powerpoint-präsentation - kendrion · - operations: electromagnetic brake and clutch systems for...

TRANSCRIPT

27-2-2013

1

Annual results 2012

Analysts' meeting

Wednesday 27 February 2013

2

Agenda

1. Kendrion at a glance

2. 2012 Highlights

3. Key figures for 2012 and financial objectives

4. Review of business units

5. Financial position

6. Dividend

7. Fine imposed by European Commission

8. ERP project HORIZON

9. Priorities and outlook

27-2-2013

2

3

1. Kendrion at a glance

4

The Kendrion organisation

KENDRION N.V.

Development, production and marketing of high-quality electromagnetic components

1,600 employees (including 100 temps) in 12 countries

Revenue: approximately EUR 300 million

Listed company on NYSE Euronext's Amsterdam Market

27-2-2013

3

5 5

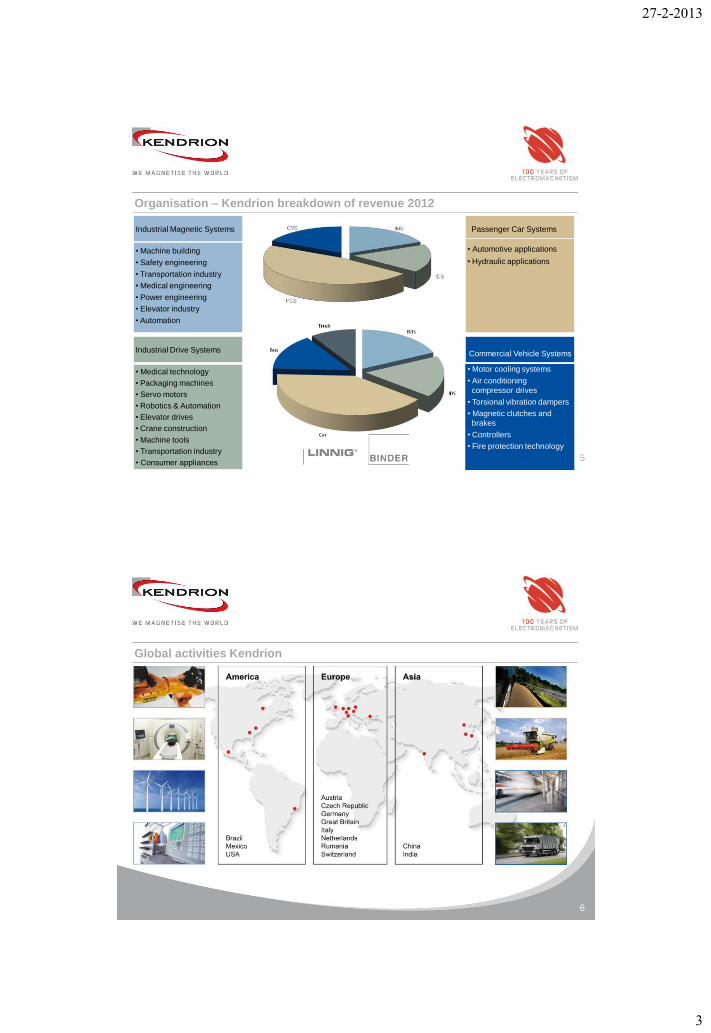

Organisation – Kendrion breakdown of revenue 2012

Commercial Vehicle Systems

• Motor cooling systems

• Air conditioning

compressor drives

• Torsional vibration dampers

• Magnetic clutches and

brakes

• Controllers

• Fire protection technology

Industrial Drive Systems

• Medical technology

• Packaging machines

• Servo motors

• Robotics & Automation

• Elevator drives

• Crane construction

• Machine tools

• Transportation industry

• Consumer appliances

Industrial Magnetic Systems

• Machine building

• Safety engineering

• Transportation industry

• Medical engineering

• Power engineering

• Elevator industry

• Automation

Passenger Car Systems

• Automotive applications

• Hydraulic applications

6

Global activities Kendrion

27-2-2013

4

7

Kendrion committed to being a high-performer in selected business units

Strategy Objectives

Organic growth > 10%

ROS > 10%

ROI > 17.5%

Spearheads

- Niche market leadership

- Organic growth in the current

operations

- Utilisation of synergy in and

between the business units

- Balanced geographical

spread of the operations

- Enhancement of flexibility in

the organisation

- Targeted add-on acquisitions

- Enhancement of the

innovative capacity

Mission

To develop business units that

have strong international

market positions in selected

business-to-business niche

markets and are market leader

whenever possible

8

Kendrion's strategy

- A clearly defined profile of a multinational, fast-growing high-tech company

- Build leading positions in business-to-business niche markets

- Balanced spread of activities

- Automotive with bus, truck EUR 200 million and growing strongly

- Industry EUR 100 million

- Ambitious growth targets (EUR 450 - 500 million in 2015)

- Selective value-adding acquisitions for expansion preferably in industrial activities

- Further improvement of geographical distribution across continents (USA, China, India)

- Financially strong

- Strategy redescribed in Mid-term Plan 2013 - 2015 "Entering another league"

27-2-2013

5

9

Key actions for achieving our strategic spearheads (1)

- Alert response to market developments in all key markets (market intelligence)

- Increase customers' commitment in projects, particularly in Industry

- Expand and retain workforce

- Very little unemployment in southern Germany, flexibility pressured as a result

- Recruiting engineers is very time-consuming

- Kendrion devotes extensive efforts to the development of its employees

- Redefine workforce flexibility and costs

- Targeted acquisitions

- In the USA and China (markets, customers)

- Niche players in Germany (technical know-how)

10

Key actions for achieving our strategic spearheads (2)

- Enhancement of innovative capacity

- Continuous flow of new initiatives and ideas

- Innovation cells and "treasure mapping"

- IP strategy

- Foundation of Kendrion Academy

- CSR

- Focus on working capital management

- Ongoing strengthening of risk management

- Good analysis of the business risks

- Tax and regulatory compliance

- Smaller entities ("Kendrion in Control")

27-2-2013

6

11

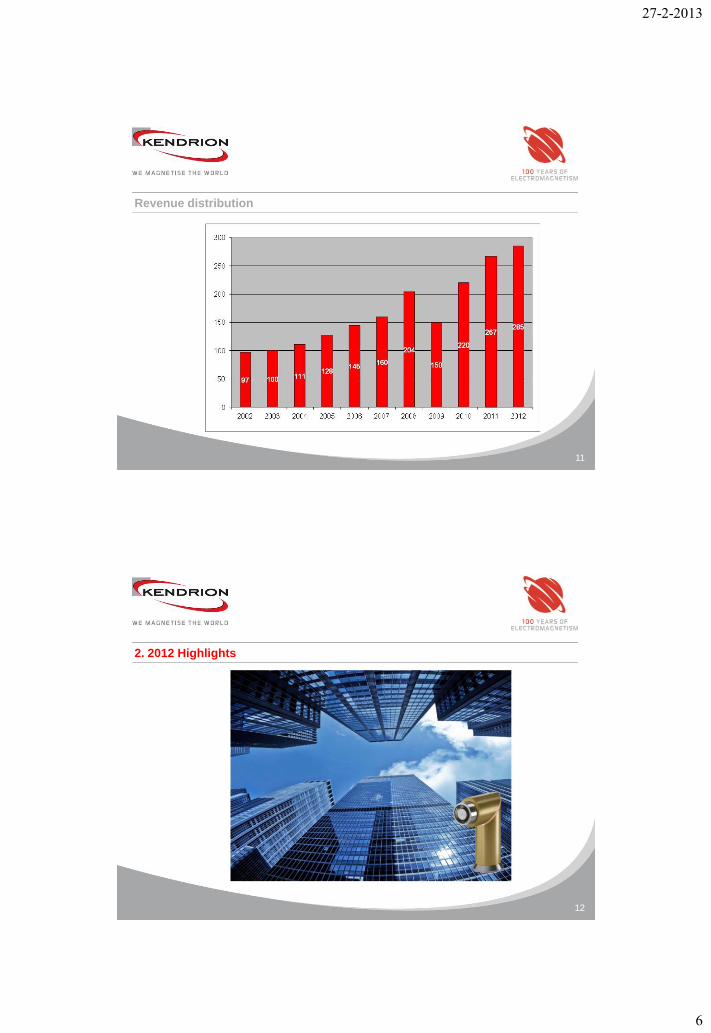

Revenue distribution

12

2. 2012 Highlights

27-2-2013

7

13

2012 Highlights

- Market conditions deteriorated during the year

- Transitional year, revenue up 6% (-4.1% on an organic basis)

- Net profit EUR 18 million (normalised net profit EUR 13.6 million)

- Growth in business units IDS and CVS

- Revenue decrease in IMS and (on an organic basis) in PCS

- Satisfactory free cash flow (EUR 9.7 million)

- Extensive focus on innovation and flexibility

- Dr. Wilhelm Binder Day highly successful (> 300 visitors)

- Acquisition of remaining 49% in Kendrion (Linz) GmbH

- Order book for industrial activities growing again to some extent

14

Revenue development per region

(x EUR 1 million) 2012 share 2011 share growth

Germany 139 49% 148 55% -6%

Rest of Europe 61 21% 65 24% -7%

Americas 50 17% 20 8% 150%

Asia 33 12% 32 12% 2%

Other 2 1% 3 1% -2%

Total 285 268 6%

27-2-2013

8

15

3. Key figures for 2012 and financial objectives

16

Key figures 2012

(x EUR 1 million unless otherw ise stated) Q4 2012 1 Q4 2011 1 Difference in %

Revenue 65.5 64.9 1%

Normalised EBITA * 2.3 6.7 -66%

Realised net profit 3.3 -36.2

Normalised net profit * 2.2 4.4 -50%

ROS 3.4% 10.3%

1 The quarterly f igures are unaudited

(x EUR 1 million unless otherw ise stated) 2012 2011 Difference in %

Revenue 284.9 267.9 6%

Normalised EBITA * 22.3 30.7 -27%

Realised net profit 18.0 -20.1

Normalised net profit * 13.6 20.5 -34%

Solvency 44.8% 39.2%

ROS 7.8% 11.5%

ROI 12.4% 22.2%

* Profit adjusted in 2012 to exclude release of FAS Controls earn-out payment of € 4.4 million (Q4 € 1.1 million) in 2011

to exclude non-recurring provision/expenses relating to EC fine of € 39.4 million and non-recurring costs

of € 1.3 million (after tax, € 1.2 million)

27-2-2013

9

17

Financial targets

Target Realisation 2012 Realisation 2011

Organic growth >10% per year -4% 21%

ROS >10% 7.8% 11.5%

ROI >17.5% 12.4% 22.2%

Solvency ≥ 35% 44.8% 40%

Interest-bearing debt/EBITDA <3.00 0.65 0.6

Free cash flow Healthy71% of normalised

net profit

71% of normalised

net profit

Dividend 35-50% of net profit50% of normalised

net profit

35% of normalised

net profit

18

Performance Q4 2012

- Difficult quarter, especially the month of December

- EBITA margin 3.4% in fourth quarter 2012

- Inventory effects (priority for working capital management)

- Tax credit (utilisation of Dutch losses)

27-2-2013

10

19

Added value 2012

Added value fell by over EUR 11 million on an organic basis due to:

- Lower revenue EUR 5 million

- Lower inventories EUR 2 million

- Price effects net EUR 1.5 million

- Revenue with low added value EUR 2.5 million

20

Changes in Kendrion organisation

- Smoothly operating organisation in 2012

- From 1 January 2013: new Business Unit Manager CVS (Erik Miersch)

- From 18 February 2013: new CFO (Frank Sonnemans)

- Engineering significantly strengthened

27-2-2013

11

21

4a. Review of business units

22

General

- Operations: electromagnetic components and systems for industrial applications

- Focus markets: mechanical engineering, locking and safety, energy sector and medical sector

- Highly innovative, customised solutions

- Global player with operations in Germany, USA, China, Switzerland, Austria and Italy;

agencies in France and other countries

- > 2,000 customers

- Project business (70%) and standard solutions (30%)

- Competitors: besides MSM, ETO and Kuhnke there is a large number of (usually smaller)

niche players in Germany, Italy, France and the USA

- Fast-growing market in China, but with poor quality

- Engineering, logistics and delivery time most important drivers

- Competitive advantage: innovation capabilities, global possibilities, know-how for decades,

reliable partner, fast delivery time

27-2-2013

12

23

2012

- Top 10 customers account for 27% of revenue, largest customer for EUR 2 million

- Successful in acquiring new projects (especially in the USA)

- Challenging market conditions, particularly in textile machine market (since Q2), but also

volume reduction at other (large) customers

- Organic revenue decrease (12%) since Q2 2012

- Cost reduction implemented successfully, part of effect only in 2013

- Sales office in Italy successful

- Progress in China difficult

24

4b. Review of business units

27-2-2013

13

25

General

- Operations: electromagnetic brake and clutch systems for industrial drive technology

- Two production sites in Germany; international service coordinated through UK sales office

- Global market leader in permanent magnetic brake systems

- Number of customers 600 of which 100 large customers

- Substantial project business (80% of revenue), in addition to services business

(20% of revenue)

- Innovative business unit with many new products

- Competitors: limited number of players with revenues between EUR 10 million and

EUR 50 million

- Engineering, logistics and delivery time most important drivers

- Competitive advantage: know-how for decades, reliable partner, fast delivery time

26

2012

- Organic growth (5%) in permanent magnetic brake systems continued in 2012, due to

German machine building

- Strong increase among top 10 customers, revenue down at smaller customers

- Top 10 customers account for 63% of revenue, largest customer for over EUR 12 million

- Strong focus on market introduction of spring applied brakes (KOBRA-line) in HY2 2013

- New projects in China (start in Q3 2013)

- Aiming for further efficiency improvement (project "Fit for Production")

- Margin improved due to lower supplier prices

- Organisation strengthened significantly

27-2-2013

14

27

4c. Review of business units

28

General

- Operations: electromagnetic components and systems for the automotive industry

- Production sites in Germany, Austria, the Czech Republic, China and the USA

- Serves European “Original Equipment Manufacturers”: Daimler, Volkswagen (incl. Audi), and

first-tier suppliers (Continental, Delphi) and increasingly also in the USA (Eaton, Navistar)

- Good spread of customers (around 30), top 10 account for 65% of revenue

- Continental largest customer, with 20% of PCS revenue (10% of Kendrion's revenue)

- High tech, focus on energy efficiency, emission reduction, safety and comfort

- Contracts for 6 - 8 years

- Established strong position with high-quality electromagnetic valves for common-rail

technology

- Existing expertise can be extended to other markets (e.g. gasoline, off-road, trucks)

- Competitive advantage: know-how for decades, focus, high entry barrier (long lead times,

high investments)

27-2-2013

15

29

2012

- In 2012 good 1st half year (organic revenue increase of 2%), organic revenue decrease

(15%) in 2nd half year 2012

- Growth slowed by limited new revenue in 2012 (was expected), by French market and by

shifts for small diesel engines at Volkwagen

- Continued success in acquiring new projects (total revenue over expected economic life

EUR 250 million), new important market segments

- Outflow of revenue in next 5 years EUR 100 - 150 million

- Good profit contribution from Kendrion (Shelby), after dip in third quarter

- Alignment of Kendrion (Shelby) with Kendrion standards on track

- Follows the trends in motor management

(smaller parts, switchable units, lower fuel consumption, CO2 reduction)

- Preparations for new business unit Heavy Duty Systems (truck market)

30

4d. Review of business units

27-2-2013

16

31

General

- Operations: components and total cooling systems for buses, trucks, special vehicles

and generators

- Global market leader in electromagnetic cooling systems for luxury coaches

- Many customers worldwide

- Sites in Germany, USA, Mexico, Brazil, China and India

- USPs are energy-efficiency and convenience

- Increasingly a systems provider

- Service business (approximately 20% of revenue) forms an important basis

- Competitive advantage: know-how for decades, strong global partner network, fast

delivery and service, close to the customers

32

2012

- Organic growth of 2%, particularly due to growth in India

- Top 10 customers account for 59% of revenue, largest customer for over EUR 9 million

- European bus market weak

- Extra focus on cooling systems for truck market

- Faltering Chinese market, introduction of new products

- New greenfield plant in Pune (India), hick-up around the summer, now steady revenue

growth

- Weak year in Brazil, new project in 2013

- Kendrion sees good scope for strong growth in truck market in the next few years

(cooling systems, Kendrion FAS products)

- Organisation expanded by adding engineers for the truck market

- Recent claim Far East US$ 1.3 million, validity and insurance coverage is investigated

27-2-2013

17

33

5. Financial position

34

Financial position

- Satisfactory free cash flow for full year 2012: EUR 9.7 million

- In control of working capital, inventories reduced

- Strong balance sheet (net debt at year-end 2012 EUR 21.3 million, solvency 45%)

- Some EUR 80 million freely available for acquisitions

- Slight adjustment of financing arrangement

27-2-2013

18

35

6. Dividend

36

Dividend

- Dividend window 35% - 50% of net profit

- Solvency of at least 35%

- Proposed optional dividend for 2012 of 50% of normalised net profit

(EUR 13.6 million)

- Dividend of EUR 0.58 per share

27-2-2013

19

37

7. Fine imposed by European Commission

38

Fine imposed by European Commission

- Fine imposed in 2005 (EUR 34 million)

- Reason: alleged involvement of former subsidiary Fardem

Packaging in cartel in period 1995 - 2002

- Recognised a provision following judgement of General Court of the European Union in

November 2011, amounting to EUR 43 million at present

- Kendrion lodged appeal, hearing on 5 February 2013

- Decision expected at the end of 2013, beginning of 2014

27-2-2013

20

39

8. ERP project HORIZON

40

ERP project HORIZON

- Investment between EUR 5.5 and EUR 6.0 million

- 1 October 2012 IDS Villingen live, 1 January 2013 PCS Eibiswald live

- 1 April 2013 IMS Villingen scheduled, i.e. 3 major entities completed then

- Within budget for investments and costs

- Uses standard software, no tailor-made adjustments

- Desired improvements incorporated in IFS standard

- All companies to be migrated by mid-2014

27-2-2013

21

41

9. Priorities and outlook

42

Priorities for 2013: "Entering another league"

- Four spearheads maintained (flexibility, innovation, sustainability, globalisation)

- Focus on the internal organisation

- Achievement of financial objectives (costs and cash)

- Further steps in the field of innovation

- Expand businesses in USA, China and India

- Focus on "green" (energy savings, convenience, sustainability), new label

"Green signed by Kendrion“

- Roll-out of CSR programme

- New steps in HORIZON project

- Targeted acquisitions

27-2-2013

22

43

Outlook

- Uncertainty about economic situation

- Developments in eurozone and China uncertain

- Further signs of recovery in USA expected

- Nervous markets, uncertain outlook

- Order book for industrial activities growing again to some extent

- New revenue in 2nd half year 2013

- First quarter difficult, gradual improvement expected after that

- Solid financial position

- No specific profit forecast

We magnetise the world!

www.kendrion.com