preparing the workforce for the automotive technology of 2025 occ/dma/win fall conference november...

TRANSCRIPT

Preparing the Workforce for the Automotive Technology of 2025

OCC/DMA/WINFall Conference

November 8, 2013

Bernard SwieckiCenter for Automotive Research (CAR)

Industry Collaboration & Partnerships

CAR collaborative working groups:

• Automotive Communities Partnership (ACP)• Connected Vehicle Working Group• United Tooling Coalition (UTC)• Program for Automotive Labor and Education (PALE)• Electric Vehicle Working Group• Advanced Automotive Information Technology Solutions Consortia• Coalition for Automotive Light-weighting Materials (CALM)

The Center for Automotive Researchbrings together stakeholders for thought

leadership and industry education.

CAR’s flagship event, August 5-8Now in its 48th year – a “can’t miss” event

More than 900 attendeesSessions on manufacturing, materials, connected vehicles, policy,

sales forecasting, purchasing, strategy, & capital investmentMore information at www.cargroup.org

Name a product … ?

• Which consists of nearly 30,000 parts,• Can be assembled at the rate of 1 per minute,• 16 hours a day, 200 days a year,• Runs for several years, most of the time without

a single manufacturing defect?• Is from the largest manufacturing sector in the

U.S. economy.

This accomplishment by the auto industry to execute mass production has become the norm.

U.S. Light Vehicle SalesPercent Change YTD Through October:

2013 vs. 2012

Passenger Cars

Light Trucks

Total

5.0%

11.8%

8.2%

Source: Automotive News; CAR Research

+ 986,53912,979,521

100.0%

+ 676,0186,419,453

49.5%

+ 310,5216,560,068

50.5%

Nissan

Hyundai-Kia

Honda

Fiat-Chrysler

Toyota

Ford

GM

Units: 1,032,134

Units: 1,057,910

Units: 1,273,550

Units: 1,497,086

Units: 1,867,155

Units: 2,078,939

Units: 2,343,861

8.0%

8.2%

9.8%

11.5%

14.4%

16.0%

18.1%

U.S. Market Share:YTD October 2013

Source: Automotive News; CAR Research

U.S. Light Vehicle Monthly Sales and SAAROctober 2011 – October 2013

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

1,400,000.0

1,600,000.0

1,800,000.0

0

2

4

6

8

10

12

14

16

1,021,185.0994,786.0

1,243,784.0

913,284.0

1,149,432.0

1,404,623.0

1,184,567.0

1,334,642.01,285,499.0

1,153,759.0

1,285,292.01,188,899.0

1,092,294.01,141,692.0

1,356,070.0

1,043,192.0

1,192,299.0

1,453,038.0

1,285,446.0

1,443,311.01,403,121.01,313,844.0

1,501,294.0

1,137,206.01,206,182.0

13.313.6 13.614.2

15.114.414.4

13.814.1 14.114.5

14.914.3

15.6 15.415.215.3 15.315.2

15.515.9

15.816.1

15.3 15.2

SALES SAAR

Mon

thly

SA

AR

Source: Automotive News; CAR Research

Big 7 Monthly U.S. Market Share1999 – 2013 YTD (October)

0%

5%

10%

15%

20%

25%

30%

35%

24.7%

16.0%

29.4%

18.0%

15.6%

11.5%

6.4%

9.8%

1.8%

8.2%

4.0%

8.0%8.7%

14.4%

Ford GM Chrysler Honda Hyundai-Kia Nissan Toyota

Year

Perc

ent o

f U.S

. Mar

ket S

ales

Source: Automotive News; CAR Research

Motor Vehicle & Parts Manufacturing Employment1999 – July 2013

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 July 2013

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

316,300

148,500

105,100

70,200

153,500

81,500

1,130,900

681,500

Michigan Indiana Ohio U.S.

Stat

e Le

vel

U.S.

50% change

64% change

53% change

47% change

Source: BLS, U.S. DOL

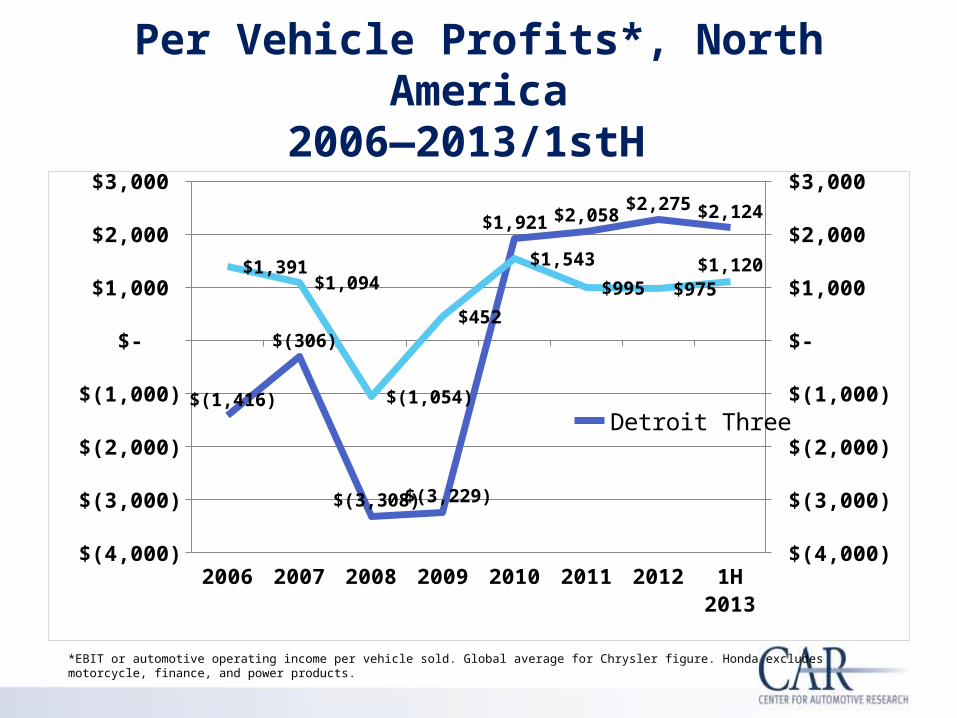

Per Vehicle Profits*, North America2006—2013/1stH

2006 2007 2008 2009 2010 2011 2012 1H 2013 $(4,000)

$(3,000)

$(2,000)

$(1,000)

$-

$1,000

$2,000

$3,000

$(4,000)

$(3,000)

$(2,000)

$(1,000)

$-

$1,000

$2,000

$3,000

$(1,416)

$(306)

$(3,308) $(3,229)

$1,921 $2,058 $2,275 $2,124

$1,391 $1,094

$(1,054)

$452

$1,543

$995 $975 $1,120

Detroit ThreeToyota and Honda

*EBIT or automotive operating income per vehicle sold. Global average for Chrysler figure. Honda excludesmotorcycle, finance, and power products.

Quarterly GDP Growth Rate07/1Q – 13/2Q

1Q 2007

3Q 2007

1Q 2008

3Q 2008

1Q 2009

3Q 2009

1Q 2010

3Q 2010

1Q 2011

3Q 2011

1Q 2012

3Q 2012

1Q 2013-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

0.3

3.1 2.71.5

-2.7

2.0

-2.0

-8.3

-5.4

-0.4

1.3

3.9

1.6

3.92.8 2.8

-1.3

3.2

1.4

4.93.7

1.2

2.8

0.11.1

2.5

Source: Bureau of Economic Analysis; Federal Open Market Committee

Auto Sales and Economic Growth are DisconnectedU.S. GDP Growth Rate and Vehicle Sales Growth Rate

1952 – Q2 2013

52535455565758596061626364656667686970717273747576777879808182838485868788899091929394959697989900010203040506070809101112

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

-30

-20

-10

0

10

20

30

40Sales Growth GDP Growth

GD

P G

row

th R

ate

Vehi

cle

Sale

s G

row

th R

ate

Source: Bureau of Economic Analysis

They are Getting Old . . .U.S. Light Vehicle Age and

Scrappage Rate

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

8.6 8.8 8.8 8.9 8.9 9.0 9.1 9.4 9.5 9.7 9.8 10.0 10.3 10.6 10.9 11.2 11.4

6.78

5.88 5.76

6.746.40 6.19

5.504.76

4.355.03 5.24

5.66

4.12

5.21 4.90

Average Age Scrappage Rate (%)

Source: R.L. Polk

Unemployment RateJanuary 2008 – July 2013

Jan-08

Apr-08Jul-0

8

Oct-08

Jan-09

Apr-09Jul-0

9

Oct-09

Jan-10

Apr-10Jul-1

0

Oct-10

Jan-11

Apr-11Jul-1

1

Oct-11

Jan-12

Apr-12Jul-1

2

Oct-12

Jan-13

Apr-13Jul-1

34%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

7.1%

14.2%

10.6%

8.7%

4.7%

10.8%

8.4%

5.7%

10.6%

8.8%

7.2%

5.0%

10.0%

7.4%

Michigan Indiana Ohio U.S.

Source: Bureau of Labor Statistics

U.S. Light VehicleCAR Sales Forecast: 2007-2016

2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

2

4

6

8

10

12

14

16

1816.1

13.2

10.411.6

12.8

14.515.7 16.0 16.2 16.2

Source: CAR Research, Oct. 2012

10.4%

11.6%

13.3%

8.3%

U.S. Vehicle Production & Automotive Employment Forecasts

2013-2016

2011 2012 2013 2014 2015 2016 2011 2012 2013 2014 2015 2016

Vehicle Production

8669700 10375257 11000000 11300000 11500000 11400000

Automotive Employment

603400 647500 670000 688000 700000 695000

1,000,000

3,000,000

5,000,000

7,000,000

9,000,000

11,000,000

13,000,000

550,000

650,000

750,000

Pro

du

cti

on

Em

plo

ym

en

tSource: Automotive News; CAR Research; BLS, July 2013

Employment not growing much:• Third party workers• More imported parts

and components• More overtime and

temporary workers• High productivity rate

Manufacturing Efficiency

Taiichi Ohno: Toyota Production System

Global Supply Chains

Flexible Manufacturing & Industrial Robotics

Global Platforms

Digital Engineering & Manufacturing

20122014

20162018

20202022

2024150

170

190

210

230

250

270

290

310

EPA

Estim

ate

gCO

2/M

ile S

tand

ard

Fuel Economy Regulation Projections

20122014

20162018

20202022

202420

25

30

35

40

45

50

55

60

Equi

vale

nt F

uel E

cono

my

Stan

dard

(MPG

)

Source: EPA and NHTSA

Grams CO2/mile

CAFE mpg 54.5

Fuel Economy & Safety

The most likely dramatic changes for the automotive market through 2025 could

well be a result of mandates by the federal government to improve the fuel economy

performance and vehicle safety

North American Automotive Manufacturing and R&D Clusters, 2011

© Center for Automotive Research, April 2013

Auto:Over 1M U.S. jobs (incl. spinoff)

Over $12B/year private R&D in Michigan

New technologies … what’s coming next ?

Automotive Innovation

• Powertrain

• Materials(Lightweighting and Crashworthiness)

• Electronics• Safety• Road use• Convenience

• Many supportive ones

Power Split

Hybrid

2-Mode H

ybrid

Conversi

on to Diese

l

Integrat

ed St

arter

Generat

or (Belt

/Cran

k)

12V Micr

o-Hybrid

Conversi

on to Adva

nced Dies

el *

Dual Clutch

Tran

smiss

ion

Mate

rial S

ubstitu

tion - 10%

Cylinder D

eacti

vation, O

HV

Turb

ocharg

ing and Downsiz

ing

6/7/8

-Spee

d Auto. T

rans.

with Im

prove

d Inter

nals

Continuously Vari

able Tr

ansm

ission

Cylinder D

eacti

vation, S

OHC *

Discrete

Variable

Valve Lift

SOHC *

Discrete

Variable

Valve Lift

DOHC *

Continuously Vari

able Valv

e Lift *

Discrete

Variable

Valve Lift

OHV *

VVT - Dual C

am Phasin

g *

Impro

ved Auto

. Tran

s. Contro

ls/Ex

ternals

Electr

ic Power

Steeri

ng

Impro

ved Acce

ssorie

s

Low Rollin

g Res

istan

ce Ti

res

Aero Drag

Reducti

on 10%

Stoich

iometric G

asolin

e Dire

ct Injecti

on *

VVT- Coupled

Cam Phas

ing SOHC

VVT - In

take

Cam Phasing

VVT - Coupled

Cam Phas

ing OHV

Engin

e Fric

tion Reduction

Low Fr

iction Lu

bricants

Higher V

oltage

/Impro

ved Alte

rnato

r 0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Assessment of Technologies for Improv-ing Light-Duty Vehicle Fuel Economy –

Over 40 Technologies

Perc

ent F

uel C

onsu

mpti

on R

educ

tion

* Preceding Technology Required Source: NAS 2011

High Impact - Strategic

Incremental – Low Risk

22

Average Material Content ofNorth American Light Vehicles

1995 2000 2005 20100.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Regular (Mild) Steel

High Strength Steel

Plastics & Composites

Aluminum

Iron Castings

Image: Porsche

Data source: Wards

Average Material Content ofNorth American Light Vehicles

1995 2000 2005 20100.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Regular (Mild) Steel

High Strength Steel

Plastics & Composites

Aluminum

Iron Castings

Image: Porsche

Data source: Wards

Joining Complexity Increasing

JoiningLaser Welding

Fasteners

Adhesives

Resistance Spot Welding

• New body shop for aluminum frame• Carbon fiber hood and roof and interior• Carbon-nano composite underbody panels• Magnesium frame seat• SMC fenders, doors and rear

quarter panels & hatch– Extrusions, castings and sheet

(castings 2mm – 11mm)– Hydro formed tubes

• Magnesium structural chassis components

• Joining: adhesive, laser welding, fasteners, spot welding

2014 Corvette Stingray: A Future Direction for Materials

Photo Source: General Motors

Key Material Trends (Next 10 years)

• Increased use of ultra high strength steel for structural components around the “safety cage” to prevent intrusion

• Aluminum use for chassis and exterior panels is increasing

• Fiber reinforced plastics (glass and carbon) for structural components are still several years away from high volume production

• Joining complexity: more laser welding, fasteners and adhesives

Structural Adhesive

Driver Attention & Connected Vehicles

Top 3 features consumers want:

1. Wireless Communications(bundle of many features)

2. Navigation

3. Automatic Crash Notification

connectivity is increasing

glance sequences

Connected Vehicles Defined• Connected vehicles use any of a number of different

wireless communication technologies to communicate with:– Each other– Roadside infrastructure– The “Cloud”

• Goals for connected vehicles are to enhance– Vehicle and roadway safety– Mobility– Environment (e.g., reduced fuel consumption)

Implications for Investment of Convergence and Self-Driving Vehicles

Crash elimination: Crash-free driving and improved vehicle safety could change the concept of a vehicle as we know it

Travel time dependability: Convergence can substantially reduce uncertainty in travel times via real-time, predictive assessment of travel times on all routes

Productivity improvements: Convergence will allow travelers to make use of travel time productively

Reduced need for new infrastructure: Self-driving can reduce the need for building new infrastructure and reduce maintenance costs

Improved energy efficiency: Reduced energy consumption in at least three ways: more efficient driving; lighter, more fuel-efficient vehicles; and efficient infrastructure

New models for vehicle ownership: Self-driving vehicles could lead to a major redefinition of vehicle ownership and expand opportunities for vehicle sharing

New business models and scenarios: Convergence of technologies may realign industries such that ecosystem participants need to compete and collaborate at the same time

Data challenges: Issues related to data security, privacy, and data analytics and aggregation could crop up due to abundance of data in vehicles

Industry Challenge Severe shortage of technical skills

Chicken-and-egg challenge with many technologies electrification/alternative fuels Materials supply chain Connectivity – retrofitting, infrastructure/automobile

Predictive modeling: CAE Powertrain control systems Materials forming and crash performance

Structures Fabrication (molding, hot forming, stamping AHSS/aluminum,

…) Joining (RSW, laser, adhesives, fasteners)

Greater industry collaboration Standards (material, testing, …)

Center for Automotive Research

Thank You