power market review 2016 - willis towers watson

TRANSCRIPT

Power market review 2016

IntroductionGraham Knight, Global Head of Power, Willis Towers Watson 3

Part one – power industry issuesBrexit: possible implications for the UK power industry 6

Risk-based design for critical facilities 15

Employee Value Proposition and Total Rewards: modernize or risk being irrelevant 20

The rush to renewables in Australia 26

Energy storage & batteries – the energy revolution continues 31

The Asia power paradox 34

Advanced condition monitoring & diagnostic technology 39

Part two – risk transfer issuesRisk and resilience: engineering a sustainable financial system 44

The 2015 UK Insurance Act 48

Power sector Business Interruption claims 52

Alternative Risk Transfer solutions revisited 54

Part three – insurance market round-upProperty Damage / Business Interruption 60

Liability 64

Construction 66

Terrorism & Political Violence 68

Political Risks 70

Regional perspectives 72

Front cover image – aerial view of Godafoss waterfalls, Iceland, in the winter (Photo credit – Arctic-Images/Getty Images)

Power market review 2016 3

IntroductionWelcome to our latest Power Market Review, our first as Willis Towers Watson. In our last edition in December 2014, we noted that although companies in the power sector were facing a seemingly unprecedented range of business challenges, they could take comfort from the fact that the insurance market was relatively stable and benign, experiencing a lengthy ‘soft’ phase for most of the main insurance types typically bought by companies in the sector. To the casual observer, it may appear that not much has changed in the months since.

Power sector companies continue to face challenges, including (but not limited to) low energy prices, decentralised generation, emissions reduction targets, the viability of aging plant, power stations designed for baseload operation having to fit around the intermittencies inherent in renewable generation, and the continuing risks of climate change, political/regulatory intervention and financial instability.

Meanwhile the insurance market is still soft, buoyed by the record amounts of capital that have flowed into the industry and a relatively benign claims environment. Such has been the sustained nature of these conditions that some commentators have suggested that we should stop referring to the insurance market as soft and instead start considering current conditions as normal. It is difficult to find any observers who are expecting any broad market hardening in the near future.

However, change continues apace. One of the biggest political events of 2016 was the referendum vote by the British people to leave the European Union, a process widely referred to as Brexit. As Joseph Dutton of the University of Exeter Energy Policy Group notes in an examination of the possible Brexit scenarios, which we are pleased to include as one of three external contributions to this Review, energy has been at the heart of the European project but received very little coverage in the referendum campaign. He looks at the implications of the vote for power and energy policy and interdependence.

Of course, most people will probably not see Brexit as the biggest political event of 2016. This prize surely goes to the stunning victory of Donald Trump in the US presidential election, which happened as this Review was going to press. As a supporter of free markets and an avowed climate change sceptic, Mr Trump is expected to relax regulations that constrain the use of fossil fuels. However, as we note in our North American regional update, this does not necessarily signal a significant slowdown in the growth of renewable energy generation in the US, as renewables have become more competitive relative to other sources of generation.

A less well-publicised but also significant development in 2016 has been the implementation of the 2015 UK Insurance Act, the first major shake-up of insurance law in the UK for over 100 years. The Act’s provisions apply to all non-consumer insurance and reinsurance contracts that are governed by English law, regardless of where they are underwritten or where the parties to the contract happen to be located. Since many international insurance and reinsurance contracts are subject to English law, the Act therefore has global interest and application. Chris Dunn, Head of Kennedys Marine, outlines the key changes and issues.

Our third external contributor is Bob Bailey of Exponent, who looks at the importance of risk-based design for critical facilities exposed to coastal windstorm, as we come to the end of this year’s Atlantic hurricane season. This has been more active than in recent years, with a hurricane making landfall in Florida for the first time in 11 years, and then Hurricane Matthew causing devastation in parts of the Caribbean before skirting Florida and making landfall in South Carolina as a Category 1 cyclone.

Although the worst fears of widespread flooding and damage in Florida were not realised, Hurricane Matthew is still expected to present insurers with billions of dollars of claims. The way that the global insurance market has strengthened its resilience over time to cope not only with losses of this size but also with ‘one in 200 year’ loss events is explained in an article in these pages by Rowan Douglas, CEO of Willis Towers Watson’s Capital Science & Policy Practice.

We are particularly pleased that this year’s Review contains, for the first time, a contribution from our Human Capital Benefits segment. This describes the fascinating findings of our 2016 Global Talent Management & Rewards and Global Workforce Studies, which among other things reveal that employers and employees tend to have differing views on the key elements of job attractiveness and employee retention. We also take a fresh look at Alternative Risk Transfer (ART) in this Review, examining how parametric solutions in particular might become more familiar tools in the armoury of the modern power and utility sector risk manager.

And of course our Review would not be complete without the usual analysis by our in-house specialists of the state of the markets for the principal property and casualty classes of insurance as they affect companies in the power and utility sectors, regional commentaries from our industry leaders around the world, and technical insight into some of the hot topics affecting the industry. We are grateful to all our contributors, and hope that you enjoy this edition of our Review. As ever, we welcome any feedback you may have. Graham Knight Global Head of Power, Willis Towers Watson

4 willistowerswatson.com4 willistowerswatson.com

Part onePower industry issues

Power market review 2016 5

6 willistowerswatson.com

Brexit: possible implications for the UK power industryEnergy has been at the heart of the European project since the European Union (EU) was originally conceived as the European Coal and Steel Community in 1951. Although the organisation has evolved considerably since, energy remains a key policy area, alongside the broader policies of climate change and environmental protection/quality. Despite this, energy received little coverage in the run- up to the UK’s EU membership referendum; most of the debate focused on immigration, the financial contributions of membership and the wider but the less-well defined notion of sovereignty.

Still no certaintyDespite the resulting vote to leave the EU (universally referred to as ‘Brexit’), it is unclear what form this will take, in terms of both how the process will be carried out once the mechanism for leaving – Article 50 of the Lisbon Treaty – has been invoked and which areas of policy the UK may wish to retain.

On the day after the referendum, the Prime Minister David Cameron resigned. He decided not to invoke Article 50 before stepping down, arguing that it should be for a new government to decide when to do so. His successor, Theresa May, initially said it would not be invoked until 2017 at the earliest, but in early October she offered more detail, saying that it would occur by March 2017 at the latest. Yet this timetable was thrown into further doubt after the High Court ruled in early November that the government must consult parliament before invoking Article 50. Although the government has said the ruling will not affect the timetable of Brexit, it is likely to appeal the decision which could lead to delays. And ultimately it still remains unclear what the UK’s official negotiating position will be and what the actual nature of the UK-EU relationship will be after Brexit.

Repeal of the ECA inevitableAlongside the announcement regarding Article 50, Mrs May also confirmed that the 1972 European Communities Act would be repealed. The Act gives direct effect of EU law over that of UK, and also recognises the role of the European Court of Justice (ECJ) in interpreting and applying laws and court judgments. Once the Act has been repealed, new European legislation will no longer

legally apply to the UK, but it is unclear what will happen to the existing legislation on UK statute books. As the ECJ is the court that upholds legislation of the Single Market, this has been interpreted by some commentators that the UK intends to end its membership of the single market. However, the government has not outlined its official position; although the comments on the ‘Great Repeal Bill’ were viewed by some as a watershed, repealing the European Communities Act is the only legislative means by which the UK can leave the EU and was therefore inevitable.

The general uncertainty extends to energy as much as other sectors of the economy, and it is not possible to say with full confidence exactly how it will be affected going forward. The UK’s Energy and Climate Change Select Committee opened two inquiries following the referendum looking specifically at the implications for energy and climate policy.

Various options availableThere are various existing options the UK could pursue for its future relationship with the EU. The cases of Norway and Switzerland are useful but not definitive examples of third party country relations with the EU; indeed, the UK could press for a more bespoke relationship than the ones Norway and Switzerland currently have. The eventual nature of UK-EU relations will have a strong bearing on the future of energy in the UK as the two parties are strongly linked in energy supply and policy terms.

Energy interdependence

UK now a net energy importer…While many sectors of the economy benefit from access to the European single market, in the energy arena the UK and EU have physical interconnection as well as being intertwined in policy. The UK has been a net importer of energy since 2004, following the peak in North Sea gas production in 1999 (see chart below). There are four high-voltage electricity interconnectors between the GB system and the EU, and there are five natural gas pipelines running to other countries - three to the EU and two to Norway. Oil and gas production from some North Sea fields is also delivered directly to non-UK facilities.

As well as being dependent on coal and oil imports from Europe and further afield, imports make up a substantial amount of the gas the UK uses for electricity generation and domestic heating. In 2015 imports accounted for 40% of gas supply, with nearly 70% of this coming from mainly Norway, and also from the Netherlands and Belgium.

Power market review 2016 7

…but also an important EU energy supplierHowever, the UK is also important for EU energy supply because of these connections. Gas from North Sea fields and that arriving on LNG tankers (liquefied natural gas) at UK terminals can be sent to the EU via the pipelines. Ireland is almost entirely dependent on gas from the UK via the Moffatt pipeline for its supply, and it also imports 4% of its electricity demand from the GB system. The electricity interconnectors between the GB system and the EU also export electricity depending on demand and wholesale prices.

EU policy influence on UK energy so far

Considerable EU influence on UK policy…The EU has had considerable influence over UK energy policy, and this can be most keenly observed in the area of electricity supply: for example, policies on the growth of electricity generation from renewable sources (Renewable Energy Directive, 2009) and the phase out of coal fired power generation (Large Combustion Plant Directive, 2001, and Industrial Emissions Directive, 2010). These high-level energy policies sit alongside directives on environmental habit protection, water quality, and air quality.

…while the UK has also driven EU energy policyBut at the same time the UK has also been a driver of energy policy at the EU level. The market liberalisation and ownership restructuring policies of the 2009 Third Energy Package drew on the UK’s own experience of privatisation and market opening in the late 1980s and 1990s. Similarly, during the UK’s 2005 EU presidency the then Prime Minister Tony Blair pushed for deeper market integration, harmonisation, and a collective approach to tackling climate change.

A weakened UK negotiating position?This move to a more internationalised approach on energy via the EU coincided with the UK becoming a net energy importer in the mid-2000s. The UK’s Climate Change Act (2008) was also regarded as front runner to the EU’s own Climate and Energy Package of 2014, which includes a binding 40% reduction in greenhouse gas emissions from the EU by 2030. Because of the UK’s global and interventionist role, climate change continues to be viewed through the lens of foreign security policy as much as environmental protection. Whether the UK maintains this type of diplomacy as an independent country remains to be seen, but its negotiating position on the international stage could be weakened through leaving the collective EU bloc.

1970

0

10

20

30

40

50

60

-10

-20

-30

1975 1980 1985 1990 1995 2000 2005 2010 2015

Net importer Net exporter

Per

cent

age

UK became a net exporter of energy in 1981 due to North Sea oil and gas development

North Sea production peaked in 1999

UK became a net imported again for a shortperiod after the 1988 Piper Alpha disaster

Reliance on imported energyhas grown in recent times

UK Energy Import Dependency 1970-2015

Source: Office for National Statistics (2016)

8 willistowerswatson.com

Electricity generation and energy supply after Brexit

UK Renewables target met…Under the EU’s 2009 Renewable Energy Directive the UK adopted a non-binding target of a 15% share of total energy consumption in power generation, transport and heating to be from renewable sources by 2020, with 30% of electricity demand to be sourced from renewables by 2020. The UK was one of the most proactive countries in developing its renewables sector, and generated 19.1% of total electricity from renewables in 2015 compared to just 6.7% in 2009. In the years following the directive, installed renewable capacity more than doubled to 27.2GW by the start of 2015 from 9.2GW in 2010.

...and sector may increase still furtherThe EU directive may no longer apply to the UK after Brexit, but the government will still be legally bound by its own Climate Change Act (2008) which requires an 80% reduction in carbon emissions by 2050. Because of this the UK renewables sector may continue to grow, despite leaving the EU. And as energy sourced from indigenous coal mines and the North Sea falls further, the government could push for more renewables. In the run up to the referendum it was reported that as part of the political restructuring after Brexit the government could remove the so-called green taxes and subsidies put in place by the EU to support renewables. However, although there is an EU-wide target for renewable energy that is binding, member states’ targets for renewable energy were set by themselves, along with the means of achieving it. This means that existing support schemes for renewable energy in the UK could also remain.

Cross-border supply

In 2015 around 6% of UK electricity demand was covered by imports through high-voltage interconnectors with other EU countries. There is currently 4GW of interconnection capacity and a further 2GW of capacity to Belgium and France is currently under development; furthermore there are plans to add at least another 5.8GW by 2022. Planned interconnectors to Norway and Iceland would deliver electricity from hydro and geothermal sources – something considered low-carbon and baseload supply for the GB market – while further connection to Ireland and northwest Europe would allow the import and export of electricity and also help balance the system in case of wind power intermittency.

Legal arrangements for interconnectors?Leaving the EU is unlikely to prevent the building of new interconnectors, but it is uncertain what legal arrangement would need to be in place for both these and the existing ones. Although Ofgem’s regulatory regime for interconnectors differs in some respects from other European countries’ own, GB interconnectors are regulated in accordance with EU rules on the single market. A situation could arise after Brexit whereby the current EU regulations and network codes that govern cross-border electricity market transactions and system operation must remain in place to ensure the GB electricity market remains operationally integrated with that of the EU.

Existing interconnectors

In development

Proposed

0 500 1,000 1,500 2,000

0 500 1,000 1,500 2,000

NorthConnect

NorthConnect

NSNNSN

Viking Link

Viking Link

BritNed

BritNed

Nemo

Nemo

Eleclink

Eleclink

IFA

IFA

IFA 2

IFA 2

FAB

FAB

EWIC

EWIC

Moyle

Moyle

GB Electricity Interconnectors (n.b. does not include planned Greenlink to Ireland or IceLink to Iceland)

Source: Reuters, 2015

Power market review 2016 9

Possible scarcity of supply scenarioHowever, in a worst-case scenario where the new interconnection capacity does not get built the UK could face electricity supply issues. In the last 12 months coal plants equivalent to 9% of the total electricity generating capacity have come offline, while the seven remaining coal plants in the UK are set to come offline by 2025. Though some plants are being shut down because of unfavourable market conditions and the cost of maintaining old facilities, some closures can also be attributed to the EU’s Large Combustion Plant Directive (2001) and Industrial Emissions Directive (2010). These introduced a choice for the highest polluting industrial units – including coal-fired power stations – of either restricted operating hours followed by eventual shut down or the installation of emission-reducing technology. The government pledged earlier this year that it will ensure the phase out of unabated coal by 2025, but an electricity supply crunch (partly because of no new interconnection) could see this delayed or the policy reversed.

New EU co-operation agreements required?The incorporation of existing EU policy post-Brexit could also arise with cooperation arrangements for oil and gas in the North Sea. For example, the UK and Norway are signatories of a framework agreement relating to cross-border cooperation that includes fields that may straddle the border between the two countries and the pipelines that deliver gas to the UK – which in 2015 accounted for 61% of total UK gas imports. Although signed bilaterally, the terms and conditions for access to pipelines – including the setting of entry and exit tariffs – are set out in accordance with EU law on the single market. Therefore if the UK did not maintain its membership of the single market, it is likely the agreement would need to be renegotiated or replaced.

“ Although signed bilaterally, the terms and conditions for access to pipelines – including the setting of entry and exit tariffs – are set out in accordance with EU law on the single market.”

Cost of energy and investment

Higher investment costs the real riskIn the run up to referendum the then Secretary of State for Energy Amber Rudd argued that Brexit could lead to a ‘£500m shock’ to the energy system which would eventually work its way on to consumer bills. The report to which Rudd was referring, commissioned by National Grid, looked at a wide range of risks posed by Brexit to the energy sector.

The report concluded that threats to physical supply of energy were of a lower risk, but higher costs of investment in energy infrastructure pose the more significant risk to the energy sector after Brexit. Equally any sustained period of uncertainty could lead to a deferral of investment in the sector.

Increased costs were expected because of a devaluation of sterling. This would raise the cost of imported equipment and services that are needed to upgrade networks and infrastructure for more renewables, replace closing electricity generation plants and develop a decentralised energy system. Any delay in critical energy investment could reduce energy supply security further ahead. The report also suggested that if the UK is excluded from the single market for energy it could lose the financial benefits that market integration offers.

Sterling has already fallen…Although the UK has not left the EU, the referendum result made an immediate impact on currency. The value of sterling fell by as much as 11% on a trade weighted basis between 23 June and September, with a 15% fall against the US dollar. Against the Euro it fell by 8% in the week following the referendum. The impact of this can be seen, for example, on wholesale gas prices at the UK’s National Balancing Point (NBP) trading hub.

…with gas prices increasingTrade at the NBP is priced in sterling but European hubs such as those in the Netherlands and Germany are priced in euros. Contracts for longer-term supply and those delivering in the winter months are typically priced in Euros, as the UK imports gas from the continent though winter. As such following the vote and sterling’s fall against the Euro gas prices at the NBP increased. This price-rise fed into the UK power market because of the high volume of electricity generated from gas-fired power stations. This also has the potential to feed in to domestic energy costs and consumer bills in if the price rise is sustained, and already some utility bills have increased on rising wholesale costs. Following Theresa May’s announcement that Article 50 would be invoked by March 2017 sterling fell further, to its lowest level against the dollar for 31 years.

10 willistowerswatson.com

Post-Brexit single market access

Hard or soft Brexit?Retaining access to the European single market is of concern to many sectors of the UK economy. In the run up to the referendum some Leave campaigners sought to assure voters and businesses alike that leaving the EU would not remove the country’s access to the single market. Although ‘Brexit means Brexit’ is the position Theresa May has reinforced, the ambiguity of Article 50 – some say deliberate – and a lack of clarity so far on the plan for the future relationship mean access to the single market could yet be maintained, as leaving the EU does not necessarily mean leaving the single market.

The confirmation by Theresa May that repealing the European Communities Act would mean that ECJ decisions would no longer be binding on UK law suggests that the UK would also leave the single market and pursue a so-called ‘hard Brexit’, though this remains unconfirmed. Given (a) the condition of membership of the single market that requires members to allow free movement of people from other member states, and (b) the role that control of immigration played in the referendum campaign, many find it difficult to see how the UK can maintain its membership status.

Before and after the referendum businesses sought clarification from the government on remaining in the single market. For example in July the British Insurance Brokers Association (BIBA) wrote to the government seeking assurance that the UK would remain in the single market, highlighting how the best interests of its members would be served through retaining tariff free cross-border trade with EU and EEA countries.

“Access to” or “membership of”?There is a fundamental difference between ‘access to’ and ‘membership of’ the single market, with the former being an option available to any World Trade Organisation (WTO) member. And though financial tariff free access to the single market could well be agreed between the UK and EU in the years ahead, it is unclear which non-tariff barriers, such as product standardisation, would remain in place.

Membership of the single market on par with existing obligations of a member of the EU would, as the legal framework stands, require the UK to be a member of the European Economic Area (EEA), like Norway (dubbed the ‘soft’ Brexit option). The UK also has the option of being a part of EFTA, with single market access secured via bilateral treaty negotiations, like Switzerland, which is a member of the European Free Trade Association (EFTA). There is also the so-called ‘hard’ Brexit option, where a free trade agreement along WTO terms would be negotiated between the UK and the EU that would secure access to the single market.

Norway option: EEA

The EEA is a group formed of the EU member states and Norway, Iceland and Lichtenstein. It was set up to extend the single market into the three non-EU EEA countries. The agreement that underpins the organisation ensures EU legislation covering the so-called ‘four freedoms’— free movement of goods, services, persons and capital – are applied equally to EEA and EU members, and guarantees equal rights and obligations within the single market for citizens and economic operators of EEA members. All relevant laws on the single market, except those dealing with agriculture and fisheries, apply to Norway. There is also cooperation on other policy areas, including the environment, known as ‘flanking and horizontal’ policies.

Not really Brexit?But UK membership of the EEA would arguably not be consistent with the ‘Brexit means Brexit’ mantra, especially in terms of financial contributions, free movement of labour and regulations. And to gain membership of the EEA the UK would first have to re-join EFTA, and then seek to join the EEA – something all members would need to agree on.

Norway maintains a mission to the EU to exert considerable lobbying pressure on EU decision makers as, under the terms of the EEA agreement, it is bound by EU legislation but does not have a vote or representation in the European Commission, Parliament or Council of Ministers. Norway has around 60 diplomatic staff in Brussels, with four people specifically focussed on energy and environment issues, and its mission shares a building with four energy companies, together with the trade body that represents some 270 electricity companies. In comparison, the UK has 84 people with diplomatic accreditation at its representation in Brussels, with just the one person designated to energy matters.

Strategic co-operation on energy policy likelyAs a ‘third party’ country Norway relies predominantly on soft power rather than the hard negotiations that member states have with EU policy makers. Because of Norway’s importance to EU energy supply – and indeed, the EU’s economic and political importance to Norway – the two have strategic cooperation on a range of energy issues, including policy developments and the implementation of EU energy rules in Norway. The UK’s importance in petroleum products and gas supply means it is likely the UK and EU would have an enhanced relationship in this area after Brexit.

Power market review 2016 11

12 willistowerswatson.com

Switzerland option: EFTA

No automatic EU regulation enforcementSwitzerland is a member of EFTA, along with Norway, Iceland and Lichtenstein, but unlike these countries it is not a member of the EEA. EFTA is an intergovernmental organisation that promotes economic integration and free trade between its four members, but it does not include political integration nor the automatic enforcement and application of EU single market regulations. EFTA is the EU’s third largest trading partner in manufactured goods and the second largest in services. The UK was originally a member of EFTA until 1973 when it left to join the EU.

Limited bi-lateral agreementsSwiss-EU relations are underpinned by more than a hundred bilateral agreements that have been negotiated on a wide-range of policy areas, the first of which was an agreement in 1972 regarding free trade. However, bilateral agreements in energy and environment are limited. In 2006 a treaty on Switzerland’s participation in the European Environment Agency – which undertakes environmental data collection and advises the Commission on policy – came into force following more than four years of negotiations.

The country is integral for electricity transport in central Europe and the functioning of the EU’s single energy market. But negotiations on establishing a legal framework for Switzerland’s participation in the European electricity market which started in 2007 are unfinished, and they had to be extended in 2010 as no solution was reached, despite the framework being a central part of the Swiss Federal government’s 2050 energy strategy.

“ CETA took seven years to negotiate and its scope is far more limited than a UK-EU agreement would need to be. It prioritised the trade of commodities, minerals and agricultural products, and made scant reference to the service sector – the UK’s largest.”

‘Canada option: “hard” Brexit

The UK would still have access to the single market as a WTO member. In the event of no agreement being reached by the end of the 2-year Article 50 period, UK-EU relations would revert to a WTO rules-only basis for trade. Such a situation would not allow the UK preferential access to the single market or to the 53 countries which have free trade agreements with the EU.

But some WTO-only countries do have agreements with the EU – such as Canada. A free trade agreement between the EU and Canada, the Comprehensive Economic and Trade Agreement (CETA), was signed in July 2016. It is referred to by some as an example of a successful agreement the UK could reach with the EU without needing to be a member of either the EEA or EFTA; however this ignores the specific focus of the agreement.

Limited scope of Canadian agreementCETA took seven years to negotiate and its scope is far more limited than a UK-EU agreement would need to be. It prioritised the trade of commodities, minerals and agricultural products, and made scant reference to the service sector – the UK’s largest. The focus of the agreement reflects the EU’s dependence on imported energy and minerals, and Canada’s desire to sell them. There is also no common agreement in CETA on setting standards and regulation, and therefore it does not offer the same degree of access to the single market that the UK enjoys now or would have under EEA or EFTA membership. Ironically, if the UK leaves the EU after CETA has been ratified it could end up having to subsequently renegotiate an agreement with Canada, even to secure what had previously been agreed under CETA.

CETA ratificationCETA has now been signed by Canadian Prime Minister Justin Trudeau, but has still to be finally ratified. Under the Lisbon Treaty the European Parliament technically has to ratify trade deals, but the European Commission has partially deferred CETA ratification to member states. The process hit a substantial block in November as the Wallonian regional parliament in Belgium initially blocked the treaty. The Belgian government is required to consult and gain approval from its regional parliaments, but there had been hostility to CETA in Wallonia because of fears of further deindustrialisation and job losses because of Canadian imports. Any future trade deals between an independent UK and the EU could also have to be approved by member state governments, leaving the process open for delay and potential collapse.

Power market review 2016 13

Conclusion: post-referendum policy change is already underway

UK energy regulations to be watered down?Although the exiting process has yet to formally begin, separately the UK government has already made changes to its energy policy. The Department of Energy and Climate Change (DECC) that was established in 2008 was disbanded following the referendum. Its successor, the department for Business, Innovation and Industrial Strategy (BEIS), has signalled the government’s intent to incorporate energy within a wider set of industrial policies. But with the climate change element removed – at least in name – and a lack of clarity regarding the future of EU environmental quality and climate change policies in the UK, there are fears from environmental groups that the government could water down the scope and requirements if it introduces new legislation to replace that of the EU.

Even before the referendum, UK energy policy was diverging from that of the EU in a number of areas. For example, the push to develop shale gas in the UK puts it at odds with a number of EU member states – such as Germany, Denmark, France and Spain – that are in the process of or have already adopted bans or moratoria on fracking. The new UK government has promised to reinvigorate the nascent shale sector, and in August it set out plans to distribute a share of tax revenues from producing areas to local communities, and even directly to households. This was followed by a decision in October by the government to overrule Lancashire County Council planning authority’s previous decision and give the go-ahead for shale gas exploration to take place.

New policy decisions requiredSerious policy decisions will need to be taken on energy by the new government in the years between now and the eventual exit from the EU, but resources are likely to be dedicated to Brexit above most other areas. Long-term challenges include adapting the energy system to growing levels of intermittent renewable electricity sources, ensuring power supply despite the closure of aging coal and gas fired power stations, declining output from North Sea fields and their eventual decommissioning, and large infrastructure investment decisions – including on new nuclear power plants. All of these would be present regardless of the referendum, but government now has to contend with the prospect of potentially unpicking and rewriting many decades of legislation while simultaneously ensuring that the UK energy system is fit for the future.

Joseph Dutton Research Fellow, Energy Policy Group, University of Exeter

Sources

British Insurance Brokers’ Association (2016): ‘BIBA asks government to consider 11 points affecting brokers and their customers during brexit negotiations’ https://www.biba.org.uk/press-releases/biba-asks-government-consider-11-brexit-points/

CapX (2016): ‘The Canda-EU trade deal is no model for Brexit’ http://capx.co/the-canada-eu-trade-deal-is-no-model-for-brexit/

Digest of UK Energy Statistics, 2015 (2016): https://www.gov.uk/government/statistics/digest-of-united-kingdom-energy-statistics-dukes-2015-printed-version

HM Government (2015): ‘Alternatives to membership: possible models for the United Kingdom outside of the European Union’ https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/504604/Alternatives_to_membership_-_possible_models_for_the_UK_outside_the_EU.pdf

House of Commons Library (2013): ‘Leaving the EU’ (Research Paper 13/42)

House of Commons Library (2014): ‘European Union (Referendum) Bill’ (Research Paper 14/55)

Office for National Statistics (2016): http://visual.ons.gov.uk/uk-energy-how-much-what-type-and-where-from/

Reuters (2015): ‘Britain banks on electricity imports to keep lights on’ http://www.reuters.com/article/britain-power-interconnectors-idUSL5N11V1LO20150925

Vivid Economics (2016): ‘The impact of Brexit on the UK Energy Sector’ http://www.vivideconomics.com/wp-content/uploads/2016/03/VE-note-on-impact-of-Brexit-on-the-UK-energy-system.pdf

“ The new UK government has promised to reinvigorate the nascent shale sector, and in August it set out plans to distribute a share of tax revenues from producing areas to local communities, and even directly to households.”

14 willistowerswatson.com

Power market review 2016 15

Risk-based design for critical facilitiesThe problem with process facilitiesTropical storms are capable of causing unprecedented levels of damage to coastal developments throughout the world. Process facilities residing in these coastal developments are a critical part of the world economy. Damage and prolonged outages have proven particularly disruptive to manufacturers, agriculture, airlines, and motorists. Not only can floodwaters and extreme winds from tropical storms damage numerous types of assets at these facilities, but they can also cause prolonged power outages, supply disruptions, and widespread employee dislocations, all major contributors to both property and business interruption losses.

Process facilities such as power plants typically have some of the following basic components: process structures, process towers, tanks of various sizes, compressors, drums, exchangers, furnaces, pumps, reactors, pipe racks, cooling towers, storage warehouses, control rooms, maintenance buildings and an administration building. Most process facilities were built during a period (pre-1982) that preceded more modern standards for minimum design loads for buildings and other structures with regard to extreme wind events.

Historically, most components of process plants impacted by tropical storms sustain nominal, if any, wind damage. Thick-walled steel process towers, pipe racks, smaller process vessels, larger tanks, control rooms, and fully engineered buildings designed to support administrative and operations functions perform relatively well. However, it is also a historical fact that a majority of process facilities located along tropical coastlines have not experienced a design-level wind event. A direct hit by a stronger storm could therefore result in major damage to a substantially larger portion of the components within these plants.

Process building risk characteristicsIn general, process buildings are fully engineered, heavy steel buildings with average to weak cladding strengths that are designed for heavy equipment and operating loads. Storage warehouse buildings are usually large span, pre-engineered metal buildings with average to weaker cladding strengths. A large percentage of both of these types of buildings are open frame structures, with damage thus comprised mainly of roof cladding damage and debris impact damage. Most control rooms are either constructed of reinforced cast-in-place concrete or reinforced concrete block, or are fully engineered steel buildings with metal cladding. Administration buildings are usually either pre-engineered metal buildings, or are constructed of un-reinforced masonry. Maintenance buildings are typically large span, pre-engineered, metal buildings.

Collapsed storage tanks

Storage tanksStorage tanks vary significantly in size. Larger tanks tend to fail due to inward collapse of the tank wall caused by lateral wind pressures, while smaller tanks tend to fail due to local buckling of the tank wall cause by wind-borne debris impacts, or in some instances simply toppling over. Large empty tanks either without a roof, or with floating roofs that rested at the bottom of an empty tank, are usually more vulnerable to extreme wind effects due to the absence of sufficient lateral support. By contrast, tanks that have wall stiffeners, fixed roofs, product inside, or a combination of these features, fare better given the added lateral stiffness provided in each case.

16 willistowerswatson.com

Cooling towersOf all the components of a process facility, cooling towers typically sustain the greatest amount of damage. Often constructed of wood with thin-wall shrouds on top, these structures exhibited various forms of damage, from broken slats to collapsed frames. In recent years designers of cooling towers have sought to comply with the performance-based criteria of ASCE/SEI 7 which establishes a minimum design load for buildings and other structures.

However, in many instances cooling towers are often older structures (30+ years) that have experienced notable material degradation of their wooden members over time, particularly when exposed to coastal environments. Although considered a less costly part of a process plant, successful operation of these towers is crucial to the ongoing operation of a facility.

Process towers Dislodged or torn insulation is a common form of wind damage to process towers. Failures of straps and fasteners result in the loss of metal coverings, allowing exposure of insulating materials to the environment and thus allowing high winds to pull insulating materials, some made of asbestos, away from vessel surfaces. However, given their weight and supporting foundations, rarely do process towers experience structure distress in the form of collapse or tilt due to high winds.

Wooden pole failuresWooden pole failures are prominent throughout areas stricken by tropical storm winds. Lines on hundreds of these damage poles have to be restrung and pulled. Prolonged power outages can be attributable, in large part, to the time it takes to repair downed poles. Experience shows that metal or reinforced concrete poles well anchored into the ground are more likely to withstand extreme wind loadings than their wooden counterparts.

The time required to replace these structures, including lines and transformers, depends on the extent of utility crew mobilization and on the priority given to a particular area or site. Emphasis is often placed on repairing downed transmission lines first, followed by distribution lines serving areas with critical functions like hospitals, then to other areas of a community. Emphasis may also be placed on restoration of a facility if its function is deemed to be critical to recovery efforts like a gasoline refinery.

Other forms of plant damage observed following hurricanes include flare tower collapse, telecommunication tower collapse, and construction crane failure. Among the greater concerns regarding tower structures is the threat they pose to nearby structures in the event that they topple over.

Collapsed cooling towers Wooden pole failure

Power market review 2016 17

Calculating wind loads and loss probabilitiesCurrent codes and standards do not address all aspects of defining wind loads for process facilities. Therefore, many engineers and companies involved in the industry have developed procedures and techniques for calculating wind loads on such structures. This lack of standardization in the industry can lead to inconsistent structural reliability. As documented in a publication (ASCE 2011) issued by the Task Committee on Wind-Induced Forces of the Petrochemical Committee of the Energy Division of the American Society of Civil Engineers, the variation in wind load estimation techniques was extremely large. The publication Wind Loads for Petrochemical and Other Industrial Facilities was subsequently issued to provide designers guidance for determination of wind loads on common types of plant components.

Knowing the chances that a certain type of event (e.g., a 100-yr event) will occur during the expected or planned operating life of a plant can be beneficial toward understanding the risk exposure of a facility to an extreme event like a hurricane.

The table below shows the probability that a particular type of event, for example a hurricane, will occur at a site during a certain time period. The calculation is based on a Poisson distribution where the probability Pn that an event associated with an annual probability Pa (in decimal form) will be equalled or exceeded at least once during an exposure period of n years is given by:

Pn = 1 – (1 – Pa)n

Occurrence Probability, Pn (%)

Annual Probability, Pa (%)

Return Period (years)

Exposure Period, n (years)

10 15 20 25 30 50 100

10 10 65 79 88 93 96 99 99.9

4 25 34 46 56 64 71 87 98

2 50 18 26 33 40 45 64 87

1.3 75 13 18 24 29 33 49 74

1 100 10 14 18 22 26 39 63

0.4 250 4 6 8 10 11 18 33

0.2 500 2 3 4 5 6 10 18

0.1 1000 1 1 2 2 3 5 10

18 willistowerswatson.com

Assume that the annual probability of a moderate Category 3 storm striking an existing plant is one percent (1%, or 0.01, i.e., the 100-yr event), and that the plant is scheduled to operate for 30 more years. Therefore, the probability is 26 percent, or about 1 in 4, that the plant will experience a moderate Category 3 (or greater) storm during the next 30 years. When considering applicable design standards and associated factors of safety at the time of construction, such an event represents a reasonable threshold of major damage for many process facilities.

Adopting the practice of risk-based designIn recognition of these levels of natural hazard exposures, companies of all types are more readily adopting the practice of risk-based design in recognition that some facilities are more critical than other facilities in terms of their overall contribution to company or agency operations. Examples include structures that contain control systems, unique equipment, or a major hazard to life safety. Such critical facilities require designs that are significantly stronger than conventional facilities. However, unless specified otherwise by the operator of a process facility, the designer will typically use the minimum required value, which often reflects an un-factored load associated with a 50-year return period event (2% annual probability of exceedance).

Coastal plant operators with catastrophic exposure have been known to experience notable increases in their insurance premiums and restrictions in coverage following the occurrence of a major tropical cyclone. For example, after Hurricanes Katrina and Rita in 2005 some Gulf Coast operators saw deductibles increase from two to five percent, wind sub-limits of US$150m or less imposed, and business interruption coverage withdrawn, even though most power and petrochemical facilities did not experience a design-level wind event. However, the damage sustained and associated costs, particularly with respect to business interruption, underscored the apparent uncertainty associated with exposures of these facilities to an extreme wind event.

Adopting a design beyond the required code levelIn addition to traditional insurance, plant operators have other options to- mitigate their risk exposures to hurricanes. For a new design, one option is to adopt performance-based design where the design-level event selected for the new facility is beyond the required code level. For example, critical plant components can be designed for a 250-yr return period event instead of a 50-yr event. The steps taken to determine the best approach for implementing a mitigation plan are:

1. Determine the occurrence probability for the event. In the case of extreme wind, the gust wind is determined as a function of exceedance probability (or return period).

2. Determine the level of damage associated with a given wind speed. This effort may require separating the components of a facility into categories of structures and equipment, then determining the associated vulnerabilities based on historical experience, published data, or engineering analyses.

3. Create a loss hazard curve showing the level of damage as a function of exceedance probability for an associated wind speed.

4. Identify mitigation options for the categories of structures and equipment, where deemed reasonable, the associated cost for each option, and the resulting reduction in estimated losses.

5. Create another loss hazard curve showing the reduced level of damage given the implementation of mitigation measures as a function of exceedance probability.

6. Integrate the two loss curves (i.e. calculate the area underneath each curve) and subtract the two values to get an estimate of the expected annual loss reduction. Once this value is known, a determination can be made about the economic feasibility of the proposed mitigation measures for the operating life of the plant.

“ For a new design, one option is to adopt performance-based design where the design-level event selected for the new facility is beyond the required code level.”

Power market review 2016 19

Conclusion: risk of 100 year storm impact can now be definedIn summary, process facilities as a whole have performed relatively well in terms of wind damage to plant components during tropical storm events. However, most process facilities have not experienced a design-level wind event. Most of the direct damage has been to cooling towers, utility poles, supply/storage (metal) buildings, and insulation on process vessels. Major business interruption losses were incurred primarily due to prolonged power outages, to displaced employees, and also to the effects of flood damage. Loss of cooling water capacity due to damage sustained by cooling towers also contributed to downtime at some facilities. A direct hit by a stronger storm could result in major damage to a substantially larger portion of the components within these plants.

The chances that a specific mean recurrence interval wind event (e.g., a 100-year storm) will occur during the expected or planned operating life of a plant can be determined, and is beneficial toward understanding the risk exposure of a facility to an extreme event like a hurricane. Heightened awareness of natural hazard exposures has led companies of all types to more readily adopt risk-based design practices in recognition that some facilities are more critical than other facilities in terms of their overall contribution to company operations.

Bob Bailey Houston Office Director and Senior Managing Engineer, Exponent

Further reading:Minimum Design Loads for Buildings and Other Structures, ASCE Standard ASCE/SEI 7-10, published by the American Society of Civil Engineers, 2010.

Wind Loads for Petrochemical and Other Industrial Facilities, Task Committee for Wind Load Design for Petrochemical Facilities, published by the American Society of Civil Engineers, 2011.

20

00 0.1

0 10 100 1,000 10,000 100,000

0.01 0.001 0.0001 0.00001

40

60

80

100

120

140

160

180

200

Loss

($M

)

Exceedance Probabillity

Return Period (Years)

With mitigation

Without mitigation

Annual Benefit: $780,000B/C Ratio: 2.0Annual expenditure: $390,000Discount rate: 5.0%Operating life: 25yrs

Present value cost: $5,496,638

20 willistowerswatson.com

Employee Value Proposition and Total Rewards: modernize or risk being irrelevant

Findings from Willis Towers Watson’s 2016 Global Talent Management & Rewards and Global Workforce Studies

Attraction, retention and sustainable engagement drivers in 2016

During the second quarter of 2016, Willis Towers Watson’s Human Capital Practice conducted two parallel studies:

�� Global Talent Management & Rewards Study (TM&R), involving 2,004 employer respondents representing over 21 million employees

�� Global Workforce Study (GWS), which involved over 31,000 employee respondents

Of these participants, 66 in the TM&R and 463 in the GWS came from the Utilities sector, with companies and employees around the world.

The main purpose of the studies was to provide employers with an understanding of the drivers of attraction, retention and sustainable engagement in a world in which workforces are facing increasing pressures and stress.

Each study looked at areas specifically relevant to their respondents, such as talent mobility and challenges, total rewards and pay for performance (TM&R) and drivers of sustainable engagement, health, stress, wellness and communication (GWS).

2016 Global Talent Management & Rewards Study

Asia Pacific

EMEA

Latin America

North America

35%

21%

18%

26%

20 willistowerswatson.com

Power market review 2016 21

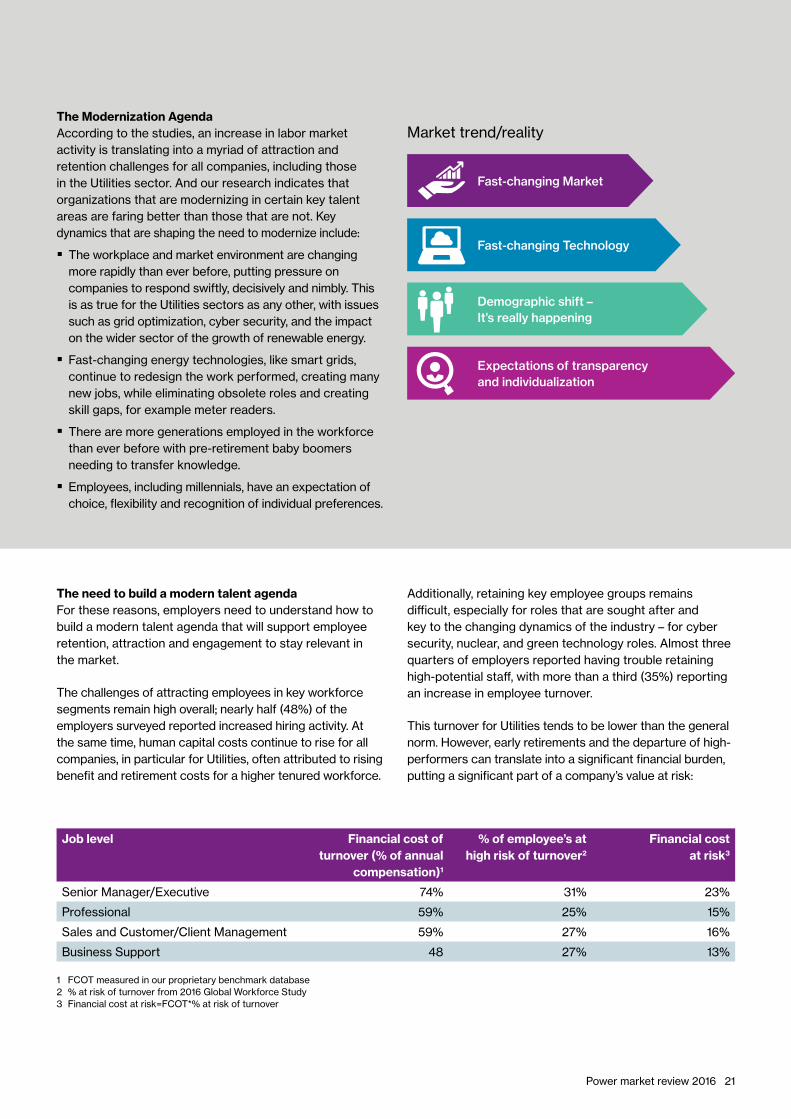

The Modernization AgendaAccording to the studies, an increase in labor market activity is translating into a myriad of attraction and retention challenges for all companies, including those in the Utilities sector. And our research indicates that organizations that are modernizing in certain key talent areas are faring better than those that are not. Key dynamics that are shaping the need to modernize include:

�� The workplace and market environment are changing more rapidly than ever before, putting pressure on companies to respond swiftly, decisively and nimbly. This is as true for the Utilities sectors as any other, with issues such as grid optimization, cyber security, and the impact on the wider sector of the growth of renewable energy.

�� Fast-changing energy technologies, like smart grids, continue to redesign the work performed, creating many new jobs, while eliminating obsolete roles and creating skill gaps, for example meter readers.

�� There are more generations employed in the workforce than ever before with pre-retirement baby boomers needing to transfer knowledge.

�� Employees, including millennials, have an expectation of choice, flexibility and recognition of individual preferences.

The need to build a modern talent agendaFor these reasons, employers need to understand how to build a modern talent agenda that will support employee retention, attraction and engagement to stay relevant in the market.

The challenges of attracting employees in key workforce segments remain high overall; nearly half (48%) of the employers surveyed reported increased hiring activity. At the same time, human capital costs continue to rise for all companies, in particular for Utilities, often attributed to rising benefit and retirement costs for a higher tenured workforce.

Additionally, retaining key employee groups remains difficult, especially for roles that are sought after and key to the changing dynamics of the industry – for cyber security, nuclear, and green technology roles. Almost three quarters of employers reported having trouble retaining high-potential staff, with more than a third (35%) reporting an increase in employee turnover.

This turnover for Utilities tends to be lower than the general norm. However, early retirements and the departure of high-performers can translate into a significant financial burden, putting a significant part of a company’s value at risk:

Job level Financial cost of turnover (% of annual

compensation)1

% of employee’s at high risk of turnover2

Financial cost at risk3

Senior Manager/Executive 74% 31% 23%

Professional 59% 25% 15%

Sales and Customer/Client Management 59% 27% 16%

Business Support 48 27% 13%

1 FCOT measured in our proprietary benchmark database2 % at risk of turnover from 2016 Global Workforce Study3 Financial cost at risk=FCOT*% at risk of turnover

Market trend/reality

Fast-changing Market

Fast-changing Technology

Demographic shift –It’s really happening

Expectations of transparencyand individualization

22 willistowerswatson.com

Modernizing your EVP should be accomplished in the context of an overarching human capital framework

Leadership

Measurement, Change Management, Communication and HR Technology

EVPEmployee Value

Proposition

Desired Culture

HumanCapital

Strategy

almost 3x as likely to report theiremployees are highly engaged

93% more likely to report significantlyoutperforming their industry peersfinancially

27% fewer regrettable new hires in the first year

More than 10% less likely to reportdifficulty attracting and retaining keyemployees segments

OutcomesHuman capital dimensionsBusiness strategy

17% lower voluntary turnover

Best practice EVP companies achieve better outcomes

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only. 4

GLOBAL

As part of the modernization agenda, companies need to be agile and nimbly respond to changes in business strategy and talent markets. Some primary practices of forward-thinking companies include:

�� Introducing flexible practices into talent and reward plan design/delivery – innovation as a driving force

�� Improving transparency in talent and reward programs – facilitated with open and honest communication

�� Tailoring programs to key segments of the workforce – one size does not “fit” all

�� Leveraging technology to digitally engage employees – the right technology is your “friend”

�� Transitioning from job security to relevance or career security – employees are “consumers” of your programs

�� Address work place stress – happy and healthy employees are more engaged.

The organizations that implement forward-thinking strategies to address the key human capital challenges such as early and/or delayed retirements, attraction of the millennial workforce, reduced training budgets, and minimal base salary increase, will be the ones that successfully modernize and address the challenges of today’s workplace and will remain relevant.

Getting Your EVP Right

Part of any modernization agenda needs to include defining and implementing a well thought out Employee Value Proposition (EVP). The EVP is the “deal” between the employee and employer which differentiates a utility from its talent competitors. The Utility industry has not traditionally been viewed as a leading-edge industry to work in, and today may be competing for talent within the broader technology and energy markets – therefore it needs to learn from these sectors as it vies for talent. As such, best practice EVP companies have:

�� A formally articulated talent differentiation strategy that is clearly aligned with what they stand for in the marketplace

�� As good an understanding of their employees and potential candidates needs as their external customers.

�� A customized EVP for high-potential employees, as well as those with critical skills

�� An effective communication plan that leverages technology to better understand employees’ preferences and delivers differentiated messages by employee segment

Best practice EVP companies achieve better outcomes

Power market review 2016 23

Understanding the top down driversWhen considering updating an EVP, a good place to start is to gain an understanding of the top drivers of employee attraction and retention. Employers need to know that what they regard as the top drivers may not be the same as those of the employees they are trying to attract.

For example, our studies indicate that base pay/salary was the number one attraction driver by employers. In contrast, employees ranked career advancement opportunities as the main attraction criterion, with employers considering this to be a less important driver. This is particularly the case for millennials who desire and expect progression at a quicker rate than other age employees and who may feel “held back” due to delayed retirements of older colleagues. Similarly, employers placed job security as the number two attraction driver, but for employees this was much less important, at number five.

This disparity also revealed itself in the top drivers of retention, or the reasons employees choose to remain with or leave an organization. Base pay/salary and career advancement opportunities were cited as the two most important criteria by both employers and employees, but in the opposite order. Interestingly, while employees ranked base pay/salary as the number two attraction driver, it was their number one retention criterion.

Employees also cited job security as an important retention factor, but this does not even appear in the employers’ view of top retention drivers. Additionally, this picture can get clouded by the fact that job security can mean different things to different people. For some their sense of job security may be defined by whether or not they are fearful of losing their job, whereas for others it may be defined by apprehension that their job will change and take them outside their comfort area. A number of jobs in the power and utilities sector have changed over the last few years as a result of renewable energy reliance and the security focus.

As part of the modernization agenda, companies need to acknowledge key differences in perspective and utilize this data to better tailor their talent and reward offerings to their specific employees’ concerns.

Effective Leadership Drives Engagement Having effective leaders is a critical foundational element to delivering a compelling EVP. Employers that are looking to or have already modernized their Talent and Reward agenda have recognized and acknowledged the important role leadership plays.

Feedback indicates that 61% of global respondents and 68% of Utilities agree or strongly agree that they develop leaders who will be able to meet changing business needs today and in the future – however this means that 32% of utility companies do not share this confidence.

For employees, there is also a strong desire to have authentic leaders who are honest to employees and can think ahead. An idea being utilized at some companies in the Utility sector is hiring back some of these seasoned, high-performing employees as contractors to help provide mentorship and skill-growth.

When asked to rate their senior leadership on the below statements, fewer than 50% of employee respondents gave their senior leadership a favorable rating.

�� I believe the information I receive from senior leadership

�� I have trust and confidence in the job being done by the senior leadership of my organization

�� Senior leadership at my organization has a sincere interest in employees’ well-being.

It is noticeable that the favorable percentages among Utilities employees were lower than the global average.

My organization makes effective use of a leadership competency model

Leadership development

61%

46%35%20%

Agree/Strongly Agree

Currently have

Plan to add in the next year or two

No plans

24 willistowerswatson.com

Highly Engaged

Unsupported

Detached

Disengaged67%

5%

17%

11%

33%

25%

24%

18% 23%

20%

32%

26%

9%

11%

26%

54%

Both e�ective

E�ective seniorleaders and ine�ectivemanager

E�ective managerand ine�ectivesenior leaders

Both ine�ective

When asked how they would rate the job that their senior leadership was doing to grow the business, manage costs and develop future leaders, again only a minority of employees gave a favorable rating, particularly when it came to developing the next generation of leaders. Since succession management is a key enabler of developing future leaders, there is a significant opportunity for a majority of employers to do more.

In terms of leaders enabling employees to perform at the highest levels possible, under 20% think their employers are providing development opportunities to top talent by removing or redeploying “blockers.”

Interestingly, employees give their immediate managers better marks than senior leaders, with favorable ratings consistently above 50% – with the exception of the sensitive issue of making fair decisions about how the employee’s performance links to pay decisions.

Lastly, our research indicates that it is not enough to have either highly effective leaders or highly effective managers. Both must be fully invested in supporting the EVP for employers to see significant increases in employee engagement levels.

My line manager/supervisor has the necessary skills

The People manager role is highly respected in my organization

Lack of effective feedback is the #1 barrier to the performance management experience

42%

45%

45%

49%

Global

Global

Utilities

Utilities

Employees with effective senior leaders and managers are much more likely to be highly engaged

Power market review 2016 25

Creating a Culture of Well Being

Stress the top workforce health issueTwo-thirds of employers globally identify stress as the top workforce health risk issue, with 75% in the U.S. indicating it is a top issue and 64% globally drawing the same conclusion. Not surprisingly, the other top wellness concerns are heavily influenced by stress and include: overweight/obesity (identified by 70% of U.S. respondents, 46% globally), lack of physical activity (61% U.S., 53% globally), poor nutrition (50% U.S., 31% globally) and lack of sleep (31% U.S., 30% globally).

Tackling the causes of stressTo combat this, employers need to focus on workplace stress and wellness, which requires identifying and tackling the main causes of stress. In this area, there are again disconnects between employers’ views and those of employees. As far as employers are concerned, lack of work/life balance is the main cause of stress, but employees report the key issues are inadequate staffing leading to employees being stretched thin due to fewer resources, followed by low pay and company culture. Yet at the same time millennials are reported to desire a greater work/life balance, with a focus on “working to live” versus a “live to work” mentality.

Reducing workplace stress and increasing wellness will involve addressing staffing issues, rethinking pay and changing an organization’s culture. Steps learned from fully optimized companies to ensure a work environment that is conducive to healthy employees includes understanding the following:

�� Moving from a “pull” (encouragement) to a “push” (driving change) for wellness must happen gradually, building employee permission along the way

�� There is a strong connection between health engagement and the broader employment “deal”

�� Leveraging worksites and supporting interactions/competitions between employees around health can be critical drivers of changed behavior

�� It is important for leaders and managers to be effective advocates of employer programs

�� Use technology, peer groups and personal communication to motivate action

In closing: the 5 steps to modernisationMany companies, including those in the Utility sector, appear to be at a crossroad of either modernizing or being left behind when it comes to attracting and retaining the brightest and the best. These organizations have everything to gain by enacting a modernization agenda that will support the creation of a more equal employee-employer relationship and value exchange. If you are an employer who has yet to implement steps towards modernization, you can start by enacting the following measures:

1. Have your leadership team role model transparency, trust and relationship building with the next generation of leaders – the leaders of the future need to be trained by the leaders of today

2. Make room for supervisors and managers to have the time needed to provide effective people management beyond their current operational roles – place importance on the skill of motivating and empowering the workforce

3. Redefine what your talent and reward programs look like – redefine what performance management is, how performance is measured and differentiate pay

4. Create flexible career paths and embrace flexible work arrangements – adaptable programs will often thrive

5. Make technology work for you by leveraging digital media to drive engagement – utilize all of the technology levers at your disposal

Utilities that want to thrive in an environment that is evolving at an unprecedented pace – regulatory changes, green energy initiatives, focused risk management and security needs – need to keep up with an ever changing market place for employee talent, and modernize. Future success requires companies to challenge conventional thinking and re-invent themselves.

Catherine Hartmann Talent and Rewards Senior Consultant, Willis Towers Watson

26 willistowerswatson.com

The rush to renewables in AustraliaDoes Australia need to make haste more slowly?

September storm cast doubt over capacity

In late September 2016, a “once-in-50-years” storm blacked out the entire state of South Australia, thrusting the energy risk debate back into the spotlight.

It was, perhaps, a little unfair to blame the state’s heavy reliance on renewable energy for that particular crisis, which affected Adelaide for days – and much longer in regional areas. South Australia takes 40 percent of its power from wind turbines, which could not operate in high winds, but the main problem came from power distribution infrastructure being knocked out by the storms, including an interconnector linking the state with neighbouring Victoria.

But the emphasis on renewable sources of electricity in South Australia raises significant questions about capacity – not just in that state but for Australia as a whole. This is not the first time South Australia’s energy grid has been found to be fragile and there have also been other documented instances across the country where capacity and security issues have led to soaring costs and intense pressure on supply.

Political debate too simplistic?

In the political context, the debate all too often comes down to a simple equation:

Renewables = good

Fossil-fuelled power = bad

Like many countries, Australia has relied heavily on coal or gas-fired electricity which historically was owned and operated by state-run institutions. The privatisation of energy supply has led to a dichotomy; while governments push energy companies to develop and bring renewable technologies on line, they face a backlash if baseload capacity is diminished.

That capacity has traditionally been provided by environmentally unpopular power plants using fossil fuels. The storms in South Australia put the electricity grid in total shutdown but there have been other occasions where lack of capacity has seen prices spike – another issue one July night saw wholesale prices hit A$9000 per megawatt hour (MWh), where the yearly average was A$60. Essentially, Australia energy prices are free-flowing, up to a $14,000 MWh ceiling mandated by Australia’s Energy Market Operator (EMO).

Power market review 2016 27

The role of the RET in the price spike

The causes of that spike were described at the time as “complex” but there is little doubt that Australia’s Renewable Energy Target (RET) is playing a role. The RET mandates that 23.5 percent of electricity must be drawn from renewable sources by 2020. The issue with South Australia is that it has gone further down the renewables path – and faster – than any other state or territory in the country and many other jurisdictions around the world.

In the September storm’s immediate aftermath, there was a shift in political rhetoric. The independent senator from South Australia, Nick Xenophon was quoted in media as saying the state’s energy arrangements were “a textbook case of how not to transition to renewable energy”.

A wake-up callSouth Australia is a wake-up call that has reverberated around Australia. In the rush to take up renewable technologies, the full impacts on the community at large have not been adequately considered. The EMO must be seen as the major culprit here, having failed to ensure that appropriate redundancies are in place, not only for uninterrupted supply but price stability.

Tasmanian exampleLet’s take another example. Tasmania has a long history of generating hydro-electricity. In the quest for much-needed revenues, the state supplied energy to mainland Australia during the period of the federal Labor government’s carbon pricing scheme, using the Basslink undersea power cable.

While hydro-electricity is an efficient way of generating power, it has one major caveat – it needs water. Tasmania made a lot of money in that period, but ran its dams to low points and seasonal rains were disappointing. When it could no longer use its hydro system to generate enough power, Tasmania found itself having to import 40 percent of its electricity needs. Then, in December 2015, the state was hamstrung by a fault in Basslink. As a result, a gas-fired power station in the Tamar Valley had to be brought back online.

So if water doesn’t flow, the sun doesn’t shine and there’s too little (or too much) wind, where does that leave Australia in terms of energy security and how can organisations manage energy risk?

The Basslink problems took more than six months to resolve with industry sources putting the economic cost of its failure at more than A$560 million. That figure apparently did not include an estimate of lost production from major manufacturers and miners in Tasmania who were required to cut back on their energy use. The Tasmanian government also had to contend with greatly reduced revenues from Tasmanian Hydro, while wholesale power prices in the island state increased four-fold to A$177 MWh in the March quarter 2016.

A reactive rather than measured approachSimply, there is no reason why outrageous price spikes should occur, but the aggressive removal of fossil fuel power generation and the maintenance of the facilities that remain to ensure that infrastructure can cope with whatever challenges are thrown at it, are resulting in enormous risks.

Many of the older facilities throughout Australia require significant capital expenditure but the push to renewables makes energy companies think twice about making that level of investment. How they run their plants, and their businesses, is done in a reactionary rather than a measured way.

Energy market systemAnd that’s the problem. Australia has developed an energy market system, not a capacity system. Energy companies are not paid for their power plants – only if they’re operating.

This is not the same as some other jurisdictions such as the UK, where a capacity market was introduced in 2014 to meet the twin challenges of a loss of capacity due to the impending closure of a large number of power plants and the need to accommodate the variability in output of the growing amount of renewable generation.

The UK schemeThe UK scheme awards payments, allocated following an annual auction, to power generation companies in exchange for an undertaking to be available when required. Its purpose (as stated by the UK government) was to “ensure security of electricity supply by providing a payment for reliable sources of capacity, alongside their electricity revenues” and to “encourage the investment we need to replace older power stations and provide backup for more intermittent and inflexible low-carbon generation sources” (source: https://www.gov.uk/government/collections/capacity-market-2016).

(It should be noted, however, that the design of the UK capacity market has attracted criticism, for example for the unintended consequence of acting contrary to the UK’s decarbonisation goals by rewarding coal- and diesel-fired generation, and earlier this year the government conducted a formal consultation on possible reforms to the capacity market.)

In Australia by contrast, the EMO and its predecessor has slowly taken a more authoritarian position within the marketplace over the past 20 years or so. Simply put, given oversight of the industry it gained more and more power to make instructions to energy companies. That seemed to work until the carbon pricing scheme was introduced in 2012 and renewables were heavily promoted.

28 willistowerswatson.com28 willistowerswatson.com

Power market review 2016 29

Victoria example – energy generators frozen in their seatsFrom there, quite frankly, it all became quite bizarre. Let’s take as an example a power station located in Victoria, which burns environmentally unfriendly brown coal. In 2012 their short-run costs to generate power were below A$5 per MWh, while the market wholesale price was around A$35 per MWh. Carbon was priced at A$20 per tonne under the scheme, which, due to their use of brown coal, equated to an increase in their fuel costs of approximately A$30 per MWh. This meant that their total generating costs were now only marginally less than the market wholesale price, almost completely eroding their profit.

But then federal government compensation to fossil fuel generators kicked in, to the tune of billions of dollars. Energy companies found themselves sitting on a pile of cash and many dropped their coal-fired production substantially – but 18 months after the scheme took effect, it was repealed.

The idea was to force companies to make the case for renewables but this was also a period of political turmoil. It was hardly surprising then, that some energy generators were effectively frozen to their seats.

The rise and rise of battery power

Australia is seeing a more moderated approach to renewables, thanks mainly to the funding and input of the Australian Renewable Energy Agency (ARENA).

Technology is also starting to help make better use of what can be generated through renewable sources, especially solar energy. The coupling of storage to photo-voltaic cells is seeing solar being taken up at a rapid rate. For the first time, users have been able to get their power generated during the day and use it at night rather than merely feeding back into the electricity grid. It has overcome one of the major issues with solar – the need for very expensive equipment on the roof that doesn’t necessarily give a return on investment.