potential of micro finance of j&k

TRANSCRIPT

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Summer TrainingProject Report

On

Potential of micro finance of j&k

Submitted toSt.Soldier Management & Technical Institute Jalandhar

In Partial Fulfillment of the RequirementsFor the Degree of

Master of Business AdministrationJune – August 2009

Submitted by BILAL AHMAD

ST.SOLDIER MANAGEMENT & TECHNICAL INSTITUTE

JALANDHAR

1

Potential of micro finance of j&k( A COMPARATIVE STUDY )

ACKNOWLEDGEMENT

I would like to acknowledge the invaluable

assistance extended by Mr.Reyaz Ahmad Mir,

Cluster II head Distt.BARAMULLA Who gave me

his kind permission to successfully complete the

project in his organization. I would like to pay

my heart full gratitude to Mr. Mohd Aslam and

Mr. Javid Ahmad Of Human Resource

Department of J&K Bank who provided me their

timely guidance to me at every step and also

provided to me all relevant and essential data

regarding my project report .I also feel a sense

of indebtedness to my reverent teacher MRS

PALKI SHARMA. who encouraged ,motivated and

guided to complete my project report .

Finally, I would also like to thank my parents

and friends who inspired me and encouraged

me to complete my project at J&K Bank in time.

2

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Bilal Ahmad

Table of Contents:I. EXECUTIVE SUMMARY……………………………………………………………………………….3

II.ACKNOWLEDGEMENT………………………………………………………………………………..6

III.ABSTRACT……………………………………………………………………………………………...7

IV.COMPANY PROFILE………………………………………………………………………………….8

V.INTRODUCTION.......................................................................................................................................10

V. MICROCREDIT …..……………………………………………………………………………………..11

VI.MICROFINANCE AND POVERTY ELLEVATION…………………………………………………12

VI.1.REQUIREMENT OF MICROFINANCE……………………………………………………12

VII.HOW DOES MICROFINANCE HELP POOR……………………………………………………..13

VIII. MICROFINANCE

INSTITUTIONS…………………………………………………………………..15

IX.GLOBAL SCENERIO OF

MICROFINANCE………………………………………………………….17

X.MICROFINANCE NETWORK

…………………………………………………………………………...19

X.I. KEY RESULTS OF MICROFINANCE……………………………………………………….23

XI.MICROFINANCE IN INDIA……………………………………………………………………………24

XI.1.PRESENT SCENARIO………………………………………………………………………….25

XI.2. POVERTY ELEVATION AND CONCEPTUALISATION…………………………………26

XII. MICROFINANCE IN JAMMU AND KASHMIR……………………………………………….…36

XII.1 OCCUPATIONAL PROFILE……………………………………………………………………

36

AN OVERVIEW OF CURRENT SCENARIO IN J & K………………………………………………..

3

Potential of micro finance of j&k( A COMPARATIVE STUDY )

SUGESSTIONS………………………………………………………………………………………………59

CONLUSION………………………………………………………………………………………………….6

0

BIBLOGRAPHY

Executive Summary

Indian banking system, which is among the largest banking networks in the world, did not reach most of the rural poor in India. About 70% of the Indian population from rural areas accounted for only 30% of bank deposits. The banks did not meet the credit requirements of the poor and they were forced to fall back on moneylenders for credit. Though the banks were nationalized, they perceived rural credit to be a high risk and high cost proposition. The rural borrowers were bogged down by elaborate procedures that were required to obtain loans.

The central bank in India, RBI, on its part, tried to cater to the needs of the rural poor by establishing regional rural banks and cooperative banks, but did not meet with success. In the early 1990s, to provide credit and savings services to the poor, microfinance was envisaged. It received further boost with involvement of several non-governmental organizations and microfinance institutions.

These efforts led to formation of Self Help Groups (SHGs), where poor from homogenous background formed into groups of around 20 each and pooled money that was lent to the needy in the group. By the mid 1990s, several mainstream banks began providing credit and savings facilities to SHGs that built credible financial discipline. The program was called SHG – Bank linkage program. Over the time, the banks provided other facilities like housing loans and micro insurance services to the poor.

There were for profit MFIs, mutual benefit MFIs and not for profit MFIs that participated actively in spreading microfinance initiatives across India. By 2004, there were around 1,000 MFIs in the country. Realizing underlying potential of microfinance, several commercial banks entered into partnership with MFIs. Both banks and MFIs stood to benefit from this association as banks could reach the interior part of the country and MFIs could access more funds and thus reach more people.

With the huge potential and low NPAs, several private and foreign banks, unveiled their plans to enter the Indian microfinance sector. The government and the RBI announced

4

Potential of micro finance of j&k( A COMPARATIVE STUDY )

several measures to boost microfinance activities in the country. RBI allowed the NGOs involved in microfinance activities to raise External Commercial Borrowings upto US$ 5 million a year. With increase in competition and availability of funds, the Indian microfinance sector could be the ultimate beneficiary.

Still there are several poor, who were not under the purview of microfinance, the number of SHGs and microfinance programs did not have any major impact on poverty alleviation in the country. Only in some of the well-developed states in the country, SHGs and microfinance gained popularity. Lot of groundwork was required to spread microfinance activities in North and North East regions of the country.

5

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Objectives of the Research:

1. To objective of the research is to understand concept of Microfinance.

2. To find out existing Structure of Microfinance in World and in India

3. . To understand Policies adopted by different bank

4. The main objective of the research is to find out Potential of Microfinance in

Jammu & Kashmir

5. To understand Microfinance structure in J&K Bank and to Find out Flaws if any.

Source of Information:

Primary Source: Through Structured questions. Face to face interview.

Secondary Source: Records maintained by Bank. Websites.

Times of India.

Research Methodology: The study pertains to detailed understanding of concept of Microfinance, its need, Supply and regulatory methods adopted by various agencies. An exploratory research design was adopted to conducted research, method of selecting sample was convenience sampling. Field survey was carried out to collect the necessary data.

Data Used: Both Primary and Secondary Data were used. Websites, Departmental visits, newspapers, Survey magazines, Statistical digest etc were used to collect data.

Data Collection: Though most of the respondents were illiterate so Face to face interview was the main source of collecting data. Respondents were interviewed in a structured format.

6

Potential of micro finance of j&k( A COMPARATIVE STUDY )

A Brief History of Banking

In the recent era, the story of "the Banks" commences with the development of the modern

banking system in Middle Ages Europe. At that time, disposable wealth was usually held in

the form of gold or silver bullion. For safety, such assets were kept in the custody of the

local goldsmith, he usually being the only individual who had a vault on his premises. The

goldsmith would issue a receipt for the deposit and, to undertake financial transactions, the

buyer would withdraw his gold and give it to the seller, who would then deposit it again,

frequently with the same goldsmith. As this was a time-consuming process, it became

common practice for people to simply exchange smiths' receipts when conducting financial

transactions.

As time passed, the goldsmiths began to issue receipts for specific values of gold, making

buying and selling easier still. The smiths' receipts thus became the first banknotes. The

goldsmiths, now fledgling bankers, noticed that at any one time only a small proportion of

the gold held with them was being withdrawn. So they hit upon the idea of issuing more of

the receipt notes themselves, notes that did not refer to any actual deposited wealth. By

giving these receipts to people seeking capital, in the form of loans, the goldsmiths could

use the money deposited with them by others to make money for themselves. It was found

that, for every unit of gold held by the goldsmith, ten times the sum could be safely issued

as notes without anyone usually becoming any the wiser. If a goldsmith held, say, 100

pounds of other people's gold in his vaults, he could issue banknotes to the value of 1000

pounds. As long as no more than 10 percent of the holders of those notes wanted their gold

at any one time, no one would realize the fraud being perpetrated. This practice, known as

"fractional reserve lending," continues to this day and is actually the backbone of the

modern banking industry. Banks typically loan ten times their actual financial holdings,

meaning 90% of the money they lend does not now, never has, and never will exist.

7

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Loans issued by the goldsmiths had to be paid back to them with interest, meaning non-

existent money slowly became converted to tangible assets in the form of goods and labor.

Should the loan be defaulted upon, the banker had the right to seize the defaulter's property.

As time passed, therefore, the goldsmiths became wealthier and wealthier. They had

devised a scheme to create money out of thin air and then convert this money into real

goods, labor, or property. A loan of money at 12% interest recouped not merely 12% for

the banker, but 112%, as it does to this day.

As the industrial era began, so the potential for furthering this scheme increased

exponentially. The goldsmiths were now fully-fledged bankers, and their ability to create

money out of thin air and then convert it into tangible assets enabled them to begin to

control whole industries to the point where the worlds of banking and industry became, to

all intents and purposes, seamless entities.

As the twentieth century dawned, the banking families hit upon a new means to

consolidate and increase their gains. They discovered that by periodically restricting the

money supply crashes within the emergent stock exchanges of the world could easily be

engineered. The most notable example of this was the famous Wall Street Crash of 1929.

What the history books usually fail to record is that, in a crash, wealth is not actually

destroyed, but merely transferred. The "Crash of '29" allowed the most powerful of the

banking and industrial families to absorb the weaker elements, generating even greater

levels of centralized control.

As the technological revolution progressed, so the buying up of TV stations and

newspapers allowed the creation and control of the mass media. This served to ensure that

only a portrayal of events that suited the interests of the elite banking families would get to

public attention - invariably one that all but denied their very existence.

8

Potential of micro finance of j&k( A COMPARATIVE STUDY )

INTRODUCTION ABOUT BANK

In modern age, Banking constitutes the fundamental basis of economic growth. The term

bank is being used since long time but there is no clear conception regarding its beginning.

According to one viewpoint, in good old days, Italian moneylenders were known as Bane

chi or Banacheri, because these people kept special type of table to transact their business,

called Ban chi. Origin of the word bank belongs to the word Banchi or to the Greek word

Banque. Both these words refer to some kind of banking. According to another viewpoint,

bank originated from the German word (ital) Banque meaning Joint Fund.

Casa De SanGiorgio was the first bank to be established in 1148.

The First Public bank of Veanice. It was established in 1157.

As per Banking Regulation Act. 1949, “Banking” means:

“Accepting for the purpose of lending or investment of deposit of money from the public,

repayable on demand or otherwise and withdraw able by cheque, draft, order or

otherwise”

In simple words, bank refers to an institution that deals in money. This institution

accepts deposits from the people and gives loans to those who are in need. Besides dealing

in money, banks these days perform various other functions such as credit creation, agency

job and general service.

Bank, therefore, is such an institution, which accepts deposits from the people,

gives loans, creates credit and undertakes agency work.

9

Potential of micro finance of j&k( A COMPARATIVE STUDY )

“Since the concept was born in Bangladesh almost three decades ago, microfinance has proved its value, in many countries, as a weapon against poverty and hunger. It really can change people’s lives for the better, especially the lives of those who need it most.”

Kofi A. Anan, the UN Secretary GeneralAbstract

More than subsidies poor need access to credit. Absence of formal employment make them non `bankable'. This forces them to borrow from local moneylenders at exhorbitant interest rates. Many innovative institutional mechanisms have been developed across the world to enhance credit to poor even in the absence of formal mortgage. By giving the world’s poor a hand up, not hand out, microfinance can help break the cycle of poverty in as little as a single generation. This project is based on detailed study of Microfinance, its various sources and its implementation. It has been evidenced worldwide that microfinance helps the poor to overcome poverty, and not through charity. It is a financial system that serves the poor with financial services in a most effective and productive wayKey Learnings: Potential unbanked customers in the bottom of the pyramid in India are estimated to range from 6-7 crore, with the propensity to consume credit worth Rs 40,000 crore As banks have so far managed to disburse only around Rs 3000 crore in the segment, the race is picking up momentum

On one side, Indian banks are financing large acquisition deals of large corporates. Simultaneously, they are trying to exploit the opportunity available among the millions of Indians at the bottom of the pyramid (BOP), who are not covered by formal banking system at present.

Nachiket Mor of ICICI Bank comments, “The financially excluded are a big opportunity

10

Potential of micro finance of j&k( A COMPARATIVE STUDY )

HISTORY OF BANKING IN INDIA

Without a sound and effective banking system in India, it cannot have a healthy economy.

The banking system of India should not only be hassle free but it should be able to meet

new challenges posed by the technology and any other external and internal factors.

For the past three decades, India's banking system has had several outstanding

achievements to its credit. The most striking is its extensive reach. It is no longer confined

to only metropolitan or cosmopolitan areas in India. In fact, Indian banking system has

reached even to the remote corners of the country. This is one of the main reasons of India's

growth process.

The government's regular policy for Indian bank since 1969 has paid rich dividends

with the nationalization of 14 major private banks of India. Not long ago, an account holder

had to wait for hours at the bank counters for getting a draft or for withdrawing his own

money. Today, he has a choice. Gone are days when the most efficient bank transferred

money from one branch to other in two days. Now it is as simple as instant messaging or

dialing for a pizza. Money has become the order of the day.

The first bank in India, though conservative, was established in 1786. From 1786 till

today, the journey of Indian Banking System can be segregated into three distinct phases.

They are as mentioned below:

Phase 1:-Early phase from 1786 to 1969 of Indian Banks

Phase 2:-Nationalization of Indian Banks and up to 1991 prior to Indian banking

sector Reforms.

Phase 3:-New phase of Indian Banking System with the advent of Indian Financial

& Banking Sector Reforms after 1991.

11

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Phase I

The General Bank of India was set up in the year 1786. Next came Bank of Hindustan and

Bengal Bank. The East India Company established Bank of Bengal (1809), Bank of

Bombay (1840) and Bank of Madras (1843) as independent units and called it Presidency

Banks. These three banks were amalgamated in 1920 and Imperial Bank of India was

established which started as private shareholders banks, mostly Europeans shareholders.

In 1865, Allahabad Bank was established and first time exclusively by Indian, Punjab

National Bank Ltd. was set up in 1894 with headquarters at Lahore. Between 1906 and

1913, Bank of India, Central Bank of India, Bank of Baroda, Canara Bank, Indian Bank,

and Bank of Mysore were set up. Reserve Bank of India came in 1935.

During the first phase, the growth was very slow and banks also experienced periodic

failures between 1913 and 1948. There were approximately 1100 banks, mostly small. To

streamline the functioning and activities of commercial banks, the Government of India

came up with The Banking Companies Act, 1949 which was later changed to Banking

Regulation Act 1949 as per amending Act of 1965 (Act No. 23 of 1965). Reserve Bank of

India was vested with extensive powers for the supervision of banking in India as the

Central Banking Authority.

During those days public had lesser confidence in the banks. As a result deposit

mobilization was slow. However, the savings bank facility provided by the Postal

department was comparatively safer. Moreover, funds were largely given to traders.

12

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Phase II

Government took major steps in Indian Banking Sector Reform after independence. In the

1960’s a major portion of nationalization was carried out with nationalization of seven

banks forming subsidiaries of State Bank of India on 19th July 1960. It was the effort of the

then Prime Minister of India, Mrs. Indira Gandhi. Fourteen major commercial banks in the

country were nationalized.

Second phase of nationalization under Indian Banking Sector Reform was carried out in

1980’s with seven more banks. This step brought 80% of the banking segment in India

under Government ownership.

The following are the steps taken by the Government of India to Regulate Banking

Institutions in the Country:

1949: Enactment of Banking Regulation Act.

1955: Nationalization of State Bank of India.

1960: Nationalization of SBI subsidiaries.

1961: Insurance cover extended to deposits.

1969: Nationalization of 14 major banks.

1971: Creation of Credit Guarantee Corporation.

1975: Creation of regional rural banks.

1980: Nationalization of seven banks with deposits over 200 crore.

After the nationalization of banks, the branches of the public sector banks in India

experienced a rise of approximately 800% in deposits and advances took a huge jump by

11,000%.

Banking in the sunshine of Government ownership gave the public implicit faith and

immense confidence about the sustainability of these institutions.

13

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Phase IIIThis phase is characterized by introduction of many more products and facilities in the

banking sector due to various reform measures. In 1991, under the chairmanship of M

Narasimham, a committee of the same name was set up. Which worked for the

liberalization of banking practices?

The country was flooded with foreign banks and their ATM’s proliferation. Efforts were

started to give a satisfactory service to customers. Phone banking and net banking were

introduced. The entire system became more convenient and swift.

The financial system of India has shown a great deal of resilience. It is sheltered from any

crisis triggered by any external macroeconomics shock as other East Asian Countries

suffered. This is all due to a flexible exchange rate regime, the foreign reserves are high,

the capital account is not yet fully convertible, and banks and their customers have limited

foreign exchange exposure.

COMPOSITION OF THE BANKING SYSTEM IN INDIA AS AT THE BEGINNING OF NEW MILLENIUM

At present, the number of nationalized banks is 20. Several Foreign banks were allowed to

operate as per the guidelines of RBI. At present the banking system can be classified in

following categories:

PUBLIC SECTOR BANKS

o Reserve Bank of India

o State Bank of India and its 7 associate Banks

o Nationalized Banks (20 in number)

o Regional Rural Banks sponsored by Public sector Banks

14

Potential of micro finance of j&k( A COMPARATIVE STUDY )

PRIVATE SECTOR BANKS

o Old Generation Private Banks o New Generation Private Banks

o Foreign Banks in India

o Local Area Banks

o Non Scheduled Banks

CO-OPERATIVE SECTOR BANKS

o State Co-operative Banks o Central Co-operative Banks

o Primary Agriculture Credit Societies

o Land Development Banks

o Urban Co-operative Banks

o State Land Development Banks

o Scheduled Co-operative Banks

DEVELOPMENT BANKS

o Industrial Finance Corporation of India (IFCI) o Industrial Development Bank of India (IDBI)

o Industrial Credit & Investment Corporation of India (ICICI)

o Industrial Investment Bank of India (IIBI)

o Small Industries Development Bank of India (SIDBI)

o National Bank for Agriculture & Rural Development (NABARD)

o Export-Import Bank of India

15

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Company Profile:

The Jammu and Kashmir Bank Limited

Founded 1938Headquarters IndiaNo. of locations 500 branches/officesIndustry Financial, Commercial BanksRevenue 20,595,000,000 (2007)Employees 6833Website http://www.jkbank.net/

Jammu & Kashmir Bank was founded on October 1,1938 and it commenced business from July 4, 1939. The Jammu & Kashmir Bank Limited has been the first of its nature and composition as a State owned bank in the country. The Bank was established as a semi State Bank with participation in capital by State and the public under the control of State Government. The Bank opened its first branch at Residency Road, Srinagar

The Jammu & Kashmir Bank is today one of the fastest growing banks in India with a network of more than 500 branches/offices spread across the country offering world class banking products/services to its customers. Today, the Bank has a status of value driven organization and is always working towards building trust with shareholders, customers, borrowers, regulators, employees and other diverse stakeholders, for which it has adopted a strategy directed to developing a sound foundation of relationship and trust aimed at achieving excellence, which of course, comes from the womb of good corporate governance. Good governance is a source of competitive advantage and a critical input for achieving excellence in all pursuits. J&K Bank considers good corporate governance as the

16

Potential of micro finance of j&k( A COMPARATIVE STUDY )

sine qua non of a good banking system and has adopted a policy based on all the four pillars of good governance– transparency, disclosures, accountability and value.

The bank expanded its areas of operation and widened its credit base by financing schemes like integrated Rural Development Programmes (IRDP), SEED, PMRY, NRY and other self employment programmes sponsored by State and Central Governments. In 1976, the Jammu & Kashmir Bank became the first and only bank, which was permitted by the Reserve Bank of India to sponsor two regional banks, namely, Kamraz Rural Bank and Jammu Rural Bank.

Introduction:

“I made a list of people who needed just a little bit of money. And when the list was

complete, there were 42 names. The total amount of money they needed was $27. I was

shocked.”

— Muhammad Yunus, economist and founder of the Grameen Bank (on how microfinance

began).Microfinance refers to the provision of financial services to low-income clients, including the self-employed. The term also refers to the practice of sustainably delivering those services.More broadly, it refers to a movement that envisions “a world in which as many poor and

near-poor households as possible have permanent access to an appropriate range of high

quality financial services, including not just credit but also savings, insurance, and fund

transfers.

Theoretically, microfinance encompasses any financial service used by poor people,

including those they access in the informal economy, such as loans from a village

moneylender. In practice however, the term is usually only used to refer to institutions and

enterprises whose goals include both profitability and reducing the poverty of their clients.

Micro financial services are needed everywhere, including the developed world. However,

in developed economies intense competition within the financial sector, combined with a

diverse mix of different types of financial institutions with different missions, ensures that

17

Potential of micro finance of j&k( A COMPARATIVE STUDY )

most people have access to some financial services. Efforts to transfer microfinance

innovations such as solidarity lending from developing countries to developed ones have

met with little success. Microfinance can also be distinguished from charity. It is better to

provide grants to families who are destitute, or so poor they are unlikely to be able to

generate the cash flow required to repay a loan. This situation can occur for example, in

war zone or after a natural disaster.

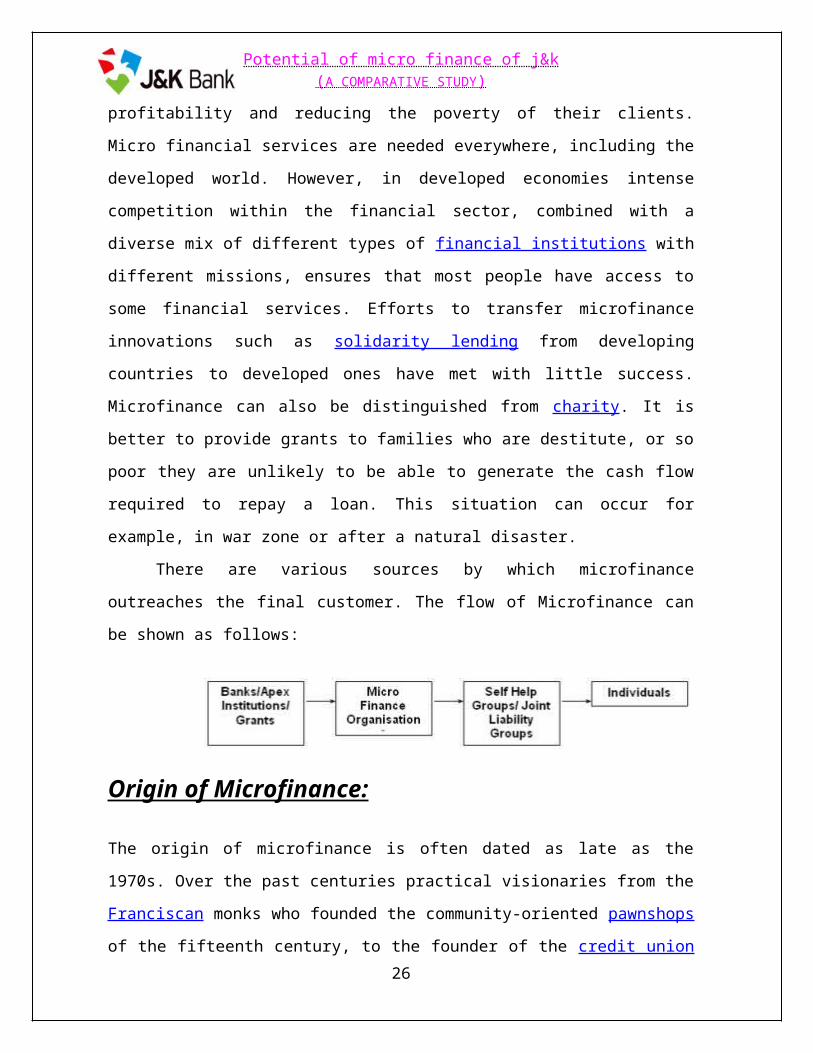

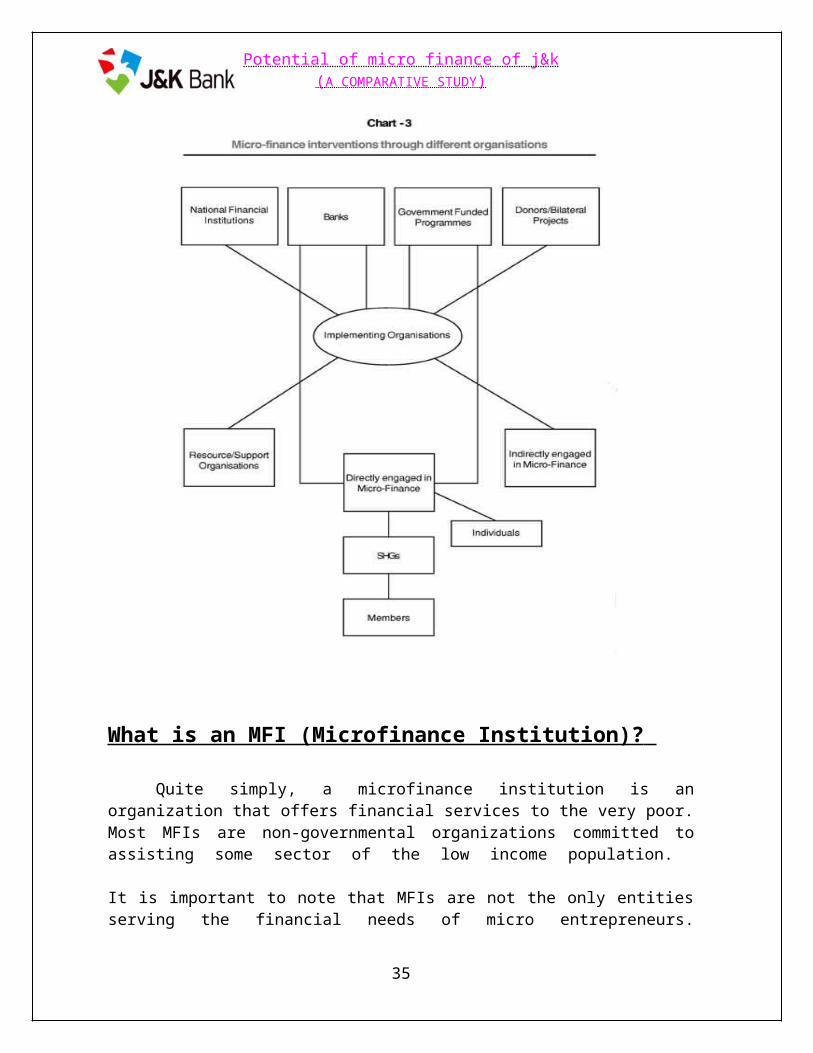

There are various sources by which microfinance outreaches the final customer.

The flow of Microfinance can be shown as follows:

Origin of Microfinance:

The origin of microfinance is often dated as late as the 1970s. Over the past centuries

practical visionaries from the Franciscan monks who founded the community-oriented

pawnshops of the fifteenth century, to the founder of the credit union movement in the

nineteenth century (Friedrich Wilhelm Raiffeisen) and the founders of the microcredit

movement in the 1970s (such as Muhammad Yunus) have tested practices and built

institutions designed to bring the kinds of livelihood opportunities and risk management

tools that financial services provide to the doorsteps of poor people. While the success of

Grameen Bank (which now serves over 7 million poor Bangladeshi women) has inspired

the world, it has proved difficult to replicate this success in practice. In nations with lower

population densities, meeting the operating costs of a retail branch by serving nearby

customers has proven considerably more challenging. Microcredit came to prominence in

the 1980s, although subsidized credit programs to targeted communities date back to the

1950s and early experiments in Bangladesh, Brazil and a few other countries began in the

1970s. The important difference of microcredit was that it avoided the pitfalls of an earlier

generation of targeted development lending, by insisting on repayment, by charging interest

rates that could cover the costs of credit delivery and by focusing on client groups whose

alternative source of credit was the informal sector.

18

Potential of micro finance of j&k( A COMPARATIVE STUDY )

In February 1997, RESULTS Educational Fund convened the first Microcredit Summit.

More than 2,900 delegates from 137 countries attended the Summit, held in Washington,

D.C., and launched a nine-year campaign to reach 100 million of the world’s poorest

families, especially the women of those families, with credit for self-employment and other

financial and business services by the end of 2005.

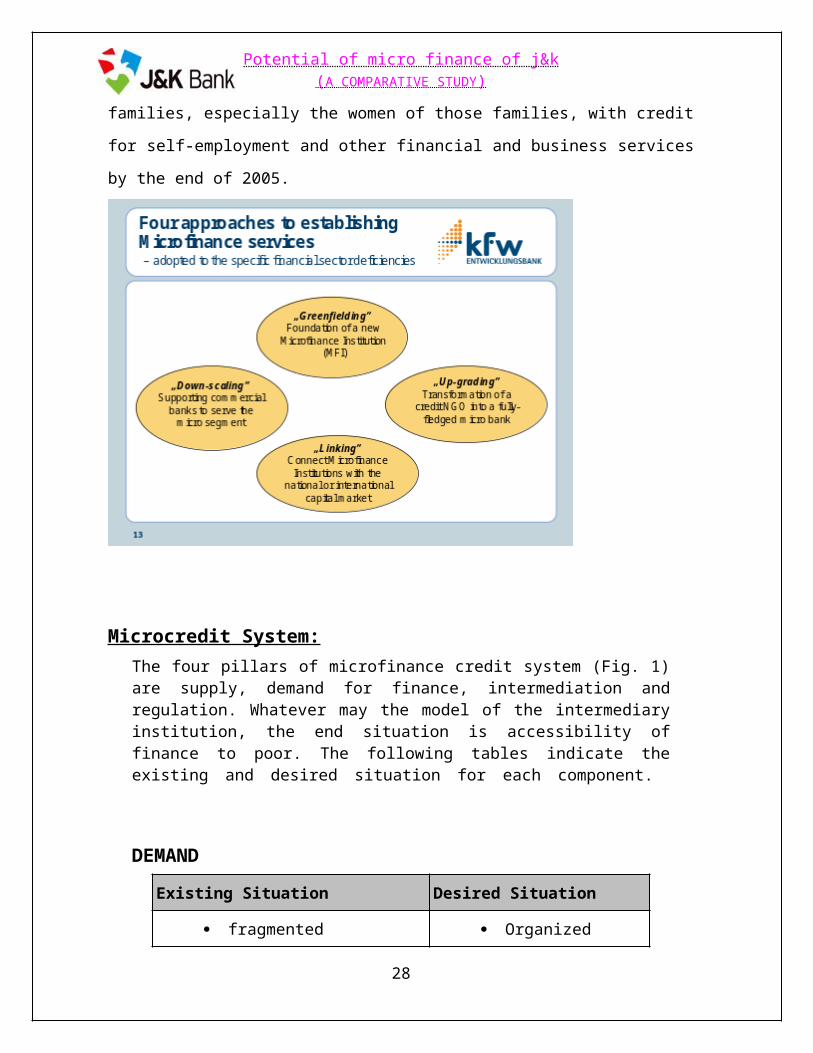

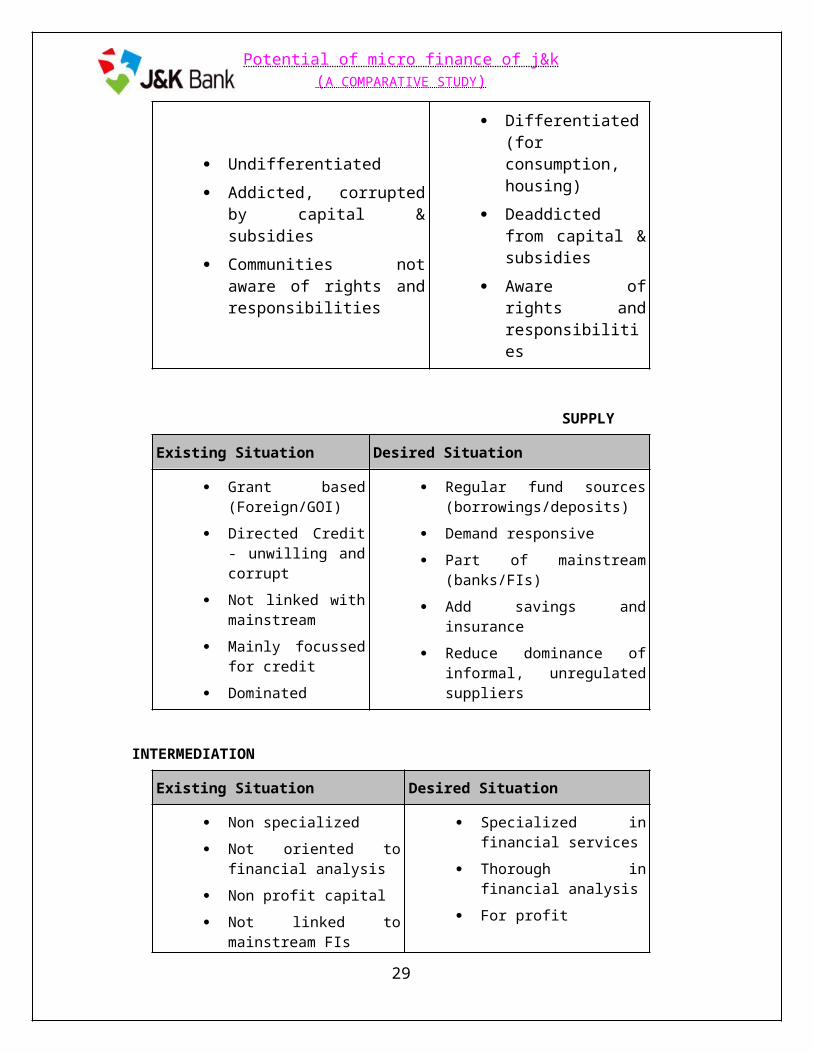

Microcredit System:The four pillars of microfinance credit system (Fig. 1) are supply, demand for finance, intermediation and regulation. Whatever may the model of the intermediary institution, the end situation is accessibility of finance to poor. The following tables indicate the existing and desired situation for each component.

DEMAND

Existing Situation Desired Situation

fragmented

Undifferentiated

Addicted, corrupted by capital

Organized

Differentiated (for consumption,

19

Potential of micro finance of j&k( A COMPARATIVE STUDY )

& subsidies

Communities not aware of rights and responsibilities

housing)

Deaddicted from capital & subsidies

Aware of rights and responsibilities

SUPPLY

Existing Situation Desired Situation

Grant based (Foreign/GOI)

Directed Credit - unwilling and corrupt

Not linked with mainstream

Mainly focussed for credit

Dominated

Regular fund sources (borrowings/deposits)

Demand responsive

Part of mainstream (banks/FIs)

Add savings and insurance

Reduce dominance of informal, unregulated suppliers

INTERMEDIATION

Existing Situation Desired Situation

Non specialized

Not oriented to financial analysis

Non profit capital

Not linked to mainstream FIs

Not organized

Specialized in financial services

Thorough in financial analysis

For profit

Link up to FIs

Self regulating

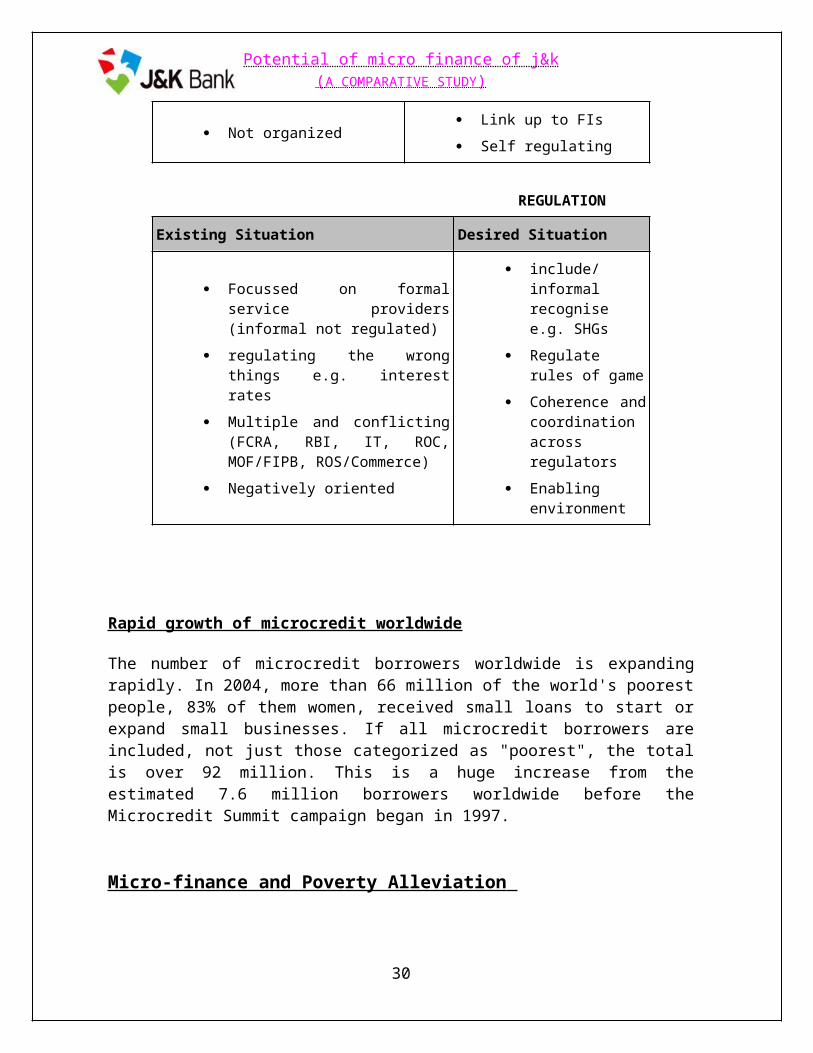

REGULATION

Existing Situation Desired Situation

Focussed on formal service providers (informal not regulated)

regulating the wrong things e.g. interest rates

Multiple and conflicting (FCRA, RBI, IT, ROC, MOF/FIPB,

include/informal recognise e.g. SHGs

Regulate rules of game

Coherence and

20

Potential of micro finance of j&k( A COMPARATIVE STUDY )

ROS/Commerce)

Negatively oriented

coordination across regulators

Enabling environment

Rapid growth of microcredit worldwide

The number of microcredit borrowers worldwide is expanding rapidly. In 2004, more than 66 million of the world's poorest people, 83% of them women, received small loans to start or expand small businesses. If all microcredit borrowers are included, not just those categorized as "poorest", the total is over 92 million. This is a huge increase from the estimated 7.6 million borrowers worldwide before the Microcredit Summit campaign began in 1997.

Micro-finance and Poverty Alleviation

Most poor people manage to mobilize resources to develop their enterprises and their dwellings slowly over time. Financial services could enable the poor to leverage their initiative, accelerating the process of building incomes, assets and economic security. However, conventional finance institutions seldom lend down-market to serve the needs of low-income families and women-headed households. They are very often denied access to credit for any purpose, making the discussion of the level of interest rate and other terms of finance irrelevant. Therefore the fundamental problem is not so much of unaffordable terms of loan as the lack of access to credit itself.

Requirement of Microfinance:

The lack of access to credit for the poor is attributable to practical difficulties arising from the discrepancy between the mode of operation followed by financial institutions and the economic characteristics and financing needs of low-income households. For example, commercial lending institutions require that borrowers have a stable source of income out of which principal and interest can be paid back according to the agreed terms. However, the income of many self employed households is not stable, regardless of its size. A large number of small loans are needed to serve the poor, but lenders prefer dealing with large loans in small numbers to minimize administration costs. They also look for collateral with a clear title - which many low-income households do not have. In addition bankers tend to consider low income households a bad risk imposing exceedingly high information monitoring costs on operation. Emphasis shifted from rapid disbursement of subsidized loans to prop up targeted sectors towards the building up of local, sustainable institutions to serve the poor. Microcredit has

21

Potential of micro finance of j&k( A COMPARATIVE STUDY )

largely been a private (non-profit) sector initiative that avoided becoming overtly political, and as a consequence, has outperformed virtually all other forms of development lending. Indeed, since the 1980s, microfinance programs have improved upon original methodologies and extended beyond conventional thinking. First, microfinance demonstrated that poor people, and especially women, had excellent repayment rates (and often, rates that performed better than those in formal financial sectors). And second, that the poor were willing and able to pay interest rates that would allow the microfinance institutions (MFIs) to cover costs.

Traditionally microfinance was focused on providing a very standardized credit product. The poor, just like anyone else, need a diverse range of financial instruments to be able to build assets, stabilize consumption and protect themselves against risks. Indeed, in many developing countries, self-employment through microenterprise is often the only way to provide for families and the local environment. Thus, we see a broadening of the concept of microfinance---our current challenge is to find efficient and reliable ways of providing a richer menu of microfinance products.

The clients of microfinance:

The typical microfinance clients are low-income persons that do not have access to formal financial institutions. Their "microenterprises" represent an estimated 80% of the total enterprises in the world, 50% of urban enterprises and 20% of the GNP of their countries. Microfinance clients are typically self-employed, often household-based entrepreneurs. In rural areas, they are usually small farmers and others who are engaged in small income-generating activities such as food processing and petty trade. In urban areas, microfinance activities are more diverse and include shopkeepers, service providers, artisans, street vendors, etc. Microfinance clients are poor and vulnerable non-poor who have a relatively stable source of income. Access to conventional formal financial institutions, for many reasons, is inversely related to income: the poorer you are, the less likely that you have access. The poor often obtain financial services from informal financial relationships - credit can be available from commercial and non-commercial lenders, but often at very high interest rates; saving services can be available through savings clubs, credit associations and the like. As a result, the chances are that, the poorer you are, the more expensive or onerous informal financial arrangements. Moreover, informal arrangements may not suitably meet certain financial service needs or may exclude you anyway. Individuals in this excluded and under-served market segment are the clients of microfinance.

Microfinance generally targets poor women because they have proven to be reliable credit risks and when they have the financial means, they invest that money back into their families, resulting in better health and education, and stronger local economies. By providing access to financial services - loans and responsibility for repayment, maintaining savings accounts, providing insurance - microfinance programs send a strong message to households and communities. Studies have shown that women become more assertive and

22

Potential of micro finance of j&k( A COMPARATIVE STUDY )

confident, have increased mobility, are more visible in their communities and play stronger roles in decision making.

How does microfinance help the poor ?

Microfinance brings the power of credit to the grassroots by way of loans to the poor, without requirement of collateral or previous credit record. Experience shows that microfinance can help the poor to increase income, build viable businesses, and reduce their vulnerability to external shocks. It can also be a powerful instrument for self-empowerment by enabling the poor, especially women, to become economic agents of change.

Poverty is multi-dimensional, and by providing access to financial services, microfinance plays an important role in the fight against the many aspects of poverty. Access to credit allows poor people to take advantage of economic opportunities - for their homes, their domestic environments and their communities. For instance, income generation from a business helps not only the business activity expand but also contributes to household income and its attendant benefits on food security, children's education, etc. Moreover, for women who, in many contexts, are secluded from public space, transacting with formal institutions can also build confidence and empowerment.Recent research has revealed the extent to which individuals around the poverty line are vulnerable to shocks such as illness of a wage earner, weather, theft, or other such events. These shocks produce a huge claim on the limited financial resources of the family unit, and, absent effective financial services, can drive a family so much deeper into poverty that it can take years to recover.

Microfinance services are provided by three types of sources:

Formal institutions Semi-formal institutions such as NGOs Informal sources such as money lenders and shopkeepers

Institutional microfinance includes microfinance services provided by both formal and semiformal institutions.Microfinance institutions (MFIs) are institutions whose major business is the provision of microfinance services.

23

Potential of micro finance of j&k( A COMPARATIVE STUDY )

What is an MFI (Microfinance Institution)?

Quite simply, a microfinance institution is an organization that offers financial services to the very poor. Most MFIs are non-governmental organizations committed to assisting some sector of the low income population.

It is important to note that MFIs are not the only entities serving the financial needs of micro entrepreneurs. Commercial banks, cooperatives and savings institutions all have important roles to play in serving this market.Over the last ten years, however, successful experiences in providing finance to small entrepreneur and producers demonstrate that poor people, when given access to responsive and timely financial services at market rates, repay their loans and use the proceeds to

24

Potential of micro finance of j&k( A COMPARATIVE STUDY )

increase their income and assets. This is not surprising since the only realistic alternative for them is to borrow from informal market at an interest much higher than market rates. Community banks, NGOs and grassroot savings and credit groups around the world have shown that these microenterprise loans can be profitable for borrowers and for the lenders, making microfinance one of the most effective poverty reducing strategies.

To be successful, financial intermediaries that provide services and generate domestic resources must have the capacity to meet high performance standards. They must achieve excellent repayments and provide access to clients. And they must build toward operating and financial self-sufficiency and expanding client reach. In order to do so, microfinance institutions need to find ways to cut down on their administrative costs and also to broaden their resource base. Cost reductions can be achieved through simplified and decentralized loan application, approval and collection processes, for instance, through group loans which give borrowers responsibilities for much of the loan application process, allow the loan officers to handle many more clients and hence reduce costs (Otero et al. 1994).

Microfinance institutions can broaden their resource base by mobilizing savings, accessing capital markets, loan funds and effective institutional development support. A logical way to tap capital market is securitization through a corporation that purchases loans made by microenterprise institutions with the funds raised through the bonds issuance on the capital market. There is atleast one pilot attempt to securitize microfinance portfolio along these lines in Ecuador. As an alternative, BancoSol of Bolivia issued a certificate of deposit which is traded in Bolivian stock exchange. In 1994, it also issued certificates of deposit in the U.S. (Churchill 1996). The Foundation for Cooperation and Development of Paraguay issued bonds to raise capital for microenterprise lending (Grameen Trust 1995). Savings facilities make large scale lending operations possible. On the other hand, studies also show that the poor operating in the informal sector do save, although not in financial assets, and hence value access to client-friendly savings service at least as much access to credit. Savings mobilization also makes financial institutions accountable to local shareholders. Therefore, adequate savings facilities both serve the demand for financial services by the customers and fulfill an important requirement of financial sustainability to the lenders. Microfinance institutions can either provide savings services directly through deposit taking or make arrangements with other financial institutions to provide savings facilities to tap small savings in a flexible manner (Barry 1995).

Convenience of location, positive real rate of return, liquidity, and security of savings are essential ingredients of successful savings mobilization (Christen et al. 1994). Governments should provide an enabling legal and regulatory framework which encourages the development of a range of institutions and allows them to operate as recognized financial intermediaries subject to simple supervisory and reporting requirements. Usury laws should be repelled or relaxed and microfinance institutions should be given freedom of setting interest rates and fees in order to cover operating and finance costs from interest revenues within a reasonable amount of time. Government could also facilitate the process of transition to a sustainable level of operation by providing support to the lending institutions in their early stage of development through credit enhancement mechanisms or subsidies.

25

Potential of micro finance of j&k( A COMPARATIVE STUDY )

One way of expanding the successful operation of microfinance institutions in the informal sector is through strengthened linkages with their formal sector counterparts. A mutually beneficial partnership should be based on comparative strengths of each sectors. Informal sector microfinance institutions have comparative advantage in terms of small transaction costs achieved through adaptability and flexibility of operations (Ghate et al. 1992). They are better equipped to deal with credit assessment of the urban poor and hence to absorb the transaction costs associated with loan processing. On the other hand, formal sector institutions have access to broader resource-base and high leverage through deposit mobilization (Christen et al. 1994).

Therefore, formal sector finance institutions could form a joint venture with informal sector institutions in which the former provide funds in the form of equity and the later extends savings and loan facilities to the urban poor. Another form of partnership can involve the formal sector institutions refinancing loans made by the informal sector lenders. Under these settings, the informal sector institutions are able to tap additional resources as well as having an incentive to exercise greater financial discipline in their management. Microfinance institutions could also serve as intermediaries between borrowers and the formal financial sector and on-lend funds backed by a public sector guarantee (Phelps 1995). Business-like NGOs can offer commercial banks ways of funding micro entrepreneurs at low cost and risk, for example, through leveraged bank-NGO-client credit lines. Under this arrangement, banks make one bulk loan to NGOs and the NGOs packages it into large number of small loans at market rates and recover them (Women's World Banking 1994). There are many on-going researches on this line but context specific research is needed to identify the most appropriate model. With this in mind we discuss various possible alternatives of formal-informal sector linkages in India.

While a census of NGOs in micro-finance is yet to be carried out, there are perhaps 250-300 NGOs, each with 50-100 Self Help Groups (SHG). Few of them, not more than 20-30 NGOs have started forming SHG Federations. There are also agencies which provide bulk funds to the system through NGOs. Thus organisations engaged in micro finance activities in India may be categorised as Wholesalers, NGOs supporting SHG Federations and NGOs directly retailing credit borrowers or groups of borrower.

The Wholesalers will include agencies like NABARD, Rashtriya Mahila Kosh-New Delhi and the Friends of Women's World Banking in Ahmedabad. Few of the NGOs supporting SHG Federations include MYRADA in Bangalore, SEWA in Ahmedabad, PRADAN in Tamilnadu and Bihar, ADITHI in Patna, SPARC in Mumbai, ASSEFA in Madras etc. While few of the NGOs directly retailing credit to Borrowers are SHARE in Hyderabad, ASA in Trichy, RDO Loyalam Bank in Manipur

26

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Microfinance Outreach -Global Scenario :

The microfinance sector has grown over time with more and different types of actors becoming involved, with increasing numbers of geographic regions around the world being serviced, with new types of products and services being developed, and with new ideas and technologies to support it.The global picture regarding microfinance outreach is quite impressive. From a mere 7.6 million poorest families in 1997, the Microcredit Summit Campaign reported an outreach of more than 92 million clients by December 31, 2004. This number includes 66.6 million families who wereamong the poorest when they started with a program. Of these 66.6 million poorest clients, 55.7 million or 83.6 percent were served by the 52 largest individual institutions, all with 100,000 or more clients. The number of microcredit borrowers worldwide is expanding rapidly. In 2004, more than 66 million of the world's poorest people, 83% of them women, received small loans to start or expand small businesses. If all microcredit borrowers are included, not just those categorized as "poorest", the total is over 92 million. This is a huge increase from the estimated 7.6 million borrowers worldwide before the Microcredit Summit campaign began in 1997Among these largest MFIs, 79% are in Asia, 17% are in Africa and only 4% are in Latin America.Of the 3,164 institutions that had reported to the Microcredit Summit Campaign by December 31, 2004, 1628 were in Asia, 994 in Africa, 388 in Latin America and Caribbean, 48 in North America, 34 in the Middle East, 72 in Europe and the Newly Independent States (NIS). The increase in the number of institutions reporting, from 618 in 1997 to 3164 in 2004, isdefinitely an indication of an impressive growth in the field of microfinance.

Of the over 92 million people reached by the end of 2004, 81.5 million were in Asia, 7 million in Africa and 3.8 million in Latin America and the Caribbean. Only 5.2 million of the 61.5 million poorest families in Africa and the Middle East were covered by microfinance programs by the end of 2004. Asia, which is home to some 67 percent of the world’s people living on less than US$ 1 a day can therefore rightfully boast of a vibrant microfinance sector.In Asia, Bangladesh distinguishes itself by reaching more than 75 percent of poor families with microfinance. It is home to 31 percent of the largest programs in the world, who have individually reached more than 100,000 clients. MFPs in Bangladesh reached over 18 million poorest clients by the end of 2004. The intensity and density of microfinance is greater in

Bangladesh than in any other country. The pioneering role of Grameen Bank; the bold initiative of NGO-MFIs; the participation of banks; the implementation of Government programs like BRDB, PDBP, etc.; the operation of PKSF; and the strong commitment and competitive spirit of the major players in the field have largely contributed to such a development of microfinance in Bangladesh.

27

Potential of micro finance of j&k( A COMPARATIVE STUDY )

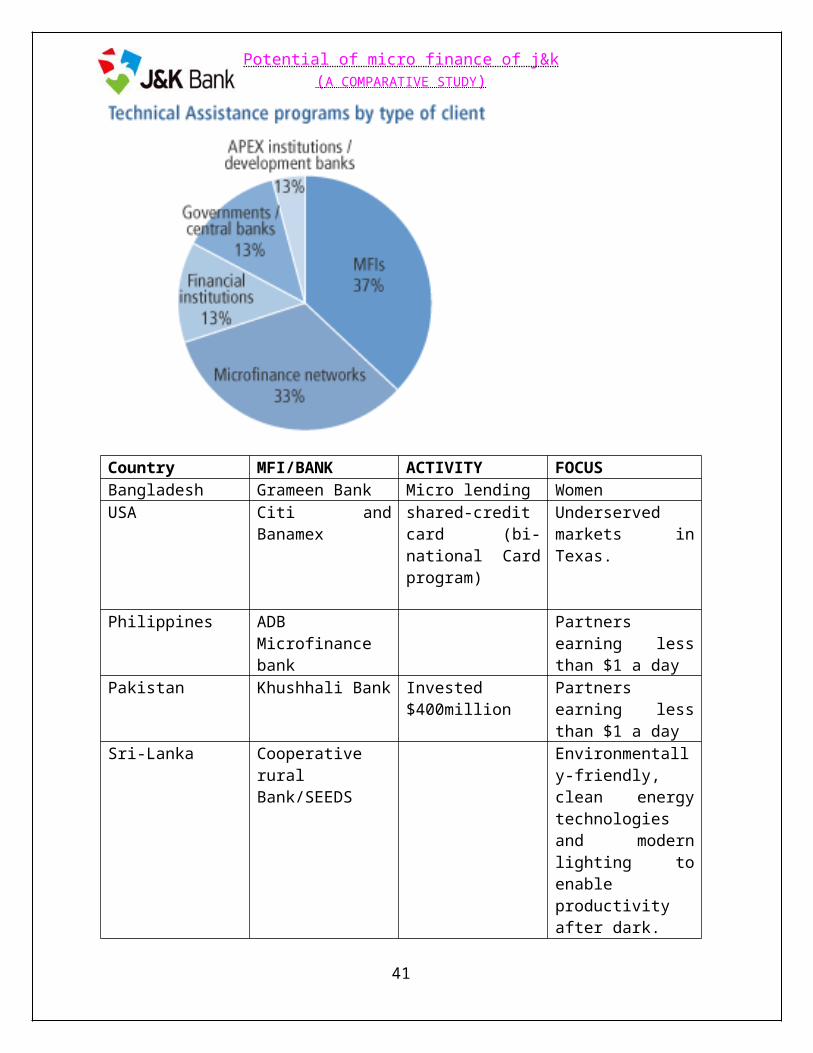

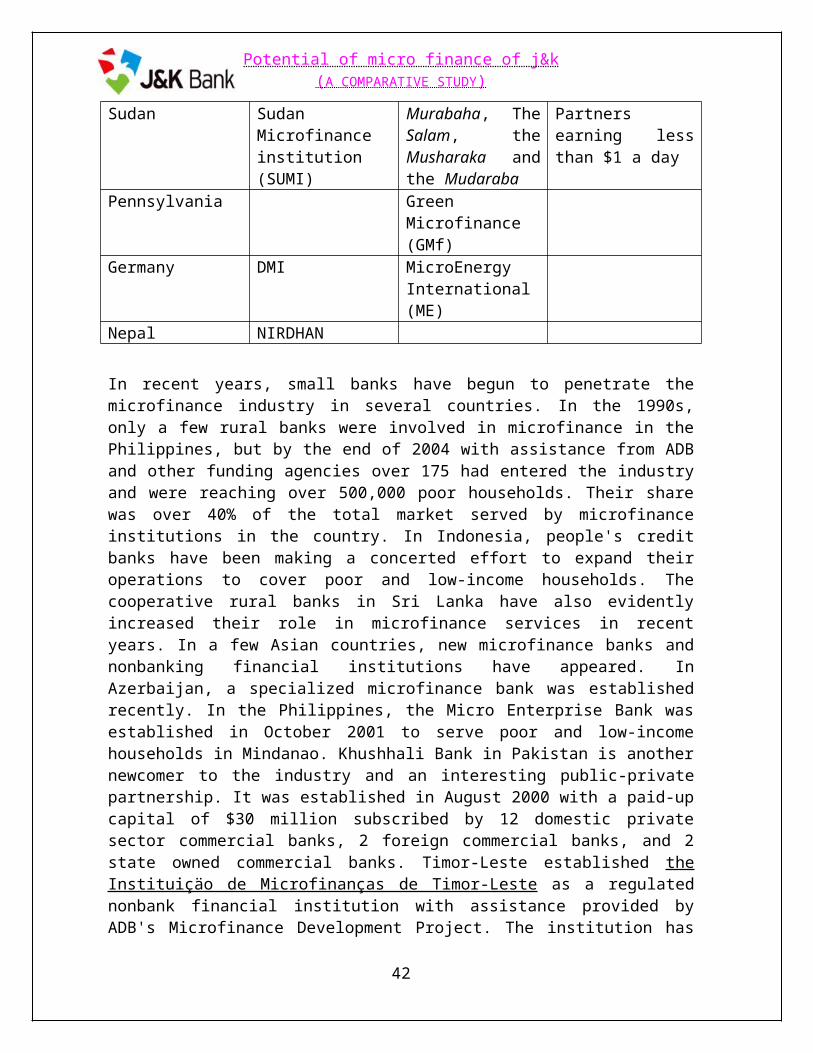

Country MFI/BANK ACTIVITY FOCUSBangladesh Grameen Bank Micro lending WomenUSA Citi and Banamex shared-credit card

(bi-national Card program)

Underserved markets in Texas.

Philippines ADB Microfinance bank

Partners earning less than $1 a day

Pakistan Khushhali Bank Invested $400million

Partners earning less than $1 a day

Sri-Lanka Cooperative rural Bank/SEEDS

Environmentally-friendly, clean energy technologies and modern lighting to enable productivity after dark.

Sudan Sudan Microfinance institution (SUMI)

Murabaha, The Salam, the Musharaka and the Mudaraba

Partners earning less than $1 a day

Pennsylvania Green Microfinance (GMf)

Germany DMI MicroEnergy International (ME)

Nepal NIRDHAN

28

Potential of micro finance of j&k( A COMPARATIVE STUDY )

In recent years, small banks have begun to penetrate the microfinance industry in several countries. In the 1990s, only a few rural banks were involved in microfinance in the Philippines, but by the end of 2004 with assistance from ADB and other funding agencies over 175 had entered the industry and were reaching over 500,000 poor households. Their share was over 40% of the total market served by microfinance institutions in the country. In Indonesia, people's credit banks have been making a concerted effort to expand their operations to cover poor and low-income households. The cooperative rural banks in Sri Lanka have also evidently increased their role in microfinance services in recent years. In a few Asian countries, new microfinance banks and nonbanking financial institutions have appeared. In Azerbaijan, a specialized microfinance bank was established recently. In the Philippines, the Micro Enterprise Bank was established in October 2001 to serve poor and low-income households in Mindanao. Khushhali Bank in Pakistan is another newcomer to the industry and an interesting public-private partnership. It was established in August 2000 with a paid-up capital of $30 million subscribed by 12 domestic private sector commercial banks, 2 foreign commercial banks, and 2 state owned commercial banks. Timor-Leste established the Instituiçäo de Microfinanças de Timor-Leste as a regulated nonbank financial institution with assistance provided by ADB's Microfinance Development Project. The institution has filled a vacuum in the microfinance industry in this new nation. Papua New Guinea also established a new microfinance bank in 2004 with ADB support. The First Microfinance Bank of Tajikistan began operations in July 2004 as the country's first full-service microfinance bank. Afghanistan also established a new microfinance bank in 2003.

In most Asian countries, cooperatives were originally established to serve poor and low-income households, but they gradually dropped the poor and focused on the nonpoor. With support from ADB and other funding agencies, many cooperatives have recently begun to make headway in the sustainable provision of microfinance services.

A case in point is the growing involvement of credit unions in the microfinance industry in the Philippines. In the Kyrgyz Republic and Viet Nam, ADB assisted in the development of credit unions and expanded their outreach to the low-income population, and in Sri Lanka, the Rural Finance Sector Development Project focuses on improving the microfinance operations of the cooperative rural banks.

29

Potential of micro finance of j&k( A COMPARATIVE STUDY )

GLOBAL PRESENCE

MICROFINANCE NETWORK:

The Microfinance Network is a global association of institutions committed to improving the quality of life of the poor through the provision of credit, savings instruments and other financial services. The members of the Network believe in the establishment of sustainable and profitable institutions that operate on commercial principles and serve large volumes of clients who are not currently served by traditional financial institutions.The Network's mission is to:

a) Promote the financial systems approach to micro-sector finance among policy makers, donors and practitioners;

b) Facilitate the process of transformation of microfinance organizations into formal financial institutions and provide Network members with access to information and expertise that increases their knowledge about best practices in micro-sector finance and accelerates their process of transformation into formal financial institutions;

c) Promote microfinance institutions that advocate commercial principles in order to sustainably realize social goals; and

d) Influence the broader microfinance community and financial system to operationalize social and commercial values.

KEY STATISTICS ON PARTNERS/MEMBERS/AFFILIATESdata as of 2006-10-30

Total number of partners : 37

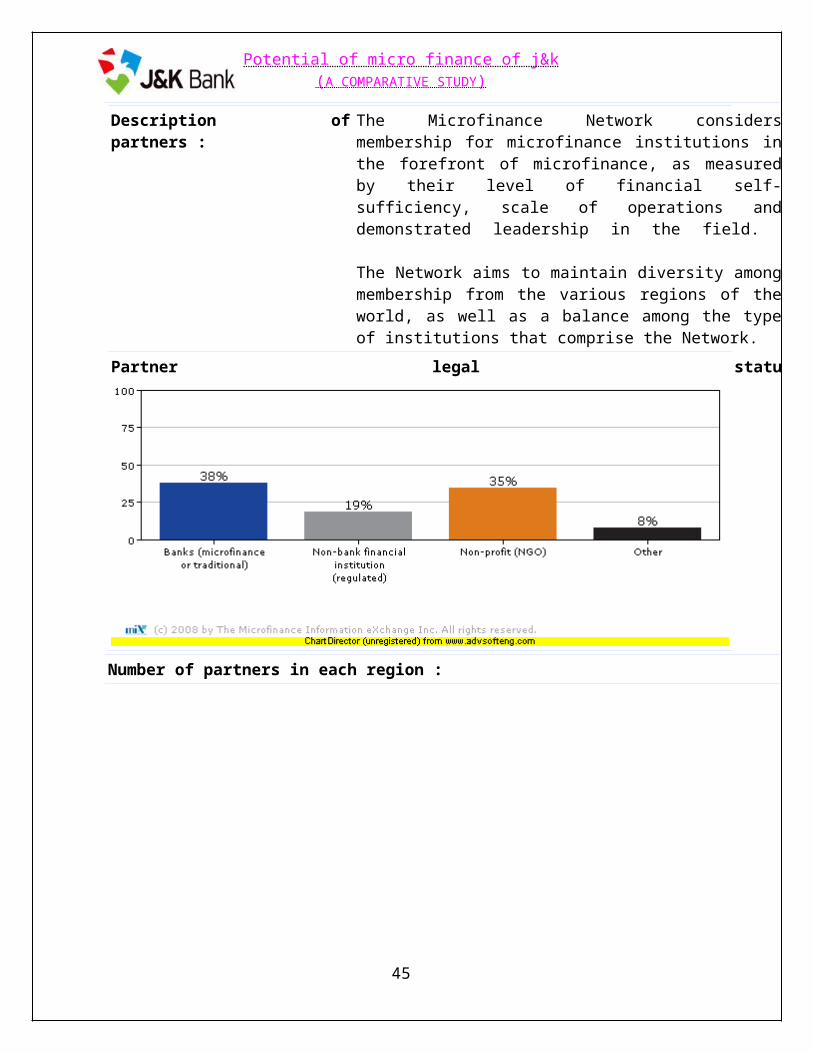

Description of partners : The Microfinance Network considers membership for microfinance institutions in the forefront of microfinance, as measured by their level of financial self-sufficiency, scale of operations and demonstrated leadership in the field.

The Network aims to maintain diversity among membership from the various regions of the world, as well as a balance among the type of institutions that comprise the Network.

Partner legal statu

30

Potential of micro finance of j&k( A COMPARATIVE STUDY )

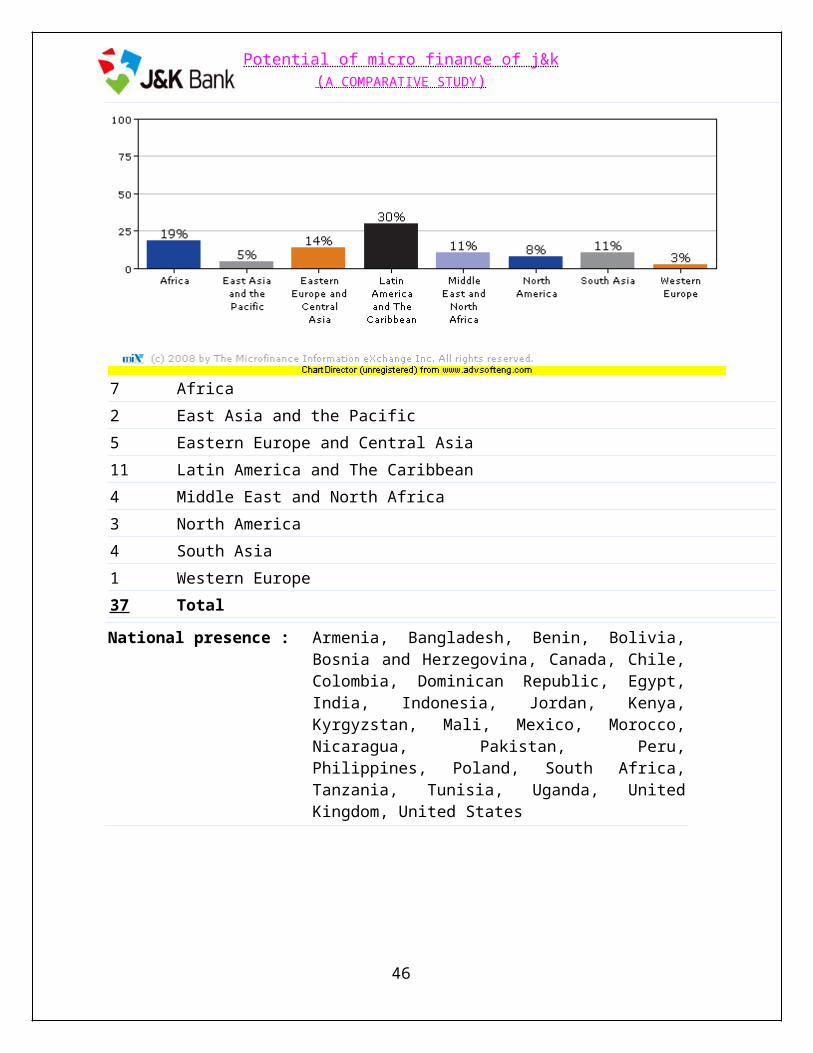

Number of partners in each region :

7 Africa

2 East Asia and the Pacific

5 Eastern Europe and Central Asia

11 Latin America and The Caribbean

4 Middle East and North Africa

3 North America

4 South Asia

1 Western Europe

37 Total

National presence : Armenia, Bangladesh, Benin, Bolivia, Bosnia and Herzegovina, Canada, Chile, Colombia, Dominican

31

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Republic, Egypt, India, Indonesia, Jordan, Kenya, Kyrgyzstan, Mali, Mexico, Morocco, Nicaragua, Pakistan, Peru, Philippines, Poland, South Africa, Tanzania, Tunisia, Uganda, United Kingdom, United States

Some of the Examples of Microfinance worldwide are

Grameen-Veolia Water deal to help Bangladesh;

Nobel laureate Muhammad Yunus unveiled a deal between his Grameen bank and French group Veolia Environment to provide clean water to poor rural communities in Bangladesh.

The Bangladeshi economist also sought support from President Nicolas Sarkozy for creating more microcredit schemes to fight poverty, particularly in Africa. Sarkozy told Yunus that France would continue and step up its efforts to provide access to loans to the poor and noted that more than a third of France's African aid funding was now directed toward microfinance.

After discussions with Sarkozy, Yunus sat down with top business leaders at the Elysee including billionaire Vincent Bollore and announced the creation of the new joint company with Veolia Environment. Called Grameen-Veolia Water, the company will operate several water treatment plants in Bangladeshi villages, with the goal of bringing clean water to 100,000 people.The project represents investments worth 500,000 euros (790,000 dollars).

The MIX 2007 Top 100 MFIs Report;

The Microfinance Information exchange (MIX) has released the 2007 Global 100: Rankings of Microfinance Institutions report. It is a ranking of the top performing microfinance institutions (MFIs) throughout the developing world, based on data from

MIX's publicly available database. The composite rankings are based on a number of criteria and were developed in an effort to present the leading, most well-rounded institutions.

The MIX Global 100 highlights leading microfinance institutions through the lens of various aspects of performance. The MIX Global 100 by category offers a snapshot of MFI results, identifying the leading performers in each of seven categories within outreach, scale, profitability, efficiency, productivity and portfolio quality. In order to widen the lens of financial service provision, outreach and scale tables include separate rankings for

32

Potential of micro finance of j&k( A COMPARATIVE STUDY )

deposit mobilizing institutions. This year’s rankings of efficiency also use a new measure to minimize the influence of loan size and neutralize differences across country environments in ranking MFI transaction costs.

The 2007 MIX Global 100 surveyed 820 institutions, an increase of nearly 40 percent over the 2006 sample set. Leading performers were drawn from a diverse sample of MFI that served over 53 million borrows with over USD 24 billion in loans and held USD 15 billion in deposits from 64 million microfinance clients.

eBay launches MicroPlace.com investment site;

MicroPlace, purchased in March 2007 by eBay Inc., has announced the launch of a new website that provides the first online marketplace for individuals to invest in microfinance and earn a financial and social return.

This is a very interesting and encouraging service as it allows anyone to participate in making a positive social impact thru personal investments. To date many of the

microfinance funds and vehicles on the market have been investment tools for institutions, other funds, VC's or high-net worth individuals. Using the new site, investors can purchase microfinance securities with as little as $100 using eBay's PayPal service or a U.S. bank checking account, and have the option to direct their investment to a specific country and microfinance institution in the developing world.

How it works:

1) Set up an account and then purchase investments on MicroPlace.com from security issuers, who are responsible for making interest and principal payments to you. 2) The security issuers adds your funds to loans given to lending organizations (such as Microfinance Institutions), who in turn use those funds to provide loans to their end-borrowers. 3) The end-borrowers are generally self-employed poor, usually working in commercial activities, agriculture, fishing or craftspeople. They earn just enough to survive and use small loans to start or expand their businesses. The majority of them are women who in turn use earned revenues for household expenses, such as clothing, medical and education fees. As loans are repaid, security issuers are able to provide you with a financial return.

33

Potential of micro finance of j&k( A COMPARATIVE STUDY )

MicroPlace plans to make money by charging issuers to list. "We aspire to break-even, and if and when we reach profitability, eBay intends to reinvest any profits back into its own social initiatives," said Tracey Pettengill Turner, Founder and General Manager of MicroPlace.

MicroPlace thus far has partnered with OikoCredit USA and the Calvert Foundation to offer its first securities, which mature in two to four years and yield between 1.5% to 3% a year. Prospectuses are available online as well as financial reports of the local lending institutions, and MicroPlace is registered as a broker-dealer with the Securities and Exchange Commission (SEC). There are over 80 funds available on the market today investing in microfinance activities in developing countries. As the service grows we anticipate a growing range of securities to become available as investment options on microplace.com.

A great opportunity to invest part of your savings towards making a social impact in areas that need it most.

Posted by Angelo SantaMaria on Friday, 26 October 2007 in MF Investment, MFI News, Technology, US | Permalink | Comments (0) | TrackBack (0)

Microcredit Summit Campaign: Phase II Goals

In April 2005, the Microcredit Summit Campaign announced the extension of the Campaign up to 2015 at the Latin America/Caribbean Region Microcredit Summit in Santiago, Chile. Phase II of the Campaign, from 2006-2015, has two goals.

The first goal is to ensure that 175 million of the world’s poorest families, especially the women receive credit for self-employment and other financial and business services by the end of 2015.

The second goal of the campaign is to ensure that 100 million of the world’s poorest families move from below US$ 1 a day adjusted for Purchasing Power Parity (PPP) to above US $ 1 a day adjusted for PPP, by the end of 2015. With an average of 5 people per family, it can be estimated that 500 million poor would rise above US$ 1 a day, implying the near accomplishment of the Millennium Development Goal of halving

absolute poverty. This is exactly the kind of progress needed to reach the Millennium Development Goals (MDGs).The task at hand is to make adequate institutional and policy preparations to ensure that the MDGs and the two new goals set by the Microcredit Summit Campaign are achieved on time. Based on the lessons learnt and successes enjoyed so far, this is the time to intensify the efforts to get to the goals as planned. It is therefore very important to project the possible who, what, when, where, why and how of microfinance expansion over the next ten years.

34

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Development of Microfinance;

In envisioning the future of microfinance, it is important to know the background of the microfinance movement, who took the initiatives, who supported the cause, and what opportunities and constraints it has faced. Poverty-focused microfinance came into existence as a private initiative, growing almost unnoticed through a process of learning by doing. Muhammad Yunus and other pioneers took the initiative based on an inner urge and then succeeded in developing a sustainable microfinance system that brought financial services to the doorsteps of the poor, especially to the poorest women who were always considered unbankable. Microcredit is the result of empathy for human suffering, continuous thinking and innovative efforts.

Key Results of microfinance;

World Bank Releases First Ever Data on Access to Financial Services Worldwide By Sidney Povall, Robert F. Wagner School of Public Service, New York University "In terms of what explains outreach, we find that geographic access to banking services is positively correlated with population density and access to and use of banking services are higher in larger economies…In addition our regression analysis suggests that other country characteristics as well as policy variables are also correlated with outreach. Specifically we find that a better communication and transportation infrastructure is associated with greater outreach. Countries with better developed institutions enjoy greater levels of outreach". The collection efforts and subsequent paper focused on measuring access to financial services by capturing data on banking branch and ATM penetration for a geographic area relative to population density, as well as measuring the number of deposit accounts and loans relative to the population and average loan size relative to GDP per capita. The resulting data showed that the indicators accurately predicted household and firm use of banking services. For example, data collected from surveys indicates that Bangladesh has 4.47 bank branches per 100,000 people, 54.73 loan accounts and 228.75 deposit accounts, while Spain has 95.87 bank branches per 100,000 people, 556.48 loan accounts and 2,075.96 deposit accounts. The data specify: "Both cross-country and firm-level regression indicate that firms in countries with higher branch and ATM penetration and more extensive use of loans report lower financing obstacles". The report also details results around data analysis efforts of cross-country variations in levels of outreach attempting to learn if the size of an economy has any affect on the level of financial services penetration and outreach. The analysis yielded interesting results. Correlation and regression results indicated that larger economies have greater levels of outreach. For example, the team was able to accurately predict the percentage of households who have bank accounts using this data and actual household deposit account data previously collected. It found that in Pakistan, .122 of households had deposit accounts while their regression predicted .101. The report goes on to suggest that this indicates that scale economies may be helpful in effectively providing banking services.

35

Potential of micro finance of j&k( A COMPARATIVE STUDY )

The final part of the report examines correlations between variations in outreach levels and cross-country differences in the perception firms have about the level financing constraints they face. The paper outlines the findings as showing, "that higher branch and ATM penetration and wider use of loan services are associated with lower financing obstacles, even after we control for a standard measure of financial sector depth". For example, increasing the number of ATM branches from the 25th to the 75th percentile decreases the probability that such firms will rate financing as a major constraint to growth by 3/8 percentage point for ATM's per population and ½ a percentage point for ATM's per area.The report concludes by expressing the authors' desires that it be a first step in "developing consistent and comparable cross-country indicators of banking system outreach", and that the findings of the research team be the start of regular assessment of the indicators so that the debate about access to financial services can be informed about its effects and determinants

Microfinance in India:

“Money, says the proverb makes money. When you have got a little, it is often easy to get more. The great difficulty is to get that little.”Adams Smith.

Today India is facing major problem in reducing poverty. About 250 million people in India are under below poverty line. With low per capita income, heavy population pressure , prevalence of massive unemployment and underemployment , low rate of capital formation , misdistribution of wealth and assets , prevalence of low technology and poor economics organization and instability of output of agriculture production and related sectors have made India one of the poor countries of the world.

Some 30 million women have formed 2.2 million small businesses and another 400,000 are expected to be in place by March, 2007, according to the National Bank of Agriculture and Rural Development. About $2.48 billion has been extended to these groups, which predominantly run by women, over the last decade (source Economic times)

Present Scenario of India:

India falls under low income class according to World Bank. It is second populated country in the world and around 70 % of its population lives in rural area. 60% of people depend on agriculture, as a result there is chronic underemployment and per capita income is only $ 326.2. This is not enough to provide food to more than one individual. The obvious result is abject poverty, low rate of education, low sex ratio, and exploitation. The major factor account for high incidence of rural poverty is the low asset base. According to Reserve Bank of India, about 51 % of people house possess only 10% of the total asset of India .This has resulted low production capacity both in agriculture (which contribute around 22-25% of GDP) and Manufacturing sector. Rural people have very low access to institutionalized credit (from commercial bank).

36

Potential of micro finance of j&k( A COMPARATIVE STUDY )

According to World Bank, out of the worlds total population of 6 billion, a total of 1.2 billion people, live on wages less than $1 (INR 60) per day; of which, the majority live in Asia. Almost 40% of the population of the South Asia region is poverty stricken. Further to this, India alone is said to host about one third of the worlds poor.

The estimates from Government of India, show that over 250 million people are left without proper access to credit despite a network of 33000 rural and semi urban branches of commercial banks, 14000 branches of Regional Rural Banks and 92000 outlets of cooperatives. The poorest people very often do not comply with the norms that banks lay down for credit seekers. They neither have salary certificates or the required collateral to show as security against the loan. Under such circumstances, the poorest citizens access credit mostly from informal finance providers who charge very high rate of interest. Non payment of principal or interest by the credit seekers invites various kind of exploitation for him and his family.

To date in India, only an estimated 5 million poor people (mostly rural women) benefit from microfinance services, leaving a vast unmet demand for developing credit, savings and insurance activities which is termed as microfinance services targeted a sector referred to as non-bankable even till date.

Source: GOI Survey, September 1998

Around 75% of all micro credit activity in the country is concentrated in the four southern states of Andhra Pradesh, Karnataka, Kerala and Tamil Nadu

Source: Government of India Survey 2006

As designed by NABARD, the women who benefit from microfinance are able to access the microfinance services by forming groups of 5 to 20 women, called self-help groups ("SHGs"). The group is intended to act as a semi-guarantor by making sure that each member repays her loan in the stipulated time thereby positively contributing to the groups credit-worthiness. SHGs are either linked to NGOs or to local banks. From the banks they can access funds @ 2-3% a month and through NGOs providing micro-credit @ 15 to 20 % per annum. There is a possibility of generating a credit demand of 25 billion Indian Rupees from savings from the poor in the short term.

Source GOI Survey, September 1998

37

Potential of micro finance of j&k( A COMPARATIVE STUDY )

Poverty alleviation programmes and conceptualization of Microfinance

India has supported social banking for a long time. Policy directions to rapidly expand rural branches, mandate credit allocations for priority sectors (including agriculture), deliver large subsidy oriented credit programmes to serve marginal communities and poor households and control interest rates have been tried for over 35 years.

The new generation microfinance was slow in coming to India. Low levels of grants to microfinance institutions, an unfavourable policy environment, substantial traditional banking infrastructure and a search for context specific solutions has constrained rapid scale up. The first breakthrough emerged from policy support to enable informal self help groups of 15-20 members (mainly women) to transact with commercial banks. These groups build up and rotate savings amongst themselves, open bank accounts and take responsibility for lending and recovering money financed by banks. With the missionary zeal of the National Bank for Agriculture and Rural Development (NABARD), insights gained by NGOs, the increasing enthusiasm of bankers and politicians and emerging successes in repayment and social impacts, this national movement now encompasses 1.4 million such groups (over 20 million members).

At a time when many questioned the need for specialised microfinance institutions (MFIs) in India, the Small Industries Development Bank of India (SIDBI) recognized the opportunity and started implementation of an ambitious national programme. Providing loan and capacity building support to MFIs and capacity building and rating support for sector development, this programme already supports 70 MFIs and has disbursed US$46 million. Microfinance has been perceived as an alternative tool of providing financial services to poorclientele in India. SEWA (Self Employed Women Association) Bank is the oldest microfinance organisation in the country. The Community Based Organisations (CBOs) and NonGovernmental Organizations (NGOs) initiated the microfinance movement and the formalfinancial Sector joined in at a later stage. The popular mode of delivering microfinance in Indiais Self Help Groups (SHGs) . Initially, NGO-MFIs motivated poor to form SHGs andsupported them to manage their savings and internal lending activities within the SHG. In theyear 1992, NABARD initiated a pilot project on SHG-Bank Linkage programme in India. Forthis pilot project, Southern States in India were chosen. NABARD took up this programme on afull-fledged manner in 1998 after experiencing an immense success of the pilot project. NowSHG-Bank Linkage Programme is the largest microfinance programme in the world. Within aspan of 15 years, the outreach of this programme had increased to 2.24 million credit linked

38

Potential of micro finance of j&k( A COMPARATIVE STUDY )

SHGs in the year 2006 from 255 credit linked SHGs in the year 1992. In the present Indianmicrofinance sector, Commercial Banks, Regional Rural Banks, Cooperative Banks, Non Banking Financial Companies (NBFCs) and NGOs are involved in offering microfinance services to the poor.Microfinance movement in India can be divided into two phases. In the first phase of thisMovement, it was found that NGOs and CBOs took the initiative of group formation. TheyNurtured these SHGs and provided micro-credit. In this phase most of the programmes were sponsored by national and international donor agencies. In the second phase, Micro-CreditMovement transformed to a broader level of intervention and came to be recognised asMicrofinance movement. Formal financial Institutions have joined this movement along withNGOs and CBOs. Apart from credit, the provision of other financial products like insurance andmicro savings is also carried out. It is important to note that that in the nascent stage it themovement was considered as a poverty lending exercise and now in the present stage it has

transformed into a profit earning financial business.

What is Exciting about Indian Microfinance? A Task Force on Microfinance recognised in 1999 that microfinance is much more than microcredit, stating: "Provision of thrift, credit and other financial services and products of very small amounts to the poor in rural, semi-urban and or urban areas for enabling them to raise their income levels and improve living standards". The Self Help Group promoters emphasize that mobilising savings is the first building block of financial services.

For many years, the national budget and other policy documents have almost equated microfinance with promoting SHG links to the banks. The central bank notification that lending to MFIs would count towards meeting the priority sector lending targets for Banks offered the first signs of policy flexibility towards MFIs. One could argue that MFIs are small and insignificant, so why bother. The larger point is about policy space for innovation and diversity of approaches to meet large unmet demand. The insurance sector was partially opened to private and foreign investments during 2000. Over 20 insurance companies are already active and experimenting with new products, delivery methodologies and strategic partnerships.

Microfinance programmes have rapidly expanded in recent years. Some examples are:

Membership of Sa-Dhan (a leading association) has expanded from 43 to 96 Community Development Finance Institutions during 2001-04. During the same period, loans outstanding of these member MFIs have gone up from US$15 million to US$101 million.

The CARE CASHE Programme took on the challenge of working with small NGO-MFIs and community owned-managed microfinance organisations. Outreach has expanded from 39,000 to around 300,000 women members over 2001-05, Many of the 26 CASHE partners and another 136 community organisations these NGO-

39

Potential of micro finance of j&k( A COMPARATIVE STUDY )

MFIs work with, represent the next level of emerging MFIs and some of these are already dealing with ICICI Bank and ABN Amro.

In addition to the dominant SHG methodology, the portfolios of Grameen replicators have also grown dramatically. The outreach of SHARE Microfin Limited, for instance, grew from 1,875 to 86,905 members between 2000 and 2005 and its loan portfolio has grown from US$0.47 million to US$40 million.

Since banks face substantial priority sector targets and microfinance is beginning to be recognised as a profitable opportunity (high risk adjusted returns),[1] a variety of partnership models between banks and MFIs have been tested. All varieties of banks - domestic and international, national and regional - have become involved, and ICICI Bank has been at the forefront of some of the following innovations:

Lending wholesale loan funds.

Assessing and buying out microfinance debt (securitisation).

Testing and rolling out specific retail products such as the Kissan (Farmer) Credit Card.

Engaging microfinance institutions as agents, which are paid for loan origination and recovery, with loans being held on the books of banks.

Equity investments into newly emerging MFIs.

Banks and NGOs jointly promoting MFIs.