practicing the resource based view: learning to play the ... · practicing the resource based view:...

TRANSCRIPT

Supervisor: Johan Brink Master Degree Project No. 2016:52 Graduate School

Master Degree Project in Innovation and Industrial Management

Practicing the Resource Based View: Learning to Play the

Song of “Theory in Practice”

A reflective case study on the challenges of formulating an expansion strategy through the lens of the resource based view

Albin Gustavsson and Jonathan Johansson

Abstract

Background and Problem: The resource based view (RBV) has been a central paradigm withinmanagement research for more than two decades and it is an accepted theory used to analyzedifferences infirmperformanceaswellasstrategyformulation.However,theRBVhasbeenaccusedofbeingtootheoreticalwithpractitionersfindingitdifficulttofullyoperationalizeitsconcepts,makingtheRBVdifficulttouseinpractice.CompanyXisaproviderofdigitalvisualizationtoolsforonlinemarketingintherealestateindustryandthusneedstoformulateanexpansionstrategythatmatchesthecompany’sresourcesandcapabilitieswiththeopportunitiesintheUSmarket.

Purpose:ThepurposeofthisthesisisatitscoretoreflectonthepracticalapplicationoftheRBVinareallife strategic setting to highlight what potential challenges practitioners face when attempting tooperationalize the theory. Since this thesis has a strong emphasis on theory in practice the situationCompanyX finds it self inpresents a good setting to apply theRBVona real strategic issue,namely aproposedexpansionintheUSmarket.ThepurposeofthisthesishasaclearpracticalcomponentintheactualstrategyforCompanyXaswellasatheoreticalcomponentintheformofthereflectiveapproachontheoryaspractice.

Method:Theresearchdesignofthisthesishastwolayers,thefirstofwhichisacasestudyofCompanyXandtheapplicationoftheRBVinformulatingaanexpansionstrategy.ThesecondlayerbeingareflectiveapproachthatallowstheauthorstoidentifychallengesofapplyingRBVtheoryinpractice.Firsthanddatacollectionhasbeenconductedthroughanumberof interviewswithmanagersatCompanyXaswellasrepresentatives from different stakeholders in the US real estate market. Secondary data has beencollected through a comprehensive narrative literature review as well as secondary sources providingadditionaldataontheUSmarket.

Findings:ThecombinedinternalandexternalfindingsshowthatCompanyXhascapabilitiesthatcanbeleveragedwithintwodifferentsubmarketstoapproachdifferenttypesofcustomers.Furthermore, theanalysisrevealssomegapsinthecompaniesresourcesstockwhererecommendationsaregivenforhowto close those resource gaps. Additionally the reflection on the RBV in practice allows the authors toidentifyanumberofchallengesthatemergewhenoperationalizingthetheoryinarealbusinesssetting.ThethesisconcludeswithrecommendationsforfutureresearchdirectionswithintheRBVwiththeaimtoincreaseitspracticalapplicability.

Acknowledgements

Thismasterthesishasbeenwrittenduringthespringsemesterof2016attheUniversityofGothenburg,School of Business Economics and Law by Albin Gustavsson and Jonathan Johansson attending theInnovationand IndustrialManagementMasterProgram. Wewould like to thankoursupervisor, JohanBrink,forprovidingguidanceandsupportthroughoutthisprocess.

Furthermorewewouldliketothankthecompany,whichinthisthesisgoesunderthenameofCompanyX, for giving us unique access to all key personnel within the firm as well as for hosting us at theirheadquarterinBangkok.TheemployeesatCompanyXprovideduswithgreatinformationregardingtheinternalprocessesandresources.AspecialthankyoutoCharlieEngelandMatthewCampbellforbeingsogenerouswiththeirtimeandeffortspentonguidingusinthestrategydevelopmentprocess.

We are also thankful towards all the external interview participants who contributed with great theirknowledgeontherealestatemarketintheUS.

Tableofcontent

1. Introduction......................................................................................................................................11.1 Background...........................................................................................................................................21.2 ResearchProblem.................................................................................................................................31.3 ResearchPurpose..................................................................................................................................41.4 ResearchQuestions...............................................................................................................................4

2. Methodology......................................................................................................................................52.1 ResearchStrategy..................................................................................................................................52.2 LiteratureReview..................................................................................................................................62.3 ResearchDesign....................................................................................................................................72.4 Datacollectionandanalysis..................................................................................................................8

2.4.1 InternalData...................................................................................................................................92.4.2 Customers.....................................................................................................................................102.4.3 Competitors..................................................................................................................................11

2.5 Sampling..............................................................................................................................................112.6 Credibilityoftheresearch...................................................................................................................12

3. TheoreticalFramework.............................................................................................................143.1 InternalPerspective............................................................................................................................14

3.1.1 TheResourceBasedView.............................................................................................................143.1.2 RBV–APracticalFramework.......................................................................................................16

3.2 Externalperspective............................................................................................................................173.2.1 Customers.....................................................................................................................................173.2.2 Competitors..................................................................................................................................213.2.3 ResourceGaps..............................................................................................................................21

4. AnalyticalModel...........................................................................................................................26

5. EmpiricalFindings.......................................................................................................................285.1 InternalPerspective............................................................................................................................28

5.1.1 Products&Services.......................................................................................................................285.1.2 Salesprocess.................................................................................................................................285.1.3 Production....................................................................................................................................305.1.4 CustomerServiceandExternalRelations......................................................................................315.1.5 Experienceandleadership............................................................................................................325.1.6 ResearchandDevelopment..........................................................................................................32

5.2 ExternalPerspective............................................................................................................................335.2.1 TheResaleVertical.......................................................................................................................335.2.2 TheRentalVertical........................................................................................................................39

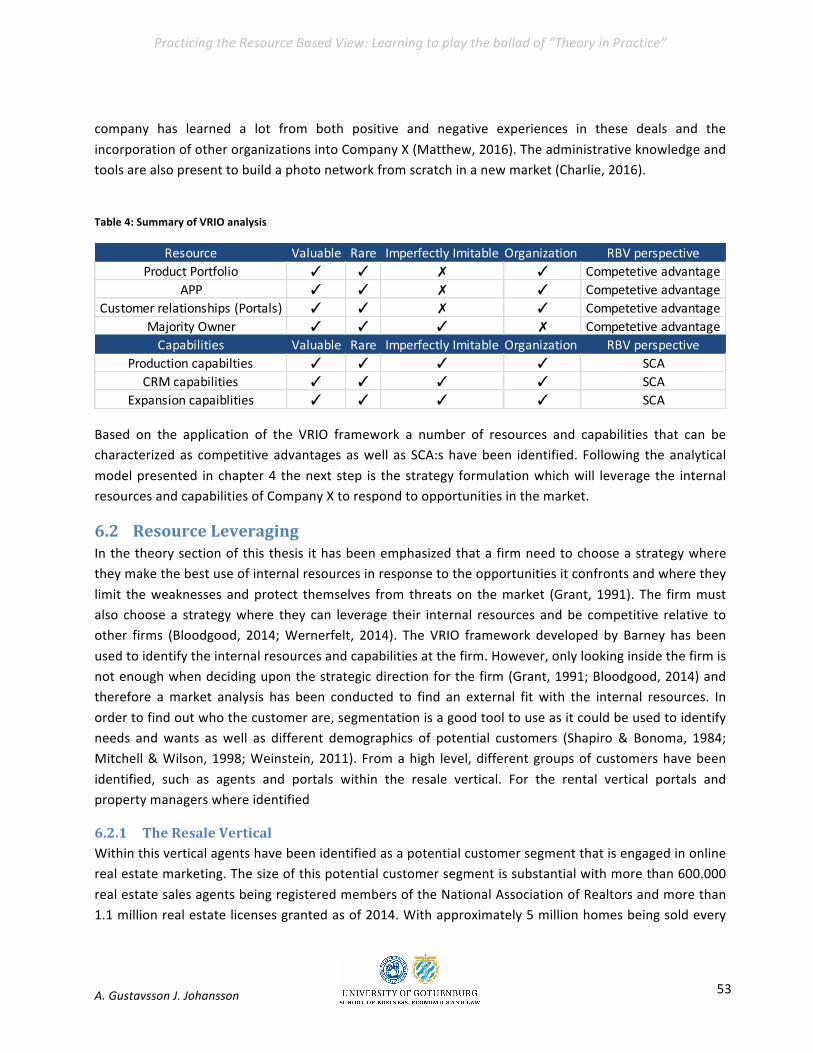

6. Analysis............................................................................................................................................466.1 IdentificationandEvaluationofSCA:s................................................................................................46

6.1.1 Resources......................................................................................................................................46

6.1.2 Capabilities...................................................................................................................................496.2 ResourceLeveraging...........................................................................................................................53

6.2.1 TheResaleVertical.......................................................................................................................536.2.2 TheRentalVertical........................................................................................................................55

6.3 ResourceGaps.....................................................................................................................................56

7. Conclusion.......................................................................................................................................587.1 ProposedstrategyforCompanyX.......................................................................................................58

7.1.1 TheResidentialResaleVertical.....................................................................................................587.1.2 TheRentalVertical........................................................................................................................597.1.3 ResourceGaps..............................................................................................................................59

7.2 Reflections...........................................................................................................................................607.2.1 FutureResearch............................................................................................................................60

8. References......................................................................................................................................63

9. Appendix1:Listofinterviews.................................................................................................69

Tableoffigures

Figure 1: The relationship between Core Assumptions - VRIO Framework - Sustainable CompetitiveAdvantage.Source:Barney&Delwyn(2007)......................................................................................15

Figure2:TheRBVapproachtostrategyformulation.AdaptedfromGrant(1991).....................................16

Figure3:TheNestedApproachSegmentationModel.RecreatedbytheauthorsfromShapiro&Bonoma(1984)...................................................................................................................................................20

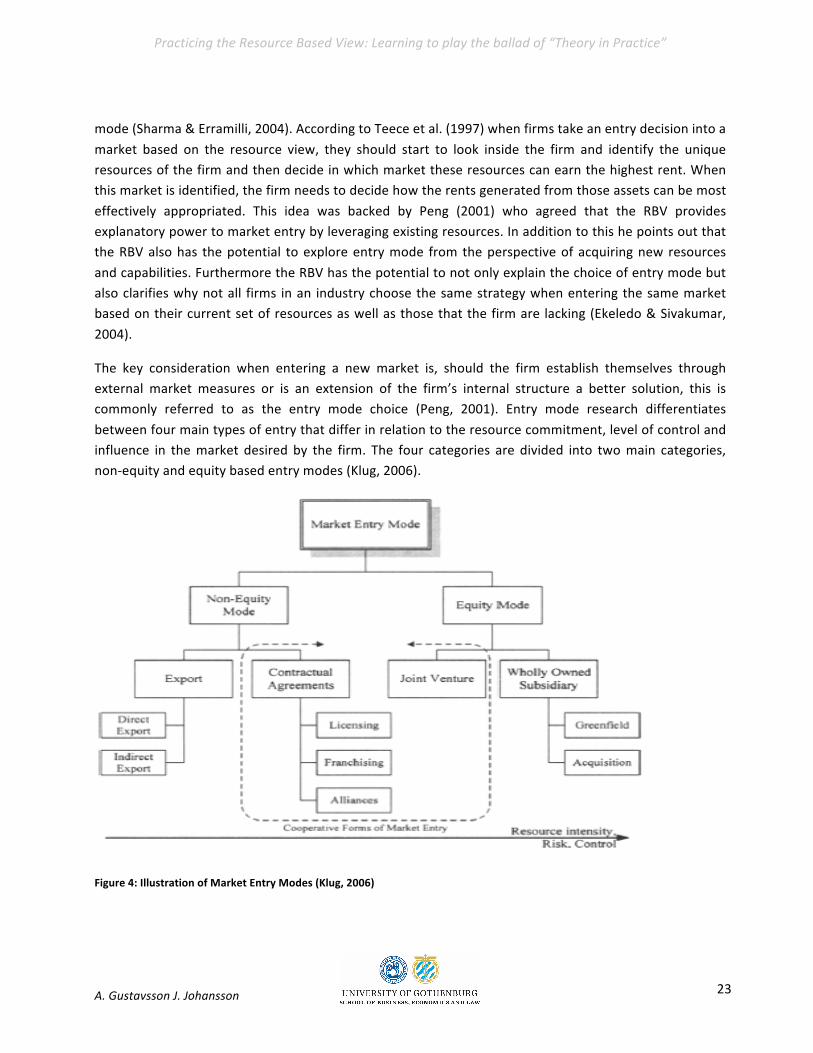

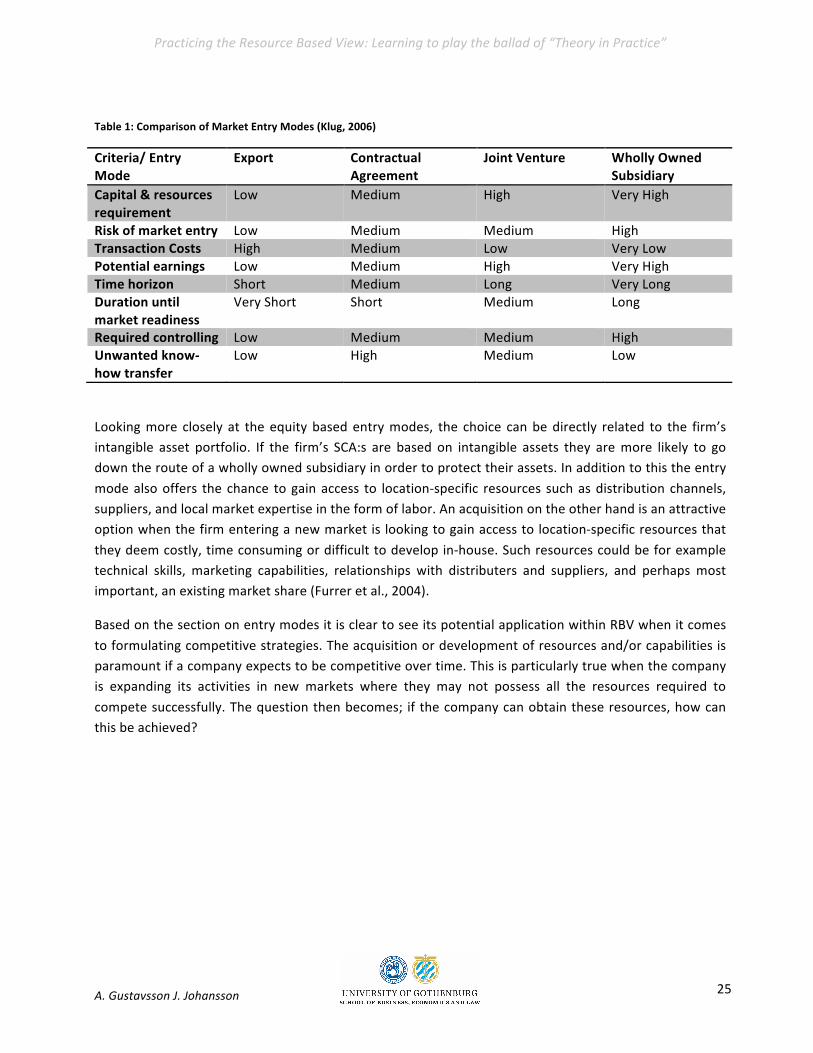

Figure4:IllustrationofMarketEntryModes(Klug,2006)...........................................................................23

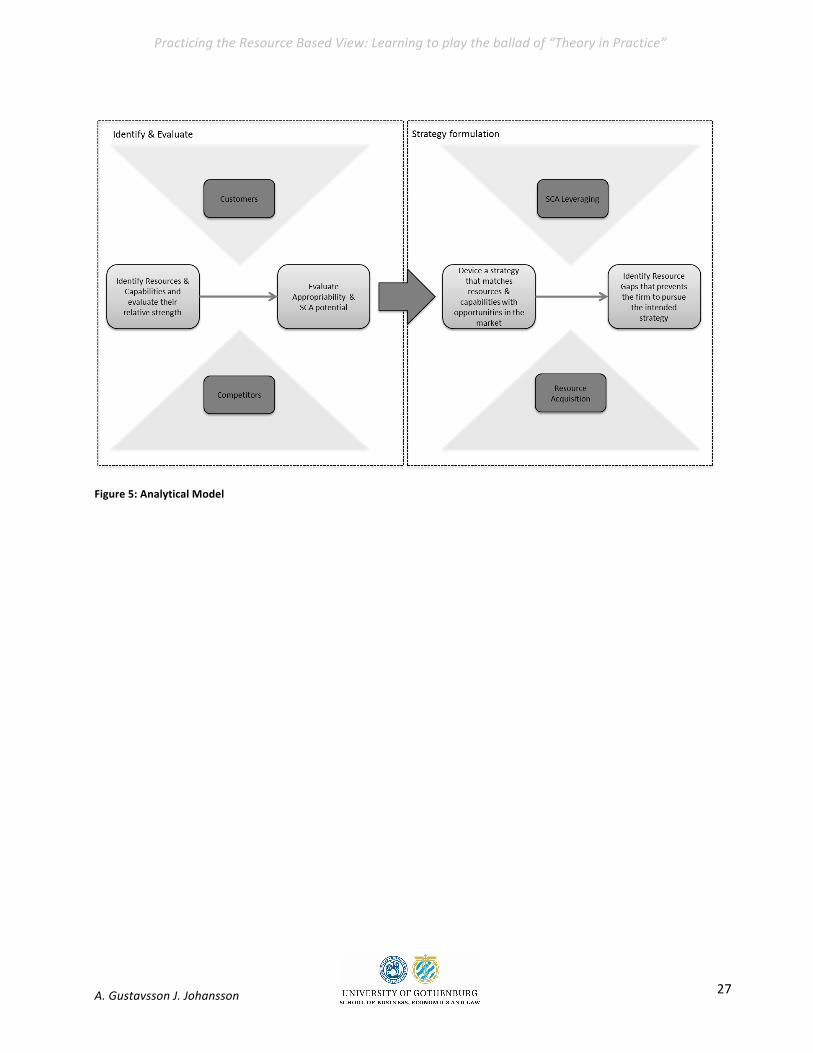

Figure5:AnalyticalModel............................................................................................................................27

Figure6:OverviewofCompanyX’ssalesprocesswithintheResaleVertical(Authorsownelaboration)...29

Figure8:OverviewofCompanyX’ssalesprocesswithintheRentalVertical(Authorsownelaboration)...30

Figure9NumberoftransactionsofRealtors(NAR,2015)............................................................................34

Figure10Percentwebsiteusebyagentstodisplaylistings(NAR,2014).....................................................36

Figure11Web-trafficmajorportalsandbrokersites,basedondatafromcompete.com..........................36

Figure12Product-portfolioofCompanyXand9othercompetitors...........................................................38

Figure13:SimplifiedoverviewofthePropertyManagementsegment(authorsownelaboration)............40

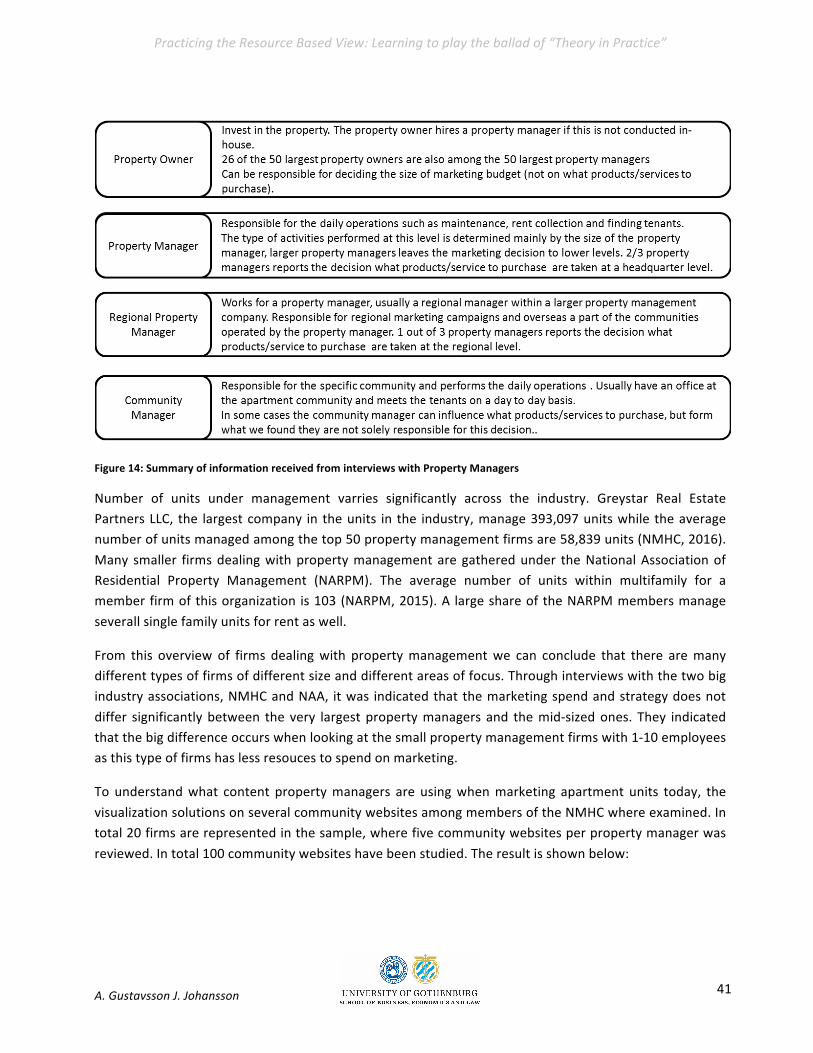

Figure14:SummaryofinformationreceivedfrominterviewswithPropertyManagers.............................41

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 1

1. IntroductionThe introduction startswithahigh levelapproach to strategyand thennarrowsdown tohighlights themainaspectsof the resourcebasedview.Furthermoreashortdescriptionof thecasecompany ismadewhichisfollowedbydefinitionoftheresearchproblemandthepurposeoftheresearch.Thesectionendswiththeresearchquestions.

Strategy is somewhatof a buzzwordwithin the field of business today.Managers often talk about theimportanceofhavingaclearbusinessstrategyinordertosucceed,butwhenaskedtospecifywhattheirstrategyis,manymanagerscannotevenprovideastraightanswer(Collis&Rukstad,2008).Inthe1950s-and-60s, strategy was about thorough planning and then execution in a step-by-step process (Grant,2013). In those days companies suppliedmass markets with products and services, making long-termplanseasier to implementdue to the supply sidepowerbalance (Denning,2015).However, thepowerbalancehasshiftedtowardsthedemandsideduetoglobalization,deregulationandtheincreasingpaceoftechnologydevelopment(Ibid).Intoday’sbusinessclimatethedynamismoftheexternalenvironmentmakes strategic planning increasingly difficult for firms adopting amarket based approach, where theindustry structure guides strategic choices (Sirmon et al., 2007). The market based approach is alsoreferred toas the industryperspective,oroutside-inmodel and itsmost famousproponent isMichaelPorterandhisFiveForcesframework(Spanos&Lioukas,2001).

Thelackoffocusontheinternalassetsofthefirmleadtoanewapproachtostrategicanalysisthatbuilton the work of Edit Penrose in the 1950s and later Paul Rubin in the 1970s (Newbert, 2007) whichestablished a new paradigm within management research called the Resource Based View (RBV)(Wernerfelt, 1984; Barney, 1991;Grant, 1991; Peteraf, 1993).Amajor problemwith themarket basedapproachwastheimplicitassumptionofastableenvironment,whichdoesnotcorrespondwellwiththeviewthatmany industriesarebecoming increasinglydynamic, thusmaking industryanalysis impractical(Barney, 2001). The major difference between the two perspectives lies in how a firm’s competitivestrategy shouldbe formulated. In themarketbasedapproach, strategy shouldbebasedonpositioningthe firmwith regards to industry forces, and thus themost attractivemarketpositiondetermineshowandwhere the firmshouldcompete (Porter,2008). In the resourcebasedviewon theotherhand, theresourcesthefirmpossessisthesourceofcompetitiveadvantageandthustheyshoulddeterminewhereandhowtocompete(Barney,2001).

Many researchers are of the opinion that today’s business environment is more turbulent than ever,which lends support to the idea that the RBV is amore suitable theoretical starting point in strategicanalysis (Guo, 2007; Sołoducho-Pelc, 2014; Švárová & Vrchota, 2014).When growing a firm, strategicmanagement is an essential component, and in order to do this successfully there needs to be analignmentofthefirm’scorporatestrategyanditscompetitiveadvantages(Švárová&Vrchota,2014).TheRBVcanbeseenasanantecedentofstrategicchoicessince itprovidesmanagersguidance inchoosingappropriatecorporateandbusinessstrategies(Bresser&Powalla,2012).Themainstrategicobjectiveof

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 2

RBVistoidentifywhichinternalresourcesandcapabilitiesthatmakeupthefirmscompetitiveadvantageinrelationtoitscompetitors,asabasisforstrategicanalysis(Prithwirajetal.,2010;Acostaetal.,2011;Barney,1991).Thisisan“inside-out”perspectivewheretheactivitiesthefirmcanperformareafunctionoftheopportunitiesitconfrontsand(moreimportantly)onwhatresourcestheorganizationcanmuster(Teece, 2007). As Grant (1991) argues; the resources and capabilities of the firm should be central tostrategyformulationsincetheyaresimultaneouslythesourceofthefirm’sidentityanditsprimarysourceofprofitability.ThislinkbetweenRBVandcompetitivestrategyissomethingthatseveralacademicshaveresearched and found empirical support for, suggesting that RBV can explain differences in firmperformancesandstrategies(Henderson&Venkatraman,1993;Mathews,2003;Jolly,2000)

However, the RBV has come under fire from academics as well as practitioners. One of the mainobjectionsfromacademialeveledatRBVisthatapplyingtheframeworkisapurelyexpostexercisethatdoesnot contribute toexplanationofhowa firmsSCA:sdevelop (Priem&Butler,2001).Asa resultofthis,thecriticsoftheRBVmakethepointthattheentireconceptistoostatictodeliverthecompetitiveadvantagethatitpurport(Kraaijenbrinketal.,2010).TherearealsoquestionsraisedaroundthelackofRBVframeworksthatcanbeappliedinaprescriptivemanner,mostlyduetoalowlevelofgeneralizabilitysincetheRBVisconcernedwithfindingtheuniqueassetsofthefirm(Priem&Butler,2001;Hinterhuber,2013; Eisenhardt & Martin, 2000). Despite the critique brought against the RBV, its contribution tomanagementresearchisundeniableasevidentfromitswidespreaddissemination(Acedoetal.,2006).IntheirreviewofthemainacademiccritiquebroughtagainsttheRBV,Kraaijenbrinketal (2010)concludethat the concepts stands up well to most of its attackers. Furthermore they state that RBV has thepotential to develop further by incorporating new conceptswith the aim to become amore completetheory.

Additionallythereisagapbetweenmanagementresearchandpractice,whichhasbeengrowingdespiteofmoreadvancedresearchmethodsbeingavailabletoday(Guo,2007).Thisisduetotheresearchresultsbeingdifficulttounderstandforpractitionersandthelackofactionablepracticalguidanceprovided(Ibid).Thiscritiqueisconsistentfrombothacademics(Hinterhuber,2013)andpractitioners(Guo,2007),whichleavesRBV ina situationwhere it isdifficult tooperationalize. Ina simulatedmodel testing ifRBV is apractical theory it is concluded that it has significant room for improvement and that future researchshould focus on how the practical applicability should be improved (Arend & Lévesque, 2010). Morespecifically RBV in practice has been shown to have difficulties in incorporating the competitiveenvironmentintheformofcompetitorsandcustomers(Knott,2009;Knott,2015),somethingwhichisanecessity within RBV (Barney, 2001; Grant, 1991). In order to bridge this divide between theory andpractice,researchersshouldfocusonoperationalizingRBVtoalargerextent(Hansenetal.,2004).

1.1 BackgroundBasedonthediscussionabovethereisaneedformorepracticalapplicationoftheRBVinreallifecontextinordertomakeitmoreusefulformanagersconsideringstrategicissues.Onesuchstrategicissuecouldbe a firm’s competitive strategy when expanding their presence in an attractive market. This is the

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 3

situationthatCompanyXisfacingastheyarecurrentlyintheveryearlystageofplanninghowtoexpandtheirfootprintontheUSmarket.

CompanyXprovidesvisualizationproductsfortherealestateindustrythatisusedtomarketpropertiesforsaleorforrentonline.Theyareworkingwithmanyofthe latesttechnologiessuchas3DanimationandVirtualReality (VR) andare todayactiveon several internationalmarkets.Due to their technologyintense product offering, new innovations occur constantly, both within the company and from othercompetitors within the industry. This makes strategic planning complicated as the competitiveenvironmentisunderconstantchangeandthetechnologydevelopmentisfast.CompanyXisafirmwithlongexperienceintherelativityyoungfieldofonlinevisualizationsolutionswithinrealestatemarketing.

The real estate industry can be divided into several sub-markets or segments according to differentcustomermarkets,productmarketsetc.Oneusefuldistinctionwhichcanbemadeinordertodividetheindustryintobroadsub-markets,isbydefiningitbyitsendcustomers.Forexampleonesub-marketcanservethe“renter”endcustomer,whileanothercouldservethe“buyer”endcustomer.Thesub-marketscan then be viewed as a vertical value chain that services different end customers and Company X´sinternal organization is set up in accordance to this distinction. Rather than referring to the differentsegmentsasverticalsub-marketsCompanyXsimplystatethattheyservicedistinct“verticals”withintherealestateindustryandthisterminologywillalsobeusedinthisthesis.Thisresearchprojectwillbesetwithin the context of the two verticalsRental andResale. The rental vertical consists of all propertiesrentedwiththeintentionofbeingtheprimaryresidenceoftherenter(whichexcludesalltypesofshortterm and vacation rentals). The resale vertical consists of existing single-family homes, townhouses,condosoranyothertypeofpropertythatisboughtandsoldwiththeintentionofbecomingaresidence.CompanyXcurrentlyhasasmallpresencewithintheRentalverticalwheretheyservicealownumberofcustomersthatgenerateslargesalesvolumes.ThecompanyisnotactivewithintheResaleverticalintheUSmarketbutthisisconsideredthecoreverticalintheScandinavianmarketswherethecompanyiswellestablished. These conditions result in Company X having accumulated a lot of knowledge as well asresources across different international markets. Now that the company is planning to expand theirpresenceintheUSmarket,theyneedtounderstandhowtheirexistingassetscanbeleveragedaswellasidentifyingwhatassetsthecompanyismissinginordertocompeteintheUSmarket.Thesefactorsallowforagoodopportunity topracticallyapply theconceptswithinRBV inorder tocomeupwithconcretestrategic recommendations for Company X, as well as contribute insight into the applicability of RBVconcepts.

1.2 ResearchProblemIn a dynamic environment the firm's internal assets becomes an obvious starting point when devisingcompetitivestrategies.Eventhoughthestartingpointisfocusedontheinternalenvironmentofthefirm,theexternalenvironmenthastobetakenintoaccount.TheRBVisatheoreticalapproachthataimstodojustthat.However,thepracticalapplicationoftheacademicconceptshasbeenproblematicformanagers

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 4

inareallifebusinesssettingduetothegapthatexistsbetweenmanagementresearchandpractice(Gou,2007).

CompanyXiscurrentlyinapositionwheretheyareevaluatingtheircompetitivestrategyinrelationtoaproposed, substantial expansion on the US market. The external environment of Company X can becharacterizedasdynamicwithnewcompetitorsaswellasproductsconstantlyemerging.Thus,CompanyXwants to investigate how their internal assets can be leveraged to expand their presence in the USmarket.

This setting provides a good research opportunity since it allows for the formulation of a competitivestrategythatisinfluencedbypreviousacademicresearchaswellasareallifestrategydevelopment.ThesituationallowsfortheexplorationofthepracticaloutcomeofoperationalizingtheRBVbypresentingthestrategicrecommendationsthetheorygenerateswhenappliedtothecaseofCompanyX.Italsoenablesreflection on the challenges of converting the theoretical concepts into a real life setting. ThesereflectionscancontributetowardsdevelopingtheRBVintoamoreusefultoolforpractitioners.

1.3 ResearchPurposeThe purpose of this thesis is at its core to reflect on the practical application of the RBV in a real lifestrategic setting to highlight what potential challenges practitioners face when attempting tooperationalizethetheory.Ashaspreviouslybeenestablishedbyseveralauthors,thereisagapbetweenresearchandpractice.ThusbyreflectingonthestrategyformulationprocessthroughthelensoftheRBVthisapproachwillprovidevaluableexanteawarenessforpractitionersaswellaspracticalguidelinesforthe application of RBV-frameworks. Since this thesis has a strong emphasis on theory in practice thesituationCompanyXfindsthemselvesinpresentsagoodsettingtoapplytheRBVonarealstrategicissue,namelyaproposedexpansionintheUSmarket.ThepurposeofthisthesisthusencapsulatestheactualformulationofaproposedexpansionstrategyforCompanyX,theprocessofwhichwillbetheobjectofpracticalreflection.PutadifferentwaythepurposeofthisthesishasaclearpracticalcomponentintheactualstrategyforCompanyXaswellasatheoreticalcomponentintheformofthereflectiveapproachontheoryaspractice.

1.4 ResearchQuestionsRQ1:WhatarethechallengesofapplyingtheResourceBasedViewinpracticewhenformulatingafirm’sexpansionstrategy?

The first researchquestion is reflectiveon thepracticalapplicationof theResourceBasedView,and inCompany X an exciting opportunity to study the contemporary application of the theory has beenpresented.Inordertoanswerthefirstresearchquestionthefollowing,secondquestionisformulated:

RQ2:WhatcouldbeasuitableexpansionstrategyforCompanyXwithintheRentalverticalandtheResaleverticalontheUSmarketwhenapplyingtheResourceBasedView?

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 5

2. MethodologyIn thissection followsadescriptionaswellasamotivationof themethodologychosen,whichhasbeenusedtotackletheresearchproblemandanswertheresearchquestions.

Inorder toanswerthe first researchquestion,whichrefers tothepracticaluseof theRBV,areflectiveapproachhasbeenchosenwhereaspecificcasewillbetheunitofobservation.Thisisasimilarapproachto theoneusedby Suomala et al (2014)where theydescribe their research ashaving two layers, oneunderlying case study previously performed by one of the authors and a second reflective layer. Theresearchers theoretical knowledgeallowed themto reflectupon thepracticalapplicationof theoreticalconcepts,which enabled them to identify challenges in turning theory intopractice. This is also in linewith another studywith a similar approachwhere the authors present their thoughts basedon logicalargumentationderivedfromacademic literature (Fogarty&Rigsby,2005).Sincethisapproach is relianton experience and insight into applying theoretical concepts in a real context the authors choose toperformanactualcasestudywheretheRBVwasappliedtothecontextofCompanyX.TheapplicationoftheRBVinthissettingisasubstantialundertakingandisthusreflectedinthesecondresearchquestion,which ismorerelatedtotheactualcase.Asaresult this thesishasasimilarapproachtoSuomalaetal(2014)withtwolayersbutwiththeaddedfeatureofthecasestudybeingperformedconcurrently.

WhenapplyingtheRBVtosuchapracticalsetting,theauthorsdeemeditnecessarytoinvolvesomeotherconcepts referring to the external environment. This resulted in an analytical model that guided theempirical data collection as well as the analysis of case company and its environment. Based on theempirical findings and the subsequent analysis the second research question is answered by providingconcretestrategicrecommendationonhowCompanyXcanapproachtheirproposedmarketexpansion.Theentireprocessofconductingtheliteraturereview,datacollectionandanalysisprovidestheauthorswiththenecessarytheoreticalknowledgeandpracticalexperiencetoanswerthefirstresearchquestion.

2.1 ResearchStrategyWhenconductingresearch,itisimportanttohaveaclearstrategyforhowtheresearchshouldbecarriedout andwhat approach to use. According to Bryman and Bell (2011) there are twomain strategies toconsider,namelyquantitativeversusqualitativestrategy,andthedistinctionbetweenthetwofallsmainlyin three areas: the role of theory in relation to research, epistemological orientation, and ontologicalorientation.Aquantitativestudycanbrieflybedescribedasastudyprimarilybasedonquantificationofthe research objectwhere the role of theory is primarily deductive (testing of theory), andwhere theepistemological orientation is based on positivism (a model closely related to natural science).Furthermore theontological orientationof a quantitative study is in general objectivism,which canbeexplainedassocialphenomenathatareindependentfromsocialactors.Aqualitativestudyontheotherhand often hasmore of an inductive approach, where the objective is to generate a theory from theresearch rather than testing an existing theory. Furthermore, the epistemological orientation of aqualitative study is often interpretivism, and thus this favor a distinction between natural science andsocial science as there is supposed to be a subjective meaning of social subjects. The ontological

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 6

orientation of a qualitative study is described as constructionism,where there is an awareness of theresearcher’sownagendaandthattheresearcherinterpretstherealityinawaythatcannotbedefinedasdefinitive.(Bryman&Bell,2011)

Theresearchstrategyforthisthesisisbasedonaqualitativeapproach,firstofallbecausetheintentionistogenerate strategic recommendations,basedonexisting theory, forhowCompanyX could formulatetheirexpansionstrategyon theUSmarket; the thesiswill thus followan inductiveapproach to theory.Furthermore,theauthorsareawareofthesubjectivecontextofthisresearchareawhereitisdifficulttoobtain reliablequantitativedata that canbeeasilyanalyzed; insteada largeamountof secondarydatahavebeencollectedandhadtobeinterpretedintoasocialcontext.EvenifthegoalistogainadefinitiveassessmentofCompany’sXresourcesandcapabilitiesthatcanbethebasefortheproposedstrategy,thecapabilitiesareofsuchnaturethattheyneedtobeinterpretedandvaluatedintoacontextofthemarketandcompetitors.Thereforetheresultofthestudyisdependentupontheauthor’sinterpretationofthoseresources and capabilities, and this assessment cannot be completely objective, instead it was moreconstructive.

Asthepurposeofthisresearchistoexploreandevaluatetheapplicationoftheoryinapracticalsetting,aqualitativestrategywasmostappropriateasitallowsforafocusonwordsratherthanquantificationofdata.Furthermore,theaimistocontributetothegenerationofatheoryregardingtheapplicabilityoftheresource based view and also to generate a theory for howCompanyX can formulate their expansionstrategy.Forthisreason,there isnosuitablehypothesisthatcanbetestedandthisfavorsaqualitativeapproach. Even if thegoal is to gainadefinitiveassessmentofCompanyX’s resources and capabilitiesthatcanbethebasefortheproposedstrategy,thecapabilitiesareofsuchnaturethattheyneedtobeinterpretedandevaluatedintoacontextofthemarketandcompetitors.ToassesstheapplicabilityoftheRBV in a practical setting, the authors reflect upon the benefits and challenges of the concept. Thisfollows an epistemological approach of interpretivism, as the authors interpret the human action ofapplyingtheRBV.Thereflectionishighlydependentupontheauthor'sownunderstandingofthetheoryaswell as theempirical findingsand the subsequentanalysis. The reflection is thus constructive ratherthanobjective

2.2 LiteratureReviewTheliteraturereviewisoftenthestartingpointforaresearchprojectandso ithasbeenforthisthesis.Whendecidingonwhat typeof literature review to conduct, relevance shouldbe given to the specificresearchproblem.Therearemainlytwobroadoptionstoconsiderwhendoingthe literaturereview,tohaveasystematicrevieworusethenarrativeapproach.Thesystematicreviewissupposedtogenerateareplicable, scientific and transparent process which should generate an unbiased and comprehensivereviewofexisting researchwithin the chosen field.However, thisprocess isoften time-consumingandcouldbe toobureaucraticwhere the focus tends tobe toomuchon the technicalaspectsof thestudyratherthanontheanalyticalinterpretationoftheresult.Anarrativeapproachtotheliteraturereviewisoftenmoresuitablewhentheresearchstrategyisofqualitativenatureandthedominantepistemological

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 7

orientation is interpretivism,where theobjectivewith the literaturereview is togainanunderstandingfor the topic, rather than finding exactly everything written about the topic. Furthermore, when theresearchisconductedwithaninductiveapproachfortherelationshipbetweenresearchandtheory,thenarrativeapproachismoresuitable,asinthiscasetheoryisseenastheoutcomeratherthanthestartingpoint. A narrative approach allows for studies of a broader subject where the rules for inclusion andexclusionofrelevantliteraturearelessexplicit.(Bryman&Bell,2011)

TheliteraturereviewforthisthesiswasaimedatenrichingtheauthorsunderstandingoftheRBVandthetheory’sroleintheareaofbusinessstrategy.Whenanunderstandingfortheconceptwasreached,theauthorsstartedtoexploreitspracticalapplicationsaswellasrelatedframeworksfortheanalysisoftheexternalenvironment.Forthisreason,theliteraturereviewisbasedonanarrativeapproachwheretheauthorsstartedtoexploretheRBVbutthenallowedtheempiricaldatatoguidefurtherexpansionofthetheoreticalbasisofthethesis.Thus,thetheoreticalbaseofthetheorywasallowedtoguidetheempiricaldatacollectionwhichinturnwasusedtoexpandthetheoreticalbasefurther.Therelationshipbetweentheory and research in this thesis is based on an inductive approach where the researcher strive toformulateatheory,ratherthantotestanexistingone,andthusthenarrativeapproachismoresuitable.Thenarrative approach is also in linewith thedesiredqualitative research strategywith interpretativeorientation.

TheRBVistodayahighlyexploredconceptthathasbeenstudiedforatleast25yearsandhasgeneratedalargenumberofarticlesandresearchpapers.Furthermore,someareasneededtobestudiedinmoredetailwhere the literature contributedwith practical guidance, and thus, topics not directly related toRBV are included in the theoretical framework. This broad scope of researchwas an additional factormakingasystematicapproachunsuitable.Themaincritiquetowardsthenarrativeapproachreferstothelackofreplicability,asthesearchforliteraturecanbedescribedasexplorativeratherthansystematicandit is thus not suitable to generate generalizable results (Bryman& Bell, 2011). However, this researchprojectdoesnotaimtoaccumulateknowledgebyaddingnewconceptstothetheory;rathertheresearchaimstogenerateabetterunderstandingofanestablishedtheorywhenusedinpractice.

2.3 ResearchDesignTheobjectivewiththisthesisistoincreasetheunderstandingfortheuseoftheRBVinpracticewhenafirm formulatesa strategy formarketexpansion.Thisentails consideringboth internal resourcesat thefirmaswellasthemarketcontext.Forthisreasonacasestudyisamostsuitableresearchdesignasitcanbeusedtounderstandtheparticularitiesofasituation(Bryman&Bell,2011).

Whendetermining if a case study is a suitable researchdesign three criteria shouldbe fulfilled; 1) theresearchquestionsshouldbeconcernedwithhoworwhyaphenomenonoccurs,2)thestudyshouldnotrequire the researcher to have control of behavioral events, 3) the research should focus oncontemporaryevents(Yin,2009).Inthisthesis,areflectionismadeonthepracticaluseoftheRBVwhenappliedonacasethataimstoansweraresearchquestionthat isconcernedwithhowastrategycouldlook like when using existing theories. Furthermore, the research is not conducted in a controlled

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 8

environment but in a real world context and it covers a contemporary event that is unfolding as theresearch takesplace.CompanyX,which is the selectedcase in this thesis,provided theauthorswithafitting context in which to investigate the research question. The company is currently considering anaggressiveexpansionofitsservicesonaglobalscaleandarethusactivelyconsideringthefundamentalsofcompetitivestrategy,namelywhereandhowtocompete.Bothofthesekeyquestionsarestillanopentopic of consideration and the top management within Company X is looking for strategicrecommendationsbasedonsolidacademictheoriesandmarketdata.

Thenature of the researchproblem is to understand a particular applicationof a theory in relation topractice and thus a case study is suitable as it helps to offer concrete context dependent knowledge,ratherthangeneralizabletheoriesonahigherlevelofabstraction(Flyvbjerg,2006).Furthermore,acasestudy is suitablewhen the predominate research strategy is qualitativewith an inductive approach totheory(Bryman&Bell,2011),suchasthisthesis.Inordertostudysociallycomplexissuescasestudiesareappropriatesince this is theirmainobjective (Yin,2009). Inaddition to thisacasestudycanbeagoodapproachtoexploringexisting theoryandallowtheresearcher tochallenge itaswellassuggest futureresearchdirections(Saundersetal.,2007).ThecasewillfocusonasingleorganizationandisselectedinaccordancetoBryman&Bell (2011)assertionthattheselectedcaseshouldbechosenbasedonwheretheresearcherexpectthelearningwillbethegreatest.

Oneofthemostcommoncritiquestowardstheuseofcasestudiesisthelackofgeneralizabilitythatthedesignoffers.Thatasinglecasecouldnotbegeneralizabletoalargeamountoffirmsisdifficulttoargueagainst,butthisdoesnotmeanthattheuseofcasestudiesshouldberejected.AsBrymanandBell(2011)argues,casestudiesofferauniqueopportunitytostudyaphenomenon indetailandthushelpwithanunderstandingof the complexityof the reality.Case studiesarealsousable for researchers toproducestudiesofrelevanceforpractitionersandtoavoidresearchthatisunclearanduntested(Flyvbjerg,2006).ThisisparticularlyrelevantinthisthesisasseveralauthorshavehighlightedthedifficultiesinpracticallyapplyingconceptswithinRBV.Withthehelpofcasestudies,researchcanvisualizethetheoryandshowwhy certain concepts are of importance and how ideas can be implemented (Siggelkow, 2007). Theseassertionsare in linewith theobjective for this thesis, toshowhowthe ideasof theRBVandadjacenttheoriescanbeputintopracticeandserveasguidanceforstrategyformulation.

2.4 DatacollectionandanalysisThe broad scope of this thesis requires several methods for data collection. The primary data wascollected through interviews and secondary data was gathered from academic literature, statisticaldatabases, industryreportsaswellas internaldocumentsatCompanyX.AsthisthesiswasproducedincollaborationwithCompanyX,theauthorshadgoodaccesstokeypersonnelwithinthecompanyandforthis reason interviewswere used formapping out the different resources and capabilities of the firm.Whenlookingatthemarketthatexistsoutsidethefirm,firsthanddatacollectionprovedmoredifficulttoobtainmainlyduetotworeasons: lackofcontacts in themarketsandthegeographicaldistancetothemarket(themajorityoftheresearchwasconductedfromSweden,whilethemarketofinterestisinNorth

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 9

America). For this reason, the primary information regarding the market was largely obtained fromsecondarysourcessuchasgovernmentproducedstatistics, industryreportsfromcommercialconsultingfirms and member surveys from industry organizations. However, several interviews in a variety offormatswereeventuallyconductedwithdifferentactorsintheUSmarket.

Qualitative data is very content rich and it is thus less straightforward to analyze compared toquantitative data, but it is recommended to have some kind of structure when dealing with the data(Bryman & Bell, 2011). A common approach when dealing with qualitative data is the concept ofgroundedtheory,which isacomprehensiveframeworkforbothcollectingandanalyzingdata(Glaser&Strauss,2008).Thisstudyisnotextensiveenoughtoincludeallstepsoftheframework,forexamplethereis no ability to test the developed theories and hypothesiswithin the given time frame. However, themajor tools of grounded theory have been used which includes theoretical sampling, coding andtheoreticalsaturation.

Theoreticalsamplingreferstothecollection,coding,andanalyzingofthedatawhichcanbedescribedasan iterative process where the phases occur in tandem (Glaser & Strauss, 2008). From this a theoryemerges,whichcontrolsthefurthercollectionofdata.Coding isoneofthekeyprocessesandreferstothe breakdown of data into component parts. Coding provides the analyst with a formal system toorganizethedatawhichhelpstouncoverlinkswithinandbetweenconcepts(Bradleyetal.,2007).Asthecollectionofdataandthecodingofthedataisaniterativeprocess,theoreticalsaturationreferstoastatewhere there is no point in collection of more data to illuminate further concepts and no point inadditionalcodingtofitwiththeconceptsorcategories(Glaser&Strauss,2008).

2.4.1 InternalDataThisresearchprojectstartedwiththeauthorsgettinganoverviewoftheconceptsoftheRBVbeforethedatacollectionprocessbegun.ThedatacollectionstartedwhenrepresentativesfromCompanyXwhereinterviewed about internal resources and capabilities. The authors possessed little knowledge of thecompanybeforehandandthusunstructuredinterviewswerechosentolettheintervieweesfreelyexplaintheirwork and their departments.Unstructured interviewsdonot followany interviewguides, insteadoneorafewquestionsareaskedwheretheresearchermakessurecertaintopicsarecoveredduringtheconversation(Bryman&Bell,2011).Basedontheinterviews,therespondents’answerswherecodedindifferentcategoriessuchaswhatwasconsideredasfactandwhatwasconsideredassubjectiveopinionsoftherespondent.Thecompany’sassetswherecodedintocategoriesofresourcesandcapabilities.ThishelpedtheauthorstogainfurtherunderstandingforhowtheRBVcouldbeusedtodeveloptheoreticallysound recommendations forhowCompanyXcouldexpand in theUSmarket,which in turnguided thecollection ofmore data about themarket. During the data collection process it became apparent thatadditionalresources,currentlynotpartofCompanyX’sassetsstock,mightbeneededtocompeteonthemarket, why collection of data and theories regarding acquisition and accumulation of additionalresourceswhere added. In termsof saturation, the interviews conductedwithinCompanyX reached asaturationpointfairlyearlyintheresearchprocess.Theauthorschosetoperformtheinterviewsduring

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 10

the time spent on site at the company’s headquarters. The numerous interviews with differentdepartmentswithintheorganizationweresupplementedafterwardsbyfollowupinterviewswiththetwomain supervisors at the company, working at the top management and senior management levelrespectively. This was done in order to ensure that the authors had not misunderstood how thecompany’s resourcesandcapabilitiesweresetup,somethingwhichboththesupervisorshadextensiveknowledgeabout.Aftertheinitialmeetingwithindividualdepartmentmanagers,withtheadditionofthefollowupmeetingstheauthorsfeelconfidentthatthesaturationpointhasbeenreached.

2.4.2 CustomersSecondarydataaboutcustomerswasretrievedfromdifferentindustryorganizationsuchasNAR(NationalAssociation of Realtors), the National Multifamily Housing Council (NMHC), National ApartmentAssociation(NAA),andNationalAssociationofResidentialPropertyManagers(NARPM).Thishelpedwithanunderstandingfordifferenttypesofcustomersfromahighlevelapproach.RespondentsfromNMHCand NAA were also interviewed through e-mail. Industry reports from IBISWorld contributed withinformation as a secondary data source. Information regarding portals and Software as a Serviceproviderswasretrievedthroughbrowsingthewebsiteofeachportal/firm.

In order to get a more granular breakdown of customers, with the ambition to find personalcharacteristics of different segment of customers, first hand data was needed. When interviewingindustry participants in the US, both the geographical distance and time-zone differences madeconventional interviews problematic and thus alternative interview approaches were used in order tocollect necessary data. Interviewing by e-mail is an approach that can be used when there is a longdistancebetweentheinterviewerandtheinterviewee,anditallowstherespondentstoansweratatimeand space that suits them, ultimately resulting in richer stories (James&Busher, 2006). Even if e-mailinterviewslacksthesocialgesturesthatisanessentialpartoffacetofaceinterviews,theinterviewsdonethrough e-mail have other benefits such as the ability to review andmodify the questions during theinterviewprocess(Reidetal.,2008).Anotherapproachistouseself-completingquestionerswhichcanbecheaperandquickertoadministratecomparedtoconventionalinterviews.Thisisalsoanapproachthatcan be more convenient for respondents as they can answer when it suits them and the risk forinterviewervariabilityisnon-existing(Bryman&Bell,2011).Thedatacollectionfromindustryparticipantswasconductedbyamixbetweene-mailinterviewsandself-completingquestionnaires.Onedisadvantagewithself-completingquestionnairesisthatthenumberofopenquestionusuallyneedstobeverylimitedsincerespondentsgenerallydon’tliketowritetoolonganswers(Bryman&Bell,2011).Becauseofthis,questionnairesthat includedapproximatelythreetofivequestionstorelevant industryparticipantswassent via email as a way to open a dialogue. Then follow-up questions were sent to those industryparticipants that indicated a willingness to participate, turning the initial questionnaire into e-mailinterviews.Oneofthedisadvantageswiththesekindsofmethodsistheuncertaintytoknowwhoactuallyanswersthequestions (Bryman&Bell,2011;Reidetal.,2008). Ina few instancesCompanyXprovidedthe authors with appropriate contacts but the majority of the interviewees where obtained by theauthors.

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 11

Fortheinterviewsthatwereconductedoutsideofthecompanywithrepresentativesfromthecustomermarket, the authors cannot claim to have reached a fully satisfactory saturation point. Given the verylargepopulationthecustomermarketsrepresentsthisisnotsurprising.Inordertoincreasethecredibilityof the first handdata collected from themarket itwas continuously compared to secondary statisticalinformationfoundinindustryreports,industrysurveysandgovernmentstatisticaldatabases.Theauthorsarguethatthecombinationoffirsthandandsecondhanddatawhichpointtosimilarconclusionheightenthevalueofthecustomermarketdata.

2.4.3 CompetitorsInformation regarding competitorswas collectedmainly through secondary data sources. According toBrymanandBell(2011)someoftheadvantagesofusingsecondarydataarethatitsavestimeandcosts,theabilitytogethighqualitydatathatspansacrosslargegeographicalareasandlargesamplesize,andthattheresearchersgetmoretimefordataanalysis.However,therearenotonlyadvantageswiththeuseof secondary data, and the researcher must be aware of some of the disadvantages when doing so.According toBrymanandBell (2011) somedisadvantageswith theuseof secondarydata is the lackoffamiliaritywith thedata (takes time to get sufficient familiarity tomake a correct analysis), difficult tocontrolthequalityofdata,andsometimesthesecondarydatamight lacksomeofthekeyvariables.Asdescribed earlier, the difficulties in obtaining first handdata and the limited time frame for this thesisforcestheauthorstorelyonsecondarydataforsomepartsofthisresearch,particularlypertainingtotheexternalenvironmentanalysis.Asthesecondarydatawasgatheredfromavarietyofsourcesthere isaneed for interpretationof thedata so that it couldhelp toanswer the researchquestion.However, toensurerightinterpretationweremadetheauthorsalways,totheextentitwaspossible,soughttoverifythesecondarydatabycomparingitwiththeinsightsgatheredfromthefirsthandinterviews.

The data collection regarding competitors began with a list being retrieved from Company X with allcompetitorsthefirmwasawareof,althoughtheyhadatthatpointnotbeenproperlyanalyzed.ThiswascomplimentedbyaGooglesearchbasedonkey-wordssuchas“floorplans”“floorplancreation”,“onlinerealestatemarketing”,“realestatephotography”and“visualcontentrealestate”.Informationregardingproductofferings,coverageandmarketpricewasretrievedbybrowsingeachcompetitorswebsite.Thisinformationwascodedandcategorized intosuitablecategories.Competitorswere labeledaccordingtoproductofferings,priceandwhethertheypossessedfirst-handinputgatheringcapabilities.Asthisthesisfollowsagroundedtheoryapproach,wherethecollectionofdataandanalysiswasaniterativeprocess,theanalysisrevealedwhatadditionaldatatocollect.Forexampletheanalysisrevealedtheimportanceofaccesstoaphoto-networkandthusinformationregardingcompetitorsthatcontrolledaphoto-networkwhereidentifiedandcodedaccordingly.

2.5 SamplingThere are twomain types of sampling techniques available for researchers; probability/representativesample or non-probability/judgment sample. For research with a quantitative research strategy arepresentativesampleisrequiredinordertobeabletomakestatisticalinferencesaboutthepopulation.

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 12

Inqualitativeresearchandinparticularwithacasestudydesignajudgmentsampleismostoftenutilizedsince the objective and research question is seldom meant to be generalizable across a population(Saundersetal.,2007).Samplinginqualitativestudiesismostoftenconcernedwithhowtheintervieweeswereselected(Bryman&Bell,2011)Howeveritisanoftencitedcritiqueagainstqualitativestudiesthatthey are not transparent enough when it comes to the selection criteria and even the number ofinterviewsthatwereconducted(Ibid).

InthisthesisanumberofinterviewswereconductedbothinsidetheCompanyX(internal)aswellaswithdifferent respondents within each vertical (external) in the USmarket. For the internal interviews theselectionofintervieweeswasguidedbyourtheoreticalfoundationwithintheRBV.TheobjectivewastoidentifyCompanyX’sinternalresourcesandcapabilities.Inordertodoso,accesstobothtopandmiddlemanagersacrossallofthemajorpartsoftheorganizationwasdeemednecessary.Talkingtolowerlevelemployees was ruled out based on two reasons; firstly there was a considerable language barrierbetweentheresearchersandthelocalworkerswhichwouldhaverequiredatranslatortobepresent(Theauthors do not speak Thai), secondly the researchers judged the identification of resources andcapabilitiesassomethingrequiringalevelofoverviewoverinternalprocesses,whichismorelikelyfoundatamanagement level.This resulted in three interviewsconductedwithtopmanagers, four interviewswithseniormanagersaswellaseleveninterviewswithmiddlemanagers.Thislargesampleofmanagersat different vertical and horizontal levels of the organization provided the researchers with a goodunderstandingofthecompaniesresourcesandcapabilities.

Theexternalinterviewswereconductedwithineachofthetwoverticalsrentalandresale.Secondarydatacollection acted as a guide to identify potential customer segments within each vertical, which wassubsequently followed by the authors contacting a number of actors within each segment. For thesesegments of customers a purposive sample was chosen, which means that the interviewees whereselectedinastrategicwaysincetheyweredeemedtoberelevantinprovidingtheresearcherswithdatathatcouldhelprealizetheresearchobjective (Bryman&Bell,2011). Inordertogetrelevantdata fromthesesegmentstheintervieweewouldneedtobeapersonthatdecideswhethertopurchaseand/orpaysforproducts liketheonesCompanyXprovidesorhaverelevant insight intothemarketingstrategiesofthecompanytheyrepresent. Intotalfourdistinctcustomersegmentswereidentifiedwitheachverticalcontaining two each. In the rental vertical the potential customers are property managers and onlinerental portals. In the resale vertical the potential customers are real estate agents and online resaleportals.AcompletelistoftheinterviewsconductedcanbefoundinAppendix1.

2.6 CredibilityoftheresearchInordertojustifythecredibilityofanyacademicresearchendeavorthestudyneedstobeofgoodquality.The quality of academic research methodology is commonly measured by the criteria of validity andreliability. These concepts are lifted from qualitative research and as a consequence they are notstraightforwardtoapplyinaqualitativestudy.Thereforemanywritersarguethattheseconceptsshould

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 13

notbeappliedtoqualitativestudiesatallwhileothermaintainthattheyneedtobemodifiedinordertobemoreapplicable(Bryman&Bell,2011).

Validity is a concept used to argue for if a research project has actually investigated the intendedphenomenon as specified by the research question (Bryman & Bell, 2011). It is argued that internalvalidity is a particular strength of quantitative studies since it can allow the researcher to have aprolonged presence within the social context of the phenomenon being studied (Ibid). Thus theresearcher will be better equipped to interpret how the context can and cannot be examined bytheoretical concepts. In this research the authors spent two weeks at Company X’s headquarters inBangkok with direct access to members of all levels within the organization. This allowed for a deepunderstandingofhowCompanyXbusinessmodelissetupandhowtheorganizationisbuilttorealizethismodel. This knowledge allowed the researchers to apply the concepts within the RBV, especially theidentificationofresourcesandcapabilities,withmorecredibility. Inadditiontothis,therepresentativesfromwithinCompanyXweregiventheopportunitytoprovidefeedbackregardingthe interpretationoftheir internal organization throughout this research project. Thus ensuring the researchers did notmisrepresent any factual elements of the organization. For all interviews that were conducted withsubjects outside of Company X a briefmemowas sent out beforehand, detailing the objective of theresearchaswellasdefinitionsofkeyconceptstobecoveredduringtheinterview.Thiswasdoneinorderto let the interviewee get a better understanding of the direction of the research to ensure that bothparties were on the same pages throughout the interview.When it comes to the concept of externalreliability,whichistheextenttheresearchcanbegeneralizedacrossothersettings,thecasestudydesignis considered week because of the highly context specific nature of the research. However since thisconceptisliftedfromschoolofquantitativeresearchitismeanttoprovidestatisticalgeneralizability(Yin,2009).This isnottheintentionofqualitativeresearch,whichisfocusedonanalyticalgeneralization, i.e.wherepreviouslydevelopedtheoriesarethetemplateofwhichtheresultscanbepotentiallygeneralized(Ibid).

The other main criteria, reliability, is concerned with if the case study is replicable, i.e. if the sameresearchapproachwasusedagain,wouldthefindingsbeconsistentwiththefirststudy.Thisissomethingthatisoftenaprobleminthecasestudydesignsinceitisbyitsverynatureverycontextspecific(Bryman& Bell, 2011). This problem can be confronted by making the steps taken during the research astransparent as possible (Yin, 2009). As a result the authors was very conscious to take down detailednotes during all conducted unstructured interviews within Company X and write summaries of theconversationassoonaspossibleafterthe interviewconcluded.Fortheemail interviewsthatwereheldwith stakeholders in the external environment an interview guidewas developed andutilized for eachtype of stakeholder. The stakeholders were differentiated depending on which type of company theywereaffiliatedwith.

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 14

3. TheoreticalFrameworkThissectionwillpresentthebasictenantsoftheResourceBasedViewstartingwithabriefoverviewofitsrisetoprominenceduringthe1990s.FurthermorethereviewwillcoverareasadjacenttotheRBV,namelyin theexplorationof competitorsandcustomerswhich the internal resourcesandcapabilitieshas tobeput in relation to. The sectionendswithhighlighting the importanceof evaluateexisting resourcesandfillingresourcegaps.

3.1 InternalPerspectiveTheinternalperspectivesectionofthischapterprimarilycoversthetheoreticalfoundationofthisthesisbypresentingtheResourceBasedViewanditsapplicabilityinstrategicanalysis.TheRBVhasaninternalperspectiveinthatthefirmsstockofresourcesandcapabilitiesshouldguidestrategicchoicesbutaswillbecomeevidentinthenextsectiontheexternalperspectiveisalsoanintegralpartofRBV.

3.1.1 TheResourceBasedViewThemodernversionofRBVwasinitiatedin1984whenBirgerWernerfeltpublished“TheResourceBasedViewof the Firm”wherehe sought tohighlight the importanceof the firm’s internal resources, ratherthanprevailingmarketconditions,whenfirmsformulatetheirstrategy.JayBarney(1991)madethefirstattempttoformalizethetheorybydefiningitskeyassumptions;firmsareheterogeneousintermsoftheirresourcesandcapabilitiesandthatthesecannotbeeasilytransferredbetweenfirms.Barney(1991)alsoprovidedthedefinitionoftheresourcesandcapabilitiesthatmakeupthefirmssustainablecompetitiveadvantage (SCA) and thus should be the basis for the competitive strategy. These resources andcapabilitieswouldhavetoberare,valuable,imperfectlyimitableandnon-substitutable.ThediffusionoftheRBVwithinstrategicmanagementhasbeenverybroadsinceitsinceptionduetomanyfactorssuchasitscompatibilitywithexistingtheoriesanditsintuitivelysoundpremise(Peng,2001).ThisallowstheRBVtoactasacomplimenttoothereconomictheoriesratherthantryingtoreplacethem(Peteraf&Barney,2003).

Thebasicideaofthisconceptistoidentifyafirm’sresourcesandcapabilitiesthatbythemselves,ormorecommonly,bundledtogethermakeupthefirm’ssustainablecompetitiveadvantageandbasedonthesedecidewhereandhowtocompete(Teeceetal.,1997;Bloodgood,2014).However, it isnotpossibletodetermineasetofresourcewhichprovidesuniversalSCA:sforeveryfirmasresourcesarecontextspecific(Barney,2001;Wernerfelt,2014).Firmsmustfirstdeterminethevalueofaresourceinaspecificmarketcontextandthenapplyresourcebasedlogictodetermineiftheresourcecanbeasourceofsustainablecompetitiveadvantageinthatspecificcontext(Barney,2001).

InordertoqualifyasanSCAtheseresourcesandcapabilitiesneedtomeetfourwell-establishedcriteria.They need to be valuable, rare, imperfectly imitable and non-substitutable; these criteria are oftenreferred to as the VRIN framework (Barney, 1991). Barney was clearly influenced by Dierickx & Cool(1989) when he specified these conditions based on the pairs assertion that the firm’s assets stock isstrategic to the extent that they are non-tradable, imperfectly imitable and non-substitutable. The

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 15

objectivethenbecomestoidentifytheinternalassetsthatactuallyfulfillalloftheseSCAcriteria.Barney(1991) defined them as follows: a resource is valuable if it can be utilized to improve efficiency andeffectiveness, or put another way; it must exploit an opportunity or neutralize a threat in the firm’senvironment(ThisshowsthateventheearlyresearchofRBVrecognizedtheimportanceofincorporatingtheexternalenvironment).Aresource is rarewhen it isnotpossessedbyanycompeting firmorat thevery least, only a few of competing firms. A resource is imperfectly imitablewhen it is impossible, orsubstantiallydifficultforcompetitorstoreplicate.Andfinally,aresourceisnon-substitutablewhentherearenootherassetsthatcanfulfillthesame,orsimilarstrategicvalue.

EventhoughthesecriteriawereestablishedintheearlydaysoftheRBVtheystillmakeuptheessenceofhowresearchersidentifySCA:swhenanalyzingthedifferencesinperformanceofcompetingfirms(Acostaetal.,2011;Lockettetal.,2009;Newbert,2007).OneofthemaincritiquesoftheRBVraisedearlywasthat it is a static setof criteria that resulted ina static setof SCA:s thatdonot sufficientlyexplain thedifferences in firmperformance (Newbert, 2007;Kraaijenbrinket al., 2010). Inotherwords, theRBV isstatic in that it doesnotpresent any conceptualmodelof how (Mohamad&Norezam,2012)orwhen(Kraaijenbrink et al., 2010) resources and capabilities are developed or how they can be utilized. ThisaccusationhassparkedareactionwithinRBVthatleadtoJayBarneytoadjusthisVRINframeworkslightlytobecomeVRIO(Kozlenkovaetal.,2014).The“O”standsforOrganizationanditisanecessaryconditionin order to realize the value of identified resources and capabilities, thus turning them into SCA:s. If aresourceorcapabilityisdeemedtobevaluable,rareandimperfectlyimitablethecompanyneedstobeset up to take advantage of them. These organizational capabilities can include things like reportingstructure and management control systems that act as support vehicles for successful exploitation ofinternalresourcesandcapabilities(Barney&Delwyn,2007).

Figure1:TherelationshipbetweenCoreAssumptions-VRIOFramework-SustainableCompetitiveAdvantage.Source:Barney&Delwyn(2007)

It isworthwhile to look a bit closer on the imperfect imitability criterion. If a resource or capability isconsideredtobevaluableandrare,RBVclassifiesitasacompetitiveadvantage(Barney&Delwyn,2007;Knott,2009;Hua-Lingetal.,2012).Thesustainabilityaspectofthecompetitiveadvantageisdeterminedby the third criterion, imperfect imitability, which Barney (2007) defines as “resources that firms notpossessingthemcanobtainthroughdirectduplicationorsubstitution.”Aresourcecanbeconsideredtobeimperfectly imitableifoneormoreofthefollowingthreeconditionsapplytoit;1)theresourcewas

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 16

developed due to unique historical conditions, 2) there is a degree of causal ambiguity in the firmscompetitive advantage i.e. the link between the firms resources and its superior performance is notunderstoodoronlypartiallyunderstood,3)whenthecompetitiveadvantageofafirmissociallycomplexitbecomeshardtoimitatewithcustomerrelationships,companycultureandinterpersonalrelationshipsbetweenmanagersbeinggoodexamples(Barney&Delwyn,2007).

ThisreworkedframeworkstillleavestheRBVopentoothercriticisms.OneofthemainobjectionsleveledisthatapplyingtheframeworkisapurelyexpostexercisethatdoesnotcontributetoneitherexplanationorpredictionofhowSCA:sdevelop(Priem&Butler,2001;Hinterhuber,2013;Eisenhardt&Martin,2000).However,thereisotherresearchthatdisagreeswiththistypeofcriticismandconsidersRBVandtheVRIOframeworkagoodstrategicdecisionmakingtool.OnesuchstudyconductedbyBresser&Powalla(2012)predictsthestockmarketperformanceofdifferentcompaniesusingVRIOandcomparestheframeworkwithtwoalternativedecisionmakingheuristics.TheyconcludethattheVRIOframeworkwassuperiorinpredicting performance of the companies in the study, which infers that the VRIO framework is apowerfultoolwhenconceivingstrategicactions.

3.1.2 RBV–APracticalFrameworkOneofthefirstscholarstodeveloptheRBVconcept intoapracticalstrategyframeworkwasRobertM.Grant(1991).EvenifsomenewdimensionshavebeenaddedtotheRBVconcept,theframeworkcanstillcontributetoapracticalunderstandingforhowtousetheconcept.Hereafterfollowsabriefintroductiontothemodel:

Figure2:TheRBVapproachtostrategyformulation.AdaptedfromGrant(1991)

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 17

Grant(1991)arguesthatasafirm’sresourcesandcapabilitiesshouldbethebasisforafirm’slongtermstrategy,identifyingitsresourcesistheappropriatestartingpoint.Whentheresourcesareidentified,thenext step is to identify the firm’s capabilities which are based on the resources. Capabilities can beexplainedas abundleof resourceswhichhelps to create value, it isoften the capabilities that are thebasisfortheSCA.Duetothebundledstructureofcapabilitiestheycanbedifficulttoidentifyandmanyexamplesexistwherefirmsandmanagersoverestimatestheirowncapabilitiesresultinginmarketfailure.Toavoidsuchfailuresitisimportanttoassessthecapabilitiesrelativetothoseofcompetitors.WhenthecapabilitiesofthefirmareidentifiedtheirSCApotentialneedstobeevaluated,inadditiontothistherentgeneratingpotentialofthosecapabilitiesneedstobeidentified.Capabilitiescanbeerodedovertimeduetodepreciationoftheirvalueorimitationfromcompetitors,andthuslowerthefirm’sabilitytogeneraterentsfromsuchcapabilities.Evenifthecapabilitiesaresustainableovertime,thefirmmustidentifytheappropriabilitypotentialofthevaluethatthesecapabilitiescangenerate.

Grant(1991)arguesthatafterthefirstthreesteps,thestrategydevelopmentisquitestraightforwardasitshouldbecomeclearforthefirmwheretheirmostvaluableresourcesandcapabilitiesareandhowtheygenerateeconomic rents for the firm. The firm should choosea strategywhere theymakebestuseoftheirstrengthsinresponsetotheopportunitiesonthemarketandwheretheylimittheirweaknessandprotectthemselvesfromthreatsonthemarket.

ThefinalstepinGrant’s(1991)frameworkistheidentificationofresourcegaps.Afirmmustcontinuouslydevelop its resources and capabilities to meet future demand and changes in the competitiveenvironment. This requires strategic direction to give the organization guidance for what kind ofresources needed to be developed. This could also constitute a capability of a firm; to be able tocontinuouslydevelopnewresourcetomaintainandupdateitscompetitiveadvantage.

3.2 ExternalperspectiveTheprevioussectionhashighlightedthe importanceof internalevaluationofresourcesandcapabilitieswhen developing strategy in the resource based view. However, it stands to reason that an isolatedanalysisof the firm’s internalmakeupwillbe insufficientwhen formulatinga competitive strategy.TheexternalenvironmentisthusnotignoredinRBVandthefollowingsectionwillpresentsomekeyconceptswhenanalyzingafirm’senvironment.

3.2.1 CustomersThefirstcriterionintheVRIN/VRIOframeworkisvaluable.Aspreviouslystatedaresourceorcapabilityisonly valuable if it can be utilized to improve efficiency and effectiveness, or put anotherway, itmustexploit an opportunity or neutralize a threat in the firm’s environment (Barney, 1991). This infers thatvalue has to be evaluated in relation to the external market rather than the firm-centric internalperspective associated with the RBV. Barney (1991) pointed this out in his seminal article where hehighlighted the complementarity of environmental models and the RBV by stating, “…environmentalmodelshelp isolate those firmattributes thatexploitsopportunitiesand/orneutralizes threatsand thusspecifywhichfirmattributescanbeconsideredasresources”.Despitethistherehasbeena lackofRBV

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 18

research that incorporates contextual factors in empirical testing. This is particularly true in the valuedimension,wheremostofthestudiesthathavebeenattempted,hasfocusedpurelyonfinancialaspectsof value (Rashidirad et al., 2015). The lack of external focus has been felt in the demand side of themarket,namelythecustomer,whichisoftenaneglectedcomponentinRBV(Zander&Zander,2005).ThishasbeenthecaseeventhoughPeteraf&Barney(2003)attemptstoclarifytheirdefinitionofthevaluethattheRBVissupposedtomeasure,“…firmswithsuperiorresourcescandelivergreaterbenefitstotheircustomers for a given cost (or can deliver the same benefit levels for a lower cost). Note that this is abroadviewof'efficiency'inthatitisconcernednotjustwithloweringcosts,butalsowithcreatinggreatervalueornetbenefits”.

One of the few studies that have incorporated the demand-based perspective is Anders Hinterhuber’sCan competitive advantage be predicted? (2013). In his article, Hinterhuber aims to add to the RBV intermsof increasedmanagerial guidanceaswell as itspredictive capabilitybyborrowingconcepts fromresearchonbreakthrough innovationsaswellasmarketing theory.Frommarketing theoryHinterhuber(2013)pointsout that the fixed costsof enteringanewproductmarket is silently assumed tobe zerowithin theRBV. If allowing this assumption to stand, a firmcan identify resourcesandcapabilities thatfulfill the VRIO requirements, device a strategy that leverages them, but still fail in themarket due tomisjudging the market size from a demand perspective. Based on this an extension of the VRIOframework is proposed that includes a size factor of the addressablemarket segmentwhichhas to besufficiently large tocover the fixedcostsof the intendedstrategy.From innovationresearchthearticleincorporates the ideas that customer research should focus on twomain premises; firstly identify theactual job that the customer is trying to performby using your product/service. Secondly,what is thedesiredoutcomeforthecustomerwhendoingtheaforementionedjob(Ulwick&Bettercourt,2008).Thisresultsinknowledgeaboutwhatcustomerneedsthatarecurrentlynotbeingsatisfiedinthemarketare,andHinterhuber(2013)extendstheVRIOframeworkbyaddingthisdimensionthathecallsUnmetneeds.

ThisextensionoftheVRIOframeworktobecomeVRIOLUisinlinewiththeoriginalassertionthatBarneymadeinhis1991articlethattheRBVworksasacomplementto,whathecalledenvironmentalmodels.ThismodifiedframeworkalsoattemptstoappeaseoneofthemaincriticismsoftheRBV,whichisthatitdoesnotincludeademand-orientedperspective.(Srivastavaaetal.,2001;Priem&Butler,2001;Zander&Zander,2005)

3.2.1.1 AnalyzingthecustomersIn order to incorporate the demand perspective, or the “L” dimension of the framework suggested byHinterhuber (2013), the concept of market segmentation is a good entry point. In a simplified waysegmentationcanbedescribedasthequesttofindoutwhothepotentialcustomersare,howmanyofthemthereareandhowdifferentgroupsofcustomersdifferfromeachother(Kotler&Keller,2012).Putanother way segmentation is concerned with where a firm competes in terms of customer groups,geographicfocusandproductmarkets(Grant,2013).

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 19

Customer segmentation is a very commonmanagement tool, particularlywithinmarketingwhere it isconsidered to be a very important, if not themost important, concept in the field (Weinstein, 2011).Segmentationcontributestostrategicmanagementthroughanalysisofmarketdatathatwillbeusedtoguide strategic marketing decisions as well as tactical execution plans. One practical application ofsegmentationdataisasaninternaldecisionsupportsystemonhowtoallocateresourceswheretheywilldothemostgood(Leeetal.,2007).

Segmentationisanextensivelyexploredfieldbothinpracticeandacademia.Despitethisthereisnorealconsensusofwhatthedefinitionofsegmentationactuallyis,howitshouldbeconducted,whenitshouldbeutilizedandwhatthestrategicandoperationalimplicationstheresultsshouldhave(Mitchell&Wilson,1998).Whatvariablestoinclude,appeartobethetopicthathasgeneratedthemostdebates.Mitchell&Wilson (1998) suggest thatwhatevervariables the researcherorpractitioner is considering theyshouldassess the variables appropriateness by asking “is this useful to understanding customer needs?” Thestrong focusonunderstanding theneedsandwantsof customers canbe seenasoneof the twomainperspectivesonsegmentation.Theothermainperspectiveissegmentationthroughdemographics(Dibb& Simkin, 1997; Mitchell & Wilson, 1998). While some researchers focus solely on the demographicaspect (Griffith & Pol, 1994) many researchers recommends that some sort of combination of bothperspectives is preferable (Shapiro & Bonoma, 1984;Mitchell &Wilson, 1998;Weinstein, 2011). Thedivisionbetweenthefocusoncustomerneedsanddemographicsisalsoreferredtoasthemicro-macromodel.

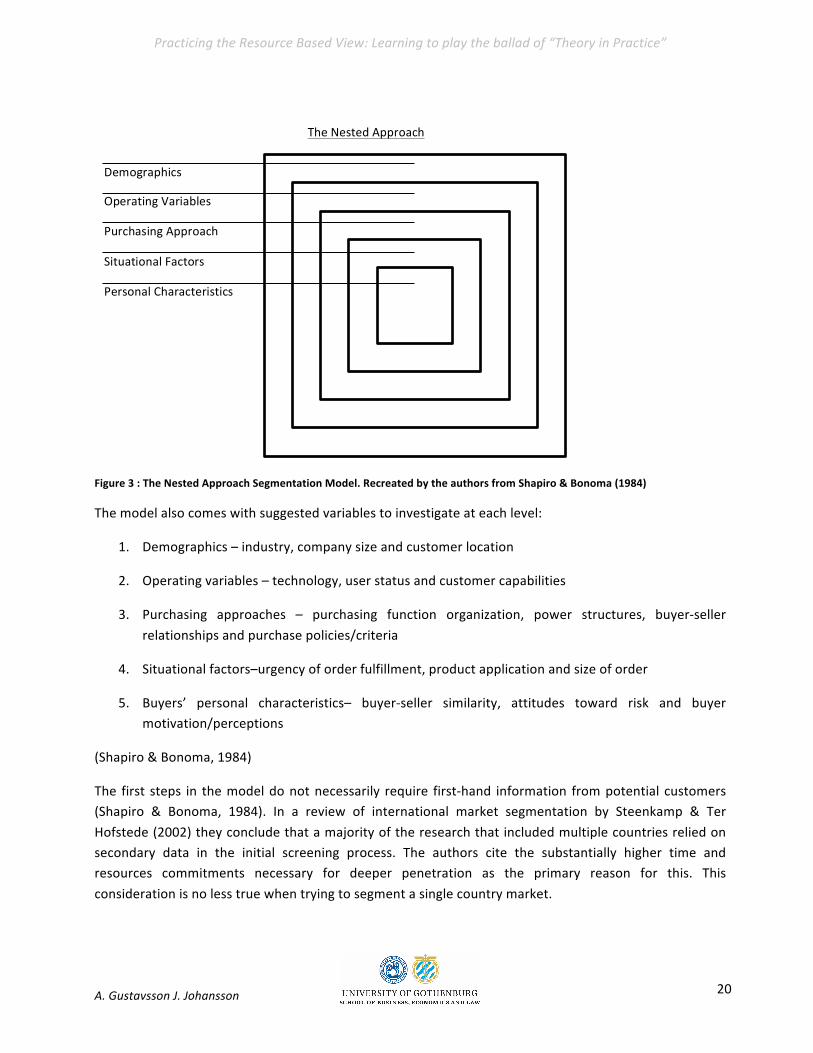

Developing conceptual models that outlines the process of segmentation has been a challenge foracademics formany years and there is no real consensus on any best practice approach. One famousmodelthatincludesbothmacroandmicrolevelanalysisistheNestedApproachdevelopedbyShapiro&Bonoma(1984),whichoutlinesfivelevelsofanalysiswhenitcomestosegmentation.Theystatethatitisdesirabletostartatthemacrolevelandmethodicallyworkyourselfinwardstowardsthemicrolevel.Thismodelgivesaclearconceptualoverviewofmanyoftheaspectsinmarketsegmentation.

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 20

Figure3:TheNestedApproachSegmentationModel.RecreatedbytheauthorsfromShapiro&Bonoma(1984)

Themodelalsocomeswithsuggestedvariablestoinvestigateateachlevel:

1. Demographics–industry,companysizeandcustomerlocation

2. Operatingvariables–technology,userstatusandcustomercapabilities

3. Purchasing approaches – purchasing function organization, power structures, buyer-sellerrelationshipsandpurchasepolicies/criteria

4. Situationalfactors–urgencyoforderfulfillment,productapplicationandsizeoforder

5. Buyers’ personal characteristics– buyer-seller similarity, attitudes toward risk and buyermotivation/perceptions

(Shapiro&Bonoma,1984)

The first steps in themodeldonotnecessarily require first-hand information frompotential customers(Shapiro & Bonoma, 1984). In a review of international market segmentation by Steenkamp & TerHofstede(2002)theyconcludethatamajorityoftheresearchthatincludedmultiplecountriesreliedonsecondary data in the initial screening process. The authors cite the substantially higher time andresources commitments necessary for deeper penetration as the primary reason for this. Thisconsiderationisnolesstruewhentryingtosegmentasinglecountrymarket.

Demographics

OperatingVariables

PurchasingApproach

SituationalFactors

PersonalCharacteristics

TheNestedApproach

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 21

3.2.2 CompetitorsThesecondcriterion intheVRIN/VRIOframework is rareandthis touchesuponan importantaspectofRBV, namely that the internal resources and capabilities needs to be put in relation to its competitors(Barney, 1991).When firms gather information about their competitive environment it is important tohaveagoodunderstandingfortheircompetitors,asthisimpactswhatresourcesandcapabilitiesthefirmneedstoexploitormaybedevelop(Fahey,1999). Inordertohaveasustainablecompetitiveadvantagetheresourcesofthefirmneedtobestrongerwhencomparedtosimilarassetsheldbythecompetition(Peteraf,1993;Hinterhuber,2013;Barney,1991).AfundamentalassumptionwithintheRBVisthatfirmsare heterogeneous in terms of the resources they control, and that some of those resources are notperfectly mobile and thus the heterogeneity among firms can be long lasting (Barney, 1991). Thishighlightstheimportanceofanalyzingthecompetitiveenvironmentwhenevaluatewhichresourcesthatarerare.Anincompleteorinaccurateviewofthemarketcanleadtopoorstrategicdecisionmakingandinworstcasemarketfailure(Bloodgood,2014).

Theimportanceofgettingagoodunderstandingofthesurroundingenvironmentandcontextualfactorswhenconductingstrategicanalysiscannotbeoverstated(Pickton&Wright,1998)asitalsoinfluencesthefirst criteriaof valuable in theVRIN/VRIO framework. If firms fail to assess their capabilities relative tocompetitors, the riskof overestimating the valueof existing capabilities increases (Grant, 1991). In thesamewaythatthepotentialvaluethattheseresourceshastobemeasuredfromacustomerperspective,strengthsofthefirmmustbemeasuredinrelationtoitscompetition(Hinterhuber,2013;Mathews,2003;Barney,1991).

Whenusing the resourcebasedview in strategic implementation theobjective for the firm is togainasustained competitive advantage. It should thus implement a strategy thatmakes best use of internalresourcesthroughrespondingtoexternalopportunitiesand/orneutralizingexternalthreatsandavoidinginternalweaknesses (Barney, 1991). A basic idea of the RBV is that firms should aim to leverage theirrelative strengths, and thus pursuing segments of buyerswhere no competitor are better equipped atmeetingaparticularcombinationofcustomerneeds(Wernerfelt,2014).

3.2.3 ResourceGapsAccording to the RBV, resources are the basis for value creation. However, it is not enough withidentifyingtheresourcesandcapabilitiesfollowedbythedevelopmentofastrategy.Animportantaspectof theRBV is continuous evaluationof existing resources followedby investments tomaintain existingand create new resources (Grant, 1991). Authors such as Teece (2007) andWu (2010) argues for theconceptofdynamiccapabilitiesasessentialformaintainingcompetitiveadvantagewhenafirmoperatesin a nonlinear and unpredictable competitive landscape. Dynamic capabilities can be defined asmanagers’ abilities to integrate, build and reconfigure internal and external competences to addressrapidly changing environments (Wu, 2010). Dynamic capabilities do fall within the boundaries of RBVsince Barney (1991) included the firm’s ability to envision potential strategies aswell as implementingthem,thusessentiallymakingthisprocessdynamic(Knott,2009).

PracticingtheResourceBasedView:Learningtoplaytheballadof“TheoryinPractice”

A.GustavssonJ.Johansson 22

By developing dynamic capabilities, a firm can increase the chance to reach sustainable competitiveadvantageasthedynamiccapabilitiescanhelpthefirmnotonlytoadapttotheenvironment,butalsoshapetheenvironmentthroughinnovationandthroughcollaborationwithotherenterprises,entitiesandinstitutions(Teece,2007).Ifthefirmonlyreliesonpreviouslyaccumulatedresources,theyarenotabletogenerate profits under volatile circumstances (Wu, 2010); instead they need to master the ability toorchestrate the resources depending on how the environment develops (Teece, 2007). With dynamiccapabilitiesafirmisbetterpreparedtobeprofitableinhighlyvolatilemarkets,suchashightechnologicalmarkets.Gooddynamiccapabilitieshelpsthefirm(1)senseandshapeopportunitiesandthreats(2)seizeopportunities, (3) maintain competitiveness through enhancing, combining, and when necessaryreconfigurethebusinessenterprise’sintangibleandtangibleassets(ibid).

Asameantofillresourcegaps,acquiringnewresourcescanbeanattractiveoptionforafirmtryingtoreachcompetitiveadvantage,withouthavingtodeveloptheresource fromscratch.However,acquiringresourcesmightnotbethateasybecause(1)resourcestakestimetodevelopin-house,(2)someassetsare not tradable, and (3) in an efficient market, a firm have to pay a price for the asset which fullycapitalizetherentsfromtheasset(Teeceetal.,1997).Simplyspeaking,resourcesneedtobefirmspecificin order to be the base for sustainable competitive advantage, and if resourceswere available on themarketeveryonewouldbeabletopurchasethemandthussuchresourcescannotbethebasisforSCA.However,Wernerfelt (2011) challenges this notion as he argues that a firm’s cost of acquiring a newresourceand/orthevalueitcangeneratewiththisresourcedependsontheresourcesalreadypossessedbythefirm.Followingthisargument,resourcespurchasedonanopenmarketcanbethebaseofSCAforfirmsthatpossessotherresourcesthatcanincreasethevaluefromthepurchasedresource,orlowerthecostforacquiringthenewresource.Forexample,afirmthatpossessesastrongbrandnamecanacquirealargecustomerbasecheapercomparedtofirmsthatlacksstrongbrandnames(Wernerfelt,2011).EvenifapotentialmissingresourceorcapabilityisnotconsideredapotentialSCAforthefirmitmaystillbeaprerequisitetoreachcompetitiveparityinamarket(Barney&Delwyn,2007).Resourcessuchasthisarevaluable in themarket since they allow the firm to exploit an opportunity, however they are not raresinceseveralcompetitorsareinpossessionofsimilarresources(Ibid).Theimplicationofthisisthatfirmsneed to consider acquiring missing resources when competing on a given market, regardless if thisresourcecanbecomeandSCAornot.