presentation to mbs 2017 forecast panel -...

TRANSCRIPT

© 2017 IHS Markit. All Rights Reserved.© 2017 IHS Markit. All Rights Reserved.

Presentation to MBS 2017 –Forecast Panel

Michael RobinetManaging Director, Automotive Advisory Solutions

© 2017 IHS Markit. All Rights Reserved.

AUTOMOTIVE

The automotive sector is one of the biggest and most competitive markets in the world and relies on in-depth analysis for its daily operations.

Our extensive global team of automotive analysts located in 15 key markets supplies the depth of information and level of comprehension needed for a competitive edge.

IHS Markit automotive solutions span the entire value chain, from product inception to sales, marketing andthe aftermarket.

We scale our insights to address virtually any domain or enterprise, improving the speed, accuracy and impact of business strategy and tactics.

2

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Past IHS Markit Forecast Panel Themes

• 2012: Constant Structural Change

> Global platforms, pressure to add capacity while building profitability

• 2013: Opportunities and Bottlenecks

> Rise of non-Detroit 3, need to look outside the traditional structures

• 2014: A Proactive Supplier

> No longer wait for RFQs and ‘innovation ideas’ from customers – find the right business

• 2015: The Next Stage

> Describing a market with faster cadence, driven by regulations and production localization

• 2016: Foresight Reigns

> Need for suppliers to take greater control of their destiny

• 2017: Focus On The Journey ….

> Level 5 & BEVs are the destination – The journey will separate winners from losers

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.© 2017 IHS Markit. All Rights Reserved.

Focus on the JourneyPresentation to MBS 2017 – Forecast Panel

Michael RobinetManaging Director, Automotive Advisory Solutions

© 2017 IHS Markit. All Rights Reserved.

Improving US Economy Will Keep Vehicle Market Steady

-3%

-2%

-1%

0%

1%

2%

3%

4%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

Real GDP Growth Rate

Real GDP Growth Rate

5

• Real GDP – Economic signals mixed; Consumer confidence and many sectors improving, but strong dollar hurting trade. Growth improving this year, 2.2%, and next year towards 3% before declining.

• Monetary Policy – FED expected to continue to raise interest rates, weak global conditions causing delays. US labor market key; do rising wages support tightening?

• Fiscal Policy – Spending will rise in 2017 thanks to proposed infrastructure and military outlays, contributing to growth for first time in years. Impact of 2017 Tax rate cut viewed as positive though replacing declining revenues will be an issue.

• Consumption – Real consumer spending improving – stronger labor markets, falling energy prices and improved household balance sheets all contributing.

• Housing – Plenty of recovery left to go, Housing Starts only at 2/3 of pre-crash averages. Sector will gain momentum as household formation and labor markets improve.

• Employment – The good times of monthly job gains averaging 200,000 or better are probably over; the rest of this year and next should be more moderate than the past couple of years.

• Foreign Trade – Strong dollar is hurting trade balances, a drag on the US economy through 2018. Recent yuan devaluation, coupled with already weak euro and yen, will impact OEM sourcing decisions.

• Investment – Strong profits, stock prices, suggest business fixed investment will accelerate; low oil prices are a “surprise” cost savings, but within the oil sector a major pullback is occurring.

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Crude Slowly Recovers Amid New Supply• In a six-month accord that took effect in

January 2017, OPEC agreed to cut its production 1.2 million barrels per day. Russia’s energy minister announced a reduction of 300,000 barrels per day.

• The US onshore oil industry is proving effective at cutting costs and achieving efficiencies. US crude oil production bottomed in fourth-quarter 2016 near 8.6 MM b/d and will increase about 400,000 b/d during 2017.

• Under the Trump administration, reduced regulation, fewer hurdles for pipeline construction, and an opening of public lands to exploration and production could lead to higher-than-expected oil and gas supplies.

• The price of Dated Brent crude oil is projected to increase from USD44/barrel in 2016 to USD54 in 2017 and USD57 in 2018.

6

$0

$25

$50

$75

$100

$125

$150

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027

Current US dollars 2016 US dollars

Price of Dated Brent crude oil (USD/Barrel)

Source: IHS Markit © 2017 IHS Markit

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

US: Light Vehicle Sales Forecast

4

6

8

10

12

14

16

18

20

Millions

Sales Vol Car Light Truck Linear (Sales Vol)

7

Market Dynamics Shifts – Conquest & Loyalty are Critical, Mix Shifts and More Players/Nameplates

Market peaks in 2018 – weaker buying conditions,

slower job creation, rising oil prices start next cycle.

Successful tax reform required ….

Source: IHS Markit Automotive, current light vehicles sales forecast

2017

17.1m

Car – sales flatten - rises as

affordability declines

LT – peaks in 2018, weaker

housing, higher fuel &

regulations force declinePre-Crash

40 year trend:

+140k annually

Model Count

2010 2016 2023

335 371 409

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Global LV Production Outlook

Region 2016 2017 2018 2019 2020 2022 2024 CTG2016-24

Notes

China 27.4 27.6 27.9 29.4 30.5 31.9 33.1 37% • Tier 3 & 4 city growth

Europe 21.5 22.1 22.4 22.5 23.0 23.6 24.0 16%• Slow rebound of Russia

and shift from West EU

NA 17.8 17.4 17.5 17.7 18.4 18.1 18.0 1% • D3/A4/G3 Realignment

South Asia 8.4 8.7 9.2 9.7 10.7 11.9 13.3 31%• India domestic &

export, ASEAN rise

Japan/Korea 12.9 13.4 13.0 12.7 12.6 12.5 12.4 -3%• Slow domestic mkts,

production co-location

South America 2.7 3.1 3.4 3.5 3.8 4.3 4.7 13%• Well below 2013 record

of 4.5 mil

Middle East/Africa

2.3 2.5 2.7 2.9 3.1 3.3 3.2 6%• Focus of more attention

by OEMs

Total 93.1 94.9 96.1 98.4 102.0 105.6 108.7

8

Over 70% of Total Growth From Emerging Asia

CTG – Contribution to Growth

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Top OEM Cooperative Groups by Production Volume 2024

0

2

4

6

8

10

12

14

16

18

20

Toyota+Mazda+Fuji+Suzuki

VW+ Tata R/N+Mits.

GM+ SAIC Hyundai Ford Honda FCA PSA Daimler BMW Geely+Proton

Changan BAIC Great Wall

Millions

Global Production Volume

9

Top-15 OEM Groups

Top-15 OEMs Total Volume

• A4: 44.6 M• D3: 21.8 M• G3: 20.2 M• Others: 12.0 M

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

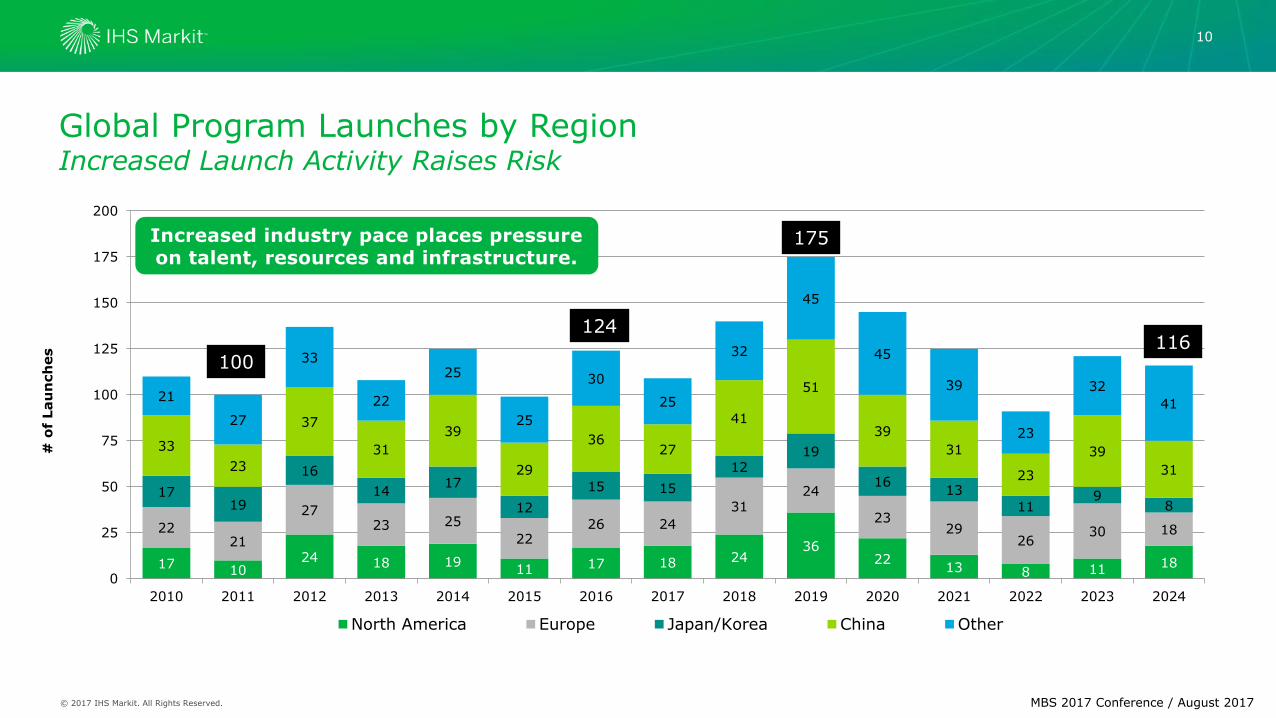

Global Program Launches by RegionIncreased Launch Activity Raises Risk

10

17 1024 18 19

11 17 18 2436

2213 8 11 18

2221

2723 25

2226 24

3124

2329

2630 18

1719

16

1417

12

15 15

1219

1613

119

8

33

23

37

31

39

29

3627

41

51

39

31

23

39

31

21

27

33

22

25

25

30

25

32

45

45

39

23

32

41

0

25

50

75

100

125

150

175

200

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

# o

f Lau

nch

es

North America Europe Japan/Korea China Other

100

124

175

116

Increased industry pace places pressure on talent, resources and infrastructure.

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

-

2

4

6

8

10

12

14

16

18

20

2000 2003 2006 2009 2012 2015 2018 2021 2024

NA

LV

Pro

du

cti

on

Millio

ns

Detroit 3 Asian 4 German 3 Other

NAFTA ProductionCustomer Dynamics Changing …

• Rise in Mazda, Fuji Heavy, Volvo and Tesla underscores ‘Other’ OEM rise – Supply base shifts.

• Detroit 3 output declines due to new competition, comparative lack of exports and inflexibility to shift to

CUVs from sedans.

11

77%17%

3%3%

Det 345%

Asian 438%

Germ 310%

Other7%

NAFTA Production Share

2000

2024

17.418.118.4

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

NA Regional ShiftLogistics and Supply Structure Under Pressure

2.4 2.4 2.3 2.3 2.2 2.2 2.2 2.3 2.2 2.2

5.6 5.44.6 4.5 4.4 4.5 4.5 4.3 4.3 4.3

-

3

6

9

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pro

d V

ol

Mil

Midwest/Ontario

13

2.7 2.8 2.7 2.6 2.6 2.8 2.8 2.8 2.7 2.7

0.9 0.9 1.0 1.0 1.1 1.0 1.0 0.9 1.0 1.0

0.8 0.8 0.8 0.8 0.9 0.9 0.9 0.9 0.9 0.9

-

3

6

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pro

d V

ol

Mil

Southeast

1.1 1.3 1.4 1.5 1.6 1.7 1.7 1.6 1.6 1.6

1.6 1.6 1.8 1.7 1.8 1.7 1.7 1.7 1.6 1.70.5 0.4

0.6 0.8 0.8 0.9 0.9 0.9 1.0 1.0

-

3

6

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pro

d V

ol

Mil

Mexico

A4 D3 G3 Oth

• Mix towards D/E-segment and Full Frame

• Detroit 3 still account for +60% of MW/ONT volume by 2024

8.06.9

4.6 4.7

3.5

4.5

• Remarkable stability – newer facilities w/export focus

• Higher concentration on C & D-segment CUVs

• Mid-Mexico now accounts for ~70% of Mex volume

• Rise of B & C-segment products with increasing luxury focus for export

7.2

4.8

4.6

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Detroit Three Volumes Peak …

0.5

0.6

0.7

0.8

0.9

1.0

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Q32019

Q42019

Millions

Quarterly NA Light Vehicle Production

General Motors General Motors Run Avg Ford

Ford Run Avg FCA FCA Run Avg

14

Peak

Peak

Peak

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

SUV/CUVs Dominate Production – Flexibility in Question

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Q32019

Q42019

Millions

Quarterly NA Light Vehicle Production

SUV SUV Run Avg Sedan Sedan Run Avg

Pickup Pickup Run Avg All Other All Other Run Avg

15

SUV Peak

Pickups Peak

Sedan Trough

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

U.S. Production In Decline as Mexico Steadily Grows

0.4

0.9

1.4

1.9

2.4

2.9

3.4

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Q32019

Q42019

Millions

Quarterly NA Light Vehicle Production

United States United States Run Avg. Canada

Canada Run Avg. Mexico Mexico Run Avg.

16

Peak

Shows no signs of slowing

Peak

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

0

10

20

30

40

50

60

CA

FÉ S

tan

dar

d (

MP

G)

Model Year

Cars

Trucks

Combined

EPA vs. NHTSA vs. CARB vs. the EU vs. China – Many Considerations …

Two key milestones for the future are the 2016 requirement and then the more difficult 2022-2025 requirement

New US Plan

??

Cars

Trucks

• US Administration is in the midst of a mid-term review with a recent note that standards may be reduced or frozen as of Model Year 2021.

• Complicating factors include the California Exemption, the ‘177’ states which follow California as well as emission reduction/electrification efforts of China, EU and Quebec.

17

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

95

98

104

107

110

13%

33%

34%

55%

45%

3%11%

29%

2.2% 3.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

75

80

85

90

95

100

105

110

115

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025%

Sh

are o

f P

ro

du

cti

on

Glo

bal Pro

duction V

ol. -

Millio

ns

Global Electrification Penetration

Volume Electrification Share Stop/Start Share Hybrid Share BEV Share

Global & NA Electrification Trends

18

Led by EU & China, Global has higher ‘electrification’ share, while North America will be slower

MBS 2017 Conference / August 2017

15.2

15.6

17.0

16.7 16.7

2%

11%

20%14%

56%

63%

7% 15%3.8% 4.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

14.0

14.5

15.0

15.5

16.0

16.5

17.0

17.5

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

% S

hare o

f P

ro

du

cti

on

N.A

. Pro

duction V

ol. –

Millio

ns

N.A. Electrification Penetration

Greater emphasis on Start/Stop tech. in N.A.

Electrification includes: Mild-/Full-Hybrid, BEV, Fuel Cell

© 2017 IHS Markit. All Rights Reserved.

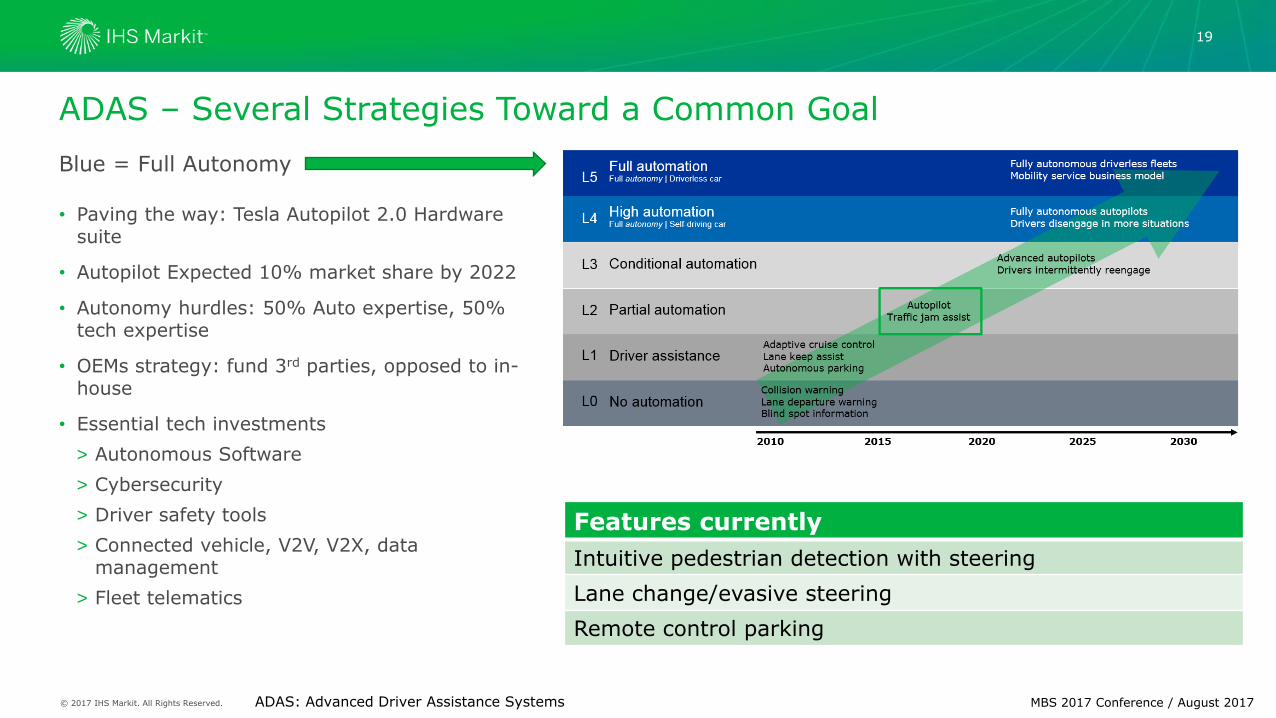

ADAS – Several Strategies Toward a Common Goal

• Paving the way: Tesla Autopilot 2.0 Hardware suite

• Autopilot Expected 10% market share by 2022

• Autonomy hurdles: 50% Auto expertise, 50% tech expertise

• OEMs strategy: fund 3rd parties, opposed to in-house

• Essential tech investments

> Autonomous Software

> Cybersecurity

> Driver safety tools

> Connected vehicle, V2V, V2X, data management

> Fleet telematics

Blue = Full Autonomy

Features currently

Intuitive pedestrian detection with steering

Lane change/evasive steering

Remote control parking

MBS 2017 Conference / August 2017

19

ADAS: Advanced Driver Assistance Systems

© 2017 IHS Markit. All Rights Reserved.

North American Engine LaunchesCombination of Engine Family, Displacement and Engine Plant

20

0

2

4

6

8

10

12

14

16

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

# o

f Lau

nch

es

GM Ford FCA Toyota Honda Nissan Hyundai VW Daimler BMW Others

1

MBS 2017 Conference / August 2017

OEMs are spending a greater share of

resources on electrification,

batteries and power structures.

13

14

10

© 2017 IHS Markit. All Rights Reserved.

The Journey to Level 5 & Battery Electric

21

Substantial Change/New Modest Change

Thermal Propulsion (Engine/Trans)

Electrical/ Power Supply Fuel

Body In White Exhaust

Steering Suspension

Braking Interior

Aerodynamics/ NVH Seating

Driveline Exterior

Electronics Passive Safety

Battery

Vision/Lighting

ADAS/ Active Safety

Wheels/Tires

• Shift towards soft from hard parts

> Many suppliers focus resources on mechatronics, electric actuation, software and system integration

> Share of ‘value’ devoted to hard parts decline – the pie slices thinner

• System shifts will be rampant

> Major transitions in body, braking, chassis, steering and thermal as electrification and autonomy have a profound impact.

> Increase in 48 volt systems and the need for efficient distribution systems all underscore looming change.

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

~2020

Mass Reduction Shifts Beyond The ‘Edge Segments’

Mild Hybrid Rise Starts in Larger Segments, 48V

L3 Autonomy, More ADAS Content, Warranty Visibility

Today

BIW & Chassis System Lightweighting Begins

Down Displacement, Multi-speed Trans & S/S

ADAS & Connectivity Content Rises, Warranty Costs

A Looming Cost Cliff Alters The EcosphereOEMs, Suppliers, Regulators and Customers Are All Impacted

~2025

Integration of ‘Non-Standard Materials’ & Joining Methods

Full Hybrid, BEV and Alternative Drive Formats Rise

L3/4 Autonomy, Global influences, System Profit Pools Shift

~2030

+

Competitive Dynamics Shift – ‘Old’ Industry versus ‘New’ Industry

Optimization of BEV Packaging – Vehicle Longevity Extends

Level 5 Emerges, New Content Suppliers/Integrators

Success in a Rising Cost Environment

• Understand your costs, markets & risk profile

• Your systems in the new structure?

• Hedge technologies

• Smart vertical integration

• Proactive engagement

• Today’s differentiators are not tomorrow’s

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Summary

• Plateauing volumes alter the landscape

> OEMs feeling the pressure of increased incentives, warranty exposure and competition –i.e. enhanced productivity/currency ‘adjustment’ requests

> Existing suppliers begin to cannibalize as new suppliers enter the market

– Indian & Chinese-owned concerns, Tier II Japanese/Korean and EU suppliers (following expanding Tier Is) and Silicon Valley entities

• Looming cost cliff drives urgency into system cost reductions

> Increased evidence of incremental cost transparency driven by OEMs

• Supplier strategies vary by system

> Vertical integration to offer enhanced capability to blunt margin erosion

> Smart capital deployment, priority opportunity targeting, less may be more

MBS 2017 Conference / August 2017

© 2017 IHS Markit. All Rights Reserved.

Thank You

Michael Robinet

Managing Director, IHS Markit AutomotiveAdvisory [email protected]

COPYRIGHT NOTICE AND DISCLAIMER

© 2017 IHS. All rights reserved. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form withoutprior written consent of IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions ofauthorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, norare the opinions and analyses which that are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors oromissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please notethat no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections,forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially fromforecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance onany information in this publication is entirely at your own risk. IHS and the IHS logo are trademarks of IHS.

IHS Markit Customer Care:

Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

Asia and the Pacific Rim: +604 291 3600; [email protected]

24