presentation to the portfolio committee on trade and industry – the dti’s 2010/11 annual report,...

TRANSCRIPT

Presentation to the Portfolio Committee on Presentation to the Portfolio Committee on Trade and Industry – the dti’s 2010/11 Annual Trade and Industry – the dti’s 2010/11 Annual

Report, including IPAPReport, including IPAP

Date : 14 October 2011Date : 14 October 2011Director-GeneralDirector-General

Mr Lionel OctoberMr Lionel October

2

Presentation OutlinePresentation Outline

Economic Context Strategic Objectives Achievements against planned targets

Industrial Development Trade, Export & Investment Broadening Participation Regulation Administration & Co-ordination

Financial Management Challenges

2

3

Economic ContextEconomic Context The focus of the dti’s work was on the upscaled implementation

of IPAP2 to deal with factors affecting the economy's productive capacity and competitiveness

The South African economy came out of recession in the second half of 2009 and showed a modest growth of 2.8% in 2010. This recovery was broad-based, with all main sectors making positive contributions to overall gross domestic product (GDP) growth in 2010.

This growth was supported by particularly strong growth rates in the first and fourth quarters at 4.8% and 4.4% respectively, with the second quarter registering 2.8% and the third quarter 2.7%.

Despite this stable recovery trajectory, unemployment was still high at 24% in 2010, though it declined by 0.1% in the first quarter of 2011.

3

4

Economic ContextEconomic ContextManufacturing performance The manufacturing sector, after showing a steep decline of 10.4%

in 2009, performed well in 2010, growing by 5% for the year with its strongest quarterly growth rates achieved in the first, second and fourth quarters at 8%, 5% and 4% respectively.

Although this sector was one of the main drivers of the South African economic recovery in 2010, its strong rebound is still limited to a few sub-sectors such as the automotive; basic chemicals; iron and steel; and food and beverages industries. (Source: South African Reserve Bank)

International Trade performance Exports of manufactured goods remained under pressure due to

poor global demand, particularly from South Africa’s traditional trading partners from the developed world, and that continues to limit export performance.

4

Economic ContextEconomic ContextInvestment performance The total real gross fixed capital formation declined by 3.7% in 2010

deteriorating from a 2.2% decline experienced in 2009. This overall decline was despite a positive growth of 3.7% achieved by state corporations which in itself represented a significant decline from the 26.1% achieved in 2009.

The economic decline was mainly due to persistent contraction in investment by the government which showed an aggregate decline of 10.9% for the year after showing consecutive declines in all quarters in 2010.

Lack of investment by private business enterprises also contributed significantly to this decline showing a contraction of 4.4% in 2010. This decline in private investment was mainly driven by the construction industry.

5

6

Economic ContextEconomic ContextEmployment performance The number of employed people increased slightly to 13 132 million

in Q4 of 2010, but that marginal increase was short-lived. A further 14 000 people lost their jobs in the first quarter of 2011,

reducing the number of employed people to 13 118 million people, despite the manufacturing sector’s creation of about 20 000 more jobs.

This decline in employment was driven mainly by the transport, construction and agriculture sectors, which lost 34 000, 25 000 and 24 000 jobs respectively. On the other hand, finance and other business services; manufacturing; and mining did increase the numbers of people employed by 37 000, 20 000 and 15 000 respectively.

6

Strategic ObjectivesStrategic Objectives

7

Strategic ObjectivesStrategic Objectivesthe dti’s strategic objectives for the period under review were:Promoting the co-ordinated and accelerated implementation of the government’s economic vision and priorities;Promoting direct investment and growth in the industrial and services economy, with particular focus on employment creation;Raising the level of exports and promoting equitable global trade;Promoting broader participation, equity and redress in the economy; andContributing to Africa’s development and regional integration within the New Partnership for Africa’s Development (NEPAD).

8

99

The structure of the dti‘s The structure of the dti‘s work work

the dti’s work is organised in terms of the following clusters:

Industrial development; Trade, Investment and Exports; Broadening participation; Regulation, and Administration and co-ordination

1010

Achievements against Achievements against planned targetsplanned targets

11

• Public procurement and SOE supplier development

Preferential Procurement Policy Framework Act Regulations- The effective date for the amended regulations is 07 December 2011. - This will enable designation for local procurement and align the PPPFA

with B-BBEE objectives. - Enable pro-active promotion of local procurement in non-designated

sectors.

State Owned Enterprises- First phase of mobilisation within SOEs to introduce localisation and

supplier development into the procurement process. SOEs introducing new policies, processes, systems and capacity building to embed supplier procurement leverage more systematically

- Some success stories e.g. recent Transnet procurement of 100 locomotives: 90 to be assembled in SA

Industrial Development: IPAP key Industrial Development: IPAP key progress – cross-cutting highlightsprogress – cross-cutting highlights

• National Industrial Participation Programme

- Study into more strategic evolution of NIPP – including consolidation of CSDP and NIPP – completed in the period.

- New framework will introduce Fleet, Indirect and Direct procurement provisions.

- Obligations monitored in the region of +/- US$15.5bn- Of these, 80% arise out of the Strategic Defence packages - More than 220 projects have been implemented- Under the Strategic Defence Packages, 5 out of the ‘Big 6’

have completed their obligations in full

12

Industrial Development: IPAP key Industrial Development: IPAP key progress – cross-cutting highlightsprogress – cross-cutting highlights

13

• Industrial FinancingIndustrial Development Corporation- IDC has made available R102 bn mostly in loan finance for IPAP and NGP

sectors - R10bn Job Creation Fund at Prime less 3% over five years- R25bn earmarked towards Green Economy- R7.7 5bn agricultural value chain, including forestry - On budget incentives such as EIP and 12i tax allowance supported an

estimated commitment of 30 085 jobs- IDC funding to create approximately 17 760 direct and indirect jobs and 9

880 have been saved as a resultStudy on long term funding- The completion of Phase 1 of a study into concessional industrial financing

lays the foundation for a framework for securing long-term sources and provision of concessional industrial financing and the requisite financial products for key sectors

- Phase 2 of the work set for completion will feed into appropriate processes

Industrial Development: IPAP key Industrial Development: IPAP key progress – cross-cutting highlightsprogress – cross-cutting highlights

14

• Trade and technical infrastructure- Exporters Early Warning System on Technical Barriers to Trade

developed by SABS launched Identified technical barriers to trade for exporters notified to WTO Distributed via free weekly email to exporters

- ITAC processed numerous applications for increases, rebates and reductions of duties in line with IPAP priorities

- SABS developed a range of enabling standards for various industries / products including solar water heaters; water efficient buildings; wind energy turbines; energy efficient appliances; electrical components; water efficient components; electric vehicle batteries; automotive fuels; energy/electricity co-generation and transport of dangerous goods.

- New accreditation program for energy efficient measurement and verification finalised

- Draft Legal Metrology policy proposal subject of stakeholder consultation

Industrial Development: IPAP key Industrial Development: IPAP key progress – cross-cutting highlightsprogress – cross-cutting highlights

• Automotives– Automotive Investment Incentive with a budget of R2, 69bn over the MTEF

period has been instrumental in securing R14 billion investment commitments, including R9 billion investment from assemblers• Volkswagen: to produce 136,000 new Polo and Vivo cars per annum (pa)• Toyota: production expansion to reach 130,000 vehicles pa• Ford's launched Ranger pickup and associated engine plant for export to 148

countries producing 85,000 pickups and 145,000 engines pa• BMWSA to increase production of fourth generation 3-Series to 80,000 units pa

from the current 50,000 with more than 80% for export• Nissan: production to rise to 76,000 vehicles pa• Daimler Chrysler's to produce 70,000 new C-Class Mercedes pa• General Motors brought production of Chevy Spark to South Africa

– APDP regulatory amendments with ITAC and SARS for finalisation

– 15 component manufacturers benchmarked

– MHCV value chain report and draft action plan completed

15

Industrial Development: IPAP key Industrial Development: IPAP key progress – sectoral highlightsprogress – sectoral highlights

• Clothing & Textiles

– R112m was approved under the Clothing and Textiles

Competitiveness Programme (CTCP) in 22 applications for 106

companies .

– Production Incentive (PI) 189 applications totalling R 619 million

approved. A total of R71m has been disbursed in the period.

– This is in support of at least 40 591 jobs

– SA handmade leather brand ‘Tsonga’ export contracts to Australia

and France.

16

Industrial Development: IPAP key Industrial Development: IPAP key progress – sectoral highlightsprogress – sectoral highlights

• Business Process Services– R42 million new investment commitments approved linked to 806 jobs

– 3,400 young trainees being trained under the Monyetla II Programme – +70% employed in period

• Green Industries– New building standards require mandatory installation of solar water

heaters or similar technologies in new buildings

– IDC allocated R25bn with 54 projects in pipeline

– Draft Green Industries customised sector programme (CSP) developed for finalisation and draft action plans for solar and wind completed

– Intra-departmental South African Renewables Initiative (SARI) initiative to leverage international climate finance to supplement domestic funding sources for renewable energy production linked to domestic manufacturing

17

Industrial Development: IPAP key Industrial Development: IPAP key progress – sectoral highlightsprogress – sectoral highlights

• Forestry- 1, 186 water licences for 14,960 hectares of land granted by DWEA

- Establishment of Panel for Environmental Impact Assessment Practitioners to assist with EIA’s

- Skills programme for new growers and land reform beneficiaries• Biofuels

- Petroleum Products Act Regulations amended to allow ethanol blending

- Standard published for fuel grade ethanol

- Mandatory upliftment and pricing formula for biofuels and support mechanism agreed to by Task Team and is being processed

• Agro- processing- Detailed action plan for organic food sector completed

- Aquaculture strategy completed and implementation plan being finalised

18

Industrial Development: IPAP key Industrial Development: IPAP key progress – sectoral highlightsprogress – sectoral highlights

• Significant progress over period with 51 KAP’s achieved• 21 KAP’s close to achievement and carried over for final sign off

• 13 KAP’s for the period affected by intra-governmental and

regulatory hurdles;– Mineral beneficiation

– Domestic production of ARV’s

– Biofuels regulation,

– Water licences, afforestation, saw mill development and charcoal production

– REFiT

– SWH’s

– STB’s and Digital TV’s

– Fluospar beneficiation

19

Industrial Development: IPAP Industrial Development: IPAP Progress overviewProgress overview

• Some KAP’s transferred to other departments in terms of refinement of roles – tourism (DOT), National Food Control Agency (DAFF) and water licences (DWEA)

• Some KAP’s deleted from future IPAP iteration because progress reliant on long term strategic decisions of government and/or business. (Projects Mthombo and Mafutha)

• Funding constraints negatively impacted some programmes:– Competitive financing for Capex suppliers

– National Tooling Initiative

– Gold Loan Scheme

– Sector Specific Centres of Excellence

– Mentoring of SME manufacturers and ERA programme in Auto Sector

20

Industrial Development: IPAP Industrial Development: IPAP Progress overviewProgress overview

Industrial Development: IPAP Industrial Development: IPAP key challengeskey challenges

• Slow recovery of global economy and key traditional export markets, in particular the US and EU with threat of prolonged recession

• Sustained rapid growth of large developing economies / regions such as China, India, Brazil and Africa

• This implies a challenging process of trade adjustment in a context where value-added exports have gone to advanced trading partners and Africa and commodity exports to other developing trading partners

• Continuous appreciation of real effective exchange rate (REER) to highest levels on record in Q3 2010 in the context of massive capital inflows and a large current account deficit

• Real interest rates significantly above major developing and developed economies

21

Industrial Development: IPAP Industrial Development: IPAP key challengeskey challenges

• South African economy still recovering domestically from the global economic crisis

• Slowdown in public and private fixed investment expenditure

• Large increases in electricity prices increasingly difficult for manufacturing sector to absorb

• Rail and port inefficiencies coupled with very high port charges

• Large drop in manufacturing employment between Q1 2008 and Q3 2010 of 153 000 with slight improvement in Q4 2010 before declining again during the first two quarters of 2011

22

Industrial Development: IPAP key Industrial Development: IPAP key challenges - currencychallenges - currency

Source: SARB

23

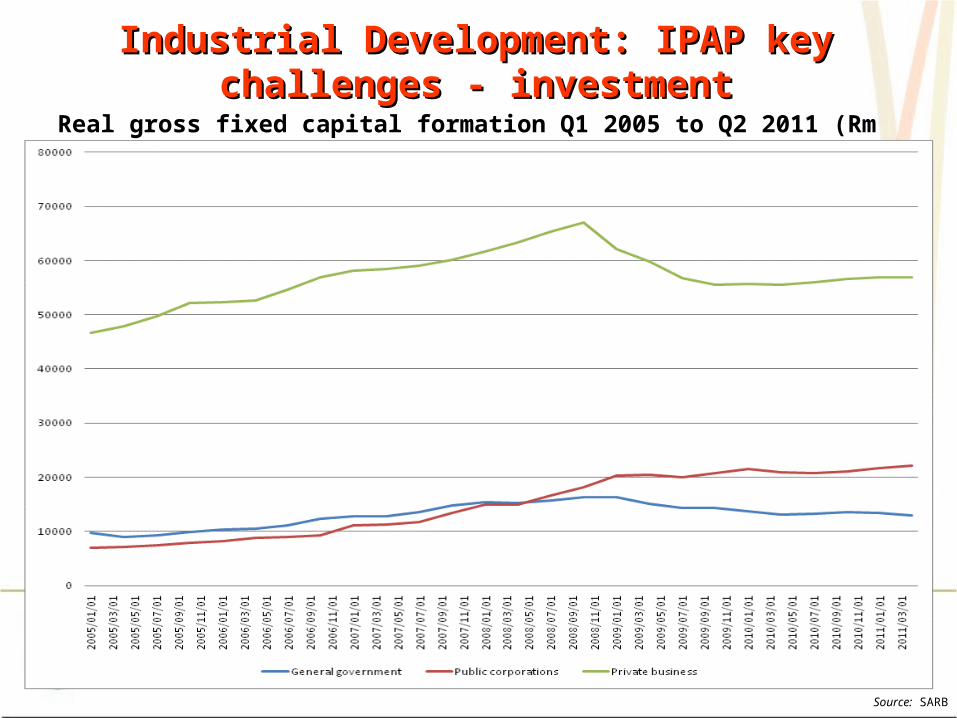

Industrial Development: IPAP key Industrial Development: IPAP key challenges - investmentchallenges - investment

Real gross fixed capital formation Q1 2005 to Q2 2011 (Rm 2005 prices)

Source: SARB

24

25

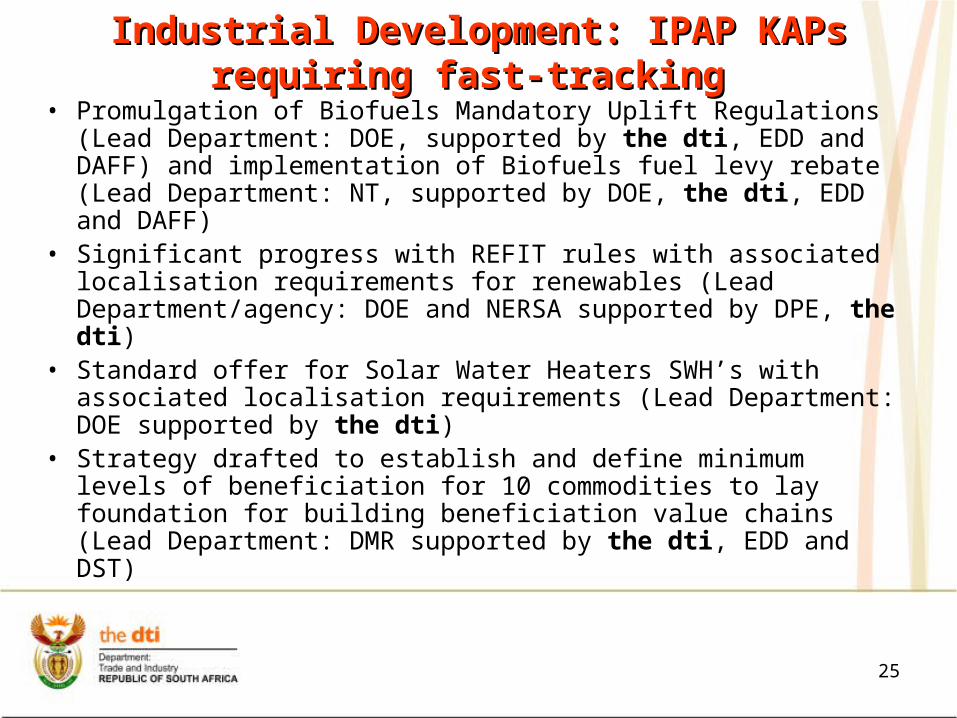

Industrial Development: IPAP Industrial Development: IPAP KAPs KAPs requiring fast-tracking requiring fast-tracking

• Promulgation of Biofuels Mandatory Uplift Regulations (Lead Department: DOE, supported by the dti, EDD and DAFF) and implementation of Biofuels fuel levy rebate (Lead Department: NT, supported by DOE, the dti, EDD and DAFF)

• Significant progress with REFIT rules with associated localisation requirements for renewables (Lead Department/agency: DOE and NERSA supported by DPE, the dti)

• Standard offer for Solar Water Heaters SWH’s with associated localisation requirements (Lead Department: DOE supported by the dti)

• Strategy drafted to establish and define minimum levels of beneficiation for 10 commodities to lay foundation for building beneficiation value chains (Lead Department: DMR supported by the dti, EDD and DST)

26

Industrial Development: IPAP Industrial Development: IPAP KAPs KAPs requiring fast-tracking requiring fast-tracking

• Set Top Boxes (STB’s) roll-out and associated localisation (Lead Department: DOC, supported by the dti)

• Process to amend SOE shareholder compacts to secure fleet identification and localisation underway and to be completed (Lead Department: DPE supported by the dti, DST and EDD)

• Customs Fraud Campaign underway but requires scaling up (Lead Agency: SARS supported by the dti, EDD and DOJ)

27

Overview of Incentive SchemesOverview of Incentive SchemesDescription

Actual

Number of firms supported Jobs supported

Investment leveraged

R'000

Export sales valueR'000

EIP 759 15,018 11,300,000 AIS 36 - 7,300,000 BPO&O 3 806 -

Film & Television 49 - 991,000

12i Allowance Programme 3 - 4,100,000

Co-operatives (CIS) 232 3,084 - BBSDP 1,104 1,067 - EMIA 1,753 - - 2,856,000COEGA 6 193 406,000 ELIDZ 7 521 342,000 RBIDZ 0 0 0 CIP 12 9,271 34,600,000 SPII 20 - 21,700 TOTALS 3,984 29,960 59,060,700 2,856,000

The incentive schemes and IDZ funding cumulatively supported 3,984 firms, 29,960 jobs and leveraged R59b in investments. The EMIA scheme supported R2,9b in export sales.

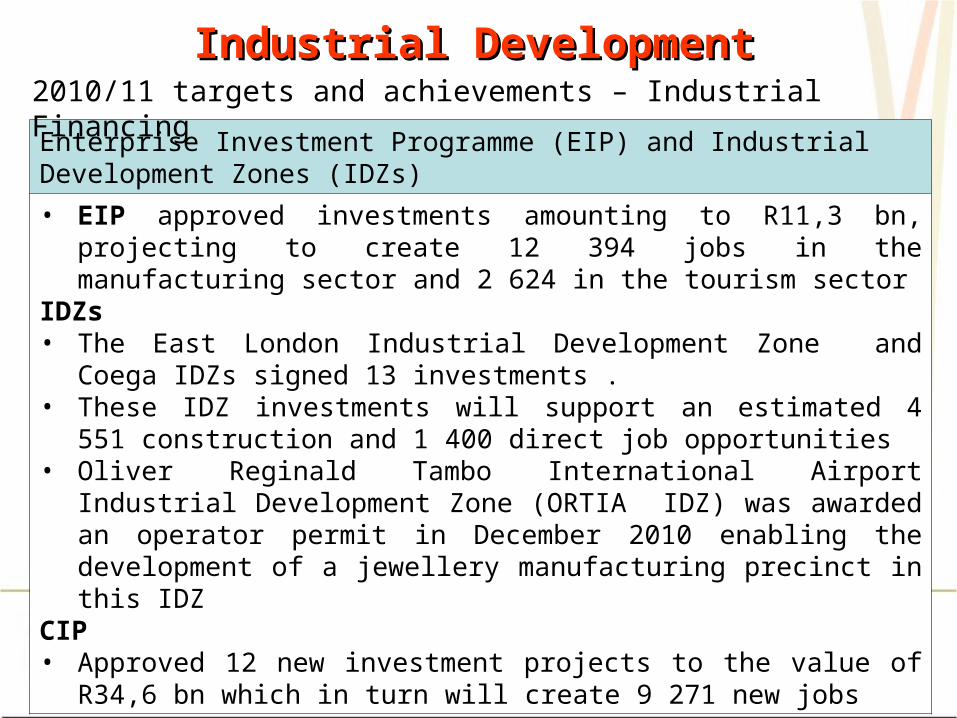

Industrial DevelopmentIndustrial Development

Enterprise Investment Programme (EIP) and Industrial Development Zones (IDZs)

• EIP approved investments amounting to R11,3 bn, projecting to create 12 394 jobs in the manufacturing sector and 2 624 in the tourism sector

IDZs• The East London Industrial Development Zone and Coega IDZs

signed 13 investments .• These IDZ investments will support an estimated 4 551 construction

and 1 400 direct job opportunities• Oliver Reginald Tambo International Airport Industrial Development

Zone (ORTIA IDZ) was awarded an operator permit in December 2010 enabling the development of a jewellery manufacturing precinct in this IDZ

CIP• Approved 12 new investment projects to the value of R34,6 bn which in

turn will create 9 271 new jobs

2010/11 targets and achievements – Industrial Financing

Trade, Investment & ExportsTrade, Investment & Exports

Africa

SACU A new Vision and Mission for the Southern African Customs Union

(SACU) was approved by the SACU Heads of State in April 2010 and South Africa hosted a SACU Summit in July 2010.

As Chair of SACU since July 2010, South Africa, through the dti has assisted in forging consensus on a work programme in SACU focused on industrialisation, infrastructure development, trade facilitation, revenue sharing and unified engagement in trade negotiations.

Work initiated in SACU to develop common competition and industrial policies.

Concept document prepared on possible industrial projects that could be the basis for the industrial work programme for SACU.

Work on amending the SACU agreement to institutionalise the SACU Summit has been undertaken

2010/11 targets and achievements

29

Trade, Investment & ExportsTrade, Investment & Exports

Africa

SADC The Southern African Development Community (SADC) Ministerial

Task Force approved an action plan with nine (9) priority focus areas that will help to consolidate the SADC Free Trade Area and provide greater impetus to regional industrialisation

SA Government Position on future of SADC agreed SADC has begun to forge a common position on the SADC- East

African Community (EAC) – Common Market for Eastern and Southern Africa (COMESA) Tripartite Free Trade Area (TFTA)

Work initiated on SDIs in Zimbabwe, Mozambique, Tanzania, DRC and Angola

2010/11 targets and achievements

30

Trade, Investment & ExportsTrade, Investment & Exports

South-South:

South Africa and China signed a Comprehensive Strategic Partnership Agreement (CSPA) that included an undertaking to increase South Africa’s value added exports to China and to encourage Chinese investment in South Africa

Agreements were reached with India and Brazil to address non-tariff barriers that impede our bilateral trade

2010/11 targets and achievements

31

Trade, Investment & ExportsTrade, Investment & Exports

Multilateral

Participated in World Trade Organisation (WTO) Doha Development Round negotiations with a view to ensuring a developmental outcome. Negotiating positions on all key issues have been strengthened and updated as the negotiations have unfolded

2010/11 targets and achievements

32

Trade, Investment & ExportsTrade, Investment & Exports

Policy

Finalised the Trade Policy Strategic Framework which sets out Government's approach to trade policy and strategy

Cabinet also approved the dti's Policy Framework on

Bilateral Investment Treaties (BITs), which will guide South Africa's approach to future international investment treaties

2010/11 targets and achievements

33

Trade, Investment & ExportsTrade, Investment & Exports

Investment and Export Promotion

Outgoing State visits: facilitated business delegations to the following countries i.e. Algeria (27), India (226), Russia (112), China (380), Lesotho (20), Egypt (150), Cuba (17), France (144), for Presidential visit by the Deputy President, facilitated business delegations to the following countries; Turkey (49), Syria (8), Kenya (19) and United Kingdom

Support for the business forum programme during State visits was also facilitated in Zambia, Angola, Botswana, Uganda and Brazil

Five (5) Investment and Trade Initiatives (ITIs) were facilitated to Zimbabwe, Brazil, Russia, the Democratic Republic of the Congo (DRC) and India and sixteen (16) National and one (1) Local Pavilion as well as twenty (20) Group Trade Missions took place

2010/11 targets and achievements

34

Trade, Investment & ExportsTrade, Investment & Exports

Investment and Export Promotion

Substantive progress has been made in recruiting foreign direct investment in a targeted manner. Targeted countries included: China, India, Russia, Brazil, Japan, Spain, Germany, France, the UK, the United States of America (USA) and the Middle East

The work programme will translate over the next three years into an investment pipeline of R115 billion in projects. The results of the year are R 31,228,820,000 in potential investment and 14 055 jobs. The pipeline reflects R 15,546,320,000 in domestic investment and R 15,682,500,000 in foreign investment

The EMIA scheme supported R2,9b in export sales

2010/11 targets and achievements

35

Broadening ParticipationBroadening Participation

Enterprise development Developed 100 new small scale co-operatives creating a

minimum of 500 self-generated income and employment opportunities

Legislative amendment of 2005 Cooperatives Act formulated and gazetted for public comment

The Technology Incubation Programme of the Department, which is managed by seda created 202 new Small Medium and Micro Enterprises (SMMEs)

2010/11 targets and achievements

36

Broadening ParticipationBroadening Participation

Enterprise development The Department through the Small Enterprise Development

Agency (seda) has to date established a network of forty two (42) branches, seventeen (17) mobile units and fifty eight (58) Enterprise Information Centres (EICs) countrywide

Close to 63 916 new clients accessed the seda branch network. Black Business Supplier Development Programme (BBSDP)

– 1 104 enterprises supported under the incentive Co-operatives Incentive Scheme (CIS) – 232 cooperatives

have been supported under the CIS incentive

2010/11 targets and achievements

37

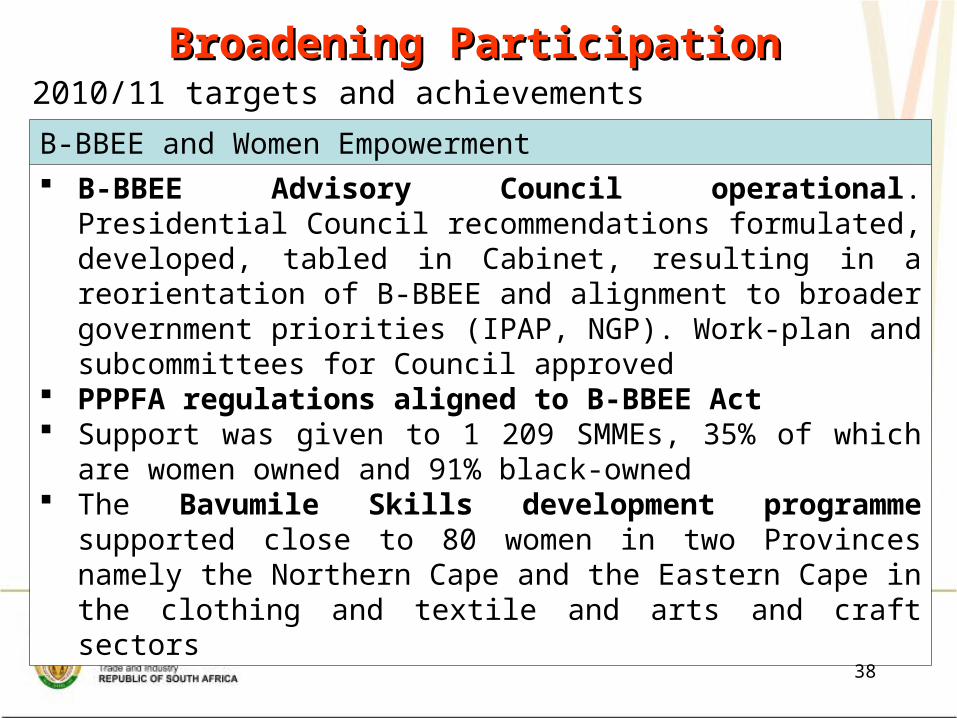

Broadening ParticipationBroadening Participation

B-BBEE and Women Empowerment B-BBEE Advisory Council operational. Presidential Council

recommendations formulated, developed, tabled in Cabinet, resulting in a reorientation of B-BBEE and alignment to broader government priorities (IPAP, NGP). Work-plan and subcommittees for Council approved

PPPFA regulations aligned to B-BBEE Act Support was given to 1 209 SMMEs, 35% of which are women

owned and 91% black-owned The Bavumile Skills development programme supported

close to 80 women in two Provinces namely the Northern Cape and the Eastern Cape in the clothing and textile and arts and craft sectors

2010/11 targets and achievements

38

Broadening ParticipationBroadening Participation

Enterprise Finance and Technology Support A Techno-girl workshop was held in Limpopo Province where 100

girl learners, from 10 schools in the five districts benefited through skills development

The Technology for Women in Business (TWIB) awards ceremony 2010/2011 was held in Gauteng and seven finalists competed for the awards, which comprised two Categories namely micro and small-sized businesses in sectors such as engineering and wood and furniture

6 Women owned enterprises have been assisted to the value of R5m through the Isivande Women’s Fund (IWF)

2010/11 targets and achievements

39

Broadening ParticipationBroadening Participation

Enterprise Finance and Technology Support

Through the Support Programme for Industrial Innovation (SPII) supported 20 projects with total SPII contribution of R22,7m and industry contribution of R21,7m.

Total value of projects assisted was R44,3m Through the Technology and Human Resources for

Industry Programme (THRIP) supported 235 projects and 1664 students

2010/11 targets and achievements

40

RegulationRegulation

Policy and legislative development Finalised the Companies Amendment Bill and

Regulations which introduces simplification of business registration processes, reduces red tape and enhances the transparency of companies

Finalised the Consumer Protection Act Regulations which give effect to the Consumer Protection Act

Finalised the Estate Agency Policy Framework and the draft Bill was produced for tabling to Cabinet which provides a framework for drafting of the new Estate Agents Act to sufficiently protect consumers

2010/11 targets and achievements

41

RegulationRegulation

Policy and legislative development Finalised the Intellectual Property Laws Amendment Bill

for the Protection of Indigenous Knowledge Developed National Liquor Licensing Guidelines and

Liquor Regulations for the 2010 FIFA World Cup to streamline application procedures and align trading terms across the country

Minister introduced Regulations and a Directive to improve accessibility of funds to needy communities and causes, improve governance structures on lottery matters and ensure optimal distribution of lottery fund for developmental purposes

2010/11 targets and achievements

42

RegulationRegulation

Policy and legislative development Interactive Gambling Regulations has been completed Gambling Review Commission assessed and produced a

report on, inter alia, the socio-economic impact of gambling particularly on the poor, proliferation of gambling which might result from legislative or implementation gaps and the impact of technological development in this industry

Draft research report produced on the review of the Alienation of Land Act aimed to align it with the Estate Agency Affairs Act and draft RIA report on the Estate Agency Policy and Law reform were finalised

2010/11 targets and achievements

43

Administration & Co-ordinationAdministration & Co-ordination

Continuous improvement

Facilitated the implementation of key projects within the IPAP2 through its participation in the Economic Sectors and Employment Cluster (ESEC) of Cabinet

Concluded a major upgrade of the ICT infrastructure which resulted in a reliable and faster ICT network

Vacancy rate reduced to 16,9% as at 31 March 2011. Vacancy rate reduced despite an increase in newly created posts and normal attrition

42.56% of women are employed at SMS level as at 31 March 2011 41% of total procurement spent on HDI and 64% of total

procurement spent on SMMEs Revised and implemented Fraud Prevention Plan based on new

risks

2010/11 targets and achievements

44

Governance (Entity Oversight)Governance (Entity Oversight)

Out of 15 agencies, 14 had unqualified audit reports with one, namely CIPC (formerly CIPRO) , being qualified

CIPC received a qualified audit due to lack of a management system to accurately account for revenue and debtors from annual returns. The new Companies and Intellectual Property Commission (CIPC) is addressing this issue

Increased capacity and strengthened processes to assist with entity oversight

45

46

Financial Financial managementmanagement

AG’s ReportAG’s Report

47

Audit Opinion• The Auditor General SA expressed an unqualified audit opinion on the 2010/11 Annual

Financial Statements

Emphasis of matters• Irregular Expenditure

This relates to single source procurement where in most instances the service provider was a sole supplier of such service (e.g. SABC Radio, training, etc.).

Additional controls introduced – new internal control unit being established and additional capacity approved: Group CFO & deputy CFO posts created.

• Material Impairments

This impairments largely relate to the General Export Incentive Scheme, which was in existence pre 1994. These debts are in a litigation process and in terms of prudent accounting provision has been made for impairment. Full report on this matter was presented to SCOPA.

AG’s Report - continuedAG’s Report - continued

48

Emphasis of matters• Asset Management

Asset verifications to be continued on a bi-annual basis. This will include reconciliation between the fixed asset register on LOGIS and count sheets. An analysis will be performed at a more senior level to ensure accuracy of the asset register.

The department is considering procuring an asset management system to address the LOGIS limitations, which include fields not being able to capture the full serial number and specific location of an asset

• Financial Statements

Additional quality checks will be implemented including a review by Internal Audit section

AG’s Report - continuedAG’s Report - continued

49

Emphasis of matters• Management of Performance Information

Engagement with NT and AG to agree on methodology for SMART criteria. Additional capacity created – Chief Risk & Compliance Officer created at CD level.

Policy developed to manage performance information.

Strategic planning session convened led by Minister Davies – key priorities set for each area.

Planning cascaded to various fora in the dti to discuss operational and divisional plans and progress is reported and assessed quarterly.

Annual departmental plan introduced.

Minister approves departmental performance information.

Formalised quarterly performance reviews to monitor and manage progress

Notes to the AFSNotes to the AFS

50

Unauthorised expenditure (Note 12.1 of the AFS)Unauthorised expenditure (Note 12.1 of the AFS)• Unauthorised expenditure to the amount of R37 380 million was incurred in the

2004/05 financial year.• R31 075 million relates to the General Export Incentive Scheme (GEIS) debts

(pre 1994), which were written off.• R6,1 million relates to claim from an investor for loss of investment.• Full report on this matter was presented to SCOPA.

World Cup Tickets (Note 39 of the AFS)World Cup Tickets (Note 39 of the AFS)• the dti took a collective decision to purchase 200 tickets for the World Cup as

part of its investment promotion drive to showcase SA as an investment destination.

• International investors were invited and officials from the department had to interact with these investors.

• Erratum to be issued regarding ticket allocation to Minister to reflect 2 instead of 5 tickets. 173/200 tickets issued to local and foreign investors.

Five Year Comparison of budget Five Year Comparison of budget vs Expenditure – R’000vs Expenditure – R’000

5151

Overview of expenditureOverview of expenditure The budget allocation for the 2010/11 financial year was

R6,194,208 million as compared to R 6,402,076 million in 2009/10. The expenditure for 2010/11 was R5,796,741 million, i.e. 93,6% of the budget.

This spending pattern should be considered in the context of the departmental cost drivers, comprising mainly incentive schemes and transfer payments. Approximately 58% of the expenditure consisted of incentives and 22% of transfers to the departmental agencies. The remaining funds were utilised for operational expenses.

The under spending was mainly in the division responsible for Incentive Administration, viz, The Enterprise Organisation division, by 4.09%, which is mainly attributable to the Automotive Investment Scheme (AIS).

52

Budget vs. expenditure for the 2010/11 financial year Budget vs. expenditure for the 2010/11 financial year – per programme– per programme

Programme 2010/11 Unspent as % of final

appropriationFinal

AppropriationActual

Expenditure Variance Expenditure as

% of final appropriationR’000 R’000 R’000

Administration 443,251 435,815 7,436 98.32% 1.68%

International Trade and Economic Development 125,088 106,949 18,139 85.50% 14.50%

Empowerment & Enterprise Development 814,034 801,173 12,861 98.42% 1.58%

Industrial Development 1,156,961 1,142,033 14,928 98.71% 1.29%

Consumer and Corporate Regulation 195,531 145,021 50,510 74.17% 25.83%

The Enterprise Organisation 3,046,652 2,792,994 253,658 91.67% 8.33%

Trade and Investment South Africa 353,476 328,582 24,894 92.96% 7.04%

Communication & Marketing 59,215 44,174 15,041 75% 25.40%

Total 6,194,208 5,796,741 397,467 93.58% 6.42%

53

Economic classification 2010/11 Unspent as % of final

appropriationFinal

AppropriationActual

Expenditure Variance Expenditure as %

of final appropriation

R’000 R’000 R’000

Compensation of Employees 551,748 514,935 36,813 93.33% 6.67%

Goods & Services 545,826 474,830 70,996 86.99% 13.01%

Interest and rent on land 276 275 1 99.64% 0%

Transfers to: 5,073,868 4,789,206 284,662 94.39% 5.61%

Departmental agencies 872,762 838,980 33,782 96.13% 3.87%

Manufacturing incentives, including:

1,389,176 1,144,261 244,915 82.37% 17.63%

**Automotive Production & Development Programme

538,000 294,252 243,748 54.69% 45.31%

Programme payments 1,216,984 1,216,225 759 99.94% 0.06%

Infrastructure incentives 1,224,374 1,224,337 37 100% 0%

Export Incentives 274,636 274,511 125 99.95% 0%

Other 95,936 90,892 5,044 94.74% 5.26%

Payments for capital assets 20,183 15,189 4,994 75.26% 24.74%

Payment for financial assets 2,307 2,306 1 100% 0%

Total 6,194,208 5,796,741 397,467 93.58% 6.42

Budget vs. expenditure for the 2010/11 financial year – Budget vs. expenditure for the 2010/11 financial year – economic classification economic classification

54** Amounts in respect of AIS are already included under the manufacturing incentives

Reasons for under spending

Item Amount unspent

Reasons

R’000

Automotive Production & Development Programme (AIS)

243,748 The Automotive Investment Scheme (AIS) only became operational in December 2010. 53 projects have been approved by the Adjudication Committee with the total concession amount of R1,861 billion as at 31 March 2011. R293,918 million was paid during the first quarter of the new financial year.

Goods & Services

70,996 • Outstanding foreign mission accounts from DIRCO. The account for March 2011 was only received on 19 May 2011 and charged against the budget for 2011/12• Postponement of the SACU Tripartite Summit from February to June 2011• Payments for funds earmarked for variation orders for a building currently occupied by CIPC could not materialise pending their move to new premises • Cost savings initiatives on venues and facilities as well as on travel contributed to the under expenditure

Compensation of Employees

36,813 Vacancies

Departmental agencies

33,782 Delays in the establishment of the National Consumer Commission and the Companies and Intellectual Property Commission.

55

If the AIS under spending excluded, the percentage underspent would be 2%

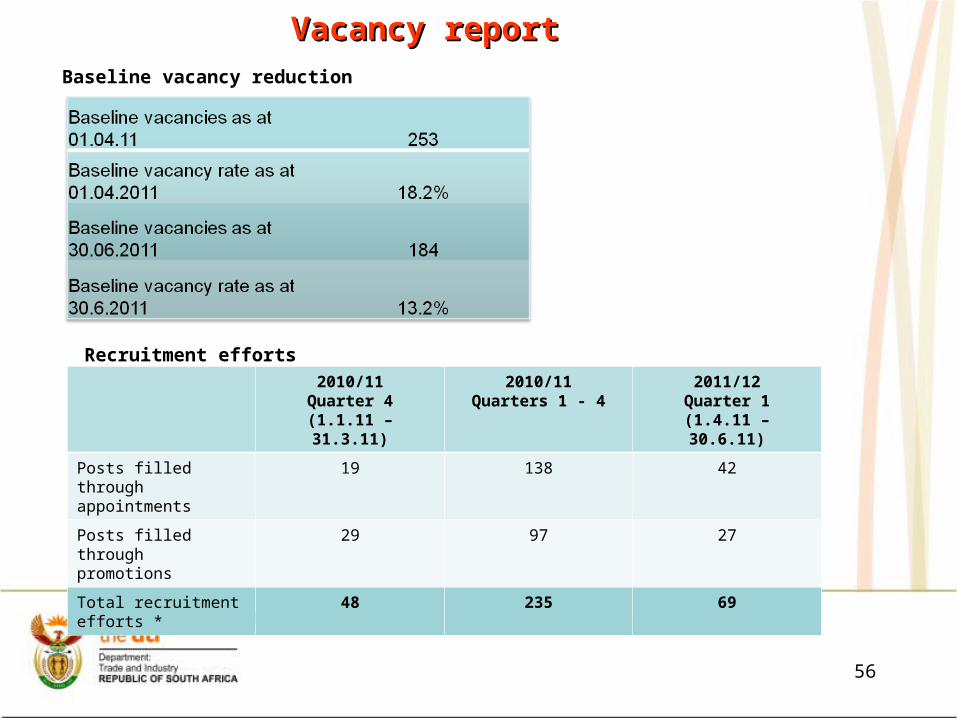

Vacancy report Vacancy report

56

Baseline vacancy reduction

Recruitment efforts

* Excludes posts additional to the establishment

2010/11Quarter 4

(1.1.11 – 31.3.11)

2010/11Quarters 1 - 4

2011/12Quarter 1

(1.4.11 – 30.6.11)

Posts filled through appointments

19 138 42

Posts filled through promotions

29 97 27

Total recruitment efforts *

48 235 69

Key ChallengesKey ChallengesGlobal economic climateChallenges to job creation and skills for economyGrowing the manufacturing sectorFunding and business support for informal sector and establishing new innovation incubatorsStrengthening corporate governance of some agenciesSubstantive application within BBEEE Framework , characterised by opportunistic fronting and lack of punitive measures

57

5858

Thank you

59

AppendicesAppendices

Appendix - Real interest rates

Short term interest rates as at August 2011

Source: The Economist

60

Appendix - Real interest rates

Long term interest rates as at August 2011

Source: The Economist

61

6262

Appendix - Currency

Source: SARB

62

Real Effective Exchange Rate (2000 = 100) and Rand / US Dollar, Jan 2009 – Jul 2011

6363

Appendix - Manufacturing

Manufacturing monthly production indexed (2005 = 100) and Y-O-Y growth, January 2005 to July 2011

Source: StatsSA

63

64

Source: Quantec

Appendix - Trade Balance

Trade balance by sector Q1 1990 – Q2 2011 (Rm)

6565

Appendix - Manufacturing employment

Source: StatsSA

65

Employment in the manufacturing sector ‘000, Q1 2008 – Q2 2011