preparing for the next mining bull market… and... · preparing for the next mining bull market...

TRANSCRIPT

Mines and Money Nov. 2016

Preparing for the next mining bull market…but have we learnt the lessons of the last one?

The Mining Sector Cycle…The mining industry is cyclical over time

Market shift between growth & survival rather than profiting and investing

Bull Market = Growth Focus

Bear Market = Survival Focus

Cost-cutting employees, exploration budgets, G&A, dividends cut Asset portfolio review impairments/write-downs, development projects shelved, non-core/lower quality assets put up for sale

Production growth is the focus, mostly via acquisitions Little or no capital return to shareholders

Financing is very expensive and very selective High quality names first in queue upon turnaround

Financing is abundant with low discount pricing Market funds growth“Loose” money for higher risk opportunities

3 years 6 years 6 years1.5

years 2.5 years 4 years0.5+ years

XAU Index

1993 2016

Source: Scotiabank - CapitalIQ

Commodity Prices…the past 20 years

0

200

400

600

800

1000

1200

1400

1600

Gold Copper Brent Crude Iron Ore 62% Fe CFR

Commodity Prices Indexed to 100 (1996 to Present)

Source: Scotiabank GBM: Market data as of November 21, 2016

Chinese led supercycle a lifetime event?

Sector Value…reckless allocation of capital results in a toxic debt pile

Source: Scotiabank - CapitalIQNote: Excludes steel producers (e.g. Nippon, POSCO, ArcelorMittal, etc.)(1) “Other” includes PGMs, uranium, lithium, coal, iron ore, diamonds and royalty companiesC

0

500

1000

1500

2000

2500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gold / Silver Diversifieds / Base Metals Other

--$100$200$300$400

2000 2002 2004 2006 2008 2010 2012 2014 Current

Market Capitalisation of mining sector

Net Debt of mining sector

$2.1T

$235B$815B

$2.4T

$690B

$935B

US$B

US$B

Financial Health…gold producers debt still high with poor debt to EBITDA ratios

Source: Scotiabank - CapIQ and company filings

US$m

0

1000

2000

3000

Barri

ckZi

jinG

oldc

orp

New

mon

tN

ewcr

est

Angl

oGol

dYa

man

aG

old

Fiel

dsKi

nros

sSi

lver

…N

ew G

old

Roy

al G

old

Agni

co…

Buen

ave…

Hec

laC

ente

rraB2

Gol

dD

etou

rH

ochs

child

Oce

anaG

…C

oeur

Prim

ero

Fres

nillo

Alam

osSi

lver

…Ta

hoe

Firs

t…Ki

rkla

nd…

Klon

dex

Pan…

Fran

co-…

SEM

AFO

Alac

erO

sisk

oIA

MG

OLD

Ran

dgol

dC

enta

min

Eldo

rado

net debt net cash~$2.9B total ~$30B total

~$18B held by top 5

0,00x1,00x2,00x3,00x

Zijin

Prim

ero

Yam

ana

New

Gol

dSi

lver

…G

oldc

orp

Roy

al G

old

Buen

ave…

Gol

d…Ba

rrick

Hec

laN

ewcr

est

Angl

oGol

dKi

nros

sD

etou

rB2

Gol

dC

ente

rraC

oeur

Hoc

hsch

ildO

cean

a…N

ewm

ont

Agni

co…

Alam

osFr

esni

lloTa

hoe

Klon

dex

Firs

t…Fr

anco

-…C

enta

min

Pan…

Ran

dgol

dIA

MG

OLD

Eldo

rado

SEM

AFO

Alac

erO

sisk

oSi

lver

…Ki

rkla

nd…

Net Debt & Net Cash Positions US$M

Net Debt to 2016E EBITDA Ratio

net cash

A substantial percentage of the gold investments made in the supercycle has been written off…

Source: BMO Equity Research

01,3 1,9 2,2 2,3 2,7

7,19,5

11,2 11,6

27,4

0

5

10

15

20

25

30Impairments US$ billion – 2009 to 2015

Base Metal Producers…debt and debt to EBITDA ratios higher than gold miners

Net Debt & Net Cash Positions US$M

Source: Scotiabank - CapIQ and company filings

$15,1$12,9 $12,5

$9,7 $9,4 $8,2$6,0 $5,3 $4,2 $2,7 $1,7 $1,1 $1,0 $0,4 $0,4 $0,8

Vale

BHP

Billit

on

Gle

ncor

e

Angl

oAm

eric

an

Free

port

MM

G L

imite

d

Rio

Tin

to

Veda

nta

Teck

Res

ourc

es

Sout

hern

Cop

per

Firs

tQ

uant

um

Turq

uois

e H

ill

KGH

M

Hud

Bay

Min

eral

s

Anto

faga

sta

Sout

h 32

OZ

Min

eral

s

Lund

inM

inin

g

net debt net cash$24.2 $24.2

~$1.6B total ~$138.2B total~$88.9B held by top 5

13,2x

7,9x4,4x 2,9x 2,6x 2,5x 2,5x 2,5x 2,4x 2,4x 1,8x 1,6x 1,6x 0,8x 0,8x 0,0x 0,0x 0,0x

MM

G L

imite

d

Turq

uois

e H

ill

Firs

t Qua

ntum

Veda

nta

Free

port

Hud

Bay

Min

eral

s

Sout

hern

Cop

per

Vale

Teck

Res

ourc

es

Angl

o Am

eric

an

KGH

M

BHP

Billit

on

Gle

ncor

e

Anto

faga

sta

Rio

Tin

to

Sout

h 32

OZ

Min

eral

s

Lund

in M

inin

g

net cashNet Debt to 2016E EBITDA Ratio

Senior Global Diversified and Base Metals impairment charges…

$1,2 $2,9 $3,2 $4,0$6,7

$15,8$18,0 $18,8 $20,3

$39,5

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45Impairments US$ billion – 2009 to 2015

Source: BMO Equity Research

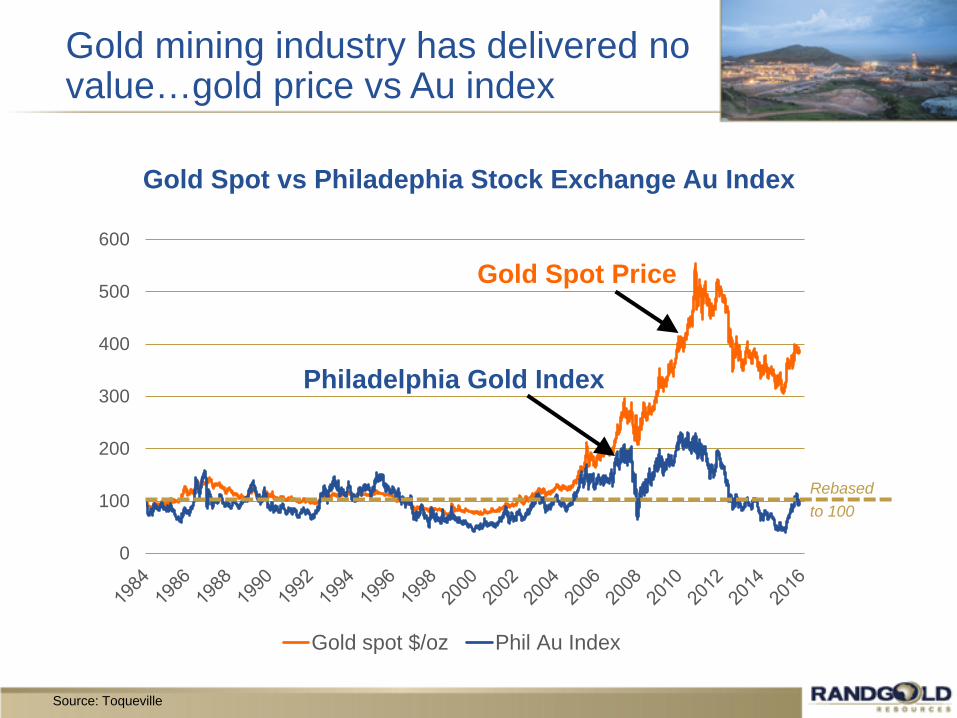

Gold mining industry has delivered no value…gold price vs Au index

0

100

200

300

400

500

600

Gold spot $/oz Phil Au Index

Rebased to 100

Gold Spot Price

Philadelphia Gold Index

Gold Spot vs Philadephia Stock Exchange Au Index

Source: Toqueville

Base Metals and Diversified…no value creation

1647,4

115,4

246,7168,1

240,8

694,3

--

500

1000

1500

2000

2500

3000

23-Nov-96 23-Nov-00 23-Nov-04 23-Nov-08 23-Nov-12 23-Nov-16

Base Metal Producer Index - Total ReturnBase Metal Producer Index - Price ReturnLME AluminiumLME CopperLME NickelLME Zinc

Base metals sector – Relative performance last 20 yearsValues indexed to 100 at 23 Nov 1996

Note: Shown in USD; Total Return Index includes reinvested dividends; LME Lead prices not available throughout entirety of period shown. 1. Base Metal Producer Index includes: Antofagasta, Boliden, First Quantum, Freeport-McMoRan, HudBay, KAZ Minerals, KGHM, Lundin Mining, Norilsk Nickel, Southern Copper. 2. Companies listed after beginning of period shown are included in index calculation following listing date.

Source: BMO Capital Markets

Exploration is not replacing the gold produced…

0

1000

2000

3000

4000

5000

6000

7000

0

20

40

60

80

100

120

140

160

180

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Gold discoveries Moz Gold production MozExploration budgets $m Gold price $/oz

Major gold discoveries Moz US$ million US$/oz

Source: SNL Metals & Mining

Why no growth in gold production? …decline in ore grade

Reserve gradevs

mining head grade

Reserve design price

vsgold price

Source: Scotiabank

0200400600800

10001200140016001800

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Reserve Price Gold Price

US$/oz

0,51,01,52,02,53,03,5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Reserve Grade Head GradeGrade g/t

Gold Supply…

Source: BMO Capital Markets

0

500

1000

1500

2000

2500

3000

3500

2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Rest of World China Australia USA Russia South Africa Peru Canada Mexico

Gold tonnes 1/3 decline in new gold supply

Base Metals and Bulk Commodities… reserve outlook better than gold

0

20000

40000

60000

80000

100000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mt

World iron ore mine reserves

0

200

400

600

800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mt

World copper mine reserves

Source: BMO Capital Markets

Top Ten Risks facing mining industry ignores requirement to replace ore reserve depletion…

2015 - 2016 2016 - 20172008

Resource nationalism has now dropped out of the top tenCash / capital access now the biggest issue for the industrySocial license to operate has remained consistently highExploration and replacement of depleted reserves with quality does not feature

EY Annual Survey

Growth is not the same as Profit…M&A is not synonymous with Creating Value

Valu

e

Timeexplorationdiscovery

production

development

Brownfields exploration -further discovery

Feasibility

Delivery of value

Feasibilities are about proper testwork and correct and realistic assumptions:

Geology Mine plans Metallurgy Reserves Trade-offsFinancial modelling Baseline and impact studiesSocio-economic

Environmental Investment terms and agreements

Adding value with M&A only starts here!!!!!

Start with a profitable businessManage your long term capital allocation against a realistic price forecastInvest in replacing reservesCapitalise on the peaks and invest in the troughsInvesting in people skills

How can the mining industry ensure it does better in the next bull market than the last?...

0200400600800

1000120014001600

Gold Copper Brent Crude Iron Ore 62% Fe CFR

Commodity Prices Indexed to 100 (1996 to Present)

Source: Scotiabank GBM: Market data as of November 21, 2016

Disclaimer…

Randgold reports its mineral resources and mineral reserves in accordance with the JORC 2012 code. As suchnumbers are reported to the second significant digit. They are equivalent to National Instrument 43-101. Mineralresources are reported at a cut-off grade based on a gold price of US$1 500/oz.The reporting of mineral reserves is also in accordance with Industry Guide 7. Pit optimisations are carried out at agold price of US$1 000/oz, except for Morila which is reported at US$1 300/oz. Mineral reserves are reported at acut-off grade based on US$1 000/oz gold price within the pit designs. Underground reserves are also based on agold price of US$1 000/oz. Dilution and ore loss are incorporated into the calculation of reserves.

Cautionary note to US investors: The United States Securities and Exchange Commission (the SEC) permitsmining companies, in their filings with the SEC, to disclose only proven and probable ore reserves. Randgold usescertain terms in this annual report such as ‘resources’, that the SEC does not recognise and strictly prohibits thecompany from including in its filings with the SEC. Investors are cautioned not to assume that all or any parts ofthe company’s resources will ever be converted into reserves which qualify as ‘proven and probable reserves’ forthe purposes of the SEC’s Industry Guide number 7.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: Except for the historical informationcontained herein, the matters discussed in this presentation are forward-looking statements within the meaning ofSection 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of 1934, andapplicable Canadian securities legislation. Forward-looking statements include, but are not limited to, statementswith respect to the future price of gold, the estimation of mineral reserves and resources, the realisation of mineralreserve estimates, the timing and amount of estimated future production, costs of production, reservedetermination and reserve conversion rates. Generally, these forward-looking statements can be identified by theuse of forward-looking terminology such as ‘will’, ‘plans’, ‘expects’ or ‘does not expect’, ‘is expected’, ‘budget’,‘scheduled’, ‘estimates’, ‘forecasts’, ‘intends’, ‘anticipates’ or ‘does not anticipate’, or ‘believes’, or variations ofsuch words and phrases or state that certain actions, events or results ‘may’, ‘could’, ‘would’, ‘might’ or ‘will betaken’, ‘occur’ or ‘be achieved’. Assumptions upon which such forward-looking statements are based are in turnbased on factors and events that are not within the control of Randgold Resources Limited (‘Randgold’) and thereis no assurance they will prove to be correct. Forward-looking statements are subject to known and unknownrisks, uncertainties and other factors that may cause the actual results, level of activity, performance orachievements of Randgold to be materially different from those expressed or implied by such forward-lookingstatements, including but not limited to: risks related to mining operations, including political risks and instabilityand risks related to international operations, actual results of current exploration activities, conclusions ofeconomic evaluations, changes in project parameters as plans continue to be refined, as well as those factorsdiscussed in Randgold’s filings with the US Securities and Exchange Commission (the ‘SEC’). Although Randgoldhas attempted to identify important factors that could cause actual results to differ materially from those containedin forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated orintended. There can be no assurance that such statements will prove to be accurate, as actual results and futureevents could differ materially from those anticipated in such statements. Accordingly, readers should not placeundue reliance on forward-looking statements. Randgold does not undertake to update any forward-lookingstatements herein, except in accordance with applicable securities laws.