prepared for cfa society of louisville april 22, 2010

Post on 21-Dec-2015

214 views

TRANSCRIPT

Prepared for

CFA Society of LouisvilleApril 22, 2010

Mary Ellen Stanek, CFA

Chief Investment OfficerBaird Advisors

Just Over a Year Ago…..

3Source: Steve Benson - The Arizona Republic

4Source: Mike Luckovich – The Atlanta Journal-Constitution

Baird Advisors Market OutlookUS Economy: Moderate Recovery with “Significant Restraints”

No “V-shaped” recovery that historically follows a severe recession

Too many “restraints” for US consumer (high unemployment, tight credit, impaired net worth)

Strong profits driving business spending-led recovery

Export-led demand driving US manufacturing output

Additional economic “headwinds” include increased regulation, higher taxes, huge Federal deficits, state/local spending cuts, rising foreclosures

Conditions still remain fragile, susceptible to “shocks” in confidence (i.e. sovereign debt)

Inflation: Modestly Higher Starting in 2011

Core Inflation, at 1-1.5%, still trending lower

Moderate economic growth and high unemployment will give Fed time to reverse policy

Housing Markets: Prices Stabilizing though Foreclosures still Rising

National Home Prices are now flat on a year-over-year basis

Current monthly data shows home prices have risen modestly for eight consecutive months

Rising foreclosures still a concern

Financial markets: Stock and Bond Prices Discounting a Sustainable Economic Recovery

Valuations generally fair with some attractive opportunities

“Easy money” has been made

5

Too Much Debt Created a Credit Bubble

Source: Bloomberg

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

$0

$5

$10

$15

$20

$25

$30Total Private Sector Debt versus Nominal GDP

Private Sector Debt (Household+Business)

Nominal GDP

Tri

llio

ns (

$)

6

The “Shadow Banking System” of Securitization

Source: Bianco Research

1952

1953

1954

1955

1957

1958

1959

1960

1962

1963

1964

1965

1967

1968

1969

1970

1972

1973

1974

1975

1977

1978

1979

1980

1982

1983

1984

1985

1987

1988

1989

1990

1992

1993

1994

1995

1997

1998

1999

2000

2002

2003

2004

2005

2007

2008

2009

2010

2012

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

12/31/09$6.76

12/31/09$9.03

The Growth of Securitization vs. Traditional Bank Lending

Time Period

Tri

llio

ns (

$)

Total Securitization(Agency & GSE-Backed Mortgage Pools And

ABS)

Total Banks Loans And Advances(Including Consumer Loans)

7

The Paradox of Deleveraging

If leveraged market participants all deleveraged at once by selling assets:

A negative feedback

loop results

A negative feedback

loop results

8

$0.0 $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0

Total U.S. Policy Response

Federal Reserve

U.S. Treasury

FDI C & FHA

Trillions ($)

Poli

cy R

esponse

Already Spent

Maximum Commitment

Spent, Lent or Guaranteed:Massive U.S. Policy Response

Note: Data as of 12/31/09Sources: Bloomberg, WSJ, Bianco Research

Total 2009 U.S. GDP = $14.5 Trillion

9

Today’s Massive U.S. Policy Response in Historical Context

World War IIOriginal Cost: $288 BillionToday’s Cost: $3.6 Trillion

Source: United States National Archives and Records Administration 10

Today’s Massive U.S. Policy Response in Historical Context

Notes: Fiscal = The Federal Budget Deficit as a % of GDP Monetary = Cumulative Change in the Fed’s Balance SheetSource: Bianco Research

What U.S. Government Did – And Didn’t DoLast 13 Recessions

Length GDP Stimulus as a % of GDP

Peak Trough (Months) Change Monetary Fiscal Combined

Aug-’29 Mar-’33 44 -27.0% 3.4% 4.9% 8.3%

May-’37 Jun-’38 13 -3.4% 0.0% 2.2% 2.2%

Nov-’48 Oct-’49 11 -1.7% -2.2% 5.5% 3.3%

Jul-’53 May-’54 10 -2.7% 0.0% -1.4% -1.4%

Aug-’57 Apr-’58 8 -3.2% 0.0% 3.2% 3.2%

Apr-’60 Feb-’61 10 -1.0% 0.7% 1.0% 1.7%

Dec-’69 Nov-’70 11 -0.2% 0.3% 2.4% 2.7%

Nov-’73 Mar-’75 16 -3.1% 0.9% 3.1% 4.0%

Jan-’80 Jul-’80 6 -2.2% 0.4% 1.1% 1.5%

Jul-’81 Nov-’82 16 -2.6% 0.3% 3.5% 3.8%

Jul-’90 Mar-’91 8 -1.3% 1.0% 1.8% 2.8%

Mar-’01 Nov-’01 8 -0.2% 1.3% 5.9% 7.2%

Dec-’07 ??? 28 -3.8% 18.0% 11.9% 29.9%

11

Short Term Economic Stimulus "Sugar High”

Cash for Clunkers Program Just EndedFirst-time Home Buyers Credit Ending 12/1

Depleted Inventories Being RebuiltSource: Dave Granlund, RE/MAX, and Petar Jankov 12

Bailout “Traffic Jam”

Source: Steve Sack – Minneapolis Star Tribune 13

Financial System Back from the Brink

Source: Bloomberg

Dec-0

7Ja

n-0

8Ja

n-0

8Fe

b-0

8Fe

b-0

8M

ar-0

8M

ar-0

8A

pr-0

8A

pr-0

8M

ay-0

8M

ay-0

8Ju

n-0

8Ju

n-0

8Ju

l-08

Jul-0

8A

ug-0

8A

ug-0

8Sep-0

8Sep-0

8O

ct-08

Oct-0

8N

ov-0

8N

ov-0

8D

ec-0

8D

ec-0

8Ja

n-0

9Ja

n-0

9Fe

b-0

9Fe

b-0

9M

ar-0

9M

ar-0

9A

pr-0

9A

pr-0

9M

ay-0

9M

ay-0

9Ju

n-0

9Ju

n-0

9Ju

l-09

Jul-0

9A

ug-0

9A

ug-0

9Sep-0

9Sep-0

9O

ct-09

Oct-0

9N

ov-0

9N

ov-0

9D

ec-0

9D

ec-0

9Ja

n-1

0Ja

n-1

0Fe

b-1

0Fe

b-1

0M

ar-1

0M

ar-1

0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%TED Spread

Time Period

Yie

ld S

pre

ad

10/10/08 4.63%

3/31/10 0.14%

14

Overall Leverage “Shift” from Private to Public

Source: Federal ReserveData as of: 12/31/09

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0%

20%

40%

60%

80%

100%

120%

Business (Finance) Household Government

Time Period

U.S

. D

ebt

as a

Perc

enta

ge o

f G

DP

U.S. Debt as a Percentage of GDP

15

Trillion Dollar Deficits as Far as the Eye can See?

Source: Bianco Research

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

-$1,650

-$1,500

-$1,350

-$1,200

-$1,050

-$900

-$750

-$600

-$450

-$300

-$150

$0

$150

$300

-$1,650

-$1,500

-$1,350

-$1,200

-$1,050

-$900

-$750

-$600

-$450

-$300

-$150

$0

$150

$300

1983-199.01 1992

-332.08

Apr-01$277.66

Apr-04-454.57

2007-169.65

2010 -1,479.33

Federal Budget Deficit/Surplus(Rolling 12-Month Sum)

Time Period

Billions($

)

Blue = Actual Red = CBO's March Forecast

16

Government Debt to GDP Growing Sharply

Source: Bianco Research

1791

1796

1801

1806

1811

1816

1821

1826

1831

1836

1841

1846

1851

1856

1861

1866

1871

1876

1881

1886

1891

1896

1901

1906

1911

1916

1921

1926

1931

1936

1941

17167

18993

20820

22646

24472

26298

28125

29951

31777

33603

35430

37164

38990

40816

42643

44469

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%Total Federal Debt To GNP/GDP

Time Period

Civil WarWW1

WW2116%

1791 to 1928 = GNP1929 to 2010 = GDP

2010 - 2020 Pro-jections

17

Nominal GDP: Today versus Great Depression

2006 2007 2008 2009 201013000

13200

13400

13600

13800

14000

14200

14400

14600

14800

1927 1929 1931 1933 1935 1937 1939 194150

60

70

80

90

100

110

120

130

Source: ISI

2 Years to Recover

12 Years to Recover

Nom

inal

GD

P (

$)

18

It’s All About Confidence

Source: Walt Handelsman - Newsday 19

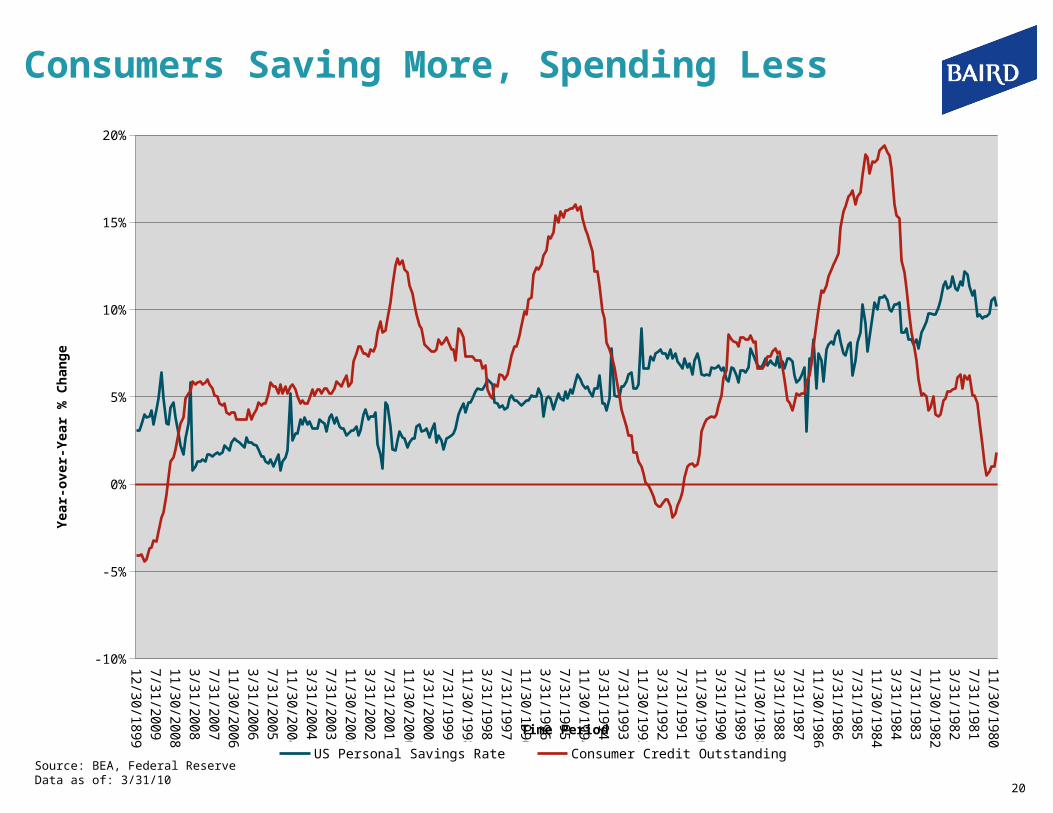

Consumers Saving More, Spending Less

Source: BEA, Federal ReserveData as of: 3/31/10

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

-10%

-5%

0%

5%

10%

15%

20%

US Personal Savings Rate Consumer Credit Outstanding

Time Period

Year-

over-

Year

% C

hange

20

A Very Weak Employment Picture

Source: BLSData as of: 3/31/10

1984 1989 1994 1999 2004 200933.0

33.5

34.0

34.5

35.0

35.5

36.0

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

US Average Weekly Hours (LHS) US Unemployment Rate (RHS) US Underemployment Rate (RHS)

Time Period

Hours

Perc

enta

ge (%

)

21

Household Net Worth Still 40% Below 2006-2007 Peak

Source: Bianco ResearchData as of: 12/31/09

1952

1953

1954

1955

1957

1958

1959

1960

1962

1963

1964

1965

1967

1968

1969

1970

1972

1973

1974

1975

1977

1978

1979

1980

1982

1983

1984

1985

1987

1988

1989

1990

1992

1993

1994

1995

1997

1998

1999

2000

2002

2003

2004

2005

2007

2008

2009

2010

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$11

$12

$13

$14

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$11

$12

$13

$14

Equity in Household Real Estate Versus Direct Stock Ownership

Time Period

Tri

llio

ns (

$)

Equity in Household Real Estate Direct Stock Ownership

22

Home Prices Fall for the First Time Since 1932

Note: Data as of 1/31/10Source: Bianco Research

1891

1894

1897

1900

1903

1906

1909

1912

1915

1918

1921

1924

1927

1930

1933

1936

1939

1942

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1900-9.79% 1914

-12.78%

1921-19.81%

1932-22.02%

194719.47%

200414.60%

Case-Shiller Nominal Home Price IndexAnnual Change

Time Period

Annual C

hange

-0.7% Year-over-year-29.63% since 7/06 peak

23

National Home Prices May Have Bottomed

Source: Bloomberg

U.S. House Price Index (Case-Shiller) M/M% Seasonally Adjusted

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Time Period

24

Mortgage Payments Relative to Income Near Record Low

Source: ISI

78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 0810

15

20

25

30

35

40

45

Time Period

Month

ly M

ort

gage P

aym

ents

as a

% o

f M

onth

ly M

edia

n I

ncom

e

12/31/0916.6%

25

Source: ISI

Strong Profits Drive Business Spending-Led Recovery

26

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

-30

-20

-10

0

10

20

30

40

Time Period

U.S. Corporate Profits

12/31/093.6%

Source: ISI

Exports-Led U.S. Recovery

27

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

-50

-40

-30

-20

-10

0

10

20

30

40

Time Period

U.S

. R

eal G

oods E

xport

s 3

Mo.

Annual R

ate

2/28/1019.52%

Short-Term Interest Rates at Zero

Source: Bianco Research

183018301831183118311832183218331833183318341834183518351836183618361837183718381838183818391839184018401841184118411842184218431843184318441844184518451846184618461847184718481848184818491849185018501851185118511852185218531853185318541854185518551856185618561857185718581858185818591859186018601861186118611862186218631863186318641864186518651866186618661867186718681868186818691869187018701871187118711872187218731873187318741874187518751876187618761877187718781878187818791879188018801881188118811882188218831883188318841884188518851886188618861887188718881888188818891889189018901891189118911892189218931893189318941894189518951896189618961897189718981898189818991899190019001901190119011902190219031903190319041904190519051906190619061907190719081908190819091909191019101911191119111912191219131913191319141914191519151916191619161917191719181918191819191919192019201921192119211922192219231923192319241924192519251926192619261927192719281928192819291929193019301931193119311932193219331933193319341934193519351936193619361937193719381938193819391939194019401941194119411942194219431943194319441944194519451946194619461947194719481948194819491949195019501951195119511952195219531953195319541954195519551956195619561957195719581958195819591959196019601961196119611962196219631963196319641964196519651966196619661967196719681968196819691969197019701971197119711972197219731973197319741974197519751976197619761977197719781978197819791979198019801981198119811982198219831983198319841984198519851986198619861987198719881988198819891989199019901991199119911992199219931993199319941994199519951996199619961997199719981998199819991999200020002001200120012002200220032003200320042004200520052006200620062007200720082008200820092009201020100%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%Short-Term Interest Rates Back to 1831

Time Period

Short

-Term

Inte

rest

Rate

s (

%)

Federal Reserve Created

28

Corporate Spreads have Narrowed Sharply

Source: Barclays Capital

Investment Grade

High Yield

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0

100

200

300

400

500

600

700

Basis

Poin

ts (

bps)

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

200

500

800

1100

1400

1700

2000

Basis

Poin

ts (

bps)

29

Source: Bloomberg

Very Steep Treasury Yield Curve

1 3 5 7 10 15 20 25 300%

1%

2%

3%

4%

5%

Mar 31, 2010Dec 31, 2009Dec 31, 2008

Maturity

Yie

ld

Maturity Dec 31, 2008 Dec 31, 2009 Mar 31, 2010 Q1 Change

1 0.34% 0.44% 0.38% -0.06

2 0.76% 1.14% 1.02% -0.12

3 0.97% 1.68% 1.58% -0.10

5 1.55% 2.68% 2.56% -0.12

7 1.73% 3.38% 3.28% -0.10

10 2.21% 3.84% 3.83% -0.01

30 2.68% 4.64% 4.72% 0.08 30

How Steep? An Historical Context

Source: BloombergData as of: 3/31/10

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

-100

0

100

200

300

400

Time Period

U.S

. 10-Y

ear

Tre

asury

Yie

ld m

inus U

.S.

3 M

onth

T-B

ill Yie

ld

31

Wage Pressure Virtually Non-Existent

Source: ISI

1965

1970

1975

1980

1985

1990

1995

2000

2005

0%

2%

4%

6%

8%

10%

12%

Time Period

Year

over

Year

Com

pensati

on p

er

Hour

12/31/090.8%

U.S. Compensation per Hour

32

Not Business as UsualSpread Volatility Goes to Extremes

Source: Barclays Capital

Option-Adjusted Spreads (bps)Excess Returns v.s. U.S. Treasuries (bps)

12/31/2007 12/31/2008 12/31/2009 3/31/201010 yr Avg

OAS 2008 2009YTD2010

U.S. Aggregate Index 91 213 61 51 75 -710 746 78

U.S. Agency (non-mortgage) Sector 43 93 30 24 43 -110 238 25

Mortgage and ABS Sectors

U.S. Agency Pass-Throughs 87 145 18 20 39 -232 495 69

Asset-Backed Securities 242 955 100 68 158 -2223 2496 133

CMBS 170 1010 473 323 208 -3274 2960 795

Corporate Sectors

U.S. Investment Grade 198 555 172 150 175 -1988 2276 114

Industrial 181 500 138 126 172 -1756 2312 80

Utility 189 537 161 144 178 -2039 2780 93

Financial Institutions 220 629 226 186 179 -2209 2141 171

U.S. High Yield 569 1669 617 570 617 -3832 5955 350

33

Too Many Treasuries/Too Little Foreign Demand

Source: Bianco Research

2002

2002

2003

2003

2003

2003

2004

2004

2004

2004

2005

2005

2005

2005

2006

2006

2006

2006

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

-50%

0%

50%

100%

150%

200%

250%

300%

-50%

0%

50%

100%

150%

200%

250%

300%

2007260%

109%

41%

24%21%

30%

200727%

23%

6%

Percentage of Treasury Issuance Bought by Non-U.S. Investors

Time Period

Tre

asury

Issuance (

%)

Blue = All ForeignersRed = China

34

Positive Supply/Demand Market Conditions

Strong demand: Investors increasing bond allocations after crisis Higher tax rates universally expected Money market yields near 0% driving investors out the yield curve

Limited Supply: Tax-exempt supply has been significantly reduced because of the taxable

“Build America” bonds program

Negative Credit Fundamentals

Tax revenue collections experiencing sharp declines Huge structural budget deficits difficult to close Rating agency downgrade risk high for many municipal issuers

Municipal Market Outlook

35

U.S. state governments

40% of revenues for US states come from personal income taxes

Personal income tax revenues dropped by more than 25% compared to the prior year in early 2009

33% of revenues for US states come from sales taxes

Sales tax revenue fell by up to 10% during certain quarters of 2009

Federal aid paid directly to states for operations through 2010 equate to roughly 6% of state monthly spending.

In aggregate, state budget shortfalls for 2010 and 2011, represent an estimated 15% of state general fund operation budgets.

Local governments

On average, property taxes account for 72% of local tax revenue.

State aid, which is particularly vulnerable for local govt’s in: CA, MI, NJ, OH, MN, NY and VA

Source: Moody’s

Municipal Tax Revenues Soften

26

Bloomberg: “U.S. state and local government tax revenues fell 6.7% as of September from a year earlier, marking the fourth consecutive quarter of decline.” 36

Treasury/Muni Yield Curves

*Assumes 30% Federal Income Tax RateSource: BloombergData as of: 3/31/2010

1 2 3 5 7 10 15 20 25 300.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Treasury

AAA Municipal

Maturity

Yie

ld

Maturity TreasuryAAA

Municipal Ratio %Tax-Adjusted

Municipal Yield*

1 0.38% 0.32% 84 0.46%

2 1.02% 0.79% 77 1.13%

3 1.58% 1.10% 70 1.57%

5 2.56% 1.77% 69 2.53%

7 3.28% 2.52% 77 3.60%

10 3.83% 3.09% 81 4.41%

30 4.72% 4.17% 88 5.96%

37

Changing Landscape in Municipal Credit

Source: Walt Handelsman - Newsday 38

Baird Advisors Investment Outlook:

Patience was rewarded in 2009 with additional outperformance expected in 2010

“Super Sale” over though finding selective opportunities

Portfolio yield advantage over benchmark still historically wide

Current prices on select securities are still below fundamental fair value

Unprecedented market volatility and dislocation subsiding

Attractive value in financials and selective mortgage-backed and asset-backed securities

Improved liquidity profile, less leverage and a very steep yield curve benefit financials

Selective opportunities in senior classes of asset-backed and mortgage-backed securities

Risk control discipline critical in a higher risk environment

Experienced investment team and risk controlled process key to strategy’slong-term success

39