plus some initial thoughts!. economics what is needed for hsc success?

TRANSCRIPT

Plus some initial thoughts!

ECONOMICS

What is needed for HSC SUCCESS?

HSC SUCCESS

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

IN THE CLASSROOM

DEVELOP LISTENING & QUESTIONING

SKILLS

USE LESSONS TO CLARIFY WORK DONE

ELSEWHERE

MAKE NOTES OF BOARDWORK &

O/HEADS

IDENTIFY YOUR PREFERRED LEARNING

STYLE & MAKE IT WORK FOR

YOU

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

IN THE CLASSROOM

DEVELOP LISTENING & QUESTIONING

SKILLS

USE LESSONS TO CLARIFY WORK DONE

ELSEWHERE

MAKE NOTES OF BOARDWORK &

O/HEADS

IDENTIFY YOUR PREFERRED LEARNING

STYLE & MAKE IT WORK FOR

YOU

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

DO BOOKWORK TO KEEP PACE WITH

CLASSWORK

USE WORKBOOK FOR REVISION & SELF-

TESTING

READ NEWSPAPERS & BRING ARTICLES

TO CLASS

DO ALL THE HOMEWORK SET

CREATE GLOSSARIES OF

KEY TERMS

IN THE CLASSROOM

DEVELOP LISTENING & QUESTIONING

SKILLS

USE LESSONS TO CLARIFY WORK DONE

ELSEWHERE

MAKE NOTES OF BOARDWORK &

O/HEADS

IDENTIFY YOUR PREFERRED LEARNING

STYLE & MAKE IT WORK FOR

YOU

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

IN THE CLASSROOM

DEVELOP LISTENING & QUESTIONING

SKILLS

USE LESSONS TO CLARIFY WORK DONE

ELSEWHERE

MAKE NOTES OF BOARDWORK &

O/HEADS

IDENTIFY YOUR PREFERRED LEARNING

STYLE & MAKE IT WORK FOR

YOU

HSC SUCCESS

BECOME AN INDEPENDENT &

LIFE-LONG LEARNER

OUTSIDE THE CLASSROOM

DO BOOKWORK TO KEEP PACE WITH

CLASSWORK

USE WORKBOOK FOR REVISION & SELF-

TESTING

READ NEWSPAPERS & BRING ARTICLES

TO CLASS

DO ALL THE HOMEWORK SET

CREATE GLOSSARIES OF

KEY TERMS

DEVELOP AN INDEPENDENCE IN LEARNING

IN THE CLASSROOM

DEVELOP LISTENING & QUESTIONING

SKILLS

USE LESSONS TO CLARIFY WORK DONE

ELSEWHERE

MAKE NOTES OF BOARDWORK &

O/HEADS

IDENTIFY YOUR PREFERRED LEARNING

STYLE & MAKE IT WORK FOR

YOU

YOU WILL BE SUCCESSFUL IF YOU ARE AN ACTIVE LEARNER NOT A PASSIVE LEARNER

SUCCESS!!

THIS TRANSLATES INTO:

15 - 20 MINUTES

5 NIGHTS A WEEK!!

From the Syllabus: Introduction to Economics Students learn to:Examine economic issues Identify* the opportunity costs involved in economic decisions made by

individuals, businesses and governments at local, state and national levels Examine* the ways that the economic problem affects individuals at

different income levels Examine* the implications of unemployment and technological change

using production possibility frontiers Compare* and contrast* the ways that different economies deal with

specific problems or issuesApply economic skills Construct* and interpret* production possibility frontiers Distinguish* between equilibrium and disequilibrium situations in the

circular flow of income model Explain* how an economy might return to an equilibrium situation from a

disequilibrium situation Identify* bias in media items on economic issues affecting the local, state

and national economies * = Key HSC words

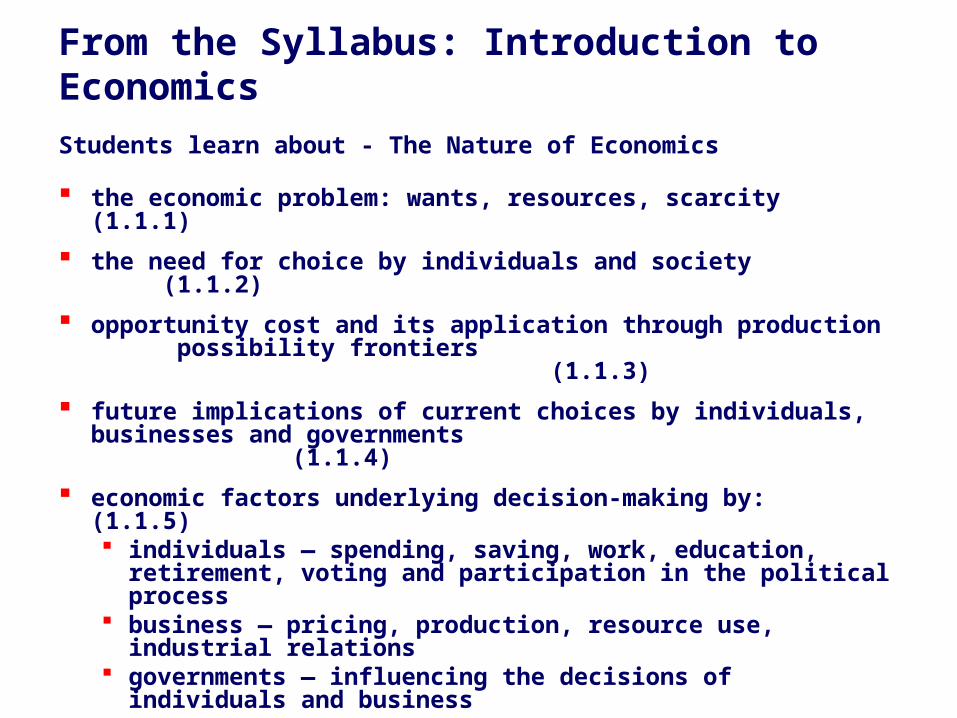

From the Syllabus: Introduction to Economics

Students learn about - The Nature of Economics

the economic problem: wants, resources, scarcity (1.1.1)

the need for choice by individuals and society (1.1.2)

opportunity cost and its application through production possibility frontiers (1.1.3)

future implications of current choices by individuals, businesses and governments (1.1.4)

economic factors underlying decision-making by: (1.1.5) individuals — spending, saving, work, education,

retirement, voting and participation in the political process business — pricing, production, resource use, industrial

relations governments — influencing the decisions of individuals

and business

Economics, like Geography and Commerce, is a social science. This means that there is a systematic & scientific study of those aspects of human behaviour relating to material welfare.

What is Economics?

Economics is derived from the Greek word ‘oikonomia’– oikod – house and nomis – law; it means the art of prudent housekeeping

What is Economics?

‘Economics is about the processes of production, consumption, utilisation and exchange – has as its goal the solution of a number of different problems that confront all societies…’ Bixley – Economics & the Economy

‘The study of the production, distribution and consumption of wealth in human society.’

Penguin Dictionary of Economics

What is Economics?

• J M Keynes: regarded as the founder of modern economic theory –’Keynesian Revolution’

“Economics is an apparatus of the mind”

- J M Keynes

What is Economics?

• Economics is a science albeit a ‘social science’ – it studies human economic behaviour.

• “Economics is the study of the process and implications of the way society makes the allocative choice - using scarce resources to satisfy unlimited wants.” T Stegman

the ‘soup line’Great Depression

(circa 1931)

The Nature of Wants 1.1.1 There exist basic needs, which are essential for survival (e.g. food, clothing & shelter) – often called basic wants. Individual and communities as a whole also have wants,

which are material desires for goods & services that give us satisfaction or utility. Wants may be classified a number of ways:

Individual wants are the wants that each person has for the type of food, clothing & shelter they desire. Collective wants are the wants that the community possesses equally and that often cannot be satisfied individually e.g. education, defence, police & justice.

The Nature of Wants 1.1.1

Human nature ensures that our wants are unlimited. Features that contribute to them being unlimited include that wants are: recurring, where they must be continually

satisfied at regular intervals e.g. food. complementary, where once a want has been

satisfied, it creates other wants e.g. buying a car means we then want petrol.

changing, where seasons, fashions, income, age and stage of life influence our wants.

Resources 1.1.1 Resources or factors of production are needed to produce

the goods & services to satisfy wants. The quantity & quality of a country’s resources will influence how many wants are satisfied (i.e standard of living)There are four factors of production: Land, which refers to all natural resources, such as

forests, minerals, fish and agricultural land – the income return is called rent.

Labour, refers to human effort both physical and intellectual – the income return is called wages.

Capital, called capital goods it includes machinery, plant or anything that aids production that is produced by man – the income return is called interest.

Enterprise, refers to that special type of labour that can organise the other resources – the income return is called profit.

The Economic Problem 1.1.1

The economic problem exists because:• we have unlimited wants and yet • there are relatively scarce resources (when compared to unlimited

wants) with which to satisfy wants and• because we cannot satisfy all our wants, a choice must be made as

to which wants are going to be satisfied and which go unsatisfied• finally, a decision has to be made about who amongst us gets to

satisfy their wants and who may go unsatisfied – distribution.

The Economic Problem 1.1.1 The existence of the economic problem

means that Economics is often described is terms such as:

The study of scarcity

OR

The science of decision making

Unemployed workersGreat Depression – circa 1931

The Economic Problem 1.1.1

The economic problem means a number of decisions have to be made. The way in which a society is organised to make these choices is known as the economic system. An economic system must make decisions about:

• What to produce, including the mix of capital and consumer goods • How much to produce• How to produce• How to share or distribute production amongst members of society

So! What is Economics?

Ideally, a suitable definition of economics should include that it is a study of the way a country or economy:

• uses limited resources for the • production of goods & services for the• satisfaction of unlimited wants and• the way is which goods & services are shared,

which is known as distribution.

What is Economics?

What is your definition of Economics?

Focus Questions1. Define Economics.

2. Explain why Economics is a social science.

3. Distinguish between needs and wants.

4. Outline why wants are unlimited.

5. Distinguish between individual wants and collective wants.

6. Identify the main factor determining standard of living.

7. Identify the different resources available to satisfy wants.

8. Explain why resources are regarded as relatively scarce.

9. Explain what is meant by the economic problem.

10. List the economic decisions that must be made by an economic system.

Need for Choice by Individuals & Society 1.1.2 Recognising that not all wants can be satisfied, individuals and society need to make choices about which

wants to satisfy and when.

When a decision is made to satisfy a particular want this creates an economic cost in addition to its financial cost (i.e. the price paid for the good or service).

The real or opportunity cost (or economic cost) of satisfying a particular want is the alternative goods & services that could be produced with those resources. Choices for individuals and society to make include: the mix of consumer goods to be consumed the mix of individual wants and collective wants to be satisfied the mix of consumer & capital goods to produced (i.e. current consumption versus future consumption)

Guns 0 25 50 75 100

Butter 120 90 60 30 0

Opportunity Cost through Production Possibility Curves 1.1.4

Production Possibility Curves (PPC) enable greater analysis of the concept of opportunity cost.

The assumptions on which production possibility curves are based are: Only two goods are produced by the economy Resources can be switched to the production of either good Technology is fixed/constant

Illustrative Example

0 30 60 90 120 Butter

25

50

75

Guns 100

0

120

x

25

90

x

100

0

50

60 x

x

30

75x

Guns 0 25 50 75 100

Butter 120 90 60 30 0

Opportunity Cost through Production Possibility Curves 1.1.4

Production Possibility Curves (PPC) enable greater analysis of the concept of opportunity cost.

The assumptions on which production possibility curves are based are: Only two goods are produced by the economy Resources can be switched to the production of either good Technology is fixed/constant

Illustrative Example

0 30 60 90 120 Butter

25

50

75

Guns 100

x

x

x

x

x

Features of production possibility curves are: Production at any point on the line or frontier, such as point

A, represents full employment of resources. Production at any point inside the line or frontier, such

as point B, represents some unemployment of resources. Production at any point beyond the frontier, such as

point C, is not achievable with the current state of technology and level of resources.

Guns 0 25 50 75 100

Butter 120 90 60 30 0

Opportunity Cost through Production Possibility Curves 1.1.4

Illustrative Example

0 30 60 90 120 Butter

25

50

75

Guns 100

A. . B

. C

Opportunity Cost through Production Possibility Curves 1.1.4

Production beyond the PPC line or frontier is only possible if: there is technological

progress in the production of: one product, such as

guns or both products

there is an increase in resources available

0 30 60 90 120 Butter

25

50

75

Guns 100

Outward movements in the PPCline or frontier represents economic growth.

Future Implications of Current Choices by Individuals, Businesses & Government 1.1.2

Decisions by all these groups are designed to provide the maximum satisfaction from the resources available – this is known as allocative efficiency.

Consumer choices not only involve decisions about which current needs & wants to satisfy but also how much of present income to save for future consumption, such as for a house or retirement – overall Australians are poor savers.

Business choices involve deciding what & how many products to produce, to maximise profits, and how much investment to undertake.

Government choices involve deciding how much to collect in taxes

& revenue, knowing it will reduce private sector activity, to maximise satisfaction, and what collective wants to satisfy with these funds.

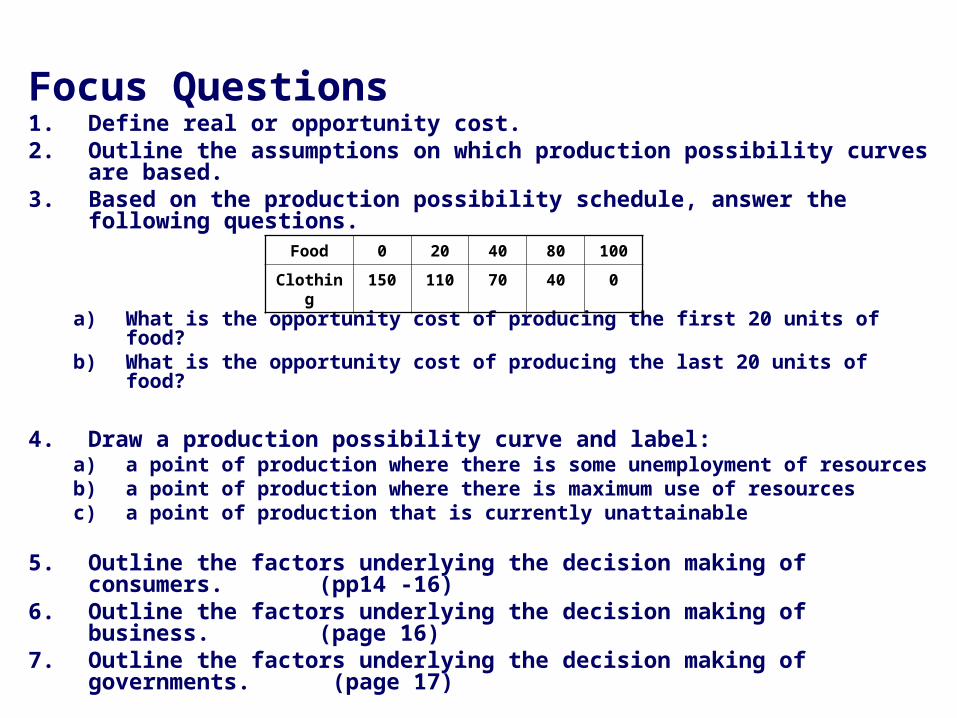

Focus Questions1. Define real or opportunity cost.2. Outline the assumptions on which production possibility curves are

based.3. Based on the production possibility schedule, answer the following

questions.

a) What is the opportunity cost of producing the first 20 units of food?b) What is the opportunity cost of producing the last 20 units of food?

4. Draw a production possibility curve and label:a) a point of production where there is some unemployment of resourcesb) a point of production where there is maximum use of resourcesc) a point of production that is currently unattainable

5. Outline the factors underlying the decision making of consumers. (pp14 -16)

6. Outline the factors underlying the decision making of business. (page 16)

7. Outline the factors underlying the decision making of governments. (page 17)

Food 0 20 40 80 100

Clothing 150 110 70 40 0