postal financial services for anywhere, anytime banking -transformation of...

TRANSCRIPT

Postal Financial ServicesFor

Anywhere, Anytime Banking-Transformation of India Post for Vision 2020-

Hans BoonVice President

Core Counter Core Counter

Fast ‘moving’ transactionsFast ‘moving’ transactions

Financial ShopFinancial Shop

Get help sale & adviceGet help sale & advice

Post Office Network and retail formulasPost Office Network and retail formulas

The Dutch Postal Law requires that – there are a minimum of 2102 postal outlets, of which 902 full service outlets – 95% of all consumers should live within 5 km of a full service postal outlet– all places >5000 inhabitants have a full service postal outlet < 5 km– For every 50.000 inhabitants there should be at least 1 full service postal outlet

Within the borders of the Postal Law, TPG Post and Postbank try to optimally balnace costs with service level by applying specific retail formulas”On top of this basic shared network there are :

– stamp resellers (bookshops, supermarkets, kiosks)– TPG Post Business Point in business areas, dedicated to bulk volume corporates and institutions- not for the individual public) – ATMs (for Postbank cash withdrawals)

Managing the post officesManaging the post offices

Post Offices Ltd

Board of Commissioners TPG - Postbank

Contract Postbank Contract TPG Post

SLA and Cost

Profit and performance

Structure of Post officesa shared mass retail distribution infrastructureStructure of Post officesa shared mass retail distribution infrastructure

50% 50%

CustomersInternet: 170.000*

Call Center: 220.000*

Mail: 365.000*

Face: 650.000*

WAP/SMS: 25.000*

Customer database

Back Office*Customer interactions per day

Multi-Channel DistributionMulti-Channel Distribution

This is PostbankThis is Postbank

Insurance Products4-10%

Market Shares 2002

Acquisition7.5 Million

Private GiroAccount Holders

77.5.5 MilMillionlionPrivate Private GiroGiro

Account HoldersAccount Holders

Payment Products42%

Savings15%

Consumer loans14%

Investment Fundsand Broking Service

4%

Mortgages7%

SME (Payments+Savings)

25%

Postbank, NetherlandsKey figuresPostbank, NetherlandsKey figures

8 million clients (75% of adult population and 80% of companies)9 million cards issued (debit card + chip)6 million payment transactions per day1.3 million On-line (Internet bank) clients0.6 Mobile bank clients>600 million mail items per year>Eur 400 m profit; per employee EUR 100.000

Responsible for all financial services through post offices65% of transactions at post offices: Postbank15% traditional postal transactionsPost offices: nearly 2,300 outlets. Organized in a Joint Venture with TPG Post as a profitable cost-centreLargest mail client

Netherlands and PostbankNetherlands and Postbank

Considered as the world’s most advanced Postbank in terms of market and financial performance

Strong impact of Postbank on:– Accessibility to basic financial services;– Efficiency in the payments system;– Sustainability of the post office retail network

Postal reform sweeps through AsiaPostal reform sweeps through Asia

Postal reform taking shapeChanging scene postal sectorIncreasing volumes Asia PacificOverview Asia postal operatorsIndicated gaps in Asian postal servicesFacing the big issues?Broadening the revenue base?Increasing efficiency?e-Commerce and e-GovernmentAssessment management priorities

Postal reform taking shapePostal reform taking shape

Increasing awareness of Post as a business leading to incorporation of Posts in many countries

– Key issue: what is (or can be) done more or differently with independent position?

Increasing private sector participation in new business markets

– Key issue: which markets are most potential?Trend towards further privatization of postal operatorsGlobal integrators taking away core markets especially in international letters and parcelsChallenge for Posts to change business models

Changing scene postal sectorChanging scene postal sector

Challenge of handling more mail in efficient wayUPU statistics indicate higher growth in Asia Pacific region

Background reform in AsiaBackground reform in Asia

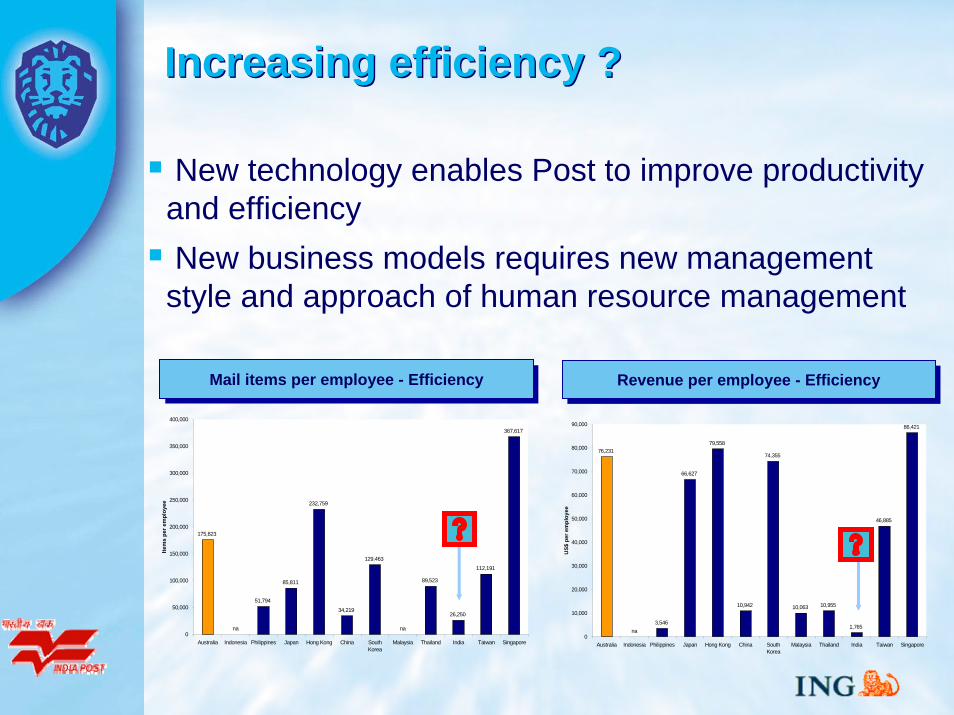

Increasing efficiency ?Increasing efficiency ?

New technology enables Post to improve productivity and efficiencyNew business models requires new management style and approach of human resource management

175,823

na

51,794

85,811

232,759

34,219

129,463

na

89,523

26,250

112,191

367,617

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Australia Indonesia Philippines Japan Hong Kong China SouthKorea

Malaysia Thailand India Taiwan Singapore

Item

s pe

r em

ploy

ee

Mail items per employee - EfficiencyMail items per employee - Efficiency

76,231

na3,546

66,627

79,558

10,942

74,355

10,063 10,955

1,765

46,885

86,421

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Australia Indonesia Philippines Japan Hong Kong China SouthKorea

Malaysia Thailand India Taiwan Singapore

US$

per

em

ploy

ee

Revenue per employee - EfficiencyRevenue per employee - Efficiency

Overview Asia postal operatorsOverview Asia postal operators

China

• Domestic Monopoly• 100% Govt. owned• Reform under consideration

South Korea

• Domestic Monopoly• 100% Govt. owned• No privatisation plans

Philippines

• Domestic Monopoly• 100% Govt. owned• Privatisation adviser appointed

Japan• Deregulated open market• 100% Govt. owned• Privatisation in 2007

Singapore

• Domestic monopoly• Recently privatised IPO

Indonesia

• Domestic Monopoly• 100% Govt. owned• Placed on privatisation list but seen

as medium rather than short term

Australia

• Domestic Monopoly• 100% Govt. owned• No firm privatisation plans

Thailand

• Domestic Monopoly• 100% Govt. owned• Incorporated as per 14 Aug 2003;• IPO in 2008

Indonesia

• Domestic Monopoly• 100% Govt. owned• Incorporated as per 1 Jan 2003 and

privatisation being prepared

Hong Kong

• Domestic Monopoly• 100% Govt. owned• No privatisation plans

Malaysia

• Domestic Monopoly• Privately Listed Company• Privatised in 2001 via trade sale

India

• Domestic Monopoly• 100% Govt. owned• Turn around plan under preparation

Indicated gaps in Asian postal servicesIndicated gaps in Asian postal services

Opportunities in postal marketsOpportunities in postal markets

Value added servicesHybrid mail solutionsLogistics and supply-chain managementAdvertising mail and mail orderPostal financial servicesRetail services

Assessment of management prioritiesAssessment of management priorities

Declining market share Not-competitive

Declining market share Not-competitive

Antiquated servicesPoor service qualityCost inefficient

Antiquated servicesPoor service qualityCost inefficient

Limited investmentsNo access to capitalNo policy priority

Limited investmentsNo access to capitalNo policy priority

Many Postal operators trapped in a vicious circle Many Postal operators trapped in a vicious circle

What future ?Acute need to Break-through with

new services and fresh capital

Worldwide PFS Development Review

TransactionsSavingsAccountsPost OfficesRegion

94 mill$5.7 bill26 mill20,000MENA (6)

7 mill$0.5 bill5 mill11,500AFR (17)

354 mill$83.0 bill335 mill289,000ASIA (6)

65 mill$0.2 bill1.5 mill37,000LAC (7)

2,850 mill$ 4.6 bill16.2 mill106,000ECA (27)

3,370 mill$93.0 bill387.5 mill463,500TOTAL (63)

> 600 million individuals access financial services through post offices

Payments

Savings

Pensions

Insurance

CreditBill Payment

Payments accounts/cards issued in an increasing number of CEE countries; also electronic money transfer networks

Tradition as agent of State Savings Bank replaced with partnerships;

Introduced in several CEE countries

Introduced in several CEE countries

Provided in cooperation with (postal) banks in Romania, Czech Rep., Ukraine..Widely existent, in many countries postal networks are large(st) operator of small value payment transactions

Europe and Central Asia

In most cases, public-private partnerships Institutional

Europe in evolution Europe in evolution Postal Financial Services in the European UnionOne Stop Shopping- Broad Range of Services

CountiresPayments

Accounts/Cards

SavingsConsumer

CreditMutual Funds Insurance

Pension Plans Internet

Austria

Belgium

Denmark

Finland

France

Germany

Greece

Iceland

Ireland

Italy

Luxemburg

Netherlands

Norway

Portugal

Spain

Sweden

Switzerland

United Kingdom

Europe in evolutionEurope in evolution

As a phase in the transformation,Swiss and Italian Posts have

established alliances for specificproduct lines (mutual funds,

insurance)

Transformation ofFinancial Services into abank or an alliance with abank is being considered

Creation of alliancewith banks in

consideration orpreparatory stage

Postbank is asubsidiary of the

Posts

Post Offices are 50%owned by Postbank (ING)

Partnership Post- Bank PFS Division of Posts PFS Subsidiary Company with >50% ownership by Posts

Originally organized within the PostTrend towards ‘partnership’ between Post and (Post) bank

– Alliance/ Contract/JV– Subsidiary

Significant market share in payments and savings

Europe in evolutionEurope in evolutionPostal Financial Services in the European Union/ Western Europe

Countires PFS division PFS Subsidiary PFS Partner Comments

Austria BAWAG- PSK Group

Belgium Fortis Group

Denmark Danske Bank

Finland Sampo

FranceDivision, Asset Mngt by Caisse des Depots et Consigniations

Germany Deutsche Postbank AG

Greece TT; 100%state-owned bank

Iceland Postgiro

Ireland AIB

ItalyBanco Posta and various Financial Institutions

Luxemburg CCP

Netherlands ING (Postbank)

Norway den Norske Banken/ Postbanken

Portugal Caixa Geral

Spain Deutsche Bank (Espania)

Sweden Nordea

Switzerland UBS/ Winterthur

United Kingdom All large banks

Central and Eastern Europethe leap forwardCentral and Eastern Europethe leap forward

Postal Financial Services Overview in The Central and Eastern EuropeBosnia & Hercegovina

Postbank in Restructuring; Raiffeisen Zentralbank acquired Hrvatska poštanska banka- Mostar

BulgariaBulgarian Postbank (Alico+ EFG-Eurobank) has been privatised

CroatiaHrvatska Poštanska Banka will merge with Croatia Bank early 2003

Czech RepublicPoštovni Sporitelna (a division owned by CSOB-KBC)

EstoniaPostipank operated as brand allliance between Eesti Post and Eesti Uhis Pank (Sampo-Finland)

HungaryPostabank in privatisation process; has 30% owners

LatviaPostal Giro Accounting Centre (PNC) as aprt of Latvia Pasts

LithuaniaContracts with various banks for a limited scope of services

MacedoniaPoštenska Stedelnica (limited banking license, majority owned by the post)

Poland Bank Pocztowy (66% owned by the Post)

Romania Banc Post (70% private, EFG-Eurobank)

Slovak RepublicPoštova Banka (11% owned by the Post, in privatisation process)

SloveniaPoštna Banka (38% owned by the Post and 62% by a State Fund, in privatisation process)

YugoslaviaPoštenska Stedionica- in process of being licensed as a full-fledged bank

Middle East North Africa

Payments

Savings

Pensions

Insurance

CreditBill

Payment

7.5 million accounts for salary payments and strong position in cash payments and remittancesStrong penetration (up to 30% of adults) and over 10% of market value, usage high (few dormant accounts)

Access to pensions non-existent;

Access to insurance non-existent, except Morocco

Virtually non-existent but some preparatory activity

Some success in bill payment (cash society)

All state-owned, some as separate divisions, and some product partnerships with private sectorInstitutional

Africa

Payments

Savings

Pensions

Insurance

CreditBill

Payment

0.5 million accounts for salary payments (teachers, military and public servants)Strong penetration (up to 30% of adults) but low usage (high number of dormant accounts)

Non-existent

Non-existent, some small scale pilots

Virtually non-existent, except through some postal banks and small-scale pilots

Widely differing per country, often non existent

All state-owned, some postal banks function as companies separated from PostsInstitutional

Payments

Savings

Pensions

Insurance

CreditBill Payment

Non existent, with the exception of Brazil

Virtually non-existent; Brazil has successfully introduced savings services

Non-existent

Non-existent

Brazil recently developed credit services, meeting strong demandBeyond Brazil existent on a small scale and where new technology exists (Uruguay, Chile, Argentina)

Latin America, Caribbean

Brazil is a public-private sector partnership; in some other cases product partnerships Institutional

Banco Postal, BrazilBanco Postal, BrazilPolicy ideas 1996-1997Feasibility Study 1998-1999 including nationwide market and opinion research) Pilot with 36 Post offices (April 2000-April 2001)Change of regulatory framework allowing post offices to become “correspondent”of a bank (March 2001)Public auction “Banco Postal” (July 2001 Bradesco won all 15 licenses (Sept 2001)Contract negotiations and preparations for implementationLaunch of services in 1,000 Post Offices in March 2002; Product offer includes VISA electron card, and current account and deposit accountSubsequently expansion to currently 5,000 post offices>3.500,000 accountholders, previously unbanked;averagedeposit > US$ 600; Micro finance offered since August 2003; within 2 weeks more than 6,000 contracts; now leader in Microfinance with > 300,000 contractsExpansion to pensions, life insurance as “Seguros Postal”expected to be launched in next 6 months.Further product diversification...

Asia

Payments

Savings

Pensions

Insurance

CreditBill Payment

Few offer services for the payment of salaries

Strong penetration with 335 million accounts but high number of dormant accounts; small product rangeAccess to pensions non-existent; except for pilot projects in India Access to insurance non-existent; except for pilot projects in India, China

Non-existent but being considered in some countries

Exist in several countries, Thailand, China, India, Sri LankaAll state-owned; very diverse models, including product partnerships/ relations with banksInstitutional

China PostChina Post

Thailand Post / Pay-at-PostThailand Post / Pay-at-Post

Vietnam Postal SavingsVietnam Postal Savings

Countries PFS divisionPFS

SubsidiaryPFS

Partner(s) Comments

AustraliaNationwide transaction and sales network for payments, current accounts and deposits

Bangla DeshMainly money transfers and collection, but also savings mobilisation

CambodiaMainly money transfers and collection, but also savings mobilisation

ChinaEstablished in 1986, strong payments and savings function; product scope being expanded through partnerships

IndiaPOSB + money transfer function within the country; new partnerships established- postal finance marts

Indonesiamainly money transfer services and savings bank agency relationhips

IranPostbank established in 1998; being developed as a provider of modern retail financial services also in rural areas

JapanDeposit, insurance and payment services; largest postal financial institution in the world

MalaysiaPrivatised postal operator operates giro and has arrangements with 6 banks, including National Savings Bank

MongoliaPostbank recently established; main focus on corporate financial services

New ZealandPostbank privatised and sold in 1988; new Kiwibank established to provide retail financial services

PakistanPakPostbank provides payments and savings services; credit function under discussion

PhilippinesPhilPostbank provides mainly deposit and transfer function; earmarked for privatisation

SingaporeAfter separation/privatison of POS Bank, a new initiative is launched to introduce financial ser

Sri LankaNational Savings Bank utilises post offices as ancillary network; money transfers done by Post

TaiwanPOSB largest deposit taker in the country; provides also money remittances; earmarked for privatisation

ThailandAfter incorporation of Thailand Post, contract with 3 banks to expand range of services "Pay-at-Post"

VietnamVPSC recently established to develop savings and money transfer services through Post

Japan Post’s Privatization 2007-2017Japan Post’s Privatization 2007-2017

Post Office Network Co.

Japan Post

Postal Savings Bank

Postal Life Insurance Co.

Holding In 2017 <30% state ownership

Third Parties’

Services

Phased restructuring ensuring the sustainability of the postal network as access point

Postal Savings Bank obliged to used all post offices for delivery of its financial services

DiagnosisDiagnosisThe Study reviewed financial service operation through postal networks in 63 developing countries, with a total of 463,500 post offices, (91% of all post offices in developing countries.

Postal networks are uniquely large. In 73% of the countries there are more post offices than bank branches, agencies and micro-finance outlets together. As a result of their historic role as component of the public communications and information infrastructure, post offices tend to be evenly spread over the country, and much more strongly represented in rural areas than banks.

Private-public partnerships between postal operators and private financial institutions have emerged in 15 countries. In the past 8 years postal banking partnerships have expanded access to more than 12 million poor and low-income individuals in both rural and urban areas with a full range incl credit and insurance on a competitive basis

DiagnosisDiagnosis

In about 50 developing countries, the historically evolved postal financial operations provide access to an estimated 600 million individuals mainly for money transfer services and small savings. This concerned in 2002 370 million postal savings accounts with a total balance of more than US$ 90 billion and 3.4 billion cash-based money transfer operations (including international remittances). In view of their network size and accessibility, the Study also finds that post offices leave much of their potential in financial service delivery to the poor and in rural areas uncaptured. Nevertheless, in 54% of the cases reviewed financial services are the single largest revenue source for the postal operator. In more than 70% of the cases, revenues from financial services are estimated to cover the expenditure of the entire post office retail network and to produce profits that help to cover losses in the postal mail services.

Historic models need to be reformedHistoric models need to be reformed

Features/SymptomsPoor service qualityLoss of market share; less than 3%Increasing dormant accountsHigh cost; inefficientLosses in asset managementInternal clashes between Post and provider of Postal Financial Services

ReasonsLack of response to customer needs due to legal and institutional frameworkLack of business orientation -unstable environmentInadequate investments in product and IT developmentLack of credible partnersConflicting missions (post-bank)

Typical product featuresState Guarantee on DepositsTax exemptLow minimum deposit requirementAvailable at all post officesLimited fragmented product approach

Typical institutional featuresOwned by Ministry of Finance or specific fundOperated and managed by PostsNot supervised by Central BankResources invested in State Treasury / Gilt-edged titles

Bypassing Capital and Money markets

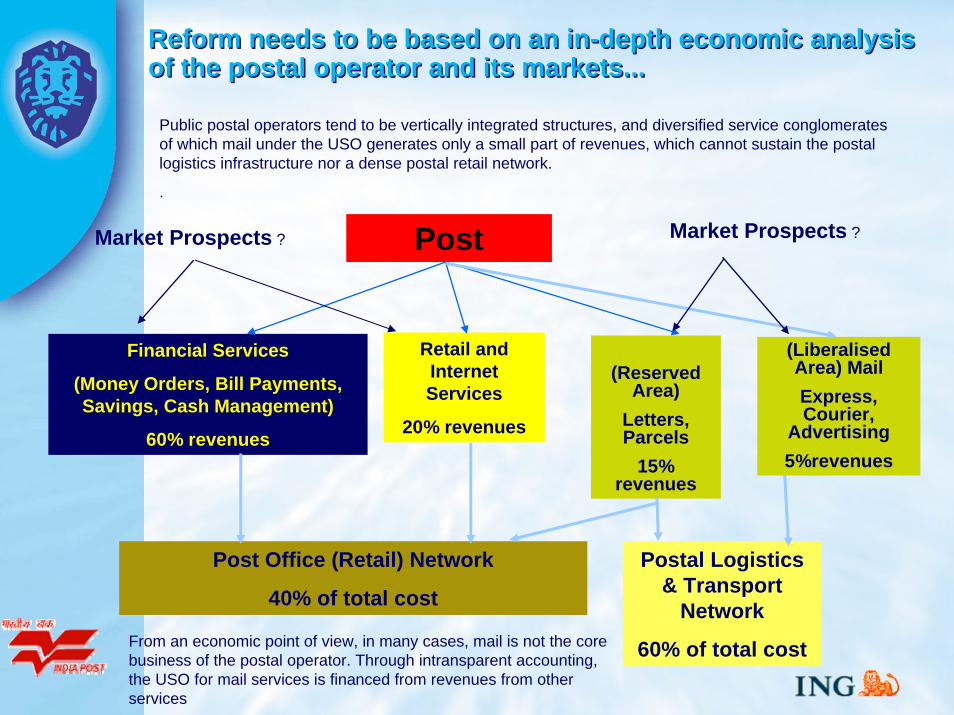

Reform needs to be based on an in-depth economic analysis of the postal operator and its markets... Reform needs to be based on an in-depth economic analysis of the postal operator and its markets...

Post

Financial Services

(Money Orders, Bill Payments, Savings, Cash Management)

60% revenues

Retail and Internet Services

20% revenues

(Reserved Area)

Letters, Parcels

15% revenues

Post Office (Retail) Network

40% of total cost

Postal Logistics & Transport

Network

60% of total cost

(Liberalised Area) MailExpress, Courier,

Advertising5%revenues

Public postal operators tend to be vertically integrated structures, and diversified service conglomerates of which mail under the USO generates only a small part of revenues, which cannot sustain the postal logistics infrastructure nor a dense postal retail network.

.

From an economic point of view, in many cases, mail is not the core business of the postal operator. Through intransparent accounting, the USO for mail services is financed from revenues from other services

Market Prospects ?Market Prospects ?

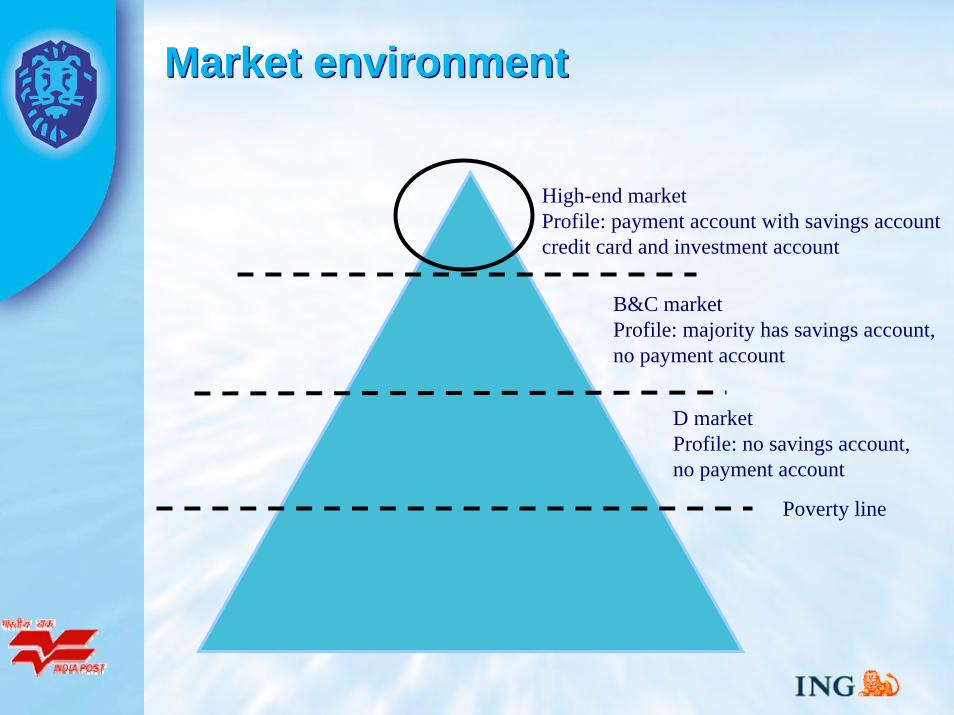

Market environmentMarket environment

High-end marketProfile: payment account with savings accountcredit card and investment account

Poverty line

B&C market Profile: majority has savings account,no payment account

D marketProfile: no savings account,no payment account

Market environment (II)Market environment (II)

Volume

Value

Low

High

Low High

Bank A

Bank D

Bank B

Bank C

Bank E

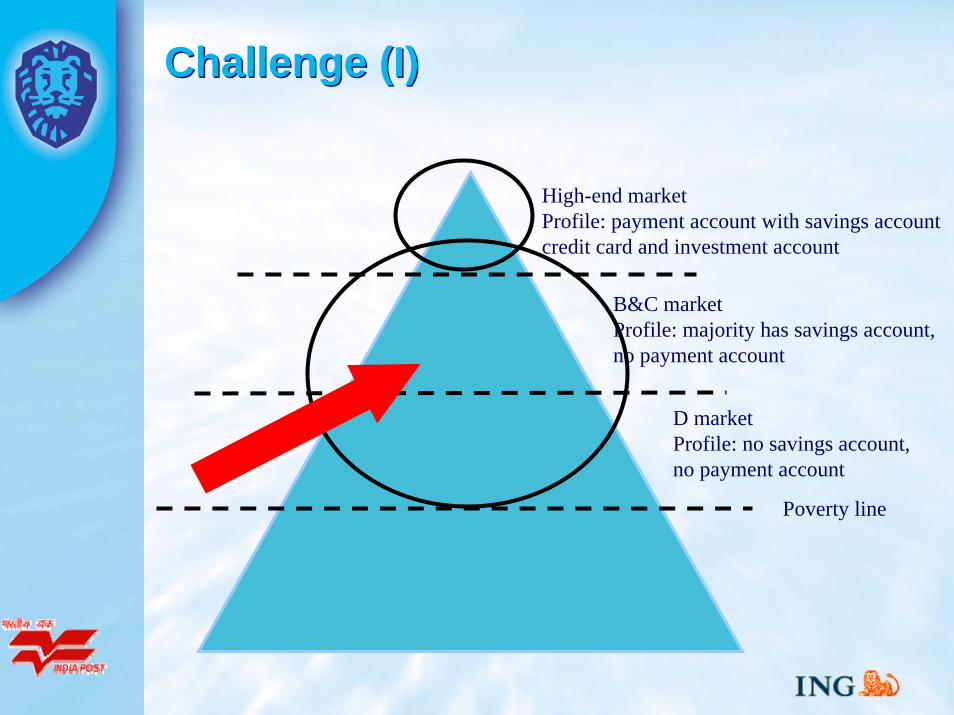

Challenge (I)Challenge (I)

High-end marketProfile: payment account with savings accountcredit card and investment account

Poverty line

B&C market Profile: majority has savings account,no payment account

D marketProfile: no savings account,no payment account

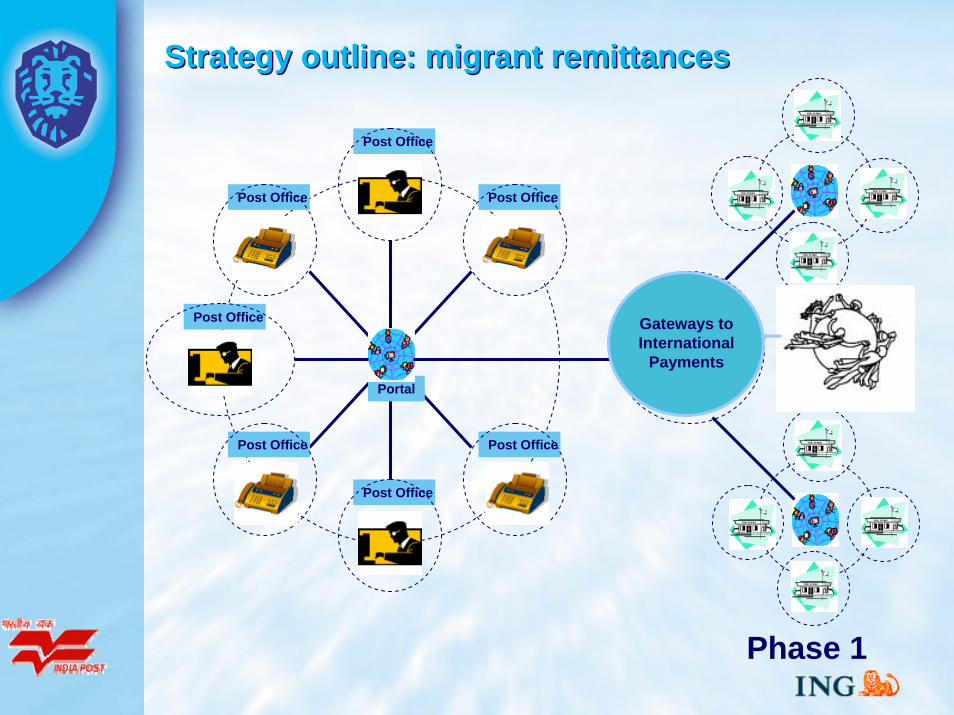

Strategy outline: migrant remittancesStrategy outline: migrant remittances

Portal

Post Office

Post OfficePost Office

Post OfficePost Office

Post Office

Post Office

Phase 1

Gateways to International

Payments

Strategy : payroll/payment servicesStrategy : payroll/payment services

PONSCounter ATM

Post Office

Post OfficePost Office

Post OfficePost Office

Post Office

Counter

Post Office

Counter

Phase 2

Strategy : other (postbank) servicesStrategy : other (postbank) services

PONSCounter ATM

Post Office

Post Office

Counter

Post Office

Post OfficePost Office

Counter

Media kiosk

Paymentterminal

Media kiosk

Paymentterminal

Post Office

Counter

Phase 3

ATM

Counter ATM

Internet café

Internet café

+ Other

Postbankservices

A learning curve- for Post, its partners and clientsA learning curve- for Post, its partners and clients

Time

Functionality

(inter) national money transfers

+ Payroll services, Internet access, e-mail, service portal

Current situation

+Insurance, mutual funds, securities, credit

+savings, /(bill) payment services, EFT POS

+loyalty/ticketing/transport applications

Value Added Postal ServicesVirtual Mobile Operator (VMO)

Internet Service Provider (ISP)

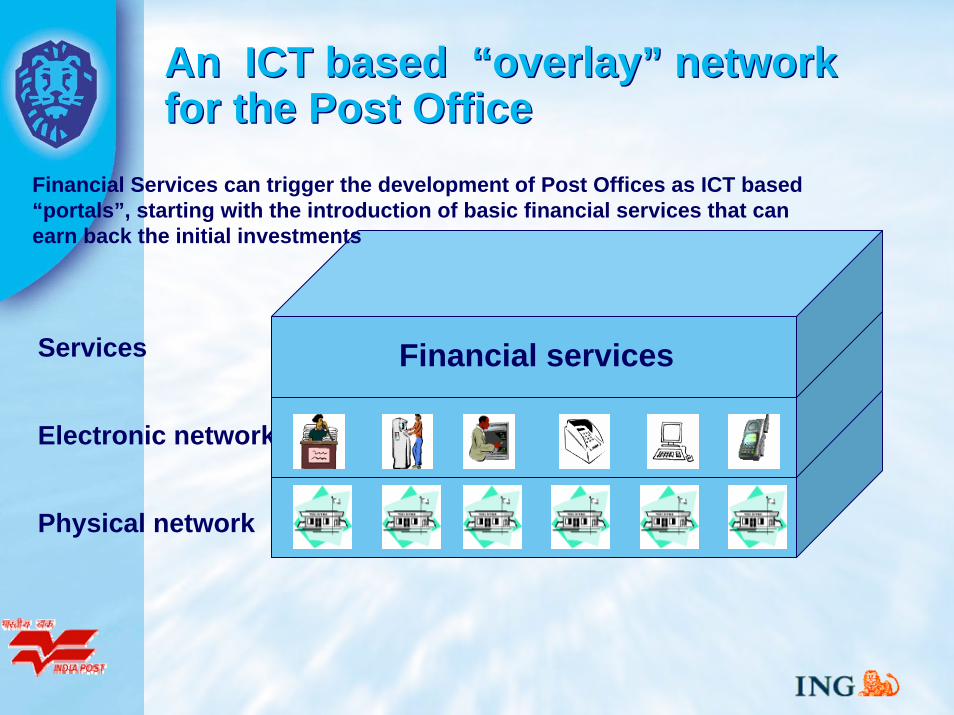

An ICT based “overlay” network for the Post OfficeAn ICT based “overlay” network for the Post Office

Physical network

Electronic network

Services Financial services

Financial Services can trigger the development of Post Offices as ICT based “portals”, starting with the introduction of basic financial services that can earn back the initial investments

Physical network

Electronic network

Services Other e-services

And provide the infrastructure towards other e-servicesAnd provide the infrastructure towards other e-services

Post Office“Portal”

PostTelephone

Banking

Government

Postcards

Fax

And help to reposition Post Offices as Portals-And help to reposition Post Offices as Portals-

Service Access Points

to a broad array of (e) services

Payments

Profile of the Financial Services offered through the Post Profile of the Financial Services offered through the Post

Customers:Focus on local consumer market and corporates (employers, utilities, retail chains)Products:Full range of standard financial products and servicesDistribution:Direct marketing approach via multichannel distributionInstitutional:Various options/model, trends towards partnership with fully licensed financial institutions

Consumer: Post (bank) is Different!Consumer: Post (bank) is Different!Traditional bank

SegmentedHigh entryPersonal sellingBroad range ofspecialist productsIntransparent

Own branches

Short opening hours/ 5 days

Post(banking):a viable solution for mass financial services

Post(bank)Mass scaleLow entry“Anonymous”Broad range of standard productsTransparent

Post Office with multichannel

Long opening hours/ 6 days

Direct BankSegmented High entry“Anonymous”Broad range of standard productsTransparent

Internet/Phone

24 hours/ 7days

Growth inaccounts

accountholders

Postal cards/accounts: the gatewayPostal cards/accounts: the gateway

Mortgages

Consumer credit

Investment fundsand discount broking

Savings

Payment products

Insurance

Retail Concept Retail Concept

Convenience• Easy access and

low threshold• Standardized products

Competitive price• Free (basic) payment

package• Value for money

Credibility• Good, efficient service• Decent (no fine print)• Reliable (mail and IT)

Crystal clear products• Full basic range• Transparent product

rangecontinuous communication pressureexcellent service qualityintegrated customer approach

++

+

... The account is our ‘shop’ without thresholds, accessible for everybody

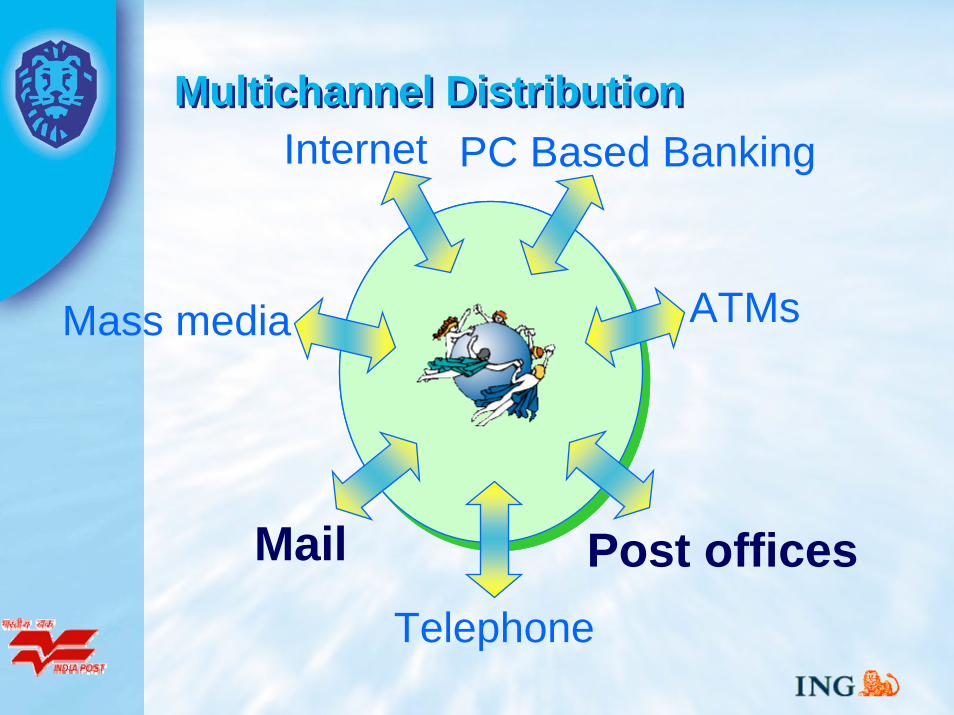

Multichannel DistributionMultichannel Distribution

Mass media

Internet PC Based Banking

ATMs

Post officesTelephone

Moving ForwardMoving Forward

Key ObjectivesKey Objectives

Expansion of the range of financial services into a fully-fledged financial institution and the set-up of a regulatory and governance framework in compliance with the financial sector;Sustainable, competitive package, that also meets public sector policy objectives (access to financial services, financial literacy, efficiency..)Transparency in accounting between postal (mail) and postal financial services and the cost/revenues related to the postal network;Economic sustainability of the postal network after the set up of the financial institution.

Key Issues (I)Key Issues (I)

Regulatory Framework Financial ServicesCorporate GovernanceManagement and managerial autonomyHuman Capital and CapacityBuildingAccess to finance to fund ModernisationChange Management and Project Implementation capacity

Key Issues (II)Key Issues (II)

Cross-coordination of Government’s sectoralpolicies (Financial, ICT and Postal);Commercialisation and building sustainable public/private sector partnerships based on a Corporate Strategy (Organic Growth vsIn/Outsourcing); Management accountability;

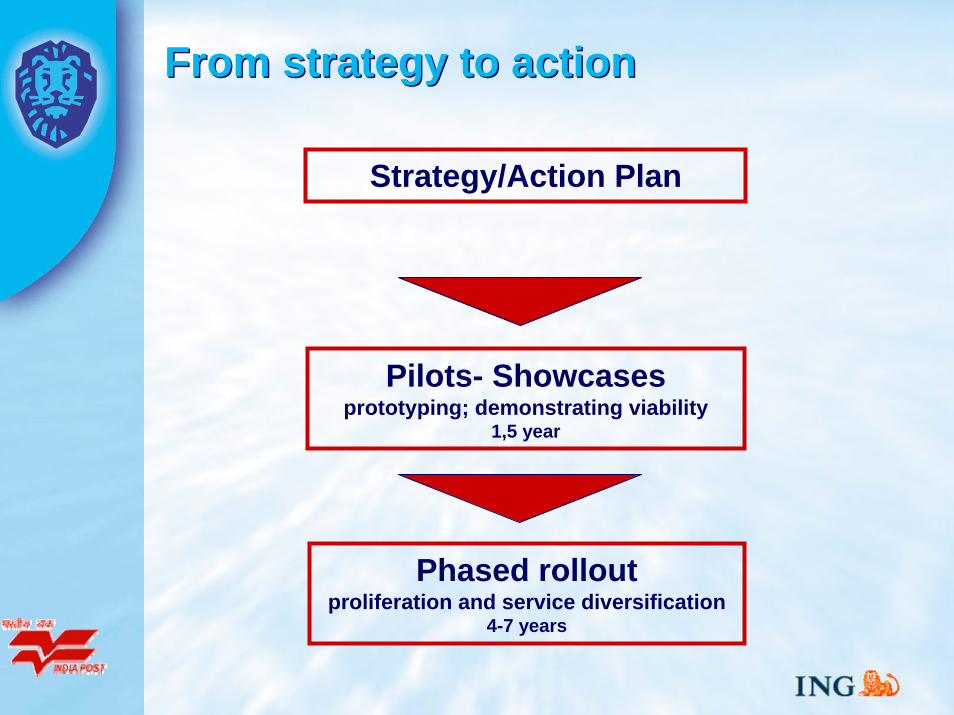

From strategy to action From strategy to action

Strategy/Action Plan

Phased rollout proliferation and service diversification

4-7 years

Pilots- Showcasesprototyping; demonstrating viability

1,5 year

From Strategy to Action PlanFrom Strategy to Action Plan

Market analysis and DiagnosisStrategic Concept Short-term steps

– Optimizing current PFS– International Payments– Consolidated Cash Management– Building of a Business Unit Financial Services within Post with Cost-Allocation/MIS

Implementation of the Strategy– Pilots– Stakeholders’ approach– Building Partnerships with other parties– Finance– Regional and International Cooperation