presentation to ppc cost to communicate (2)pmg-assets.s3-website-eu-west-1.amazonaws.com/... ·...

TRANSCRIPT

Presentation to PPC Cost to communicate (2) 7 November 2014

1. Reflection: Cost to communicate 2008 – 2012 (Cape Town 30 November 2012)

2. Cost to communicate 2012 onwards

3. South Africa achievements

4. International ranking and challenges towards available, accessible and affordable services

5. Comparison

6. Concluding thoughts

Contents

Reflection: Cost to Communicate 2008 - 2012 Cape Town 30 November 2012

• 44% decrease in effective prepaid PPM to 79c

• 30% decrease in effective total PPM to 1.07c

R

1.53

1.07 1.41

0.79

June'08

Blended ppm Prepaid ppm

Pricing: Blended and prepaid

June’12

Pricing: Data

R 0

R 200

R 400

R 600

R 800

R 1 000

R 1 200

500MB Price

1GB Price

2GB Price

• 88.5% decrease in 1GB data package from R599 to R69 (24 Month Mobile Broadband)

• Out of bundle rate decreased by 90% from R10 to R1 per MB

Reducing the cost to communicate 2008-2012 Prices are declining and will continue to go down due to…

…. effective competition in the telecommunications market.

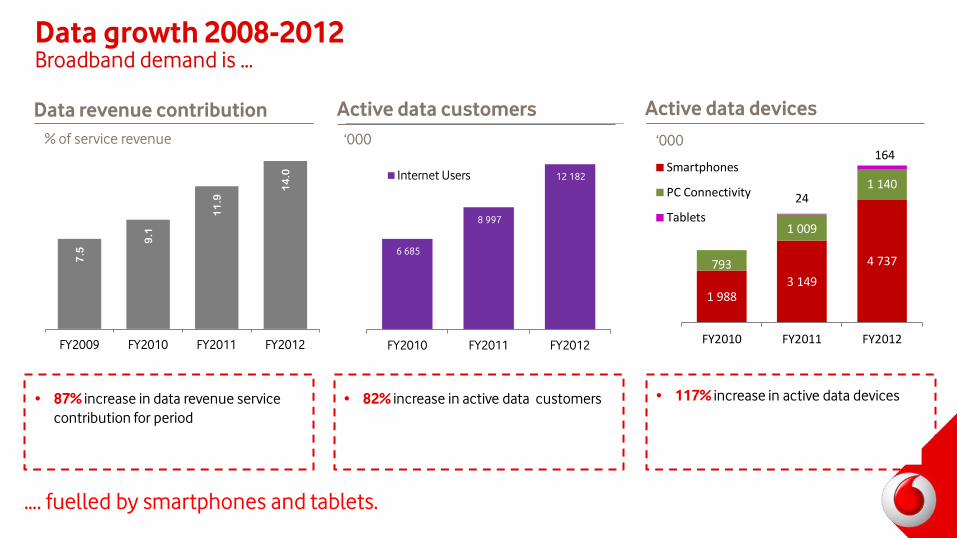

1 988 3 149

4 737 793

1 009

1 140 24

164

FY2010 FY2011 FY2012

Smartphones

PC Connectivity

Tablets

5

Active data devices Data revenue contribution

• 87% increase in data revenue service contribution for period

Active data customers ‘000

• 82% increase in active data customers

• 117% increase in active data devices

Data growth 2008-2012 Broadband demand is …

7.5

9.1

11

.9 1

4.0

FY2009 FY2010 FY2011 FY2012

% of service revenue

6 685

8 997

12 182

FY2010 FY2011 FY2012

Internet Users

‘000

…. fuelled by smartphones and tablets.

Cost to communicate 2012 onwards Cape Town 7 November 2014

The journey: Significant progress in transforming pricing…

Pricing Transformation

Data growth

Simplification

Investment • Invested heavily in network to carry more traffic as prices are reduced. • Invested in increased coverage especially 3G/4G.

• Substantially reduced pricing for voice and data. • Much more value offered. • Launched worry free innovations – RED, PowerHour, My5, Everyday Extra, SMS

• All tariffs are simple & transparent – On net, All net, Anytime offers. • Old tariffs shifted to legacy. • Proactive migration in place for both voice and data legacy plans.

• Significant data growth to supplement declining voice revenues.

Bundles • On net bundles and all net bundles to drive down cost to communicate and target low end users.

Where to next… • Work proactively to build network capacity to maintain best network experience. • Embed and activate new pricing through education campaigning.

…. delivering value to customers.

The journey: Prepaid pricing catering for…

…. access and affordability.

Vodacom Smart/Red

Subscription (no device)

Subscription (with device)

Voice Data SMS

Smart S R149 R 199 75 200 200

Smart M R229 R 299 120 300 300

Smart L R379 R 499 250 500 500

Smart XL R529 R 699 400 800 800

Red Advantage R749 R 999 700 1 GB Limitless

Red Premium R1199 R 1 599 1 200 2 GB Limitless

Red VIP R1499 R 1 999 Limitless 5 GB Limitless

• Simplified price plans with any network anytime pricing.

• Substantial value added.

• Integrated price plans with smartphones included driving data adoption.

The journey: Simplified and much more value…

…. to Contract customers.

0.91

0.68

0.64

0.46

Blended ppm Prepaid ppm

The journey: Further price reductions and more choice

• Converted 63% of voice only contracts to Smart and Red plans

• 28% decrease in effective prepaid PPM to 46c

• 25% decrease in effective blended PPM to 68c

• 26% increase in total outgoing voice traffic

R

• 83% of monthly gross connections in Top Up are on uChoose plans

37

63

Voice plans Integrated plans

Pricing: Blended and prepaid Hybrid: Smart and flexi plans Contract: Integrated plans %

Jun 14

Prices continued to decline

Jun 13

• 18.4% increase in data revenue

The journey: Accelerating take-up of mobile data

25.8% of service revenue

Data contribution Active data devices

• Smartphone average usage up 44.5% to 312MB

‘000

Active data customers

• 25.0% growth in active data customers

‘000

12 182 14 385 16 996

FY2012 FY2013 Q1 2015

Active data customers Penetration

43.5% 48.1%

52.3%

4 737 5 967 7 393

1 140

1 129

1 073 164

364

567

FY2012 FY2013 Q1 2015

Smartphones PC connectivity Tablets

12

Broadband demand is …

…. fuelled by smartphones and tablets.

The journey: Simple and transparent engagement

Retail Call Centre Online Self Service

Direct

…. towards informed decisions on service provider, service and tariff.

The journey: Customer satisfaction We track our net promoter score (‘NPS’) on a monthly basis …

…. our key measure of customer satisfaction.

South Africa achievements

25%

42% 44% 51% 55% 64% 67% 71%

79% 89%

96%

126% 134%

145% 148%

Mad

agas

car

Mal

awi

DRC

(ex-

Zaire

)

Moz

ambi

que

Tanz

ania

Swaz

iland

Ango

la

ave

Zam

bia

Leso

tho

Zim

babw

e

Nam

ibia

Mau

ritiu

s

Sout

h Af

rica

Bots

wan

aSource: GSMA, Intelligence (2015-2017 estimates)

Mobile penetration and coverage SA has a vibrant mobile market

Population Coverage

…. 3G where we have 2G.

3G 94.1%

2G 99.9% Vodacom’s accelerated capital investment programme

• Completed network RAN renewal – 4G ready

• 2000 LTE sites

• 76% of sites connected to own high capacity transmission network

International ranking and challenges towards available, accessible and affordable services

Brazil Russia India China South Africa

Ranking for period 2012 2014 2012 2014 2012 2014 2012 2014 2012 2014

Network Readiness Index 66 69 56 50 69 83 51 62 72 70

Source:http://www3.weforum.org/docs/WEF_GlobalInformationTechnology_Report_2014.pdf

• SA continued to show robust growth.

• SA’s global ranking improved based on certain important improvements in the penetration of ICTs among individuals.

• SA has overtaken India and ranks favourable with Brazil and China.

South Africa’s ranking improved Network Readiness Index

…..favourable compared with Brazil and China

Spectrum challenge: Timely assignment is vital for growth

European Regulators assigned 800MHz spectrum between 2010 and 2013

When will Regulators in Africa follow suite?

Source Vodafone and ITU IDI*: Global ICT Development Index 2012

7 8 11 16 19 23 24 27 30 31 32 34 36

42

55

69

80 84 86

113 116 121

142 147 148

0

20

40

60

80

100

120

140

160

0

20

40

60

80

100

120

140

160

180

200

IDI R

anki

ng

Am

ount

of S

pect

rum

(MH

z)

Operators & IDI Rankings (ITU)

Amount of Spectrum Allocated (MHz) IDI ranking

…correlates with ITU ICT Development Ranking

The amount of assigned spectrum…

Other challenges … • Site acquisition

– High rentals

– Cumbersome approval process

– Objections from public

– Lack of policy or alignment of policy in municipalities

– Long lead times to obtain AC power

• Fibre and microwave deployment – Way leaves

– Cumbersome approval process

– One-trench policy

– Mast space and strength on existing infrastructure

Comparison

Coverage Pricing

http://explorer.netindex.com/maps#

Speed

Technology e.g. LTE

Internet users

http://techtalkafrica.com/south-african-internet-users-infographic.html

Investment

Penetration Devices

Comparison against peer countries Performance indicators should amongst other consider…

8.4

…. in assessing SA’s global ranking.

Concluding thoughts

Concluding thoughts • Prices continue to decline

• Increased customer centricity

• Increased investment in coverage and capacity

• Spectrum required towards further improvement

• Be assured of Vodacom’s commitment

Thank you

29