presentation to cmu · no matter what business challenge you're facing, ... march 2010 initial...

TRANSCRIPT

November 2, 2012

Presentation to CMUFinancing Your Startup

Presented by Brian Goncher and Joe Krolczyk

AgendaPART I

Venture Capital Trends

PART II

Presenting Your Plan

PART III

Creating Financial Projections

PART IEmerging Growth Companies

Venture Capital Trends

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Our commitment to companies like yours

Deloitte Emerging Growth Companies

Our emerging growth company practice is a part of our national Deloitte Growth Enterprise Services practice.

Private ,companies form the backbone of our economy. At Deloitte, more than 50% of our U.S. clients operate in this sector.

Our Deloitte Emerging Growth Company practice, and its professionals who will be serving you, fully understand and are focused on addressing the unique needs and challenges of companies like yours. Some of those challenges are:

• Financing your business• Executing your strategy• Anticipating market forces• Organic growth, acquisitions, other transactions• Risk management• Reputation in capital markets• Sustainability

At Deloitte, we serve all our clients with the same passion, quality, and audit and tax sophistication, while tailoring our approach to the unique circumstances of each company.

Our Perspectives program is a multifaceted series of live events, signature reports, research publications, webcasts, podcasts, and other vehicles that deliver tailored and relevant insights to privately held companies in an integrated fashion.

Deloitte Growth Enterprise Services held its third Private Perspectives live eventon May 9, 2012, featuring guest speaker Jeff Immelt, chairman and CEO of GE, and a panel discussion with senior Deloitte leaders. Previous events featured former Federal Reserve Chairman Alan Greenspan and former President Bill Clinton.

These events are simulcast to dozens of locations in the United States where Deloitte professionals and private company executives meet to listen to the program and then discuss the issues among themselves. These are excellent forums for networking, and we welcome the participation of GridSpeakexecutives.

4

Distinctive client service experience

Our Deloitte Emerging Growth Company Services professionals deliver a distinctive, personalized client service experience.

Tailored approach

Our team works collaboratively to customize and scale our integrated service delivery to each client’s specific needs, size, ownership structure, and opportunities.

Trusted service

Deloitte works to become a trusted independent service provider by genuinely listening to each client’s individual issues, understanding their business inside-out, and addressing issues with objectivity and candor.

Breadth and depth

Deloitte is dedicated to helping clients benefit from the full breadth of our global network, deep technical skills, and industry knowledge.

Our Deloitte Emerging Growth Company approach

Click on the link below, or paste it into your browser, and you will access our Deloitte Growth Enterprise Services website, where you can read our proprietary surveys on issues relevant to private companies, client newsletters, and more: http://www.deloitte.com/view/en_US/us/Services/deloitte-growth-enterprise-services/index.htm

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Global leadership and strength

their commitment to a single vision: to be the standard of excellence.

Deloitte is the global leader in professional services, and we understand the risks, rewards, and complexities of business today. Our multidisciplinary approach –drawing from the experience of our audit, tax, consulting, and financial advisory professionals – gives our teams a broader perspective on emerging issues and leading practices, and we bring that knowledge to you. Through years of experience, our professionals have gained the ability to anticipate and respond to our clients’ needs in today’s economy.

No matter what business challenge you're facing, our team has likely faced the same challenge or something similar. In addition, we provide access to our global network of resources who know and understand your industry, issues, and opportunities.

Together, in a culture of collaboration, we offer the capability through our local service team to deliver insights that others might miss.

5

Worldwide • Approximately 182,000 professionals

located in more than 150 countries

• 55 member firms

• More than $28 billion in revenue

• Deloitte’s global organization serves nearly 90% of the technology, media, and telecommunications companies in the Fortune Global 1000

National• More than 51,000 professionals

• 100 offices in nearly 90 cities

• More than $10 billion in revenue

• Our U.S. network of more than 4,500 professionals provides audit or non-audit services to more than 1,400 clients in the technology, media, and telecommunications industries

West Region• More than 5,000 professionals in 11

locations

• Fastest-growing venture capital practice

• Fastest-growing emerging growth practice

• Washington national tax office west

• National office west — accounting consultations

Deloitte by the Numbers

The Deloitte member firm organization, Deloitte Touche Tohmatsu Limited, is the largest professional services network in the world. Approximately 182,000 professionals in more than 150 countries demonstrate

Initial public offering experience

Source: NASDAQ.com

Initial Public OfferingAntheraPharmaceuticals6,000,000 SharesCommon StockPrice $7.00 Per Share

March 2010

Initial Public OfferingRosetta Stone6,250,000 SharesCommon StockPrice $18.00 Per Share

April 2009

Initial Public OfferingOpenTable3,000,000 SharesCommon StockPrice $20.00 Per Share

May 2009

Initial Public OfferingMedidata Solutions6,300,000 SharesCommon StockPrice $14.00 Per Share

June 2009

Initial Public OfferingLogMeIn7,666,667 SharesCommon StockPrice $16.00 Per Share

July 2009

Initial Public OfferingA123 Systems28,180,501 SharesCommon StockPrice $13.50 Per Share

September 2009

Initial Public OfferingFortinet12,500,000 SharesCommon StockPrice $12.50 Per Share

November 2009

Initial Public OfferingGAIN Capital407,692 SharesCommon StockPrice $9.00 Per Share

December 2010

Initial Public OfferingLinkedIn7,840,000 SharesCommon StockPrice $45.00 Per Share

May 2011

Initial Public OfferingBG Medicine5,000,000 SharesCommon StockPrice $7.00 Per Share

February 2011

Initial Public OfferingGEVO7,150,000 SharesCommon stockPrice $15.00 per share

February 2011

Initial Public OfferingSolazyme10,975,000 Shares Common StockPrice $18.00 Per Share

May 2011

Initial Public OfferingApollo Management29,757,559 SharesCommon StockPrice $19.00 Per Share

March 2011

Initial Public OfferingResponsys6,619,654 SharesCommon StockPrice $12.00 Per Share

April 2011

Initial Public OfferingM/A – COM TechnologySolutions Holdings6,000,000 Shares Common StockPrice $19.00 Per Share

March 2012

Initial Public OfferingYelp!7,150,000 Shares Common StockPrice $15.00 Per Share

March 2012

Initial Public OfferingInvensense10,000,000 Shares Common StockPrice $7.50 Per Share

November 2011

Initial Public OfferingDemandware5,500,000 Shares Common StockPrice $16.00 Per Share

March 2012

Technology, media, and telecom (TMT)IPOs from Q1 2007‒Q1’12

Deloitte leads in TMT IPOs

Deloitte29%

EY25%

KPMG10%

PwC24%

Other12%

Initial Public OfferingEnphase Energy8,969,697 Shares Common StockPrice $6.00 Per Share

March 2012

Initial Public OfferingRenewable Energy Group7,200,000 SharesCommon stockPrice $10.00 per share

January 2012

Initial Public OfferingSynacor6,818,170 SharesCommon stockPrice $5.00 per share

February 2012

Over the last ten years, Deloitte & Touche LLP and Deloitte Tax LLP have assisted with more than 265 IPOs in the U.S. Our team consists of professionals with extensive experience with the IPO process. Our commitment to responsive service and meeting client expectations will assist in your successful transition to a public company.

Several recent IPOs where Deloitte was the auditor include:

From January 2007 through March 2012, Deloitte assisted with more than 50 IPOs in the technology, media, and telecom industry, and 25 software company IPOs – both first among the Big Four.

Venture Capital Virtuous Cycle

Company Funded

Company Grows

Company Goes Public

Venture Capital Relationships

Deloitte Venture Capital Team

Success Story: LinkedIn

LinkedIn founded in 2003, raised about $125 M in 5 rounds

LinkedIn has annual sales of $200M and grew 100% in the past year with 90 million users

Public Offering in 2011

LinkedIn Investors Include Sequoia, Greylock and Bessemer

U.S. Investment: Overall

Source: Dow Jones VentureSource

Investment Off Pace in 2012Deal Flow and Equity into Venture-Backed Companies

$23.6$25.1

$31.1$34.4 $33.0

$24.2

$29.5

$34.7

$15.3

24602628

28573106 3031

2742

3093

3404

1595

0

1,000

2,000

3,000

$0

$10

$20

$30

$40

$50

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Amount Invested ($B) Number of Deals

Source: Dow Jones VentureSource

Momentum Picks Up in 2Q’ 12Deal Flow and Equity into Venture-Backed Companies

$6.2 $6.0

$7.5

$5.1

$8.5

$6.1

$9.8

$7.7

$8.8$9.9

$8.3

$7.2$8.1

682 669

827

683

827

726

857794

889 859 862

732

863

0

150

300

450

600

750

900

$0

$2

$4

$6

$8

$10

$12

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12

Amount Invested ($B) Number of Deals

Source: Dow Jones VentureSource

Early Stage Deal Flow Steady in 2012

Deal Flow Allocation by Round Class (Annual)

*Seed and First Rounds Combined

*36% *36%

*45% *46%

22% 24%

19% 19%

35%37%

35% 34%

8% 3%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Restart

Later

Second

First

Seed

Source: Dow Jones VentureSource

Early Stage Investment Rises in 2Q’ 12Investment Allocation by Round Class

*Seed and First Rounds Combined

*17% *17% *19% *19% *23%

20% 22% 22%17%

17%

60% 58% 55% 63% 59%

3% 1%

0%

20%

40%

60%

80%

100%

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12

Restart

Later

Second

First

Seed

Source: Dow Jones VentureSource

Median Deal Size Increases in 2Q’ 12 Median Amount Invested Per Financing Round

$5.0 $5.0 $4.7

$4.0

$4.5 $4.8

$4.1

$4.5

$5.0

$5.9

$4.2 $4.0

$5.0

$0

$2

$4

$6

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12

Source: Dow Jones VentureSource

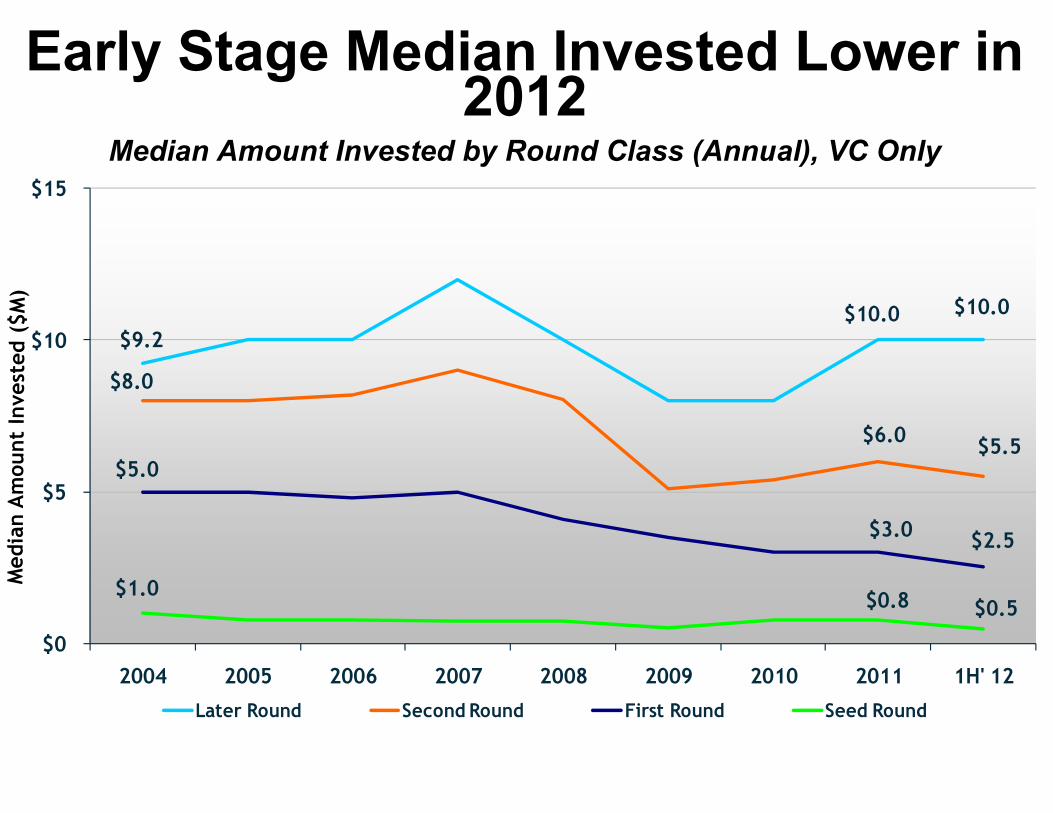

Early Stage Median Invested Lower in 2012

Median Amount Invested by Round Class (Annual), VC Only

$9.2$10.0 $10.0

$8.0

$6.0 $5.5$5.0

$3.0 $2.5

$1.0 $0.8 $0.5

$0

$5

$10

$15

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Later Round Second Round First Round Seed Round

Source: Dow Jones VentureSource

Seed Round Median Invested Higher in 2Q’ 12

Median Amount Invested by Round Class, VC Only

$8.2

$10.0 $10.1

$5.0 $5.0$5.5

$3.0 $2.8 $2.4

$0.5 $0.3 $0.8

$0

$2

$4

$6

$8

$10

$12

$14

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12

Later Round Second Round First Round Seed Round

U.S. Investment: Sources

Source: Dow Jones VentureSource

Corporate Equity Invested Falls in 2Q’ 12

Corporate Equity into Venture-Backed Companies

$492

$76 $73 $103 $30

$138

$425

$258 $254 $198 $145

$1,334

$121

14

10 1012

910

1513

17

8

16

19

10

0

5

10

15

20

25

$0

$500

$1,000

$1,500

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12Amount Invested ($M) Number of Deals

Source: Dow Jones VentureSource

VC Investment Bounces Back in 2Q’ 12

Equity Investment into Venture-Backed Companies, VC Rounds Only

$5.7 $5.8

$7.4

$4.9

$8.2

$5.9

$9.2

$7.3 $8.3

$9.6

$8.1

$5.8

$7.9 652 646

794

647

794

696

821

760

857838 826

703

839

0

150

300

450

600

750

$0

$2

$4

$6

$8

$10

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12

Amount Invested ($B) Number of Deals

Source: Dow Jones VentureSource

Most Active U.S. Investors in 2Q’ 12By Number of Equity Investments in U.S. Venture-Backed Companies

500 Startups LP 36

First Round Capital LLC 25

New Enterprise Associates 25

Kleiner Perkins Caufield & Byers 21

Google Ventures 20

Khosla Ventures 19

SV Angel 16

Accel Partners 14

Andreessen Horowitz 14

Battery Ventures 14

Greylock Partners 14

InterWest Partners 14

Source: Dow Jones VentureSource

Half of U.S. Investment Goes to California

Regional Investment Dollars in the United States 2Q’ 12

Northern California42%

Southern California12%

Mid-Atlantic13%

New England10%

Pacific Northwest5%

South Central2%

Mountain6%

South East3%

All Other US6%

Source: Dow Jones VentureSource

Early Stage Valuations Higher in 2012

Median Pre-money Valuations by Round Class (Annual)

$29.3

$57.0

$46.4

$12.1

$18.3

$30.3

$5.6 $6.0

$10.4

$1.7 $2.9 $3.3$0

$20

$40

$60

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Later Stage Second Round First Round Seed Round

U.S. Liquidity

Source: Dow Jones VentureSource

Exit Opportunities Via IPO Increase in 2012

Percentage Breakdown of Venture Backed Liquidity Events: IPO vs. M&A

0% 20% 40% 60% 80% 100%

2004

2005

2006

2007

2008

2009

2010

2011

1H' 12

IPOs M&As

Source: Dow Jones VentureSource

M&A Activity Sluggish in 2012Transactions and Amount Paid ($B) in M&As

$26.9$30.3

$39.3

$54.9

$26.0$23.8

$39.5

$51.0

$26.4

531508

536 525

443 426

536

208

0

100

200

300

400

500

$0

$20

$40

$60

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Amount Paid ($B) Number of Transactions

Source: Dow Jones VentureSource

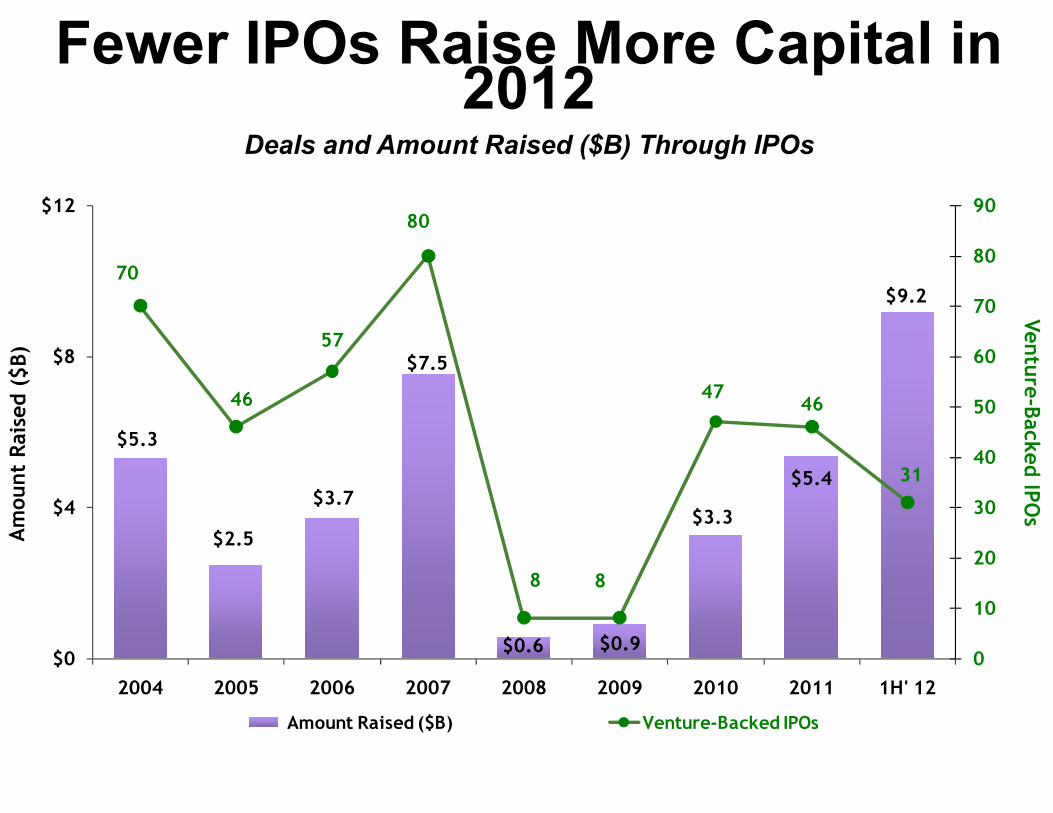

Fewer IPOs Raise More Capital in 2012

Deals and Amount Raised ($B) Through IPOs

$5.3

$2.5

$3.7

$7.5

$0.6 $0.9

$3.3

$5.4

$9.270

46

57

80

8 8

4746

31

0

10

20

30

40

50

60

70

80

90

$0

$4

$8

$12

2004 2005 2006 2007 2008 2009 2010 2011 1H' 12

Amount Raised ($B) Venture-Backed IPOs

PART IIThe Fundraising Process

Tools for Financing your Company

Presenting your Plan

Sales Process

PrepareApproach

Term Sheet

1 to 2 Months 1 to 3 Months 1 to 2 Months

Sales Process (Prepare)

Prepare

1 to 2 Months

Key Elements include:•Create Runway (or Perceived Runway)

•Get Current Investor Commitment

•Scrub The #s

•Align The Organization

•Define Your Objective

•Define Roles & Responsibilities

•Prepare Sales Tool Kit

•Identify Targets

•Create Scarcity Value

Sales Process (Approach)

Approach

1 to 3 Months

Key Elements include:•Get Referrals

•First Meeting

•Subsequent Meetings

•All-Partners Meeting

•Consultant Meetings

•Customer Meetings

•Due Diligence

•Site Visit

•Term Sheet (or Pass)

Sales Process (Term Sheet)

Term Sheet

1 to 2 Months

Key Elements include:•Negotiate

•Draw Legal Documents

•Signature

•Pre-Close Review

•Close

•Confirm $ Deposited

•Due Diligence IS Still Happening!

Financing your Companyv Be realistic on timing and pricing

v Become a great writer and spreadsheet jock

v Plan your approach using all resources

v Practice, practice, practice

v The first term sheet is often the best

Financing Tool Kitv Elevator Pitch

v Story/Demo

v Presentation

v Executive Summary/Plan

v Due Diligence

Elevator PitchDefinition

• 2-3 sentences that defines the market, customer, problem/solution and uniqueness of the business

• Place on slide one (display as brief bullets with a graphic)

Framework• What market are you in? • What urgent problem are you solving?• What is the size of the opportunity? • Why will you win (differentiation, barriers to

entry, unfair advantage)? • Where is the validation (customers, investors,

etc.)?

Elevator Pitch$35 billion is what US commercial medium-duty truck

fleets spend each year on fuel. Wrightspeed has invented an extended range electric truck powertrain that uses 1) plug-in grid power, 2) regenerative braking and 3) a multi-fuel turbine generator for range extension. The result is high a mpg equivalent, full power and low emissions which can radically transform an entire fleet of trucks.

Light and medium duty delivery trucks represents a $16 billion addressable market with companies such as UPS and FedEx. The management team has experience from top tech companies such as Tesla, Cisco and Apple. Wrightspeed represents a patented technology which competitors cannot match.

Executive SummaryPrimary Uses• Initial introduction to investors (may accompany introductory

email)• Prepares investors for meetingBest Practices• Text derived from your presentation• Drill down in key areas, but be concise• Highlight external validation• Less than 5 pages• Use as tool to sell the teamSupporting Materials• Business plan, sales pipeline, IP roadmap, competitive landscape,

etc.• Make available only as appropriate (avoid material overload)

Executive Summary Outline Definition

• 1-3 page text document which includes all the elements of a business plan

Outline• Business Definition/Company Purpose• Business/Technology Problem• Company/Product Solution• Market Trends/Size /Growth• Competitive Assessment/Point-of-Difference• Product/Technology/IP• Sales/Distribution• Team/BOD• Financials

Business Plan OutlineDefinition: 6-10 page document before appendicesOutline

• Executive Summary (1-3 pages)• Business Overview and Strategy (1 page)• Technology and Product (1-2 pages)• Market and Competition (1 page)• Management and Board (1-2 pages)• Financial Summary (1 page)

Due Diligencev Full management resumes

v Annual Financial Projections

v Product Information

vMarket Studies

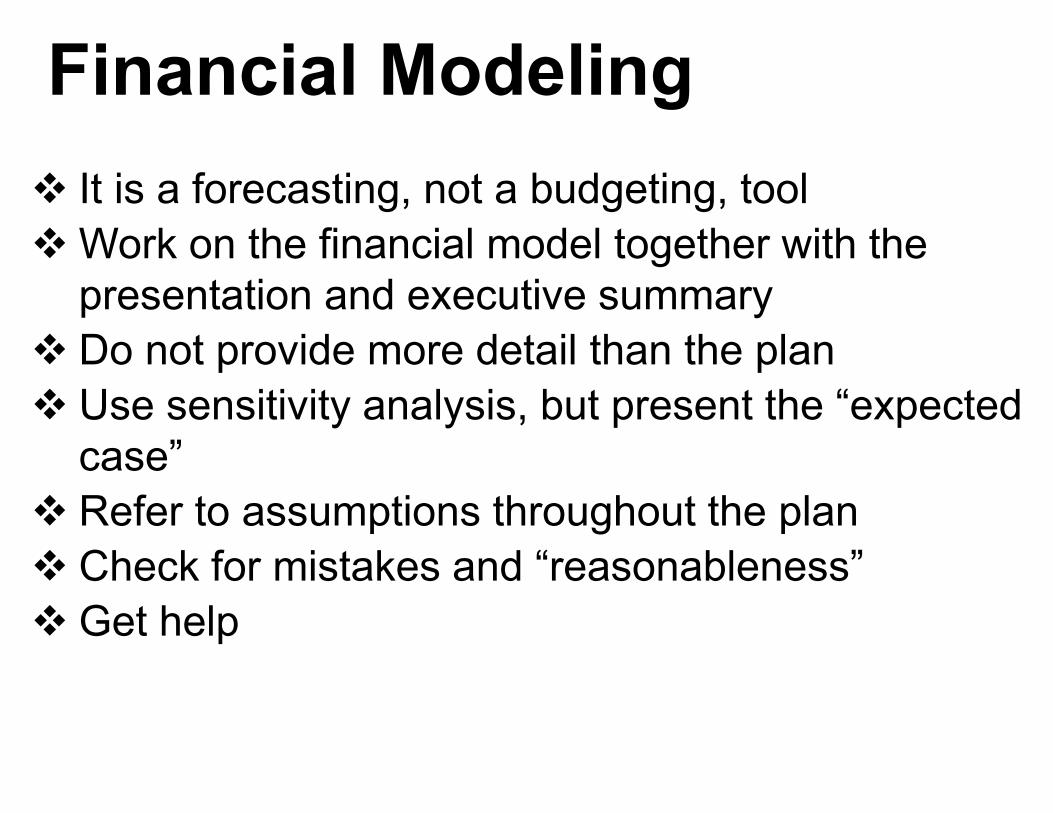

PART IIIFinancial Modeling

Summary

Financial Modelingv It is a forecasting, not a budgeting, toolvWork on the financial model together with the

presentation and executive summaryv Do not provide more detail than the planv Use sensitivity analysis, but present the “expected

case”v Refer to assumptions throughout the planv Check for mistakes and “reasonableness”vGet help

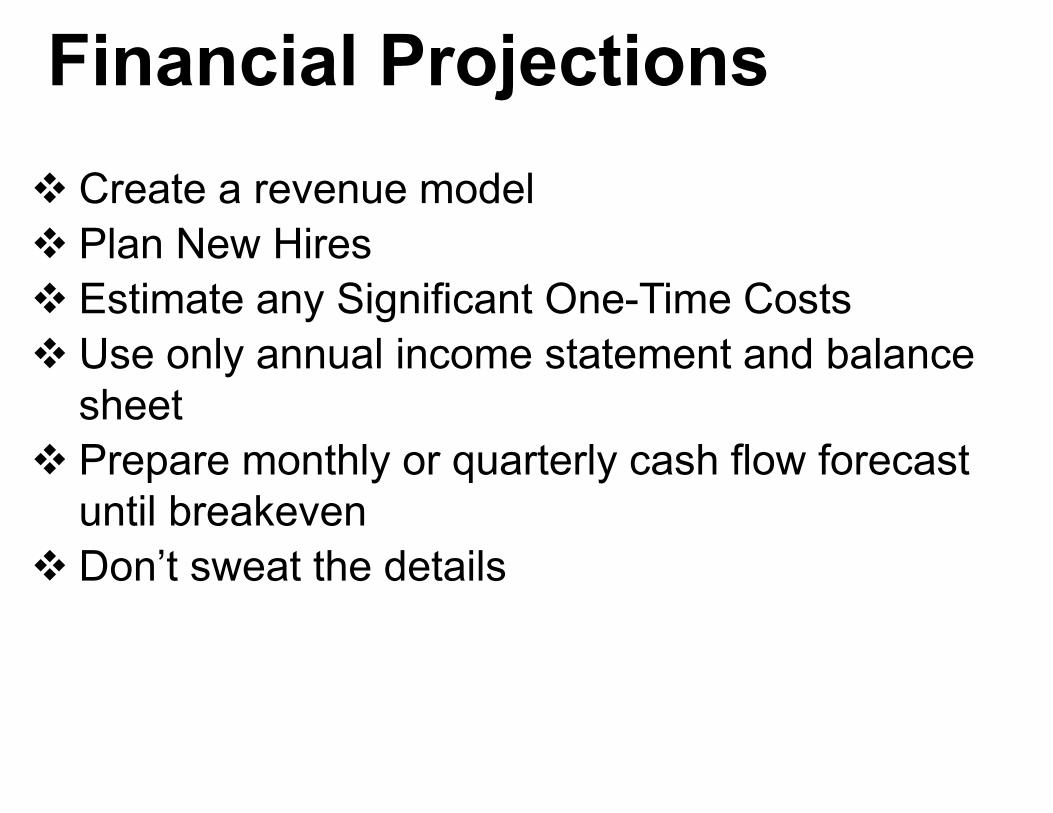

Financial Projectionsv Create a revenue modelv Plan New Hiresv Estimate any Significant One-Time Costsv Use only annual income statement and balance

sheetv Prepare monthly or quarterly cash flow forecast

until breakevenv Don’t sweat the details

Revenue Modelv Build a specific revenue model that mirrors your

industryv Compare with industry standards, highlight any

differencesv Prepare the model from the “bottoms up”v Do not over estimate first year revenuev Do make a 5 year forecastv Know the way revenue is recorded for your

industry

Headcountv 80% of all early year expenses are headcount

relatedvMake sure you are reasonable with salariesvMatch additions of people with company

milestonesv Don’t forget taxes, benefits and recruiting

expensesv Build a sales commission model, if necessaryv Index salaries to inflation and add bonuses

Other Expensesv Don’t sweat the other expensesvMake sure rent increases as neededvWatch consulting and professional servicesv Begin taxes at the appropriate time

Balance Sheetv Do create a balance sheet v Use industry standards for AR and AP

assumptions (typically 60 days and 30 days)v Include financing assumptions on your balance

sheetvMake sure it balances (the balancing item is cash)

Cash Flow Statementsv A Flow of Funds statement is typical and easiestv Use the Receipts and Disbursements statement if

you are bravev Cash flow statements are derived from the

income statement and balance sheetv Do not make changes on the cash flow statementv Show monthly or quarterly cash flows until

breakeven in the appendix or as backup slide

Charts and Tablesv In the presentation or business plan, use charts

and tables to highlight the following:Revenue (esp. as compared to competitors)Sales and distribution model

vFive year annual summary

vOther charts and graphs can show key events to next funding round, cash flow breakeven or the cash flow cycle

Summaryv Create a great demo and presentationv Use the executive summary to market your

companyvMake the financial projections work with the

assumptions in your pitchv Practice your pitch with an experienced audiencev Keep revising your plan and projections as you

growvGood luck

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Appendix A: Tools and knowledge resources - continuedDbriefs webcasts: Timely, interactive web based presentations covering a wide range of topics of interest to financial professionals. Accounting-related Dbriefs, conducted at least twice a quarter, cover each EITF meeting and recent accounting developments. Special editions of Dbriefs are produced when significant accounting events occur (e.g., when the FASB issues a major exposure draft or final standard). Attendees of accounting-series Dbriefs are eligible for continuing professional education credits. To sign up for a free Dbriefs subscription, go to https://deloitte.zettaneer.com/Subscriptions/ and select the “Audit & Enterprise Risk Services” or “Tax” areas of interest.

TMT Predictions 2012: This annual publication presents Deloitte's view of the major trends likely to have a significant medium- to long-term impact oncompanies across TMT. The goal of Predictions is to catalyze discussions around important topics that may require organizations to respond. We provide a view on what we think will happen, what will occur as a consequence, and what the implications are for various types of companies.Over the last decade, the TMT sector - and its impact on how we work, live, and are entertained - has changed markedly. One key trend over the last ten years has been convergence: the technology, media, and telecom sectors are more interconnected and interdependent than ever before.

Strategies for Going Public Third Edition: This publication provides information to assist companies through the initial public offering (IPO) process by providing practical, working knowledge of the stages for going public in the U.S. Broad in scope, it addresses both pre- and post-IPO considerations, so companies can remain well informed and prepared at every stage. Along with key information on the requirements and regulations of a successful offering, the publication also includes helpful tools, such as a timetable for going public, a sample due diligence checklist, and a discussion of the different securities exchange listing requirements.

Perspectives – for mid-market and privately held companies: Published by the Deloitte Growth Enterprise Services (DGES) group, this bi-monthly newsletter is distributed to nearly 60,000 DGES clients, recent Private Company Dbriefs attendees, and participants in our semiannual Private Perspectives interactive events. Each newsletter features articles of interest to mid-market and private company executives provided by Deloitte specialists from audit and enterprise risk, consulting, tax, and financial advisory services – Deloitte’s multidisciplinary resources.

50

Deloitte Growth Enterprise Services

Perspectives

For mid-market and privately held companies

October 2011 Perspectives is a multifaceted program that utilizes live events, signature reports, research publications, webcasts, and podcasts to deliver content focused on relevant trends and issues. This month we feature a new survey-based report, Mid-market perspectives: America's economic engine — competing in uncertain times. In an April survey, mid-market company executives told us they were cautiously optimistic about the economy. Since then, expectations have gone from modest to minimal. Nevertheless, this new report shows that most executives in this segment continue to believe that their businesses will improve in the coming year. Increased media recognition of the growing importance of mid-market companies is highlighted by CNBC's new segment, The Mighty Middle Market. The inaugural program featured an interview with Tom McGee, national managing partner, Deloitte Growth Enterprise Services, Deloitte LLP. We will share timely elements of Perspectives on a regular basis and we hope you find this content valuable. Please contact us if you would like to take a deeper dive into any specific topic.

Important noticeThis document has been prepared by Deloitte (as defined below) for the sole purpose of providing a proposal to the parties to whom it is addressed in order that they may evaluate the capabilities of Deloitte to supply the proposed services.The information contained in this document has been compiled by Deloitte and includes material which may have been obtained from information provided by various sources and discussions with management but has not been verified or audited. This document also contains confidential material proprietary to Deloitte. Except in the general context of evaluating our capabilities, no reliance may be placed for any purposes whatsoever on the contents of this document or on its completeness. No representation or warranty, express or implied, is given and no responsibility or liability is or will be accepted by or on behalf of Deloitte or by any of its partners, members, employees, agents, or any other person as to the accuracy, completeness, or correctness of the information contained in this document or any other oral information made available and any such liability is expressly disclaimed.This document and its contents are confidential and may not be reproduced, redistributed, or passed on, directly or indirectly, to any other person in whole or in part without our prior written consent.This document is not an offer and is not intended to be contractually binding. Should this proposal be acceptable to you, and following the conclusion of our internal acceptance procedures, we would be pleased to discuss terms and conditions with you prior to our appointment.Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.