• Most beneficiaries are coming for “general illnesses"

Challenges

Linking Social Franchising Clinics to Health

Financing Mechanisms

Joyce Wanderi- Maina – PS Kenya

Context – Kenya

30

• Universal health coverage is a government priority in Kenya

• Decision made to anchor the country’s UHC aspirations on the

National Hospital Insurance Fund (NHIF)

• Only 1 in every 5 Kenyans has some form of health insurance

coverage

• NHIF covers 88% of those insured, private insurance – 9%, while

community based/other 3% of the population

• High out of pocket spending denying poor access to health care

▪ Approximately 41% of all outpatient

services are through private sector

▪ UHC commitments require wider

geographical foot print

▪ Social insurance traditionally biased

towards accrediting public sector

facilities

▪ Organized private sector – (social

franchising) provides an opportunity

to achieve scale and quality

Private sector role

44.10%41.60%

55.90%58.40%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Inpatient Outpatient

Providers of outpatient and inpatient Services

Private Public

Our contribution towards meeting Kenya’s

UHC goals

32

Creating demand for enrolment into social health insurance

Facilitating empanelment and quality assurance

Advocating on policy issues with the public sector

• Uptake of social insurance is a behavior change

issue requiring intensive consumer education

• Development and implementation of a marketing

strategy to drive awareness of social insurance &

product benefits

• Improve product accessibility by simplifying

registration process

• Business case for providers

Creating demand for enrollment into

social insurance

33

Key Successes - National

scheme (Supacover)

34

370,000

New H/Holds registered in

12 months

Ease of

Registration

✓ Mobile phone registration

✓ NHIF e-wallet App

Online/NHIF website

✓ Premium remittance

through mobile money

• Enrolment numbers continue to grow at an

average of 50,000 new members per month

• Ownership of marketing strategy and

communication by NHIF beyond the initial

catalytic phase

• Integrating demand creation and enrolment into

other health outreach activities

• Use of feedback for continued improvement of

the product offering

87%Attended to by medical staff

74%Got prescribed drugs at facility

92%Described staff at facility as friendly

• Franchise providers contracted to provide

services to the indigents in priority regions

• Customer education, push for registration and

utilization stimulation in 8,500 households in 17

counties

• 96% of households registered by end of pilot

• Service utilization at 63%

• Customer feedback to NHIF to advice scale up

Beneficiary perception HISP

Key Successes – Health Insurance Subsidy

program (HISP)

35

Demystification of accreditation for providers

Quality improvement plans geared towards

improving facility readiness

Application of comprehensive quality tools to

assure quality of services and accelerate

accreditation process

Collaboration with national and regional

branches to pitch franchises on premise of

quality services

Facilitating empanelment and quality

assurance

36

36

Progress to date: Tunza

37

of Tunza facilities are

NHIF empaneled

• 173 providers empaneled to NHIF

• Target is to get 60% of Tunza

facilities empaneled by 2019

• Working towards fast tracking

contracting for various schemes

46%

NHIF members registered in Tunza facilities

for OP services

$ 1,003,562 Capitated value

“

• Contracting of small private sector providers –

preference was larger facilities

• Systems to measure and regulate service quality

• Recognition of other QA systems such as

franchise standards and external accreditation

• Balanced tariffs and efficient payment

mechanisms e.g. capitation amounts

• Advocacy for inclusion of comprehensive FP/RH

services and creating awareness of benefits

Advocating on policy issues

39

Growing recognition

of franchises and

notable readiness to

work with organized

private sector

39

“

▪ Increasing registration of dependents - lack of required documents

results to partial registration

▪ Clear communication on penalties and how they accrue to reduce

attrition as well as exclusions

▪ Simplification of benefits package to reduce subjective

interpretation by providers and clients

▪ Significance of the membership cards at the point of service

Opportunity: Using provider and customer

feedback to strengthen national schemes

▪ Government in the process of rollout FMS in

2,458 private and faith based (FBOs) facilities

in a phased approach

▪ Linda Mama comprises of an expanded

package of benefits to pregnant women and

their newborns for periods of one year

▪ The cover expires 90 days after delivery

Opportunity: Public sector contracting (Linda

mama) – skilled delivery

41

One on One Household sessions

Network Management Organization :An organization that

aggregates healthcare providers into a structured network

and presents this network to payers and healthcare

consumers.

• Customers: access to a panel of

quality providers, lower premiums or

lower out-of-pocket costs.

• Providers: Increased client volumes

(profitability)

• Insurance Companies: healthcare

services which meet a pre-defined set

of standards, lower administration fee

42

The future - Aggregation of providers

Thank You!Thank you

The impact of NHIF accreditation on

sustainability and contraceptive uptake

MSK

SEPTEMBER 2017

Marie Stopes International45

MSK’s value proposition• MSK set up the Amua social franchise network in 2004.

• Offer private providers a relevant and compelling ‘value proposition’ in order to:

• Motivate them to provide SRH services.

• Build their capacity to provide quality SRH services.

• MSK supports franchisees with NHIF accreditation, e.g.

• Acquisition of necessary licences and certificates.

• Support with SLAs for waste disposal, pharmacies and lab companies.

• Navigation of the process - NHIF Compliance Code/Certificate; Board

approvals; facility gazettment and tracking.

Marie Stopes International46

NHIF accreditation of Amua facilities

0

20

40

60

80

100

120

140

160M

ay-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Mar-

16

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Se

p-1

6

Oct-

16

No

v-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Ju

n-1

7

Cu

mu

lati

ve

Da

ta

Month

Marie Stopes International47

NHIF’s impact on franchisee sustainability

Positive:

• Created opportunities for cross ‘selling’ services

• Improved provider reputation in their communities

• Improved provider status with other companies (e.g. insurance, workplaces, etc.)

• Client member volumes increasing, promoted through word-of-mouth by existing

members

• Utilisation increasing, cited as a benefit but also a challenge

• Client confidence - NHIF as a sign of service quality

• NHIF management information system (MIS) - providers like the automated

reporting and verification of client membership.

Marie Stopes International48

NHIF’s impact on franchisee sustainability

Negative:

• Increasing utilisation, including unnecessary visits (the Patient Moral Hazard).

• Influx of high risk clients / adverse selection i.e. chronic clients.

• Length of time to get empaneled

• Slow release of the capitation payments.

• Membership verification

• Provider changes

• Lack of scheme specificity

Marie Stopes International49

NHIF’s impact on contraceptive uptake

• Capitation covers all but permanent methods.

• NHIF guidelines on FP is vague and contradictory.

• Situation exacerbated by branch offices:

• Some branch managers unsure of the methods themselves.

• Others specify that implants are too expensive to be included.

• Consequently most providers are not providing FP services under capitation.

• Women are paying fees even if enrolled.

• This is probably impacting on method choice – e.g. chose OCP over more

expensive implants

• Providers benefit from Gov’t supplies of FP commodities but this is unreliable and

implants they are ‘last in the queue’ over public health facilities.

• Providers do not think it’s feasible to provide FP, esp. LARC, under capitation.

THANK YOU

51

- Meyer C, Bellows N, Campbell M, Potts M (2011)

52

Population

34.6 million people

34.6%

$1.90

28.4%

Fertility Rate

5.4

53

60%

Working through 220 private sector BlueStar franchisees,

using vouchers to target valuable subsidies to the most

vulnerable populations, reducing unmet need amongst

the lower wealth quintiles

.

Community Based Distributors trained and equiped to conduct community based mobilization, counseling and referral using

vouchers

Health workers trained to provide Quality counselling an

FP services to the most vulnerable populations

BLUESTAR

Improving access to affordable quality FP services including LARCs & PMs at health facility and community levels in the Private Sector

54

Family Planning Voucher (220), Youth Voucher (53). A client gets a service at any franchisees at no extra cost.

Vouchers distributed to

clients through the Community

Based Distributors

56

Clients reached with FP services

through Franchisees

rred ARC/PM

ervice

Voucher Redemption,

the highest ever in the 6year existence of

Voucher programme

Under the age of 24years

JULY, 2015 – JULY 2017Trends and Performance

202,218 172,075 91% 81% 44%

57 57

Learning

Perceiving Quality as a driver of business growth

Learning

58

Vouchers empower young people to demand for services at the health facility without fear of being judged

A driver of Business Growth

Infrastructure of the Franchisees improved as a result of reimbursement realized from offering services.

59

Learning

60

Neal Creative | click & Learn moreNeal Creative ©

Then 2014 Now 2017

SEE HOW FAR WE HAVE COME

Masterclass:

The Essentials of Contracting to Provide

Family Planning and Reproductive Health

Services

Jeanna Holtz

Abt Associates

28 September 2017

Global Workshop on Social Franchising

Accra, Ghana

63

QUIZ!

64

1. Which of these entities might purchase services from private providers?

a) Government

b) Private Employers

c) Private Insurance Companies

d) Donors

e) All of the above

QUIZ: Contracting basics

65

1. Which of these entities might purchase services from private providers?

a) Government

b) Private Employers

c) Private Insurance Companies

d) Donors

e) All of the above

QUIZ: Contracting basics

ANSWER

66

2. Why might private providers contract with governments?

a) Expand their client base

b) Improve their legal expertise

c) Tap into new revenue streams

d) A and C

e) All of the above

QUIZ: Contracting basics

67

2. Why might private providers contract with governments?

a) Expand their client base

b) Improve their legal expertise

c) Tap into new revenue streams

d) A and C

e) All of the above

QUIZ: Contracting basics

Contracts can help providers gain new clients and

access additional, stable sources of funding to expand

their practices and service offerings.

ANSWER

68

QUIZ: Contracting basics

3. Why might a government contract a private provider to deliver FP services?

a) Increase the number of service delivery sites in underserved areas

b) Help government avoid controversial or culturally sensitive issues

c) Improve efficiency in the health system

d) All of the above

69

QUIZ: Contracting basics

3. Why might a government contract a private provider to deliver FP services?

a) Increase the number of service delivery sites in underserved areas

b) Help government avoid controversial or culturally sensitive issues

c) Improve efficiency in the health system

d) All of the above

ANSWER

70

QUIZ: Contracting, UHC, and FP

4. Three common dimensions of UHC include:

a) Financial protection, facilities included, payment mechanisms

b) Payment mechanisms, health management information systems, services covered

c) Population covered, financial protection, services covered

d) Population covered, financial protection, facilities included

71

QUIZ: Contracting, UHC, and FP

4. Three common dimensions of UHC include:

a) Financial protection, facilities included, payment mechanisms

b) Payment mechanisms, health management information systems, services covered

c) Population covered, financial protection, services covered

d) Population covered, financial protection, facilities included

UHC focuses on increasing the number of people able to

access a greater range of services with increased

financial protection.

ANSWER

72

5. Insurance programs that support achieving UHC

always include benefits for FP.

True or False?

QUIZ: Contracting, UHC, and FP

73

5. Insurance programs that support achieving UHC

always include benefits for FP.

True or False?

QUIZ: Contracting, UHC, and FP

False. Benefits are often limited, and may focus on

inpatient services

ANSWER

74

6. Purchasers might face challenges contracting with private providers because:

a) Private sector is large and fragmented

b) Providers are accredited

c) Purchasers lack sufficient resources to pay private providers enough to cover their costs and make a reasonable return

d) A and C

e) All of the above

QUIZ: Contracting, UHC, and FP

75

6. Purchasers might face challenges contracting with private providers because:

a) Private sector is large and fragmented

b) Providers are accredited

c) Purchasers lack sufficient resources to pay private providers enough to cover their costs and make a reasonable return

d) A and C

e) All of the above

QUIZ: Contracting, UHC, and FP

ANSWER

76

7. Government contracting with private sector may support UHC by:

a) Encouraging efficient use of financing resources

b) Establishing a range of services that each provider must offer

c) Expanding access to subsidies and reducing financial barriers for underserved groups

d) Increasing the number of health facilities delivering covered services

e) All of the above

QUIZ: Contracting, UHC, and FP

77

7. Government contracting with private sector may support UHC by:

a) Encouraging efficient use of financing resources

b) Establishing a range of services that each provider must offer

c) Expanding access to subsidies and reducing financial barriers for underserved groups

d) Increasing the number of health facilities delivering covered services

e) All of the above

QUIZ: Contracting, UHC, and FP

ANSWER

78

Session agenda

• Overview of SHOPS contracting lifecycle

• Group activity on contracting

• Wrap up

79

Session Objectives

• Articulate how contracting supports objectives of

purchasers and providers

• Understand contracting lifecycle

• Identify obstacles/solutions to create and sustain

contracts for FP services

• Know where to go for additional resources

80

Contracting within the health sector

• Specify “gives and gets”

• Examples: service agreement,

lease, grant, franchising

• Focus today: service agreements

(purchaser and provider)

Contracts are legal instruments that set forth obligations,

rights, and duties of the partners involved.

81

Why contract?

• What motivates a government purchaser of health care

to contract with a health provider?

• What motivates a private provider to contract with a

government purchaser?

82

Objectives of purchasers (e.g. government)

• Improve access, relieve pressure on public facilities

• Harness private sector expertise and resources

• Improve efficiency

• Avoid controversial, culturally sensitive issues

83

Objectives of providers

• Increase revenue; establish regular income

source

• Expand and maintain client base

• Increase operating efficiency

• Fulfill social mission

84

The Contracting Lifecycle

85

The Contracting Lifecycle

Contracts can follow a “one cycle” pathway

86

The Contracting Lifecycle

…or a repeating cycle

87

Stage One: Evaluate Feasibility

88

Stage One: Evaluate Feasibility

• Assess internal, external environment

• Analyze strengths, weaknesses, opportunities, and

threats

• Understand payment mechanisms

• Fixed rates, results-based, or capitation are replacing grants, input-based, cost-based agreements

89

Stage Two: (Re)Design the Contractual

Relationship

90

Stage Two focuses on negotiation

• Payment mechanism and rates

• Covered services (including LA/PM)

• Monitoring and reporting

• Accreditation (quality)

• Dispute resolution

• Termination terms

Stage Two: (Re)Design the Contractual

Relationship

91

Stage Three: Implement the Contract

92

FP service providers need to

• Train staff for new roles and procedures

• Ensure adequate resources

• Staff

• Supplies

• Equipment

• Educational materials

Relationship management is key!

Stage Three: Implement the Contract

93

Stage Four: Manage, Monitor, Evaluate

94

Purchasers and providers will monitor:

• Volume, quality, efficiency, cost, client feedback

Providers should additionally monitor:

• Timeliness, accuracy of

payments

• Profitability

Stage Four: Manage, Monitor, Evaluate

95

Providers should establish procedures to track indicators

and prepare for audits:

• Clinical, utilization indicators

• % of target population reached

• # of FP services provided

• # of women counseled on FP

• # of adverse FP incidents

• # of CYPs

Stage Four: Manage, Monitor, Evaluate

96

Providers should establish procedures to track indicators

and prepare for audits:

• Non-clinical indicators

• Client satisfaction

• Costs

• Timeliness of reports

Stage Four: Manage, Monitor, Evaluate

97

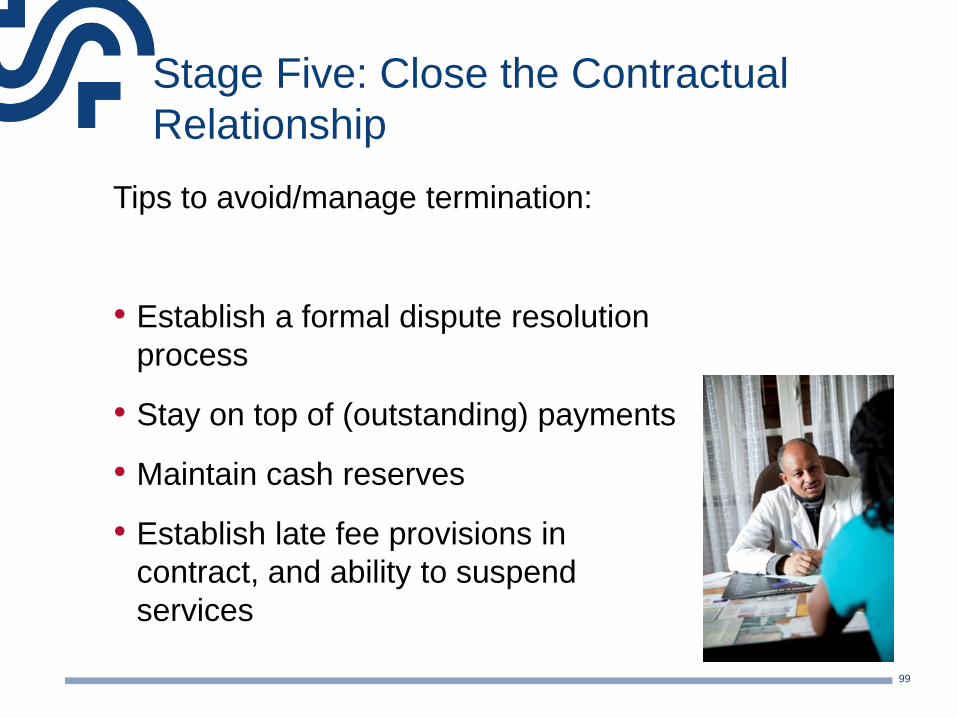

Stage Five: Close the Contractual

Relationship

98

Contracts can end in two ways:

• Closure: Contract ends as planned

• Termination: Action taken to end contract before its

full performance (unplanned)

NOTE: Providers should understand their

obligations under termination, including

length of time to continue service delivery.

Stage Five: Close the Contractual

Relationship

99

Tips to avoid/manage termination:

• Establish a formal dispute resolution

process

• Stay on top of (outstanding) payments

• Maintain cash reserves

• Establish late fee provisions in

contract, and ability to suspend

services

Stage Five: Close the Contractual

Relationship

100

The Contracting Lifecycle

101

Small group work

Case study:

• Takes place in country of Manyland

• Involves the Ministry of Health and the Health Association of Manyland

Instructions:

30 minutes

• Read case study provided on tables

• Discuss based on prompts

• Prepare brief response to question

20 minutes

• Groups report out

102

Group report out

103

Key Takeaways

• Trend toward contracting for FP services to access

patients and revenue streams

• Success in contracting occurs at all stages of the

contracting lifecycle.

• Variety of skills needed to succeed under contracting

• Invest in relationships

• It’s a learning process!

104

SHOPS Plus has resources on contracting

• Published 2 primers on contracting for FP/RH

• One for policymakers, donors

• One for providers

• online FAQ tool to complement primers at: https://www.shopsplusproject.org/contractingfaq

• eLearning course at USAID Global Health eLearning

Center: https://www.globalhealthlearning.org/course/contracting-family-

planning-and-reproductive-health-services

Tables

Innovations in Social Franchising

Creating Sustainable Businesses

Improving business skills and creating linkages to business

improvement loans

Sylvia Wamuhu – PS Kenya

Growing businesses to grow health impact

108

Program Overview

Objectives of the overall program

• Offer holistic quality improvement leading to SafeCare

accreditation

• Help in bridging provider gap in business skills

• Provide access to affordable financing

173Tunza Providers Implementing

Business Skills

General Business Operations:

• Business registration, tax and statutory compliance, risk

management, general facility layout and client satisfaction

Financial Management:

• Setting up financial systems, bank accounts, managing debts, using

data for decision making

Stock Management:

• Manual and automated

Marketing and Demand Creation:

• Basic / community marketing techniques to spur growth

How the business program works

Sensitization, Recruitment

Business Assessment

Business Improvement Plan

Training / Continuous Support supervision and linkage to credit

Stepwise Business Improvement

Using business levels to help clinics grow & improve…

• Segment the providers into different levels to target resources and create efficiencies.

• Do not implement a “one size fits all” model (due to different sized clinics with varying capability to take on new services)

Business Level

Score Bracket Business Description

Level 1 0% - 25% No Business Skills

Level 2 26% - 50% Limited Business Skills

Level 3 51% - 75%Good Business

Management

Level 4 76% - 100%Excellent Business

Management

• Client Flow: Increased by an avg. of 35%!!!!!

• Revenue: Up by 28%

• Improved systems: 41 facilities have Clinic

Management Systems (up from 15)

• 59% - have moved from one level to another

• 29% - accessed credit

Tunza facility Levels

Level 1: 24 facilities Level 3: 78 facilities

Level 2: 60 facilities Level 4: 12 facilities

Impact

0

500

1000

1500

2000

2500

Level 1(0-25%) Level 2( 26-50%) Level 3( 51-75%) Level 4( 76-100%)

Business Level Vrs Average Patient No.s

Average Number of patients

Impact

What has worked?• Providers receptive to learning new business skills e.g.

Improved business systems, improved inventory management, cash management, data use etc.

• The program often led to rapid business growth/facility expansion e.g. lab

Sara (our PSI client archetype!)• Improved customer service (exit survey – 95% satisfied)• Increased scope of services (continuum of care)• Access to quality and affordable drugs

What has not worked?

Lessons learnt• Facilities in the business program perform better in

other quality related assessments e.g. NHIF, JHIC• Considerable effort initially required as providers

need hand holding

• Some providers are reluctant to share revenue data

`

Loans for growth

What worked?

• Access to financing led to improved quality of

services, increased clients and revenue

• Linkage to banks and facilitation of loans application

process

Lessons learnt• Assumption that providers lack other sources of

funding is not entirely true!

What happened?• Provides became credit worthy and banks

became more willing to lend to providers• 29% of providers accessed formal credit

through this program

• On joining the business

program, she

transformed her

approach to doing

business. Within the

first 1 year, Patients

increased from 20 to 45

per day.

Grace Wanjiku’s clinic

“The Tunza Business team

gave me business legs to stand on.’’Grace Wanjiku Masila,

Registered Nurse

I urge other clinics to

take up the advice of

the Tunza business

team and watch how

your business will

grow.

THANKYOU

Improving Business SkillsIs it a Zee or a Zor Question?Miguel Antonio S. Lindo

Friday, 29 September 2017

Marie Stopes International119

Who we are in the Philippines

To provide sustainable sexual and reproductive health services of the highest quality to Filipinos Nationwide

Successful Franchisees Lead to Family Planning

BlueStar Operational Excellence

Clinical Standards Execution

Active Demand Generation Activities

Marie Stopes International120

The challenge of managing two bottom lines

“[We] must effectively manage two bottom lines when operating a social

franchise; mission results and financial results.”

Benjamin C. Litalien, CFE

“[The manager] must be committed to the mission of the nonprofit and

motivated to control cost of goods, provide good training and supervision

for employees and constantly monitor and market sales.”

Judi Bishop, executive director of the Fort Worth YWCA

Marie Stopes International121

Understanding our client – the franchiseeGraduate of a 2 year course

Primarily a Service Provider

Ages between 40-60 years old

Before BlueStar either called for home service

Assistants of Doctors in Maternity Hospitals

No established professional fees

Earned by daily wage or by tips

Mothers and Home Makers

No formal graduate or post graduate education

Computer skills limited to Facebook and Facetime

Deliver babies according Philippine DOH Standards

Provide FP according to Philippine and MSI Standards

Manage employees (DOLE), facilities (PHIC), and supplies

Engage with Governing Bodies (LGU, DOH, PHIC, BIR, Bank)

Reportorial Duties of Data Validation, QTA, MDT, and others

Run a business that should gross $ 20,000.00 annually

Demand Generation

Behavior Modification

Cooking

Cleaning

Rearing Children

Husband-Wife Duties

Marie Stopes International122

Three Simple Tools to Improve Business Skills

Marie Stopes International123

The Franchise E-Factor• Model developed by Greg Nathan of the Franchise Relationships Institute

(Australia) to help franchisees and franchisors better understand their

relationship.

• Explains why dealings become strained and how both parties might use this

tension to enhance the relationship.

Marie Stopes International124

The Franchise E-Factor

GleeFranchisee

nervous but

excited and

optimistic

FeeFranchisee

feeling more

sensitive and

concerned

about return on

fees

MeFranchisee

concludes their

success is due

mainly to their

own efforts

FreeFranchisee tries

to assert their

independence

SeeMutual

understanding

and respect

grows after

frank and open

discussions

WeFranchisee

recognises

value of

collaborating

with franchisor

Dependence Independence Interdependence

AVOID:Reckless

optimismConfusion Fear Revenge Greed

COMMUNICATE:Cautious

optimismClarity

Confidence

and valueEmpathy Commitment

Fra

nc

his

ee s

ati

sfa

cti

on

Marie Stopes International125

Establishing basic financial KPI’s

• Sales

• Expenses

• Total Operating Expenses

• Net Profit

• Net Sales

• MCP Clients

• IUD Clients

• Implant Clients

• PSP Clients

• MCP 79:21

• If with PPIUD 65:35

• Interval IUD 30:70

• Implant 22:78

• Pap Smear 27:73

• MCP 80:20

• FP 60:40

• Separating Clinic Money from Personal Money

• Post Dated Check

• Giving oneself a salary

• Schedule of Payments

Develop an easy to use

Income Statement

Figure Out How Many Customers They Need

Per Month to Break Even

Maintain Per Service Cost to Revenue

Ratio

Maintain PHIC to

OOP Service Ratio

Develop Cash

Discipline

Marie Stopes International126

Continued education

The Certified Franchise Executive Program (CFE) is a career development program offered by the

Institute of Certified Franchise Executives (ICFE) of the International Franchise Association (IFA)

Education Foundation. It offers franchise professionals the opportunity to learn, grow

professionally and reach a recognized standard of excellence in the franchise community.

Franchise Asia Philippines is Asia’s biggest international Franchise Conference loaded with powerhouse international and local experts and

speakers discussing Global Best Practices, Latest Trends, and Innovations and Disruptive Strategies. It presents unparalleled educational, professional

development , and networking opportunities

Certified and Professional

Learn from the Best

40 años con bienestar

Red Plan SaludSocial Franchising in Lima: Expanding the value proposition

Red Plan Salud: Develop, Launch, Grow

Baseline Study

Market Study

MVP Study/Lean Experimentation

Franchise ModelDeveloped.

Signing of 7 agreementswith obstetric privateproviders

Adjustments to franchisemodel

Implementation of pilotwith 7 franchisees

Expansion of franchisenetwork

Expanding the Value Proposition forProviders: Business Management Training

Strategic Planning Marketing

Financial Planning Business Planning

Technical assistance

and accompaniment in

the development of

business planning and

training in business

management that

enables franchisees

to build business

skills to strengthen the

sustainability of their

clinics and reduce

overall costs of the

network, therefore also

increasing the

sustainability of the

network

Business Planning Training Topics

Business Description

Background

Actual Context

Vision, Mission, Goals

SWOT Analysis

Market Study- Marketing

Market

Client

Marketing Plan – Commercial

Strategy

Competition

Business Structure

Staff Required

Responsibilitiesof each position

OrganizationalChart

OperationsPlan

List of requirements

Classification of Direct and

Indirect Costs

Standard Costs

Break-evenPoint

FinancialPlan

Seeking and obtainingfinancial

resources

InvestmentRequired

Cash Flow

Activity Plan

Achievements

7 franchisees have strengthenedtheir business managementcapacities and have a businessplan

As part of the implementation of their business plans they have improved the infrastructure and adaptation of their clinics.

Focus on the user has improvequality of care

These factors lead to increased client demand, increased revenue, and increased provider sustainability. As the provider becomes more self-sustainable, there is less reliance on the franchising network to subsidize operating costs, thus the network becomes more sustainable as well.

Difficulties

Time to meet with all franchisees

Internet bandwidth within a franchisee clinic

Availability of commercial products

Referrals of clients

Challenges

Additional follow up of businessplan implementation

Long-term accompaniment

Implementation of médium- and long-term goals of business plan

Lightning Rounds

Sustainability and

affordability in low-income

countries

Alexis Aimé Miharimanana

Social Franchise Channel Manager

MSI Madagascar

September 2017

Marie Stopes International134

Our ambitions

• We – the SF community - are very ambitious! We want SF to achieve:

• Health impact

• Quality

• Equity

• Cost-effectiveness

• Health market expansion

• Sustainability

• We have a proposed definition of sustainability: ‘continued high quality health

outcomes over time while achieving the social goals of social franchising’.

• We expect franchisors to reduce their dependence on institutional donors.

• We hope to secure public and private health financing of services and recover

costs from franchisees.

Marie Stopes International135

The reality of a low income country

• How do these expectations apply to a low income country like Madagascar?

• 77.1% live in extreme poverty

• 83% live in rural areas

• 64% of the population is <25 years old

• mCPR is 33.3%

• Absence of financial means with the treatment 68.6%

• Net ODA received is 53% of central gov’t expense (World Bank, 2014)

• All MoH activities depend on ODA.

• This context presents challenges for many SF goals, including sustainability.

Marie Stopes International136

Addressing affordability

• We can’t achieve health impact, equity and health market expansion without

addressing affordability.

• We’ve demonstrated this is possible with our voucher programmes:

• At least 70% of SF LARC clients are voucher clients.

• Vouchers can also incentivise and finance franchisees to deliver quality.

2013 2014 2015 2016 2017 Total

Unintended pregnancies

averted19,569 62,726 39,634 47,467 17,022 186,418

Maternal deaths averted52 157 95 109 37 450

Unsafe abortions averted5,809 18,621 11,765 14,091 5,053 55,339

Total DALYs averted 25,339 80,639 50,708 60,378 21,526 238,589

Direct healthcare costs

saved (2015 GBP)704,922 2,259,577 1,427,710 1,709,883 613,194 6,715,286

Marie Stopes International137

Who pays for the service if the client can’t?

• What options are available to a low-income country like Madagascar?

• Institutional donors: Invaluable USAID funding is ending; some other key

donors are yet to be convinced of the value of investing in voucher

programmes; DFID are beginning to show interest in.

• Public health financing: No prospect the government will purchase

services in the short-medium term.

• Private health financing: Few schemes exist; don’t enrol the poorest.

Marie Stopes International138

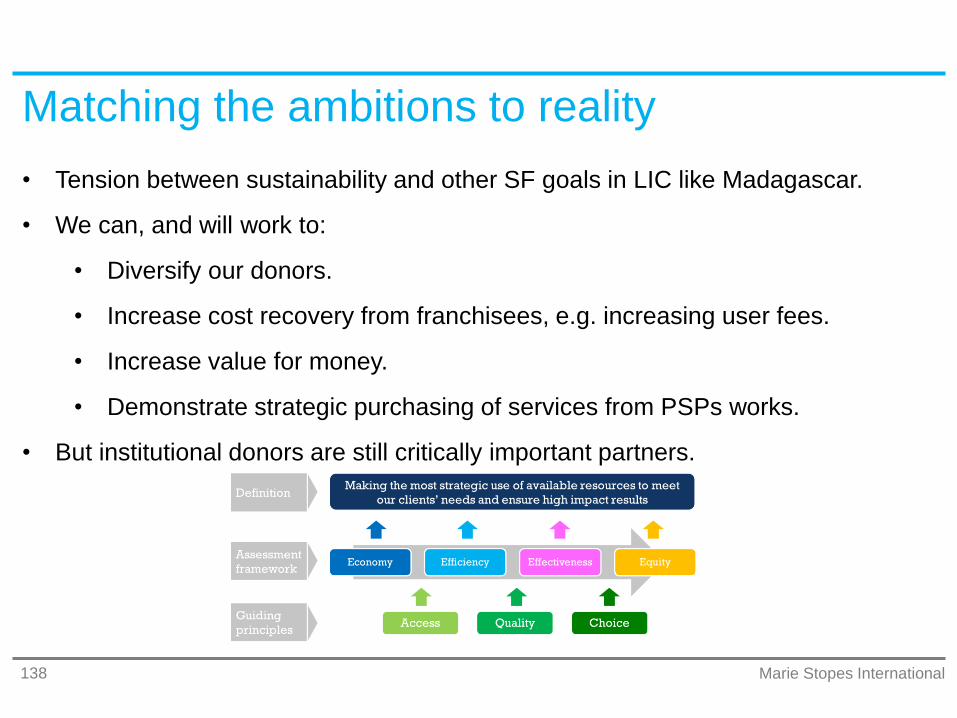

Matching the ambitions to reality

• Tension between sustainability and other SF goals in LIC like Madagascar.

• We can, and will work to:

• Diversify our donors.

• Increase cost recovery from franchisees, e.g. increasing user fees.

• Increase value for money.

• Demonstrate strategic purchasing of services from PSPs works.

• But institutional donors are still critically important partners.

Striving for Excellence in Sexual & Reproductive Health

Genet Mengistu

Executive Director

Family Guidance Association of Ethiopia

Enhancing Sustainability of Social Franchising

Supervision through Decentralization

Background Information

Established in 1966 as the first indigenous, non-

governmental, voluntary FP organization

IPPF affiliated member – since 1971

FGAE Operates in Eight Regions and Two City

Administrations

47 own facilities

1 Obst/Gynae Specialty, 8 Higher and 13 Medium Clinics

15 Youth Centres

10 Confidential Clinics

326 Social Franchised Clinics

226 Outreach sites in HLIs, Factories, Plantations,

Rural Health Posts and Public Youth Centres

Family Health Network Brand

Growth in size of Family Health Network

174 Primary FHNCs, 116 Medium FHNCs, 21 Higher FHNCs and 15

Plantation and Factories

Growth in impact

YearDALYs

Averted

CYPs

Provided

2014 119,431 181,897

2015 134,602 207,824

2016 196,330 325,443

Total 450,363 715,164

Social Franchise + Static Clinics

Shift in proportion of CYPs delivered by SF

clinics and static clinics

20%

42%62%

80%

58%38%

0%10%20%30%40%50%60%70%80%90%

100%

2014 2015 2016

SF Static

Reduced total cost of providing supportive

supervision to franchisees

-

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

600,000.00

2014 2015

FGAE’s Decentralization Approach

Decentralising management to enable

sustainable growth

8 Area Offices manage all franchisees in their area.

Model clinics have between 4-15 SF clinics anchored

to them

Quality assurance and monitoring decentralized and

costs associated with quality assurance and

supervision are reduced

Franchisees in an area are bought together for

learning and sharing

Thank You!

Sustaining Sun Quality Health Network

through linkage with health financing

schemesSocheat Chi, Executive Director, PSI Cambodia

150

Roadmap to move SQHN

toward sustainability

• Using improved business approaches as incentive

• Access to micro loan for business expansion

• From FP only to a wide range of services: including maternal child health,

malaria testing and treatment – integrated service delivery

• Quality assurance/improvement continuous medical education

• Data collection, reporting and link with national HMIS

• Accreditation

• Link to existing health financing scheme: National Social Security Fund, Health

Equity Fund etc - will require advocacy work

• Pay for service/support - membership fees

151

• Business training – financial/ HR

management and marketing

• Connect SF network to micro financial

institutions

• Expand services to fit with health

financing schemes

• Quality improvement to get accreditation

• Linkage with the NSSF for a specific

target group: garment factory workers

Areas of Focus

““

I want to put more

investment because

my clinic still has gaps

and not yet attractive,

that’s why I have few

clients, and I want to

serve more women…..

152

THANKYOU

The Philippines’ evolving

health financing landscapeOpportunities for a truly sustainable social

franchise

Miguel Antonio S. Lindo, Social Franchise Director

PSPI

September 2017

Marie Stopes International154

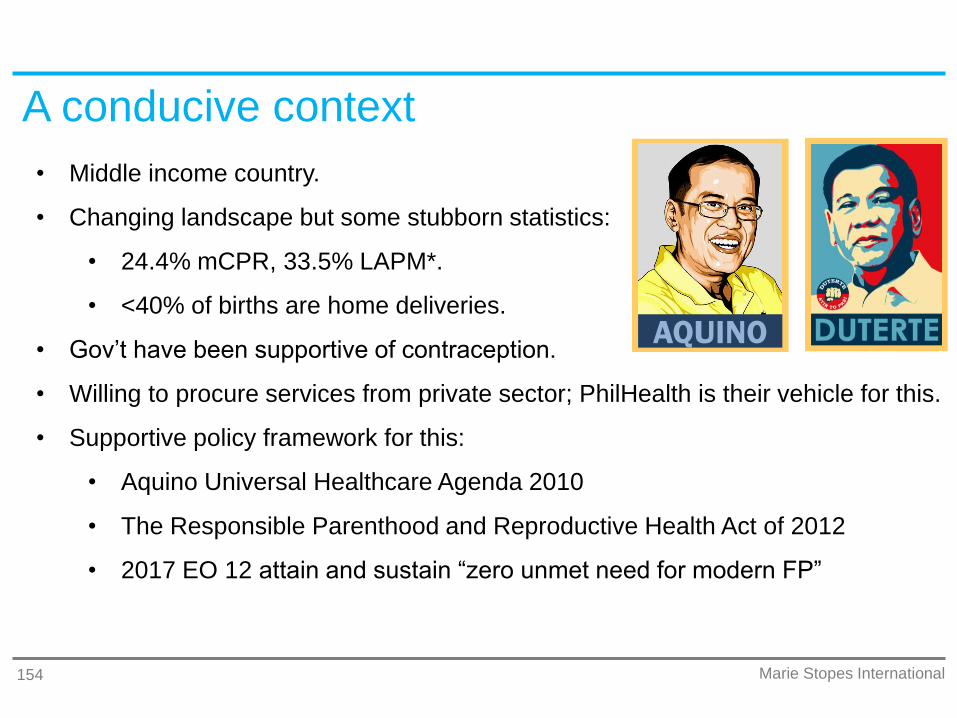

A conducive context

• Middle income country.

• Changing landscape but some stubborn statistics:

• 24.4% mCPR, 33.5% LAPM*.

• <40% of births are home deliveries.

• Gov’t have been supportive of contraception.

• Willing to procure services from private sector; PhilHealth is their vehicle for this.

• Supportive policy framework for this:

• Aquino Universal Healthcare Agenda 2010

• The Responsible Parenthood and Reproductive Health Act of 2012

• 2017 EO 12 attain and sustain “zero unmet need for modern FP”

AQUINO

Marie Stopes International155

The story so far• PSPI convinced gov’t to allow midwives to perform LARC in

maternity homes and pay for it:

• Gradual process, first PPIUD, then interval IUDs, then implants.

• Administrative Order licencing birthing homes to provide LARC.

• Circular accrediting midwives to receive LARC reimbursements.

• $ 40.00 for IUD, $ 60.00 for implants

• PSPI successfully franchised maternity homes, providing clinical

training, quality assurance, business training, etc.

• This expanded access and increased the franchisees’ sustainability.

Marie Stopes International156

It’s not all good news• Many challenges claiming reimbursements:

• National and regional government bureaucracy.

• Inconsistency in implementing the administrative orders.

• Low capacity to file reimbursement claims.

• ‘Buggy’ government IT and ERP Systems

• Increasingly competitive space

• Politics is still involved.

• This results in payment delays of <180 days.

• Creates cash flow problems.

• Impacts on midwives’ operations and personal lives.

• Midwives beginning to feel demoralised and exploring alternative careers.

Marie Stopes International157

The future - commercial franchise, social goals

1. Switching from franchisee fees to a commission based system

• Recently PSPI has started supporting midwives to set up maternity homes.

• Give: $25,000 no collateral loans, 5 years, 6% interest.

• Get: Higher franchise fees and 10% commission on LARC reimbursements.

2. Evolving our value proposition

• Mediation between PhilHealth and franchisees for claims management.

• Improved technical assistance to assure clinical and data compliance.

• Investment in brand visibility and marketing activities.

• A more robust entrepreneurial support and training program

3. Franchising standalone FP clinics

• Shape implementation guidelines; test in MSI centres; assess viability.

Marie Stopes International158

Further reflection and advocacy

Specialization vs Integration

Birthing + Family Planning Model

Polyclinic Model

Hospital Model

Expanding Services in

Lower Facilities

What other benefit packages can be performed in Birthing Homes, Stand Alone FP Clinics, Infirmaries

How can we expand government subsidies on Primary Care Benefit Packages

Influencing Government

on Family Planning

Where is FP in the Philippine Healthcare Agenda? Where is the FP Charter on the Philippine Health Insurance Corporation

What changes do we need to raise the value FP Services as a healthcare priority rather than a simple token or added service

How do we truly engage government

to pay for family planning?

Looking Towards the Future