platt’s conference presentation - latest oil, energy ... · pdf fileplatt’s...

TRANSCRIPT

Platt’s Conference Presentation

April 2017

The opinions and views expressed in this presentation are those of the author(s) and do not necessarily reflect the views of Valero Energy Corporation.

2

Safe Harbor Statement

Statements contained in this presentation that state the company’s or

management’s expectations or predictions of the future are forward-looking

statements covered by the safe harbor provisions of the Securities Act of

1933 and the Securities Exchange Act of 1934. The words “believe,” “expect,”

“should,” “estimates,” “intend,” and other similar expressions identify forward–

looking statements. It is important to note that actual results could differ

materially from those projected in such forward-looking statements. For more

information concerning factors that could cause actual results to differ from

those expressed or forecasted, see Valero’s annual reports on Form 10-K and

quarterly reports on Form 10-Q, filed with the Securities and Exchange

Commission, and available on Valero’s website at www.valero.com.

3

Introduction to Valero

Refineries and ethanol plants

are in advantaged locations

15 refineries with 3.1 million

barrels per day of capacity

4

Discussion Agenda

Refining margins, Is the recent “boom” time over?

Light tight oil (LTO) processing and how have refiners adapted

Can US refiners raise product exports and compete other markets?

Impact of IMO regulation to reduce sulfur in bunker fuel

Is it time to worry?

5

Historical Margins

Heavy Sour Margins Light Sweet Margins

“Golden Age” shown on the charts from 2004-2008. Recent heavy sour margins not approaching “Golden Age”

Light sweet margins peaked in 2014-2015. 2016 margins down from peak, but, above historical average.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USGC Heavy Sour Coking Margin

Is the recent “boom” time over? First question is were 2014-2015 really a “boom” or just part of a cyclical refining business?

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USGC Light Sweet Cracking Margin

6

Mid-Continent Historical Margins

WTI Discounts

Mid-Con margins and “boom” driven by wide differential between WTI and LLS in 2011-2014.

Mid-Con “boom” driven by low cost “stranded” crude as WTI to LLS spread widened. Increased pipeline “takeaway” capacity most likely prevents reoccurrence.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

3-2-1 Crack Spreads

Group 3 3-2-1 WTI based USGC 3-2-1 LLS based

Mid-Con and USGC 3-2-1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

WTI Minus LLS

WTI less LLS

7

Current Product Inventory Weighing on Margins

Product inventory draw needed or 2017 could follow similar pattern as 2016

Can increased demand draw down inventory?

Will supply reduce due to a heavy Spring Turnaround season?

8

Macro Environment Looks Favorable

Abundant global supply of crude oil

and natural gas. US crude

production on the rise. Adequate

supply of heavy crude from Canada

Forecasted world GDP growth

Product shortages in Latin America,

Europe, Africa, and Eastern Canada

Demand response to lower

product prices

SUPPLY DEMAND

North American logistics build out

added efficiency and removed

Mid-Continent bottlenecks to move

crude to USGC

2

Expect ample supply to keep prices low, which should continue driving increased petroleum demand.

1 3

4

5

9

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

2013 2014 2015 2016E-2020E Avg

MMBPD Europe China Middle East Other Net CDU Capacity Additions World Petroleum Demand Growth

Source: Consultant and Valero estimates. Net Global Refinery

CDU Additions = New Capacity + Restarts – Announced

Closures. (Does not include Condensate Splitters.)

Global Petroleum Demand Growth Expected

to Outpace Refinery Capacity Expansion

Expected demand growth to be supportive of business for coming years.

However, the winds of change are blowing and 2020 forward could bring a return to “Golden Age” type margins.

10

Forecasted Margins

Heavy Sour Margins Light Sweet Margins

Heavy Sour Coking margins exceed the “Golden Age”. Light Sweet Cracking margins at historical high.

Margins driven by market disruptions from the low sulfur bunker fuel regulations.

The recent “boom” is insignificant compared to the potential of what is coming.

0

2

4

6

8

10

12

14

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

USGC Light Sweet Cracking Margin

Consultant Range Historical

0

5

10

15

20

25

30

35

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

USGC Heavy Sour Coking Margin

Consultant Range Historical

11

Global Marine Fuel Sulfur Cap, Is it Time to Worry?

Bunker Sulfur Limits

• The International Maritime

Organization (IMO)

regulation reduces sulfur in

bunker fuel from 3.5 wt.% to

0.5 wt.% or requires

installation of scrubbers to

remove SO2 from exhaust

gas. Rule to be

implemented in 2020.

Product Market Impact

• HSFO to bunker market is

around 3 MMBPD

• Shift of 2 MMBPD of diesel

into bunker market

• Shift of VGO and ULSR into

bunkers to produce ULSFO

• HSFO could move to coal

parity, $15/bbl

Shippers Options for Compliance

• Marine gasoil. Higher

priced fuel, simple to

manage

• Scrubbed HSFO. Shippers

are reluctant to invest, but,

scrubbers will eventually

penetrate the market

• ULSFO creates new market

• LNG, developing, but small

Crude Market Impact

• Sweet crude market

develops two tiers with a

higher priced tier for crudes

that produce ULSFO

• Sweet/Sour differentials

widen

• Resid imports will compete

with sour crude for available

conversion capacity

Compliance Level is the Great Unknown

• Main compliance option to

be marine gas oil

• Scale of penalties and

method of enforcement for

non-compliance unclear

• Availability of compliant fuel

in developing nations

• Potential exemptions

Impact on Refiners

• Heavy Sour Coking refiners

to be advantaged especially

on the USGC

• Marginal European

refineries given life line due

to increased diesel demand

• Sour refineries without resid

conversion capacity will be

challenged

12

Valero Well Positioned for Future

• Valero USGC refineries fit into one of the three

configuration categories shown in the table

• Typical refinery configurations for similar feed

stocks are also shown in the table

• Valero Sour Coking refineries produce little to no

fuel oil blend stock

• Valero light sweet refineries have the capability

to crack resid in FCC units. This greatly reduces

fuel oil yield relative to typical light sweet

cracking refineries

• Typical Medium Sour Cracking refinery produces

high yield of fuel oil

• High conversion capacity and complexity gives

Valero an advantage

No need to worry over low sulfur fuel oil regulations, if, refineries are high complexity.

Yields from Valero vs. Typical Refineries

Valero Sour

Coking, HCU,FCC

Valero Sour

Coking, FCC

Valero Light

Sweet Cracking

Typical Light

Sweet Cracking

Typical Medium

Sour Cracking

FEEDSTOCK PURCHASES

Light Sweet 0.0 0.0 100.0 100.0 0.0

Medium Sour 0.0 60.0 0.0 0.0 100.0

Heavy Sour 100.0 40.0 0.0 0.0 0.0

H2 (FOE) 3.7 2.2 2.4 0.6 1.5

Other 9.0 12.8 5.4 1.1 1.8

PRODUCT SALES

Gasoline 37.6 45.8 40.8 41.3 34.4

Distillates 58.0 47.9 39.2 44.3 35.4

LPG 6.1 6.1 5.4 4.0 3.9

FO/FO Blendstock 0.0 1.1 1.6 11.2 27.4

Coke (FOE) 11.4 7.7 0.0 0.0 0.0

Other 3.7 10.7 22.5 0.0 0.0

13

0

100

200

300

400

500

600

700

800

900

1000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Other

Europe

Other Latin America

Mexico

Canada

Gasoline Exports 12 Month

Moving Average (MBPD)

Gasoline represents all finished gasoline plus all blendstocks (including ethanol, MTBE, and other oxygenates)

Source: DOE Petroleum Supply Monthly data through November 2016.

Can U.S. Continue or Raise Exports and Compete

14

Source: DOE Petroleum Supply Monthly data through November 2016.

Can U.S. Continue or Raise Exports and Compete

0

200

400

600

800

1000

1200

1400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Other

Europe

Other Latin America

Mexico

Canada

Distillate Exports 12 Month

Moving Average (MBPD)

15

$2.55/mmBtu U.S.

$0.83/bbl

$4.73/mmBtu Europe

$1.54/bbl

Natural Gas Cost Sensitivity for Valero’s Refineries

U.S. Natural Gas Cost Provides Opex and

Feedstock Cost Advantages for US Refiners

Average annual natural gas prices for 2016 through December 30 for U.S. and Europe. Estimated per barrel cost of 912,000 mmBtu/day of natural gas

consumption at 93% refinery throughput capacity utilization, or 2.8 MMBPD.

$719 MM

pre-tax

annual cost

advantage

• As an example, Valero’s refining operations consume approximately 912,000 mmBtu/day of

natural gas, of which 57% is operating expense and balance is cost of goods sold

• Significant annual pre-tax cost savings compared to refiners in Europe

• Prices expected to remain low and disconnected from global oil and gas markets

USGC has an operating cost advantage.

16

USGC Location Facilitates Optimization of Product

Exports

Distillate

Gasoline

Mexico

Load Vsl Size $/bbl

USG LR1 base

NW Europe LR2 1.01

Saudi Arabia LR2 2.02

India LR2 2.54

S. Korea LR2 3.68

Chili

Load Vsl Size $/bbl

USG LR1 base

NW Europe LR2 0.15

S Korea LR2 0.2

India LR2 0.43

Saudi Arabia LR2 0.52

Columbia

Load Vsl Size $/bbl

USG LR1 base

NW Europe LR2 0.4

Saudi Arabia LR2 1.4

India LR2 1.93

S. Korea LR2 2.07

West Africa

Load Vsl Size $/bbl

USG LR2 base

NW Europe LR2 -0.41

Montreal

Load Vsl Size $/bbl

USG LR1 base

NW Europe LR1 0.02

New York Harbor

Load Vsl Size $/bbl

USG MR base

NW Europe MR -0.91

USGC has freight advantage to Mexico and Latin America.

17

U.S. Advantage to Export Products

• Access to low cost natural gas and abundant low

cost North American crudes lowers production costs

• Pipeline capacity additions have increased crude

optionality and resulted in improved pricing

• Refineries have the flexibility to process wide range

of crudes and feedstocks

• Proximity to growing product export markets in

Mexico and Latin America provides freight advantage

• Competitive refined products supplier to Eastern

Canada and Northwest Europe

69 124

246 324

119

251

447

541

2011 2012 2013 2014 2015 2016 CurrentCapacity

PotentialFuture

Capacity

VLO’s U.S. Product Exports (MBPD)

Gasoline Diesel

USGC Refineries have Lower Costs than

Alternative Suppliers in Europe into Product

Markets in Mexico and Latin America

18

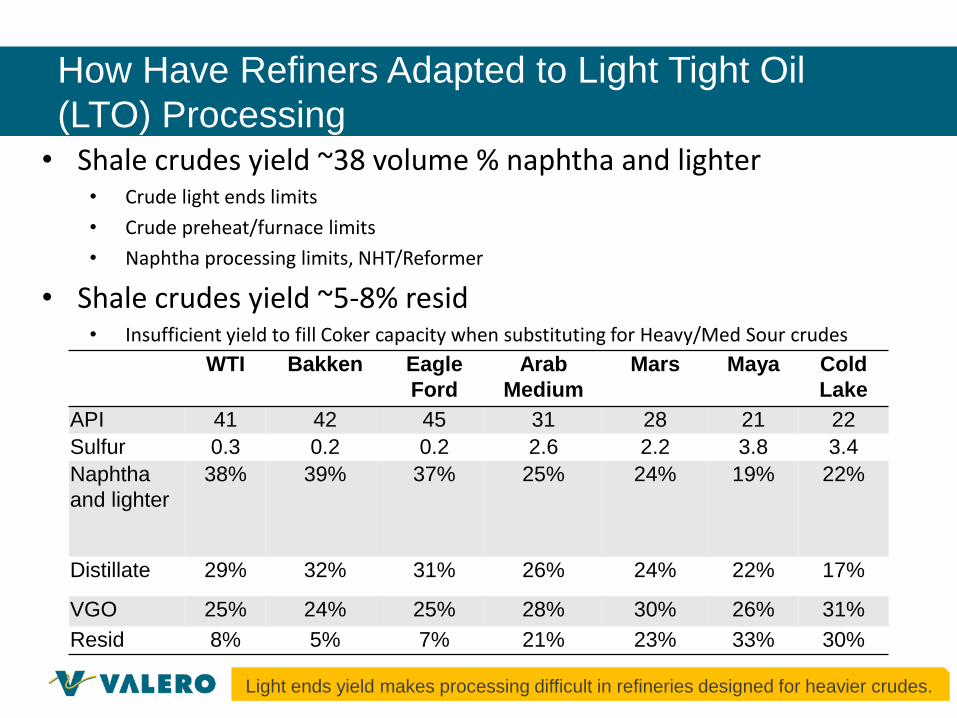

How Have Refiners Adapted to Light Tight Oil

(LTO) Processing

WTI Bakken Eagle

Ford

Arab

Medium

Mars Maya Cold

Lake

API 41 42 45 31 28 21 22

Sulfur 0.3 0.2 0.2 2.6 2.2 3.8 3.4

Naphtha

and lighter

38% 39% 37% 25% 24% 19% 22%

Distillate 29% 32% 31% 26% 24% 22% 17%

VGO 25% 24% 25% 28% 30% 26% 31%

Resid 8% 5% 7% 21% 23% 33% 30%

• Shale crudes yield ~38 volume % naphtha and lighter • Crude light ends limits

• Crude preheat/furnace limits

• Naphtha processing limits, NHT/Reformer

• Shale crudes yield ~5-8% resid • Insufficient yield to fill Coker capacity when substituting for Heavy/Med Sour crudes

Light ends yield makes processing difficult in refineries designed for heavier crudes.

19

Valero’s Flexibility to Adapt Crude Diet

• As an example, before the shale boom, domestic sweet processing was 19% of crude diet,

mainly at mid-continent refineries.

• At the height of the shale boom, domestic light sweet processing increased to 44% of crude

diet. This includes the addition of the Crude Toppers at Corpus and Houston, plus

maximum processing of domestic sweet crude at heavy refineries.

• Post shale boom, domestic light sweet removed from heavy refineries and replaced with

medium sour. Foreign sweet replaces domestic sweet in some sweet crude units.

44%

19%

11%

15%

6% 5%

Shale Boom

Domestic Sweet Medium Sour Foreign Sweet

S. America Residuals Cand. Heavy

32%

25%

18%

13%

7% 5%

Post Shale Boom

Domestic Sweet Medium Sour Foreign Sweet

S. America Residuals Cand. Heavy

19%

32% 24%

16%

7% 2%

Pre Shale Boom

Domestic Sweet Medium Sour Foreign Sweet

S. America Residuals Cand. Heavy

20

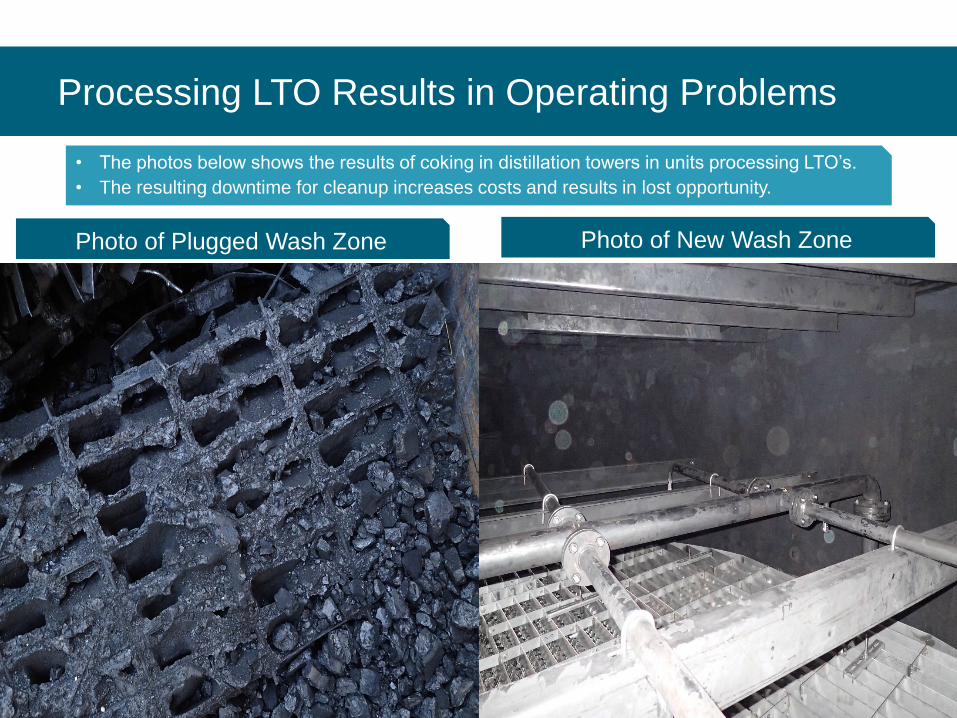

Processing LTO Results in Operating Problems

• The photos below shows the results of coking in distillation towers in units processing LTO’s.

• The resulting downtime for cleanup increases costs and results in lost opportunity.

Placeholder for Coking Photos

Photo of Plugged Wash Zone Photo of New Wash Zone

21

Processing LTO Results in Operating Problems

• The photos below show the results of fouling in distillation towers in units processing LTO’s.

• The resulting downtime for cleanup increases costs and results in lost opportunity.

Placeholder for Coking Photos

Photo of Fouled Tray Photo of Cleaned Tray

22

Photos of Eagle Ford Crude Receipts

• Variations in crude quality make predicting

yields and income from refining operations

challenging.

• API gravity and sulfur are not the only qualities

of interest to refiners.

• Distillation specifications are becoming more

prevalent as well as con carbon, metals, and

acid number.