portfolio strategies bear-mauled portfolio: makeover for a … · figure 1 is a “scatterplot,”...

TRANSCRIPT

Port

folio S

trat

egie

s

AAII Journal4

Makeover for a

Bear-Mauled Portfolio:

How to Create a Winning Game Plan

By Vern C. Hayden

L ike a desert mirage, the stock market shim-mered its way through the dream merchants ofWall Street to investors all over America.For example, on March 10,2000, Merrill Lynch introduced,with great fanfare, their brandnew Internet fund—joining thetech feeding frenzy the day theNasdaq hit a peak of 5028 andstarted to crash. It gives new mean-ing to the old cliché “timing is ev-erything.”

In January of 2002, Herband Jocelyn Edwards (fictitiousnames, but real circumstances)walked into my office withwhat was left of a portfolio ofmutual funds. They had bought into thehype of the times, and then suffered as the bear marketstarted to trash their lifetime of savings.

Their experience has a number of important lessonsthat other investors can readily learn from.

Their original investment was about $450,000 whenthey went to a stockbroker for advice on investing theirassets. But when they walked into my office, the then-current value was about $210,000, for a loss of about 53%.

Keep in mind that to recover from a 53% loss, aninvestor has to make 114% just to get back to even again.

One look at their portfolio, and you could see it was aticking time-bomb, ready to blow up the moment themarket turned south—which it did.

The Edwards’ portfolio is shown in Table 1, but it isalso depicted in the graph in Figure 1, giving a much better

“picture” of their portfolio.Figure 1 is a “scatterplot,” which

reflects various pieces of informationover, in this instance, a three-year pe-riod.

The horizontal (x) axis represents“standard deviation.” This is a mea-sure of the risk of any portfolio—

an individual mutual fund, or anentire portfolio of mutualfunds. Standard deviation mea-

sures volatility, and the higherthe number, the higher the risk.

So, if you go from left to rightacross the chart, you are going

from lower risk to higher risk.The vertical (y) axis of the chart

indicates return—the numbers range from lower returns atthe bottom to higher returns at the top.

The square box in the middle of the scatterplot repre-sents the benchmark portfolio, in this instance the S&P 500(this isn’t necessarily the perfect index for an entire portfolio,but I’m using it as a convenience for this article). As you cansee, the index has a standard deviation of about 17.26 andthe return has averaged –8.29% annually over the last threeyears through October 2003.

If you draw vertical and horizontal lines through thebenchmark, you create four sections of the scatterplot, indi-cating:

Upper left: Higher return and lower risk relative to thebenchmark;Lower left: Lower return and lower risk relative to thebenchmark;

January 2004 5

Upper right: Higher return and higherrisk relative to the benchmark; andLower right: Lower return andhigher risk relative to the benchmark.

The most desirable sector to be inis the upper left because it indicatesyour portfolio had higher returns withlower risk relative to the market.

I like to use scatterplots becausethey graphically depict how the variouselements of a portfolio are workingtogether. It is possible, for example, ineven a conservative portfolio, to havesome holdings that are much higherrisk—located on the right-hand side ofthe scatterplot—as long as they are bal-anced by less risky holdings, with theoverall portfolio in the upper-left sec-tion of the scatterplot.

Of course, it is important to re-member that this is a snapshot of howthe portfolio operated in the past, andthere is no guarantee performance willbe repeated in the future. But lookingat how a portfolio performed histori-cally is a good way to get your bear-ings.

In the Edwards’ scatterplot in Fig-ure 1, the clear round circles representtheir individual fund holdings; the solidblack dot is their overall portfolio ofmutual funds. (Various portfolio soft-ware programs can perform this kindof function; I use Morningstar Principiasoftware.)

You can see that the Edwards’portfolio at that time was in the lower

right-hand corner, the least desirablesection of the scatterplot—it took onmore risk than the S&P 500, yet itproduced a lower return. The risk fac-tor (standard deviation) of the portfo-lio is about 29.09, significantly morethan the S&P 500. The return of theportfolio was in the lower right at–16.94% for each of the three years—it had significantly more loss than theS&P 500 index.

Obviously, this wasn’t a desirableportfolio, and the scatterplot empha-sized that from a quantitative stand-point.

What Went Wrong?

Before beginning the makeover of

the Edwards’ portfolio,there are important les-sons to be learned fromwhat went wrong:

1) The Edwards didn’thave a game plan that wasbased on their long-terminvestor profile.

Lesson: Make sure your gameplan is based on your investorprofile. Your profile con-sists of at least three im-portant ingredients: Whatis your timeframe (howmuch time do you havebefore you will need the

money)? What are your financialgoals? And, how much risk canyou live with? If you know howmuch money it will take to achievea goal and you know your invest-ment timeframe, then you can fig-ure out what kind of return youneed to achieve your goals andwhether that return is achievablegiven your tolerance for risk. Next,you need to determine if the re-turn you need is reasonable. Formost planning purposes, I use a7% to 8% rate of return as areasonable maximum for long-term stock investing.

2) They did not correctly analyze theirrisk tolerance. With most of their

Table 1. The Edwards’ Original Mutual Fund Portfolio

3-YearAvg Annual

Portfolio Allocation Return*Fund Category ($) (%) (%)Firsthand Tech Value Tech 30,000 14.29 –77.89Dreyfus Premier Tech Growth B Tech 50,000 23.81 –71.66Putnam Int’l Capital Opp B Growth 40,000 19.05 –45.00Seligman Henderson Gl Tech B Tech 30,000 14.29 –63.37Alliance Bernstein Premier Gr B Growth 20,000 9.52 –58.78Calamos Growth Growth 25,000 11.90 –1.69MFS Mid Cap Growth Growth 15,000 7.14 –54.73

$210,000

*Through year-end 2002.

Figure 1. The Edwards’ Original Portfolio

17.26 29.09 50.00–35.0

–31.1

–27.2

–23.3

–19.4

–15.5

–11.6

–7.7

–3.8

0.1

4.0

3 Year Standard Deviation

3 Year Average Return

Lower Risk Higher Risk

Lower Return

Higher Return

This quadrant means Higher Risk and Lower Return

Original Portfolio

Portfolio Individual Holding Benchmark

AAII Journal6

Portfolio Strategies

portfolio in aggressive growth,their game plan can best be de-scribed as only having an “of-fense.” You can’t win any gamewith pure “offense.” Boxed be-low are two hypothetical portfo-lios. Most people would havepulled out of the offensive port-folio after it was down around50% and suffered a significant loss.They would probably also lose

some sleep over it. However, aportfolio with an offense and de-fense and even 10% annual returnswould let the investor sleep at night.Such an investor would probablystay in the market and have almostthe same gain in their portfolio asan extremely volatile one.

Lesson: Start with a portfolio allocationthat takes into consideration your risktolerance and leads to providing a goodoffense and defense.

3) With the price-earnings ratio ofthe portfolio at about 60 in 1999,they ignored the time-proven valu-ations of the market. Yet, one ofthe red flags of a charging bullmarket is the overvaluation ofstock. The buzz of the hyper bullmarket was: “Things are differentnow” and “we’re in a neweconomy—if it goes down, it will

come back up!” Yardsticks likethe price-earnings ratio, price-to-book ratio, and dividend yield allwent out the window.

Lesson: Don’t let time-proven traditionsbased on proven fundamentals get swal-lowed up during “unfashionable” mo-ments. The S&P 500 index is over-valued by traditional measureswhen its price-earnings ratio is over

15 to 18; thep r i c e - t o -book value“safe” num-ber is consid-ered to bearound 2.5.Currently, theS&P 500’s

price-earnings ratio is over 20, andits price-to-book is now over 4.So, even to-day, we are inan overval-ued situation,which meansyou have tokeep an eyeon the fun-damentals. Inother words,just becausewe have hada great ninem o n t h s ,keep yourdefense ingood shape.

4) Their portfo-lio wash e a v i l yweighted in

technology—itwas an “emo-tional” portfolio:Back in 1999, ifyou weren’t intechnology youhad no status atcocktail parties—everybody was onboard the techbandwagon. The

smartest people’s minds were leftat the door of the fervent greed-driven market.

Lesson: Leave your emotions at the door,listen to your mind and use it to balanceagainst greed and fear.

5) They thought it was easy: All youhad to do was throw your moneyat tech.

Lesson: It is NEVER easy; in fact it’shard work. You either need to spenda lot of time doing it yourself (andyou can) or spend some moneyto find a good advisor to do itfor you.

The Makeover Game Plan

In general, I divide investors into

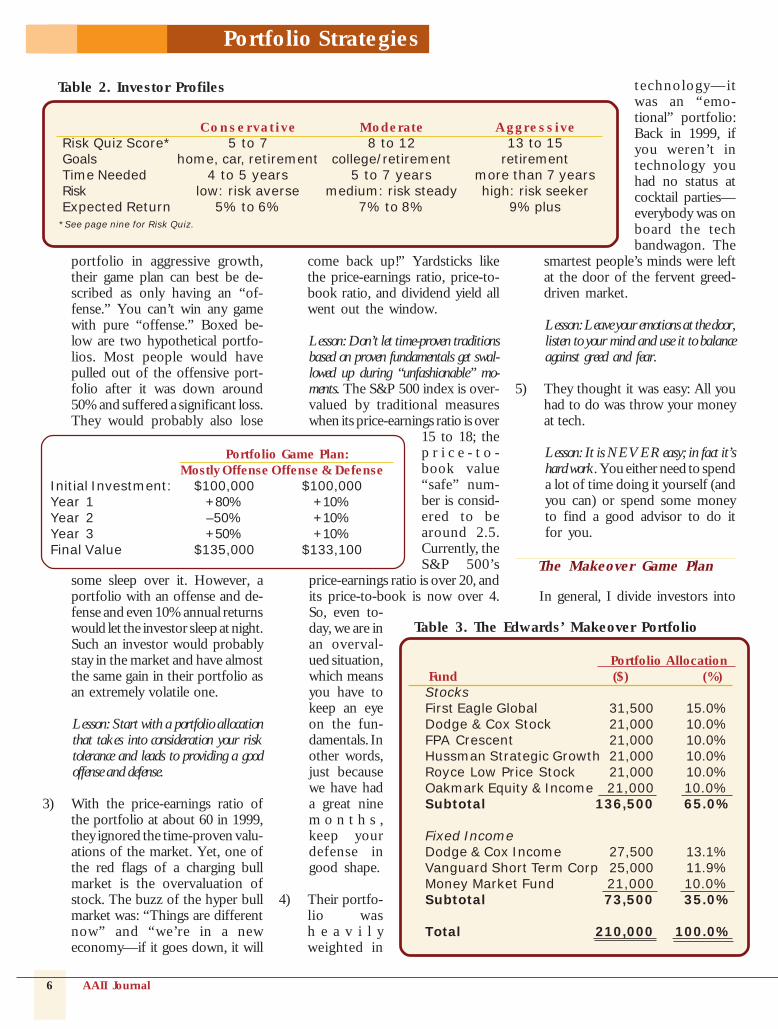

Table 2. Investor Profiles

Conserva t i ve Moderate Aggress iveRisk Quiz Score* 5 to 7 8 to 12 13 to 15Goals home, car, retirement college/retirement retirementTime Needed 4 to 5 years 5 to 7 years more than 7 yearsRisk low: risk averse medium: risk steady high: risk seekerExpected Return 5% to 6% 7% to 8% 9% plus

Table 3. The Edwards’ Makeover Portfolio

Portfolio AllocationFund ($) (%)StocksFirst Eagle Global 31,500 15.0%Dodge & Cox Stock 21,000 10.0%FPA Crescent 21,000 10.0%Hussman Strategic Growth 21,000 10.0%Royce Low Price Stock 21,000 10.0%Oakmark Equity & Income 21,000 10.0%Subtotal 136,500 65.0%

Fixed IncomeDodge & Cox Income 27,500 13.1%Vanguard Short Term Corp 25,000 11.9%Money Market Fund 21,000 10.0%Subtotal 73,500 35.0%

Total 210,000 100.0%

Portfolio Game Plan:Mostly Offense Offense & Defense

Initial Investment: $100,000 $100,000Year 1 +80% +10%Year 2 –50% +10%Year 3 +50% +10%Final Value $135,000 $133,100

*See page nine for Risk Quiz.

January 2004 7

three basic profiles: conservative, mod-erate, and aggressive—with character-istics that are summarized in Table 2.

To makeover the Edwards’ port-folio, we went through a discoveryprocess to determine their investor pro-file. The process included goal-setting,timeframe analysis and risk tolerance analy-sis.

The basic objective was to meet aretirement goal in 15 years, since the kids’education was already taken care of.

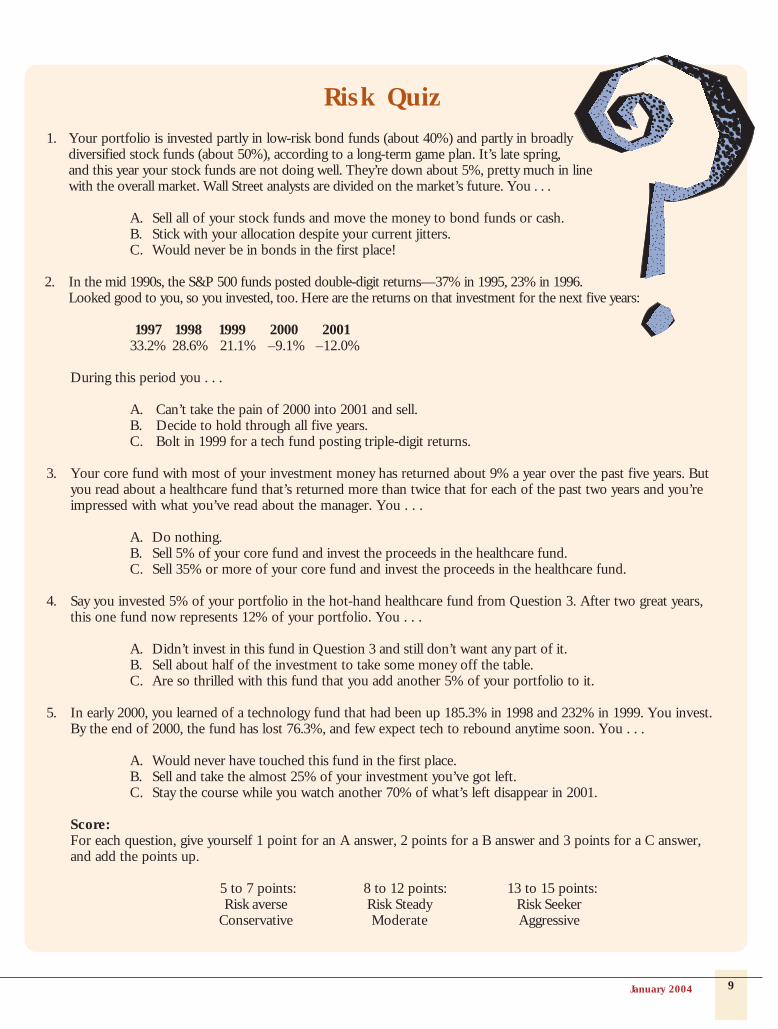

Risk tolerance analysis included ex-tensive discussions and tests to deter-mine the Edwards’ risk profile. Ex-amples of the kinds of questions thatneed to be considered in any risk analy-sis are presented in the Risk Quiz onpage nine.

After testing and discussion of risktolerance, we agreed that a portfoliowith moderate risk would be appro-priate.

The Edwards most closely fit intothe moderate investor profile. Althoughthey had a retirement goal that was 15years down the road, they clearly didnot have the staying power to ride outthe volatility inherent in an aggressiveportfolio.

While the moderate portfolio wasour target, we didn’t immediately imple-ment it. The Edwards were severelybruised and losing sleep, so we de-clared a “time out.” The first thing wedid for the Edwards was sell every-thing and park the entire sum of moneyin money market and bond funds. Therewere no taxes because there were lossesrather than gains. In fact, they havelosses to carry forward. And there wereno commissions. There were some feesthat totalled roughly $300.

The typical “game plan” (alloca-tion) that I use for moderate allocationshas an “offense” that uses stock for65% of the portfolio; the remaining35% of the portfolio is the “defense,”with 25% in bond funds and 10% in amoney market fund. Of the 65% instock funds, the majority is placed withvalue or blend managers.

A value manager is one who as-sesses the intrinsic value of a companyand will buy the stock only when it is30% to 50% discounted from that value;a growth manager pays more attentionto the expected growth of the stock,and if they sense momentum in theprice, they may buy it. A blend man-

ager combines the best of both worlds.

Player Criteria

Now it’s time to pick the playersfor the Edwards’ portfolio—the indi-vidual mutual funds. Here are someguidelines for picking a suitable fund:

StyleTry to vary the style, since value

and growth perform differently duringvarious time periods. The value man-agers are generally safer during weakmarkets. Growth managers generallywill do better in up markets.

Performance• The first thing to look for in

performance figures is how a fund faredduring bad years. Check out 1987, 1990,1994, 2000, 2001, and 2002 (usewww.morningstar.com). I like to see afund that doesn’t go down as much asthe market during those bad periods.

• Determine the appropriate bench-mark for each fund you are consider-ing. For instance, let’s say the bench-mark is the Russell 2000 for small-company stocks. I want to see the fund

Table 4. Player Criteria: How the Funds Stack Up

Avg Annual Return (%)YTD* 2002 2001 2000 3 Yr 5 Yr 10 Yr Risk Beta Investment Style

Stock FundsDodge & Cox Stock 25.00 –10.54 9.33 16.31 8.27 12.47 14.08 avg 0.74 large valueFirst Eagle SoGen Global 31.00 10.24 10.21 9.72 15.83 15.62 11.72 avg 0.47 medium valueFPA Crescent 23.00 3.71 36.14 3.59 18.89 11.82 12.92 ab avg 0.55 small blendHussman Strategic Gr 18.50 14.02 14.67 16.40 18.35 — — low –0.07 medium blendOakmark Equity & Inc 19.10 –2.14 18.01 19.89 10.89 13.26 — blw avg 0.42 medium blendRoyce Low Price Stock 41.00 –16.28 25.07 23.95 8.92 19.06 — ab avg 1.08 small blend

Bond FundsDodge & Cox Inc 4.80 10.75 10.32 10.70 10.09 7.25 7.28 blw avg 0.75Vanguard Short Corp 3.00 5.22 8.14 8.17 6.55 5.78 5.98 avg 0.41

BenchmarksS&P 500 20.27 –22.09 –11.88 –9.10 –8.33 0.53 10.42Nasdaq 46.78 –31.53 –21.05 –39.29 –16.92 1.75 9.51Russell 2000 42.66 –20.48 2.49 –3.03 3.44 8.34 8.88Lehman Bros Agg Bond 3.06 10.27 8.42 11.63 8.37 6.54 6.78

* Through 11/28/03.Source: Morningstar, Inc.

AAII Journal8

Portfolio Strategies

outperform its benchmark two out ofthree years, but also cumulatively overthree years. In addition, it should out-perform its benchmark three out offive years and cumulatively over fiveyears. In other words, I allow a man-ager to miss the benchmark in one yearor two, but not overall.

• The ideal, but seldom accom-plished, goal is to find a manager whosefund doesn’t go down as much as themarket but who does better than themarket on the upside.

FundamentalsTo keep this task manageable let’s

use just two measurements: price-earn-ings ratio and price-to-book ratio.Morningstar.com will give you this in-formation.

• Price-earnings ratios: 20 or less isgood; over 20, be very cautious.

• Price-to-book value: 3 or less isgood; over 3, be very careful.

RiskThere are several numbers to look

for when determining risk. Combinethe riskiness of the fund with its perfor-mance in down years and you’ll have a

good idea how risky the fund is overall.The most common risk measurementsare:

• Standard deviation: This simplymeasures how widely the returns var-ied over a certain period of time. If afund has large variations, it is consid-ered volatile and therefore more risky.The lower the number, the better, butgenerally below 18 is best.

• Beta: This addresses the volatilityof a fund relative to its appropriatebenchmark. It’s a measure of a fund’ssensitivity to market movements. Forinstance, the S&P has a beta of 1.00; ifa fund has a beta of 1.10, this impliesthat the fund has performed 10% bet-ter than its benchmark index in upmarkets and 10% worse in down mar-kets. The lower the number the lessrisky, but 1.00 or below is a goodstarting point.

Fund Structure and Company• Don’t use funds that employ

rapid timing, after-hours trading or otherscams that have been publicized re-cently.

• Character counts—you want toinvest only with managers and compa-

nies that have excellent character.• At least half of the fund’s board

members should be true independents.It’s preferable that the chairman be anindependent.

• It is best if board members arepaid in shares of their fund. They shouldalso hold investments in their fund.

• If fund performance takes a“pop” up at the end of a month, quar-ter or year, watch for “portfolio pump-ing.” That occurs when a manager usessome of the cash to buy stocks healready owns to drive the price up atthe end of a reporting period.

• I like managers with 10 to 15years of experience under their belts.

That gives you an overview ofsome of the things to look for whenpicking a fund. The Edwards had$210,000 left to invest. Table 3 showshow I would eventually invest it.

The information matrix in Table 4gives you a significant amount of datafrom Morningstar for each of the fundsin the makeover—these are all excep-tional numbers. So far all have escapedscandal, and all of the funds have passedthe criteria I mention here.

Teamwork

Once you have made the overallallocation decision, you are still not fin-ished. You must examine how theseplayers work as a team. And for that,we go back to the scatterplot.

Figure 2 shows the scatterplot forthe makeover portfolio—it is now inthe most desirable quadrant, the upper-left corner, with lower risk (a standarddeviation of 8.87) than the overallbenchmark, and a higher return overthe last few years through October2003.

In summary, by properly under-standing your objectives, timeframe andrisk tolerance, you have the basic neces-sities for creating a winning game plan—a portfolio that will work better foryou in both up and down markets.

Figure 2. The Edwards’ Makeover Portfolio

8.87 17.26 29.0–12.0

–8.3

–4.6

–0.9

2.8

6.5

10.2

13.9

17.6

21.3

25.0

3 Year Standard Deviation

3 Year Average Return

Lower Risk Higher Risk

S&P 500

Lower Return

Higher Return

This quadrant is Lower Risk & Higher Return

New Portfolio

Portfolio Individual Holding Benchmark

Vern Hayden, CFP, is president of Hayden Financial Group, a fee-only financial planning firm based in Westport, CT, 203/454-3377. Mr.Hayden is author of “Getting an Investment Game Plan,” published by John Wiley & Sons and available for $29.95 in bookstores and throughamazon.com at a 30% discount.

January 2004 9

Risk Quiz1. Your portfolio is invested partly in low-risk bond funds (about 40%) and partly in broadly

diversified stock funds (about 50%), according to a long-term game plan. It’s late spring,and this year your stock funds are not doing well. They’re down about 5%, pretty much in linewith the overall market. Wall Street analysts are divided on the market’s future. You . . .

A. Sell all of your stock funds and move the money to bond funds or cash.B. Stick with your allocation despite your current jitters.C. Would never be in bonds in the first place!

2. In the mid 1990s, the S&P 500 funds posted double-digit returns—37% in 1995, 23% in 1996.Looked good to you, so you invested, too. Here are the returns on that investment for the next five years:

1997 1998 1999 2000 200133.2% 28.6% 21.1% –9.1% –12.0%

During this period you . . .

A. Can’t take the pain of 2000 into 2001 and sell.B. Decide to hold through all five years.C. Bolt in 1999 for a tech fund posting triple-digit returns.

3. Your core fund with most of your investment money has returned about 9% a year over the past five years. Butyou read about a healthcare fund that’s returned more than twice that for each of the past two years and you’reimpressed with what you’ve read about the manager. You . . .

A. Do nothing.B. Sell 5% of your core fund and invest the proceeds in the healthcare fund.C. Sell 35% or more of your core fund and invest the proceeds in the healthcare fund.

4. Say you invested 5% of your portfolio in the hot-hand healthcare fund from Question 3. After two great years,this one fund now represents 12% of your portfolio. You . . .

A. Didn’t invest in this fund in Question 3 and still don’t want any part of it.B. Sell about half of the investment to take some money off the table.C. Are so thrilled with this fund that you add another 5% of your portfolio to it.

5. In early 2000, you learned of a technology fund that had been up 185.3% in 1998 and 232% in 1999. You invest.By the end of 2000, the fund has lost 76.3%, and few expect tech to rebound anytime soon. You . . .

A. Would never have touched this fund in the first place.B. Sell and take the almost 25% of your investment you’ve got left.C. Stay the course while you watch another 70% of what’s left disappear in 2001.

Score:For each question, give yourself 1 point for an A answer, 2 points for a B answer and 3 points for a C answer,and add the points up.

5 to 7 points: 8 to 12 points: 13 to 15 points:Risk averse Risk Steady Risk Seeker

Conservative Moderate Aggressive