post-issuance compliance for municipal bond issuers you for participating in foster pepper’s...

TRANSCRIPT

Thursday, October 22, 2015

PRESENTATION MATERIALS

Post-Issuance Compliance for Municipal Bond Issuers

Basic Training on Tax and Securities Responsibilities

Thank you for participating in Foster Pepper’s seminar, “Post-Issuance Compliance for Municipal Bond Issuers: Basic Training on Tax and Securities Responsibilities.” Short speaker biographies are included and you can learn more by visiting www.foster.com. Speaker Biographies (in speaking order): Kate Manley, State of Washington

William Tonkin, Foster Pepper

Lindsay Coates, Foster Pepper

Marc Greenough, Foster Pepper

Nancy Neraas, Foster Pepper

Lunch Speaker Biography Thomas Ahearne

Kate Manley Debt Compliance Officer, State of Washington Kate is the Debt Compliance Officer in the Debt Management division of the Office of the State Treasurer. She has been at OST since 2011 and worked primarily in the bond program until transitioning into compliance. Before working at OST, Kate worked for several years in the nonpartisan research office of the state House of Representatives.

Post-Issuance Compliance for Municipal Bond Issuers

Speaker Biographies

William Tonkin Member 206.447.8967 [email protected] Bill's practice is focused on public finance, specializing in federal tax requirements and restrictions, including arbitrage and arbitrage rebate requirements, applicable to all kinds of tax-exempt obligations, including state and local bonds, qualified 501(c)(3) bonds, qualified small issue (industrial development) and exempt facility bonds. He has extensive experience in general business and corporate area emphasizing federal taxation and securities regulation.

Lindsay Coates Associate 206.447.7263 [email protected] Lindsay focuses her practice on municipal and public finance law, including general municipal issues pertaining to state and local governments, public authorities, civil service, and public employment. She also supports various aspects of clients’ public finance transactions and participates in a wide range of roles, including bond counsel, underwriter’s counsel, and borrower’s counsel. Prior to obtaining her law degree, Lindsay brokered directors’ and officers’ liability insurance on behalf of publicly traded and complex private companies.

Marc Greenough Member 206.447.7888 [email protected] Marc is a member of the firm’s Municipal Government and Public Finance practices and serves as bond counsel, underwriters' counsel, and disclosure counsel on general obligation, revenue, and special obligation financings by state, local, and tribal governments. In addition, Marc has extensive experience in structuring municipal and public/private ventures and in providing representation in administrative proceedings and litigation.

Nancy Neraas Member 206.447.6277 [email protected] Nancy has more than 25 years of experience as bond counsel for cities, counties, and special districts (public utility districts, water, sewer, park, school, and fire protection) in Washington and other states on municipal financings, including general obligation bonds, revenue bonds and special assessment district financings. Nancy has worked on numerous electric utility financings for various cities, public utility districts, and other special districts. Nancy is disclosure counsel for many issuers, including the State of Washington.

Thomas Ahearne Member 206.447.8934 [email protected] Tom Ahearne has over 30 years of litigation experience. His practice focuses on two distinct areas: (1) representing policyholders in insurance coverage disputes, and (2) representing litigants in suits based on constitutional law, statutory rights, and election disputes. Insurance Coverage: Tom has been successfully representing insureds and claimants in a wide array of state and federal court coverage litigation since the 1980s. He’s a frequent speaker on insurance coverage at trade association and legal industry seminars, and was named the Best Lawyers® 2011 Insurance Law “Lawyer of the Year” in Seattle. Constitutional Law, Statutory Rights, & Elections: Tom’s experience over the past three decades includes major constitutional suits such as the McCleary education funding litigation, election disputes such as the Rossi-Gregoire Governor’s election lawsuits, numerous ballot title challenges including I-933, I-895, I-892, I-885, I-884, I-864, & I-860, and cases resolving the enforcement or validity of statutes and initiatives such as Washington’s Top-Two primary system and various Tim Eyman measures. Tom’s related work has been recognized in publications such as Washington Super Lawyers (2012 “Paramount Duty” article) and Seattle Magazine (“2010 Most Influential Lawyer of the Year”).

Post-Issuance Compliance for Municipal Bond Issuers:

Basic Training on Tax and Securities Responsibilities

October 22, 2015

Tax Kate Manley, Debt Compliance Officer, State of Washington

Bill Tonkin, Foster Pepper Lindsay Coates, Foster Pepper

3

The Purpose of Post-Issuance Compliance Policies and Procedures

Review of Private Use Rules

Identifying Private Use Issues

Review of Arbitrage Rebate Rules

Identifying Arbitrage Rebate Issues

Summary of Compliance Tips

Tax Discussion Topics

4

Revised Form 8038-G Line 43: Written procedures relating to “remedial action” Line 44: Written procedures relating to compliance with arbitrage rules

Purpose of Post-Issuance Compliance Policies

5

Provide Continuity of Attention Allow the policies and procedures to survive employee turnover during the life

of the bonds

Prevent or Avoid Violations

Promote Early Discovery of Violations Regular review of federal tax law compliance Correspond with required EMMA filing deadlines?

Purpose of Post-Issuance Compliance Policies

6

Ability to exercise remedial action because of a change in use of bond financed property Any permitted redemption or defeasance of non-qualified bonds must occur

within 90 days

Waiver of 50% penalty on late arbitrage payment Requires finding of no “willful neglect,” which may be shown by following

established compliance policies and procedures

Purpose of Post-Issuance Compliance Policies

7

Potential Benefit under IRS Voluntary Closing Agreement Program (VCAP) Information that an issuer must submit includes:

an affirmative or negative statement as to whether it has adopted comprehensive written compliance procedures

Detailed description of the portion of such comprehensive procedures which relate to the violation

Purpose of Post-Issuance Compliance Policies

8

Equitable factor in determining appropriate closing agreement amount with the IRS under VCAP Measure “taxpayer exposure” from date of discovery of violation

New IRS resolution standards for VCAP requests after March 30, 2016 100% of “taxpayer exposure” if submit VCAP application within 6 months

after violation 110% of “taxpayer exposure” if submit VCAP application between 6 months

and 1 year after violation

Purpose of Post-Issuance Compliance Policies

9

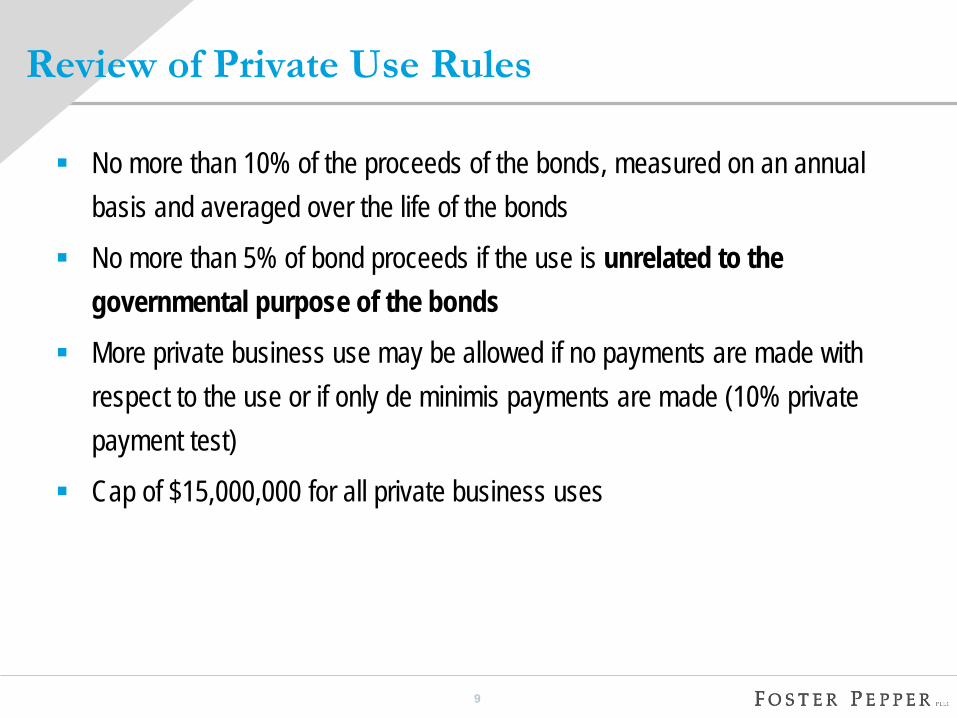

No more than 10% of the proceeds of the bonds, measured on an annual basis and averaged over the life of the bonds

No more than 5% of bond proceeds if the use is unrelated to the governmental purpose of the bonds

More private business use may be allowed if no payments are made with respect to the use or if only de minimis payments are made (10% private payment test)

Cap of $15,000,000 for all private business uses

Review of Private Use Rules

10

For buildings, private business use generally is measured by percentage of space used in private business use averaged over life of bonds

May allocate equity to portions of building used in private business use

Management contracts that are not qualified can result in private business use of the entire building

Review of Private Use Rules (con’t.)

11

Examples of arrangements that can result in private use include: Private Ownership Nonqualified management and service contracts Leases, including cell tower leases Naming rights Preferential rates for certain customers Use by federal government and nonprofits on preferential basis Certain “take” and “take or pay” contracts for “output facilities”

Keep records of any contracts providing special legal entitlements to use property

Identifying Private Use Issues

12

Examples of arrangements that are not private use include: General public use Use by a person not engaged in a trade or business Use by another state or local governmental entity Use according to a uniformly applied rate schedule Qualified management and service contracts Certain short-term uses Incidental use, such as advertising displays and vending machines

Identifying Private Use Issues (con’t.)

13

Educate users of property Includes persons with authority to propose:

Any lease of the property Operation or the property under a management or service contract Any sale or other disposition of all or any part of the property

Involve legal counsel when new use arrangements proposed “Was this property financed with tax-exempt bonds?”

Identifying Private Use Issues (con’t.)

14

Arbitrage and Rebate rules apply to: Earnings on investments of bond proceeds prior to being spent, and Earnings on investments of certain revenues set aside to pay bonds

Rebate excess of amount earned over what would have been earned if invested at bond yield.

Generally not applicable since 2008, but future investment rates could be higher – e.g., on reserve fund investments

Review of Arbitrage Rebate Rules

15

Timing for Rebate Computation

At least every five years from issue date Upon expenditure of bond proceeds Upon final maturity or early redemption of all bonds

Form 8038-T and payment due within 60 days after the computation date

Yield reduction or rebate is only necessary if you cannot show that interest earned was below the bond’s arbitrage yield

Review of Arbitrage Rebate Rules (con’t.)

16

Maintain records for life of the bonds (including refunding bonds) plus three years

Records to be maintained include Bond Transcript Purchases and sales of investments made with bond proceeds and receipt of

earnings on those investments Records showing how bond proceeds were spent: purchase contracts,

construction contracts, invoices, and records of “allocations”

Identifying Arbitrage Rebate Rules

17

Private Use Tracking and Post Issuance Compliance Procedures Educate users of property Keep post-issuance policies in places that assure continuity Include responsibilities in job descriptions Ensure both periodic and timely reviews

Arbitrage and Rebate Spend bond proceeds first on capital improvements within three years Deplete debt service funds annually Reserve funds are subject to rebate (unless small issuer exception applies) Keep records of expenditures and investments for life of the bonds (longer

than issuer’s general record retention period)

Summary

Securities Law Nancy Neraas, Foster Pepper

Marc Greenough, Foster Pepper

19

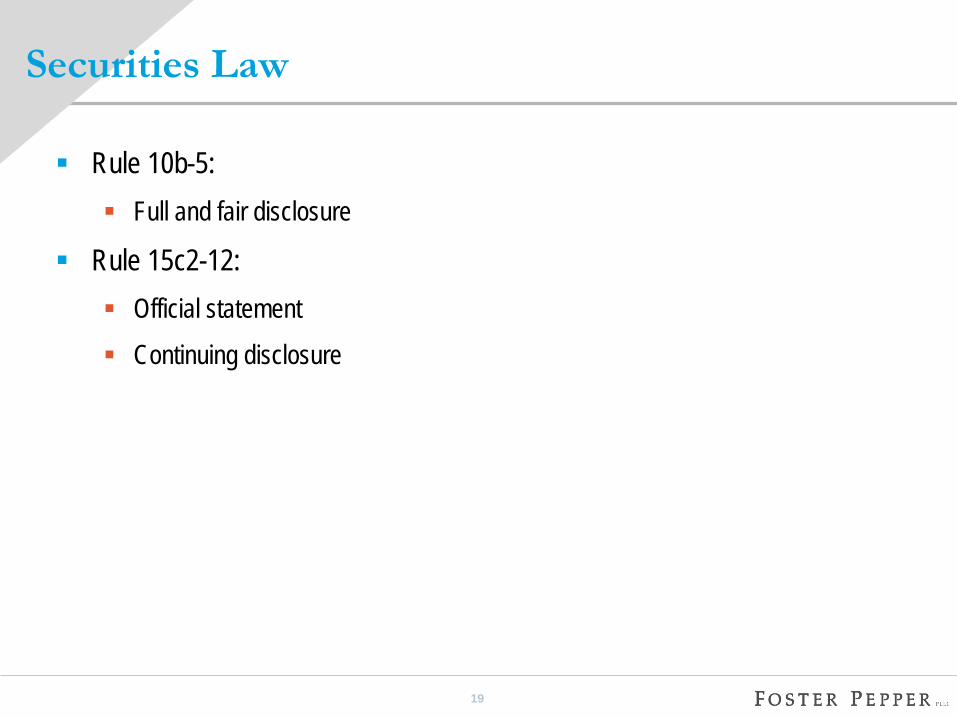

Rule 10b-5: Full and fair disclosure

Rule 15c2-12: Official statement Continuing disclosure

Securities Law

20

Unlawful, in connection with the purchase or sale of securities in interstate commerce, (a) to employ any device, scheme, or artifice to defraud, (b) to make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, or (c) to engage in any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person.

Rule 10b-5

21

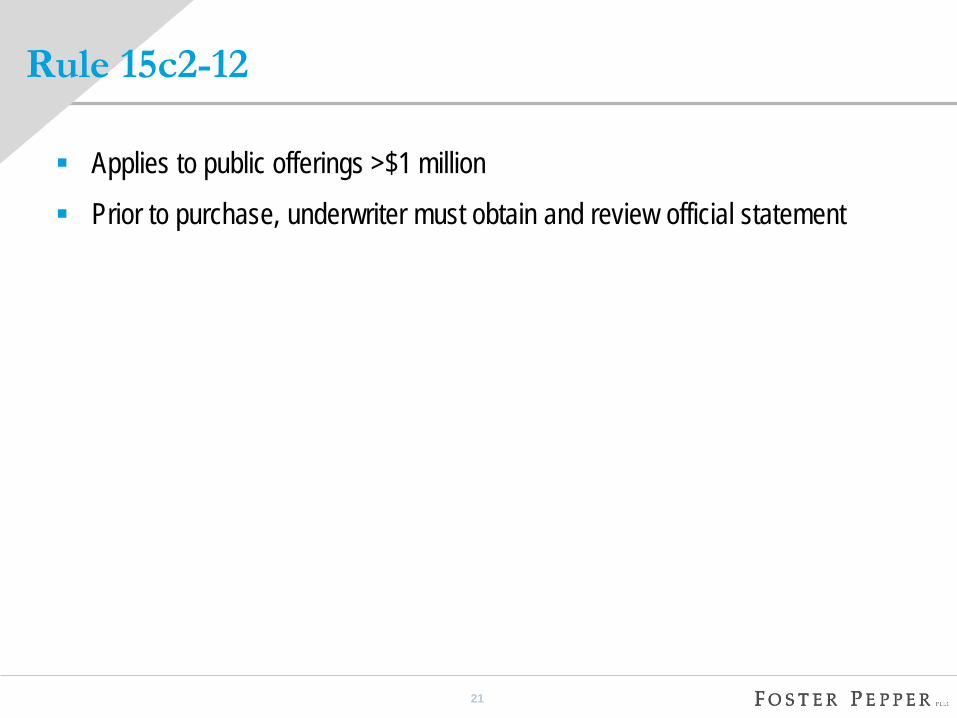

Applies to public offerings >$1 million

Prior to purchase, underwriter must obtain and review official statement

Rule 15c2-12

22

Applies to public offerings >$1 million

Underwriter must obtain undertaking to provide disclosure

Annual disclosure of financial information and operating data

Timely disclosure of listed events

Official statement must disclose past noncompliance with prior undertakings

Rule 15c2-12 (con’t.)

23

A document prepared by an issuer of municipal securities that sets forth information concerning the terms of the proposed issue of securities, including financial information or operating data concerning such issuer and those other entities, enterprises, funds, accounts, and other persons material to an evaluation of the securities.

Official Statement

24

Materiality: Objective standard

Substantial likelihood that, under all the circumstances, a fact would assume actual significance in the deliberations of a reasonable investor

Full and Fair Disclosure

25

Speaking to the market

Release of information that may reasonably be expected to reach investors

Full and Fair Disclosure (con’t.)

26

Continuing Disclosure: EMMA

27

Continuing Disclosure: MCDC

28

Increased initial and continuing disclosure

Protection of individual investors

Regulation of states as issuers

Enforcement in the absence of defaults

SEC Enforcement

29

New Jersey

Harrisburg

South Miami

West Clark

Allen Park

SEC Enforcement (con’t.)

30

No written policies for offering documents

Pension accounting not disclosed: One-time use of mark-to-market and subsequent use of five-year smoothing

From 2002 to 2007, UAAL grew to 100% of payroll

Case Study: New Jersey

31

Near bankrupt and under state receivership

No continuing disclosure: information vacuum

Statements in budget and financial reports

Case Study: Harrisburg

32

Tax-exempt bond-financed public/private parking

Subsequent revisions to lease violated tax law

No procedures to ensure continuing compliance

Case Study: South Miami

33

OS: In compliance with prior 15c2-12 undertakings

No diligence to uncover noncompliance

Underwriter also charged

Case Study: West Clark Community Schools

34

Mayor active proponent and “control person”

Project plans deteriorated prior to issuance

Outdated financial information in OS

Case Study: Allen Park

35

Policies designed to reduce chance of failing to comply with requirements and establish a defense of reasonable care

Policy can avoid “silo” effect where facts known by one department are not known by finance department

SEC has indicated if it investigates an issuer it will look more favorably is the issuer has a disclosure policy

Disclosure Policies

36

National Association of Bond Lawyers has provided guidance on policies Policies should be tailored to the size, complexity and other features of

particular issuers Policies should cover

1. Types of disclosures covered, 2. Process involved in disclosure and documenting compliance, 3. Adequate supervision and disbursement of responsibilities, and 4. Training.

Disclosure Policies (con’t.)

37

Draft policy is included in the materials. Tailor the policy to your situation and adopt something you expect to be able to comply with.

If you adopt a policy, you need to comply. Ignoring policy may document failure to exercise reasonable care.

Disclosure Policies (con’t.)

38

Pensions are the topic of the day in disclosure. Official statements have expanded pension disclosure.

GASB 68 liability will need to be disclosed, including share of unfunded liability and pension expense for the reporting period. Does not impact funded status or contribution rates, which also need to be disclosed.

GASB 68

39

Rules requiring registration of municipal advisor became effective in 2010; 2014 rules define “municipal advisor”

Underwriters only can provide advice to municipalities on municipal financial products in the following circumstances: In response to an RFP Of a general nature If an issuer has confirmed that it has retained and relies on an independent

registered municipal advisor

Municipal Advisor Rules

40

Underwriters may request confirmation that issuer has municipal advisor. Read communications from underwriters carefully You do not need to hire an underwriter before there is a bond issue Get a certification from your municipal advisor

Also impacts advice on investing funds that include bond proceeds

Municipal Advisor Rules (con’t.)

Post-Issuance Compliance for Municipal Bond Issuers:

Basic Training on Tax and Securities Responsibilities

October 22, 2015

Post – Issuance Compliancefor Municipal Bond Issuers

Basic Training on Tax and SecuritiesResponsibilities

Post – Issuance Compliancefor Municipal Bond Issuers

Basic Training on Tax and SecuritiesResponsibilities

McClearyof Washington Legislators

Constitutional

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

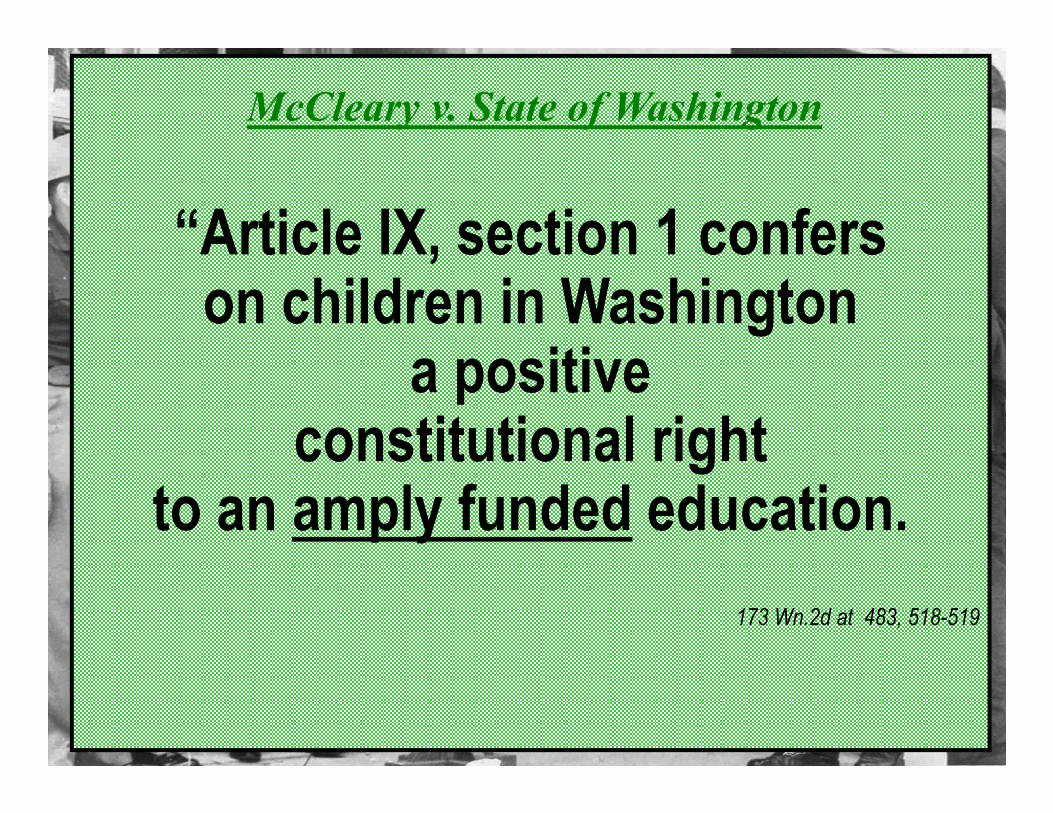

McCleary v. State of Washington (January 5, 2012)

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.”173 Wn.2d at 483, 518-519.

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

McCleary v. State of Washington (January 5, 2012)

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.”173 Wn.2d at 483, 518-519.

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“paramount duty” means

McCleary v. State, 173 Wn.2d at 520.

“the State must amply provide for the education of all Washington children

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“paramount duty” means

McCleary v. State, 173 Wn.2d at 520.

“the State must amply provide for the education of all Washington children

as the State’s first and highest priority

before any other State programs or operations.”

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“ample” means

McCleary v. State, 173 Wn.2d at 484.

“considerably more than just adequate.”

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“all” means

McCleary v. State, 173 Wn.2d at 520.

“each and every child” in Washington “No child is excluded.”

Washington State Constitution, Article IX, section 1

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.”McCleary v. State, 173 Wn.2d at 483, 518-519.

How much funding is ample?

• Yardstick to measure whether ample

• Dollars that result with that measure

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.”McCleary v. State, 173 Wn.2d at 483, 518-519.

How much funding is ample?

• Yardstick to measure whether ampleProvide each child residing in Washington a realistic andeffective opportunity to become equipped with the knowledgeand skills needed to compete in today’s economy andmeaningfully participate in our State’s democracy– includes (but are not limited to) our State’sEssential Academic Learning Requirements (EALRs).

February 2010 Final Judgment, ¶¶212 & 231(a).

Other Dollars(local bonds,

federal programs, donations, fees)

State Dollars

Local Levy Dollars

SCHOOL FUNDING TESTIMONYNot sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Not sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Other Dollars(local bonds,

federal programs, donations, fees)

State Dollars

SCHOOL FUNDING TESTIMONY

Local Levy Dollars

Local Levy Dollars

Not sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Local Levy Dollars

Other Dollars(local bonds,

federal programs, donations, fees)

State Dollars

SCHOOL FUNDING TESTIMONY

State Dollars

Not sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Local Levy Dollars

Other Dollars(local bonds,

federal programs, donations, fees)

State Dollars

SCHOOL FUNDING TESTIMONY

State Dollars

Not sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Local Levy Dollars

Other Dollars(local bonds,

federal programs, donations, fees)

State Dollars

SCHOOL FUNDING TESTIMONY

State Dollars

Other Dollars(local bonds,

federal programs, donations, fees)

SCHOOL FUNDING TESTIMONYNot sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

Local Levy Dollars

State Dollars

Other Dollars(local bonds,

federal programs, donations, fees)

SCHOOL FUNDING TESTIMONY

Local Levy Dollars

State Dollars

Not sufficient to provideevery child a realistic &effective opportunity tolearn the knowledge &skills needed to competein today’s economy andmeaningfully participate inour State’s democracy(including State’s EALRs).

IT IS THE

PARAMOUNT DUTY OF THE

STATE TO MAKE

AMPLE PROVISION FOR THE

EDUCATION OF

ALL CHILDREN RESIDING

WITHIN ITS BORDERS....

Washington State Constitution, Article IX, section 1

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.”McCleary v. State, 173 Wn.2d at 483, 518-519.

How much funding is ample?

• Yardstick to measure whether ample

• Dollars that result with that measure

Ample funding under State’s testimony

Ample funding under State’s testimony

What steady progress would thus require....

Ample funding under State’s testimony

December 2012 enforcement Order:

submit your compliance plan

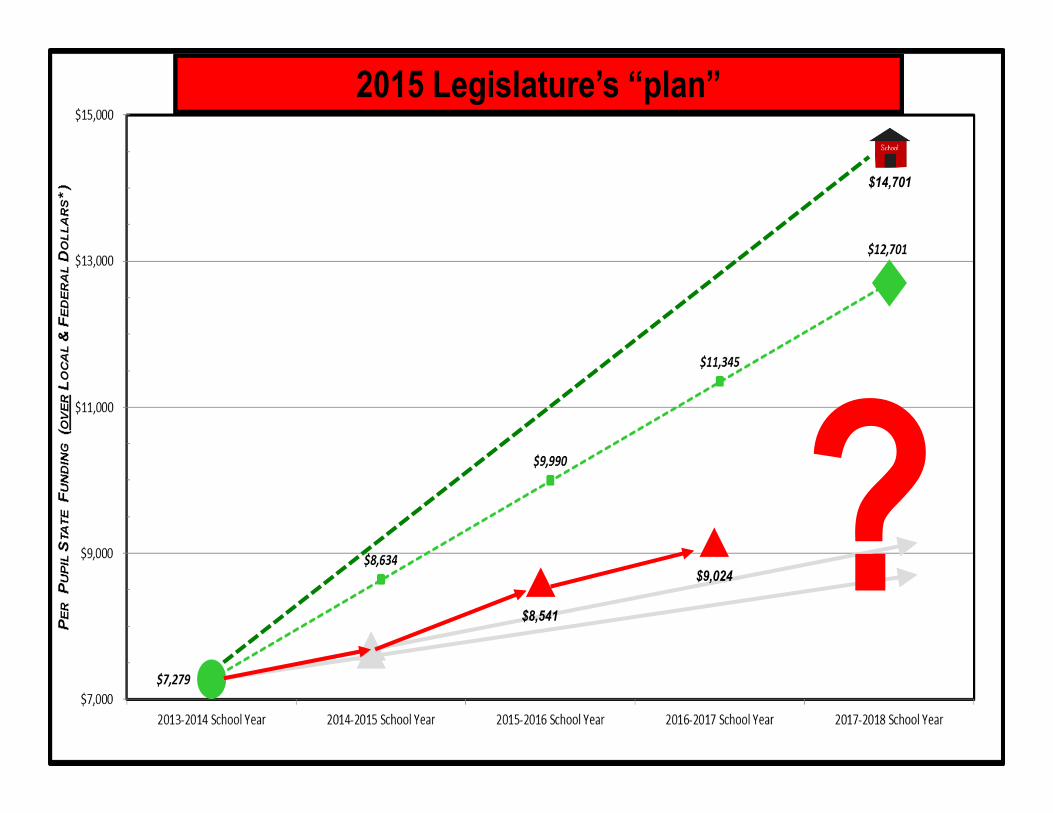

▲$7,646

Ample funding under State’s testimony2013 Legislature’s “plan”

▲$7,646

December 2012 enforcement Order:

submit your compliance plan

Ample funding under State’s testimony2013 Legislature’s “plan”

January 5, 2014 enforcement Order: We really mean it -

submit your compliance plan !!!

▲▲$7,704

2013 Legislature’s “plan”2014 Legislature’s “plan”

▲▲$7,704

2013 Legislature’s “plan”2014 Legislature’s “plan”

▲▲

2013 Legislature’s “plan”2014 Legislature’s “plan”2015 Legislature’s “plan”

$14,701

2013 Legislature’s “plan”2014 Legislature’s “plan”2015 Legislature’s “plan”

$14,701

▲▲▲$8,541

▲$9,024

2013 Legislature’s “plan”2014 Legislature’s “plan”2015 Legislature’s “plan”

$14,701

▲▲▲$8,541

▲$9,024

2013 Legislature’s “plan”2014 Legislature’s “plan”2015 Legislature’s “plan”

$14,701

▲▲▲$8,541

▲$9,024

UNCHARTED WATERS

2013 Legislature’s “plan”2014 Legislature’s “plan”2015 Legislature’s “plan”

$14,701

▲▲▲$8,541

▲$9,024

UNCHARTED WATERS

Brown v. Board of Education

The 14th Amendment confers on children in the United States

a positive constitutional right

to a non-segregated education.347 U.S. 483

McCleary v. State of Washington

“Article IX, section 1 confers on children in Washington

a positive constitutional right

to an amply funded education.173 Wn.2d at 483, 518-519

McCleary v. State of Washington“Education ... plays a critical civil rights role inpromoting equality in our democracy.”

“For example, amply provided, free publiceducation operates as the great equalizer in ourdemocracy, equipping citizens born intounderprivileged segments of our society with thetools they need to compete on a level playing fieldwith citizens born into wealth or privilege.”

“Education ... is the number one civil right of the 21st century.” McCleary Final Judgment (Feb. 2010) at ¶¶132 & 134.

the Court has “usurped the powers of the State Legislature”

prompt compliance with Supreme Court ruling “is not feasible”

“We cannot levy taxes to pay for what the Supreme Court ruling requires”

we will not approve budget that complies with Supreme Court ruling

conduct a study before positive steps are taken to comply with Court ruling

PREDICT DELAYSNo Quick End In Sight

the Court has “usurped the powers of the State Legislature”

prompt compliance with Supreme Court ruling “is not feasible”

“We cannot levy taxes to pay for what the Supreme Court ruling requires”

we will not approve budget that complies with Supreme Court ruling

conduct a study before positive steps are taken to comply with Court ruling

PREDICT DELAYSNo Quick End In Sight

State Attorney General arguesthe Court has “usurped the powers of the State Legislature”Brown v. Bd. of Education report in The Augusta (Georgia) Chronicle [June 1, 1955]

Legislators sayprompt compliance with Supreme Court ruling “is not feasible”Brown v. Bd. of Education reaction in New Orleans (Louisiana) Times-Picayune [June 1, 1955]

State officials say “We cannot levy taxes to pay for what the Supreme Court ruling requires”

Brown v. Bd. of Education response reported in Atlanta (Georgia) Constitution [June 1, 1955]

Elected officials saywe will not approve budget that complies with Supreme Court ruling

Brown v. Bd. of Education report in Aiken (South Carolina) Standard & Review [June 1, 1955]

Legislature says it needs to conduct a study before positive steps are taken to comply with Court ruling

Brown v. Bd. of Education report in Aiken (South Carolina) Standard & Review [June 1, 1955]

PREDICT DELAYSBrown v. Bd. of Education headline in Danville (Virginia) Bee [June 1, 1955]

No Quick End In SightBrown v. Bd. of Education headline in Biloxi (Mississippi) Daily Herald [May 31, 1955]

6/12/2014 Supreme Court Order at page 4

1. Impose monetary or other contempt sanctions;

2. Prohibit expenditures on certain other matters until the Court’s constitutional ruling is complied with;

3. Order the legislature to pass legislation to fund specific amounts or remedies;

4. Order the sale of State property to fund constitutional compliance;

5. Invalidate education funding cuts in the budget;

6. Prohibit any funding of an unconstitutional education system;

7. Order any other appropriate relief

6/12/2014 Supreme Court Order at page 4

1. Impose monetary or other contempt sanctions;

2. Prohibit expenditures on certain other matters until the Court’s constitutional ruling is complied with;

3. Order the legislature to pass legislation to fund specific amounts or remedies;

4. Order the sale of State property to fund constitutional compliance;

5. Invalidate education funding cuts in the budget;

6. Prohibit any funding of an unconstitutional education system;

7. Order any other appropriate reliefInvalidate Tax Exemption Statutes?

Transportation package?

K-3 classroom construction?

Prior COLA suspensions?

Strike down every underfunded school statute?

Invalidate new bills on OTHER matters?

Legislators’ 11% pay raise?

Invalidate budget sections above the shut-down prep. “essential services”?

Trial Court’s February 2010 final judgment against the State:http://waschoolexcellence.org/the-mccleary-case/the-trial/

Daily summaries of the trial:http://waschoolexcellence.org/the-mccleary-case/the-trial/daily-trial-reports/

Supreme Court Briefs, etc.:http://waschoolexcellence.org/the-mccleary-case/court-documents/

Supreme Court’s 2012, 2013, 2014, & 2015 Rulings:http://waschoolexcellence.org/the-mccleary-case/the-supreme-court/

McCleary v. State background information

DISCLOSURE POLICY

As an issuer of municipal securities, the ______ is subject to the antifraud provisions of the Securities Act of 1933 and the Securities and Exchange Act of 1934 and the Securities Act of Washington (chapter 21.70 RCW). These acts impose various obligations on the [Issuer], including requiring disclosure of material information regarding its publicly-offered bonds to allow investors to make informed decisions. All documents and statements prepared or made in connection with the purchase or sale of the [Issuer’s] securities cannot contain any untrue statement of a material fact or omit to state a material fact necessary in order to make the statements not misleading.

This policy is designed to assist the [Issuer] in its compliance with securities laws and to promote best practices regarding disclosure.

The [Issuer] has three major disclosure obligations: (1) to prepare an official statement for all public offerings of its securities that is delivered to the underwriter(s) for distribution to potential and actual purchasers and that sets forth the terms of the securities and information regarding the [Issuer], (2) to provide ongoing disclosure in compliance with paragraph (b)(5) of Securities and Exchange Commission Rule 15c2-12 (“Rule 15c2-12”), and (3) if and when the Issuer provides information that can reasonably be expected to be relied on by the market, to ensure that the information is not inaccurate or misleading.

1. Official Statements and Other Disclosure Documents

The [Issuer] prepares an official statement for each publicly offered security offering. The [Finance Director] and the [Issuer’s bond counsel/disclosure counsel/financial advisor] are responsible for preparing the official statement. If the [Issuer] requests a rating, a rating presentation is prepared. [In addition, an investor presentation for larger bond issues may be prepared.]

A. Procedure and Timeline for Preparing Official Statements

In advance of each financing, the [Finance Director] determines the financing team, including [titles of certain Issuer officials if applicable], financial advisor(s), bond counsel and underwriters (for negotiated offerings only). [Currently, the Issuer’s bond counsel/underwriter/financial advisor compiles official statements.] The [Finance Director] and [preparer] are responsible for providing drafts of the official statement or sections of the official statement, as appropriate, drafts of the rating presentation and investor presentation, if applicable, to the financing team and other [Issuer] officials in a timely manner to provide adequate time for such individuals to perform a thorough review. The financial advisor or underwriter prepares a schedule for each financing, including dates for distributing drafts of the official statement and financing team calls and meetings to discuss the official statement.

51475354.1

[Alter/expand as applicable: The [Finance Director] shall provide certain sections of the disclosure documents to individuals with subject matter knowledge of that section for their review and comments.

The _______[senior official] shall review the disclosure documents to provide a broader perspective.

The _______ [governing body] shall be given a copy of the official statement in advance of its publication and be given the opportunity to comment and ask questions.]

B. Training

The [Issuer] shall provide periodic training opportunities to finance staff who participate in the [Issuer’s] debt offerings regarding disclosure obligations and best practices. Such training sessions shall include education on the [Issuer’s] disclosure obligations under applicable securities laws and responsibilities and potential liabilities regarding such obligations.

C. Document Retention

The [Finance Director] shall retain for a period of at least five years printed copies of each preliminary and final official statement and any written certifications or opinions relating to disclosure matters. The [Finance Director] is not required to retain drafts of any disclosure materials. [Consider adding language regarding documenting compliance: In connection with each bond issue, the [Finance Director] shall document the persons involved in the review and the areas reviewed.]

D. Certifications and Opinions

In connection with the closing of bonds, the transcript will include a disclosure counsel opinion, if applicable, [Issuer] attorney’s certificate or opinion regarding litigation, and a certificate of the [Issuer] regarding the official statement. [In addition, other Issuer officials that are responsible for major sections of the official statement will be asked to certify that they have reviewed the section and there are no misstatements or material omissions in the section.]

2. Ongoing Disclosure

Each time the [Issuer] issues publicly-offered securities it enters into a written undertaking to provide continuing disclosure for the benefit of the holders and beneficial owners of the securities as required by Rule 15c2-12. The undertakings require the [Issuer] not later than nine months after the end of each fiscal year, to provide to the Municipal Securities Rulemaking Board an annual report consisting of the [Issuer’s] audited financial statements and specified historical financial and operating data. In each undertaking, the [Issuer] also agrees to provide or cause to be provided, in a timely manner, not in excess of 10 business days after the occurrence of the event, to the MSRB notice of the occurrence of the “Listed Events,” as defined in the undertaking.

2 51475354.1

The _______________ is responsible for complying with each undertaking, including to file the annual reports within the specified time and to provide timely notice of any Listed Event. In addition, _________ is registered with EMMA and familiar with the filing requirements and procedures. [The duty to comply with the undertaking is included in the __________’s job description.] The __________ shall keep a record of each undertaking and a copy of each filing pursuant to the undertakings. Any failure to comply with an undertaking shall be disclosed in future [Issuer] official statements for five years. [The Issuer has signed up with EMMA for email reminders.]

3. Speaking to the Market

The SEC has stated that when a municipal issuer of outstanding securities provides “information to the public that is reasonably expected to reach investors and the trading market, those disclosures are subject to the antifraud provisions”; the information cannot be misleading or contain incorrect information. In order to violate the antifraud rules, the misrepresentation must be made publicly, must be material, must involve a security traded on an efficient market and must be such as would induce a reasonable, relying investor to misjudge the value of the security. Examples of information that could be relied on by investors in the [Issuer’s] outstanding securities include ongoing disclosure filings, audited financial statements, investor presentations, and financial information posted on the Issuer’s website.

[4. Website

The Issuer maintains an “Investor Information” section on its website. As part of that site, official statements and _____from recent bond sales are maintained. _____ shall be responsible for maintaining that site and adding appropriate disclaimers, removing information when appropriate and assessing the consistency of such information with other information intended to reach investors. ]

Approved this __________.

_________________________

__________________________

[add title]

3 51475354.1