portfolio investment in turkey

DESCRIPTION

Portfolio Investment in Turkey. Gregor Holek, Senior Fund Manager Raiffeisen Capital Management/ Emerging Markets Equities London, 4th of March 2008. Presentation Overview. The Turkish Economy (page 3-10) EU Membership and IMF Program (page11-15) The Turkish Stock Market (page 16-22) - PowerPoint PPT PresentationTRANSCRIPT

Portfolio Investment in Turkey

Gregor Holek, Senior Fund ManagerRaiffeisen Capital Management/ Emerging Markets Equities

London, 4th of March 2008

3© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> Presentation Overview

1. The Turkish Economy (page 3-10)

2. EU Membership and IMF Program (page11-15)

3. The Turkish Stock Market (page 16-22)

4. Valuation in Emerging Markets (page 23-26)

5. Outlook (page 27-28)

The Turkish Economy

5© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Economy

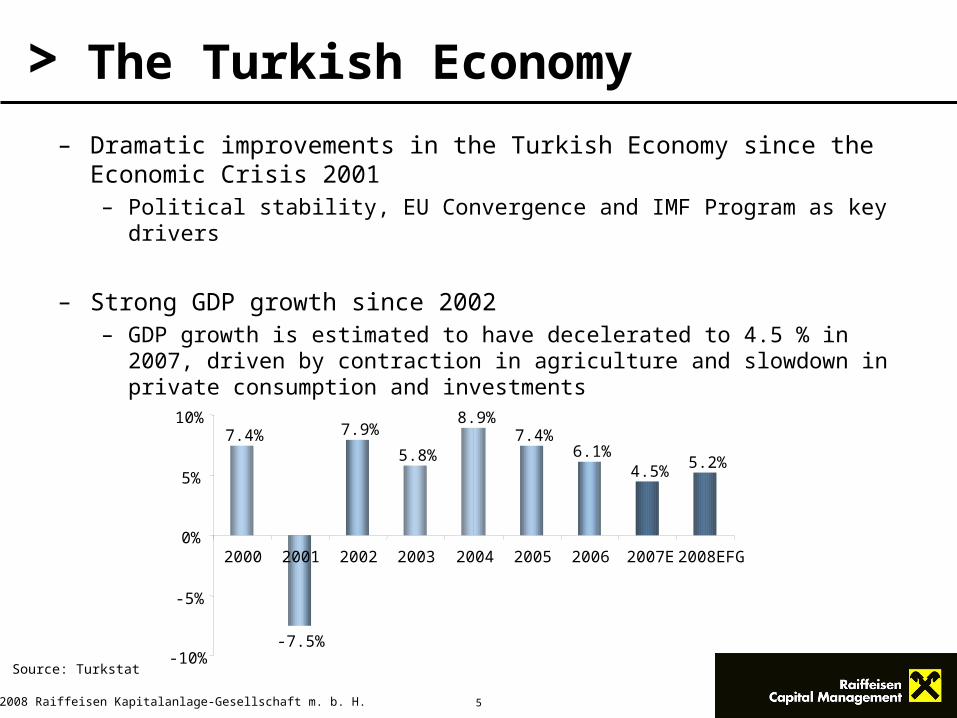

– Dramatic improvements in the Turkish Economy since the Economic Crisis 2001– Political stability, EU Convergence and IMF Program as key drivers

– Strong GDP growth since 2002– GDP growth is estimated to have decelerated to 4.5 % in 2007,

driven by contraction in agriculture and slowdown in private consumption and investments

Source: Turkstat

7.4%

-7.5%

7.9%

5.8%

8.9%7.4%

6.1%4.5% 5.2%

-10%

-5%

0%

5%

10%

2000 2001 2002 2003 2004 2005 2006 2007E2008EFG

6© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Economy

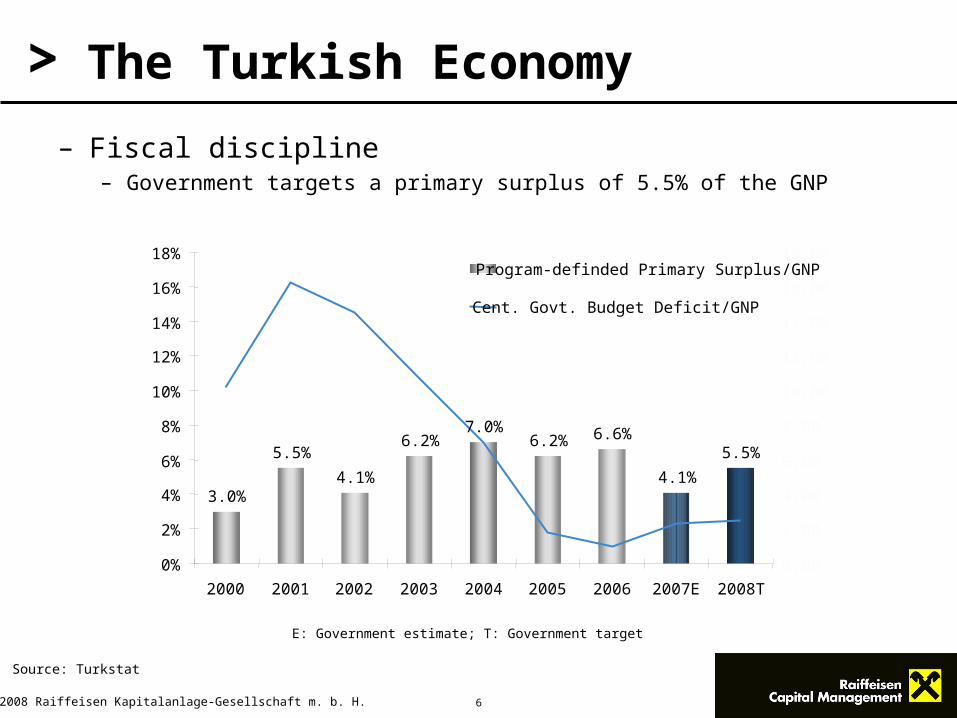

– Fiscal discipline– Government targets a primary surplus of 5.5% of the GNP

E: Government estimate; T: Government target

Source: Turkstat

3.0%

5.5%

4.1%

6.2%7.0%

6.2% 6.6%

4.1%

5.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2000 2001 2002 2003 2004 2005 2006 2007E 2008T

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00Program-definded Primary Surplus/GNP

Cent. Govt. Budget Deficit/GNP

7© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Economy

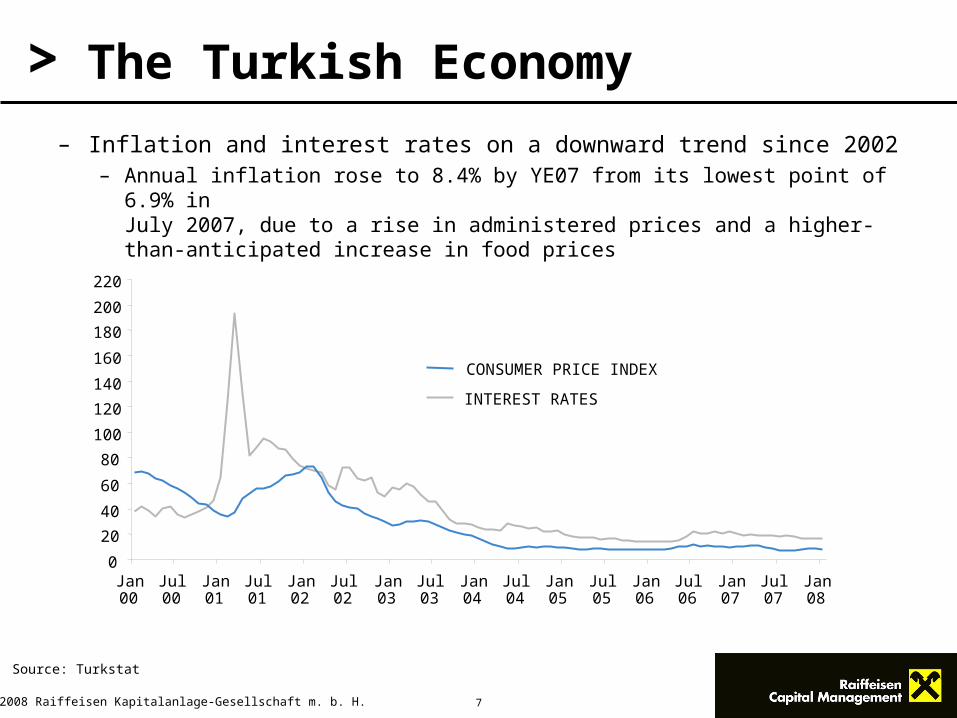

– Inflation and interest rates on a downward trend since 2002– Annual inflation rose to 8.4% by YE07 from its lowest point of

6.9% in July 2007, due to a rise in administered prices and a higher-than-anticipated increase in food prices

Source: Turkstat

0

20

40

60

80

100

120

140

160

180

200

220

Jan00

Jul00

Jan01

Jul01

Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

INTEREST RATES

CONSUMER PRICE INDEX

8© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Economy

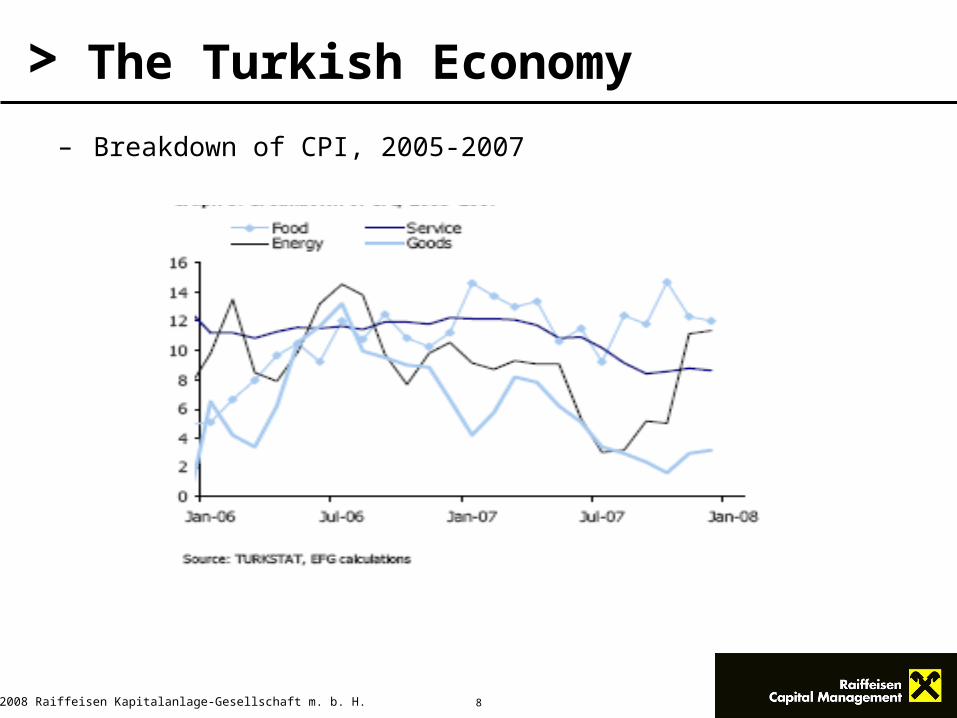

– Breakdown of CPI, 2005-2007

9© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Economy

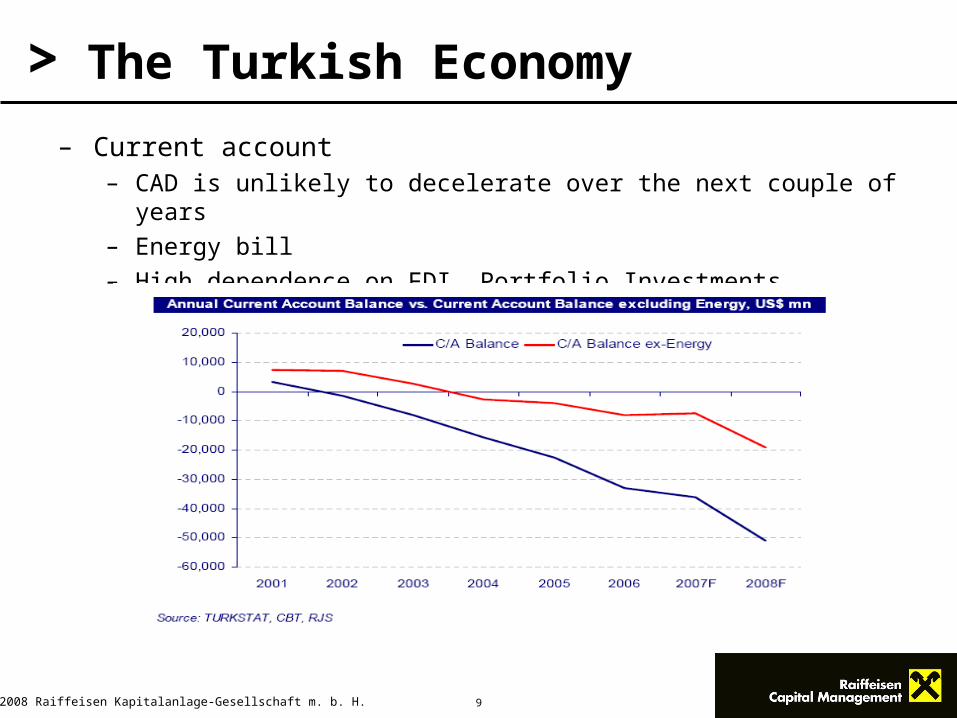

– Current account– CAD is unlikely to decelerate over the next couple of years– Energy bill– High dependence on FDI, Portfolio Investments

10© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

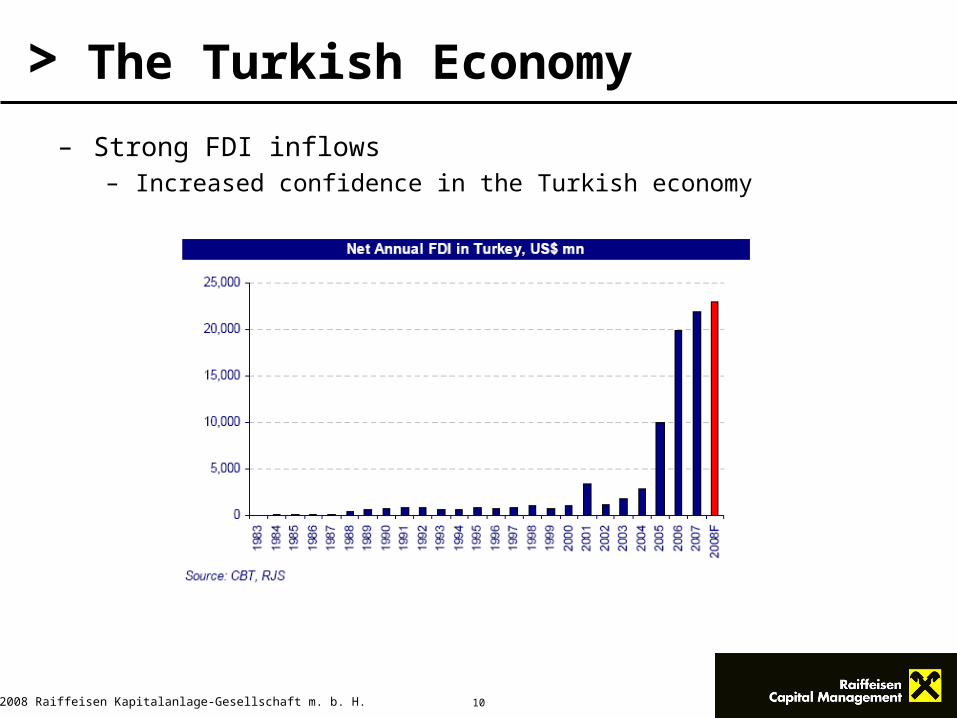

> The Turkish Economy

– Strong FDI inflows – Increased confidence in the Turkish economy

11© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

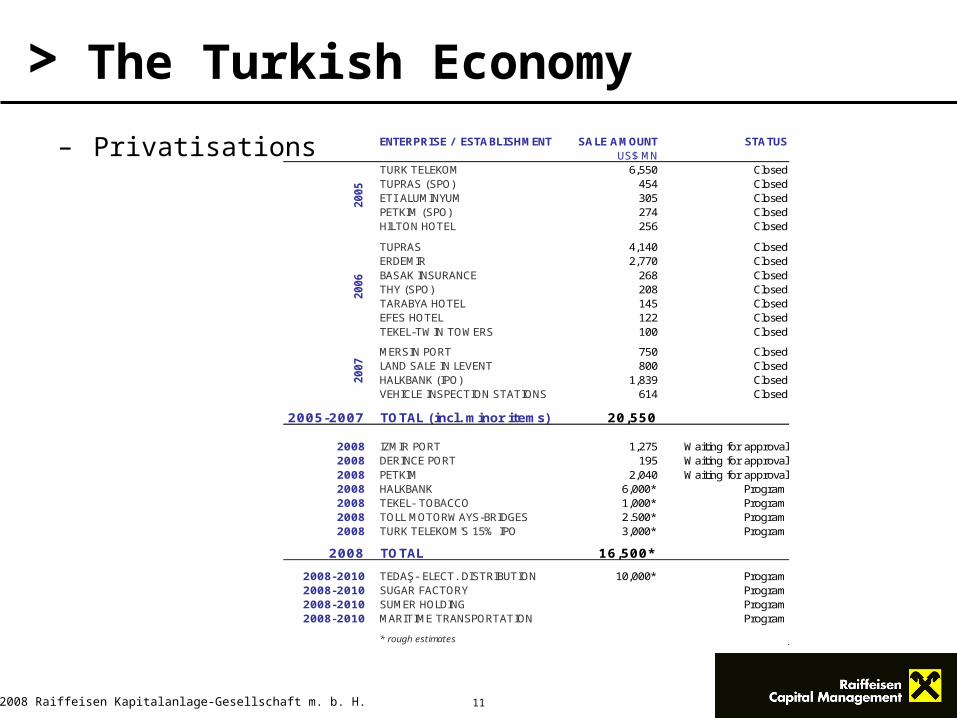

>ENTERPRISE / ESTABLISHMENT SALE AMOUNT STATUS

US$ MNTURK TELEKOM 6,550 ClosedTUPRAS (SPO) 454 ClosedETI ALUMINYUM 305 ClosedPETKIM (SPO) 274 ClosedHILTON HOTEL 256 Closed

TUPRAS 4,140 ClosedERDEMIR 2,770 ClosedBASAK INSURANCE 268 ClosedTHY (SPO) 208 ClosedTARABYA HOTEL 145 ClosedEFES HOTEL 122 ClosedTEKEL-TWIN TOWERS 100 Closed

MERSIN PORT 750 ClosedLAND SALE IN LEVENT 800 ClosedHALKBANK (IPO) 1,839 ClosedVEHICLE INSPECTION STATIONS 614 Closed

2005-2007 TOTAL (incl. minor items) 20,550

2008 IZMIR PORT 1,275 Waiting for approval2008 DERINCE PORT 195 Waiting for approval2008 PETKIM 2,040 Waiting for approval2008 HALKBANK 6,000* Program2008 TEKEL- TOBACCO 1,000* Program2008 TOLL MOTORWAYS-BRIDGES 2.500* Program2008 TURK TELEKOM'S 15% IPO 3,000* Program

2008 TOTAL 16,500*

2008-2010 TEDAŞ- ELECT. DISTRIBUTION 10,000* Program2008-2010 SUGAR FACTORY Program2008-2010 SUMER HOLDING Program2008-2010 MARITIME TRANSPORTATION Program

* rough estimates

2007

2005

2006

The Turkish Economy

– Privatisations

EU Membership & IMF Program

13© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> EU Membership and IMF Program

– The European Convergence Play– IMF and EU “anchors” have been largely responsible for

continued improvement of the country’s macroeconomic fundamentals and its social transformation in recent years.

– EU negotiations– Start of EU membership negotiations: 3rd October 2005– 35 chapters- 6 opend and 1 closed so far– Main goal for investors is the ongoing convergence and not the

final outcome of the negotiations

– IMF Program– Standby agreement ends May 2008– Banking Reform, Tax Reform, Fiscal Reform

14© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> EU Membership and IMF Program

Reforms - 1

AKP Election Manifesto- Reforms to continue in line with EU Convergence Program, irrespective of

the pace of negotiations

Real Sector:- Draft Commercial Code to be legislated — emphasis on enhancement of

corporate governance, enforcement of international audit standards - SMEs’ access to funding - Revisions to legal regulations regarding credit

reporting system to allow efficient sharing of information on companies’ credit history; to expedite enforcement of lien on property; to encourage M&As.

- Restrictions on entry to market/bankruptcy to be eased- Social security premiums paid by employers to be reduced gradually

starting with a 5pp cut in 2008 - Stamp tax & other transaction taxes to be lowered - SMEs to be supported via subsidised loans for additional employment

15© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> EU Membership and IMF Program

Reforms - 2

Incentive scheme:- Project based incentives focused on development of new products &

technologies- Subject to clear performance criteria to measure productivity gains- Incentive scheme to be revised & regional incentives to be emphasised

Competitiveness:- Privatisation - All public sector banks to be privatised, starting with

Halkbank- Micro reforms to be adopted to enhance competitiveness

Labour Market Reform: - Flexible employment formats to be developed

16© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

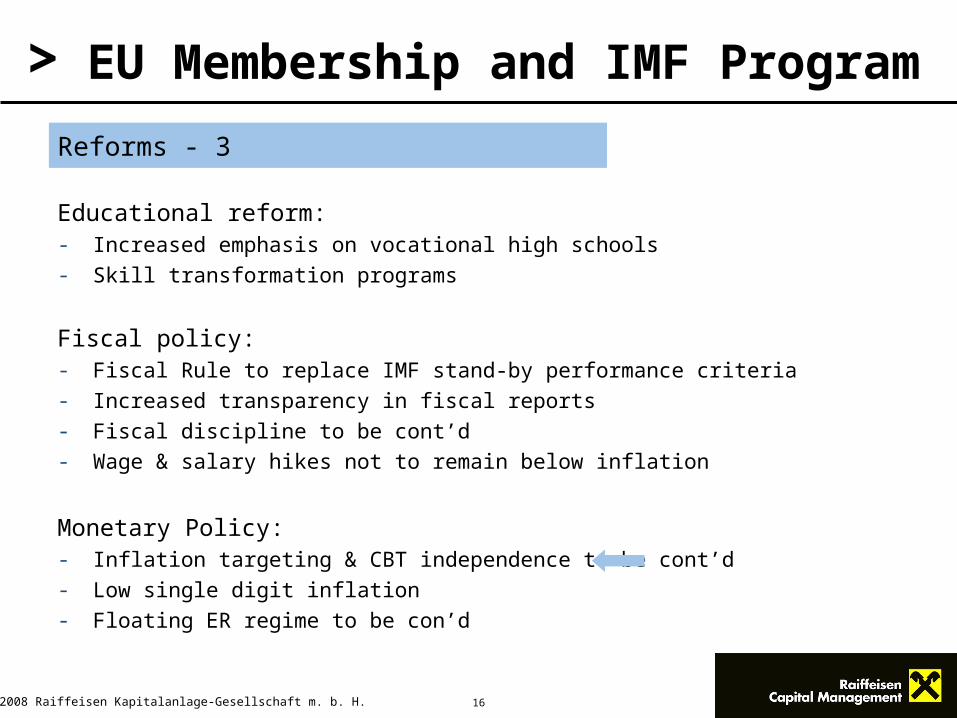

> EU Membership and IMF Program

Reforms - 3

Educational reform:- Increased emphasis on vocational high schools- Skill transformation programs

Fiscal policy: - Fiscal Rule to replace IMF stand-by performance criteria- Increased transparency in fiscal reports - Fiscal discipline to be cont’d- Wage & salary hikes not to remain below inflation

Monetary Policy: - Inflation targeting & CBT independence to be cont’d- Low single digit inflation - Floating ER regime to be con’d

The Turkish Stock Market

18© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

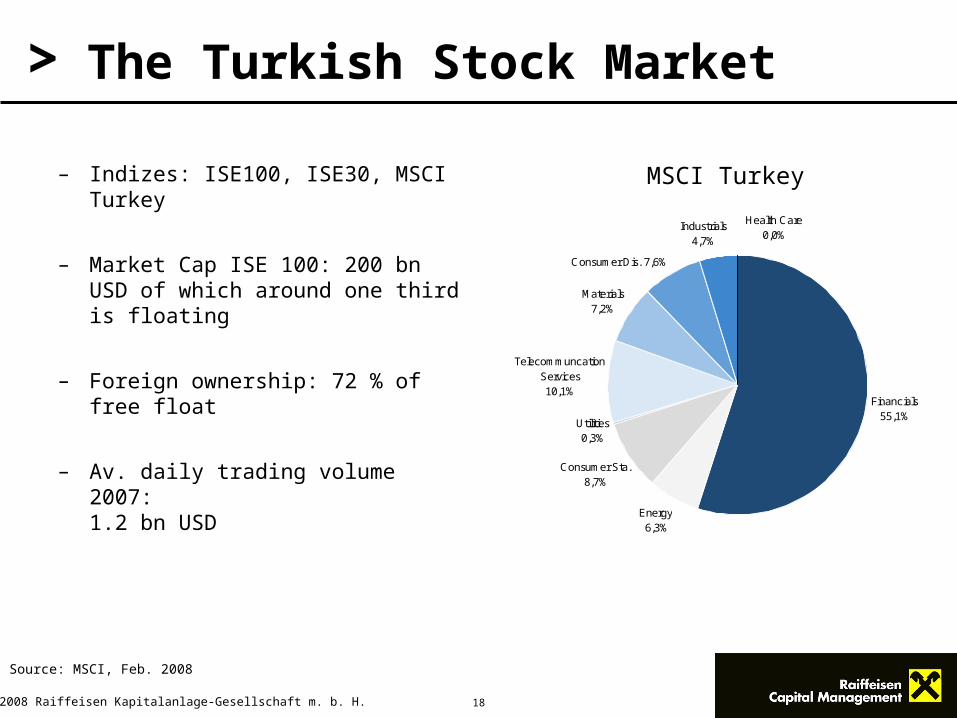

> The Turkish Stock Market

– Indizes: ISE100, ISE30, MSCI Turkey

– Market Cap ISE 100: 200 bn USD of which around one third is floating

– Foreign ownership: 72 % of free float

– Av. daily trading volume 2007: 1.2 bn USD

MSCI Turkey

Financials55,1%

Health Care0,0%

Energy 6,3%

Consumer Sta. 8,7%

Utilities 0,3%

Telecommuncation Services 10,1%

Materials 7,2%

Consumer Dis. 7,6%

Industrials 4,7%

Source: MSCI, Feb. 2008

19© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Stock Market

Source: ITIS, data as at 22/02/2008

80

100

120

140

160

180

200

220

240

Feb

05

Sep 0

5

Mar

06

Oct

06

May 0

7

Nov 0

7

MSCI Turkey net dividend reinvested (USD):

MSCI EM Eastern Europe (USD):

66.5 %

91.4 %

Total Return (rebased, EUR)

18.5 % p.a.

24.2 % p.a.

20© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Stock Market

Source: Bloomberg

21© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> The Turkish Stock Market

MSCI Turkey

Security Weighting (%)

TURKIYE GARANTI BANKASI 14.207492 DOGAN YAYIN HOLDING 1.237138

AKBANK T.A.S. 10.967625 TOFAS TURK OTOMOBIL FABRIKA 1.176604

TURKCELL ILETISIM HIZMET AS 10.723902 ARCELIK A.S. 1.176486

TURKIYE IS BANKASI-C 9.810924 ASYA KATILIM BANKASI AS 1.139625

TUPRAS-TURKIYE PETROL RAFINE 6.57688 TURK SISE VE CAM FABRIKALARI 1.089159

EREGLI DEMIR VE CELIK FABRIK 6.277653 HURRIYET GAZETECILIK VE MATB 0.980793

ANADOLU EFES BIRACILIK VE 4.954341 PETKIM PETROKIMYA HOLDING AS 0.92234

TURKIYE HALK BANKASI 4.674899 TRAKYA CAM SANAYII AS 0.346747

HACI OMER SABANCI HOLDING 4.500509 AYGAZ AS 0.318567

TURKIYE VAKIFLAR BANKASI T-D 3.933218 ULKER BISKUVI SANAYI AS 0.257339

YAPI VE KREDI BANKASI 3.364074 IS GAYRIMENKUL YATIRIM ORTAK 0.241666

MIGROS TURK TAS 3.160007 AKCANSA CIMENTO 0.237325

KOC HOLDING AS 2.875594 CIMSA CIMENTO SANAYI VE TIC 0.212564

DOGAN SIRKETLER GRUBU HLDGS 1.535455 ADANA CIMENTO-A 0.20395

FORD OTOMOTIV SANAYI AS 1.403799 VESTEL ELEKTRONIK SANAYI 0.145747

AKSIGORTA 1.34758

Source: MSCI, Feb. 2008

22© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

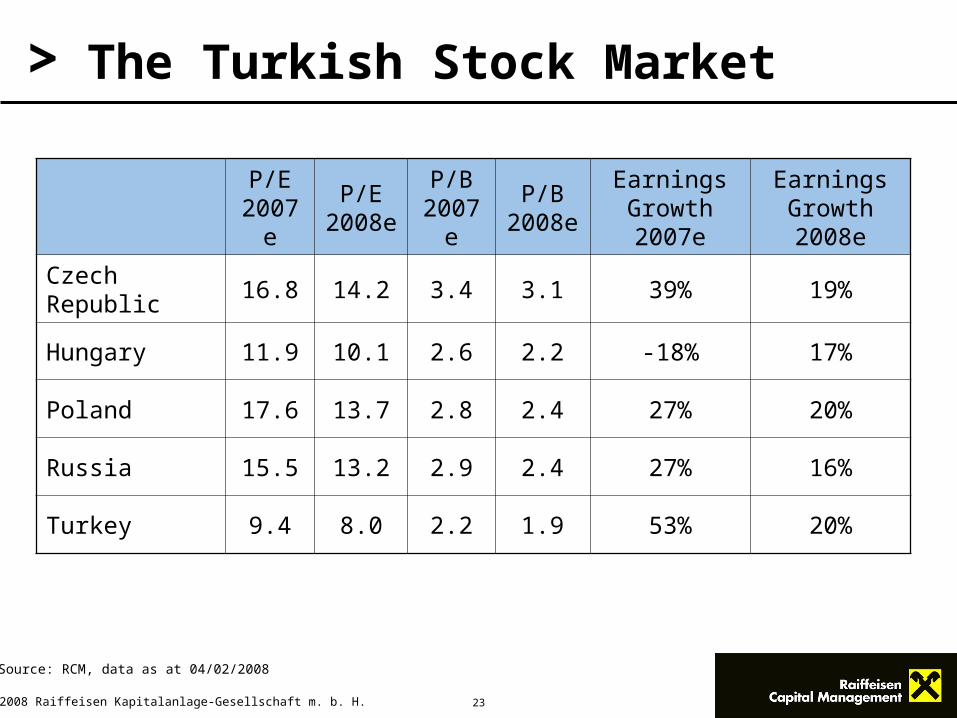

> The Turkish Stock Market

23© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

>

P/E 2007

e

P/E 2008

e

P/B 2007

e

P/B 2008e

Earnings Growth 2007e

Earnings Growth 2008e

Czech Republic

16.8 14.2 3.4 3.1 39% 19%

Hungary 11.9 10.1 2.6 2.2 -18% 17%

Poland 17.6 13.7 2.8 2.4 27% 20%

Russia 15.5 13.2 2.9 2.4 27% 16%

Turkey 9.4 8.0 2.2 1.9 53% 20%

The Turkish Stock Market

Source: RCM, data as at 04/02/2008

Valuation in Emerging Markets

25© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> Valuation in Emerging Markets

– Risk Free Rate in Emerging Markets

– EM market government debt is

– Not risk free (below investment grade)– Traded in illiquid markets– Often denominated in mayor crncy like the USD

– Estimate the risk free rate by adding the inflation differential between the local market and the US to the US Treasury 10-year-yield

– Risk free rate = 10-year U.S gov. Bond yield + (local inflation – US inflation)

– Price target in local crncy

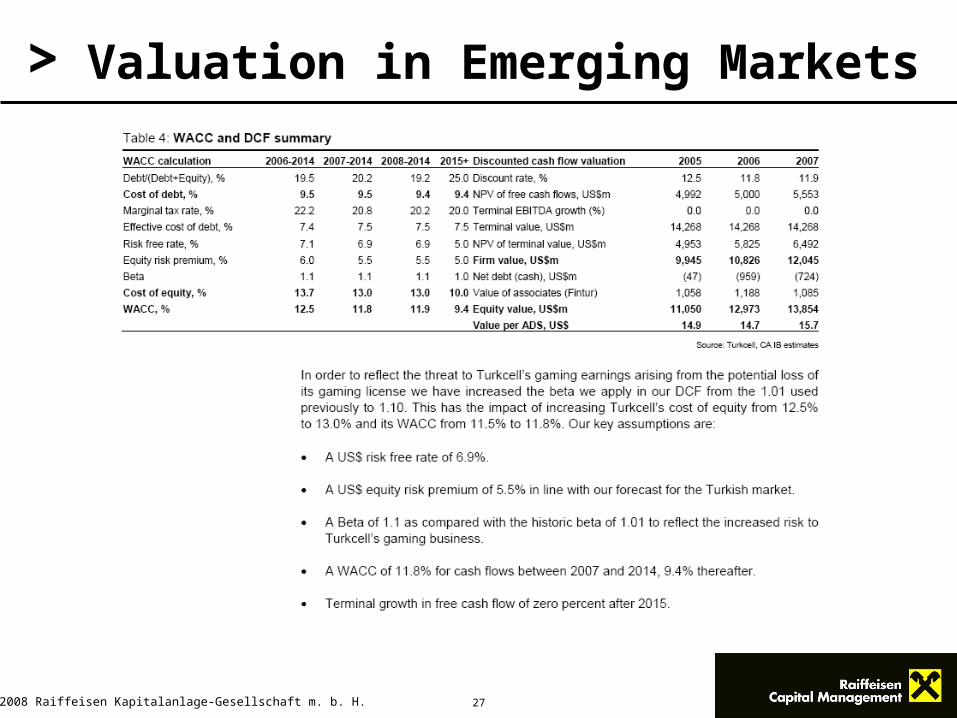

26© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> Valuation in Emerging Markets

– Country Risks can also be captured by adjusting the cash flows in a scenario analysis rather than including them in the discount rate

– Widely used approach

– As cash flows are measured in foreign crncy long term exchange rate estimates are needed to derive local crncy price targets.

27© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> Valuation in Emerging Markets

Outlook

29© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

> Outlook

– The prolonged rate cut cycle due to high real rates will lead to strong domestic consumption

– Privatizations in the energy, telecom and banking sector will be positive for the stock market

– Global slowdown have muted effect on Turkish economy due to strong domestic dynamics

– Risks: Turkey is historically sensitive to global risk appetite, we thus expect a positive but volatile performance for 2008. We also see inflation risk due to rising food & oil prices.

30© 2008 Raiffeisen Kapitalanlage-Gesellschaft m. b. H.

>

This document was prepared and edited by Raiffeisen Kapitalanlage-Gesellschaft m.b.H., Vienna, Austria (“Raiffeisen Capital Management” or “Raiffeisen KAG“). Despite careful research, the statements contained herein are intended as non-binding information for our customers and are based on the knowledge of the staff responsible for preparing these materials as of the time of preparation and are subject to change by Raiffeisen KAG at any time without further notice. Raiffeisen KAG assumes no liability whatsoever in relation to this document or verbal presentations based on such, in particular with regard to the timeliness or completeness of the information presented and the sources of information, or in respect of the accuracy of the forecasts presented herein. Similarly, any forecasts or simulations of earlier fund performance presented in this document do not provide a reliable indication of future performance. It is furthermore noted that the return on foreign currency products may rise or fall due to exchange rate developments.

This document is neither an offer, nor a recommendation to buy or sell, nor an investment analysis. The contents of this document are not intended for use in lieu of professional consultation and advice on making specific investments. Specific investments should only be undertaken following professional consultation. It is expressly noted that securities transactions can involve significant risks and that taxation of such depends on personal circumstances and is subject to change in the future. Past performance is not a reliable indicator of the future development of an investment fund or portfolio. Raiffeisen KAG calculates performance of investment funds in accordance with the methodology of the Austrian Control Bank ‘OeKB’, based on the data of the depository bank. Issue and repurchase fees are not included. Development of funds is stated in percent (excluding fees), taking into account reinvestment of dividends. The current version of the prospectus on the investment funds described in this document, including all of the amendments since its original publication, is available at www.rcm.at/eng.Reproduction of the information or data, in particular the use of texts, text sections or graphic material from this document requires the prior written consent of Raiffeisen KAG.

Raiffeisen Zentralbank Österreich AG, RZB Austria London Branch, 10 King William Street, London EC4N 7TWAuthorised by the Austrian Financial Market Authority and by the Financial Services Authority; regulated by the Financial Services Authority for the conduct of UK business

Disclaimer