pre-payment the “aqualectra experience” by steven martina president & ceo aqualectra...

TRANSCRIPT

Pre-PaymentPre-Paymentthe “Aqualectra Experience”the “Aqualectra Experience”

by Steven Martinaby Steven Martina President & CEO AqualectraPresident & CEO Aqualectra

Metering, Billing, CRM/CIS Americas

Sao Paulo, Brazil, 12, 13, 14 August 2003

Curaçao, Netherlands Antilles182 square miles, population 135.000, Avg. Temp 27 0C

Legal structure of the corporation

ProductionProduction

StIP/EGCHolder of 100% Common stock

Mirant Holder of 100% Preferred stock

100% Common

Stock

100% Common

Stock

100% CommonStock

49% Common

Stock

DistributionDistribution Multi UtilityMulti Utility

CUCCUCHoldings Holdings

B.O.OB.O.O

Aqualectra Key Figures year end 2002

Total Assets 208 USD Million

Shareholders Equity 292 USD Million

Revenue 2002 183 USD Million

Net result 2002 3.5 USD Million

Capacity Electricity 235 MW nameplate

Capacity Water 69.000 M3 / Day nameplate

Peak Load Electricity 120 MW

Daily average Usage 38.000 M3 / Day

Electricity connections 67.000

Water connections 63.000

Personnel 737

THE AQUALECTRA EXPERIENCE

Challenges to overcome

• Increasing untimely payment by customers

• Increasing non payment by customers

• Increasing theft

As a Consequence

• Collection process becomes more complex

• Increasing provision bad debts

Pre-Payment as a solutionMain objectives

• A solution for purchasing of electricity and water in portions according the customers budget

• Rationalize the process of dis-/ reconnects

• Minimize credit lines and outstanding arrears

• Improve public image of Aqualectra

Improve overall efficiency of theImprove overall efficiency of the the collection processthe collection process

Pre-Payment as a solutionThe Economic Rationale – The Model basics

• Supports conversion of conventional to pre-paid water, electricity separately or jointly

• Implicit assumptions that the products are converted jointly. Unmatched conversion has less benefit on e.g. meter reading and bill distribution

• Time span of 10 years, coincides with the life cycle of the meter

Pre-Payment as a solutionThe Economic Rationale – The benefits

• Earlier collection of revenue

• Reduction of bad debts write off

• Collection of old debt through pre-payment surcharge

• Gain in efficiency of personnel

• Reduction in dis / re-connect procedures and cycle time

• Reduction of cost in printing and distributing invoices

• Reduction of cost in meter reading

• A profit tax reduction due to increased depreciation and investment allowance of 8% as allowed by Antillean tax laws

Pre-Payment as a solutionThe Economic Rationale – Expenses

• Required investment in meters, central equipment and payment points

• Possible reduction of volume purchased by a more conscious client

• No collection of surety, Pay back of surety to converted clients

• Commissions payable to payment points

• Operational costs of the prepayment system

• Payment is received before products are used rather than afterwards

• The time to process readings and produce and distribute an invoice

• The time the bill remains outstanding at a customer

Pre-Payment as a solutionThe Economic Rationale – Main assumptions“Cash collected earlier”

Pre-Payment as a solutionThe Economic Rationale – Main assumptions“Aggressiveness in converting problem accounts”

The policy is to convert problem accounts into prepaid accounts.

This has a significant impact on financial attractiveness of prepaid.

An “aggressiveness index” varying from 0% to 100% has been included in the model.

The significance of the index is as follows:– if the index is set to 0%, problem accounts are converted to prepaid at the

same rate as other accounts. – if the index is set to 100%, problem accounts are aggressively converted to

prepaid. Problem accounts are converted to prepaid before any normal accounts.

The aggressiveness index has been set to 75%

Pre-Payment as a solutionThe Economic Rationale – Main assumptions“Aggressiveness in converting problem accounts”

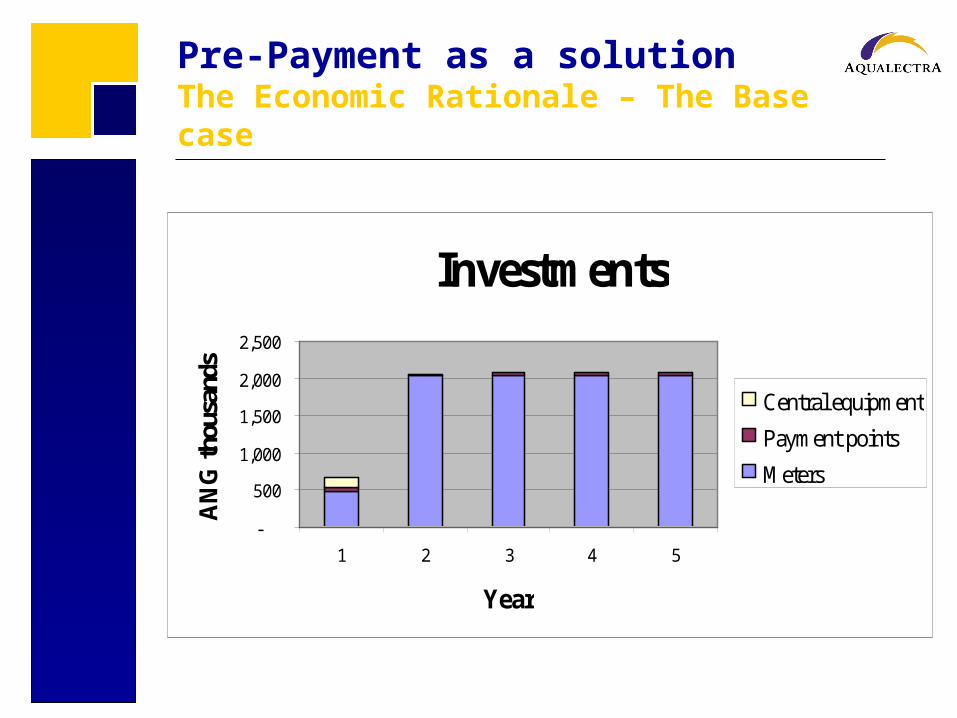

Pre-Payment as a solutionThe Economic Rationale – The Base case

• The following pages illustrate the variable settings and the results of the financial model for a base case, which consists of the most likely assumed values

• The proportion of the achieved investments, benefits and expenses in the base case is displayed graphically over the first 5 years, which in the base case is the period in which the conversions from traditional to prepaid occur

• Note: meter investments include installation but are net of recovered installation charges and saved traditional meter replacements

Pre-Payment as a solutionThe Economic Rationale – The Base case

Investments

-

500

1,000

1,500

2,000

2,500

1 2 3 4 5

Year

AN

G th

ousa

nds

Central equipment

Payment points

Meters

Pre-Payment as a solutionThe Economic Rationale – The Base case

Expenses

-

200

400

600

800

1,000

1,200

1 2 3 4 5

Year

AN

G t

hou

san

ds Operational costs

Commissions

Returned deposits

Reduction in usage

Pre-Payment as a solutionThe Economic Rationale – The Base case

Benefits

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1 2 3 4 5

Year

AN

G t

hou

sdan

ds

Personnel savings

Saved bill distr

Recovery old debts

Saved cutoff/reconn

Tax savings / depr

Saved meter readings

Early collection

Fewer A/R writeoffs

Pre-Payment as a solutionConclusions and recommendations

• The base scenario provides a positive picture of the project, with a return on investment (IRR) of 24%

• In the base scenario, with a yearly investment in prepaid meters (incl. installation), more than half of this expenditure is recovered immediately through the earlier collection of revenues

• The financial viability is sensitive, however, to a number of the input variables, some of which the utility does not have under its control (reduction in usage)

• The major benefits in financial terms are the effects of fewer accounts receivable write-offs, early collection, and the tax break caused by depreciation and the investment allowance

• The investment in meters is by far the largest component of investment, overshadowing investment in central equipment and payment points

Pre-Payment as a solutionConclusions and recommendations continued

• We believe that prepaid has clear financial benefits when performed for problem accounts

(because conversion to prepaid reduces account receivable write-offs and money-losing cutoff procedures)

and in the case of new installations, where most or all of the investment can be recovered from the client.

• We believe the model shows that the benefits of conversion of a normal account (a well-paying customer) does not outweigh the investment, however:

In the case that a normal account is charged for the conversion to prepaid the ROI will not be negatively impact

Pre-Payment as a solutionConclusions and recommendations continued

• The “aggressiveness index” is a major factor in the financial viability of the project. It is recommended to pursue at least a moderately aggressive policy of converting problem accounts to prepaid. The sensitivity analysis shows only marginal to negative viability if lower aggressiveness indices are used.

• The above must be tempered by the realization that Prepaidshould probably not be marketed as a solution for problem accounts only. Doing so might create a stigmatization of the concept, endangering the overall project.

Some ImagesElectricity Distribution – Pre-Paid Meters

Some ImagesElectricity Distribution – Pre-Paid Meters

Some ImagesElectricity Distribution – Pre-Paid Meters

Concluding RemarksStakeholder perspective

StakeholderSatisfaction

StakeholderContribution

Investors

Customers &

Intermediaries

Employees

Regulators &

Communities

Suppliers

Concluding Remarks The Aqualectra Experience

DIVERSIFICATION / DIVERSIFICATION / INNOVATIONINNOVATION PARADIGM PARADIGM

• Pre-payment concept fully accepted (10.000 pre-paid electricity meters installed/ Water in pilot phase )

• Increasing demand (instead of technology push)

• Economic rationale

• Contributed to a positive image of “Aqualectra Corporate Citizenship”

Pre-PaymentPre-Paymentthe “Aqualectra Experience”the “Aqualectra Experience”

by Steven Martinaby Steven Martina President & CEO AqualectraPresident & CEO Aqualectra

Metering, Billing, CRM/CIS Americas

Sao Paulo, Brazil, 12, 13, 14 August 2003

THANK YOU FOR YOUR ATTENTIONTHANK YOU FOR YOUR ATTENTION