prepared by coredata happy planners how to make sure your advisers stick around june 2011

TRANSCRIPT

Prepared by Coredata

Happy PlannersHow to make sure your advisers stick around

June 2011

Prepared by Coredata 2

About CoreData

CoreData is an Australian based market intelligence and research consultancy specialising in financial services.

The group provides clients with market intelligence, guidance on strategic positioning, methods for developing new business, advice on operational marketing and other consulting services.

We pride ourselves on our ability to:

identify market trends at the earliest opportunity formulate insightful quantifiable research bring deep market knowledge to research and strategy development blend experienced financial services, research, marketing and media professionals bring perspective to existing market conditions and evolving trends.

Prepared by Coredata

Where Does CoreData Operate?

Prepared by Coredata

Sampling

Prepared by Coredata

What We’ll Talk About Today

• Background and methodology: Licensee Research

• Key Insights:

• Wrap Up/Q&A

5

1. Shape of the industry

2. What advisers want

3. And the winner is…

Prepared by Coredata 6

About the Licensee Research

CoreData’s annual licensee study aims to deliver financial planning dealer groups key insight into the evolving needs and demands of financial advisers and outlines the specific triggers influencing them to join/leave a given licensee.

It assesses the ability of dealer groups to attract and retain quality financial advisers in the Australian financial services market.

The research provides insight into the shifting demands of financial advisers and their overall satisfaction with their licensee across a broad range of areas.

Prepared by Coredata

Research Context

Online survey sent to CoreData’s adviser database (1,558 respondents).

Total sample: 966 financial advisers & 592 practice principals

By licensee versus the industry and by adviser behavioural profile. Year-on-year comparisons provide a view as to the trends in the market and how the industry is shifting.

March 2011

7

methodology

sample

segmentation

period

Prepared by Coredata

STAR Index - Internal

8

Quantitative adviser ratings within the following subsets

Support

Trade Mark Brand

Autonomy

Revenues

Depth and quality of compliance support Extent of practice management support We will also separately assess value of marketing and technical support

Adviser opinion towards operating under their dealer brand Adviser perception towards each licensee brandWeighting given to branding importance by advisers

Range of available investment and administration products Adviser opinion on levels of bureaucracy in the dealer group Perceived independence of dealer group

Existing income structure of licensee (benchmarked against broader industry) Satisfaction levels of planners with remuneration

Prepared by Coredata

STAR Index - External

9

Quantitative external adviser ratings within the following subsets

Trade Mark Brand

Autonomy

Support

Revenues

Perceptions of depth and quality of compliance, practice management, marketing and all types of support of dealers

External adviser opinion on pros/cons of operating under each licenseeHow important is branding per se to external advisers

Industry view as to the range of investment products available Adviser perceptions as to the levels of bureaucracy in the dealer External opinions on the independence of the licensee

Comparison of all income structures of industry advisers Comparison of the attitudes of each licensee’s advisers towards remuneration levels vs the broader industry

Prepared by Coredata 10

3. And the winner is…

2. What advisers

want

1. Shape of the industry

Key Insights

Prepared by Coredata 11

Which of the following are a part of the remuneration model you operate under?

How do your clients pay you for the financial advice they receive?

Commission Still Relied Upon By Many

Prepared by Coredata

Things Will Have To Change…

12

Approximately how many clients do you have? What percentage of these would you personally meet with at least once a year?

•On average advisers oversee 300 clients, a reduction on 2010 (360) but still too many to service in an Opt-in environment.

•On average, advisers meet with just three in five clients in person at least annually (58.3%).

Prepared by Coredata

Which of the following advisory services do you offer clients?

The Success Of Diversified Businesses

13

Have you experienced profit growth in your business in the past 12 months? By Services offered cluster

•Those businesses offering the four key pillars plus either SMSFs, direct equities or direct property are more likely to have experienced profit growth both in 2010 and 2011.

Prepared by Coredata

Profit Growth Up, But Loyalty Down

14

Profit growth & industry sentiment towards their licensee

•Profit growth is on a strong upwards trend, yet loyalty at an industry level is declining, suggesting that advisers’ focus has shifted beyond survival mode and they are now focusing on their future.

Prepared by Coredata

An Industry Divided

15

Fee driven generalists Salaried support seeker Stretched risk specialist Unloved disengaged

Remuneration

Most upfront & ongoing fees from clients & revenue from Investment/Risk products More likely to be Salary/ Bonus

More likely to get revenue from Investment/Risk products More likely to be on Salary

Charging method

Mostly fees based on a percentage of assets (74.6%) and fees determined by the service provider (51.7%)

Mostly fees based on a percentage of assets (67.5%)

Mostly paid by Commission per transaction (77.8%)

Mostly fees based on a percentage of assets (69.6%)

Years as an adviser

Slightly more experienced (21.8% have advised for 21 years or more)

Predominandtly less experienced (55.6% have advised for 0-10 years)

Most experienced (42.4% have advised for 21 years or more)

Predominandtly less experienced (47.7% have advised for 0-10 years)

Number of clientsSlightly likely to have larger client base (33.2% > 300)

Much less likely to have larger client base (24.9% > 300 clients)

Fairly likely to have larger client base (45.5% > 300 clients)

Much less likely to have larger client base (28.1% > 300 clients)

Client contactMeet many clients (50.8% meet more than 60% of clients)

Meet less clients (49.6% meet more than 60% of clients)

Least likely to meet clients (52.5% meet less than 40% of their clients)

Meet many clients in person (51.7% meet more than 60% of clients)

FUABigger FUA (22.9% have more than $60 milion )

Biggest FUA (23.0% have more than $60 million)

Smaller FUA (61.6% have less than $10 million)

Mid-size FUA (59.4% have $10-60 million)

Average FUA per clientMid Size Fish (30.7% have $60<$140k)

Bigger Fish (34.9% have more than $250k)

Smaller Fish (64.6% have less than $60k)

Bigger Fish (34.9% have more than $250k)

Licensee helps you develop your business Most feel helped (88.1%) Feel very helped (94.3%) Much less feel helped (59.6%) Feel least helped (24.4%)

Licensee focused on your needs Focused on needs (82.1%)Extremely focused on needs (91.2%)

Much less focused on needs (54.5%)

Feel least focused on needs (7.4%)

Loyalty to LicenseeExtremely loyal to licensee (97.5%)

Extremely loyal to licensee (98.3%) Loyal to licensee (81.8%) Much less loyal (53.1%)

Feel valued as an adviser within your Licensee Feel completely valued (90.9%) Feel completely valued (93.6%) Much less feel valued (59.6%) Feel least valued (19.6%)

Profit growth in last yearMore likely had profit growth (80.9%)

More likely had profit growth (81.7%)

Less likely had profit growth (70.7%)

Much less likely had profit growth (60.2%)

Overall satisfaction Extremely satisfied (92.5%) Extremely satisfied (91.2%) Much less satisfied (53.5%) Very few satisfied (4.5%)

Likely to recommendMost likely to recommend (89.0%)

Most likely to recommend (88.6%)

Much less likely to recommend (56.6%)

Very few likely to recommend (8.5%)

Have actually recommendedMost have recommended (82.4%)

Many have recommended (73.9%)

Much less have recommended (62.6%)

Least have recommended (40.6%)

Switching potential within the year Much less likely (3.1%) Much less likely (5.0%) More likely (17.2%) Much more likely (36.4%)Switching potential within the next 5 years Much less likely (10.7%) More likely (16.6%) More likely (16.7%) Much more likely (35.8%)

Prepared by Coredata

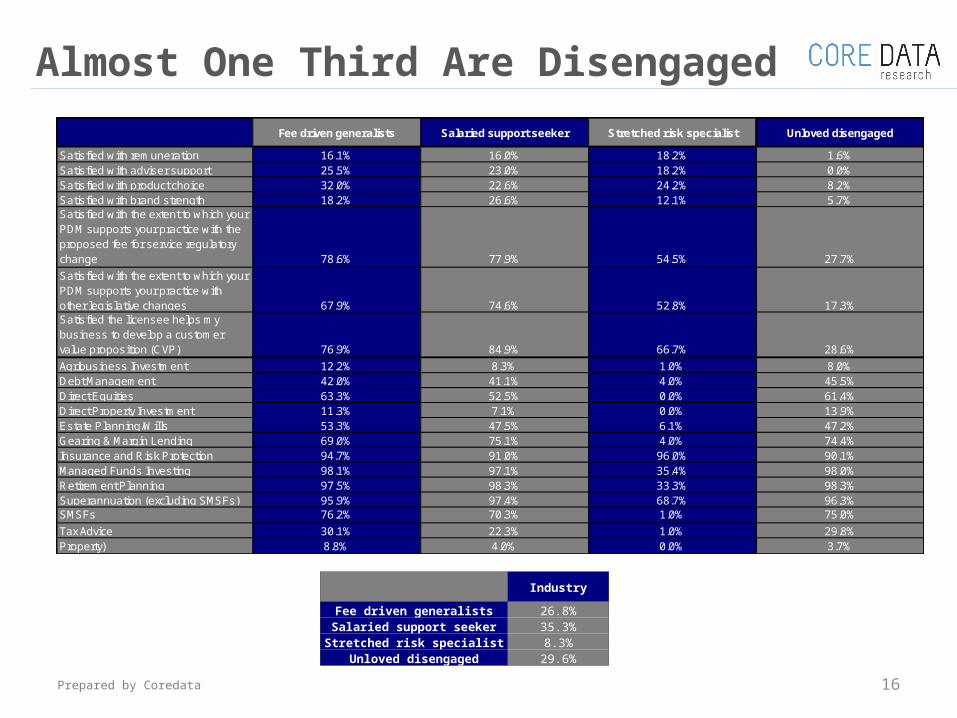

Almost One Third Are Disengaged

16

Fee driven generalists Salaried support seeker Stretched risk specialist Unloved disengaged

Satisfied with remuneration 16.1% 16.0% 18.2% 1.6%Satisfied with adviser support 25.5% 23.0% 18.2% 0.0%Satisfied with product choice 32.0% 22.6% 24.2% 8.2%Satisfied with brand strength 18.2% 26.6% 12.1% 5.7%Satisfied with the extent to which your PDM supports your practice with the proposed fee for service regulatory change 78.6% 77.9% 54.5% 27.7%

Satisfied with the extent to which your PDM supports your practice with other legislative changes 67.9% 74.6% 52.8% 17.3%Satisfied the licensee helps my business to develop a customer value proposition (CVP) 76.9% 84.9% 66.7% 28.6%

Agribusiness Investment 12.2% 8.3% 1.0% 8.0%Debt Management 42.0% 41.1% 4.0% 45.5%Direct Equities 63.3% 52.5% 0.0% 61.4%Direct Property Investment 11.3% 7.1% 0.0% 13.9%Estate Planning/Wills 53.3% 47.5% 6.1% 47.2%Gearing & Margin Lending 69.0% 75.1% 4.0% 74.4%Insurance and Risk Protection 94.7% 91.0% 96.0% 90.1%Managed Funds Investing 98.1% 97.1% 35.4% 98.0%Retirement Planning 97.5% 98.3% 33.3% 98.3%Superannuation (excluding SMSFs) 95.9% 97.4% 68.7% 96.3%SMSFs 76.2% 70.3% 1.0% 75.0%

Tax Advice 30.1% 22.3% 1.0% 29.8%Unlisted Investing (Excl Residential Property) 8.8% 4.0% 0.0% 3.7%

Industry

Fee driven generalists 26.8%Salaried support seeker 35.3%Stretched risk specialist 8.3%

Unloved disengaged 29.6%

Prepared by Coredata 17

State Representation By Segment

•Salaried support seekers are most prevalent in NSW, QLD and SA.

•The highest proportion of Unloved disengaged advisers are in TAS (34.6%) and NSW (33.5%).

In which state are you based? By Segments

Prepared by Coredata 18

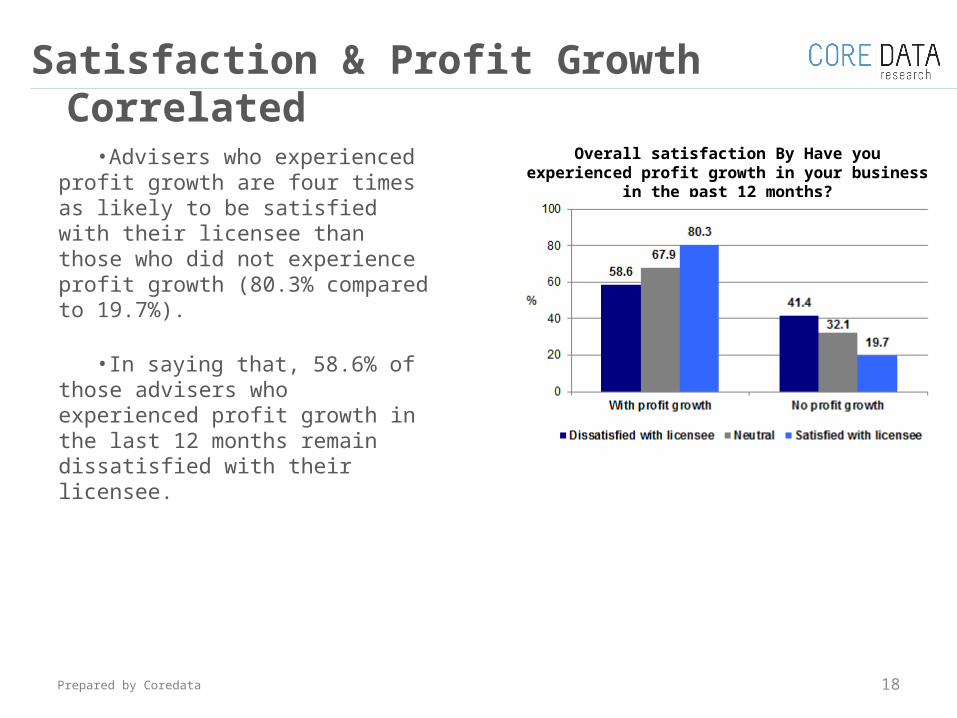

Satisfaction & Profit Growth Correlated

Overall satisfaction By Have you experienced profit growth in your business in the past 12 months?

•Advisers who experienced profit growth are four times as likely to be satisfied with their licensee than those who did not experience profit growth (80.3% compared to 19.7%).

•In saying that, 58.6% of those advisers who experienced profit growth in the last 12 months remain dissatisfied with their licensee.

Prepared by Coredata 19

Risk A Boon For Advisers

•Those advisers offering insurance and risk protection are more likely to have experienced profit growth than those who are not (75.8% vs. 61.9%). Likewise, advisers offering agribusiness investment, direct equities, direct property investment and SMSFs are slightly more likely to have reported a growth in profits in the last 12 months.

Which of the following advisory services do you offer clients? By Have you experienced profit growth in your business in the past 12 months?

Prepared by Coredata 20

3. And the winner is…

2. What advisers

want

1. Shape of the industry

Key Insights

Prepared by Coredata

Value For Money & Flexibility Valued

21

“Some of the new licensees that are positioning themselves now with the ‘pick and poke’ service menu where you tick what you want on the shopping list and that’s what you

pay for… I think that that will gather momentum, particularly in the new environment we’re

moving to because everybody’s at a different stage in their career and everyone requires

something different. Where the licensees have an offering that allows you, depending on which stage you’re at within your business, to choose

the services you want and pay for those, that’s a winning structure”

“It’s value for money. So it’s essentially looking at it like a client. ‘Am I getting value for money for what I want?’ And

also, can you support MDAs? If there’s a check list of I want this, this and this and it adds up to a fee that’s

reasonable – and they’re not going to be ramming stuff down your throat that challenges your independence.”

“It comes back to things like, to me, the recommended list. What are the available

investments on the recommended list? What is the policy for recommending outside the recommended list? What’s their policy on direct equities? Can we buy some direct equities? That to me is important,

the flexibility around that.” Male, adviser for 30 years, Futuro Financial Services

Male, adviser for 22 years, Morgan Stanley Smith

Barney

Male, adviser for 19 years, Financial

Wisdom

Prepared by Coredata

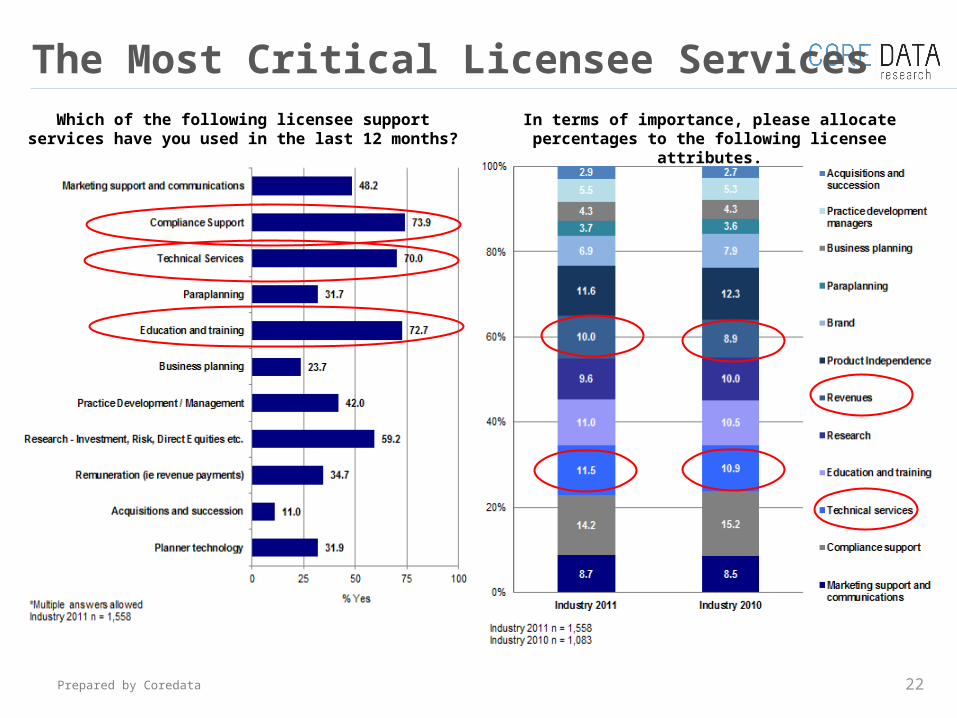

The Most Critical Licensee Services

22

Which of the following licensee support services have you used in the last 12 months?

In terms of importance, please allocate percentages to the following licensee attributes.

Prepared by Coredata

Product Independence A Key Trigger

23

Please tick any of the following factors that if good/bad would make you more inclined to join/leave a licensee?

•Product independence/choice is the number one driver for joining a licensee (49.9%), just ahead of compliance support (44.9%), remuneration (43.2%) and technical services (42.7%).

•However compliance support & remuneration appear to be ‘hygiene factors’; advisers are more likely to leave a licensee if compliance is poor, than they are to join if it’s strong.

Prepared by Coredata 24

Driver Analysis (STAR Index)

Prepared by Coredata

Top 15 Attributes

25

2011 Importance

Rank

2010 Importance

RankAttribute Movement Category Top 3 Leaders

1 3 Quality of technical information provided Technical servicesipac EP, Commonwealth, ipac

FP

2 9 Relevance of technical presentations and seminars Technical services ipac EP, Commonwealth, ipac FP

3 26Licensee helps me recruit and retain the right staff for my business

Business planningCommonwealth, NAB, ipac

EP

4 14Audit process helps me develop my business by identifying problems and providing solutions

Compliance supportipac EP, Commonwealth,

MLC/Garvan

5 1Research team is able to clearly communicate their requirements

ResearchCommonwealth, Genesys,

ipac EP

6 23 Paraplanners are competent and knowledgeable Paraplanning ipac EP, AXA, Genesys

7 25 Licensee pays revenue accurately RemunerationGenesys, Commonwealth,

ipac EP

8 NewLicensee helps me articulate the value of my advice to my clients -

Marketing support and communications

Commonwealth, Charter, ipac EP

9 New Licensee helps me source the right advisers for my business - Business planning Commonwealth, NAB, ipac EP

10 22 Quality of technical publications Technical servicesCommonwealth, ipac EP,

Financial Wisdom

11 12Licensee keeps me informed of what is going on in the industry in a timely manner

Marketing support and communications

Commonwealth, Charter, Securitor

12 20 Quality of training materials provided Education and trainingCommonwealth, Genesys,

Charter

13 29 The extent to which your PDM adds value to your businessPractice Development Managers (PDMs) / Practice Managers /

Business Coaches

Genesys, Commonwealth, ipac EP

14 19The investment guidelines provided by the licensee are appropriate for my business

ResearchCommonwealth, ipac EP,

Genesys

15 18 Revenue statements are easy to read RemunerationGenesys, Commonwealth,

PIS

Prepared by Coredata

Attribute Ratings

26

Marketing support and communications Industry 2010 Industry 2011% Contribution to the Overall model

Quality of the marketing materials provided to promote my business 6.56 6.90 1.68%Ability to customise marketing materials 6.54 6.76 1.19%Licensee keeps me informed of what is going on in the industry in a timely manner 7.20 7.49 3.48%Licensee helps me articulate the value of my advice to my clients 7.07 4.48%Overall satisfaction with marketing support and communications 6.75 7.09

Compliance support Industry 2010 Industry 2011% Contribution to the Overall model

Advice guidelines are easy to understand 7.00 6.83 1.00%Advice tools are easy to use 6.78 6.58 0.56%Audit process helps me develop my business by identifying problems and providing solutions 7.01 6.95 5.85%Overall satisfaction with compliance support 7.06 6.93

Technical services Industry 2010 Industry 2011% Contribution to the Overall model

Relevance of technical presentations and seminars 7.27 7.34 7.87%Quality of technical information provided 7.59 7.72 8.05%Quality of technical publications 7.41 7.56 3.77%Timeliness of information on legislative and technical changes 7.53 7.72 1.21%Overall satisfaction with technical services 7.48 7.68

Paraplanning Industry 2010 Industry 2011% Contribution to the Overall model

Paraplanning service provided by my licensee represents good value for money 6.64 7.46 2.01%Quality of the Statements of Advice provided by the paraplanning service 6.77 7.28 1.36%Paraplanners are competent and knowledgeable 6.99 7.52 5.42%Overall satisfaction with the paraplanning service 6.78 7.34

Prepared by Coredata

Attribute Ratings

27

Education and training Industry 2010 Industry 2011% Contribution to the Overall model

Availability of adviser to adviser information sharing and networking opportunities 6.76 0.07%Relevance of professional development days and national conferences 7.06 6.96 0.71%Quality of training materials provided 7.08 7.07 3.43%Overall satisfaction with education and training 7.08 7.05

Business planning Industry 2010 Industry 2011% Contribution to the Overall model

Licensee helps with my business development 6.06 6.91 1.39%Licensee helps me recruit and retain the right staff for my business 5.57 6.42 7.81%Licensee helps my business to develop a customer value proposition (CVP) 7.37 2.46%Licensee helps me source the right advisers for my business 5.58 6.62 4.13%Licensee helps me segment my client base 7.01 1.95%Licensee helps me determine appropriate pricing of my services 7.06 2.25%Overall satisfaction with business planning 6.08 7.16

Practice Development Managers (PDMs) / Practice Managers / Business Coaches Industry 2010 Industry 2011% Contribution to the Overall model

The extent to which your PDM adds value to your business 6.12 6.83 3.42%The extent to which your PDM supports your practice with the proposed fee for service regulatory change 7.03 1.78%The extent to which your PDM supports your practice with other legislative changes 6.74 0.42%The responsiveness of your PDM 6.92 7.46 2.65%Overall satisfaction with your PDM 6.66 7.27

Research Industry 2010 Industry 2011% Contribution to the Overall model

The ease of contacting the research team 6.93 7.25 1.05%Research team is able to clearly communicate their requirements 6.80 7.27 5.67%The investment guidelines provided by the licensee are appropriate for my business 7.00 7.14 3.15%The quality of investment and risk research 7.07 7.40 0.36%Overall satisfaction with research 6.94 7.29

Remuneration Industry 2010 Industry 2011% Contribution to the Overall model

Licensee pays revenue in a timely manner 8.28 8.37 0.76%Licensee pays revenue accurately 8.04 8.09 4.65%Revenue statements produced by the licensee are accurate 8.02 8.09 1.13%Revenue statements are easy to read 7.73 7.72 2.82%Overall satisfaction with revenue payments 7.99 7.98

Acquisitions and succession Industry 2010 Industry 2011% Contribution to the Overall model

Licensee has a wide choice of succession options 6.05 7.27Licensee provides technical guidance when acquiring another practice 5.76 6.94Licensee makes resources available to help me integrate an acquisition 5.86 7.01Overall satisfaction with acquisitions and succession 5.93 7.08

Prepared by Coredata 28

3. And the winner is…

2. What advisers

want

1. Shape of the industry

Key Insights

Prepared by Coredata

Internal STAR: Commonwealth FP

29

Overall STAR Internal Ratings

Prepared by Coredata

External STAR: ipac EP & ipac FP

30

Overall STAR External Ratings

Prepared by Coredata

CFP & ipac EP Top Overall Satisfaction...

31

Overall, how satisfied are you with your licensee?

Prepared by Coredata

... And Have Highest Advocacy Levels

32

How likely are you to recommend your licensee?

Prepared by Coredata

Switching Intent Increases Over Time

33

How likely are you to switch to a new licensee within the next 12 months?

How likely are you to switch to a new licensee within the next 5 years?

Prepared by Coredata 34

Having Own AFSL Trumps All OffersPlease rank who you believe are the top 5 dealers to work for, where 1

indicates the top dealer to work for.•When asked to rank the ‘top

five’ dealer groups to work for, having their own ASFL was deemed the most attractive option.

•There was little differentiation among the licensees with Charter Financial Planning placing second by a small margin (3.4). AXA Financial Planning, ipac Equity Partners, Shadforth and CFP also rated highly, all with a score of 3.3 out of 5.

Prepared by Coredata 35

Charter FP ‘Best Licensee’ In IndustryOverall, which licensee do you perceive to be the best in the industry?

24.48.0

7.26.1

4.83.7

3.13.12.92.52.32.22.21.91.51.41.31.11.11.01.00.90.90.80.70.70.70.60.40.40.40.30.20.20.20.10.10.10.10.1

9.2

0 10 20 30

Own AFSLCharter Financial Planning

Macquarie Private WealthAXA Financial PlanningAMP Financial Planning

Godfrey PembrokeMLC/Garvan Financial Planning

Shadforth Financial Groupipac Financial Planning

Count FinancialProfessional Investment Services

Commonwealth Financial PlanningLonsdale Financial Group

SecuritorGenesys Wealth Advisers

ipac Equity PartnersApogee Financial Planning

RBS MorgansWestpac Financial Planning

AFSHillross Financial Services

Tynan MackenzieMatrix Planning Solutions

Financial WisdomMillennium3 Financial Planning

WealthsureWHK Financial Planning

Bridges Financial PlanningAon Financial Planning and Protection

Financial Services PartnersNational Australia Bank Financial Planning

RI AdviceANZ Financial Planning

St George Financial PlanningSentry Group

Guardian Financial PlanningMagnitude

Australian Financial Group (AFG)Futuro Financial ServicesMeritum Financial Group

Other

%

•When asked to name the licensee they perceive to be the best in the industry (excluding their own), again having their own AFSL ranked first, with one quarter of advisers considering this option to exceed the offer of any licensee in the market (24.4%).

•Charter FP was the highest ranked licensee with 8.0% of adviser votes, followed by Macquarie Private Wealth (7.2%), AXA FP (6.1%) and AMP FP (4.8%).

Prepared by Coredata

CoreData Licensee Of The Year 2011

36

8.24 8.01 7.91 7.54 7.48 7.41 7.397.06 7.06 7.03 6.88 6.62

6.20 5.96

0

2

4

6

8

10C

om

mo

nw

ealt

h F

inan

cial

P

lan

nin

g

ipac

Eq

uit

y P

artn

ers

Gen

esys

Wea

lth

Ad

vise

rs

Ch

arte

r Fin

anci

al P

lan

nin

g

ML

C/G

arva

n F

inan

cial

Pla

nn

ing

AX

A F

inan

cial

Pla

nn

ing

Sec

uri

tor

Nat

ion

al A

ust

ralia

Ban

k F

inan

cial

Pla

nn

ing

Pro

fess

ion

al In

vest

men

t S

ervi

ces

Fin

anci

al W

isd

om

Gu

ard

ian

Fin

anci

al P

lan

nin

g

AM

P F

inan

cial

Pla

nn

ing

Co

un

t Fin

anci

al

ipac

Fin

anci

al P

lan

nin

g

Licensee of the Year 2011

Ave

rag

e ra

ting

sco

res

(0-1

0)

Prepared by Coredata 37

In Summary….