positioning of mozambique in the international trade · 2019-11-07 · positioning of mozambique in...

TRANSCRIPT

2016 Edition

REPUBLIC OF MOZAMBIQUEMINISTRY OF INDUSTRY AND COMMERCE

POSITIONING OF MOZAMBIQUE IN THE INTERNATIONAL TRADE

Trade Flows in Mozambique: Trends and Policy Measures

REPUBLIC OF MOZAMBIQUE

MINISTRY OF INDUSTRY AND COMMERCE

2016 Edition

POSITIONING OF MOZAMBIQUE IN THE INTERNATIONAL TRADE

Trade Flows in Mozambique: Trends and Policy Measures

Positioning of Mozambique in the International Trade 2016 iii

Foreword

This report seeks to analyse the position of Mozambique in the international trade in the period of 2010-2015 vis-à-vis relations with principal trade partners. This analysis essentially systematizes the information signalling the status of various socio-economic factors which are infl uencing the performance of economy.

Mozambique’s trade fl ows, especially the value and volume of imports and exports, are important data to un-derstand the situation of Mozambique in the international trade, and to take corrective measures to the coun-try’s less favourable position, as well as to extract the maximum benefi ts granted by the facilities resulting from the implementation of the various trade agreements of which the country is a signatory.

With the modifi cation of the structure of traditional export products (as fi sheries and primary agriculture products reduced its proportion in the exports structure), the country should explore new opportunities in the international trade, increasing the value of primary products, and the opportunities which are emerging in competitive markets for minerals and hydrocarbons.

There is a need to explore all the avenues offered by the greater openness of international trade, the global population increase, as well as the dynamics in the indicators of the ease of doing business, par ticularly in the regional markets, in the context of the profi le of the least developed countries that Mozambique is part of.

The challenge is to orient the government to defi ne trade policies, to benefi t more from trade opportunities in regional and international markets with the aim of improving the balance of payment, and creating new jobs and using trade as a tool for reducing poverty.

We would like to express our appreciation to the United Nations Development Programme (UNDP), for its assistance to the Ministry of Industry and Commerce (MIC) in the elaboration of this report. This support was provided through capacity building for statistical data collection and analysis related to international trade.

We look forward to continuing to engage with UNDP in the future on trade related matters that will enable us to make informed decisions that help the country to use trade as an additional tool in economic growth and development.

Maputo, 12th December 2016

Minister of Industry and Commerce

Ernesto Max Tonela

TECHNICAL NOTE

TITLE:

Positioning of Mozambique in the International Trade

REVIEW:

Sabado Matsolo, Cláudia Langa, José Leonardo, Agonias Macia, Calado Silva, Samuel Zita, Masaki Mifune and John Barns.

PRODUCTION:

Ministério da Indústria e Comércio (MIC)

Direcção de Planifi cação e Estudos – Cláudia Correia Langa e José LeonardoDirecção Nacional Comércio Interno – Isabel SimangoEnhanced Integrated Framework (EIF) – Herlander Namuiche, Samuel ZitaUnited Nations Development Programme (UNDP) – Masaki Mifune

LAYOUT:

Elografi co

EDITION:

1st Edition 2016

PRINTING

500 copies

PUBLISHED BY:

REPUBLIC OF MOZAMBIQUE

MINISTRY OF INDUSTRY AND COMMERCE

Praca 25 de Junho, n° 300Tel: +258 21 320401www.mic.gov.mz

WITH SUPPORT FROM:

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP)

Av. Kenneth Kaunda 921/931, P.O Box 4595www.undp.org

Positioning of Mozambique in the International Trade 2016 iii

Foreword

This report seeks to analyse the position of Mozambique in the international trade in the period of 2010-2015 vis-à-vis relations with principal trade partners. This analysis essentially systematizes the information signalling the status of various socio-economic factors which are infl uencing the performance of economy.

Mozambique’s trade fl ows, especially the value and volume of imports and exports, are important data to un-derstand the situation of Mozambique in the international trade, and to take corrective measures to the coun-try’s less favourable position, as well as to extract the maximum benefi ts granted by the facilities resulting from the implementation of the various trade agreements of which the country is a signatory.

With the modifi cation of the structure of traditional export products (as fi sheries and primary agriculture products reduced its proportion in the exports structure), the country should explore new opportunities in the international trade, increasing the value of primary products, and the opportunities which are emerging in competitive markets for minerals and hydrocarbons.

There is a need to explore all the avenues offered by the greater openness of international trade, the global population increase, as well as the dynamics in the indicators of the ease of doing business, par ticularly in the regional markets, in the context of the profi le of the least developed countries that Mozambique is part of.

The challenge is to orient the government to defi ne trade policies, to benefi t more from trade opportunities in regional and international markets with the aim of improving the balance of payment, and creating new jobs and using trade as a tool for reducing poverty.

We would like to express our appreciation to the United Nations Development Programme (UNDP), for its assistance to the Ministry of Industry and Commerce (MIC) in the elaboration of this report. This support was provided through capacity building for statistical data collection and analysis related to international trade.

We look forward to continuing to engage with UNDP in the future on trade related matters that will enable us to make informed decisions that help the country to use trade as an additional tool in economic growth and development.

Maputo, 12th December 2016

Minister of Industry and Commerce

Ernesto Max Tonela

TECHNICAL NOTE

TITLE:

Positioning of Mozambique in the International Trade

REVIEW:

Sabado Matsolo, Cláudia Langa, José Leonardo, Agonias Macia, Calado Silva, Samuel Zita, Masaki Mifune and John Barns.

PRODUCTION:

Ministério da Indústria e Comércio (MIC)

Direcção de Planifi cação e Estudos – Cláudia Correia Langa e José LeonardoDirecção Nacional Comércio Interno – Isabel SimangoEnhanced Integrated Framework (EIF) – Herlander Namuiche, Samuel ZitaUnited Nations Development Programme (UNDP) – Masaki Mifune

LAYOUT:

Elografi co

EDITION:

1st Edition 2016

PRINTING

500 copies

PUBLISHED BY:

REPUBLIC OF MOZAMBIQUE

MINISTRY OF INDUSTRY AND COMMERCE

Praca 25 de Junho, n° 300Tel: +258 21 320401www.mic.gov.mz

WITH SUPPORT FROM:

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP)

Av. Kenneth Kaunda 921/931, P.O Box 4595www.undp.org

Positioning of Mozambique in the International Trade 2016 v

Contents

Abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

Executive Summary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

Chapter I. Overview of Trade Trends in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.1 The Landscape of Trade in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Trade Partners in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Chapter II. Trend Analysis of Trade Products in Mozambique . . . . . . . . . . . . . . . . . . . . . . 5

2.1 Trade Products Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2 Main Cash Crops and Foods Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.3 Main Food Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Chapter III. Global & Regional Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.1 Demographic Trends and Food Security . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.2 Demographic Trends and Socio-Economic Structure. . . . . . . . . . . . . . . . . . . . . . . 29

3.3 Energy Demand and Industrialization. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3.4 SDGs and Trade. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Chapter IV. Policy and Institutional Framework for Trade in Mozambique . . . . . . . . . . . . . . . . 40

4.1 Policy and Institutional Framework in the Trade Sector . . . . . . . . . . . . . . . . . . . . . . 40

4.2 International Trade Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.3 Business Environment in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Reference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Figures

Figure 1.1: Degree of trade openness 2000-2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Figure 1.2: Current account, trade and FDI fl ow in Mozambique 2010-2014 . . . . . . . . . . . . . . 2

Figure 1.3: Principal trade products exported from Mozambique 2000 and 2015. . . . . . . . . . . . 3

Figure 1.4: Commodity price trend (Index, 2005=100). . . . . . . . . . . . . . . . . . . . . . . . . . 3

Figure 2.1: Megaproject/extractive industry export value 2000-2015 (selected prducts) . . . . . . . . 6

Figure 2.2: Cash crops and foods exports value 2000-2015 (selected products) . . . . . . . . . . . 6

Figure 2.3: Exports destinations by product (2011-2015 avg.). . . . . . . . . . . . . . . . . . . . . . 7

Figure 2.4 Mozambique cashew nuts exports and global trends . . . . . . . . . . . . . . . . . . . . 8

Figure 2.5: Mozambique cashew nuts export destinations. . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 2.6: Mozambique sesame exports and global trends . . . . . . . . . . . . . . . . . . . . . . 10

Figure 2.7: Mozambique sesame export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 2.8: Mozambique almonds exports and global trends . . . . . . . . . . . . . . . . . . . . . . 12

Figure 2.9: Mozambique almonds export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 2.10: Mozambique cotton exports and global trends . . . . . . . . . . . . . . . . . . . . . . . 14

Figure 2.11: Mozambique cotton export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Positioning of Mozambique in the International Trade 2016 v

Contents

Abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

Executive Summary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

Chapter I. Overview of Trade Trends in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.1 The Landscape of Trade in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Trade Partners in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Chapter II. Trend Analysis of Trade Products in Mozambique . . . . . . . . . . . . . . . . . . . . . . 5

2.1 Trade Products Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2 Main Cash Crops and Foods Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.3 Main Food Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Chapter III. Global & Regional Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.1 Demographic Trends and Food Security . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.2 Demographic Trends and Socio-Economic Structure. . . . . . . . . . . . . . . . . . . . . . . 29

3.3 Energy Demand and Industrialization. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3.4 SDGs and Trade. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Chapter IV. Policy and Institutional Framework for Trade in Mozambique . . . . . . . . . . . . . . . . 40

4.1 Policy and Institutional Framework in the Trade Sector . . . . . . . . . . . . . . . . . . . . . . 40

4.2 International Trade Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.3 Business Environment in Mozambique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Reference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Figures

Figure 1.1: Degree of trade openness 2000-2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Figure 1.2: Current account, trade and FDI fl ow in Mozambique 2010-2014 . . . . . . . . . . . . . . 2

Figure 1.3: Principal trade products exported from Mozambique 2000 and 2015. . . . . . . . . . . . 3

Figure 1.4: Commodity price trend (Index, 2005=100). . . . . . . . . . . . . . . . . . . . . . . . . . 3

Figure 2.1: Megaproject/extractive industry export value 2000-2015 (selected prducts) . . . . . . . . 6

Figure 2.2: Cash crops and foods exports value 2000-2015 (selected products) . . . . . . . . . . . 6

Figure 2.3: Exports destinations by product (2011-2015 avg.). . . . . . . . . . . . . . . . . . . . . . 7

Figure 2.4 Mozambique cashew nuts exports and global trends . . . . . . . . . . . . . . . . . . . . 8

Figure 2.5: Mozambique cashew nuts export destinations. . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 2.6: Mozambique sesame exports and global trends . . . . . . . . . . . . . . . . . . . . . . 10

Figure 2.7: Mozambique sesame export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 2.8: Mozambique almonds exports and global trends . . . . . . . . . . . . . . . . . . . . . . 12

Figure 2.9: Mozambique almonds export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 2.10: Mozambique cotton exports and global trends . . . . . . . . . . . . . . . . . . . . . . . 14

Figure 2.11: Mozambique cotton export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Positioning of Mozambique in the International Trade 2016 vii

Tables

Table 1.1: Mozambique’s major trading partners (2011-2015 avg.) . . . . . . . . . . . . . . . . . . . 4

Table 2.1: Main export and import products in Mozambique . . . . . . . . . . . . . . . . . . . . . . 5

Table 2.2: Cashew nuts export world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Table 2.3: Sesame exports word ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Table 2.4: Almonds export world ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table 2.5: Cotton exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

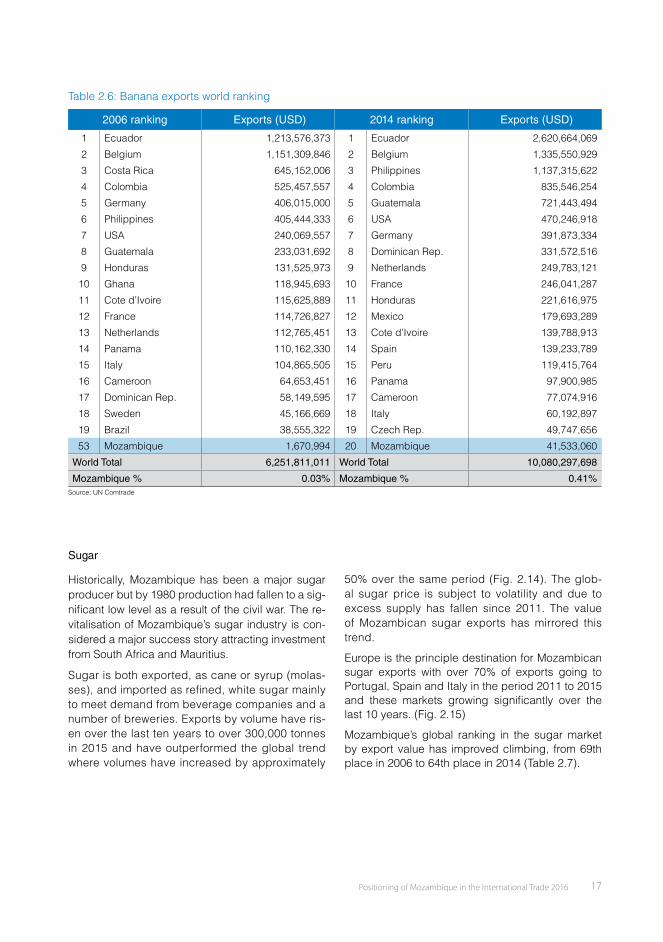

Table 2.6: Banana exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

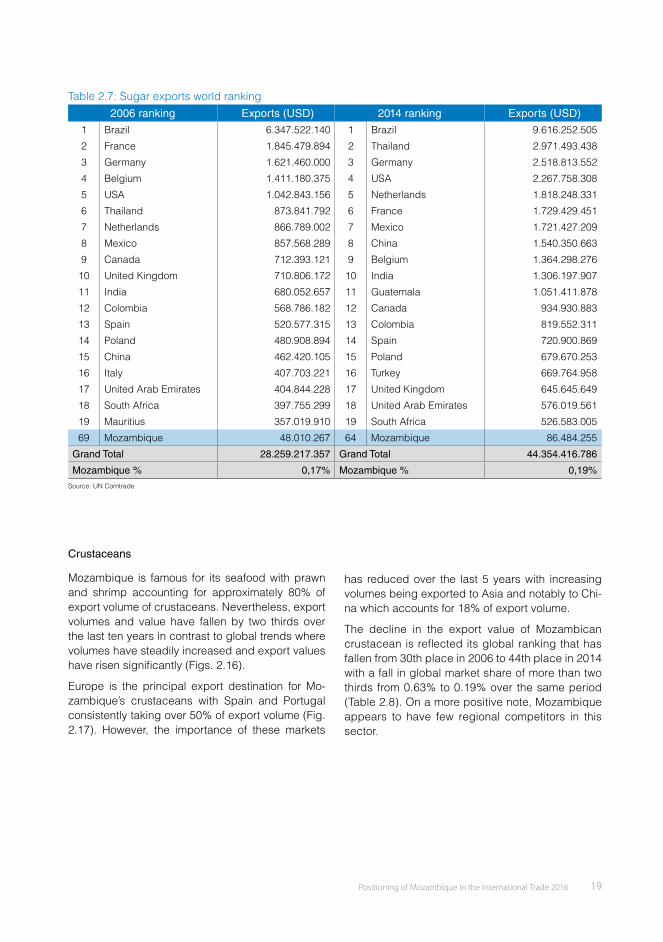

Table 2.7: Sugar exports world ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

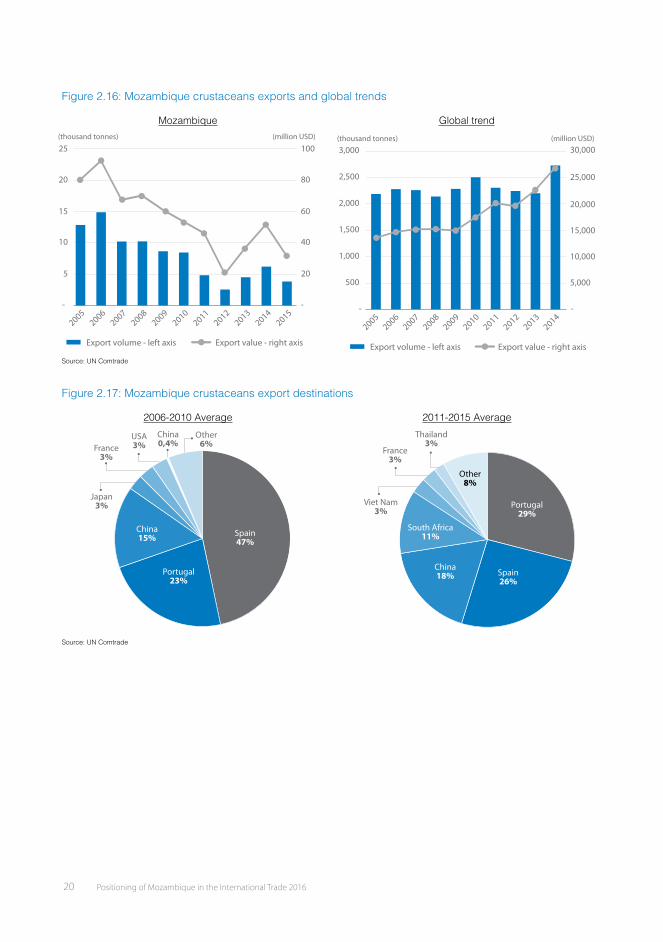

Table 2.8: Crustaceans exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

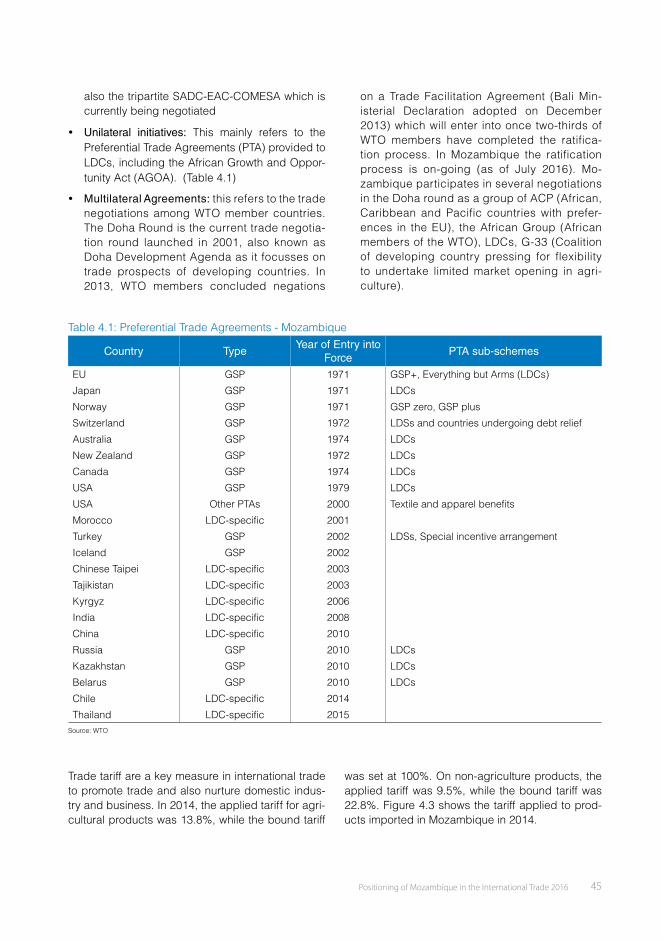

Table 4.1: Preferential Trade Agreements - Mozambique . . . . . . . . . . . . . . . . . . . . . . . . 45

Table 4.2: Bilateral investment agreements – Mozambique . . . . . . . . . . . . . . . . . . . . . . . 46

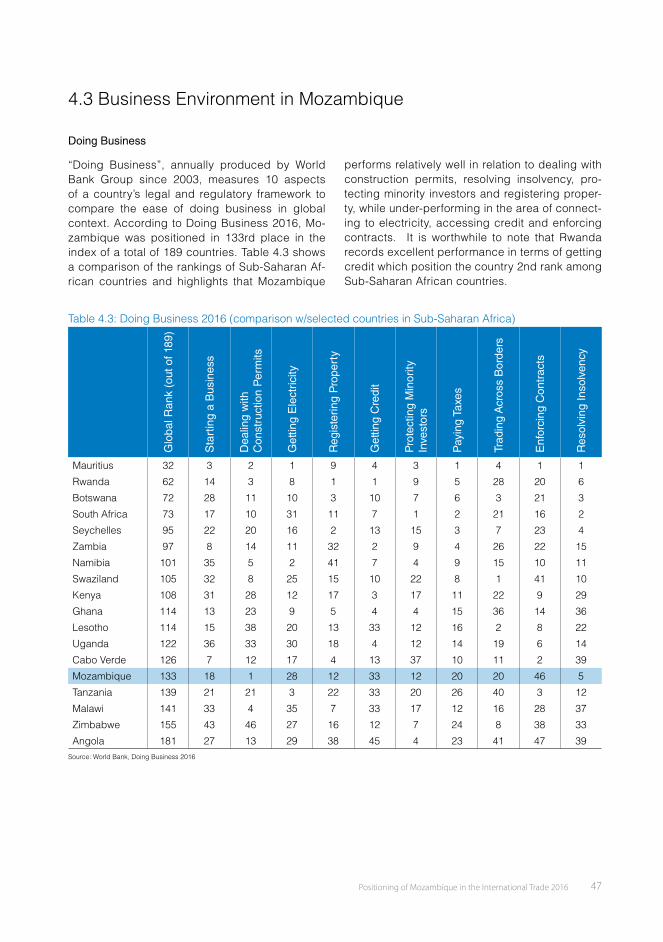

Table 4.3: Doing Business 2016 (comparison w/selected countries in Sub-Saharan Africa) . . . . . . 47

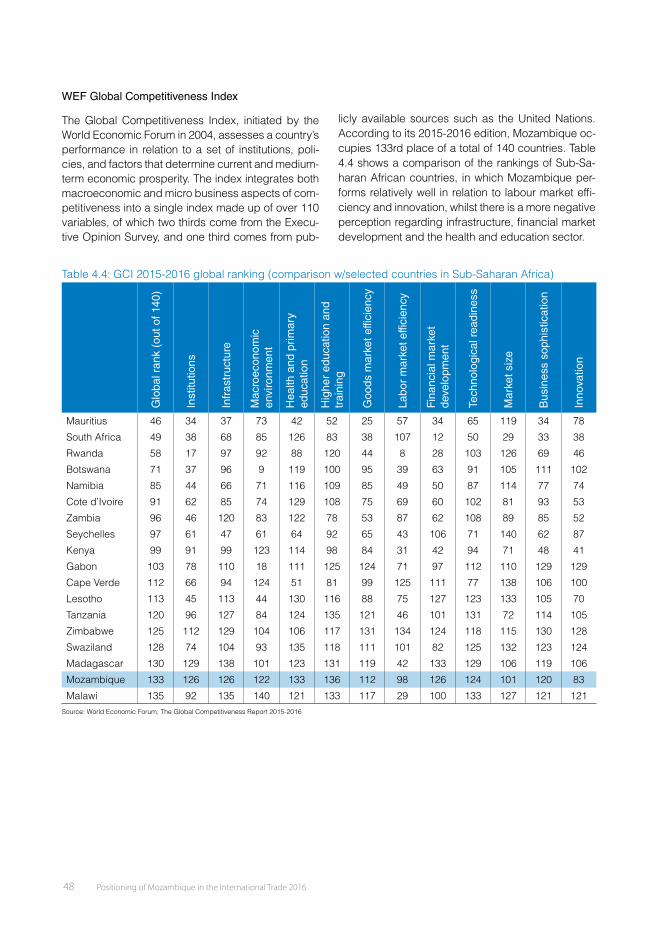

Table 4.4: GCI 2015-2016 global ranking (comparison w/selected countries in Sub-Saharan Africa). . 48

Table 4.5: LPI 2016 Sub-Saharan Africa ranking (comparison w/selected countries) . . . . . . . . . . 49

Boxes

Box 1.1: Volatile commodity prices destabilize the economy . . . . . . . . . . . . . . . . . . . . . . 3

Box 2.1: Food security and trade. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

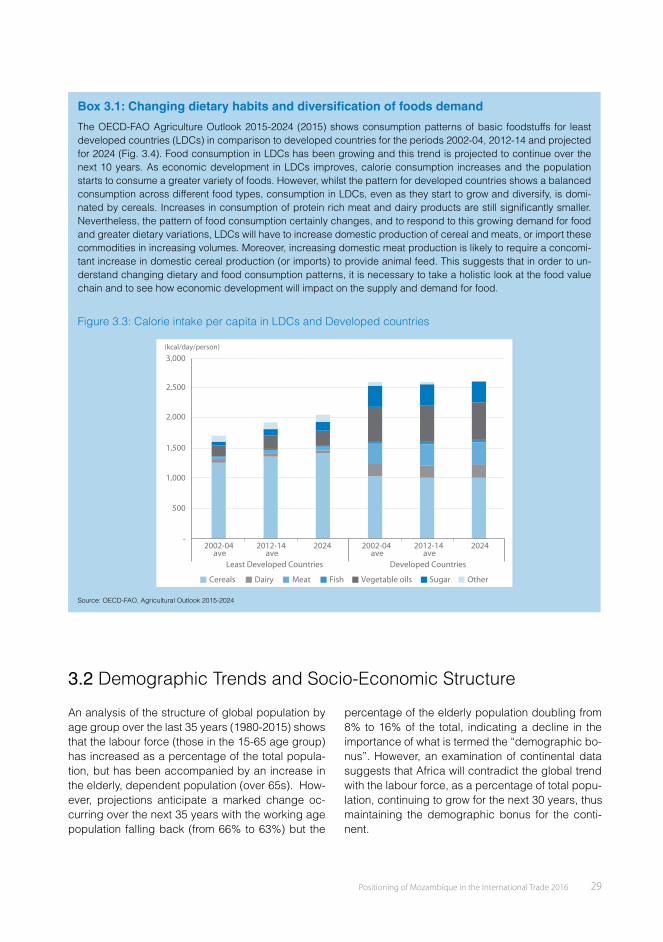

Box 3.1: Changing dietary habits and diversifi cation of foods demand . . . . . . . . . . . . . . . . . 29

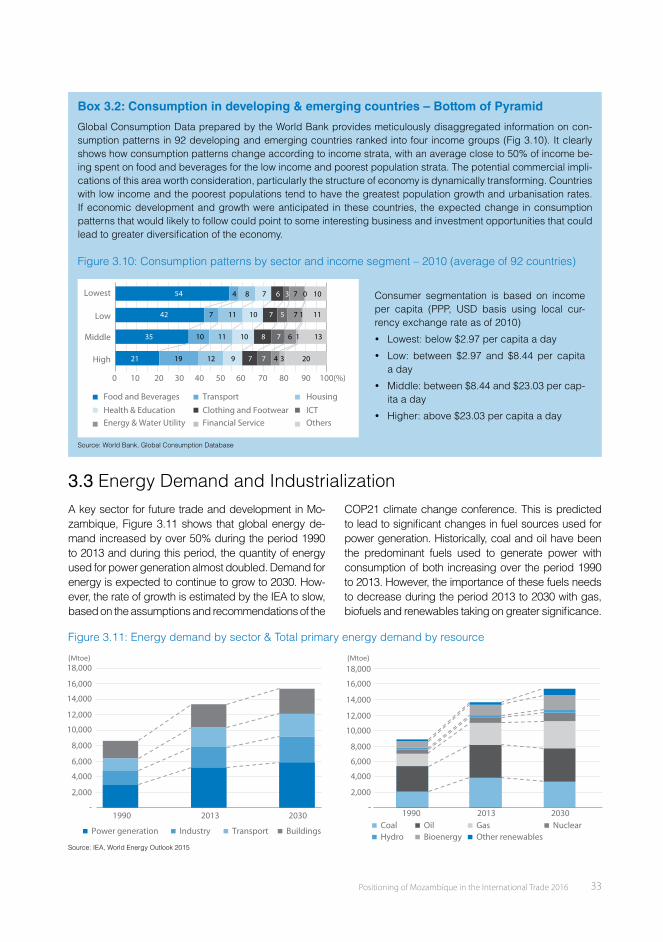

Box 3.2: Consumption in developing & emerging countries – Bottom of Pyramid . . . . . . . . . . . . 33

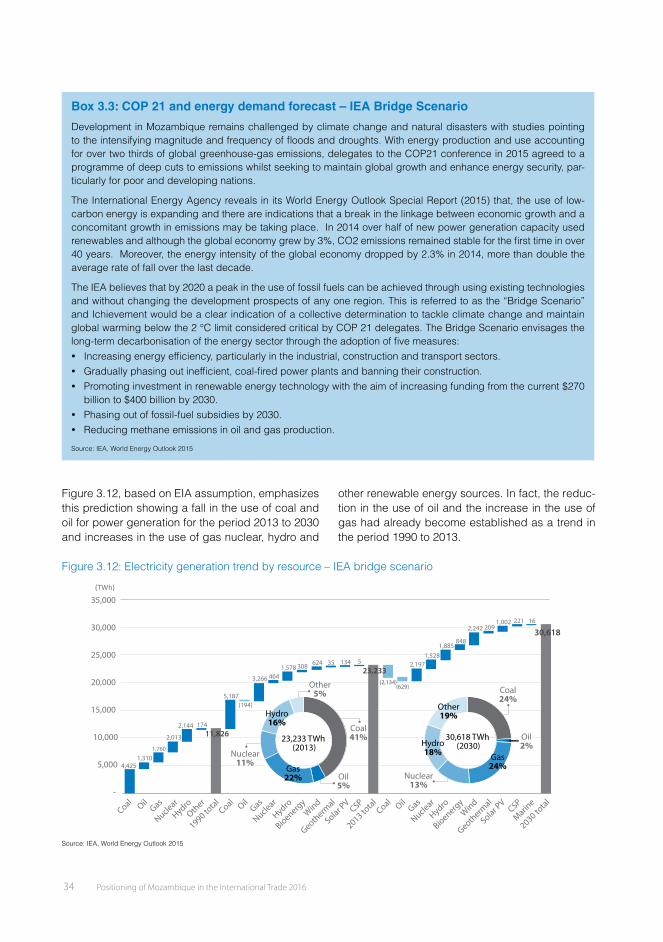

Box 3.3: COP 21 and energy demand forecast – IEA Bridge Scenario . . . . . . . . . . . . . . . . . 34

Box 3.4: Global Value Chains (GVCs) – opportunities and risks . . . . . . . . . . . . . . . . . . . . . 36

Box 3.5: Trade and Development Agenda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

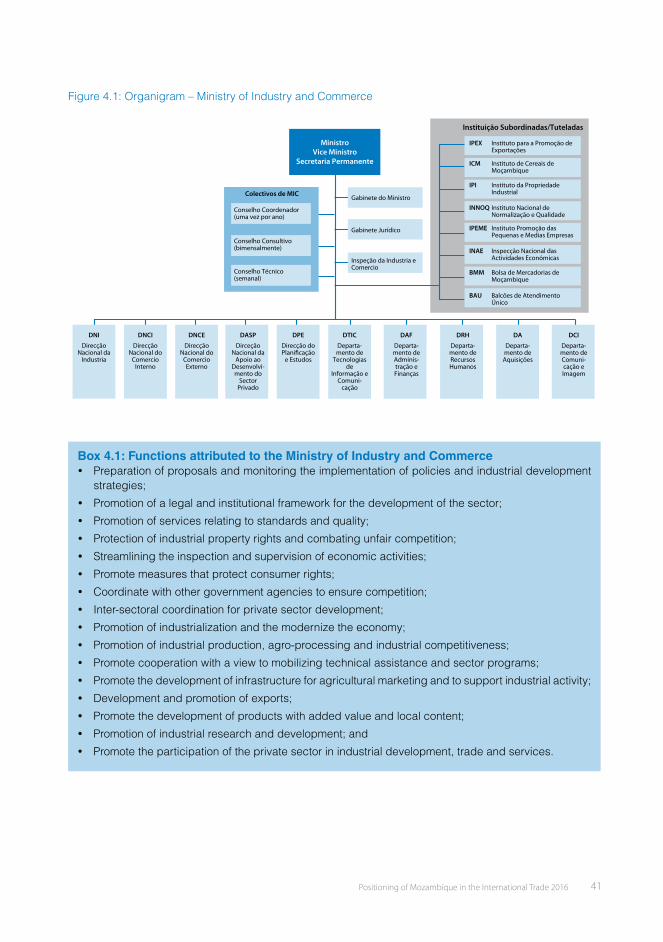

Box 4.1: Functions attributed to the Ministry of Industry and Commerce . . . . . . . . . . . . . . . . 41

Box 4.2: Trade related issues coordination mechanism – Aid for Trade and EIF in Mozambique . . . . 43

Box 4.3: Logistics Performance Index (LPI) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

vi Positioning of Mozambique in the International Trade 2016

Figure 2.12: Mozambique banana exports and global trends . . . . . . . . . . . . . . . . . . . . . . 16

Figure 2.13: Mozambique banana export destination . . . . . . . . . . . . . . . . . . . . . . . . . . 16

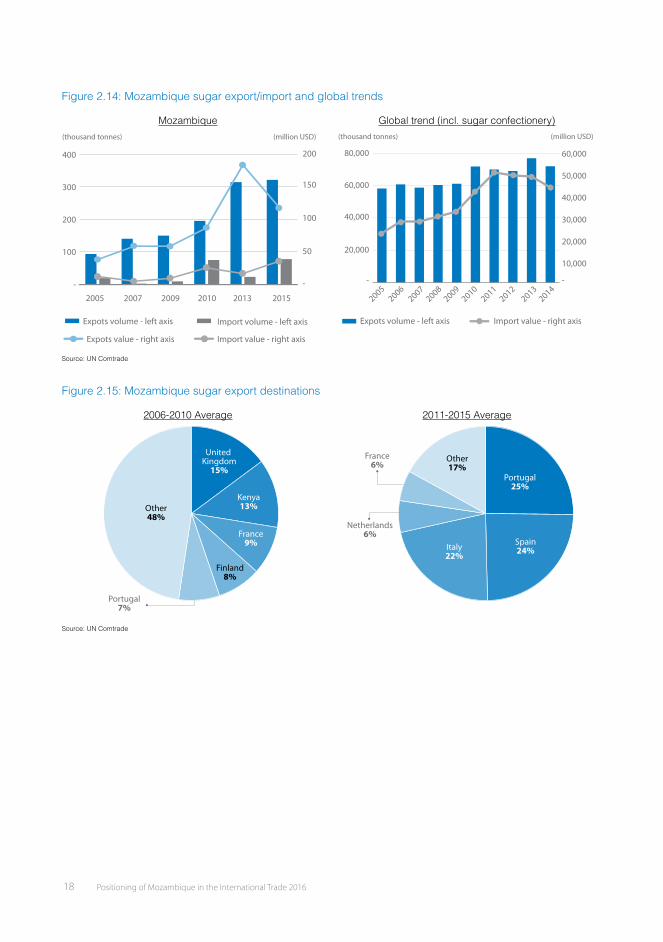

Figure 2.14: Mozambique sugar export/import and global trends . . . . . . . . . . . . . . . . . . . . 18

Figure 2.15: Mozambique sugar export destinations . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Figure 2.16: Mozambique crustaceans exports and global trends . . . . . . . . . . . . . . . . . . . 20

Figure 2.17: Mozambique crustaceans export destinations . . . . . . . . . . . . . . . . . . . . . . . 20

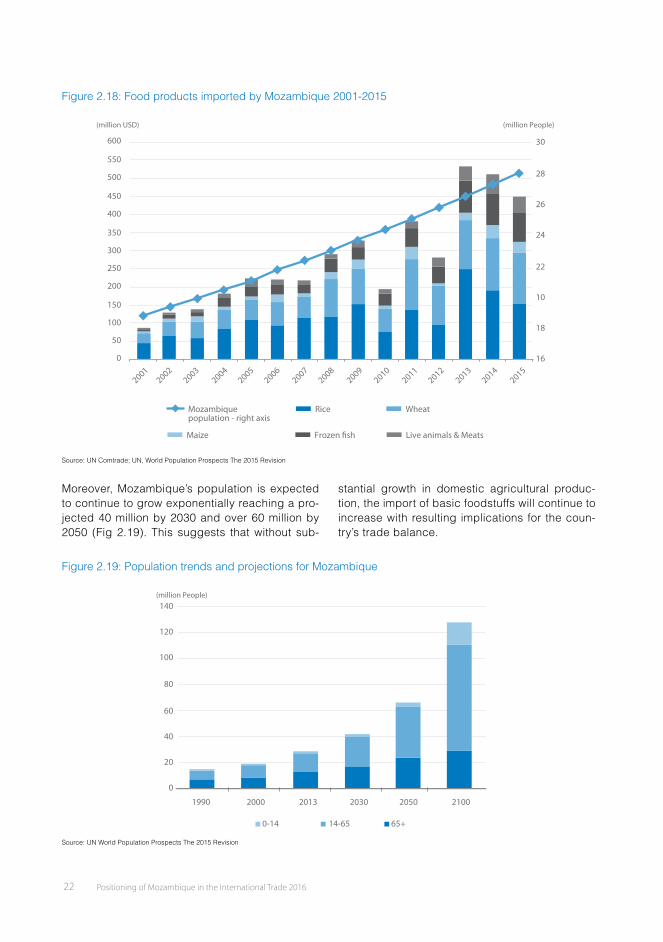

Figure 2.18: Food products imported by Mozambique 2001-2015 . . . . . . . . . . . . . . . . . . . 22

Figure 2.19: Population trends and projections for Mozambique . . . . . . . . . . . . . . . . . . . . 22

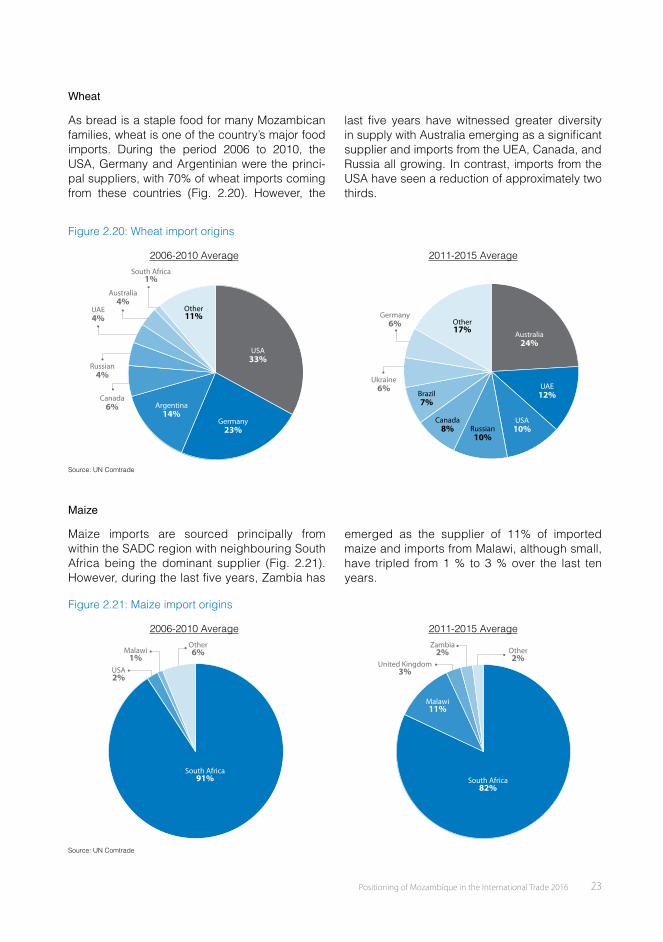

Figure 2.20: Wheat import origins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Figure 2.21: Maize import origins. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

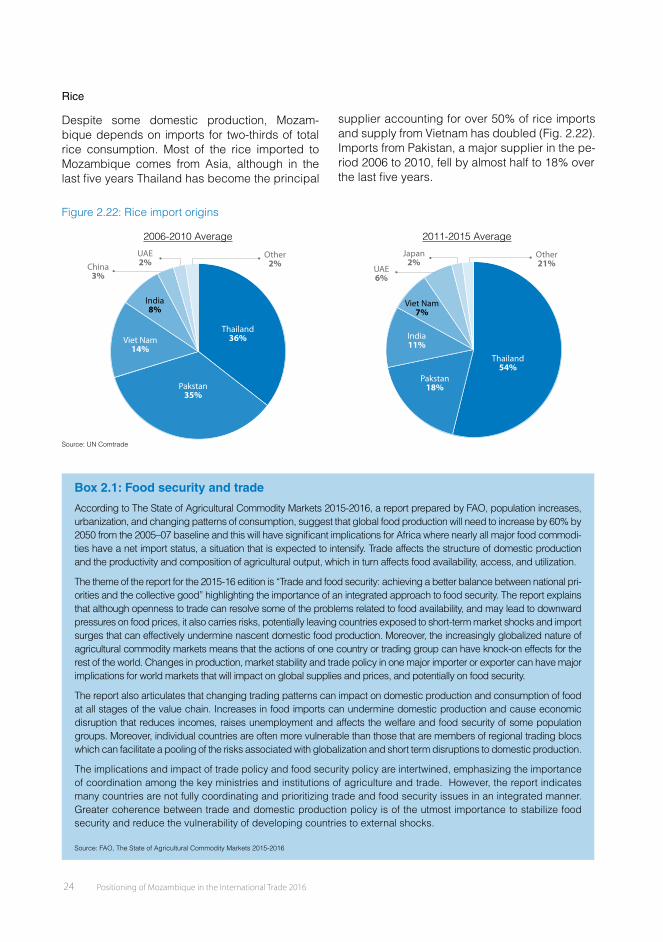

Figure 2.22: Rice import origins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

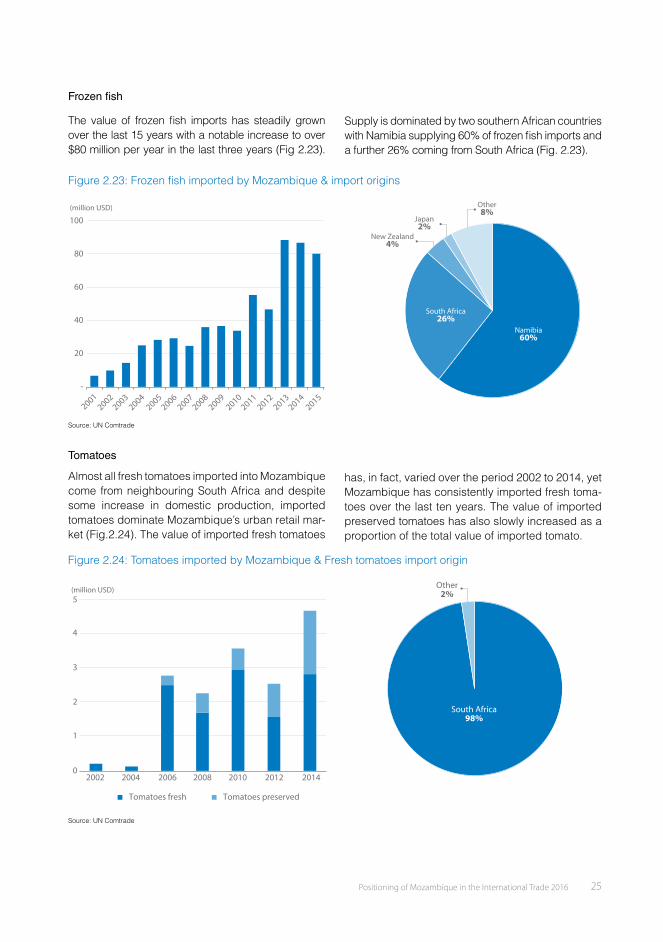

Figure 2.23: Frozen fi sh imported by Mozambique & import origins . . . . . . . . . . . . . . . . . . . 25

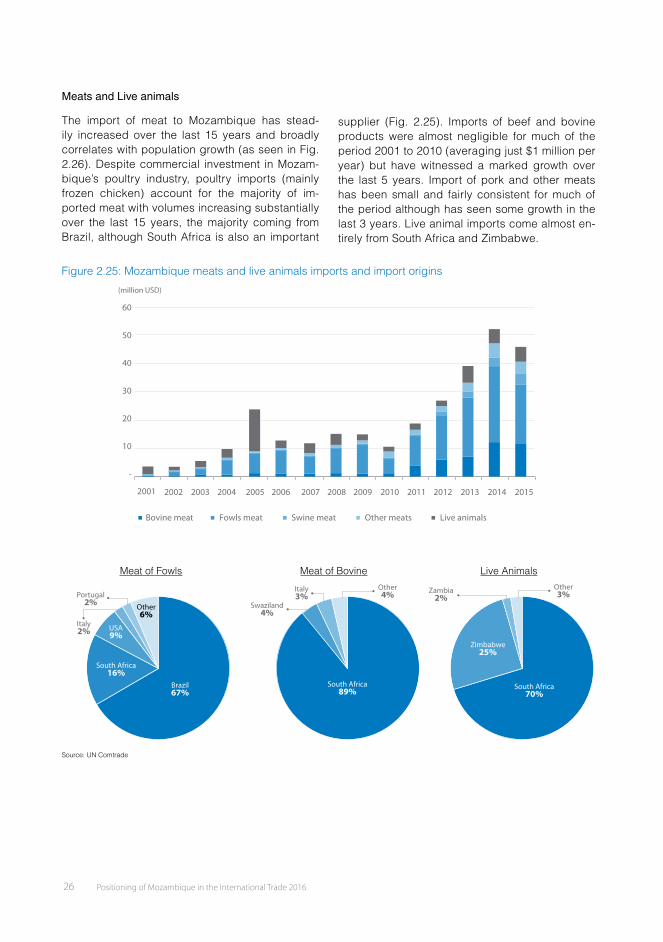

Figure 2.24: Tomatoes imported by Mozambique & Fresh tomatoes import origin . . . . . . . . . . . 25

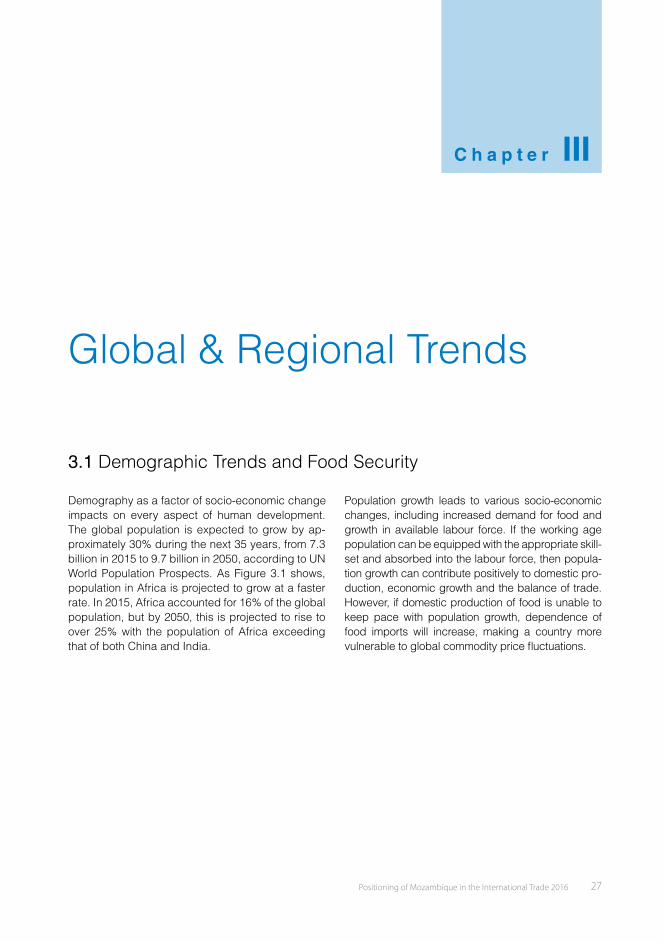

Figure 2.25: Mozambique meats and live animals imports and import origins . . . . . . . . . . . . . 26

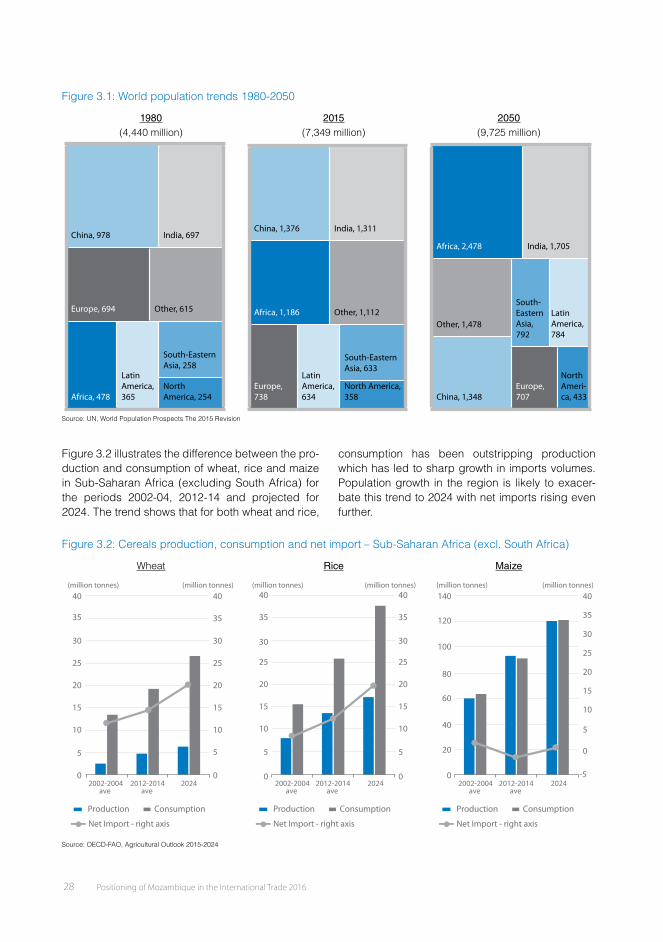

Figure 3.1: World population trends 1980-2050 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Figure 3.2: Cereals production, consumption and net import – Sub-Saharan Africa (excl. South Africa) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Figure 3.3: Calorie intake per capita in LDCs and Developed countries. . . . . . . . . . . . . . . . . 29

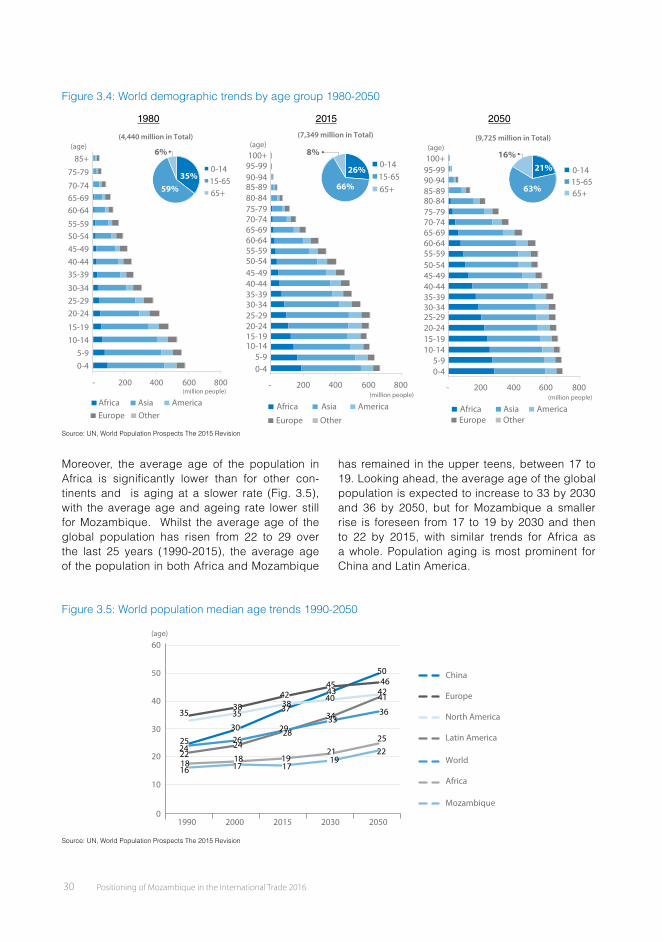

Figure 3.4: World demographic trends by age group 1980-2050 . . . . . . . . . . . . . . . . . . . . 30

Figure 3.5: World population median age trends 1990-2050. . . . . . . . . . . . . . . . . . . . . . . 30

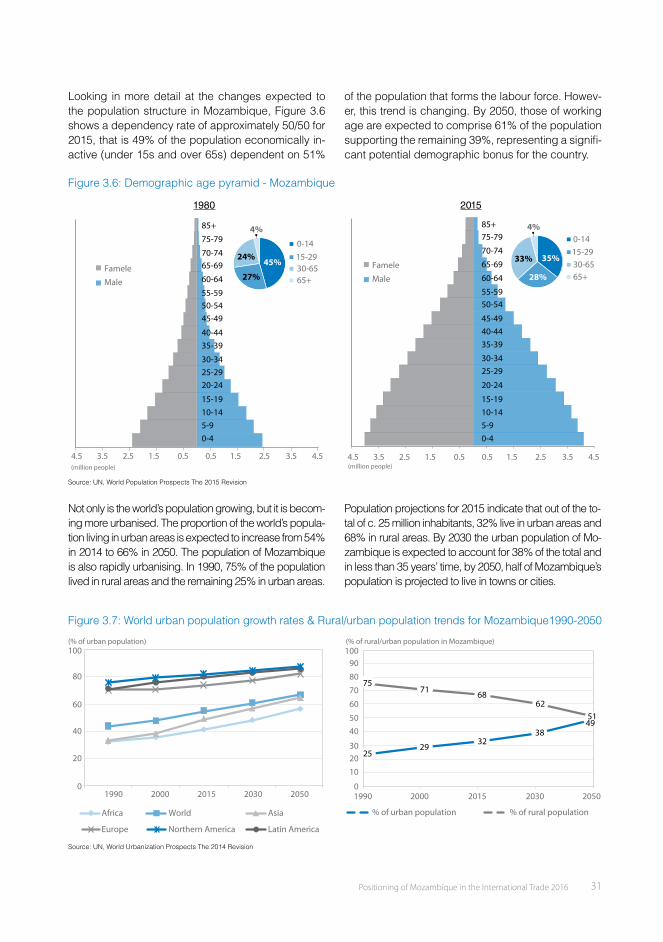

Figure 3.6: Demographic age pyramid - Mozambique. . . . . . . . . . . . . . . . . . . . . . . . . . 31

Figure 3.7: World urban population growth rates & Rural/urban population trends for Mozam-bique1990-2050 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Figure 3.8: Trend of urbanization and services value added (% of GDP) 1980-2014 . . . . . . . . . . 32

Figure 3.9: Mobile and fi xed telephone subscription & International tourism arrivals and revenues . . 32

Figure 3.10: Consumption patterns by sector and income segment – 2010 (average of 92 countries) . . 33

Figure 3.11: Energy demand by sector & Total primary energy demand by resource . . . . . . . . . 33

Figure 3.12: Electricity generation trend by resource – IEA bridge scenario . . . . . . . . . . . . . . 34

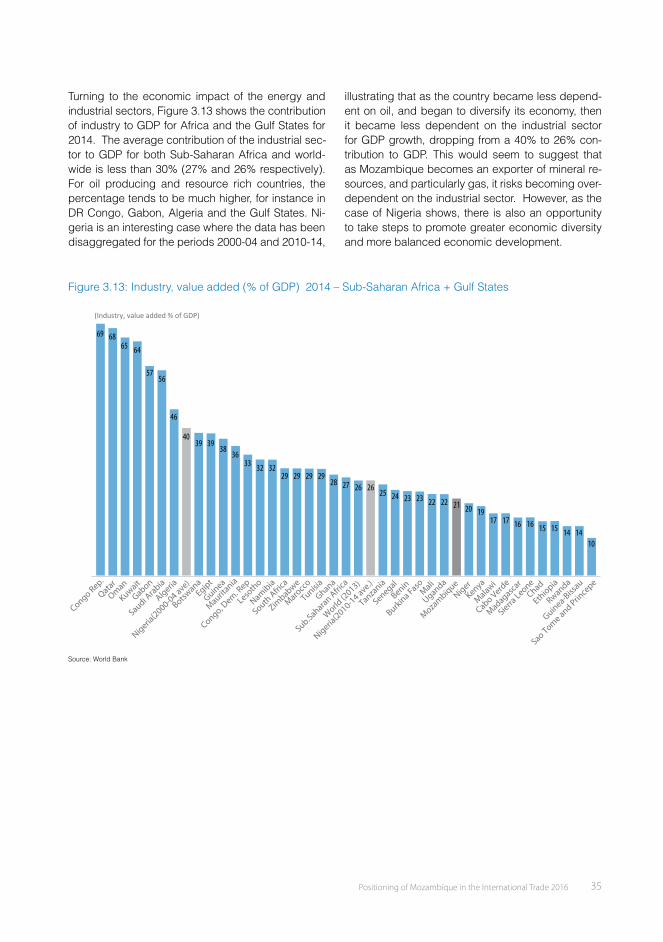

Figure 3.13: Industry, value added (% of GDP) 2014 – Sub-Saharan Africa + Gulf States . . . . . . . 35

Figure 3.14: Fuel price trends and world trade (exports) 2002-2014 . . . . . . . . . . . . . . . . . . 36

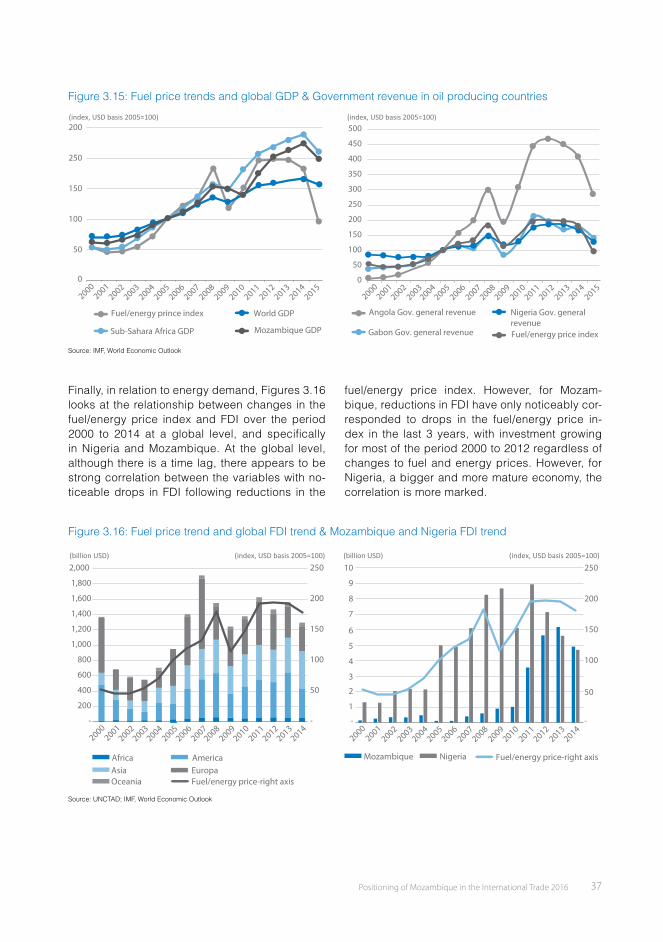

Figure 3.15: Fuel price trends and global GDP & Government revenue in oil producing countries . . . 37

Figure 3.16: Fuel price trend and global FDI trend & Mozambique and Nigeria FDI trend . . . . . . . 37

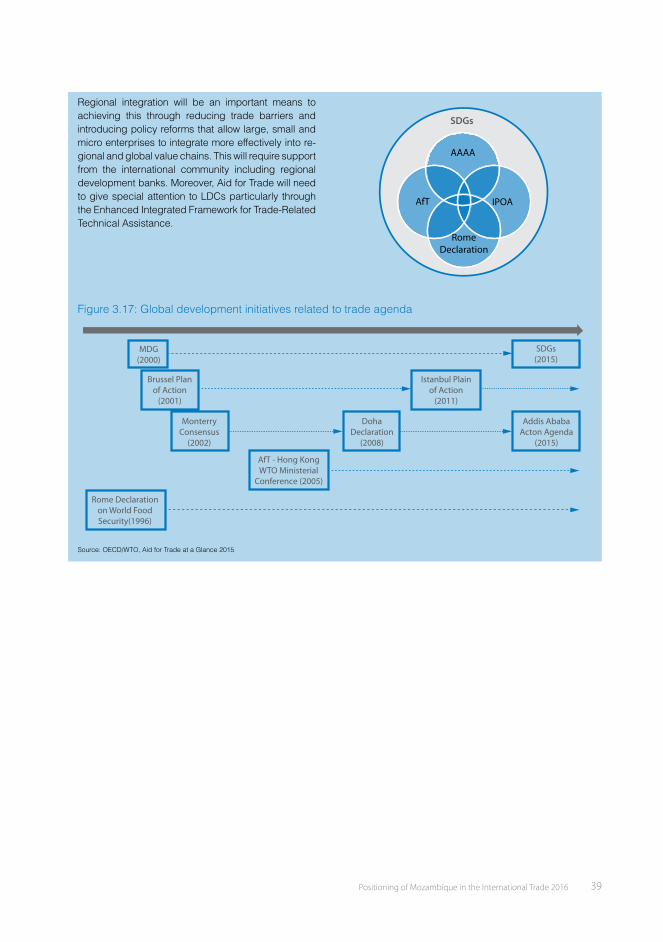

Figure 3.17: Global development initiatives related to trade agenda . . . . . . . . . . . . . . . . . . 39

Figure 4.1: Organigram – Ministry of Industry and Commerce. . . . . . . . . . . . . . . . . . . . . . 41

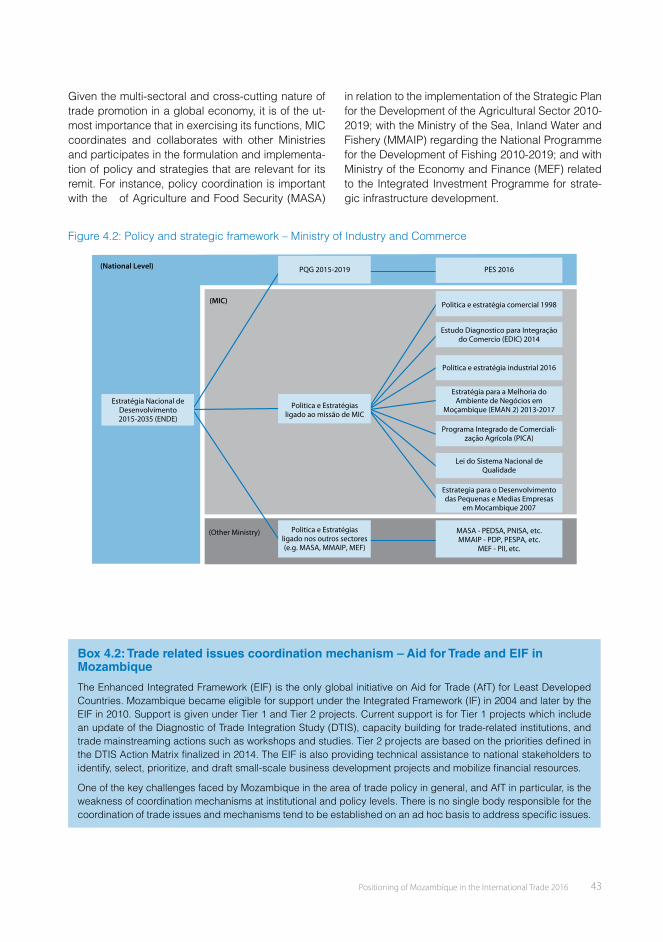

Figure 4.2: Policy and strategic framework – Ministry of Industry and Commerce. . . . . . . . . . . . 43

Figure 4.3: Average MFN applied duties 2014 – Mozambique . . . . . . . . . . . . . . . . . . . . . 46

Figure 4.4: LPI – Mozambique 2010 vs 2016. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Positioning of Mozambique in the International Trade 2016 vii

Tables

Table 1.1: Mozambique’s major trading partners (2011-2015 avg.) . . . . . . . . . . . . . . . . . . . 4

Table 2.1: Main export and import products in Mozambique . . . . . . . . . . . . . . . . . . . . . . 5

Table 2.2: Cashew nuts export world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Table 2.3: Sesame exports word ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Table 2.4: Almonds export world ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table 2.5: Cotton exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Table 2.6: Banana exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Table 2.7: Sugar exports world ranking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Table 2.8: Crustaceans exports world ranking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Table 4.1: Preferential Trade Agreements - Mozambique . . . . . . . . . . . . . . . . . . . . . . . . 45

Table 4.2: Bilateral investment agreements – Mozambique . . . . . . . . . . . . . . . . . . . . . . . 46

Table 4.3: Doing Business 2016 (comparison w/selected countries in Sub-Saharan Africa) . . . . . . 47

Table 4.4: GCI 2015-2016 global ranking (comparison w/selected countries in Sub-Saharan Africa). . 48

Table 4.5: LPI 2016 Sub-Saharan Africa ranking (comparison w/selected countries) . . . . . . . . . . 49

Boxes

Box 1.1: Volatile commodity prices destabilize the economy . . . . . . . . . . . . . . . . . . . . . . 3

Box 2.1: Food security and trade. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Box 3.1: Changing dietary habits and diversifi cation of foods demand . . . . . . . . . . . . . . . . . 29

Box 3.2: Consumption in developing & emerging countries – Bottom of Pyramid . . . . . . . . . . . . 33

Box 3.3: COP 21 and energy demand forecast – IEA Bridge Scenario . . . . . . . . . . . . . . . . . 34

Box 3.4: Global Value Chains (GVCs) – opportunities and risks . . . . . . . . . . . . . . . . . . . . . 36

Box 3.5: Trade and Development Agenda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Box 4.1: Functions attributed to the Ministry of Industry and Commerce . . . . . . . . . . . . . . . . 41

Box 4.2: Trade related issues coordination mechanism – Aid for Trade and EIF in Mozambique . . . . 43

Box 4.3: Logistics Performance Index (LPI) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Positioning of Mozambique in the International Trade 2016 ix

Executive Summary

This report was prepared by the Ministry of Indus-try and Trade with the support of UNDP to illustrate Mozambique’s position in relation to business/trade opportunities with its economic partners. Mozam-bique’s rich endowment in natural resources rep-resent signifi cant trading opportunities that could transform the country from one which is dependent on agricultural, marine, mineral and energy based exports, to a major player in the global market of value added products, creating the fi scal space for sustainable investment in its increasingly young population and socio-economic infrastructure. Yet, such opportunities often present a complex set of macro-economic challenges, and in an increasingly globalized economy, Mozambique will need to care-fully consider ways to improve its productivity and competitiveness and promote greater diversifi ca-tion through greater integration into the global value chains. To address such challenges, evidence-based policy coordination is a condition sine qua non to ensure effective policy implementation and meaningful economic transformation.

The trade landscape in Mozambique has changed signifi cantly in the last 15 years with substantial increases in both imports and exports and there is evidence that points to an intensifi cation of this transformation over the next fi fteen years. Chap-ter I looks at the changing nature of trade in Mo-zambique and the growing importance of trade for the economy. Mozambique’s historical exports like cashew, cotton and shellfi sh, still signifi cant two decades ago, have been overtaken by the export in the minerals and energy sector. As a result of inte-grating into the regional and global trade networks, the importance of trade for the Mozambican econo-my had grown to attain a value equivalent to 100% of GDP by 2012. Substantial growth in imports over the period 2010-14 was driven by Foreign Direct In-vestments in extractives sector.

Mozambique’s abundant natural resources, not only in terms of minerals but including agricultural land and fi sheries, potentially place the country in a strong position as a major exporter of commodities. Chapter II analyses the signifi cance of changes in

Mozambique’s trade product portfolio and principle trade partners. The export of minerals has grown, particularly in the last 5 years, with much greater growth anticipated in the future. However, the ex-port and import of agricultural and food products is also signifi cant given its importance for sustain-ing livelihoods and food security, and its impact on the balance of trade. This chapter focusses on the trade volume and value of a set of key agricultural and marine exports and changes in global market share. Mozambique is a net importer of food and the growth of food imports has closely correlated with population growth, which is expected to grow exponentially suggesting that the import of basic foods will continue to increase. The implications and impact of trade policy and food security policy are intertwined, emphasizing the importance of a coor-dinated effort among the key ministries and institu-tions responsible for agriculture and trade policy.

Growth in Mozambique’s trade has resulted in its re-integration into the regional and global econ-omy. Chapter III looks at key global trends and their impact on socio economic development and on trade. The world’s population is growing and becoming more urbanized and these trends are creating a new dynamism for Africa and for Mozambique. Population growth can contribute positively to domestic production and the bal-ance of trade. Mozambique’s young population and growth in the working age population could bring a signifi cant demographic bonus for the country. However, if domestic production of food is unable to keep pace with population growth, dependence of food imports will increase. Global energy demand increased by over 50% in the pe-riod 1990-2013. Although this growth is expected to continue, the world leaders are determined to curb growth in the demand for energy to meet the COP 21 global target. Coal and oil has been the major energy sources for power generation for many decades, but their relative importance is declining with natural gas becoming more im-portant, a trend which is potentially positive, to a great extent, for Mozambique. However, fl uc-

viii Positioning of Mozambique in the International Trade 2016

Abbreviations

ACP African, Caribbean and Pacifi c Countries

AfT Aid for Trade

AGOA African Growth and Opportunity Act

CAADP Comprehensive African Agriculture Development Program

COMESA Common Market for Eastern and Southern Africa

COP Conference of the Parties

DTIS Diagnostic of Trade Integration Study

EAC East African Community

EIF Enhanced Integrated Framework

ENDE Estratégia Nacional de Desenvolvimento (National Development Strategy)

FAO Food and Agriculture Organization

FDI Foreign Direct Investment

GSP Generalized System of Preferences

GVCs Global Value Chains

ICT Information and Communication Technology

IEA International Energy Agency

INE Instituto Nacional de Estatistica (National Statistics Institutions)

LDCs Least Developed Countries

LPI Logistics Performance Index

MASA Ministro da Agricultura e Segurança Alimentar (Ministry of Agriculture and Food Security)

MDG Millennium Development Goals

MEF Ministro de Economia e Finanças (Ministry of Economy and Finance)

MFN Most Favoured Nation

MIC Ministro da Indústria e Comércio (Ministry of Industry and Commerce)

MMAIP Ministro do Mar, Águas Interiores e Pescas (Ministry for the Sea, Inland Water and Fishery)

MTOE Million Tonnes of Oil Equivalent

OECD Organisation for Economic Co-operation and Development

PES Plano Economico e Social (Social Economic Plan)

PEDSA Plan for the Development of the Agricultural Sector

PPP Purchasing Power Parity

PQG Programa Quinquenal do Governo (Government’s fi ve-year programme)

PTA Preferential Trade Agreement

SADC Southern African Development Community

SDGs Sustainable Development Goals

SDT Special and Differential Treatment

TWh Terawatt Hour

UNDP United Nations Development Programme

UNCTAD United Nations Conference on Trade and Development

WEF World Economic Forum

WTO World Trade Organization

Positioning of Mozambique in the International Trade 2016 ix

Executive Summary

This report was prepared by the Ministry of Indus-try and Trade with the support of UNDP to illustrate Mozambique’s position in relation to business/trade opportunities with its economic partners. Mozam-bique’s rich endowment in natural resources rep-resent signifi cant trading opportunities that could transform the country from one which is dependent on agricultural, marine, mineral and energy based exports, to a major player in the global market of value added products, creating the fi scal space for sustainable investment in its increasingly young population and socio-economic infrastructure. Yet, such opportunities often present a complex set of macro-economic challenges, and in an increasingly globalized economy, Mozambique will need to care-fully consider ways to improve its productivity and competitiveness and promote greater diversifi ca-tion through greater integration into the global value chains. To address such challenges, evidence-based policy coordination is a condition sine qua non to ensure effective policy implementation and meaningful economic transformation.

The trade landscape in Mozambique has changed signifi cantly in the last 15 years with substantial increases in both imports and exports and there is evidence that points to an intensifi cation of this transformation over the next fi fteen years. Chap-ter I looks at the changing nature of trade in Mo-zambique and the growing importance of trade for the economy. Mozambique’s historical exports like cashew, cotton and shellfi sh, still signifi cant two decades ago, have been overtaken by the export in the minerals and energy sector. As a result of inte-grating into the regional and global trade networks, the importance of trade for the Mozambican econo-my had grown to attain a value equivalent to 100% of GDP by 2012. Substantial growth in imports over the period 2010-14 was driven by Foreign Direct In-vestments in extractives sector.

Mozambique’s abundant natural resources, not only in terms of minerals but including agricultural land and fi sheries, potentially place the country in a strong position as a major exporter of commodities. Chapter II analyses the signifi cance of changes in

Mozambique’s trade product portfolio and principle trade partners. The export of minerals has grown, particularly in the last 5 years, with much greater growth anticipated in the future. However, the ex-port and import of agricultural and food products is also signifi cant given its importance for sustain-ing livelihoods and food security, and its impact on the balance of trade. This chapter focusses on the trade volume and value of a set of key agricultural and marine exports and changes in global market share. Mozambique is a net importer of food and the growth of food imports has closely correlated with population growth, which is expected to grow exponentially suggesting that the import of basic foods will continue to increase. The implications and impact of trade policy and food security policy are intertwined, emphasizing the importance of a coor-dinated effort among the key ministries and institu-tions responsible for agriculture and trade policy.

Growth in Mozambique’s trade has resulted in its re-integration into the regional and global econ-omy. Chapter III looks at key global trends and their impact on socio economic development and on trade. The world’s population is growing and becoming more urbanized and these trends are creating a new dynamism for Africa and for Mozambique. Population growth can contribute positively to domestic production and the bal-ance of trade. Mozambique’s young population and growth in the working age population could bring a signifi cant demographic bonus for the country. However, if domestic production of food is unable to keep pace with population growth, dependence of food imports will increase. Global energy demand increased by over 50% in the pe-riod 1990-2013. Although this growth is expected to continue, the world leaders are determined to curb growth in the demand for energy to meet the COP 21 global target. Coal and oil has been the major energy sources for power generation for many decades, but their relative importance is declining with natural gas becoming more im-portant, a trend which is potentially positive, to a great extent, for Mozambique. However, fl uc-

Positioning of Mozambique in the International Trade 2016 1

1.1 The Landscape of Trade in Mozambique

Overview of Trade Trends in Mozambique

C h a p t e r I

Political reforms and sound macro-economic man-agement have been important factors in stimulating economic development in Mozambique over the past 15 years, securing one of the highest growth rates for African non-oil economies with annual real GDP growth over the period 2002-2012 averaging 7.5%.

Economic reforms since 2000 have resulted in the gradual reintegration of the economy into both re-gional and global markets, directly impacting on the country’s trade structure and enabling trade to play an important role in facilitating economic growth.

The trade landscape in Mozambique has changed signifi cantly over the last 15 years, as both imports and exports have grown dramatically as a result of Foreign Direct Investment (FDI) in mega-projects, and this dynamic is likely to continue for the fore-seeable future as the country’s trading potential be-comes a reality, particularly in the extractive sector.

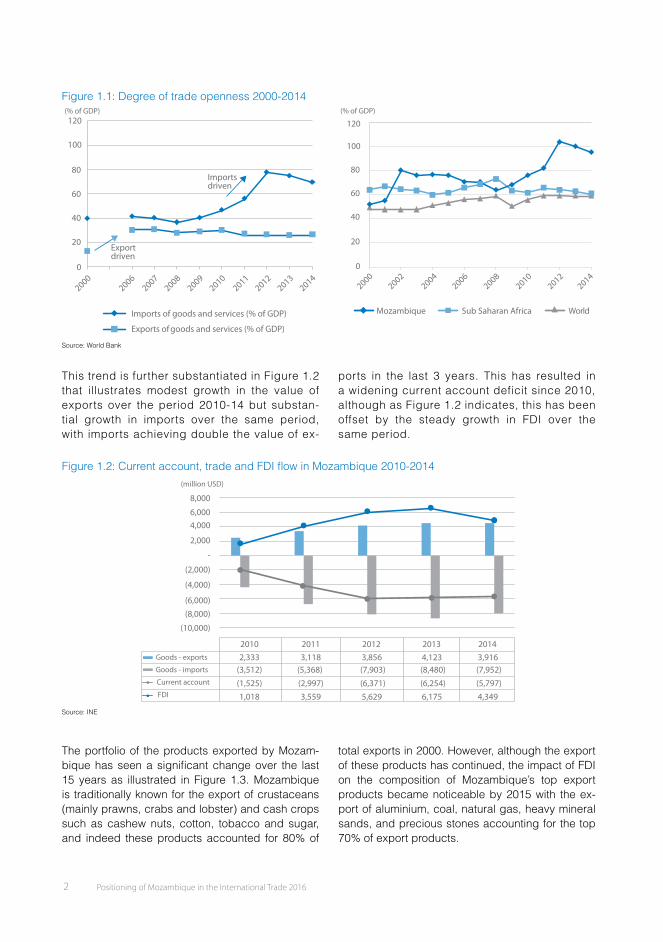

The Trade Openness Index measures the relation-ship between the combined value of imports and exports in relation to the size of GDP. Figure 1.1 il-lustrates the changing importance of trade for the Mozambican economy. There has been a notable change in Mozambique’s score on the index since 2000 in comparison to regional and global averages emphasizing the steady re-integration of Mozam-bican trade into regional and global trade networks.

A closer examination of the value of imports and exports as a percentage of GDP over the same pe-riod shows that changes in trade openness appear to be largely export driven in the period 2000-2002 and import driven in the period 2008-12. This almost certainly refl ects the beginning of the export of alu-minium in the early part of the decade and the im-port of equipment and machinery associated with investments in the energy and mineral resources sector, particularly coal and natural gas, at the end of the decade.

x Positioning of Mozambique in the International Trade 2016

tuations in fuel and energy prices have shown signifi cant impacts on global export market and GDP growth, casting a shadow on extractive de-pendent economies. Excessive dependence on extractive industry can disproportionately expose developing nations to volatile and unpredictable global markets.

The complex nature of trade at the local, regional and global level requires an organized and coor-dinated policy response to seize the potential op-portunities and to mitigate the risks of volatility as-sociated with global markets. Chapter IV looks at

the role of the Ministry of Industry and Commerce, the key institution in Mozambique responsible for the trade agenda, and the composition of a num-ber of trade and commerce related policy instru-ments and strategies. A number of international trade and investment agreements to which Mo-zambique is a signatory provide the framework for the promotion of bilateral and multi-lateral trade. Finally, an review of the business environment in Mozambique evaluates the country’s trade com-petiveness and weaknesses in relation to regional counterparts.

Positioning of Mozambique in the International Trade 2016 1

1.1 The Landscape of Trade in Mozambique

Overview of Trade Trends in Mozambique

C h a p t e r I

Political reforms and sound macro-economic man-agement have been important factors in stimulating economic development in Mozambique over the past 15 years, securing one of the highest growth rates for African non-oil economies with annual real GDP growth over the period 2002-2012 averaging 7.5%.

Economic reforms since 2000 have resulted in the gradual reintegration of the economy into both re-gional and global markets, directly impacting on the country’s trade structure and enabling trade to play an important role in facilitating economic growth.

The trade landscape in Mozambique has changed signifi cantly over the last 15 years, as both imports and exports have grown dramatically as a result of Foreign Direct Investment (FDI) in mega-projects, and this dynamic is likely to continue for the fore-seeable future as the country’s trading potential be-comes a reality, particularly in the extractive sector.

The Trade Openness Index measures the relation-ship between the combined value of imports and exports in relation to the size of GDP. Figure 1.1 il-lustrates the changing importance of trade for the Mozambican economy. There has been a notable change in Mozambique’s score on the index since 2000 in comparison to regional and global averages emphasizing the steady re-integration of Mozam-bican trade into regional and global trade networks.

A closer examination of the value of imports and exports as a percentage of GDP over the same pe-riod shows that changes in trade openness appear to be largely export driven in the period 2000-2002 and import driven in the period 2008-12. This almost certainly refl ects the beginning of the export of alu-minium in the early part of the decade and the im-port of equipment and machinery associated with investments in the energy and mineral resources sector, particularly coal and natural gas, at the end of the decade.

2 Positioning of Mozambique in the International Trade 2016

Figure 1.1: Degree of trade openness 2000-2014

Imports of goods and services (% of GDP)

Exports of goods and services (% of GDP)

0

20

40

60

80

100

120

20002006

20072008

20092010

20112012

20132014

Importsdriven

Exportdriven

(% of GDP)

0

20

40

60

80

100

120

20002002

20042006

20082010

20122014

Mozambique Sub Saharan Africa World

(% of GDP)

Source: World Bank

This trend is further substantiated in Figure 1.2 that illustrates modest growth in the value of exports over the period 2010-14 but substan-tial growth in imports over the same period, with imports achieving double the value of ex-

ports in the last 3 years. This has resulted in a widening current account deficit since 2010, although as Figure 1.2 indicates, this has been offset by the steady growth in FDI over the same period.

Figure 1.2: Current account, trade and FDI fl ow in Mozambique 2010-2014

2010 2011 2012 2013 2014Goods - exports 2,333 3,118 3,856 4,123 3,916Goods - imports (3,512) (5,368) (7,903) (8,480) (7,952)Current account (1,525) (2,997) (6,371) (6,254) (5,797)FDI 1,018 3,559 5,629 6,175 4,349

(10,000)

(8,000)

(6,000)

(4,000)

(2,000)

-

2,000

4,0006,000

8,000

(million USD)

Source: INE

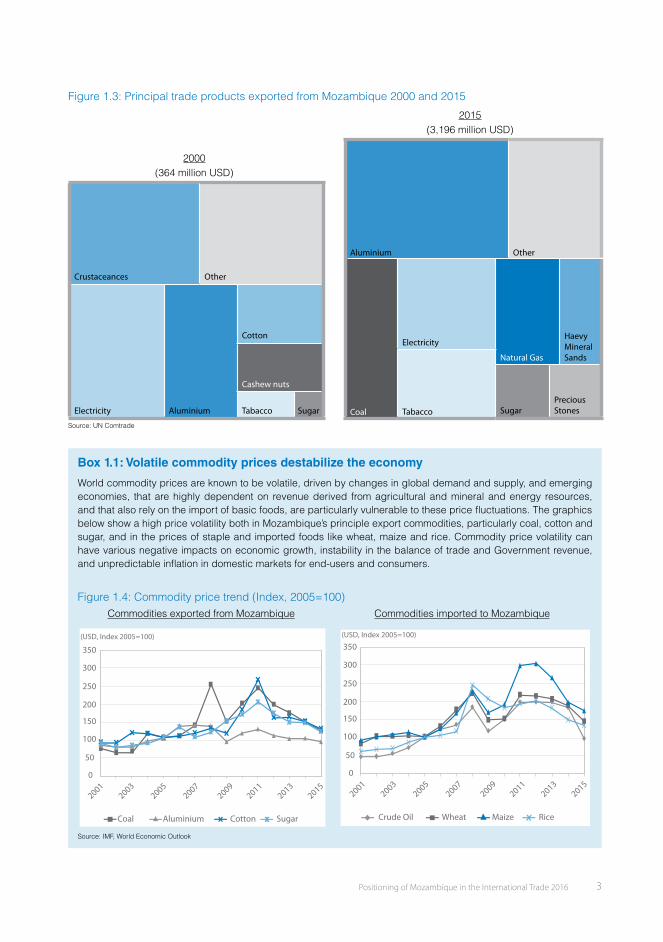

The portfolio of the products exported by Mozam-bique has seen a signifi cant change over the last 15 years as illustrated in Figure 1.3. Mozambique is traditionally known for the export of crustaceans (mainly prawns, crabs and lobster) and cash crops such as cashew nuts, cotton, tobacco and sugar, and indeed these products accounted for 80% of

total exports in 2000. However, although the export of these products has continued, the impact of FDI on the composition of Mozambique’s top export products became noticeable by 2015 with the ex-port of aluminium, coal, natural gas, heavy mineral sands, and precious stones accounting for the top 70% of export products.

Positioning of Mozambique in the International Trade 2016 3

Figure 1.3: Principal trade products exported from Mozambique 2000 and 2015

2000 (364 million USD)

Crustaceances Other

Electricity Aluminium

Cotton

Cashew nuts

Tabacco Sugar

2015 (3,196 million USD)

Aluminium Other

Coal

Electricity

Natural Gas

Haevy Mineral Sands

Tabacco SugarPreciousStones

Source: UN Comtrade

Box 1.1: Volatile commodity prices destabilize the economy

World commodity prices are known to be volatile, driven by changes in global demand and supply, and emerging economies, that are highly dependent on revenue derived from agricultural and mineral and energy resources, and that also rely on the import of basic foods, are particularly vulnerable to these price fl uctuations. The graphics below show a high price volatility both in Mozambique’s principle export commodities, particularly coal, cotton and sugar, and in the prices of staple and imported foods like wheat, maize and rice. Commodity price volatility can have various negative impacts on economic growth, instability in the balance of trade and Government revenue, and unpredictable infl ation in domestic markets for end-users and consumers.

Figure 1.4: Commodity price trend (Index, 2005=100)Commodities exported from Mozambique Commodities imported to Mozambique

0

50

100

150

200

250

300

350

(USD, Index 2005=100)

20012003

20052007

20092011

20132015

Coal Aluminium Cotton Sugar

0

50

100

150

200

250

300

350(USD, Index 2005=100)

20012003

20052007

20092011

20132015

Crude Oil Wheat Maize Rice

Source: IMF, World Economic Outlook

Positioning of Mozambique in the International Trade 2016 3

Figure 1.3: Principal trade products exported from Mozambique 2000 and 2015

2000 (364 million USD)

Crustaceances Other

Electricity Aluminium

Cotton

Cashew nuts

Tabacco Sugar

2015 (3,196 million USD)

Aluminium Other

Coal

Electricity

Natural Gas

Haevy Mineral Sands

Tabacco SugarPreciousStones

Source: UN Comtrade

Box 1.1: Volatile commodity prices destabilize the economy

World commodity prices are known to be volatile, driven by changes in global demand and supply, and emerging economies, that are highly dependent on revenue derived from agricultural and mineral and energy resources, and that also rely on the import of basic foods, are particularly vulnerable to these price fl uctuations. The graphics below show a high price volatility both in Mozambique’s principle export commodities, particularly coal, cotton and sugar, and in the prices of staple and imported foods like wheat, maize and rice. Commodity price volatility can have various negative impacts on economic growth, instability in the balance of trade and Government revenue, and unpredictable infl ation in domestic markets for end-users and consumers.

Figure 1.4: Commodity price trend (Index, 2005=100)Commodities exported from Mozambique Commodities imported to Mozambique

0

50

100

150

200

250

300

350

(USD, Index 2005=100)

20012003

20052007

20092011

20132015

Coal Aluminium Cotton Sugar

0

50

100

150

200

250

300

350(USD, Index 2005=100)

20012003

20052007

20092011

20132015

Crude Oil Wheat Maize Rice

Source: IMF, World Economic Outlook

Positioning of Mozambique in the International Trade 2016 5

2.1 Trade Products Portfolio

Trend Analysis of Trade Products in Mozambique

C h a p t e r II

Table 2.1 summarizes Mozambique’s principle ex-port and import products across three broad cat-egories: mega-projects, extractive industries (min-erals) and industrial products, cash crops and food products. Principal exports comprise aluminum,

minerals, and cash crops whereas imports include petrol, industrial and manufactured products, par-ticularly vehicles, machinery and construction ma-terials, and basic foodstuffs, including cereals, fro-zen fi sh and meat.

Table 2.1: Main export and import products in Mozambique

Megaproject, Extractive industry, Industrial products

Cash Crops Foods

Exports

� Aluminium � Coal � Natural gas � Electricity � Heavy mineral sands � Precious stones � Woods

� Cashew nuts � Sesame � Almonds � Sugar � Cotton � Banana � Tobacco

� Crustaceans

Imports

� Petroleum � Unwrought aluminum � Electricity � Machinery � Construction materials � Vehicle � Pharmaceutical products � Furniture

� Sugar

� Wheat � Maize � Rice � Fish frozen � Live animals and meats

4 Positioning of Mozambique in the International Trade 2016

Table 1.1 shows Mozambique’s top ten trading partners according to the value of exports and im-ports. Proximity to South Africa, the second-larg-est economy in Africa, accounting for 24% of the continent’s gross domestic product in 2015, make it Mozambique’s biggest trading partner. Mozam-bique’s principle exports to South Africa are gas from Inhambane, and electricity from the Cahorra Bassa hydro dam in Tete. However, the importance of South Africa as a trading partner lies principally in its role as a source of imports particularly in re-lation to machinery, vehicles, and foods, and as a result Mozambique runs a signifi cant trade defi cit with its neighbour that has averaged close to $2bn per annum over the last fi ve years. In fact, Mozam-

1.2 Trade Partners in Mozambique

bique runs a trade defi cit with most of its top ten trade partners with the exception of the Netherlands and India. The Netherlands is a special case due to the trading of aluminum and India is Mozambique’s largest coal export destination.

China and India, ranked in 3rd and 4th position, are gaining increasing importance as trade partners and are the principle destinations for primary commodities such as coal and heavy mineral sands. The impor-tance of Bahrain and the UEA is related to the import of petroleum. Traditional trading partners amongst de-veloped countries, notably Portugal, the UK, the USA and Japan, are international suppliers of machinery, vehicles, and electrical and electronic products.

Table 1.1: Mozambique’s major trading partners (2011-2015 avg.)

(million USD)Trade value

(exports + imports)Trade balance

South Africa 3,264 -1,789Netherlands 1,678 537China 851 -371India 625 34United Arab Emirates 550 -465Bahrain 465 -447Portugal 434 -336United Kingdom 354 -68USA 289 -152Japan 238 -198

Source: UN Comtrade

Figure 1.5: Mozambique’s principle export destination and import origins (2011-2015 avg.)

Exports destinations Imports origins

South Africa19%

China6%

Netherlands29%

India9%

USA2%

Italy2%

Switzerland2%

Zimbabwe2%

Singapore4%

United Kingdom

4%

Other21%

South Africa32%

China8%

Netherlands7%

United Arab Emirates

6%Bahrain6%

Portugal5%

India4%

USA3%

Japan3%

United Kingdom

3%

Other23%

Source: UN Comtrade

Positioning of Mozambique in the International Trade 2016 5

2.1 Trade Products Portfolio

Trend Analysis of Trade Products in Mozambique

C h a p t e r II

Table 2.1 summarizes Mozambique’s principle ex-port and import products across three broad cat-egories: mega-projects, extractive industries (min-erals) and industrial products, cash crops and food products. Principal exports comprise aluminum,

minerals, and cash crops whereas imports include petrol, industrial and manufactured products, par-ticularly vehicles, machinery and construction ma-terials, and basic foodstuffs, including cereals, fro-zen fi sh and meat.

Table 2.1: Main export and import products in Mozambique

Megaproject, Extractive industry, Industrial products

Cash Crops Foods

Exports

� Aluminium � Coal � Natural gas � Electricity � Heavy mineral sands � Precious stones � Woods

� Cashew nuts � Sesame � Almonds � Sugar � Cotton � Banana � Tobacco

� Crustaceans

Imports

� Petroleum � Unwrought aluminum � Electricity � Machinery � Construction materials � Vehicle � Pharmaceutical products � Furniture

� Sugar

� Wheat � Maize � Rice � Fish frozen � Live animals and meats

Positioning of Mozambique in the International Trade 2016 7

Regarding cash crops, the markets for sugar and cotton are relatively diverse. Sugar is exported al-most entirely to Europe, although split relatively equally between Portugal, Spain and Italy and with smaller volumes going to France and the Nether-lands. Cotton exports go almost entirely to Asia with the biggest volumes going to Indonesia but with

Bangladesh, China, Singapore and Vietnam as im-portant destinations. Over 60 % of the exports of sesame go to China, with the balance exported to various countries mainly in Asia. Finally, India is the principal market for Mozambican cashew nuts ac-counting for over 40% of export volume, but the USA and Canada are also important export destinations.

Figure 2.3: Exports destinations by product (2011-2015 avg.)Destinations of export products - megaproject/extractive resources (2011-2015 avg.)

Aluminium Coal Natural gas Heavy mineral sands

Netherlands83%

Singapore3%

United Kingdom

9%

Other5%

China16%

Italy17%

India22%

USA15%Spain

6%

Other20%

Japan4%

India52%

Other7%

China25%

Singapore16%

Other5%

South Africa95%

Destinations of export products - cash crops (2011-2015 avg.)

Sugar Cotton Sesame Cashew nuts

Netherlands6%

Portugal25%

France6%

Spain24%

Italy22%

Other17%

China14%

Indonesia24%

Bangladesh16%

Other16%

Viet Nam7%

Singapore9%

Mauritius10%

Malaysia4%

South Africa3%

Turkey6%

China61%

Singapore2%

India2%

Japan16%

UAE2%

Other8%

South Africa5%

Canada14%

India43%

USA17%

Lebanon2%

UAE3%

Other16%

Source: UN Comtrade

2.2 Main Cash Crops and Foods Exports

Turning from general trends to look in more detail at specifi c export products, this section will analyse seven key export products for Mozambique: cash-ew, sesame, almonds, cotton, banana, sugar and crustaceans.

Cashew Nuts

Since production began in the early 20th century, cashew nuts have been an important cash crop for Mozambique. In the post war period numerous factories were built for processing cashew nuts for

export. Production peaked in the 70’s when Mozam-bique was the world’s leading exporter of shelled cashew. However, in recent years the volume and quality of cashew nuts produced and exported has declined.

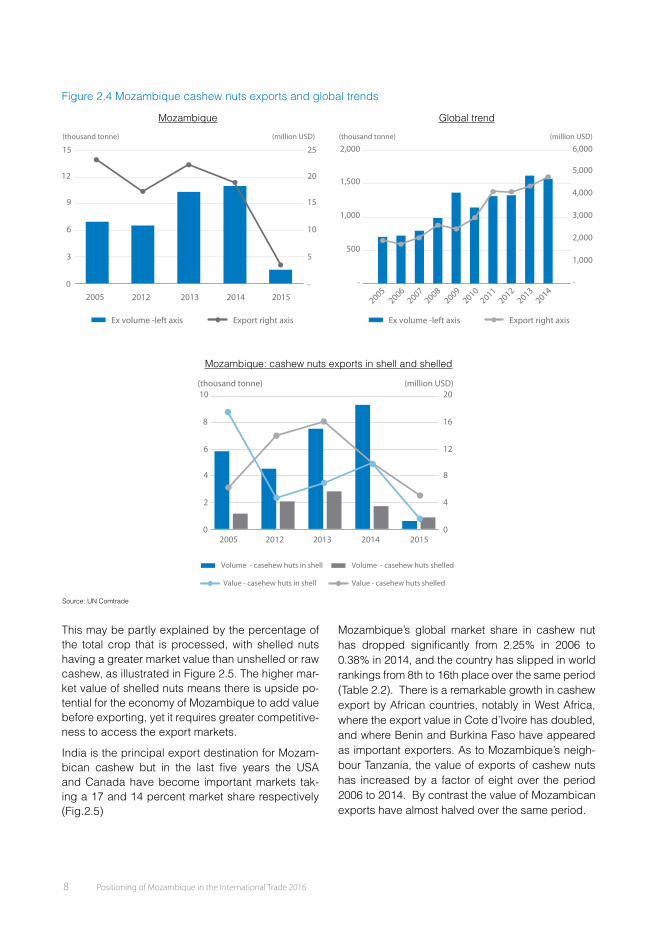

The volume of cashew nuts exported over the pe-riod 2005-2015 has been fl uctuating as export value has sharply declined in 2015 (Fig. 2.4). This shows a marked contrast to global trends where export vol-umes have more than doubled over the same period and export value has increased by almost tenfold.

6 Positioning of Mozambique in the International Trade 2016

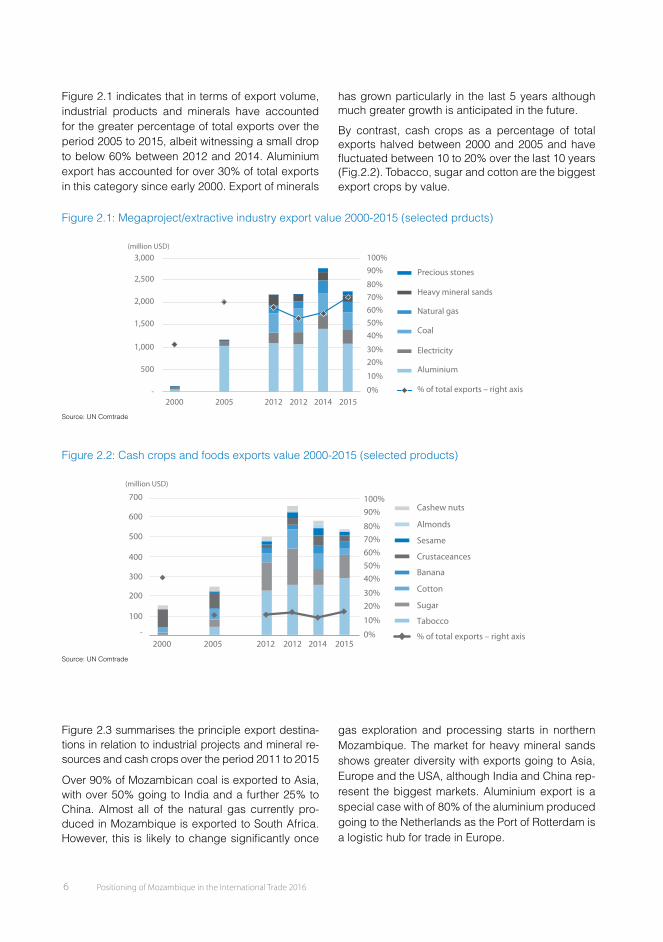

Figure 2.1 indicates that in terms of export volume, industrial products and minerals have accounted for the greater percentage of total exports over the period 2005 to 2015, albeit witnessing a small drop to below 60% between 2012 and 2014. Aluminium export has accounted for over 30% of total exports in this category since early 2000. Export of minerals

has grown particularly in the last 5 years although much greater growth is anticipated in the future.

By contrast, cash crops as a percentage of total exports halved between 2000 and 2005 and have fl uctuated between 10 to 20% over the last 10 years (Fig.2.2). Tobacco, sugar and cotton are the biggest export crops by value.

Figure 2.1: Megaproject/extractive industry export value 2000-2015 (selected prducts)

100%3,000(million USD)

2,500

2,000

1,500

1,000

500

-

Precious stones

Heavy mineral sands

Natural gas

Coal

Electricity

Aluminium

% of total exports – right axis

90%

80%70%60%50%40%

30%20%

10%

0%2000 2005 2012 2012 2014 2015

Source: UN Comtrade

Figure 2.2: Cash crops and foods exports value 2000-2015 (selected products)

100%90%

80%70%60%50%40%

30%20%

10%

0%

700

600

500

400

300

200

100

-

Cashew nuts

Almonds

Sesame

Crustaceances

Cotton

Banana

Sugar

Tabocco

% of total exports – right axis2000 2005 2012 2012 2014 2015

(million USD)

Source: UN Comtrade

Figure 2.3 summarises the principle export destina-tions in relation to industrial projects and mineral re-sources and cash crops over the period 2011 to 2015

Over 90% of Mozambican coal is exported to Asia, with over 50% going to India and a further 25% to China. Almost all of the natural gas currently pro-duced in Mozambique is exported to South Africa. However, this is likely to change signifi cantly once

gas exploration and processing starts in northern Mozambique. The market for heavy mineral sands shows greater diversity with exports going to Asia, Europe and the USA, although India and China rep-resent the biggest markets. Aluminium export is a special case with of 80% of the aluminium produced going to the Netherlands as the Port of Rotterdam is a logistic hub for trade in Europe.

Positioning of Mozambique in the International Trade 2016 7

Regarding cash crops, the markets for sugar and cotton are relatively diverse. Sugar is exported al-most entirely to Europe, although split relatively equally between Portugal, Spain and Italy and with smaller volumes going to France and the Nether-lands. Cotton exports go almost entirely to Asia with the biggest volumes going to Indonesia but with

Bangladesh, China, Singapore and Vietnam as im-portant destinations. Over 60 % of the exports of sesame go to China, with the balance exported to various countries mainly in Asia. Finally, India is the principal market for Mozambican cashew nuts ac-counting for over 40% of export volume, but the USA and Canada are also important export destinations.

Figure 2.3: Exports destinations by product (2011-2015 avg.)Destinations of export products - megaproject/extractive resources (2011-2015 avg.)

Aluminium Coal Natural gas Heavy mineral sands

Netherlands83%

Singapore3%

United Kingdom

9%

Other5%

China16%

Italy17%

India22%

USA15%Spain

6%

Other20%

Japan4%

India52%

Other7%

China25%

Singapore16%

Other5%

South Africa95%

Destinations of export products - cash crops (2011-2015 avg.)

Sugar Cotton Sesame Cashew nuts

Netherlands6%

Portugal25%

France6%

Spain24%

Italy22%

Other17%

China14%

Indonesia24%

Bangladesh16%

Other16%

Viet Nam7%

Singapore9%

Mauritius10%

Malaysia4%

South Africa3%

Turkey6%

China61%

Singapore2%

India2%

Japan16%

UAE2%

Other8%

South Africa5%

Canada14%

India43%

USA17%

Lebanon2%

UAE3%

Other16%

Source: UN Comtrade

2.2 Main Cash Crops and Foods Exports

Turning from general trends to look in more detail at specifi c export products, this section will analyse seven key export products for Mozambique: cash-ew, sesame, almonds, cotton, banana, sugar and crustaceans.

Cashew Nuts

Since production began in the early 20th century, cashew nuts have been an important cash crop for Mozambique. In the post war period numerous factories were built for processing cashew nuts for

export. Production peaked in the 70’s when Mozam-bique was the world’s leading exporter of shelled cashew. However, in recent years the volume and quality of cashew nuts produced and exported has declined.

The volume of cashew nuts exported over the pe-riod 2005-2015 has been fl uctuating as export value has sharply declined in 2015 (Fig. 2.4). This shows a marked contrast to global trends where export vol-umes have more than doubled over the same period and export value has increased by almost tenfold.

Positioning of Mozambique in the International Trade 2016 9

Figure 2.5: Mozambique cashew nuts export destinations

2006-2010 Average 2011-2015 Average

South Africa7%

India50%

USA7%

Lebanon2%

UAE1%

Other13%

Netherlands20%

South Africa5%

Canada14%

India43%

USA17%

Lebanon2%

UAE3%

Other16%

Source: UN Comtrade

Table 2.2: Cashew nuts export world ranking

2006 ranking Exports value (USD) 2014 ranking Exports value (USD)

1 India 544,229,716 1 Viet Nam 1,931,387,530

2 Viet Nam 455,763,308 2 India 883,240,879

3 Brazil 187,538,588 3 Cote d’Ivoire 818,171,096

4 Netherlands 107,124,478 4 Tanzania 391,880,956

5 Cote d’Ivoire 92,376,962 5 Netherlands 199,009,852

6 Indonesia 56,584,795 6 Brazil 110,302,452

7 Tanzania 49,900,621 7 Indonesia 103,642,649

8 Mozambique 36,688,195 8 Nigeria 91,662,971

9 Benin 16,553,863 9 UAE 90,739,498

10 Belgium 16,342,431 10 Germany 68,597,104

11 USA 12,775,166 11 Benin 65,149,698

12 Germany 9,148,000 12 Burkina Faso 42,951,571

13 Ghana 9,012,535 13 Belgium 29,418,299

14 Italy 7,495,788 14 Guinea 23,445,523

15 United Kingdom 6,173,580 15 Singapore 19,222,269

16 Singapore 3,770,318 16 Mozambique 19,092,930

17 Kenya 3,258,871 17 USA 16,441,894

18 Hong Kong 1,742,720 18 United Kingdom 15,997,026

19 Greece 1,682,427 19 Italy 11,712,756

20 Sri Lanka 1,148,251 20 Austria 6,644,115

World Total 1,632,531,586 World Total 4,994,341,256

Mozambique % 2.25% Mozambique % 0.38%

Source: UN Comtrade

Sesame

Mozambican farmers have been encouraged to produce sesame as the price paid for the product

is considered more favourable to that of other more traditional cash crops such as cotton and tobacco.

8 Positioning of Mozambique in the International Trade 2016

Figure 2.4 Mozambique cashew nuts exports and global trends

Mozambique Global trend

-

5

10

15

20

25

0

3

6

9

12

15

(thousand tonne) (million USD)

2005 2012 2013 2014 2015

Ex volume -left axis Export right axis Ex volume -left axis Export right axis

-

1,000

2,000

3,000

4,000

5,000

6,000

-

500

1,000

1,500

2,000(thousand tonne) (million USD)

20052006

20072008

20092010

20112012

20132014

Mozambique: cashew nuts exports in shell and shelled

0

4

8

12

16

20

0

2

4

6

8

10

2005 2012 2013 2014 2015

Volume - casehew huts in shell Volume - casehew huts shelled

Value - casehew huts in shell Value - casehew huts shelled

(thousand tonne) (million USD)

Source: UN Comtrade

This may be partly explained by the percentage of the total crop that is processed, with shelled nuts having a greater market value than unshelled or raw cashew, as illustrated in Figure 2.5. The higher mar-ket value of shelled nuts means there is upside po-tential for the economy of Mozambique to add value before exporting, yet it requires greater competitive-ness to access the export markets.

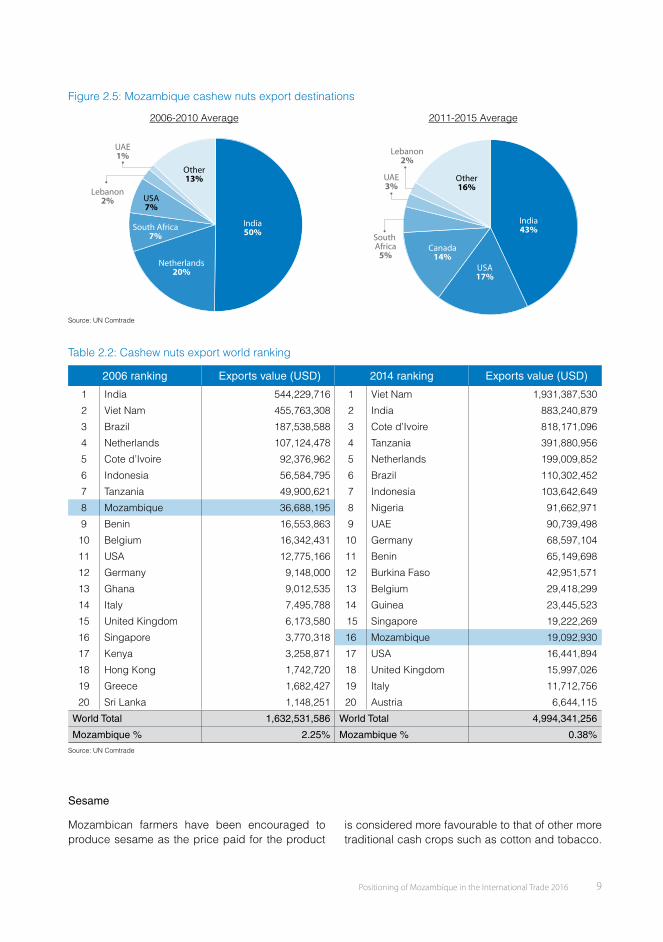

India is the principal export destination for Mozam-bican cashew but in the last fi ve years the USA and Canada have become important markets tak-ing a 17 and 14 percent market share respectively (Fig.2.5)

Mozambique’s global market share in cashew nut has dropped signifi cantly from 2.25% in 2006 to 0.38% in 2014, and the country has slipped in world rankings from 8th to 16th place over the same period (Table 2.2). There is a remarkable growth in cashew export by African countries, notably in West Africa, where the export value in Cote d’Ivoire has doubled, and where Benin and Burkina Faso have appeared as important exporters. As to Mozambique’s neigh-bour Tanzania, the value of exports of cashew nuts has increased by a factor of eight over the period 2006 to 2014. By contrast the value of Mozambican exports have almost halved over the same period.

Positioning of Mozambique in the International Trade 2016 9

Figure 2.5: Mozambique cashew nuts export destinations

2006-2010 Average 2011-2015 Average

South Africa7%

India50%

USA7%

Lebanon2%

UAE1%

Other13%

Netherlands20%

South Africa5%

Canada14%

India43%

USA17%

Lebanon2%

UAE3%

Other16%

Source: UN Comtrade

Table 2.2: Cashew nuts export world ranking

2006 ranking Exports value (USD) 2014 ranking Exports value (USD)

1 India 544,229,716 1 Viet Nam 1,931,387,530

2 Viet Nam 455,763,308 2 India 883,240,879

3 Brazil 187,538,588 3 Cote d’Ivoire 818,171,096

4 Netherlands 107,124,478 4 Tanzania 391,880,956

5 Cote d’Ivoire 92,376,962 5 Netherlands 199,009,852

6 Indonesia 56,584,795 6 Brazil 110,302,452

7 Tanzania 49,900,621 7 Indonesia 103,642,649

8 Mozambique 36,688,195 8 Nigeria 91,662,971

9 Benin 16,553,863 9 UAE 90,739,498

10 Belgium 16,342,431 10 Germany 68,597,104

11 USA 12,775,166 11 Benin 65,149,698

12 Germany 9,148,000 12 Burkina Faso 42,951,571

13 Ghana 9,012,535 13 Belgium 29,418,299

14 Italy 7,495,788 14 Guinea 23,445,523

15 United Kingdom 6,173,580 15 Singapore 19,222,269

16 Singapore 3,770,318 16 Mozambique 19,092,930

17 Kenya 3,258,871 17 USA 16,441,894

18 Hong Kong 1,742,720 18 United Kingdom 15,997,026

19 Greece 1,682,427 19 Italy 11,712,756

20 Sri Lanka 1,148,251 20 Austria 6,644,115

World Total 1,632,531,586 World Total 4,994,341,256

Mozambique % 2.25% Mozambique % 0.38%

Source: UN Comtrade

Sesame

Mozambican farmers have been encouraged to produce sesame as the price paid for the product

is considered more favourable to that of other more traditional cash crops such as cotton and tobacco.

Positioning of Mozambique in the International Trade 2016 11

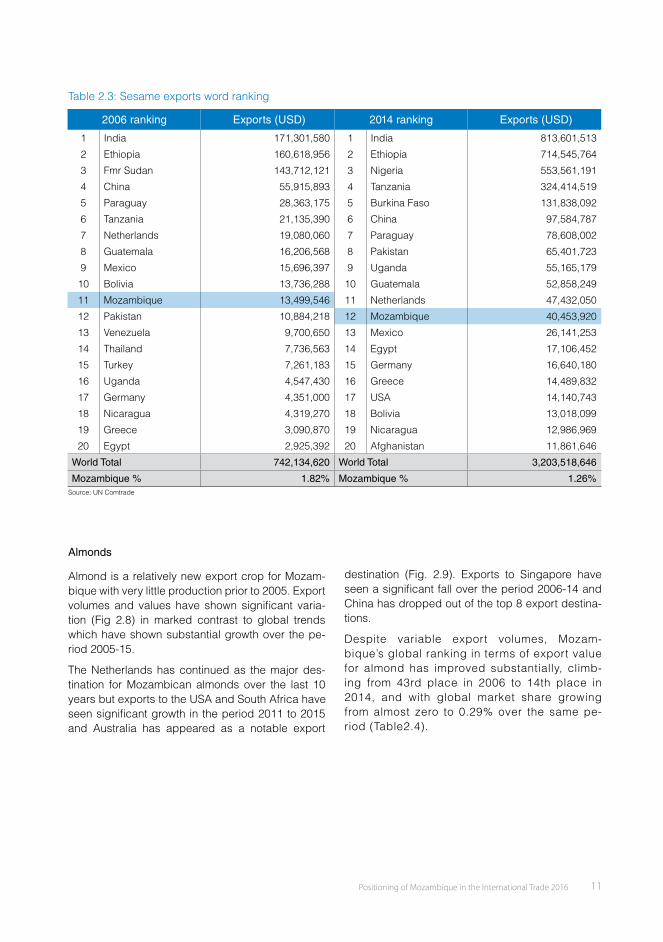

Table 2.3: Sesame exports word ranking

2006 ranking Exports (USD) 2014 ranking Exports (USD)

1 India 171,301,580 1 India 813,601,513

2 Ethiopia 160,618,956 2 Ethiopia 714,545,764

3 Fmr Sudan 143,712,121 3 Nigeria 553,561,191

4 China 55,915,893 4 Tanzania 324,414,519

5 Paraguay 28,363,175 5 Burkina Faso 131,838,092

6 Tanzania 21,135,390 6 China 97,584,787

7 Netherlands 19,080,060 7 Paraguay 78,608,002

8 Guatemala 16,206,568 8 Pakistan 65,401,723

9 Mexico 15,696,397 9 Uganda 55,165,179

10 Bolivia 13,736,288 10 Guatemala 52,858,249

11 Mozambique 13,499,546 11 Netherlands 47,432,050

12 Pakistan 10,884,218 12 Mozambique 40,453,920

13 Venezuela 9,700,650 13 Mexico 26,141,253

14 Thailand 7,736,563 14 Egypt 17,106,452

15 Turkey 7,261,183 15 Germany 16,640,180

16 Uganda 4,547,430 16 Greece 14,489,832

17 Germany 4,351,000 17 USA 14,140,743

18 Nicaragua 4,319,270 18 Bolivia 13,018,099

19 Greece 3,090,870 19 Nicaragua 12,986,969

20 Egypt 2,925,392 20 Afghanistan 11,861,646

World Total 742,134,620 World Total 3,203,518,646

Mozambique % 1.82% Mozambique % 1.26%Source: UN Comtrade

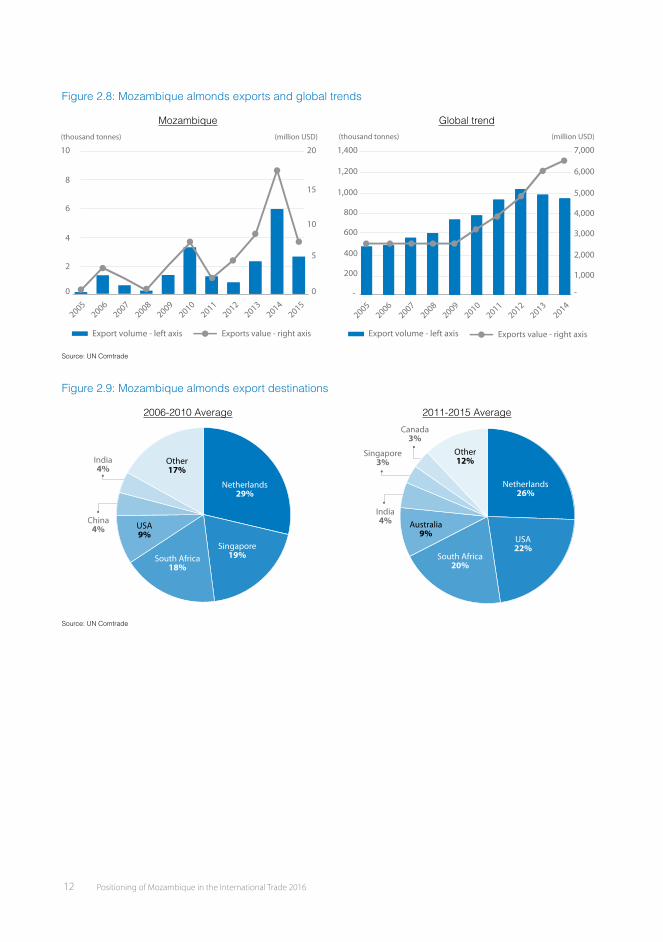

Almonds

Almond is a relatively new export crop for Mozam-bique with very little production prior to 2005. Export volumes and values have shown signifi cant varia-tion (Fig 2.8) in marked contrast to global trends which have shown substantial growth over the pe-riod 2005-15.

The Netherlands has continued as the major des-tination for Mozambican almonds over the last 10 years but exports to the USA and South Africa have seen signifi cant growth in the period 2011 to 2015 and Australia has appeared as a notable export

destination (Fig. 2.9). Exports to Singapore have seen a signifi cant fall over the period 2006-14 and China has dropped out of the top 8 export destina-tions.

Despite variable export volumes, Mozam-bique’s global ranking in terms of export value for almond has improved substantially, climb-ing from 43rd place in 2006 to 14th place in 2014, and with global market share growing from almost zero to 0.29% over the same pe-riod (Table2.4).

10 Positioning of Mozambique in the International Trade 2016

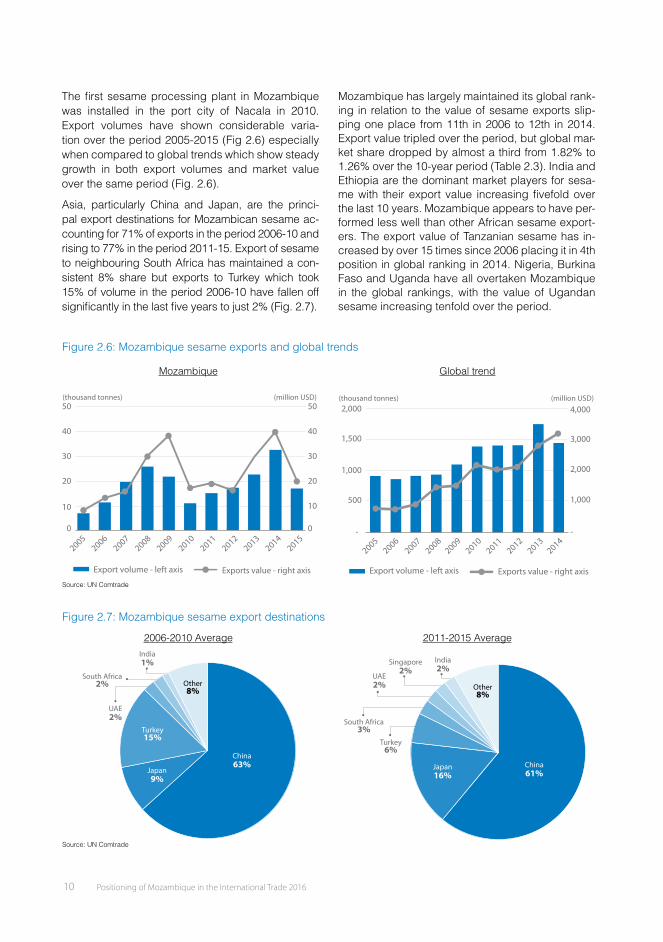

The fi rst sesame processing plant in Mozambique was installed in the port city of Nacala in 2010. Export volumes have shown considerable varia-tion over the period 2005-2015 (Fig 2.6) especially when compared to global trends which show steady growth in both export volumes and market value over the same period (Fig. 2.6).

Asia, particularly China and Japan, are the princi-pal export destinations for Mozambican sesame ac-counting for 71% of exports in the period 2006-10 and rising to 77% in the period 2011-15. Export of sesame to neighbouring South Africa has maintained a con-sistent 8% share but exports to Turkey which took 15% of volume in the period 2006-10 have fallen off signifi cantly in the last fi ve years to just 2% (Fig. 2.7).

Mozambique has largely maintained its global rank-ing in relation to the value of sesame exports slip-ping one place from 11th in 2006 to 12th in 2014. Export value tripled over the period, but global mar-ket share dropped by almost a third from 1.82% to 1.26% over the 10-year period (Table 2.3). India and Ethiopia are the dominant market players for sesa-me with their export value increasing fi vefold over the last 10 years. Mozambique appears to have per-formed less well than other African sesame export-ers. The export value of Tanzanian sesame has in-creased by over 15 times since 2006 placing it in 4th position in global ranking in 2014. Nigeria, Burkina Faso and Uganda have all overtaken Mozambique in the global rankings, with the value of Ugandan sesame increasing tenfold over the period.

Figure 2.6: Mozambique sesame exports and global trends

Mozambique Global trend

Export volume - left axis Exports value - right axis

0

10

20

30

40

50(thousand tonnes) (million USD)

0

10

20

30

40

50

20052006

20072008

20092010

20112012

20132014

2015

Export volume - left axis Exports value - right axis

- -

500

1,000

1,500

2,000(thousand tonnes) (million USD)

1,000

2,000

3,000

4,000

20052006

20072008

20092010

20112012

20132014

Source: UN Comtrade

Figure 2.7: Mozambique sesame export destinations

2006-2010 Average 2011-2015 Average

South Africa2%

Turkey15%

China63%

India1%

Japan9%

UAE2%

Other8%

South Africa3%

Turkey6%

China61%

Singapore2%

India2%

Japan16%

UAE2% Other

8%

Source: UN Comtrade

Positioning of Mozambique in the International Trade 2016 11

Table 2.3: Sesame exports word ranking

2006 ranking Exports (USD) 2014 ranking Exports (USD)

1 India 171,301,580 1 India 813,601,513

2 Ethiopia 160,618,956 2 Ethiopia 714,545,764

3 Fmr Sudan 143,712,121 3 Nigeria 553,561,191

4 China 55,915,893 4 Tanzania 324,414,519

5 Paraguay 28,363,175 5 Burkina Faso 131,838,092

6 Tanzania 21,135,390 6 China 97,584,787

7 Netherlands 19,080,060 7 Paraguay 78,608,002

8 Guatemala 16,206,568 8 Pakistan 65,401,723

9 Mexico 15,696,397 9 Uganda 55,165,179

10 Bolivia 13,736,288 10 Guatemala 52,858,249

11 Mozambique 13,499,546 11 Netherlands 47,432,050

12 Pakistan 10,884,218 12 Mozambique 40,453,920

13 Venezuela 9,700,650 13 Mexico 26,141,253

14 Thailand 7,736,563 14 Egypt 17,106,452

15 Turkey 7,261,183 15 Germany 16,640,180

16 Uganda 4,547,430 16 Greece 14,489,832

17 Germany 4,351,000 17 USA 14,140,743

18 Nicaragua 4,319,270 18 Bolivia 13,018,099

19 Greece 3,090,870 19 Nicaragua 12,986,969

20 Egypt 2,925,392 20 Afghanistan 11,861,646

World Total 742,134,620 World Total 3,203,518,646

Mozambique % 1.82% Mozambique % 1.26%Source: UN Comtrade

Almonds

Almond is a relatively new export crop for Mozam-bique with very little production prior to 2005. Export volumes and values have shown signifi cant varia-tion (Fig 2.8) in marked contrast to global trends which have shown substantial growth over the pe-riod 2005-15.

The Netherlands has continued as the major des-tination for Mozambican almonds over the last 10 years but exports to the USA and South Africa have seen signifi cant growth in the period 2011 to 2015 and Australia has appeared as a notable export

destination (Fig. 2.9). Exports to Singapore have seen a signifi cant fall over the period 2006-14 and China has dropped out of the top 8 export destina-tions.

Despite variable export volumes, Mozam-bique’s global ranking in terms of export value for almond has improved substantially, climb-ing from 43rd place in 2006 to 14th place in 2014, and with global market share growing from almost zero to 0.29% over the same pe-riod (Table2.4).

Positioning of Mozambique in the International Trade 2016 13

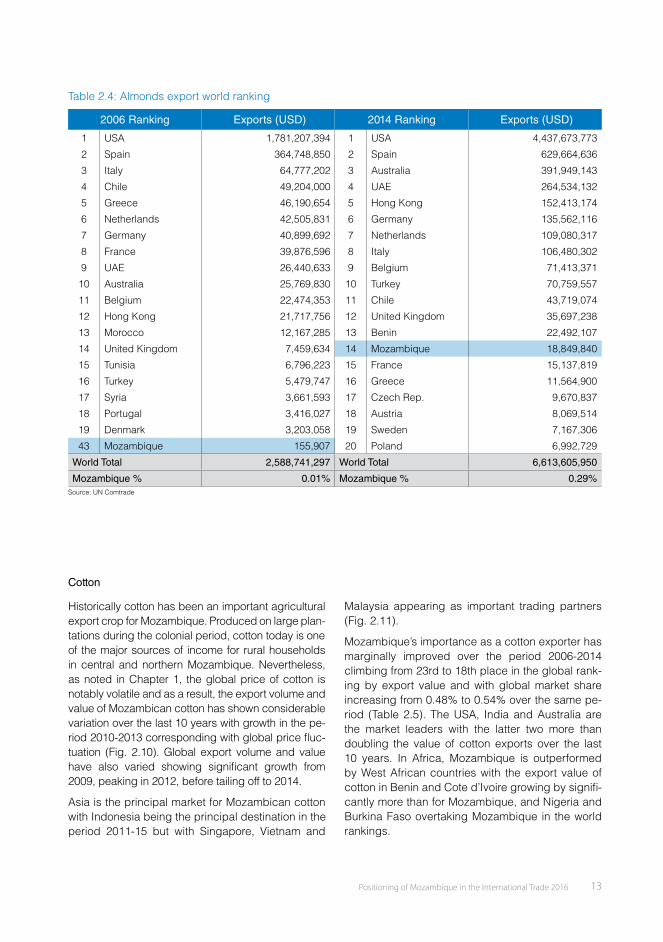

Table 2.4: Almonds export world ranking

2006 Ranking Exports (USD) 2014 Ranking Exports (USD)

1 USA 1,781,207,394 1 USA 4,437,673,773

2 Spain 364,748,850 2 Spain 629,664,636

3 Italy 64,777,202 3 Australia 391,949,143

4 Chile 49,204,000 4 UAE 264,534,132

5 Greece 46,190,654 5 Hong Kong 152,413,174

6 Netherlands 42,505,831 6 Germany 135,562,116

7 Germany 40,899,692 7 Netherlands 109,080,317

8 France 39,876,596 8 Italy 106,480,302

9 UAE 26,440,633 9 Belgium 71,413,371

10 Australia 25,769,830 10 Turkey 70,759,557

11 Belgium 22,474,353 11 Chile 43,719,074

12 Hong Kong 21,717,756 12 United Kingdom 35,697,238

13 Morocco 12,167,285 13 Benin 22,492,107

14 United Kingdom 7,459,634 14 Mozambique 18,849,840

15 Tunisia 6,796,223 15 France 15,137,819

16 Turkey 5,479,747 16 Greece 11,564,900

17 Syria 3,661,593 17 Czech Rep. 9,670,837

18 Portugal 3,416,027 18 Austria 8,069,514

19 Denmark 3,203,058 19 Sweden 7,167,306

43 Mozambique 155,907 20 Poland 6,992,729

World Total 2,588,741,297 World Total 6,613,605,950

Mozambique % 0.01% Mozambique % 0.29%Source: UN Comtrade

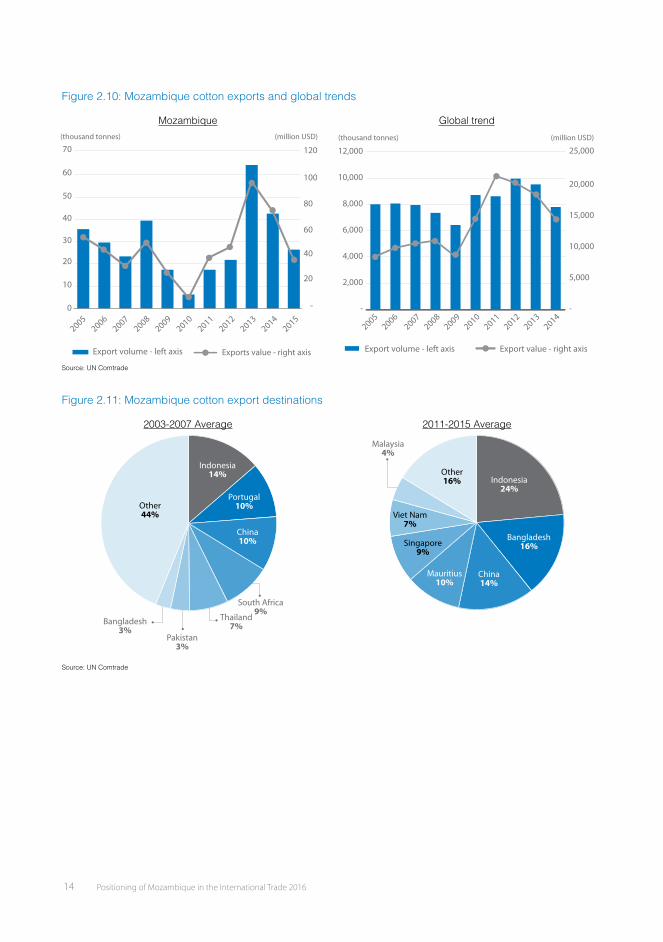

Cotton

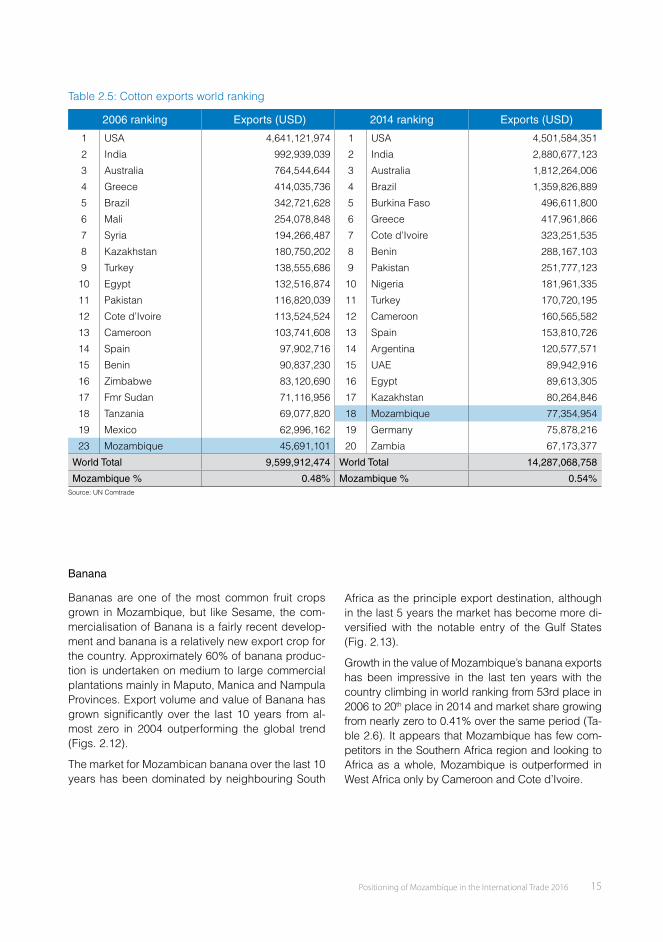

Historically cotton has been an important agricultural export crop for Mozambique. Produced on large plan-tations during the colonial period, cotton today is one of the major sources of income for rural households in central and northern Mozambique. Nevertheless, as noted in Chapter 1, the global price of cotton is notably volatile and as a result, the export volume and value of Mozambican cotton has shown considerable variation over the last 10 years with growth in the pe-riod 2010-2013 corresponding with global price fl uc-tuation (Fig. 2.10). Global export volume and value have also varied showing signifi cant growth from 2009, peaking in 2012, before tailing off to 2014.

Asia is the principal market for Mozambican cotton with Indonesia being the principal destination in the period 2011-15 but with Singapore, Vietnam and

Malaysia appearing as important trading partners (Fig. 2.11).

Mozambique’s importance as a cotton exporter has marginally improved over the period 2006-2014 climbing from 23rd to 18th place in the global rank-ing by export value and with global market share increasing from 0.48% to 0.54% over the same pe-riod (Table 2.5). The USA, India and Australia are the market leaders with the latter two more than doubling the value of cotton exports over the last 10 years. In Africa, Mozambique is outperformed by West African countries with the export value of cotton in Benin and Cote d’Ivoire growing by signifi -cantly more than for Mozambique, and Nigeria and Burkina Faso overtaking Mozambique in the world rankings.

12 Positioning of Mozambique in the International Trade 2016

Figure 2.8: Mozambique almonds exports and global trends

Mozambique Global trend

Export volume - left axis Exports value - right axis

0

2

4

6

8

10

0

5

10

15

20

20052006

20072008

20092010

20112012

20132014

2015

(thousand tonnes) (million USD)

Export volume - left axis Exports value - right axis

20052006

20072008

20092010

20112012

20132014

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

-

200

400

600

800

1,000

1,200

1,400

(thousand tonnes) (million USD)

Source: UN Comtrade

Figure 2.9: Mozambique almonds export destinations

2006-2010 Average 2011-2015 Average

South Africa18%

China4%

India4%

Other17%

Netherlands29%

Singapore19%

USA9%

Canada3%

South Africa20%

India4%

Other12%

Netherlands26%

Australia9%

Singapore3%

USA22%

Source: UN Comtrade

Positioning of Mozambique in the International Trade 2016 13

Table 2.4: Almonds export world ranking

2006 Ranking Exports (USD) 2014 Ranking Exports (USD)

1 USA 1,781,207,394 1 USA 4,437,673,773

2 Spain 364,748,850 2 Spain 629,664,636

3 Italy 64,777,202 3 Australia 391,949,143

4 Chile 49,204,000 4 UAE 264,534,132

5 Greece 46,190,654 5 Hong Kong 152,413,174

6 Netherlands 42,505,831 6 Germany 135,562,116

7 Germany 40,899,692 7 Netherlands 109,080,317

8 France 39,876,596 8 Italy 106,480,302

9 UAE 26,440,633 9 Belgium 71,413,371

10 Australia 25,769,830 10 Turkey 70,759,557

11 Belgium 22,474,353 11 Chile 43,719,074

12 Hong Kong 21,717,756 12 United Kingdom 35,697,238

13 Morocco 12,167,285 13 Benin 22,492,107

14 United Kingdom 7,459,634 14 Mozambique 18,849,840

15 Tunisia 6,796,223 15 France 15,137,819

16 Turkey 5,479,747 16 Greece 11,564,900

17 Syria 3,661,593 17 Czech Rep. 9,670,837

18 Portugal 3,416,027 18 Austria 8,069,514

19 Denmark 3,203,058 19 Sweden 7,167,306

43 Mozambique 155,907 20 Poland 6,992,729

World Total 2,588,741,297 World Total 6,613,605,950

Mozambique % 0.01% Mozambique % 0.29%Source: UN Comtrade

Cotton

Historically cotton has been an important agricultural export crop for Mozambique. Produced on large plan-tations during the colonial period, cotton today is one of the major sources of income for rural households in central and northern Mozambique. Nevertheless, as noted in Chapter 1, the global price of cotton is notably volatile and as a result, the export volume and value of Mozambican cotton has shown considerable variation over the last 10 years with growth in the pe-riod 2010-2013 corresponding with global price fl uc-tuation (Fig. 2.10). Global export volume and value have also varied showing signifi cant growth from 2009, peaking in 2012, before tailing off to 2014.

Asia is the principal market for Mozambican cotton with Indonesia being the principal destination in the period 2011-15 but with Singapore, Vietnam and

Malaysia appearing as important trading partners (Fig. 2.11).