presentation to retail investors - kingfisher plc

TRANSCRIPT

Kingfisher plcJanuary 2014

Agenda

2

Kingfisher at a Glance

Strategic History

Our Markets and Brands

‘Creating the Leader’ Strategy

2013/14 YTD(1) Summary and Outlook

Questions

Up to 2013/14 Q3 ended 2 November 2013

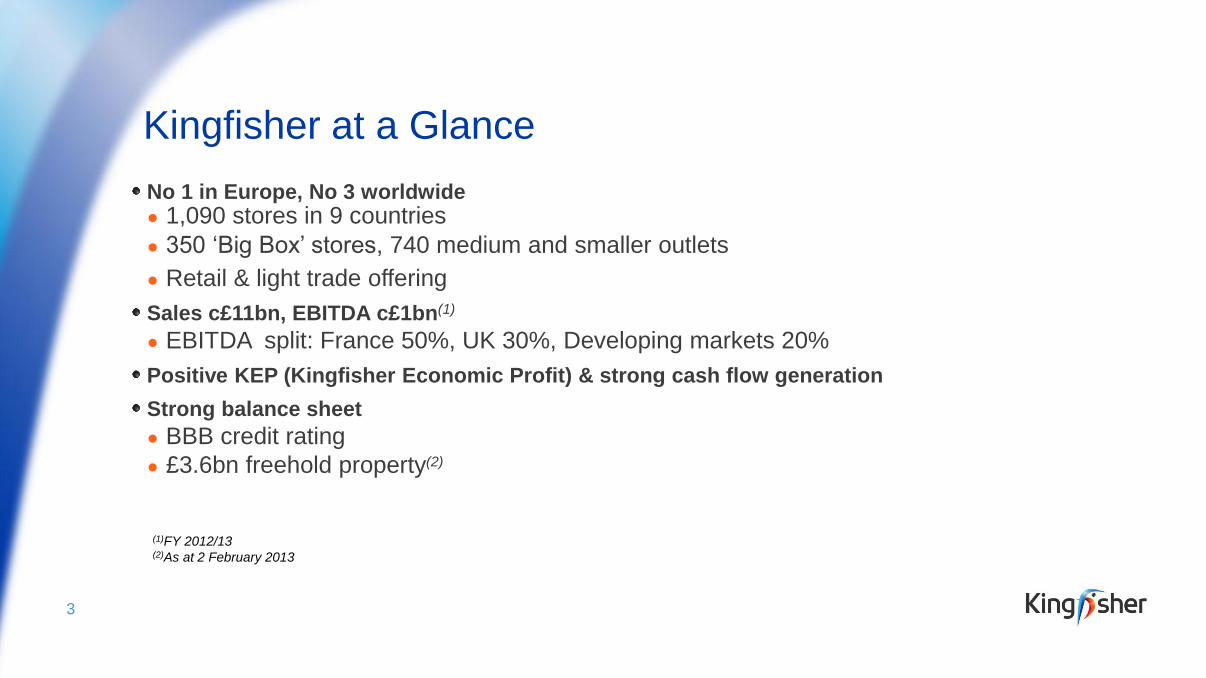

Kingfisher at a Glance

3

No 1 in Europe, No 3 worldwide● 1,090 stores in 9 countries

● 350 ‘Big Box’ stores, 740 medium and smaller outlets

● Retail & light trade offering

Sales c£11bn, EBITDA c£1bn(1)

● EBITDA split: France 50%, UK 30%, Developing markets 20%

Positive KEP (Kingfisher Economic Profit) & strong cash flow generation

Strong balance sheet

● BBB credit rating

● £3.6bn freehold property(2)

(1)FY 2012/13(2)As at 2 February 2013

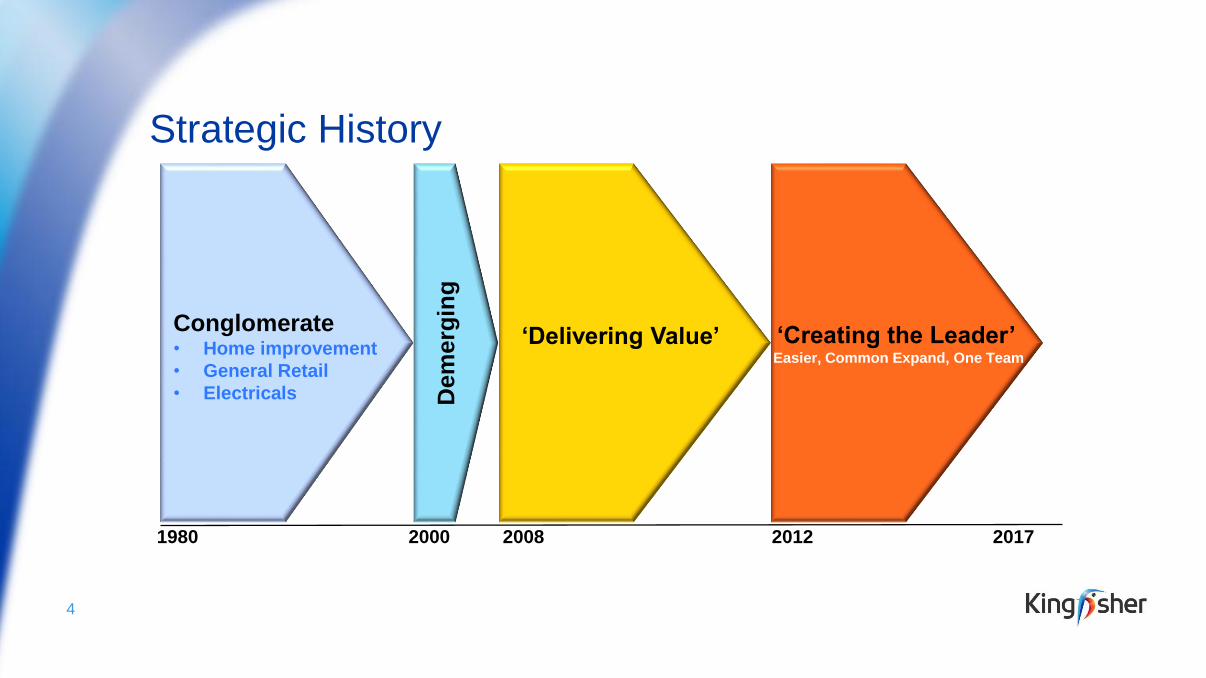

Strategic History

4

Dem

erg

ing

‘Delivering Value’ ‘Creating the Leader’Easier, Common Expand, One Team

Conglomerate • Home improvement

• General Retail

• Electricals

1980 2000 20122008 2017

Home Improvement is an attractive sector of Retail

Scale advantage

● Customer tastes converging across markets

● Few known manufacturer brands

Defensible ● Huge range breadth, need for interaction, difficult home delivery economics means

– Difficult category for grocers

– Low online sales penetration

Positive retail space/consumer demand balance

● Many of our markets still developing (space immature)

● UK competitor space is reducing

5

Strategic History

6

Dem

erg

ing

‘Delivering Value’ ‘Creating the Leader’Easier, Common Expand, One Team

Conglomerate • Home improvement

• General Retail

• Electricals

1980 2000 20122008 2017

2008 – Ian Cheshire becomes

Kingfisher CEO

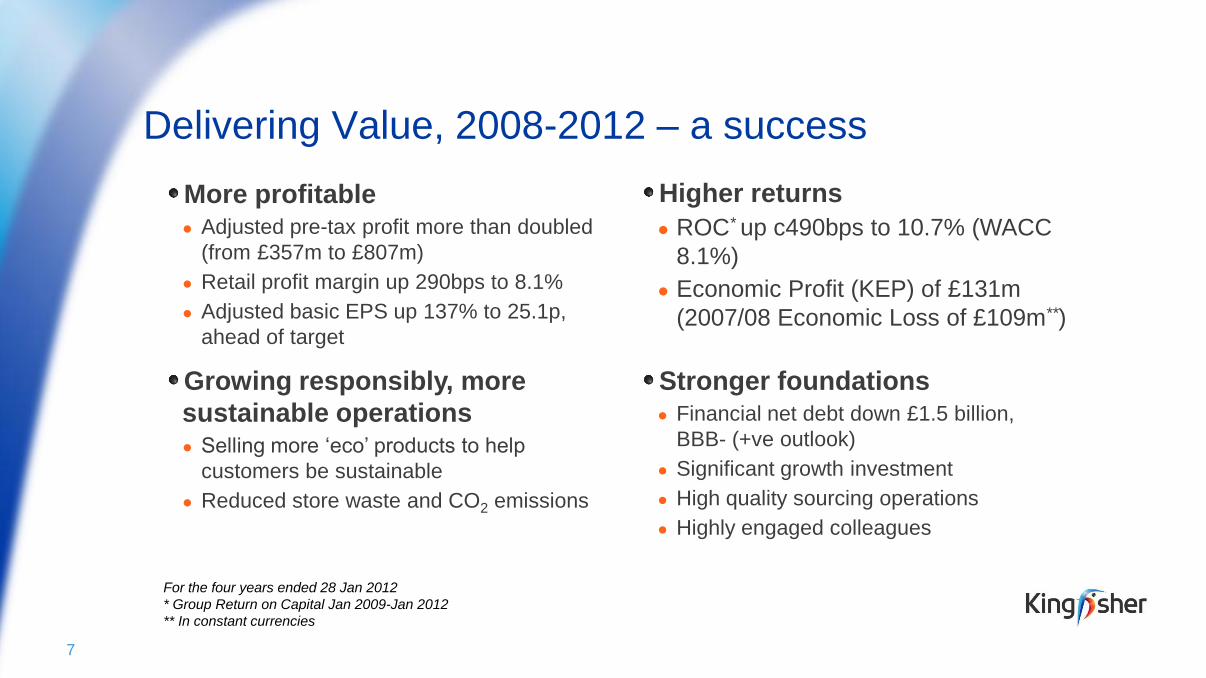

Delivering Value, 2008-2012 – a success

More profitable● Adjusted pre-tax profit more than doubled

(from £357m to £807m)

● Retail profit margin up 290bps to 8.1%

● Adjusted basic EPS up 137% to 25.1p,

ahead of target

Higher returns

● ROC* up c490bps to 10.7% (WACC

8.1%)

● Economic Profit (KEP) of £131m

(2007/08 Economic Loss of £109m**)

For the four years ended 28 Jan 2012

* Group Return on Capital Jan 2009-Jan 2012

** In constant currencies

7

Growing responsibly, more

sustainable operations● Selling more ‘eco’ products to help

customers be sustainable

● Reduced store waste and CO2 emissions

Stronger foundations● Financial net debt down £1.5 billion,

BBB- (+ve outlook)

● Significant growth investment

● High quality sourcing operations

● Highly engaged colleagues

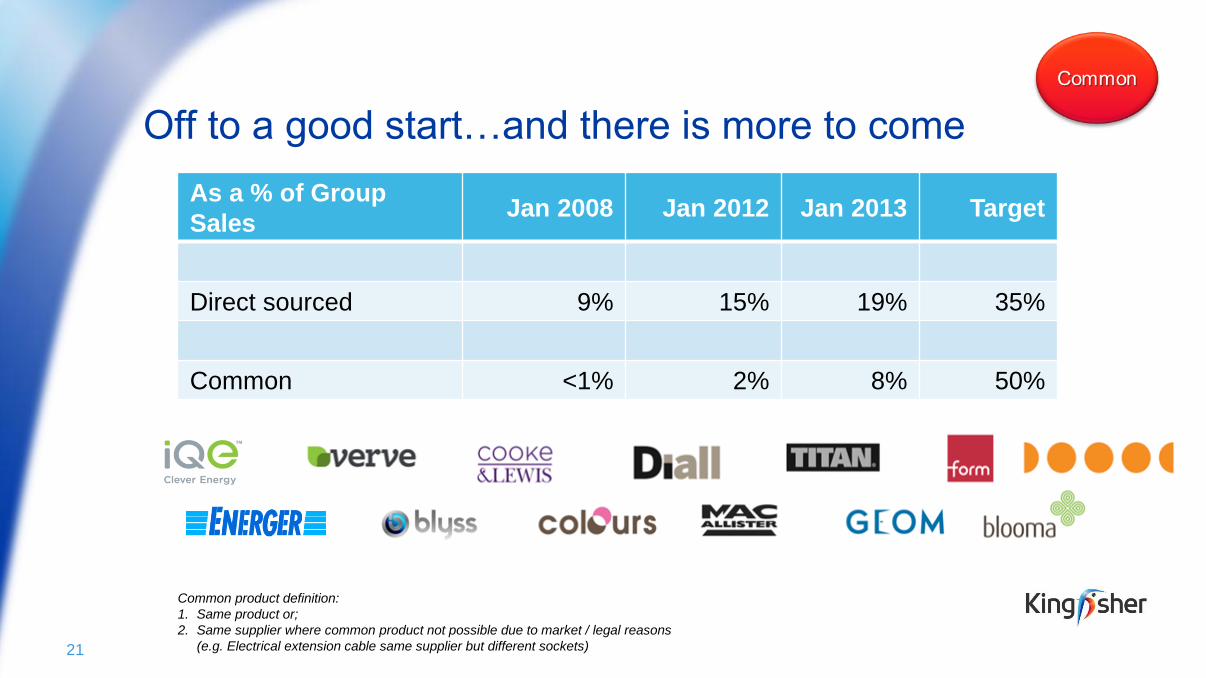

Off to a good start on Common(1) and Direct sourcing

8

Common product definition:

1. Same product or;

2. Same supplier where common product not possible due to market / legal reasons

(e.g. Electrical extension cable same supplier but different sockets)

As a % of Group SalesJan

2008

Jan

2012

Direct sourced 9% 15%

Common <1% 2%

Established 11 Group-wide

common own brands ● Replacing the 150+ local own brands

● Enabling investment in innovation

and prices

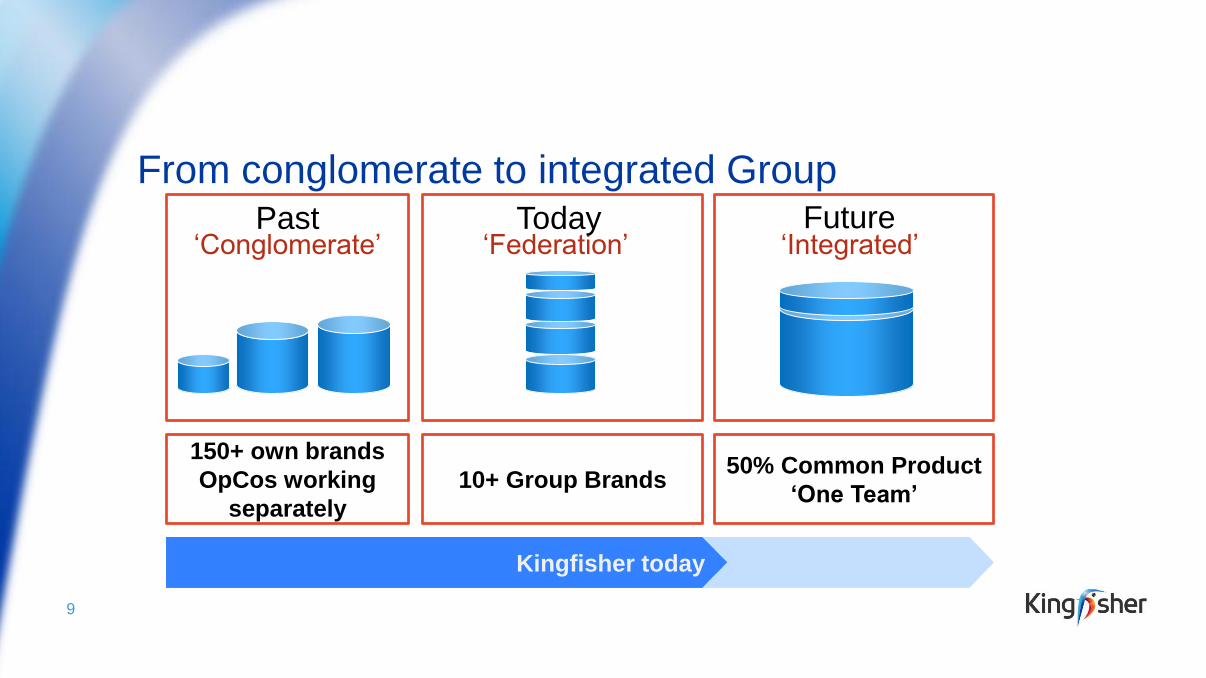

From conglomerate to integrated Group

9

‘Federation’ ‘Integrated’ ‘Conglomerate’Past Today Future

150+ own brands

OpCos working

separately

10+ Group Brands50% Common Product

‘One Team’

Kingfisher today

Strategic History

10

Dem

erg

ing

‘Delivering Value’ ‘Creating the Leader’Easier, Common Expand, One Team

Conglomerate • Home improvement

• General Retail

• Electricals

1980 2000 20122008 2017

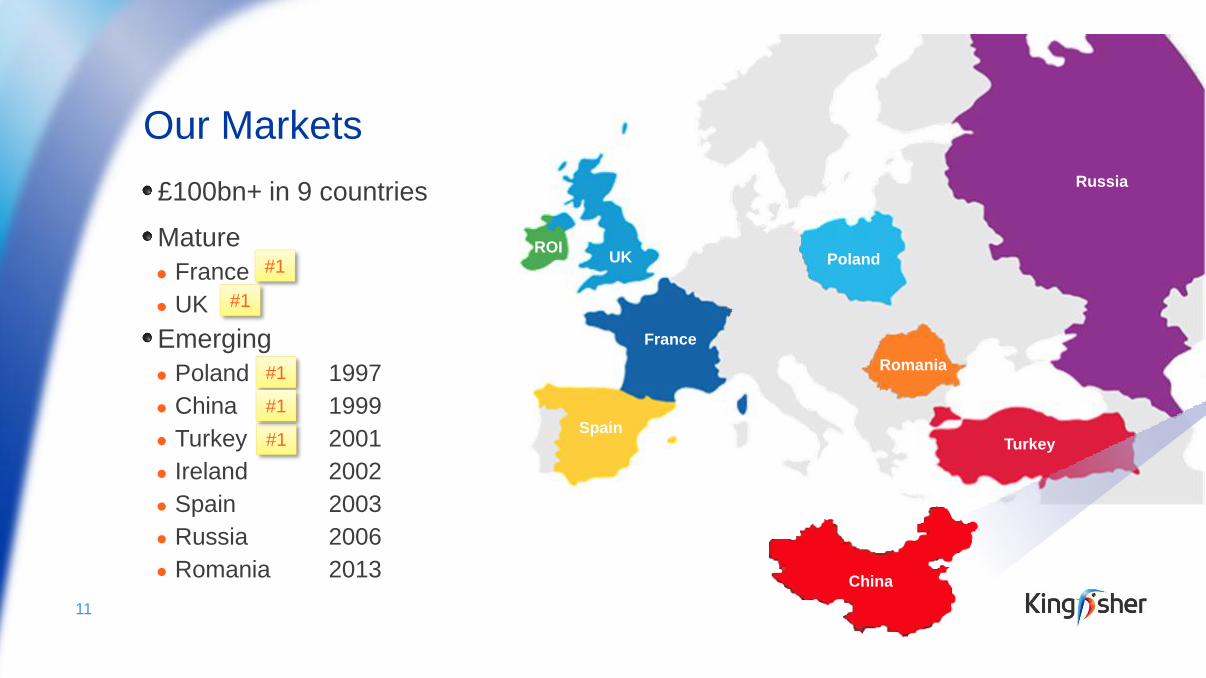

£100bn+ in 9 countries

Mature

● France

● UK

Emerging

● Poland 1997

● China 1999

● Turkey 2001

● Ireland 2002

● Spain 2003

● Russia 2006

● Romania 2013

Our Markets

11

China

China

Romania

France

ROIUK

Russia

TurkeySpain

Poland#1

#1

#1

#1

#1

France

27 million households

DIY is number one pastime in France helped by

● High level of home ownership and growing

● 35h working week

● High savings ratio

Compete on Product and Service more than price

● Two largest Home Improvement retailers make up 50% of the market

● Planning restrictions; difficult to open space

12

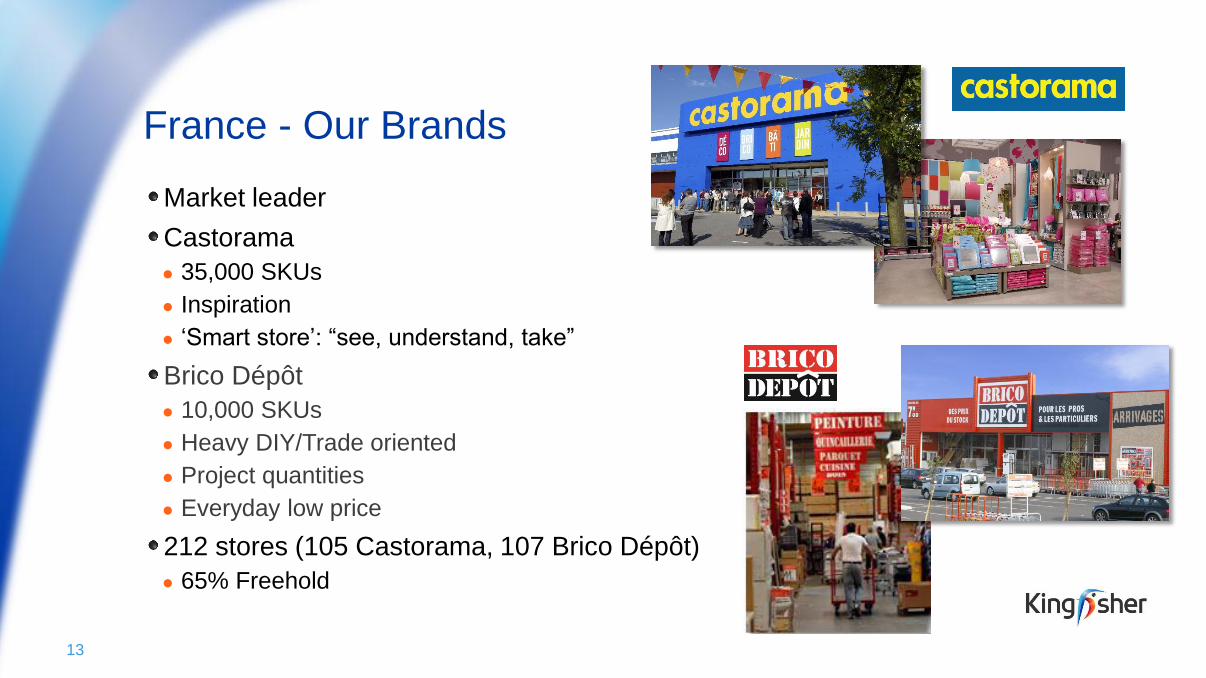

France - Our Brands

Market leader

Castorama

● 35,000 SKUs

● Inspiration

● ‘Smart store’: “see, understand, take”

Brico Dépôt

● 10,000 SKUs

● Heavy DIY/Trade oriented

● Project quantities

● Everyday low price

212 stores (105 Castorama, 107 Brico Dépôt)

● 65% Freehold

13

UK & Ireland

26 million households

High level of home ownership

Nation of gardeners

Government initiatives supporting housing market

Fragmented market, lots of smaller players

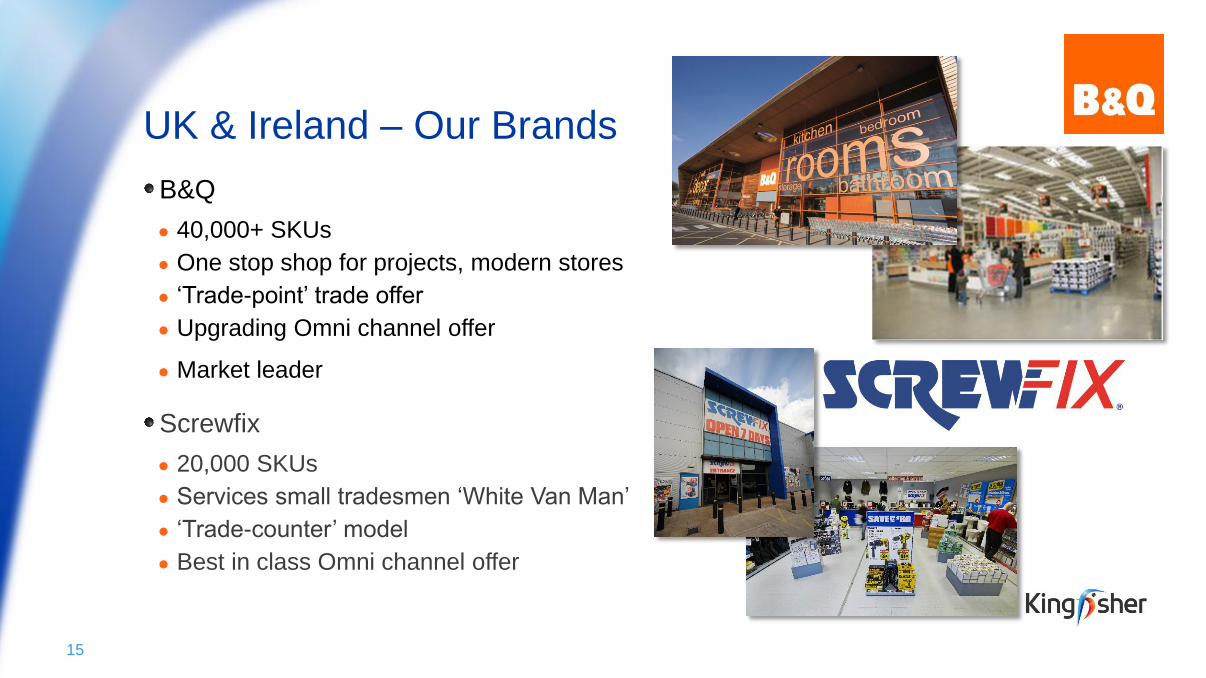

662 stores (359 B&Q, 303 Screwfix)

● 95% leasehold

14

UK & Ireland – Our Brands

B&Q

● 40,000+ SKUs

● One stop shop for projects, modern stores

● ‘Trade-point’ trade offer

● Upgrading Omni channel offer

● Market leader

Screwfix

● 20,000 SKUs

● Services small tradesmen ‘White Van Man’

● ‘Trade-counter’ model

● Best in class Omni channel offer

15

Poland

14 million households

Skilled population, big project DIY

Increasing aspiration, tastes changing

Lots of Soviet era housing and high occupancy ratio

Lots of small local players but underserved by big

retailers

Store revamp program

72 stores

● 80% freehold

16

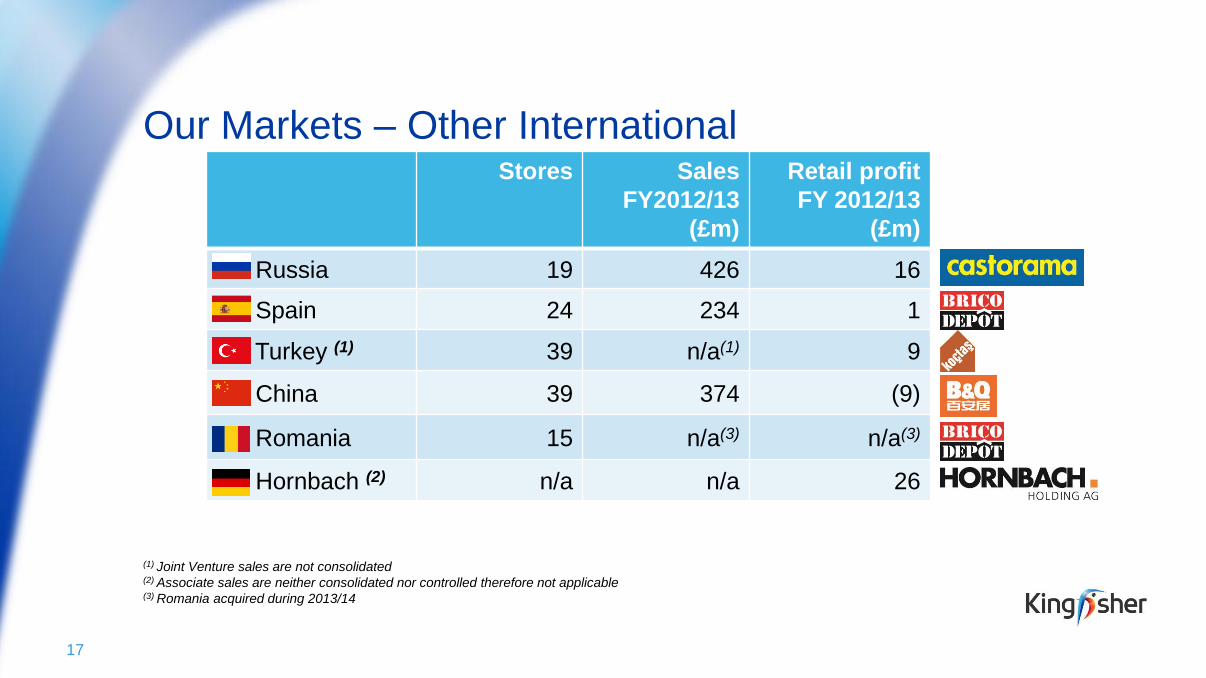

Our Markets – Other International

17

Stores Sales

FY2012/13

(£m)

Retail profit

FY 2012/13

(£m)

Russia 19 426 16

Spain 24 234 1

Turkey (1) 39 n/a(1) 9

China 39 374 (9)

Romania 15 n/a(3) n/a(3)

Hornbach (2) n/a n/a 26

(1) Joint Venture sales are not consolidated(2) Associate sales are neither consolidated nor controlled therefore not applicable(3) Romania acquired during 2013/14

‘Creating the Leader’

18

‘Creating the Leader’

1.Making it easier for customers to improve their home

2.Giving our customers more ways to shop

3. Building innovative common brands

4. Driving efficiency and effectiveness everywhere

5. Growing our presence in existing markets

6. Expanding in new and developing markets

7. Developing leaders and connecting people

8. Sustainability: becoming ‘Net Positive’

Easier

Common

Expand

One

Team

19

Sales

Cost

efficiencies

Gross

margin

‘Creating the Leader’ in action

1.Product innovation

2.Omni channel/click & collect

3. 10+ group brands replacing OpCo own brands

4. One Team Product Show

5. Adding c.3% space per year excl. Romania(1)

6. Screwfix Germany trial, 4 stores summer 2014

Easier

Common

Expand

20(1) Romania acquisition completed in H1 2013/14 added 3% space.

Off to a good start…and there is more to come

21

Common product definition:

1. Same product or;

2. Same supplier where common product not possible due to market / legal reasons

(e.g. Electrical extension cable same supplier but different sockets)

As a % of Group

SalesJan 2008 Jan 2012 Jan 2013 Target

Direct sourced 9% 15% 19% 35%

Common <1% 2% 8% 50%

Expansion where returns attractive,

Rightsizing in UK

22

24%

28%

43%

5%

Existing stores

Omnichannel

IT, Supply Chain & Other

New stores & relocations

FY 2013/14

c.£400m (including Romania)Rightsizing program in UK

● 1 store completed with positive

results

18 store package underway

● 5% less space

Looking at the potential for more

% Space

growth

2013/14

UK & Ireland +1.0%

France +3%(2)

Poland +3%

China (1)%

Romania n/a

Russia +5%

Spain +21%

Turkey +12%

6%

Expand

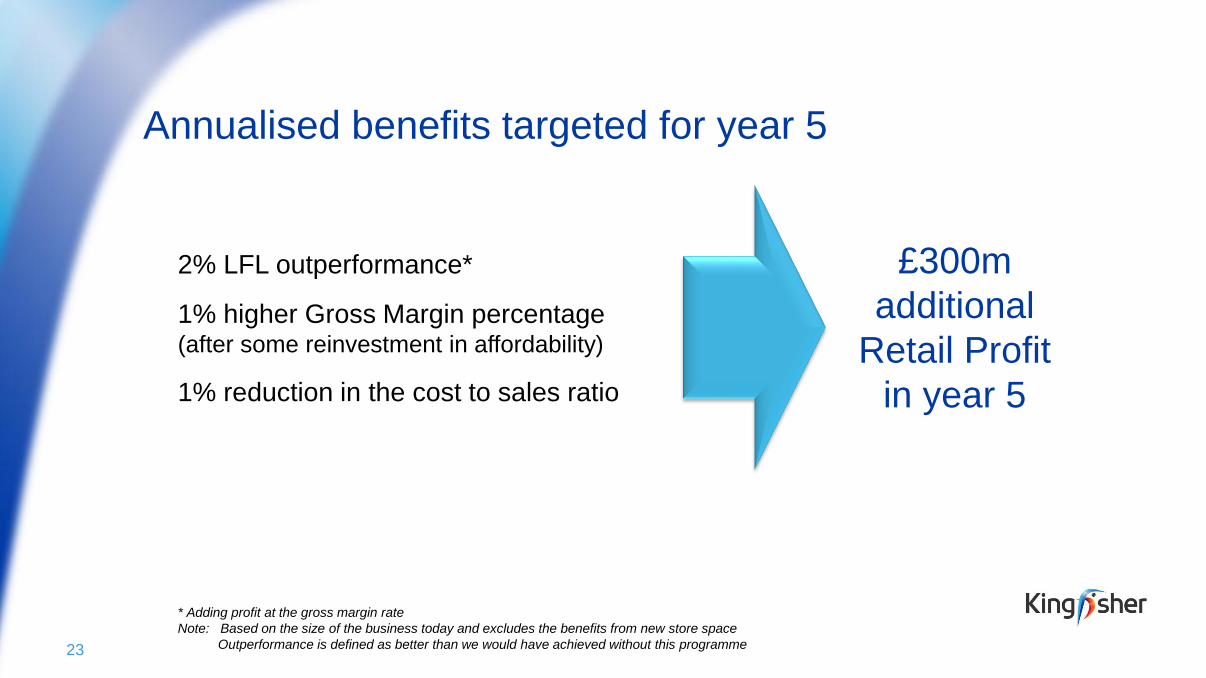

Annualised benefits targeted for year 5

2% LFL outperformance*

1% higher Gross Margin percentage (after some reinvestment in affordability)

1% reduction in the cost to sales ratio

£300m

additional

Retail Profit

in year 5

* Adding profit at the gross margin rate

Note: Based on the size of the business today and excludes the benefits from new store space

Outperformance is defined as better than we would have achieved without this programme23

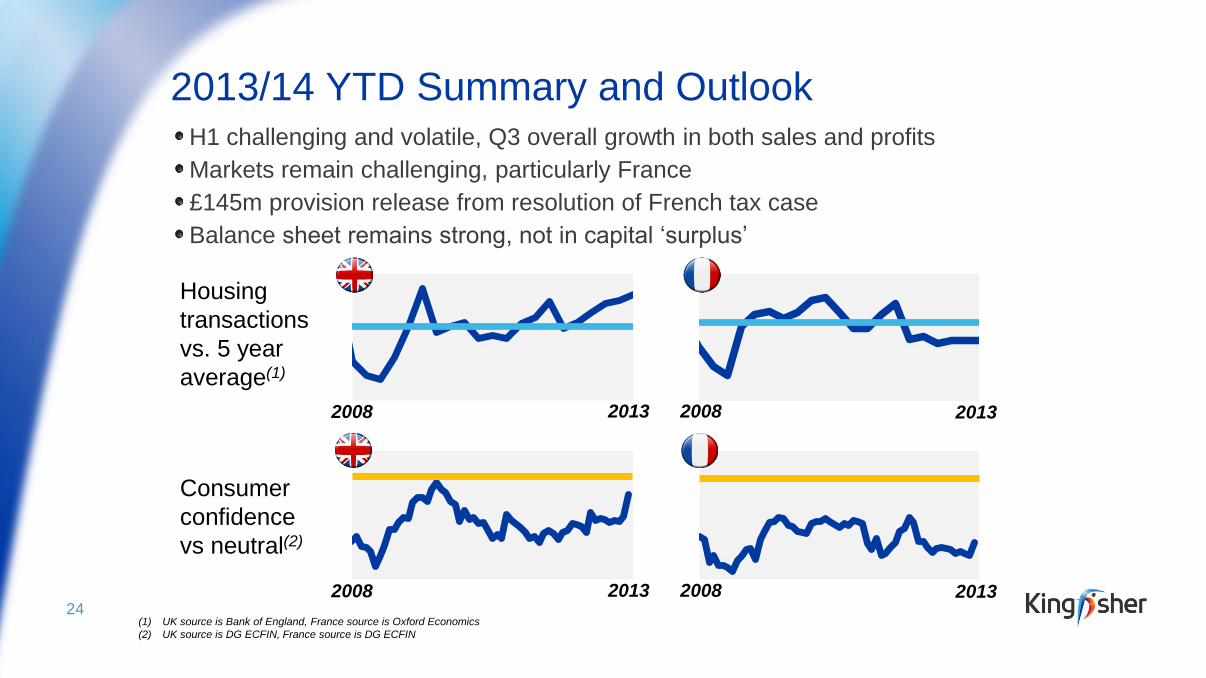

2013/14 YTD Summary and OutlookH1 challenging and volatile, Q3 overall growth in both sales and profits

Markets remain challenging, particularly France

£145m provision release from resolution of French tax case

Balance sheet remains strong, not in capital ‘surplus’

24

Housing

transactions

vs. 5 year

average(1)

Consumer

confidence

vs neutral(2)

2008 2013 20132008

2008 2013 20132008

(1) UK source is Bank of England, France source is Oxford Economics

(2) UK source is DG ECFIN, France source is DG ECFIN

Questions

Contacts

26

Further copies of this presentation will be available for download from www.kingfisher.com

or viewed on the Kingfisher IR iPad App available for free at the Apple App store.

We can be followed on twitter @kingfisherplc.

Ian Harding, Group Communications Director +44 (0)20 7644 1029

Sarah Levy, Director of Investor Relations +44 (0)20 7644 1032

Matt Duffy, Investor Relations Manager +44 (0)20 7644 1082