policy and research agenda on prudential supervision

TRANSCRIPT

Policy and research agenda on prudential supervision

Final SYRTO conference

Paris, 19 February 2016

Simone Manganelli

European Central Bank

Disclaimer: Any views expressed are only the author’s own and do

not necessarily reflect the views of the ECB or the Eurosystem

Rubric

www.ecb.europa.eu ©

• Modern economies need well-functioning financial systems. – Transfer resources when and where they are most needed.

– Allow entrepreneurs to finance project with positive NPV.

– Enhance the growth potential of the economy, creating job and wealth.

– Large literature on causal relationship b/w finance and growth.

– Dating back to Schumpeter (1912), King and Levine (1993).

• Well-functioning financial systems are necessary for central banks

to perform their functions. – Monetary policy is implemented by steering short term interest rates.

– Via expectations and no arbitrage relationships, this affect the whole term

structure and therefore the cost of funding of the economy.

– In exceptional times, when the lower bound is reached, non-standard

measures affect directly the longer end of the term structure, via forward

guidance and QE.

• ECB (and other central banks) attempt to bypass a malfunctioning

financial system by means of non-standard measures.

2

Motivation – Why effective supervision is important

Rubric

www.ecb.europa.eu ©

Composite Indicator of Systemic Stress

3 Source: BCE e Hollo, Kremer, Lo Duca (2012), ECB WP No. 1426

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Se

p 2

00

0

Ma

r 2

00

1

Se

p 2

00

1

Ma

r 2

00

2

Se

p 2

00

2

Ma

r 2

00

3

Se

p 2

00

3

Ma

r 2

00

4

Se

p 2

00

4

Ma

r 2

00

5

Se

p 2

00

5

Ma

r 2

00

6

Se

p 2

00

6

Ma

r 2

00

7

Se

p 2

00

7

Ma

r 2

00

8

Se

p 2

00

8

Ma

r 2

00

9

Se

p 2

00

9

Ma

r 2

01

0

Se

p 2

01

0

Ma

r 2

01

1

Se

p 2

01

1

Ma

r 2

01

2

Se

p 2

01

2

Ma

r 2

01

3

Se

p 2

01

3

Ma

r 2

01

4

Se

p 2

01

4

Ma

r 2

01

5

Se

p 2

01

5

CISS EA (monthly average) SovCISS EA (GDP weights)

Subprime

crisis

Forward

guidance

QE start

Lehman

Start Greek

crisis

Draghi

speech

Terrorist

attacks

WorldCom

bankruptcy

3y

LTRO

AQR

and CA

QE

Rubric

www.ecb.europa.eu ©

• ECB measures have been successful in fixing a malfunctioning

financial system.

• But it should be clear that these measures have dealt only with the

short term symptoms of the crisis.

• To improve the long term efficiency of the system requires

addressing the deep causes of the crisis.

• Many initiatives have been taken. My focus today is on the

Banking Union.

4

The road ahead

Rubric

www.ecb.europa.eu ©

1. Market failures

2. Narrow banking

3. Banking Union a) Single Supervisory Mechanism

b) Single Resolution Mechanism

c) Common Deposit Insurance

4. Really big questions: a. Interaction between monetary and prudential policies

b. Shadow Banking

5

Overview

Rubric

www.ecb.europa.eu ©

Government intervention is justified on the basis of market failures:

• Negative externalities – Panic run (Diamond and Dybvig)

– Bank-sovereign nexus

– Too-big-too-fail

– Systemic risk

• Asymmetric information – Opacity and complexity of banks’ balance sheets

– Deposit insurance, government interventions and moral hazard problems

6

1. Market failures

Rubric

www.ecb.europa.eu ©

• In its most extreme form, “narrow banks” issue deposits which are

fully backed by cash.

• Financing of the economy is left to “investment funds”, which are

financed with equity and long-term debt.

• The classic Chicago plan goes back to Douglas et al. (1939).

Recent contributions are Kotlikoff (2010) and Benes and Kumhof

(2012).

But not so fast:

• The transition from the current system is not trivial.

• The maturity transformation function of the banking system is lost.

• The new “investment funds” could also be subject to run (‘fire

sales’) with unpredictable consequences for the financing of the

economy.

• Prohibiting short term debt in the regulated banking system will

push it to the unregulated shadow banking sector.

7

One extreme solution: Narrow banking

Rubric

www.ecb.europa.eu ©

Manage overall risks of the financial system, building on regulatory

requirements, together with well-designed supervision and resolution

mechanisms.

The Banking Union rests on three pillars:

1. Single Supervisory Mechanism – Operational as of November

2014

2. Single Resolution Mechanism – Operational as of January 2016

3. Common Deposit Insurance – Details yet to be agreed

8

A more balanced solution: Banking Union

Rubric

www.ecb.europa.eu © 9

Why a Banking Union?

The Banking Union has been essentially created to break the bank-

sovereign nexus.

• Fragile banks undermine government finances and weak

government finances undermine the banking system.

• This has an impact on the real economy, by reducing lending and

further aggravating the positions of banks and government.

• Within a monetary union, this bank-sovereign nexus can only be

broken if banks are supervised and recapitalized at European

level.

Rubric

www.ecb.europa.eu © 10

The case for macro-prudential policies

From ‘VaR’ to ‘VAR for VaR’: safety of individual banks does not

guarantee safety of the financial system as a whole.

Long standing issue of whether to use monetary policy to deal with

asset price misalignments and financial stability risks.

Important emerging research on measurement of business cycle

and financial cycle:

• If the two cycles are synchronized, monetary policy can be also

used to lean against the wind.

• However, financial cycles tend to have larger amplitude and

lower frequency than business cycles.

• When the objective of price and financial stability are not

synchronized, monetary policy should be accompanied by a

suitable macro-prudential policy, with a differentiated set of tools.

Rubric

www.ecb.europa.eu © 11

SSM: The Single Supervisory Mechanism

SSM started its operations in November 2014.

It is governed by a Supervisory Board of 25 members, similar to the ECB

Governing Council.

Its main aims are to:

• ensure the safety and soundness of the European banking system

• increase financial integration and stability

• ensure consistent supervision

The ECB directly supervises the 129 significant banks of the participating

countries. These banks hold almost 82% of banking assets in the euro

area.

• Supervision of the significant banks is carried out by Joint Supervisory

Teams, comprising staff of the ECB and the national supervisors.

• Banks that are not considered significant continue to be supervised by

their national supervisors, in close cooperation with the ECB.

Rubric

www.ecb.europa.eu © 12

Prudential tools of the SSM

SSM has both micro and macro prudential powers:

- Lender-based instruments: - Capital requirements

- Capital buffers for systemically important institutions

- Countercyclical capital buffers

- Liquidity requirements

- Borrower-based instruments (available at national level): - Loan-to-value

- Loan-to-income

- Debt service-to-income

Rubric

www.ecb.europa.eu © 13

Effectiveness of prudential policies

Key research and policy questions:

• How to resolve the tension between micro and macro

perspective?

• What is the effectiveness of these measures?

• How do they interact among themselves?

• Are there spillovers across national borders and how to best

coordinate these instruments?

• What is the optimal design of stress tests and the optimal

amount of disclosure?

Rubric

www.ecb.europa.eu © 14

Single Resolution Mechanism and bail-in

When all of the above measures fail, in the absence of orderly

resolutions, governments may have to bail-out banks to avoid

contagion and severe impairment of the financial system.

But:

• Bail-outs strain public finances

• Bail-outs fuels moral hazard behaviour and distorts incentives

Since bank failures are inevitable (even under optimal supervision),

it is important to have resolutions mechanisms in place.

Questions:

• How is bail-in affecting the cost of funding of banks?

• Optimal resolution strategy?

Rubric

www.ecb.europa.eu © 15

Common Deposit Insurance

This is the area where research can have the greatest impact, as

there is no agreement yet on its optimal design.

In general, public guarantees induce moral hazard and excessive

risk-taking problems, because:

- Creditors no longer have incentives to discipline banks

- Banks’ funding costs are artificially reduced

European Deposit Insurance Scheme (EDIS), building on national

deposit guarantee schemes.

Many issues to be clarified, related to:

- How to trigger the insurance

- How to ensure that national DGS manage their costs and risks

properly

- How to fund the Scheme

Rubric

www.ecb.europa.eu ©

1. Market failures

2. Narrow banking

3. Banking Union 1. Single Supervisory Mechanism

2. Single Resolution Mechanism

3. Common Deposit Insurance

4. Really big questions: a. Interaction between monetary and prudential policies

b. Shadow Banking

16

Overview

Rubric

www.ecb.europa.eu © 17

Additional challenges: Interaction with monetary policy

Global inflation has been subdued for a few years.

Central banks have answered by injecting large amounts of liquidity

and with large scale asset purchases.

Low inflation can be a problem because

• higher real interest rates

• higher debt burden for borrowers

• slower adjustment of highly indebted households, firms and

governments

• low interest rates may induce excessive “search for yields”

BIS view that low rates present a threat to financial stability.

Rubric

www.ecb.europa.eu ©

-1

0

1

2

3

4

5 1

99

9

20

01

20

03

20

05

20

07

20

09

2011

20

13

20

15

Euro area inflation below its objective in the past few years…

18 Source: ECB

Rubric

www.ecb.europa.eu ©

-1

0

1

2

3

4

5

6

7

19

99

20

01

20

03

20

05

20

07

20

09

2011

20

13

Deposit Facility Marginal Lending Facility MRO

… and interest rates have reached their lower bound

19 Source: ECB

Rubric

www.ecb.europa.eu © 20

Forward guidance and quantitative easing

• Interest rates cannot fall too much below zero: “Investing” in cash

gives a return of zero.

• Central banks can charge slightly negative interest rates,

because bank accounts are more convenient (to make payments

and to prevent theft).

• Once short term interest rates have reached their lower bound,

central banks use “forward guidance” and “quantitative easing”:

• The main objective remains to further stimulate the economy,

lowering long term interest rates.

Rubric

www.ecb.europa.eu ©

4 July 2013 – Forward guidance

The Governing Council expects the key ECB interest rates to remain at present or

lower levels for an extended period of time.

22 January 2015 – Expanded asset purchase programme

• ECB expands purchases to include bonds issued by euro area central governments,

agencies and European institutions

• Combined monthly asset purchases to amount to €60 billion

• Purchases intended to be carried out until at least September 2016

• Programme designed to fulfil price stability mandate

9 March 2015 – ECB starts purchases

21

Main announcements of the ECB

Rubric

www.ecb.europa.eu ©

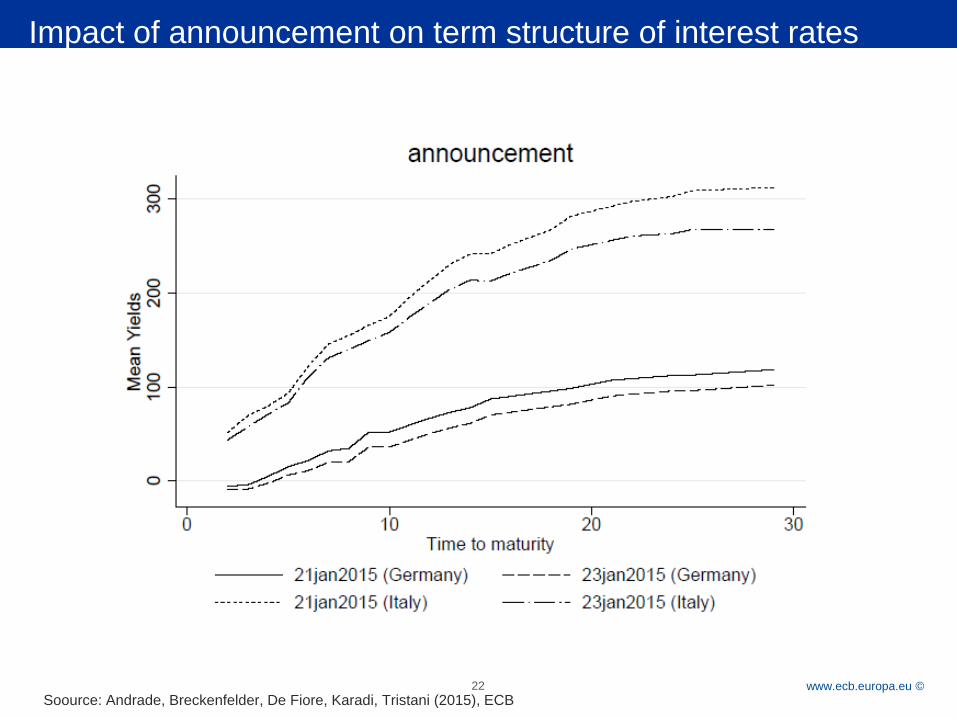

Impact of announcement on term structure of interest rates

22

Soource: Andrade, Breckenfelder, De Fiore, Karadi, Tristani (2015), ECB

Rubric

www.ecb.europa.eu © 23

Impact of ultra low interest rates on banks

With negative deposit rates, banks are required to pay a tax to

deposit excess liquidity with the ECB.

• Retail deposit rates are constrained at zero, so further lowering of

interest rates may squeeze banks’ profitability and create

fragilities.

• Of course this neglects the macro channel: an accommodative

monetary policy should stimulate economic growth and

strengthen banks’ balance sheets, for instance by reducing non-

performing loans.

• In any case, interest rates are foreseen to remain low for a long

period of time, so any study which may shed light on the impact

on financial stability would be welcome.

• More generally, what is the optimal monetary/prudential policy

mix?

Rubric

www.ecb.europa.eu © 24

Additional challenges: Shadow banking

What is the best way to think about shadow banking? As banks

become increasingly regulated, some activities will shift outside the

banking sector.

Key issues:

1. Information on non-banking sectors is much more limited.

Studies should pull together data from different sources.

2. Understand the incentive structures and how the non-banking

and banking sector interact.

3. Indicators to detect new sectors in which risks are accumulating

and find ways of including them in early warning and stress-

testing frameworks.

4. Effective policy measures to increase resilience of non-bank

institutions and to mitigate risks in financial markets.