pngisd board of trustees update 27, 2003.pdf · resolution reaffirming their support for the...

TRANSCRIPT

PNGISD BOARD OF TRUSTEES UPDATE

June 27, 2003

“Based on the guidance provided by the Supreme Court, I do not believe that the state can prevail in this lawsuit.”---School Finance Expert Lynn Moak speaking to superintendents at Region IV ESC in June, 2003

TASB SUMMER LEADERSHIP CONFERENCE Thanks to each of you who gave of your time and energy to attend the TASB SLI in San Antonio. Your efforts made it possible for us to have 100% participation of the Board and the Team of 8 at this important event. This year was only the second year in my tenure at PNGISD that we have been successful in achieving this goal. Thanks again for your dedication and selfless contributions to the students and staff of this district. While I attended several interesting sessions, one of the most interesting (and scary) was the session on Closed Meetings that was presented by TASB Attorney Kathleen Wells. I have asked Bonnie to scan the handout from this session for your review. Even though Dr. Thompson appeared to be convinced that there is some latitude in the Open Meetings Act, I become frightened each time I hear a discussion and particularly, when I hear of lawsuits and challenges that have been successful in testing the OMA regulations. I am contemplating buying the TASB OMA video tapes “ 72 Hours OMA” and “The Second Half” for a training session in the future. If any of the rest of you have handouts that you think would benefit the rest of us, please let us borrow them and we will scan them for the next update and return the original to you. (ATTACHED: Copy of “OMA 301: Closed Meetings Revealed”

TASA SUMMER CONFERENCE/ Texas School Coalition I left the TASB Conference for Austin, Texas and the TASA Summer Conference. On Sunday evening, I met with the executive board of the Texas School Coalition. Our impressive success at the Supreme Court appears to have given us some additional leverage with administrators and officials across the state. We have received contacts from several other districts seeking to join our group and the lawsuit. Members of the executive board agreed to pay their district fees and dues early so that our lawyers can begin the process of preparing for the district court trial. In addition, we will be asking each board to pass another resolution reaffirming their support for the lawsuit against the state school finance system. I have asked Mark Trachtenberg to visit with us again at our August Board Meeting and we

2

will place this item on the agenda for the August meeting. I have attached a copy of the financial sheet that I sent to Cheryl Hernandez asking her to submit payment for this activity. Money was included in the current budget for this purpose and we are including dollars in next year’s budget for this purpose as well. I have been asked to work with David Hicks of Deer Park ISD to schedule and implement a regional meeting of all Chapter 41 Districts in Regions 4,5, and 6. Since there will be a significant increase in the number of Chapter 41 Districts across the state this year, it is our hope that we will see a sizable increase in the membership of the coalition. The TASA Summer Conference was well-planned and provided good information. I can tell you that I am very tired of sitting in workshops and presentations after attending the TASB and TASA Conferences back to back. It is fortunate that we (superintendents) were in Austin this week. It appears that TEA officials, after a preliminary reading of the recent school finance legislation, decided that Chapter 41 schools would have their per student allocation offset by the amount of the technology allotment ($30). A number of the Chapter 41 Superintendents immediately visited with TEA and then sought opinions from several key legislators who happened to be attending the conference as well—primarily Representative Grussendorf and Senator Shapiro as well as aides from the Governor and Lt. Governor’s office. After receiving assurance from the legislators that it was not their intent to offset Chapter 41 funds, TEA backed off their original interpretation. As it stands today, we will receive an additional $110 per ADA for the next two years. However, there are numerous unfunded mandates in the new legislation, especially in the federal No Child Left Behind legislation. We will be bringing these to your attention as we work through the budget and curriculum issues in coming weeks.

STRATEGY SESSION WITH LAWYERS Yesterday, I met all day in Dallas with the lawyers who represented us in the School Finance Litigation. As we reviewed the litigation and the influence of the organization in the recent legislative session, we believe that there is a clear swing of the pendulum toward increased leverage and toward concern for our issues. For example, our lawyers were invited to speak to the House Committee on School Finance on Tuesday of this week. This is the first time that our side has been asked to provide testimony. David Thompson, who is a well-respected attorney with experience and knowledge about the school finance system, testified in the same hearing before the committee. Our attorneys felt like Mr. Thompson reaffirmed our arguments in this case and that he more or less told the committee that the Supreme Court has “teed up the issues” in our favor. I have provided for your review a copy of the comments prepared by Mr. Thompson and delivered to the House Committee. In addition, for your information, I have provided a copy of the Supreme Court ruling that may interest you. While this litigation will cost additional money, the lawyers feel that this is the time to press forward with the litigation. Based on the latest rumors, it appears that the special session for school finance is likely to be called next spring. Continued action in the court will do nothing but increase the pressure on these guys to do something to fix the system. I CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

3

still believe that the legislature would love nothing more than to walk away from the problem. However, our recent success in court and the prospect for continued success appear to minimize the legislators’ option of leaving things at the status quo. They asked me if we were prepared to stay on board and I assured them that we are committed to WINNING this fight. Indeed, I told the group that our only disagreement with the current situation is that we felt like our name (Port Neches-Groves ISD) should have been listed first in the lawsuit rather than West Orange Cove. The lawyers and everyone else at the meeting agreed. The lawyers indicated that we could change the order of the plaintiffs even now. However, they advised against that strategy since the case is already known as West Orange-Cove. I told them that we were more interested in winning the case than getting recognition, but we would have much preferred to have been the lead plaintiff in this case. According to the lawyers, we will need to expend some resources preparing our case at the district court level. After the district court rules, the lawyers will attempt to circumvent the Austin Appeals Court and get the case back to the Supreme Court. Our lawyers feel that we need to prevail in this case at the Supreme Court Level. Whether we win or lose at the District Court Level, our lawyers feel like our real success will come when we get the case back before the Supreme Court of Texas. We will be scheduling a regional meeting and a meeting of the entire school coalition has been scheduled in Dallas during the TASB Fall Conference. I will let you know more about this later. (ATTACHED: Copy of Supreme Court Ruling, Copy of statement of David Thompson.

TEXAS SCHOOL COALITION LEVERAGE DURING THIS PAST SESSION

CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR

While I could not characterize the last legislative session as a “positive” one for public schools, I believe the presence of the Texas School Coalition did help PNGISD as well as other school districts to benefit from the legislative action as much or more so than any other group. Certainly, everyone suffered as a result of this session. When one begins to describe their victories in terms of things that did not happen, it is easy to see that the session was not a good one. However, we can be glad that the legislature approved the $110 per WADA per year outside the finance formula. This represents new money and it has never been funded outside the formula. This, in effect, is unequalized enrichment. In addition, the relationship that our organization enjoyed with key legislative leaders made it possible for us to quash the TEA interpretation of recent legislation that would have cost us thousands of dollars. The lobbying efforts and the lawsuit have pretty much re-introduced the concept of “adequacy” as a school finance precept and the supreme court ruling as well as comments from people like David Thompson seem to suggest that adequacy may be a cornerstone of new legislation. It now appears that a special session for school finance may be called in April of next year. A recent article in the Equity Center newsletter suggested that Chapter 41 School Districts fared better than Chapter 42 Districts in the recent legislative session. While I don’t know that we fared better, I do believe that much of our success during this session could be attributed to the efforts of the school coalition. For those of you who plan to attend the Fall School Board

INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

4

Conference, the coalition will be meeting on September 20, 2003 at 4:30 p.m. By that time, the Supreme Court will have remanded the lawsuit back to the district court and we will know who the judge will be and we may even have a timeline for discovery and a trial date.

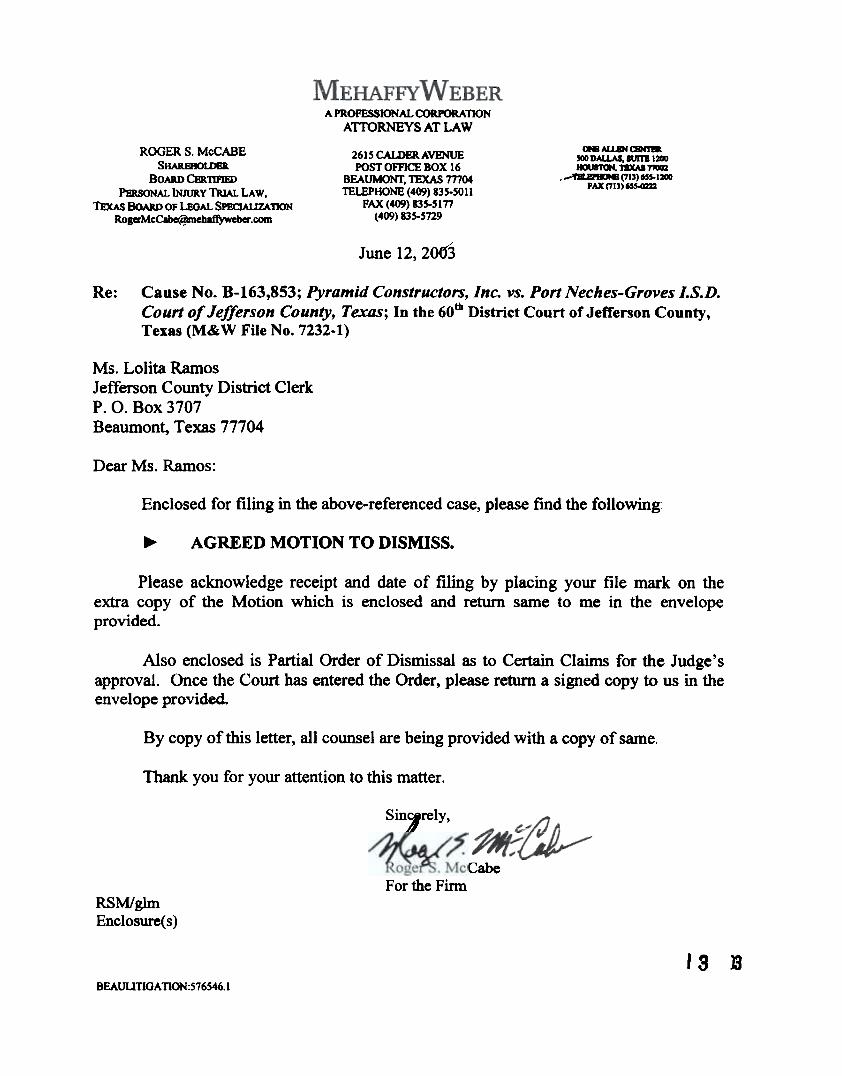

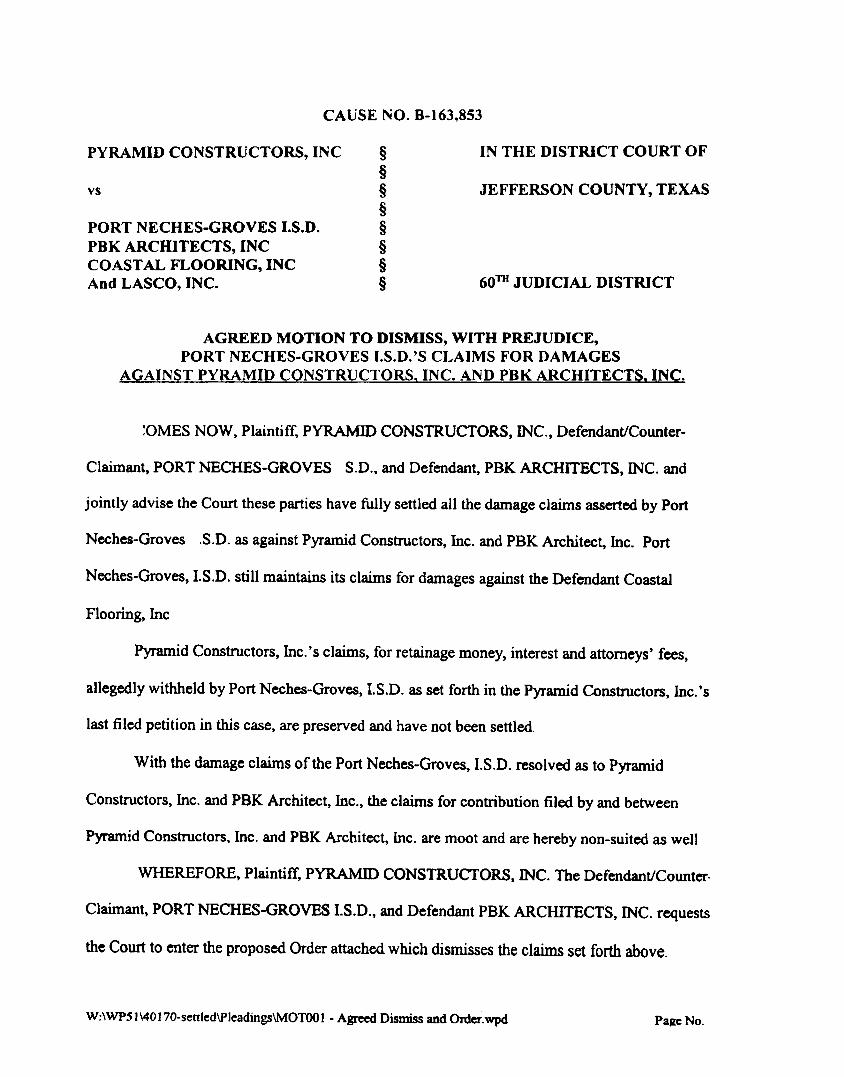

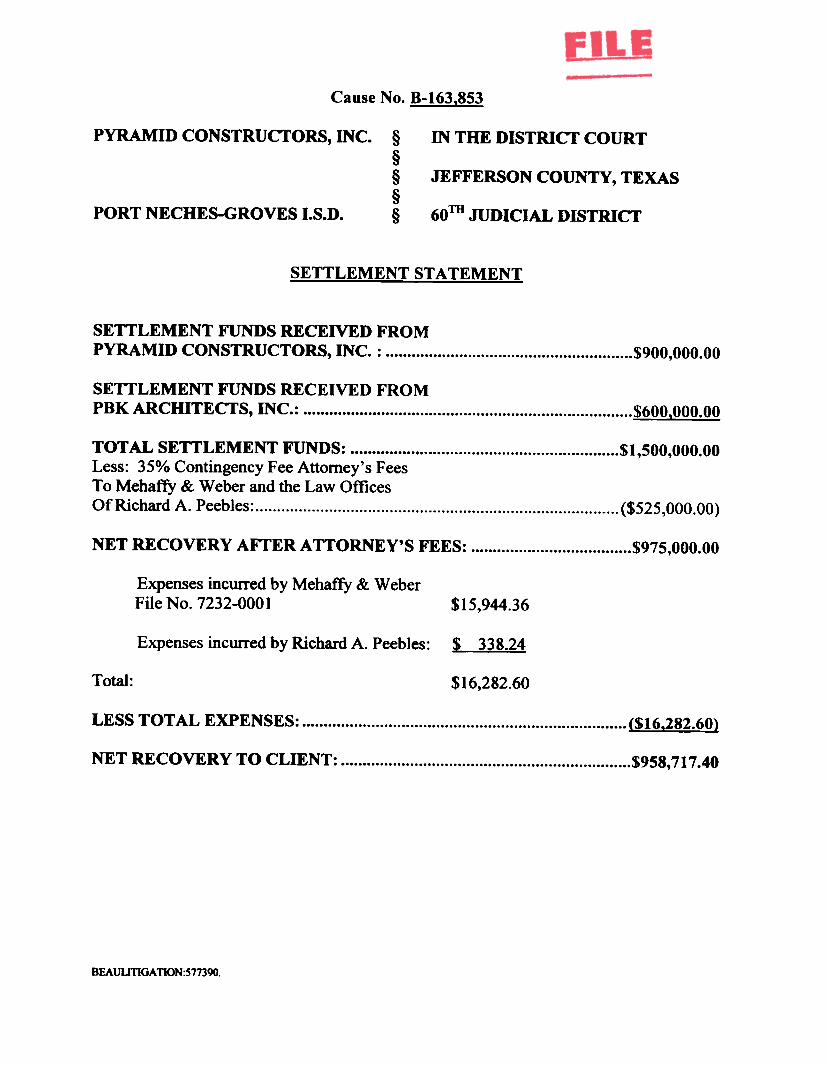

PYRAMID CONSTRUCTORS AND PBK ARCHITECTS As you know, we have dismissed our lawsuit against Pyramid Constructors and PBK Architects in exchange for a $958,000 check from their insurance companies. The check is now drawing interest in our bank. We still have a lawsuit against Coastal Flooring and Pyramid still has a lawsuit against PNGISD to recover their retainage as well as attorney’s fees and interest. Roger and Rick called me in Austin this week to tell me that the judge had set a hearing for this Friday (6-27-03) on a motion by Coastal Flooring to grant summary judgment. The lawyers did not think it was likely that the judge would grant the motion. Just to be safe, they asked me to attend and to invite Harvey to join us in the audience. We agreed to do so but the hearing was abruptly cancelled on Thursday evening and rescheduled for July 7 at 1:30 p.m. Rick and Roger informed me that Coastal has taken the position that they did not do anything wrong and that it is grossly unfair for them to be sued over this matter. However, they did offer $50,000 to make the case go away. Roger thinks they are liable for about $200,000 and he suggested that we consider settlement offers when (and if) the judge denies their motion for summary judgment. I will let you know how this goes. Please remember that Pyramid still claims that we owe them $210,000 plus interest and attorney’s fees. If we settle the case with Coastal, only the suit brought against us by Pyramid will be outstanding. This issue has demanded many hours of time, but I believe we will have about $1,000,000 to address the construction problems that we most definitely would not have had if we had not challenged the work of the construction company, contractors, and architect. I believe that our time and effort in this case have proved to be good investments. Of course, we will never have the floor that we should have gotten. However, we at least have some resources to implement a reasonable repair that would not have been possible without these settlements. Thank you for your support in taking a stand on these issues. I have attached for your review a copy of the motion to dismiss our suits against Pyramid and PBK. (ATTACHED: Copy of motion to dismiss and copy of settlement statement)

ARTICLE ON NEW SCHOOL FUNDING I have attached for your review a copy of a recent article from The Beaumont Enterprise that describes the “new” money allocated by the legislature for public schools. While there are many other unfunded mandates in the legislation, this money flows outside the formula and will help considerably. (ATTACHED: Copy of article from The Beaumont Enterprise)

CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

5

FEDERAL HEARING As you are aware, we are required to make a special report to the Board each year about the expenditure of federal funds. A special hearing for this purpose is scheduled prior to the next meeting on July 8, 2003. The hearing is scheduled to being at 6:30 p.m. As usual the regular board meeting will commence at 7:00 p.m. after the hearing on federal funds. Dr. Randall will present the report on federal expenditures. Please mark your calendars for a 6:30 p.m. start time for the hearing that will be held prior to the regular board meeting. REMINDER: HEARING ON FEDERAL DOLLARS TO BEGIN AT 6:30 P.M. JULY 8, 2003

RETIREMENT RECEPTION NOTE I am attaching for your review another nice note we received thanking us for the retirement reception. As you will recall, the reception idea in lieu of a formal recognition banquet or luncheon was new to our district last year. In our second year of the reception, it appears that our employees have embraced this activity as an appropriate forum for expressing our appreciation and best wishes to those who are leaving us. (ATTACHED: Copy of note from Elaine Sherman)

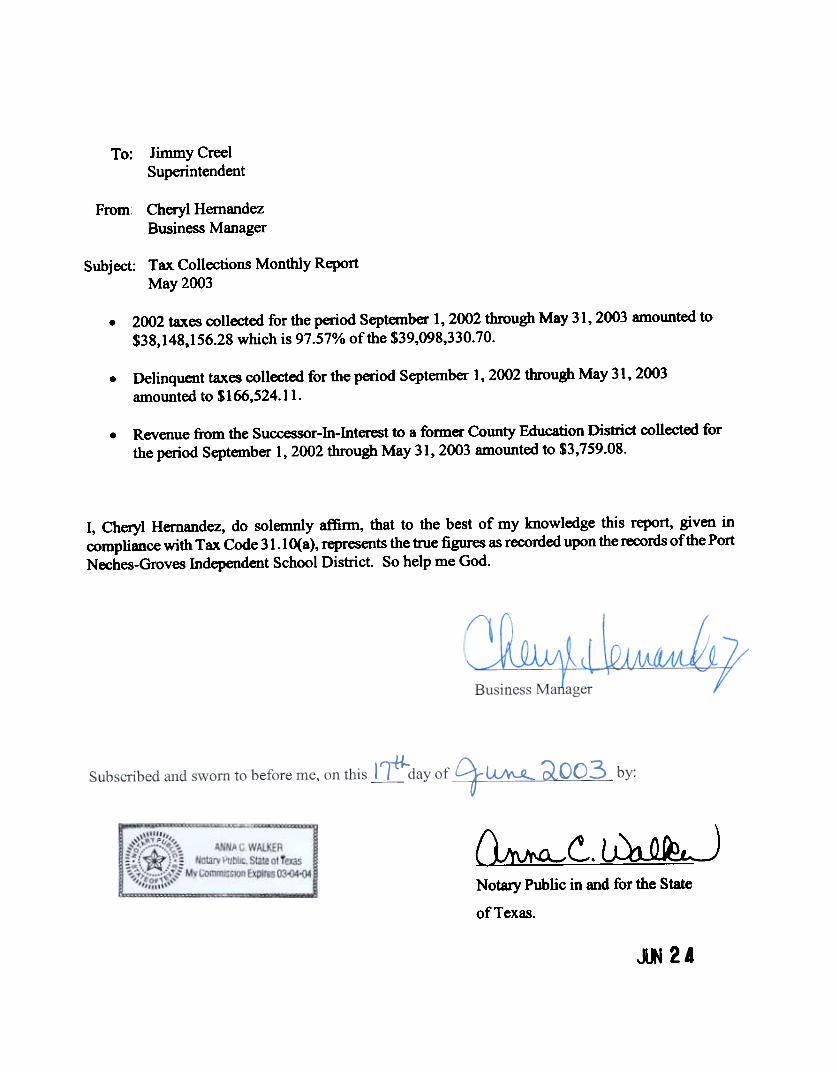

TAX COLLECTIONS MONTHLY REPORT Please find attached a copy of the monthly tax collections report submitted by Cheryl Hernandez. (ATTACHED: Copy of monthly tax collection report)

AMERIPOL-SYNPOL EFFORTS I met last week with Jess Byerly of the Economic Development Corporation regarding their efforts to keep Ameripol-Synpol in our community. She asked me to make a commitment regarding our willingness to consider agreements that might enhance the tax status of a new buyer. I explained to Jess that the law limits our options regarding school taxes. However, I did provide her with a written statement indicating that we would be happy to consider another HB 1200 agreement if we perceived the agreement to be in our best interests (Copy of my letter attached). I explained that the company would be required to bring us an application and proposal with a non-refundable application fee of $75,000. This fee was established at the beginning of our negotiations with Sabina Petrochemicals and it applies to all potential applicants. (ATTACHED: Copy of letter regarding HB 1200)

GROWTH PLAN As you will recall, during the Level III hearing of a complaint against Ms. Clara Graham, the Board directed us to implement a growth plan and to provide the Board with a progress report at the August Board meeting. However, since that time, Mrs. Graham has chosen to retire thus making the progress report a moot point. I have attached a copy of an e-mail I CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

6

received from Dr. Randall reminding me of the fact that we will not be making this report to the Board. (ATTACHED: Copy of e-mail from Dr. Randall regarding progress report to be made to the Board)

EARLY CHILDHOOD CAMPUS As I mentioned in a previous Update, the retirement of Ms. Graham has created gaps in various areas of responsibility within the district. We have attempted to cover most of those responsibilities by reassigning duties and making changes to the job descriptions of other employees. However, the responsibility for supervision and administration of the Early Childhood Campus and program is a significant responsibility that must be filled. Indeed, the No Child Left Behind legislation has the potential to generate many changes and significant responsibility for the leader of this campus. Yet, we would prefer not to hire a new employee to manage this campus and assume the responsibilities that were formerly assigned to Ms. Graham. As I mentioned, we have restructured many of these duties to include them in the job descriptions of other employees. However, we have decided to assign responsibility for the Early Childhood Campus to Ms. Suzanne Mondey in addition to her current responsibilities as Director of Special Education. Since Ms. Mondey indeed does have a full time responsibility as Director of Special Education, the additional responsibility will require Ms. Mondey to work additional hours and to expend additional effort. However, Ms. Mondey has assured us that she is willing and able to assume this additional responsibility and we have confidence in her ability to do so. Therefore, it is our intention to provide Ms. Mondey with an additional stipend of $5,000 to compensate for the significant additional time and energy that will be required to meet this obligation. Please find attached copies of e-mail from Dr. Randall and from Mr. Martin in which they recommend this change in responsibility. I have also attached a copy of the updated job description for Ms. Mondey to reflect this change. As I stated previously, we would prefer to hire a replacement to take all the job responsibilities formerly held by Ms. Graham. However, this combination of restructuring and reassignment of the major responsibilities with a stipend payment provide the best strategy, in our opinion, to meet the obligations and responsibilities while conserving an additional professional position in our budget. We believe that these changes will provide adequate supervision and direction for the Early Childhood Center and will cover the responsibilities formerly held by Ms. Graham in an effective and efficient manner. (ATTACHED: Copies of e-mail from Dr. Randall, Mr. Martin, and updated job description for Ms. Mondey)

HAVE A GREAT WEEKEND! CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

CONFIDENTIAL: ANY PERSON WHO HAS ACCIDENTALLY OR INADVERTENTLY GAINED ACCESS TO THIS MATERIAL WHO IS NOT A PNGISD BOARD MEMBER OR SELECTED PNGISD ADMINISTRATOR SHOULD CLOSE THE DOCUMENT IMMEDIATELY AND RETURN TO THE OFFICE OF THE SUPERINTENDENT, PNGISD, 620 AVENUE C, PORT NECHES, TEXAS 77651 OR E-MAIL [email protected]

7

II~ Texas Association of School Boards512-467-3610 . 800-580-5345

: E-mail: [email protected]

2003 Summer Leadership InstituteJune 19-21, 2003

Presented by Kathleen Wells, Director of Legal ServicesTexas Association of School Boards

OMA 301: Closed Meetings RevealedT ASH Legal Services Division

Thou Shalt Obey the OMA Exceptions.L

A. General Rule: Open Meeting Required

All business open to public: In gen~ all school board meetings must be open tothe public. Tex. Gov't Code § 551.002. Nevertheless, the Open Meetings Act (OMAor Act) authorizes boards to meet in closed session for certain specific purposes. Tex.Gov't Code §§ 551.071-551.086. For a closed meeting to be legal, it must be held forone of these enumerated purposes.

.

Closed meetings permitted, not required: The Act does not require a board to gointo closed meeting on any matter. Even if a subject falls within one of the limitedstatutory exceptions, those exceptions are pennissive, not mandatory, in nature.

.

B. Exceptions to the Rule: Valid Reasons for Holding Closed Meetings

Consultation with attomey: To consult with the board's attorney when the boardseeks advice about pending or contemplated litigation or a settlement offer, or whenthe attorney will have an ethical duty of confidentiality. Tex. Gov't Code § 551.071

Real property: To deliberate the purchase, exchange, lease, or value of real propertyif deliberation in an open meeting would have a detrimental effect on the board'sposition in negotiations with a third person. Tex. Gov't Code § 551.072.

Prospective gifts: To deliberate a negotiated contract for a prospective gift to thedistrict if deliberation in an open meeting would have a detrimental effect on theboard's position in negotiations with a third person. Tex. Gov't Code § 551.073.

.

C Texas Association of School BoardsLegal Services Division

. Personnel matters: To deliberate the appointment, employment, evaluatio~reassignment, duties, discipline, or dismissal of a public officer or employee, or to heara complaint or charge against an officer or employee. This exception does not apply ifthe officer or employee who is the subject of the deliberation or hearing requests apublic hearing. Tex. Gov't Code § 551.074. See also Tex. Gov't Code § 551.082.

Security: To deliberate the deployment, or specific occasions for implementatio~ ofsecurity personnel or devices. Tex. Gov't Code § 551.076.

.

Student discipline: To deliberate in a case involving discipline of a public schoolchild. unless the child's parent requests an open hearing in writing. Tex. Gov't Code§ 551.082.

.

Student information: To deliberate a matter regarding a public school student ifpersonally identifiable information about the student will necessarily be revealed bythe deliberation, unless an open meeting about the matter is requested in writing by thestudent's parent or guardian or by the student, if the student has attained 18 years ofage. Tex. Gov't Code § 551.0821 (lIB 1226, passed by the 78th Texas Legislature).

.

Economic development: To deliberate about commercial or fInancial infonnationthat the board has received from a business prospec~ or to deliberate the offer of afmancial or other incentive to a business prospect. Tex. Gov't Code § 551.087.

.

Assessment instruments: To discuss or adopt individual assessment instruments orassessment instrument items. Tex. Educ. Code § 39.030.

.

Thou Shalt Give Proper Notice.u.

Proper notice required: The notice requirements for items to be discussed in closedmeetings are the same as those for items to be discussed in open meetings. Tex. Att'yGen. LO-90- 27 (1990). So begin with a properly posted meeting, giving 72 hours'notice of all items to be discussed or about which information will be received. Tex.Gov't Code §§ 551.041,551.043.

.

Don't specify in advance: The notice does not have to identify which items will beheard in a closed meeting as opposed to an open meeting. Rogers v. State Board ofOptometry, 619 S. W.2d 603 (Tex. App.-Eastland 1981, writ dism'd); Tex. Att'yGen. L0-90-27 (1990). A board can achieve flexibility by posting a single list of alltopics to be discussed, followed by a statement that any closed meeting will be heldin accordance with Texas Government Code, Chapter 551, subchapters D and E.(See sample notice in Attachments.)

.

Notice only for closed session: Posting notice of a subject only for discussion inclosed session does not provide adequate notice that the board will take subsequentaction on the issue in open session. Weaver v. Santa Maria Indep. Sch. Dist., Tex.Comm'r ofEduc. Decision No. 166-RI-599 (Dec. 12, 1999).

.

2

C Texas Association of School BoardsLegal Services Division

Thou Shalt Not Vote in a Closed Meeting.m.Get "out" to vote: Neither final action nor a straw poll may be taken in a closedmeeting. Tex. Gov't Code § 551.102; Bd. of Trustees of Austin Indep. Sch. Dist. v.Cox Enter., Inc., 679 S. W.2d 86 (Tex. App.-Texarkana 1984), aff'd in part andrev'dinpart, 706 S. W.2d 956 (Tex. 1986); Op. Tex. Att'y OeD. Nos. H-1198 (1978),H-1163 (1978).

.

. Express yourself: Although the board may not vote in a closed meeting, boardmembers may express their opinions and vol\Ultarily anno\Ulce how they intend tovote when an actual decision is made in open session. Bd. of Trustees of .AustinIndep. Sch. Dist. v. Cox Enter., Inc., 679 S. W.2d 86 (Tex. App.-Texarkana 1984),aff'd in part and rev'd in part, 706 S. W.2d 956 (Tex. 1986).

Be specific: The board must return to open session in order to vote on a matterdeliberated in closed session. The board must vote on a motion that adequatelydescribes the action the board wishes to take; the motion cannot be simply "to dowhat was discussed in closed session."

.

IV. Honor Thy Lawyer.

Legal advice only: A board may meet in closed session with its attorney to discuss"strictly legal matters." For example, a board may consuh with its attorney in closedsession to receive advice on legal issues raised by a proposed contract but not todiscuss the merits of the proposed con~ financial considerations, or other non-legal matters. Op. Tex. Att'y Gen. No. JC-0233 (2000).

Long distance: A board may consult with its attorney by telephone conference call,video conference call, or Internet communications during a meeting in open or closedsession. This provision does not apply to consultations between the board and "in-house'counsel (attorneys who are employees of the district). If the consultation takes place inopen session, the consultation must be audible to the public. Tex. Gov't Code § 551.129

Thou Shalt Not Take the Name of Your Employee in Vain.v.. Individual employees: The personnel exception, Texas Government Code section

551.074, applies only when the board discusses a particular officer or employee, not awhole class of employees. For example, a board may not use the exception to discussits salary schedule. The board may, however, use the exception to discuss an individualemployee's salary because that discussion inherently includes an evaluation of theemployee's performance. Op. Tex. Att'y Gen. No. H-496 (1975).

Board members: This exception applies to board members as well as employees.For example, the board may deliberate the selection ofboard officers in closedsession; however, the decision must be made in open session. Bd. of Trustees ofAustin Indep. Sch. Dist. v. Cox Enter., Inc., 679 S. W.2d 86 (Tex. App.- Texarkana1984), aff'd in part and rev ' d in part, 706 S. W .2d 956 (T ex. 1986).

.

3

C Texas Association of School BoardsLegal Services Division

Independent contractors: The exception does not apply to deliberations regardingindependent contractors, such as attorneys, engineers, architects, or consultants. Op.Tex. Att'y Gen. No. MW-129 (1980).

.

Thou Shalt Not Ignore a Valid Request for an Open Meeting.VI.

Exception to the exception: The personnel exception does not apply if the officer oremployee who is the subject of the deliberation or hearing requests a public hearing.Tex. Gov't Code § 551.074. See also Tex. Gov't Code § 551.082. When this occurs,the board must conduct a public hearing and also deliberate about the matter in opensession, unless the employee consents to the board's deliberating in private. James v.Hitchcock Indep. Sch. Dist., 742 S. W.2d 701 (Tex. App.-Houston [1st Dist.] 1987.writ denied); Corpus Christi Teachers' .Ass'n v. Corpus Christi Indep. Sch. Dist., 535S.W.2d429 (Tex. Civ. App.-Corpus Christi 1976. no writ).

.

Level m grievances: Most districts have a local policy that calls for personnelmatters to be discussed in closed session, unless the employee requests otherwise.Consequently, Level ill grievances regarding personnel issues should be conducted inclosed session unless the employee requests an open session.

.

Public comment: Although most districts have a local policy that calls for personnelmatters to be heard in closed session, there is no requirement that a board move intoclosed session to hear "public comment" complaints about an employee. Dixon v.Grand Prairie Indep. Sch. Dist., Tex. Comm'r ofEduc. Decision No. 064-R3-1299(Nov. 6,2001).

.

The trump card: When two or more employees are involved in a grievance, whichone has the power to request an open meeting? When an employee brings a generalemployment grievance (about a condition of work, for example), the employeebringing the grievance has the power to request an open meeting. When an employeebrings a grievance about another employee, however, the officer or employee who isthe subject of the complaint is the one who may request an open meeting. CompareTex. Gov't Code § 551.074 with Tex. Gov't Code § 551.082.

.

What's it aU about? A school board should exercise caution and seek legal advice ifnecessary to determine the true subject matter of a grievance before denying anemployee's request for an open hearing. For example, after a teacher requested an openhearing of his complaint about "the principal's and the superintendent's actions in theevaluation process," the board met in closed session, erroneously reasoning that theprincipal and superintendent, not the teacher's evaluation, were the subjects of thecomplaint. The attorney general concluded that "[t]he teacher's complaints about theprincipal and superintendent [were] incidental to his grievance against the school district,which necessarily acts through its agents." Op. Tex. Att'y Gen. No. JM-1191 (1990).

.

4

C Texas Association of School BoardsLegal Services Division

Parental complaint about employee: An even more complicated situation can arisewhen a parent complains about a school employee. For example, if a parent complainsabout the discipline imposed by a teacher, and the parent wants the complaint heard inan open meeting while the teacher does not, where should the board hear the complaint?The attorney general recommends separating the two issues-the discipline issue andthe personnel issue-so that one may be heard in open meeting and the other in closed.If this bifurcation is not possible, then the parent's request for an open meeting hearingmust be honored because the teacher has no corresponding "right" to request a closedhearing. Tex. Att'y Oen. LO-95-082 (1995).

.

Thou Shalt Follow All Proper Procedures, Lest Grievous Harm Befall You.VB.

A. Conducting a Closed Meeting

. Convene in open meeting: Before a board may conduct a closed meeting, asauthorized by the Act. a quorum of the board must first convene in a properly postedopen meeting. Tex. Gov't Code § 551.101; Rd. of Trustees of Austin Indep. Sch. Dist.v. Cox Enter., Inc., 679 S. W.2d 86 (Tex. App.-Texarkana 1984), aff'dinpart andrev'd in part, 706 S. W.2d 956 (Tex. 1986).

Announce authority: At an appropriate point on the agenda during open session, thepresiding officer must publicly (1) announce that a closed session will be held and (2)identify the section or sections of the Act under which the closed meeting will beheld. Tex. Gov't Code § 551.101. Although it is not necessary for the presidingofficer to state the actual section number of the statute that authorizes the closedmeeting, the presiding officer must give enough information about the subject matterof the closed meeting to enable the public to identify the board's authority for themeeting. Lone Star Greyhound Park v. Tex. Racing Comm 'n, 863 S. W.2d 742 (Tex.App.-Austin 1993, writ denied).

.

Convene the closed meeting: The presiding officer must annoWlce the date and timeat the beginning and end of each closed session. Tex. Gov't Code § 551.103.

.

B. Recording a Closed Meeting

Required record: Either a certified agenda or an official tape recording must be keptof the proceedings of each closed meeting, except for a board's private consultationwith its attorney as permitted WIder section 551.071. Tex. Gov't Code § 551.103(a).This record provides a method of verifying in court proceedings that the boardcomplied with the requirements of the Act. Tex. Gov't Code §§ 551.103,551.104; Op.Tex. Att'y Gen. No. JM-840 (1988). (See sample certified agendas in Attachments.)

.

5

C Texas Association of School BoardsLegal Services Division

Required contents: A certified agenda or official tape recording must record thepresiding officer's statement of the date and time at both the beginning and end of theclosed session. Tex. Gov't Code § 551.103(c), (d). A certified agenda must alsoinclude a statement of the subject matter of each item discussed in closed session, notjust each item scheduled for discussion. Tex. Gov't Code § 551.103(cXl); Op. Tex.Att'y Gen. No. JM-840 (1988). It must include a record of any further action taken inopen session on the closed session items. Tex. Gov't Code § 551.103(cX2). Finally,the presiding officer must certify that a certified agenda is a true and correct record ofthe closed session proceedings. Tex. Gov't Code § 551.103(b).

Record retention: A certified agenda or tape recording must be maintained for atleast two years after the date of the closed meeting. Iflitigation involving themeeting is brought within that time peri~ the certified agenda or tape must bepreserved while the litigation is pending. Tex. Gov't Code § 551.105(a).

.

Release to the public: A certified agenda or tape recording of a closed meeting isavailable for public inspection and copying only under a court order. Tex. Gov't Code §551.IO4(c); Op. Tex. Att'y Oen. No. JM-995 (1988); Tex. Att'y Gen. ORD-330 (1983).However, forwarding the record of a closed session Level ill grievance hearing to thecommissioner on appeal is not a violation of the Act. Tex. Educ. Code § 7.057(c).

Access for board members: Trustees who attended a closed meeting may review thecertified agenda or tape recording of that meeting. Op. Tex. Att'y Gen. No. DM-227(1993). Likewise, current board members may review the tape recording or certifiedagenda of a closed meeting even if they did not attend the meeting. The board mayadopt procedures for review; however, the board may not absolutely prohibit a boardmember from reviewing the tape or certified agenda. The board may not give a boardmember a copy of the tape or certified agenda. In addition, a former board membermay not review the tape recording or certified agenda after he or she has left office.Op. Tex. Att'y Gen. No. JC-OI20 (1999); Tex. Att'y Gen. L0-98-033 (1998).

.

Thou Shalt Know Who May Come into Your Presence.vm.

Board's discretion: A board has the discretion to invite anyone it chooses to attendits closed session. Op. Tex. Att'y Gen. Nos. IC-0375 (2001), JM-OO06 (1983). Ifaclosed session is convened under the attorney consultation exception, however, theboard may not admit an adversary or individual whose presence would preventprivileged communication between the board and its attorney. Op. Tex. Att'y Gen.Nos. JM-0238 (1984), IC-0506 (2002).

.

. Superintendent's "right" to attend: A contractual provision requiring asuperintendent to attend all closed sessions, except those pertaining to thesuperintendent's contract or salary and benefits, does not violate the Act. On the otherhand, a contractual provision that confers on the superintenden~ a righ~ rather than anobligation, to attend all closed sessions may not be pennissible under the Act. Op.Tex. Att'y Gen. No. JC-O375 (2001).

6

C Texas Association of School BoardsLegal Services Division

. Ex£luding witnesses: A governmental body that is investigating a matter mayexclude a witness from a hearing (open or closed) during the examination of anotherwitness in the investigation. Tex. Gov't Code § 551.084. This provision is designedto protect the integrity of the hearing process by preventing witnesses from beingswayed by the testimony of other witnesses.

IX. Thou Shalt Not Blab.

. Criminal penalties: The Act itself does not provide criminal penalties for a personpresent in a closed meeting who discloses the substance of closed meetingdeliberations. Nevertheless, other serious penalties may apply. Op. Tex. Att'y. Gen.No. 1M-I071 (1989). For example, a board member may violate Texas Penal Codesection 39.06 if he releases "official information."

Civil actions: In additio~ a board member who releases closed session informationmay be subject to civil lawsuits. For example, a board member who repeats falseinformation discussed in a closed meeting could be held liable for defamation. Inadditio~ a board member who reveals closed session deliberations is likely violatingthe board's code of ethics policy or violating fiduciary duties to the district.

.

x. Thou Shalt Not Get Dragged into Court.

A. Civil Actions for Closed Meeting Violations

. Injunction or mandamus: Any interested person may sue for an injunction ormandamus to stop, prevent, or reverse a violation or threatened violation of the Act.Costs of litigation and attorneys' fees may be assessed against a board if a violation isfound. Tex. Gov't Code § 551.142.

Voidable action: Any action taken by the board in violation of the Act is voidableby a court. Tex. Gov't Code § 551.141; Piazza v. City o/Granger, 909 S. W.2d 529(Tex. App.-Austin 1995, no writ); Toyah v. Pecos-Barstow Indep. Sch. Dist., 466S. W.2d 377 (Tex. Civ. App.-San Antonio 1971, no writ); Op. Tex. Att'y Gen. No.H-594 (1975).

.

Corre&:Dng mistakes: If a board discovers that it has taken action in violation of theAct, the action may be corrected and reauthorized at a subsequent meeting. SeeLowerC%. RiverAutk v. City of San Marcos, 523 S.W.2d641 (Tex. 1975). Butactions taken in violation of the Act, even when subsequently corrected, may subjectboard members to criminal penalties.

.

7

~ Texas Association of School BoardsLegal Services Division

B. Criminal Actions for Closed Meeting Violations

.

.

Circumventing the Act: A board member commits a misdemeanor offense if he orshe "knowingly conspires to circumvent" the Act by meeting in numbers less than aquorum for secret deliberations. The punishment is a fine of $100 to $500,confinement for one to six months in county jail, or both. Tex. Gov't Code § 551.143.

Holding an illegal closed meeting: A board member commits a misdemeanor offenseif a closed meeting is not permitted by the Act, and the member knowingly calls or aidsin calling, closes or aids in closing, or participates in the lDllawful closed session ormeeting. The punishment is a fine of $1 00 to $500, confinement for one to six monthsin county jail, or both. Tex. Gov't Code § 551.144. The Texas Court of CriminalAppeals (the highest criminal court in Texas) has interpreted this statute to mean that aboard member can be convicted of a criminal violation ifhe or she participates in anillegal closed meeting, even if the board member does not know that the closed meetingis not authorized by the Act. Tovar v. State, 978 S. W.2d 584 (Tex. Crim. App. 1998)(en banc). It is a defense to prosecuti~ however, that the board member acted inreasonable reliance on a written opinion of a court, the attorney general, or the schooldistrict's attorney. Tex. Gov't Code § 551.144(c).

Failing to record a closed meeting: A board member commits a misdemeanor offenseifhe or she participates in a closed meeting knowing that a certified agenda or taperecording is not being kept. Tex. Gov't Code § 551.145.

Disclosing a certified agenda: A person commits a misdemeanor offense if theperson, without authority, knowingly discloses to a member of the public the certifiedagenda or tape recording of a lawfully closed meeting. In addition, a person injuredor damaged as a result of the disclosure may seek actual damages, attorneys' fees,and punitive damages as remedies in a civil lawsuit. Tex. Gov't Code § 551.146.

.

8

C Texas Association of School BoardsLegal Services Division

C Texas Association of School BoardsLegal Services Division

Helpful Resources:Texas Open Meetings Act

T ASH Legal Senrices DivisionThe School OffICial's Guide to the Texas Open Meetings ActThis recently updated and revised book answers the most common questions about the OpenMeetings Act and assesses the ongoing interpretations of the Act by the comts and the attorneygeneral. It includes procedures for closed meetings, an expanded set of meeting agenda examples foruse in your district, and information on meeting notices and enforcement of the Act. 02002

Pocket Guide to The Texas Open Meetings Act111is convenient, pocket-sized flip chart includes the basics on the Texas Open Meetings Act,including the definition of "meeting, " exceptions to allow "closed meeting, " notices, and more.

Introduced at SU 2002 and inspired by a Leadership TASB team, this handy pocket reference will beyour first line of defense to answer those thorny OMA questions on the spot. C 2002.

72 Hours: Investigating the Open Meetings ActThis one-hour training video offers a light-hearted look at the legal requirements of the OpenMeetings Act. The video package provides the basics of conducting legal and effective school boardmeetings and explores scenarios ~ are likely to enco\D1ter. Extensive written materials includedUpdated to reflect 1999 legislative changes. 01999.

The Second Half: Going Deep into the Texas Open Meetings ActIn less than an hoW', this entertaining video package will cover OMA basics and push YoW' board todte next level by answering some tough questions. When can board members communicate outsideof board meetings? How does dte new definition of "meeting" change YOW' posting practices? Howshould a board address a subject that's not on dte agmda? This video package converts tough topicsinto simple scenarios and an easy way for YoW' team to earn one hoW' of board training ~t. 02000.

OutlinesIHandoutsLegal Services offers outlines on a number of legal topics, including the Open Meetings Act.

Open Meetings Act FAQ'shttD:/ /www.tasb.0r2/0r0ducts services/le2a1/faa oma.shtml

T ASH Policy ServiceBE series in your district's policy manual.

TASB Leadership Team Servi&:es:Effective Meetings: Your Leadership Makes the Difference<:>2001 (book and CD ROM available)

Tens Attorney GeneralTaas Open Meetings Ad HandbookOnline: httD:/ /www.oae:.state.!x.us!AG Publications/txts/ooenmeetine:s2000.htm

~ Texas Association of School BoardsLegal Services Division

SAMPLE: NOTICE OF REGULAR MEETING

Notice of Regular MeetingBoard of Trustees

Star of Texas Independent School DistrictMarch 25, 2002

A regular meeting of the Board of Trustees of the Star of Texas Independent School District will beheld on March 25,2002, beginning at 7 p.m., in the Board conference room of the Star of TexasIndependent School District at 54321 East Center Avenue, Center Star, Texas.

The subjects to be discussed or considered or upon which any formal action may be taken are listedbelow. Items do not have to be taken in the same order as shown on this meeting notice.

Unless removed from the consent agenda, items identified within the consent agenda will be actedon at one time.

1.2.

3.

4.5.6.7.8.

9.

10.11.12.

Public comments/audience participationConsent agendaa. Minutes of the FebnJaIY 25,2002, meeting of the Boardb. Resolution to affimt Child Safety Monthc. Monthly financial reportContracts with Region XXX Education Service Center regarding cooperative purchasingprogram and cooperative special education programConsultation with school district attorney concerning pending condemnation lawsuitSettlement of pending condemnation lawsuitPresentation by personnel director concerning future district staffing requirementsTexas Education Agency accreditation audit/inspectionPolicy changesa. DEC(LOCAL): Employee compensation and benefits-leaves and absencesb. FOB(LOCAL): Student disciplineDistrict employees and officersa. Trustee resignationb. Appointment to fill trustee vacancyc. Report on district salary studyd. Resignation of administrative employeesAcquisition of real estate for possible school sitePurchases of supplies and equipmentPublication for competitive bid notices regarding contract for renovation to industrial artsbuilding

C Texas Association of School BoardsLegal Services Division

13. Superintendent's reporta. Progress of construction of high schoolb. Resignation of teachersc. Student achievementd. Budget issues

If, during the course of the meeting, discussion of any item on the agenda should be held in a closedmeeting, the Board will conduct a closed meeting in accordance with the Texas Open Meetings Act,Texas Government Code, Chapter 551, Subchapters D and E. Before any closed meeting isconvened, the presiding officer will publicly identify the section or sections of the Act authorizingthe closed meeting. All final votes, actions, or decisions will be taken in open meeting. [See

BEC(LEGAL)].

This notice was posted in compliance with the Texas Open Meetings Act on March 22,2002 at 3 :00p.rn.

For the Board of Trustees

~ Texas Association of School BoardsLegal Services Division

SAMPLE: CERTIFIED AGENDA FORM[On School Letterhead]

CER'.'lt'lED AGENDA OF CLOSED SESSIONMeeting of (Date)

CONFIDENTIAL: No one shall, without lawful authority, knowingly disclose to a member of thepublic this certified agenda of a closed meeting. A person who violates this subsection commits aClass B misdemeanor and may be liable to any party injmed or damaged by the disclosure. TexasGovernment Code § 551.146(a).

Statement of Beginning of Closed Session. The presiding officer annolDlced at the beginningof the closed session:

I

"The Board of Trustees on (date), beginning at _.m. (time), convened inclosed session in accordance with the Texas Open Meetings Act. "

n. Subjects Discussed in the Session Closed to the Public:

(Subject No. 1)

(Subject No.2)

(Subject No. 3)

Statement at End of Closed Session. The presiding officer announced at the end of theclosed session:

ill.

"The Board ended its closed session at _.m. (time) on (date)."

N. Record of Further Action Taken, if Any, on.Above Items in the Subsequent Open Session:

(Subject No. 1)

(Subject No. 2)-

(Subject No.3)

v Certification by Presiding Officer. I hereby certify that the foregoing is a true and correctrecord of the closed session proceedings on the above date.

Signature

Presiding Officer (type name)

C T cxas Association of School BoardsLegal Services Division

SAMPLE: CERTIFIED AGENDA[On School Letterhead]

CERTD'lED AGENDA OF CLOSED SESSIONMeeting of March 25, 2002

CONFIDENTIAL: No one shall, without lawful authority, knowingly disclose to a member of thepublic this certified agenda of a closed meeting. A person who violates this subsection commits aClass B misdemeanor and may be liable to any party injured or damaged by the disclosure. TexasGovernment Code § 551.146(a).

Statement of Beginning of Closed Session. The Presiding officer annolU1ced at the beginningof the closed session:

I.

"The Board of Trustees on March 25, 2002, beginning at 7:45 p.rn., convened in a closedsession in accordance with the Texas Open Meetings Act. "

Subjects Discussed in the Session Closed to the Public.n.

1. Evaluation and consideration of two-year extension of contract of the high schoolprincipal, Ms. Jane Doe

2. Implementation of a sniffer dog program3. Market value of real estate proposed as high school site4. Expulsion of Johnny Roe

Statement at End of Closed Session. The presiding officer announced at the end of theclosed session:

m

"The Board ended its closed session at 9 p.rn. on March 25, 2002."

IV. Record of Further Action Taken, if Any, on Above Items in the Subsequent Open Session.

1. Board approved one-year extension of the principal's contract2. Board approved contract with sniffer dog handler company3. No action taken4. Board voted to expel student

v. Certification by Presiding Officer. I hereby certify that the foregoing is a tJUe and correctrecord of the closed session proceedings on the above date.

Signature

Presiding Officer (type name)

THE SUPREME COURT OF TEXASPost Office Box 12248Austin. Texas 78711 -- ~ ~ .46,}.1312

May 29, 2003

Mr. George W. Bramblett, Jr.Haynes &: Boone, LLP901 Main Street, Suite 3100Dallas, TX 75202-3789

Mr. Mark Ryan TrachtenbergHaynes and Boone, U.P1000 Louisana Street, Suite 4300HoUSton, TX 77002-5012

Mr. Doug W. RayRay Wood &: Bonilla LLP2700 Bee Caves Road 1200Austin. TX 78746

Ms. Julie Caruthen PanteyOffice of the Solicitor General of TexasPost Office Box 125-48Austin, TX 78711-2548

Ms. Letici2 Marie SaucedoMexican American Lep1 Defense (MAlDEf)140 E. Houston St., Ste. 300San Antonio, TX 78205

Case Number 02-0427Court of Appeals Number: OJ..Ql-00491-CVTrial Court Number: GV100528

WEST ORANGE-COVE CONSOLIDATED lSD,. ET AL.v.FEmE ALANIS, IN HIS OFFICIAL CAPAcrrY AS nIE COMMISSIONER OFEDUCATION, ET AL.

Dear Counsel:

Today the Supreme Court of Texas issued the following opinions in the above-referenced case.See enclosed opinions.

Sincerely.

-1~~~::!~~~-aukcc: The Hon. B. B. Schraub

Paul PomeroyMr. Tom ThomasJames C. HarringtonMs. Diane O'Neal, ClerkMs. Amalia Rodriguez-Mendoza

IN THE SUPREME COURT OF TEXAS

No. 02-0427

WEST ORANGE-COVE CoNSOLIDATED I.SD.ET AL., PEnTIONERS

FELIPE ALANIS, IN IDS OFFICIAL CAPACITY AS

THE COMMISSIONER OF EDUCAnON, ET AL., REsPONDENTS

ON PETmON FOR. REVIEW FROM nfECoURT OF APPEALS FOR. THE 'nI1RD DISTR.ICT OF TExAS

Argued March 27, 2003

JUS11CE HECKT delivered the opinion of the Court, in which CHIEF Jus11cePl ml.IPS, JumCEOWEN, JUS11CE 0 'NEn.L, JumCE JEFFERSON, JUS'nCE SCHNEIDER, and JUS11CE W AINWRIOHr joined.

JUSTICE ENOCH filed a concuning opinion.

JumCE SMmf filed a dissenting opinion.

Article ~ section l-e of the Texas Constimtion states: -No State ad valorem taxes shall

be levied upon any property within this State.8' We have held that 8[a]n ad valorem tax is a state tax

when it is im~ed directly by the State or when the State so completely controls the levy,

TEx. CONlY. lit. vm. . l-e

assessment and disbursement of revenue, either directly or indirectly, that the [taxing] authority

employed is without meaningful discretion.-2

The maintenance and operation of Texas public schools are funded mostly by ad valorem

taxes levied by local school districts under comprehensive state regulation that, among other things,

caps the rates at which districts can tax and redistributes local revenue among districts. In 1995, we

held that the State's control of this school funding system bad not made local property taxes an

unconstitutional state tax because school districts retained meaningful discretion in generating

revenue, but we foresaw a day when increasing costs of education and evolving circumstances might

force local taxation at maximum rates.3 At that point, we said, the conclusion that a state property

tax had been levied would be "unavoidable.,.

In the case before us, four plaintiff school districts allege that that day has come.

Specifically. they contend that they and other districts have been forced to tax at maximum rates set

by statute in order to educate their students. These taxes, they say, have become indistinguishable

from a state ad valorem tax prohibited by article vIll, section I-e.

The district court dismissed the case on the pleadings, holding that a constitutional violation

could not be alleged because far fewer than half of Texast 1,035 school districts were taxing at the

maximum rates aJlowed. The court of appeals affimled, focusing not on bow many districts were

l Carrollton-Fan71en Branch Indep. Sch. Dut. \I. Edgewood lndep. Sch. Di.st., 826 S. W.2d 489, S02 (Tex.

1992) [Edgewood 0/).

'Edgewood Indep. Sch. Dirt. v. MellO, 917 S.W.2d 717, 738 (Tex. 1995) [Edgewood lYJ.

41d.

2

taxing at maximwn rates but on whether any of them were forced to do so just to provide an

accredited education as defined by statute.' We disagree with both courts and therefore reverse and

remand the case to the trial court for further proceedings

I

This is the fifth in a series of cases to come bef~ us challenging the constitutionality of the

Texas public school finance system on various grounds.' Central to some of the cases and basic to

them all is article vn. section I of the Texas Constitution, which states:

A general diffilSion of knowledge being essential to the preservation of the libertiesand rights of the people, it shall be the duty of the Legislature of the State to establishand make suitable provision for the support and maintenance of an efficient systemof public free schools.7

By assigning to the Legislature a duty, this section both empowers and obligates. It gives to the

Legislature the sole authority to set the policies and fashion the means for providing a public school

system.. Thus we have said that 8[w]e do Dot prescribe the means which the Legislature must

employ in fulfilling its duty .-9 But the provision also requires the Legislature to meet three

, 78 S. W.3d S29 (Tex. Aw.-Austin 2002)

, Ed~ Indep. Sch. Dirt. Y. Kirby, m s. W.2d 391 (Tex. 1989) [Edpwood /); ~ Indep. SciL Dirt.". Kirby, 804 S.W.2d 491 (Tex. 1991) [;EdB~1I]; Edgewood m,.rI'PI'a note 2; Edgewood JY"rupra DOte 3.

7 TEX. CONST. U1. vn. § 1

. MII",me v. Marrs, 40 S.W.2d 31,36 (Tex. 1931) (.SiDce the Legislature hu the mandatory duty to make

suitable provision for the support and maintenance of an efficient system of public free school.. and bas the power topus any law relative tbcreto, Dot pobibited by the CoosbbJbc... it ~~ follows that it bas a choice in the ~~of methods by which the object of the organic law may be effectuated. The Legislature alone is to judge what meansarc necessary and appropriate for a purpose which the CoD5titution makes legitimate. 1.

, EdgrltlOod //,804 S. W.2d at 498

3

standards. First, the education provided must be adequate; that is, the public school system must

accomplish that "general diffi1sion of knowledge. . . essential to the preservation of the liberties and

rights of the people-. Second, the means adopted must be 8suitable8. Third, the system itself must

be Mefficien~. M[T]hese are admittedly not precise tem1S,. as we have acknowledged, but Mthey do

provide a standard by which this court must, when called upon to do so, measure the constitutionality

of the legislature's actions,-IO The final authority to detennine adherence to the Constitution resides

with the Judiciary.lt Thus, the Legislature has the sole right to decide how to meet the standards set

by the people in article vn, section 1, and the Judiciary bas the final authority to determine whether

they have been met 12

In 1989, we decided Edgewood I, the first case challenging the constitutionality of the public

school finance system under article vll, section 1. The system's principal component for funding

10 Edgewood I, 777 S. W.2d at 394; accord Edgewood lV, 917 S. W.2d at 736.

II Marbury v. Madison, 5 U.S. (1 Crmch) 137, 176-178 (1803) (8Jbe powers of the 1egislabUe are defined and

limited; and that d1ose limits may not be mistakm or forgotten, the constitution is written. To what purpose are powerslimited, and to what pwpose is that limitation committed to writing, iftbese limits may, at any time, be passed by thoseintended to be restrained? . .. So if a law be in OWOSition to the CODSIituaoo; ifboth the law and the constitution applyto a particular case, so that the cowt must either decide the case conformably to the law, disregarding the constitution;or confonnably to the constitution, disregarding the law; the court must determiDe which of these confficting rulesgoverns the case. This is of the very essence of judicial duty. 1; Lo'IIe v. W"Ilcox, 28 S. W.2d 515, 520 (Tex. 1930) (.SinceMarbury v. Madison, [5 U.S. (1 Cranch) 137, 166-167 (1803)], the coW1l ofJast resort of the several states have almost

universally followed the opinion of Chief Justice Manhal1 to the effect that it is clear that: 'Where a specific duty isassigned by law, and individual rights depend upon the performance of that duty, . . . the individual who considershimself injured. bas a right to resort to the laws ofhis country for a remedy.'i.

12 Edgewood w, 917 S. W.2d at 726 (8This Court's role under OW' Consti~on's separation of powers provision

should be ODe ofresttaint We do not dictate to the LegisJatwe how to discharge ita duty. As prominent as this Com'srole bas been in recent years on this impo11aDt issue, it is subsidiary to the constitutionally conferred role of theLegislature. The people of Texas have themselves set the standard for their schools. Our responsibility is to decidewhether that standard has been satisfied, not to judge the wisdom of the policy choices of the Legislature, or to imposea different policy of oW" own choosing,-).

4

maintenance and operations was the Foundation School Program, a two-tiered mechanism that the

Legislature had set up in 1975.13 The first tier was designed to fund a basic education. I. Every

school district that could not, by taxing at a specified minimum rate, generate a certain level of

revenue per'student in .weighted average daily attendance8 (.W ADA 8 - weighted by taking into

account special needs and conditions such as special or bilingual education) was given state fun~

to make up the difference. IS Despite its stated purpose, first-tier funding did not cover the cost of

meeting bare educational requirements mandated by the Legislature.16 The system' s second tier

provided state funds to guarantee a certain level of additional revmue per student in W ADA for exh

penny a school district increased its tax rate above the prescribed minimum.11 School district tax

rates were capped at $1.50 per $100 property valuation.' as they bad been for d-~A~..9 Smaller

components of the school finance system were the Available School Fund established by the

IJ Ed~ I, 777 S. W.2d It 392; Edpwood H, 804 s. W.2d It 495; Edgrft/Ood m, 826 S. W.2d It 496; TExASLEGIS LA 11VE BUDGET BoARD, FINAJ«:rNG PuBuc EooCA TION IN TEXAS KlNDBRGARTEN THRoOOH GRADE 12LEGIsLATIVE PRIMER It 25-26 (2d cd. 2000) [hcrciDaftcr LBB PRWER].

14 Edg,WQod 0, 804 S. W.2d at 49S

'S[d.

., Edg,WQod 1. m S. W.2d at 392.

., Ed,~ O. 804 S. W.2d at 495.

.8 Act of June 2, 1969,6151 Lea., R.S.. ch. 889, f I, 1969 Tex. Gen. l.aWI273S, 289S-2896.

I' See Act of May 17, 1945, 49th Leg., R.S.. ch. 304, § I, 1945 Tcx. Gal. LaWl488.

5

Constitution. ZO which provided all school districts about $300 per student, 21 and federal funding.n

Facilities and other expenses were funded separately.23

Then. as now, local ad valorem taxes supplied more than half the funding for public

schools,34 the tax bases of the more than 1,000 school districts, and consequently the tax revenue

available to them, were vastly different, 2S and state tax revenues were inadequate to level local

funding disparities.» At that time. local tax revenues were not redistributed among school districts

as they are now. We described the situation thus:

There are glaring disparities in the abilities of the various school districts toraise revenues from property taxes because taxable property wealth varies greatlyfrom district to district. The wealthiest district has over $14,000,000 of propertywealth per student, while the poorest bas approximately $20,000; this disparity

m TEX. CONST. lit. vn. § S(a) (8TIJe priDa.-I of all bonds and other fImds, and the principallrisiDg from the

sale of llndl hereinbefore set 8put to said school fund, IbaI1 be the pelmlDCDt school fimd, md all the interat derivabletherefrom and the taxa herein authorized md levied Ibal1 be the available ~l fImd. The available school fund sballbe applied annually to the support of the free public schools. 1.

ZI Ed~n. 804 S.W.2d 11495 0.10.

22 Edg~ I, m s. W.2d at 392.

DId.

14ld. ('Of tolal education costa, the state provides about forty-two percent. school districu provide about fifty~ 8Dd die rsn-ifttt ~~ from vario.. other IOUIeea including federal funds. 1; ..- LBB PRIMER. .nIprII Dote13. at 1 (-For the 2000-01 bienniwn, state taxes are estimated to generate approximately 44 ~t of the tolal fundsand loc.aI school district property taxes 47.5 percent of the total. The federalaovernmeot provides approximately 8.5percent of the revenue, most of it e8rm8rked for specific federal education pI'OIIImS.1.

~ Ed~ I, m s. W.2d at 392-393; LBB PRIMER..nIprG DOte 13, It 6 (sIatiDIo u of2000: ~ are 1,035

school districts in the Itate. The tax base 8ID0IIg 1beIe districts varia considerably. K.encdy County Wide ISD bu morethan $3 million in property wealth per enrolled student, while Bola ISD bas less than $10,000 in property wealth perenrolled student 8).

26 Edg~od /,777 S. W.2d at 392;..- LBB PRIMER, mpra note 13, at 21 (stating, as of 2000: ~e nwnber

of districts subject to the recapture provisions range from 85 to 100 in a given year. The associated recapture revenueis anticipated to total 5949.8 million in 1be 2000.01 biennium. j.

6

reflects a 700 to 1 ratio. The 300,000 students in the lowest-wealth schools have lessthan 3% of the state's property wealth to support their education while the 300,000students in the highest-wealth schools have over 25% of the state's property wealth;thus the 300,000 students in the wealthiest districts have more than eight times theproperty value to suppon their education as the 300,000 students in the poorestdistricts. The average !Jloperty wealth in the 100 wealthiest districts is more thantwenty times greater than the average property wealth in the 100 poorest districts. . . .

. . .

Because of the disparities in district property wealth, spending per studentvaries widely, ranging from $2,112 to $19,333. Under the existing system, anaverage of $2,000 more per year is spent on each of the 150,000 students in thewealthiest districts than is spent on the 150,000 students in the poorest districts.

The lower expenditures in the property-poor districts are not the resUlt of lackof tax effort. Generally, the property-rich districts can tax low and spend high whilethe property-poor districts must tax high merely to spend low. In 1985-86, local taxrates ranged from S.09 to SI.55 per SI00 valuation. The 100 poorest districts had anaverage tax rate of 74.5 cents and spent an average of $2,978 per student. The 100wealthiest districts had an average tax rate of 47 cents and spent an average of $7,233per student. . .. A person owning an S80,OOO home with no homestead exemptionwould pay SI,206 in taxes in the east Texas low-wealth district ofLeveretts Chapel,but would pay only S59 in the west Texas high-wealth district of Iraan-Sheffield.Many districts have become tax havens.77

The plaintiffs in Edgewood 1 asserted that this public school finance system ~ not efficient

within the meaning of article vn, section 1. .'Efficimt,'. we said, .conveys the meaning of effective

or productive of results and connotes the use of resources so as to produce results with little waste;

this meaning does not appear to have changed ov~ time,8n Givm these circwnstances, a unanimous

Court had little difficulty concluding that the constitutional standard of efficiency had not been met:

27 Edgewood 1, m s. W.2d at 392-393.

J8 [d. at 395 (citations omitted).

.,

We hold that the state's school financing system is neither financiallyefficient nor efficient in the sense of providing for a 8general diffilsion ofknowledge8statewide, and therefore that it violates article vll, section I of the TexasConstitution. Efficiency does not require a per capita distribution, but it also doesnot allow concentrations of resources in pro-~"j-rich school districts that are taxinglow when property-poor districts that are taxing high cannot generate sufficientrevenues to meet even minimum standards. There must be a direct and closeconelation between a district's tax effort and the educational resources available toit; in other words, districts must have substantially equal access to similar revenuesper pupil at similar levels of tax effort. Children who live in poor districts andchildren who live in rich districts must be afforded a substantially equal opportunityto have access to educational funds. Certainly, this much is required if the state isto educate its populace efficiently and provide for a general diffusion of knowledgestatewide.29

Because constitutional efficiency does not require absolute equality of spending, we

expressly acknowledged that -local communities would [not] be precluded from supplementing an

efficient system established by the legislature., but we added that -any local enrichment must derive

solely from local tax effort. 830 In other words, the constitutional standard of efficiency requires

substantially equivalent access to revenue only up to a point, after which a local community can elect

higher taxes to .supplemen~ and .enrich. its own schools. That point, of course, although we did

not expressly say so in Edgewood I, is the achievement of an adequate school system as required by

the Constitution. Once the Legislamre has discharged its duty to provide an adequate school system

for the State, a local district is free to provide enhanced public education ~rtunities if its residents

vote to tax themselves at higher levels. The requirement of efficiency does Dot preclude local

supplementation of schools. Although we were not called upon in Edgewood I to consider what

a [do at 397.

)lId. at 398,

8

constitutional adequacy entails, the interrelationship between the standards of adequacy and

efficiency was fundamental to our reasoning in that case.

We ordered that state funding of public schools cease on May I, 1990, unless the Legislature

conformed the system to meet constitutional standards}1 Although we expressly did not 8instruct

the legislature as to the specifics of the legislation it should enact . or order it to raise taxes,.» we

cautioned that -[a] band-aid will not suffice; the system itself must be changed. -33 Eight months

later, in a sixth special session, the Legislanue adjusted the system to provide incentives it believed

would 8achieve substantial equity among the districts that ~'!C:-c!.te 95% of our studcnts.834 The

plaintiffs in Edgewood I inunediateiy challenged this legislation, Senate Bill 1. again OD the ground

that the system was not efficient within the meaning of article VB, section 1 of the Constitution.

Without attempting to determine whether the incentives added by Senate Bill I could realistically

reach their goals, we concluded in Edgewood n that the system as a whole remaL~ constitutionally

inefficient:

Even if the approach of Senate Bill I produces a more equitable utilization of stateeducational dollars, it does not ~edy the major causes of the wide opportunity gapsbetween rich and poor districts. It does not change the boundaries of any of thecurrent 1052 school districts, the wealthiest of which continues to draw funds froma tax base roughly 450 times greater per weighted pupil than the poorest district Itdoes not change the basic funding allocation, with approximately half of alleducation funds coming from local property taxes rather than state revenue. And it

)\ [d. at 399; accord Edgrwood II, 804 S. W.2d at 493

u~/.ms.W.2d.t399.JJ [d. at 397.

J4 Edgewood O. 804 SoW old at 49S

9

makes no attempt to equalize access to funds among all districts. By limiting thefunding fonnula to disaicts in which 95% of the students attend school, theLegislature excluded 132 districts which educate approximately 170,000 students andharbor about 15% of the property wealth in the state. A third of our students attendschool in the poorest disaicts which also have about 15% of the property wealth inthe state. Consequently, after Senate Bill I, the 170,000 students in the wealthiestdistricts are still supported by local revenues drawn from the same tax base as the1,000,000 students in the poorest districts.

These factors compel the conclusion as a matter of law that the State basmade an unconstitutionally inefficient use of its resources. The fundamental flaw ofSenate Bill 1 lies not in any particular provisions but in its overall failure torestructure the system. 3'

We rcaffinncd that efficiency did not preclude local supplementation of school funding.36

On rehearing, we stressed:

The current system remains unconstitutional not because any uncqua1iz~ localsupplementation is employed, but because the State relies so heavily on unequalizedlocal funding in attempting to discharge its duty to -make suitable provision for thesupport and maintenance of an efficient system of public free schools.- Once theLegislature provides an efficient system in compliance with article vn, section 1, itmay, so long as efficiency is maintained, authorize local school districts tosupplement their educational resources if local property owners approve an additionalI ocal property tax. 3 7

B~~~ the Legislature was then in session, we required that it respond without delay, and

it promptly enacted Senate BiIl3S1.3I The legislation created 188 new 8county education districts-

,s [d. at 496.

J6 Id. at 495 0.11 (-ne question of local enrichment continues to be controlled by this Court'. opinion in

Edgewood I, 777 S. W.2d at 397-98.-).

)7/d. at SOO (emphasis in original) (citation aDd footnotes omiUed).

JI Ed~ m, 826 S. W.2d at 492.

10

In most instances, a CED comprised the school districts in a single county ,39 The sole purpose of

dIe CEDs was to levy, collect, and distribute property taxes among their component school districts,

respectively, in effect consolidating school districts' tax bases while leaving them in control of their

own schools. ~ CED tax rates and distributions were prescribed by statute to ensure unifonnity. This

state-controUed tax-base consolidation Mreduced the geographical disparities in the availability of

revenue for education"' and was not challenged as failing to satisfy the efficiency standard of article

VB. section 1. It was. however. challenged as imposing a state ad valorem tax in violation of article

vm. section l-e of the Constitution. We sustained that challenge in Edgewood m:

Senate Bill 351 mandates the tax CEDs levy. No CED may decline to levythe tax. The tax rate for aU CEDs is predetennined by Senate Bill 3S I. No CED cantax at a bigb~ rate or a lower rate under any circwnstanccs. Ind~ the very purposeof the CEDs is to levy a unifono tax statewide. The distribution of the proceeds isset by Senate Bill 351. No CED bas any discretion to distn"bute tax proceeds in anymanner except as ~ by statute. Every function of the CEDs is purelyministerial. If the State mandates that a tax be levied, sets the rate, and prescribes thedistribution of the proceeds, the tax is a state ~ regardless of the instnuncntalitywhich the State may choose to USC.42

To place the siOlation created by Senate Bill 35 I in the broader context of the. constitutional

prohibition of state ad valorem tax. we explained:

An ad valorem tax is a state tax when it is imposed directly by the State orwhen the State so completely controls the levy, assessment and disbursement ofrevenue, either directly or indirectly, that the authority employed is without

'9 [d. at 498.

-1d.

4. [d. at 500.

G [d. (citation and footnote omitted)

11

meaningful discretion. How far the State can go toward encouraging a local taxingauthority to levy an ad valorem tax before the tax becomes a state tax is difficult todelineate. Clearly, if the State merely authorized a tax but left the decision whetherto levy it entirely up to local authorities, to be approved by the voters if necessary,then the tax would not be a state tax. The local authority could freely choose whetherto levy the tax or not To the other extreme, if the State mandates the levy of a taxat a set rate and prescribes the distn'bution of the proceeds, the tax is a state tax,irrespective of whether the State acts in its own behalf or through an intermediary.Between these two extremes lies a spectrum of other possibilities. If the Staterequired local authorities to levy an ad valorem tax but allowed them discretion onsetting the rate and disbursing the proceeds, the State's conduct might not violatearticle vIll, section l-e. It is difficult, perhaps impossible, to define for everyconceivable hypothetical precisely where along this continuum such taxes becomestate taxes. Therefore, if the Legislature, in an effort to remedy Senate Bill 3S I withas few changes as possible, chose to inject some additional element of leeway in theassessment of the CED tax, it is impossible to say in advance whether that elementwould remove the tax from the prohibition of article vm, section l-e. Each casemust necessarily turn on its own particulars. Although parsing the differences maybe likened to dancing on the bead of a pin, it is the Legislature which bas created thepin, summoned the dancers, and called the tune. The Legislature can avoid theseconstitutional conundra by choosing another path altogether."

We also held that by levying a tax without an election, the CEDs violated article vn. section 3(e)

of the COnstitution.44

We delayed enforcem=t of our niling for more than a year, until the end of the next regular

session of the Legislarure in 1993.4' During that session, the Legislarure's tint reaction was to

U [d. at S02-S00.

.. Id. at 506; Sft !EX. CONST. art. VB. § 3(e) (~e LegislatuR shall be authorized to pea laws for the

assessment and collection of taxes in aU school diltricts and for the management and control of the public school orsclx>Ols of IUC;b diltricts, whether such districts ~ co~ of territory whoUy within a county or in parta of two ormore counties, and the Legislature may authorize an additioaal ad valorem tax to be levied and coUected withm aUschool districts for the further maintenance of public free ~1s, IDd for the er=on - .pneot of 8:Iloo1 OOildingstherein; provided that a majority of the qualified voters of the district voting at an election to be held for that purpose,shall approve the tax. 8).

4S Edgewood U, 826 sw2d at S22-sn.

12

attempt to amend the Constitution. A proposed amendment that would have rewritten article W,

section I to remove its standards and conunit the responsibility for public education to local school

districts was introduced but Dot reported out of committee." A proposed amendment that would

have authorized the system structured by Senate Bill 3S 1 passed the Senate and narrowly passed the

House47 but was soundly defeated by the people before the session ended. 41 The Legislature then

enacted Senate Bill 7.49

Senate Bill 7 returned to the two-tiered Foundation School Program. $0 the buic structure of

which remains in place today." As before, M(t]hc stated purpose ofTi=: 1 is to guarantee 'sufficient

financing for all school districts to provide a basic program of education that meets accreditation and

other legal standards. '.52 At a minimum $0.86 tax rate, a school district that cannot generate revenue

equal to a "basic a11otmcn~ per student in WADA-in 1993, $2,300,'3 and today, $2,537," subject

46 Tex. HJ. Rea. 10, HJ. ofTex., 13rd LeJ., KoS. 184 (1993).

47 Tcx. SJ. Res. " 13rd lei., R.S., 1993 Tex. OeD. Laws 5560 (passed Senate 21-41nd House 102-43).

.. YotuonProposedAmerldmentr to tire TQQ.S o'lI.rtiIutioIt 1875 -May, 1993, at 21, repriIIIed in [4] 1993 Tex.

Gen. Laws (amendment submitted May 1, 1993, defeated 155,411 to 1,293,224); EdgrIIJOod /Y, 911 S.W.2d at 121.

.. Act of May 28, 1993, 73n1 Lei., R.S., ch. 347,1993 Tex. Ocn. Lawl 1479 [hereinafter C1Jap1er 347]; see

Edgewood lY, 917 S.W.2d at 727.

50 Edgrf4'Ood /Y. 917 S. W.2d 81 727

5. LBB PRIMB. supra Dote 13. at 2.

52 Edgewood !Y, 917 S. W .2d It 727 (quoting fonner TEx. BDUc. CoDE § 16.002(b), Chapter 347, mprG note

49, at 1492, now TEX. EDUC. CoDE f 42.002(bXIXA»;.fa LBB PRJNER, mprG note 13, at 2.

II Cbaptcr 347, supra Dote 49, at 1498 (codifying fonncrTEx. BDUc. CODE § 16.101)

,. TEX. BDtx:. CODE f 42.101

13

does not cover the cost of an education that meets legislated accrediting standards.57 Tier 2 provides

sometimes referred to as Tier 3 in the systcm.62

SS LBB PRIMER, silpra note 13, at 14-16.

58 Sa LBB PRIMER. supra note 13, at 2.

at 1514).

. TEX. EDUc. CODE § 42.302;.fee LBB PRIMER..rupro note 13, at 16-17.

62 See LBB PRIMER. supra DOte 13. at 2, 19-20.

14

$280,000 in 1993," and $305,000 today" - must transfer the excess, or the tax revenue generated

from it, either actt1ally or effectively t so as to provide funding for school districts with less wealth. 66

The local tax revenue Mrecaptured8 and redistributed by this mechanism amO\Ulted to almost S I

billion in 2000.67 This taxable wealth equalization scheme, dubbed by some MRobin Hood-,

eliminates the geographical disparities in available revenue among school districts that characterized

the pre-I993 venion of the Foundation School Program

The public school finance system set up by Senate Bill 7 was challenged on numerous