plastic industry: brazil and us market challenges …

TRANSCRIPT

PLASTIC INDUSTRY: BRAZIL AND US MARKET CHALLENGES AND OPPORTUNITIES

Overview of the Plastic Converting Industry in Brazil

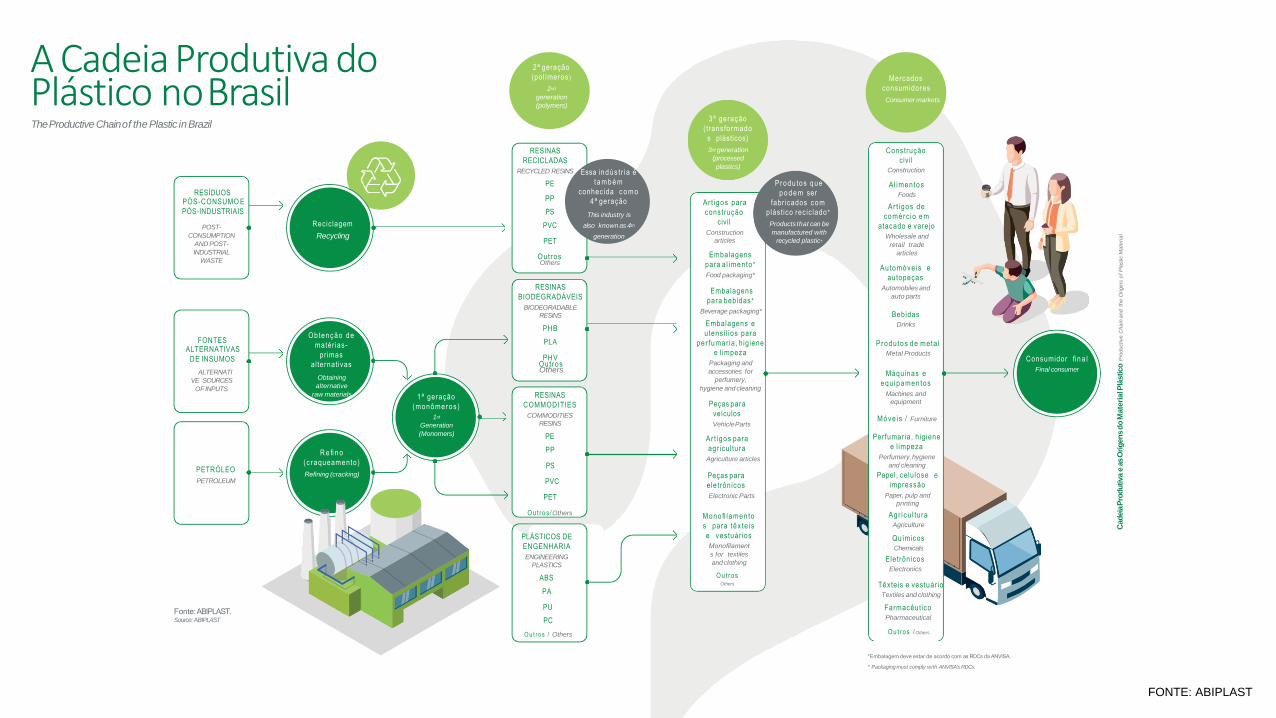

A Cadeia Produtiva do Plástico noBrasilTheProductive Chainof the Plastic inBrazil

Cad

eia

Pro

du

tiva

eas

Ori

gen

sd

oM

ate

rialP

lástico

Pro

du

ctive

Ch

ain

an

dth

eO

rig

ins

of

Pla

stic

Ma

teri

al

RESÍDUOSPÓS-CONSUMO E

PÓS-INDUSTRIAIS

POST-

CONSUMPTION

AND POST-

INDUSTRIAL

WASTE

PETRÓLEO

PETROLEUM

FONTESALTERNATIVAS

DE INSUMOS

ALTERNATI

VE SOURCES

OFINPUTS

Recic lagem

Recycling

RESINAS

RECICLADAS

RECYCLED RESINS

Obtenção de

matér ias-

pr imas

a l ternativas

Obtaining

alternative

raw materials

R e fi n o

( c raqueamento )

Refining (cracking)

PE

PP

PS

PVC

PET

OutrosOthers

Ar t igos para

construção

civil

Construction

articles

Embalagens

para a l imen to *

Food packaging*

Embalagens

para bebidas *

Beverage packaging*

Embalagens e

utensíl ios para

pe r fumar ia , hig iene

e l impeza

Packaging and

accessories for

perfumery,

hygiene and cleaning

Peças para

veículos

VehicleParts

Ar t igos para

agr icultura

Agriculture articles

Peças para

e letrônicos

Electronic Parts

Monofi lamento

s para têx te is

e vestuár ios

Monofilament

s for textiles

andclothing

O u t ro sOthers

Construção

civil

Construction

Al imentos

Foods

Ar t igos de

comérc io e m

atacado e varejo

Wholesale and

retail trade

articles

Automóveis e

autopeças

Automobiles and

auto parts

Bebidas

Drinks

Produ tos d e meta l

Metal Products

Máquinas e

equ ipamentos

Machines and

equipment

Móve is / Furniture

Perfumar ia, hig iene

e l impeza

Perfumery,hygiene

and cleaning

Papel, celulose e

impressão

Paper, pulp and

printing

Agr icu l tu ra

Agriculture

Químicos

Chemicals

Eletrônicos

Electronics

Têxteis e vestuár io

Textiles and clothing

Farmacêutico

Pharmaceutical

RESINAS

BIODEGRADÁVEIS

BIODEGRADABLE

RESINS

PHB

PLA

PHV

RESINAS

COMMODITIES

COMMODITIES

RESINS

PE

PP

PS

PVC

PET

O u t ro s /Others

1ª geração

(monômeros )

1st

Generation

(Monomers)

Consumidor fi n a l

Final consumer

Essa indús t r ia é

t a m b é m

conhecida c o m o

4ª geração

This industry is

also known as 4th

generation

Produ tos que

p o d e m ser

fabr icados com

plástico rec ic lado *

Products that can be

manufactured with

recycled plastic*

2ª geração

(polímeros )

2nd

generation

(polymers)

3ª geração

( transformado

s plásticos)

3rd generation

(processed

plastics)

Mercados

consumidores

Consumer markets

Fonte:ABIPLAST.Source:ABIPLAST

PLÁSTICOS DE

ENGENHARIA

ENGINEERING

PLASTICS

ABS

PA

PU

PC

O ut ros / Others

*Embalagem deve estar de acordo com as RDCs da ANVISA.

* Packaging must comply with ANVISA's RDCs.

FONTE: ABIPLAST

OutrosOthers

O u t ro s / Others

Cad

eia

Pro

du

tiva

eas

Ori

gen

sd

oM

ate

rialP

lástico

Pro

du

ctive

Ch

ain

an

dth

eO

rig

ins

of

Pla

stic

Ma

teri

al

Tendências demercadoMarket trends

•Segundo a McKinsey, em pesquisa divulgada em

maio de 2020, há expectativa de mudanças no com-

portamento do consumo para o “novo normal”,

sendo dois deles o consumo seguro e a sustentabili-

dade redefinida. A pesquisa aponta que a preocupa-

ção com saúde e contaminação deve continuar no

topo de prioridades para os consumidores, além das

máscaras que serão parte do “novo normal” e devem

afetar o uso de algumas categorias. No caso da

sustentabilidade redefinida, verifica-se que 2/3

acham mais importante do que antes limitar impac-

tos de mudanças climáticas e cerca de 60% estão

fazendo mudanças significativas de estilo de vida

para reduzir o impacto no meio ambiente. A poten-

cial implicação, portanto, neste caso, é repensar

como sustentabilidade deve ser incorporada à

proposta de valor de marcas e negócios.

•Segundo a pesquisa “How is COVID-19 Affecting the

Top 10 Global Consumer Trends 2020”, divulgada em

abril de 2020 pela Euromonitor, em um cenário

pré-COVID-19, os consumidores estavam em busca

de produtos com maior vida útil, reduzindo o volume

de resíduos. Palavras como dividir, reutilizar e alugar

estavam emergindo e, por isso, empresas educavam

seus consumidores sobre segurança e opções reutili-

záveis. Por outro lado, com a crise do coronavírus, o

estudo aponta que o foco está em “foco está na

segurança sanitária, em relação a fatores priorizados

anteriormente. No curto prazo, apontou-se que os

consumidores têm mudado seu foco para segurança

e saúde e se preocupado com o tema “contamina-

ção”. No longo prazo, por fim, espera-se um retorno

lento dos produtos reutilizáveis.

•According to McKinsey, in a survey released in May 2020,

changes in consumption behavior are expected for the “new

normal”, two of which are safe consumption and redefined

sustainability. The research points out that the concern with health

and contamination must remain a top priority for consumers, in

addition to the masks that will be part of the "new normal" and

should affect the use of some categories. In the case of defined

sustainability, it appears that 2/3 think it is more important than

before to limit impacts of climate change and about 60% are

making significant lifestyle changes to reduce the impact on the

environment. The potential implication, therefore, in this case, is

how sustainability should be incorporated into the value

proposition of brands and businesses.

Source: “Winning the Recovery: The new consumer COVID post”/ McKinsey

•According to the survey "How is COVID-19 Affecting the Top 10

Global Consumer Trends 2020", released in April 2020 by

Euromonitor, in a pre-COVID-19 scenario, consumers were looking for

products with a longer useful life, reducing the volume of waste.

Words like dividing, reusing and renting were emerging and,

therefore, companies educated their consumers about safety and

reusable options. On the other hand, with the coronavirus crisis, the

study points out that the focus is on health safety in relation to

previously prioritized factors. In the short term, it was pointed out

that consumers have shifted their focus to safety and health and are

concerned with the “contamination” topic. Finally, in the long run, a

slow return of reusable products is expected.

Source: “How is COVID-19 Affecting the Top 10 Global Consumer Trends 2020”/

Euromonitor and “Winning the Recovery: The new consumer COVID”/ McKinsey

Dow

“We believe that the circular economy and recycling will

transform our sector. We are investing and advancing in

mechanical and chemical recycling processes, and we

understand that this movement is also undergoing

improvements in the collection and sorting processes that exist

today. By valuing the actors in this chain, the new plastic

economy is capable of promoting environmental sustainability,

with social impact and value creation.

This is the model that will allow us to solve the current and

future challenges of the chain and the planet, such as climate

change and greenhouse gasemissions”.

Source: Dow Testimony.

Vedacit

“We have seen an increase in the concern of governments,

companies and society with the destination of plastic. Due to

the importance of proper packaging disposal, we believe that

there will be greater movement by the business sector to

increase the circularity of plastic. Through partnerships, there

will be mobilization for the creation of a reverse logistics

structure and for the greater incorporation of recycled resins

in the supply chain”.

Source: VedacitTestimony

Fonte: “How is COVID-19Affecting the Top10 GlobalConsumer

Trends2020”/ Eu romon i to r e “Winn ing t h e Recovery:

O novo consumidor pós COVID” / McKinsey

Acredi tamos que a economia circular

e a reciclagem i rão t ransformar

nosso setor.

Estamos invest indo e avançando

e m processos d e reciclagem mecânica

e química, e en t endemos que este

mov imen t o t a m b é m passa po r

melhor ias nos processos d e coleta

e separação que existem hoje.

A o valorizar os atores desta cadeia,

a nova economia d o plást ico é capaz

d e p romover sustentabi l idade

ambiental , com impacto social e

geração d e valor.

É este o mode lo que nos permi t i rá

solucionar os desafios atuais e f u t u ros

da cadeia e d o planeta, como a

mudança cl imát ica e as emissões de

gases d e e f e i t o estufa” .

“ “

Fon te : Depoimento Dow

(abril de 2020)

Observamos o aum ent o da

preocupação d e governos, empresas

e sociedade com o dest ino d o plástico.

Devido à importância d o descarte

adequado das embalagens,

en t endemos que haverá maior

movimentação d o setor empresarial

para aument a r a circularidade

d o plást ico. At ravés d e parcerias,

haverá mobi l ização para a criação

d e est rutura d e logíst ica reversa

e para a ma io r incorporação de

resinas recicladas pela

cadeia d e fornecimento” .

Fon te : Depoimento Vedacit

(abril de 2020)

FONTE: ABIPLAST

Aplic

ações d

o M

ate

rial P

lástico

Ap

plic

atio

ns o

f P

lastic M

ate

ria

l

Setores consumidores de transformados plásticos emvalorde consumo(2017)

Consumerssectorsof processed plastics– in valueof consumption (2017)

Ciclo longode vida (acimade 5 anos)–49%Longuseful life (over 5 years)– 49%

3,0%

1,0%

0,0% 5,0% 10,0% 20,0%15,0% 25,0%

3,1%

8,1%

0,0%

0,6%

1,8%

4,6%

5,2%

5,6%

8,6%

22,5%

5,0% 15,0%10,0% 20,0% 25,0%

Construção civil Construction

Automóveis e autopeçasAutomobiles and auto parts

Produtos de meta l Metal products

Máquinas e equipamentosMachinery and equipment

Móveis Furniture

Eletrônicos Eletronics

Outros equip. de transporteOther transportequipments

Ciclomédio de vida (entre 1 e 5 anos)–15,2%Average useful life (between 1 and 5 years)–15,2%

Ciclocurtode vida (até 1 ano)–35,8%Shortuseful life (up to 1 year) – 35,8%

0,0%

20,3%

5,0% 10,0% 15,0% 25,0%20,0%

Art igos de comércio em atacado e varejoWholesale and retail goods

AgriculturaAgriculture

Papel, celulose e impressãoPaper, pulp and printing

Têxteis e vestuárioTextiles andclothing

AlimentosFood

BebidasBeverages

6,1%

P e r f u m a r i a , h i g i e n e e l i m p e z aToiletry, hygiene and cleaning products

3 ,3%

QuímicosChemicals

DescartáveisDisposable

Farmacê u t i coPharmaceutical

2 ,7%

2,5%

0,9%

FONTE: ABIPLAST

Extrusão:Consiste em forçar a passagem controlada do

material plástico fundido através de um cilindro e na

sua saída, o material é comprimido em uma matriz

com a forma desejada do produto. Por meio desse

processo são fabricados, por exemplo, chapas, perfis

ou filmes, para posterior acabamento.

Aplic

ações d

o M

ate

rial P

lástico

Ap

plic

atio

ns o

f P

lastic M

ate

ria

l

Extrusion: Consists of forcing the controlled passage of the

cast plastic material through a cylinder and upon its exit, the

material is compressed in a matrix into the desired shape of the

product. This process is used to make, for instance, sheets, profiles,

of films for later finish.

Fi lms extrusion: Produces very fine, mono and multilayer films that

will be later used to make flexible packanging.

Profiles extrusion: Used to make pipes, coated cables, wires, and

hoses for civil construction.

Monofilam ent s extrusion: To make contínuos and fine filaments,

such as fishing lines, brush and broom bristles, and when braided

they originate products such as ropes, cables, fishing nets, screens

in general, etc. Fibres for the textile industry can also be made.

Sheets extrusion: Used to make sheets and plates that will be used as

input for the production of thermoformed packaging and White

line accessories, such as refrigerators and microwave ovens.

Blow moulding: Consists in the extrusion of a “house” commonly

known as parison wich is inserted into a mould and by compressed

air injected inside

forms a hollow product. It is the process used to make bottles,

gallons, packaging for foods, cosmetics, cleaning products, and

automotive tanks.

Injection: This process gives very specific details to the

products such as threads, holes, and perfect fitting, and is very

much used in the auto parts industry (such as car dashboards)

making intermediate products that serve as inputs for the

automotive industry and also to produce household items

intended for the end consumer.

Rotational moulding: Use to make hollow products such as toy

pieces (doll heads and parts) or large parts such as agricultural

machine and water tanks. Vacuum thermoforming: Process to

mould parts by using plates os sheets (made by extrusion).

Consists of heating the sheet wich receives vacum to remove

the air caught between the sheet and the mould to enable the

forming of the final part. This technique is used to manufacture

products such as disposable utensils, trays,autoparts, etc.

Other process: The blown injection is a variation very much used

to make PET bottles, combining both injection (pre-mould) and

blown (PET bottles) processes in the same machine.

Processosprodutivospara fabricação de transformadosplásticosProductive processesfor manufacturing processed plastics

Extrusão sopro: Consiste na extrusão de uma “man-

gueira” comumente chamada de parison que é

inserida em um molde e com a injeção de ar compri-

mido em seu interior forma um produto oco. É o

processo utilizado na fabricação de garrafas, garra-

fões, frascos para alimentos, cosméticos, produtos

de limpeza e tanques automotivos.

Extrusão de per fi l : Utilizada para a fabricação de

tubos, cabos revestidos, fios e mangueiras para a

construção civil.

Extrusão de m onofi lam en tos : Para fabricação de

filamentos contínuos e finos, como linhas de pesca,

cerdas para escovas e vassouras e quando tramados

originam produtos como cordas, cabos, redes de

pesca, telas em geral, etc. Existe ainda a fabricação

de fibras para a indústria têxtil.

Extrusão de chapas: Utilizada para a fabricação das

chapas e lâminas que serão insumos para a produção

de embalagens termoformadas e acessórios de linha

branca, como geladeiras e micro-ondas.

Extrusão de fi lmes : Produz filmes, películas muito

finas, mono e multicamadas que serão utilizados

para posterior confecção de embalagens flexíveis.

Injeção:Esse processo confere detalhes muito específicos

aos produtos como roscas, furos e encaixes perfei-

tos sendo muito utilizado na indústria de autopeças

(como painéis de carros) fabricando produtos

intermediários que servem como insumos para a

indústria automotiva e também na produção de

utilidades domésticas que se destinam ao consumi-

dor final.

Rotomoldagem:Utilizada para a fabricação de produtos ocos como

peças de brinquedos (cabeças e partes de bonecas)

ou peças de grandes dimensões como tanques para

máquinas agrícolas e caixas d’água.

Termoformação a vácuo:Processo de moldagem de peças a partir de lamina-

dos ou chapas (obtidos por extrusão). Consiste no

aquecimento da chapa sendo essa submetida ao

vácuo o qual elimina o ar existente entre a chapa e o

molde permitindo a formação da peça final. Com

esta técnica são fabricados produtos como utensí-

lios descartáveis, bandejas, autopeças, etc.

Outros processos:Uma variação muito utilizada para a fabricação dos

frascos em PET é a injeção sopro, que combina em

uma mesma máquina os dois processos de injeção

(pré-forma) e sopro (frasco ou garrafa).

Injeção

Injection

32,9%

Rotomoldagem

Rotational moulding

0,5%

Extrusão

Extrusion

65,9%

Termoformação a vácuo

Vacuum thermoforming

0,7%

Extrusão de chapas

Sheets extrusion

23%

Extrusão de filmes

Films extrusion

47%

Extrusão sopro

Blow moulding

13%

Extrusão de perfis

Profiles extrusion

15%

Extrusão de monofilamen tos

Monofilaments extrusion

1%

Fontes: Pesquisa Industrial Anual – Produto 2016 e

Pesquisa Industrial Mensal – Produção Física.

Elaboração ABIPLAST.

Sources: Annual Industrial Survey - Product 2016and Monthly Industrial Survey- Physical Production.

Prepared by: ABIPLAST

6PERFIL 2019 |ABIPLAST

FONTE: ABIPLAST

A In

dú

str

ia d

e T

ransfo

rmados P

lásticos n

o B

rasil

Th

e P

rocessed P

lastics In

du

str

y i

n B

razil

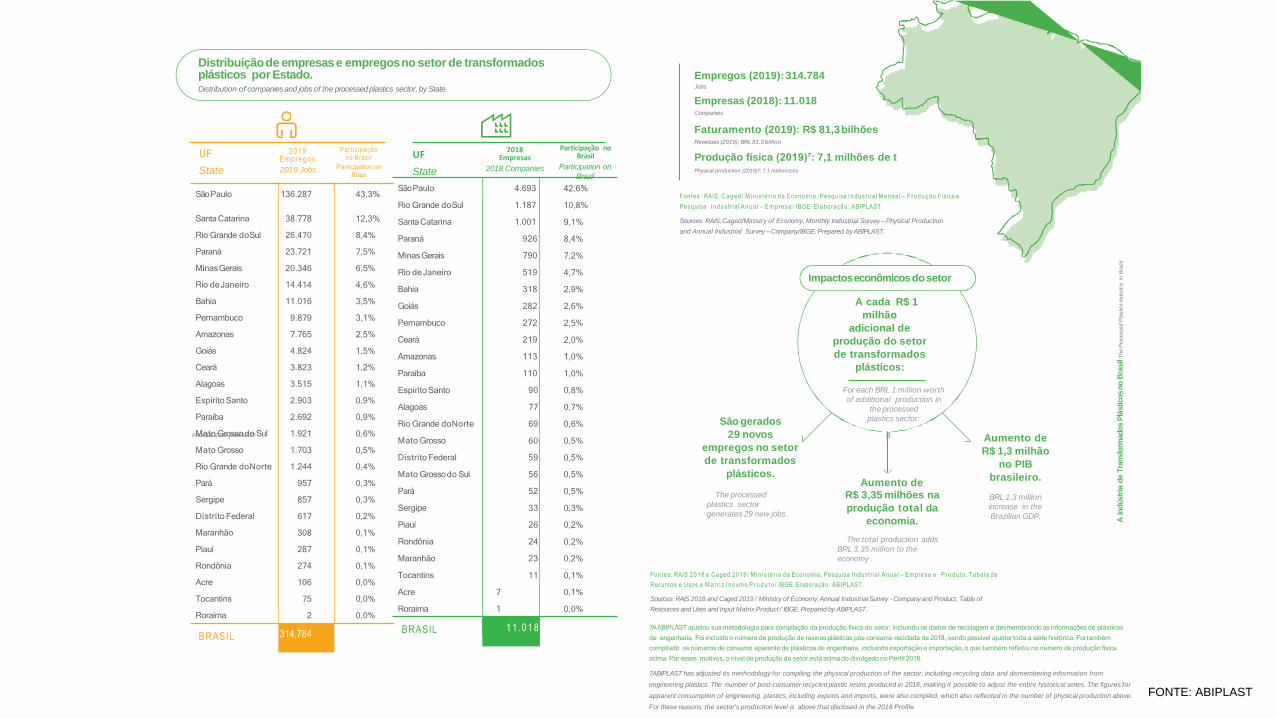

Tota l de

Empregos: 314.784Total of Jobs

Tota l de

Empresas: 11.018Total of Companies

52

Pará

957

M a t o Grosso

Goiás

Paraná

Rio Grande d o Sul

0 a 49 50 a 199 200 a 499 500 a 999 >1000

Sources: RAIS, Caged/Ministry of Economy, Monthly Industrial Survey – Physical

Production and Annual Industrial Survey– Company/IBGE. Preparedby ABIPLAST.

F o n te s : RAIS, C a g e d / M in i s té r io d a E co n o mia , Pesqu isa In d u s t r i a l

M e n sa l – P ro d u çã o Física e Pesqu isa In d u s t r i a l A n u a l – E m p re sa /

IBGE. E laboração: ABIPLAST.

Localizaçãode empresase empregosno setor de transformadosplásticosno Brasil, por Estado.Empresas(2018), Empregos(2019)Location of companiesand jobs of the processed plastics sector, by Sate.Companies (2018), Jobs(2019)

1

Rora ima

2

113

Amazonas

7.765

7

Acre

106

24

Rondôn ia

274

601.703

2824.824

M a t o Grosso d o Sul

1.921 56

92623.721

1.18726.470

1.001

Santa Cata r ina

38.778

4.693

São Pau lo

136.287

79020.346

90

M i nas Gera is

2.903

D i s t r i t o Federa l

59617

Espí r i t o S an t o

Alagoas

773.515

Pernambuco

2729.879

Ceará

2193.823

Piauí

26287

Maranhão

23308

Tocan t ins

1175

Rio Grande d o N o r te

1.244 69

Paraiba

1102.692

Serg ipe

33857Bahia

31811.016

Rio d e Jane i ro

14.414 519

7PERFIL 2019 |ABIPLASTPROFILE 2019 | ABIPLAST

Indústria de transformados plásticos no Brasil

FONTE: ABIPLAST

A In

dú

str

ia d

e T

ransfo

rmados P

lásticos n

o B

rasil

Th

e P

rocessed P

lastics In

du

str

y i

n B

razil

2019Empregos

2019 Jobs

Participação noBrasil

Participation on

Brazil

Part i c ipação

n o Brasi l

Participation on

Brazil

UF

State

SãoPaulo 4.693 42,6%

Rio Grande doSul 1.187 10,8%

SantaCatarina 1.001 9,1%

Paraná 926 8,4%

MinasGerais 790 7,2%

Rio deJaneiro 519 4,7%

Bahia 318 2,9%

Goiás 282 2,6%

Pernambuco 272 2,5%

Ceará 219 2,0%

Amazonas 113 1,0%

Paraíba 110 1,0%

Espírito Santo 90 0,8%

Alagoas 77 0,7%

Rio Grande doNorte 69 0,6%

Mato Grosso 60 0,5%

Distrito Federal 59 0,5%

Mato Grossodo Sul 56 0,5%

Pará 52 0,5%

Sergipe 33 0,3%

Piauí 26 0,2%

Rondônia 24 0,2%

Maranhão 23 0,2%

Tocantins 11 0,1%

Acre 7 0,1%

Roraima 1 0,0%

BRASIL 11 .018

SãoPaulo 136.287 43,3%

SantaCatarina 38.778 12,3%

Rio Grande doSul 26.470 8,4%

Paraná 23.721 7,5%

MinasGerais 20.346 6,5%

Rio deJaneiro 14.414 4,6%

Bahia 11.016 3,5%

Pernambuco 9.879 3,1%

Amazonas 7.765 2,5%

Goiás 4.824 1,5%

Ceará 3.823 1,2%

Alagoas 3.515 1,1%

Espírito Santo 2.903 0,9%

Paraíba 2.692 0,9%

Mato Grossodo Sul 1.921 0,6%

Mato Grosso 1.703 0,5%

Rio Grande doNorte 1.244 0,4%

Pará 957 0,3%

Sergipe 857 0,3%

Distrito Federal 617 0,2%

Maranhão 308 0,1%

Piauí 287 0,1%

Rondônia 274 0,1%

Acre 106 0,0%

Tocantins 75 0,0%

Roraima 2 0,0%

BRASIL 314.784

UF

State

2018Empresas

2018 Companies

Faturamento (2019): R$ 81,3bilhõesRevenues (2019): BRL 81.3 billion

Empregos (2019): 314.784Jobs

Empresas (2018): 11.018Companies

Produção física (2019)⁷: 7,1 milhões de tPhysical production (2019)7: 7.1 milliontons

For each BRL 1 million worth

of additional production in

the processed

plastics sector:

Aumento deR$ 3,35 milhões na

produção total da

economia.

The total production adds

BRL 3.35 million to the

economy .

São gerados

29 novos

empregos no setor

de transformados

plásticos.

The processed

plastics sector

generates 29 new jobs.

Aumento de

R$ 1,3 milhão

no PIB

brasileiro.

BRL 1.3 million

increase in the

Brazilian GDP.

Distribuiçãode empresase empregosno setor de transformadosplásticos por Estado.Distribution of companiesand jobs of the processed plastics sector, by State.

Fontes: RAIS, C aged / M i n i s té r i o d a Economia, Pesquisa I ndust r ia l M ensa l – P rodução Física e

Pesquisa I ndust r ia l A nua l – E m presa / IBGE. Elaboração: ABIPLAST.

Sources: RAIS, Caged/Ministry of Economy, Monthly Industrial Survey – Physical Production

and Annual Industrial Survey – Company/IBGE. Prepared byABIPLAST.

Fontes: RAIS 2 0 1 8 e Caged 2 0 1 9 / M i n i s té r io d a Economia, Pesquisa Indust r ia l A nua l – Empresa e P rodu t o, Tabela d e

Recursos e Usos e M a t r i z I nsumo P r o d u t o / IBGE. Elaboração: ABIPLAST.

Sources: RAIS 2018 and Caged 2019 / Ministry of Economy,Annual Industrial Survey - Companyand Product, Table of

Resources and Uses and Input Matrix Product / IBGE. Prepared by ABIPLAST.

7A ABIPLAST ajustou sua metodologia para compilação da produção física do setor, incluindo os dados de reciclagem e desmembrando as informações de plásticos

de engenharia. Foi incluído o número de produção de resinas plásticas pós-consumo reciclada de 2018, sendo possível ajustar toda a série histórica. Foi também

compilado os números de consumo aparente de plásticos de engenharia, incluindo exportação e importação, o que também refletiu no número de produção física

acima. Por esses motivos, o nível de produção do setor está acima do divulgado no Perfil 2018.

7ABIPLAST has adjusted its methodology for compiling the physical production of the sector, including recycling data and dismembering information from

engineering plastics. The number of post-consumer recycled plastic resins produced in 2018, making it possible to adjust the entire historical series. The figures for

apparent consumption of engineering plastics, including exports and imports, were also compiled, which also reflected in the number of physical production above.

For these reasons, the sector's production level is above that disclosed in the 2018 Profile.

Impactoseconômicosdosetor

A cada R$ 1

milhão

adicional de

produção do setor

de transformados

plásticos:

8PERFIL 2019 |ABIPLASTPROFILE 2019 | ABIPLAST

FONTE: ABIPLAST

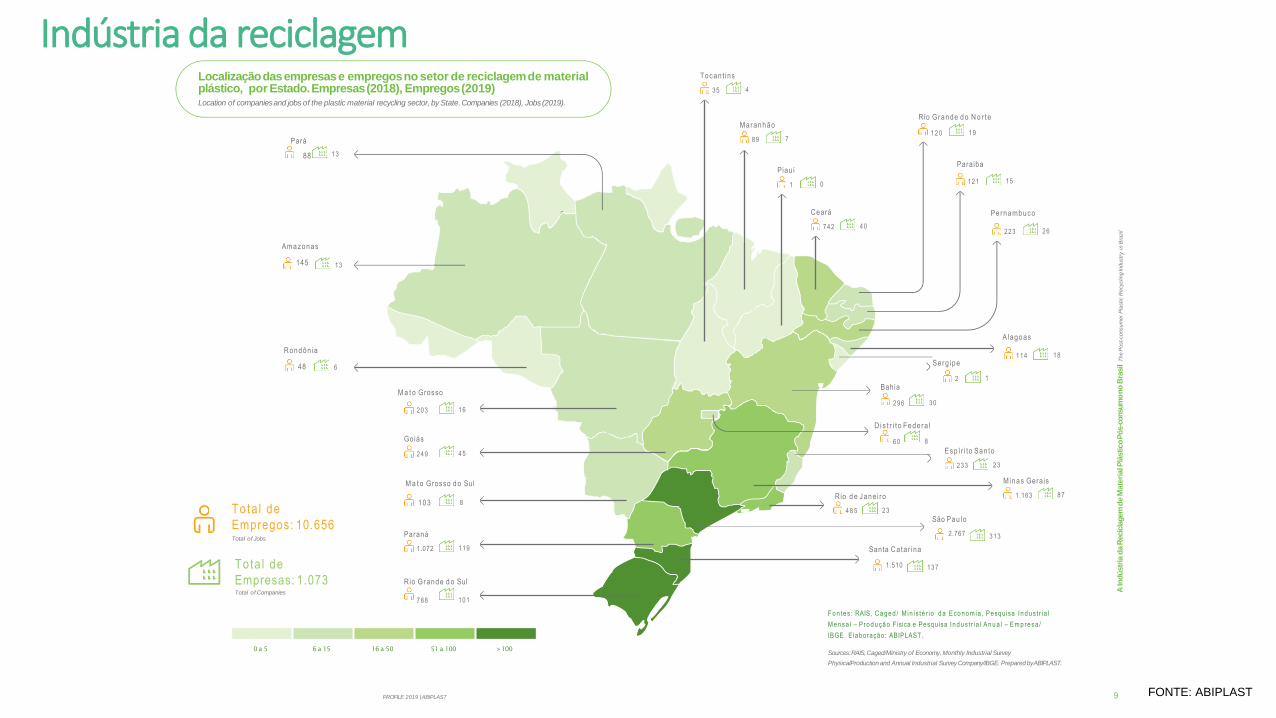

AIn

dú

str

iad

aR

ecic

lagem

de

Mate

rialP

lástico

Pós-c

onsum

on

oB

rasil

Th

eP

ost-

co

nsu

me

rP

lastic

Re

cyclin

gIn

du

str

yin

Bra

zil

Tota l de

Empregos: 10.656Total of Jobs

Tota l de

Empresas: 1.073Total of Companies

13

Pará

88

M a t o Grosso

Goiás

Paraná

Minas Gerais

Localizaçãodasempresase empregosno setor de reciclagemde materialplástico, por Estado.Empresas(2018), Empregos(2019)Location of companiesand jobs of the plastic material recycling sector, by State.Companies (2018), Jobs(2019).

13

Amazonas

145

6

Rondôn ia

48

16203

45249

M a t o Grosso d o Sul

103 8

1191.072

Rio Grande d o Sul

788 101

137

Santa Cata r ina

1.510

313

São Pau lo

2.767

871.163

Espír i to San to

23233

Alagoas

18114

Pernambuco

26223

Ceará

40742

Piauí

01

Maranhão

789

Tocan t ins

435

Rio Grande d o N o r te

1 2 0 19

Paraiba

15121

Serg ipe

12

Bahia

296 30

D i s t r i t o Federa l

60 8

Rio d e Jane i ro

4 8 5 23

0 a 5 6 a 15 16 a 50 51 a 100 >100Sources:RAIS,Caged/Ministry of Economy, Monthly Industrial Survey

PhysicalProduction and Annual Industrial Survey Company/IBGE. Prepared byABIPLAST.

9PERFIL 2019 |ABIPLAST PROFILE 2019 | ABIPLAST

F o n te s : RAIS, C a g e d / M in i s té r io d a E co n o mia , Pesqu isa In d u s t r i a l

M e n sa l – P ro d u çã o Física e Pesqu isa In d u s t r i a l A n u a l – E m p re sa /

IBGE E laboração: ABIPLAST.

Indústria da reciclagem

FONTE: ABIPLAST

Resumo da cadeia produtiva doplástico

Summaryof the plasticproductivechain in Brazil

Principais resinas

consumidas

Main resinsconsumed

PP | 21,0%

PVC | 13,6%

PEAD | 12,7%

HDPE

PEBDL | 11,9%

LLDPE

Plásticos

reciclados (2018) | 10,6%

Recycled plastics (2018)

PEBD | 8,8%

LDPE

Plásticos de

engenharia | 6,9%

Engineeringplastics

PS | 6,0%

PET | 5,4%

EPS | 2,1%

EVA | 1,0%

Construção civil | 22,5%

Construction

Alimentos |20,3%

Food

Automóveis e autopeças | 8,6%

Vehicles and parts

Artigos decomércio em

atacado e varejo 8,1%

Wholesale and retailgoods

Bebidas |6,1%

Beverages

Produtosde metal | 5,6%

Metal products

Máquinas e equipamentos| 5,2%

Machinery and equipment

Móveis4,6%

Furniture

Perfumaria, higiene e limpeza | 3,3%

Perfumary, toiletryand cosmetics

Agricultura |3,1%

Agriculture

Papel, celulosee impressão | 3%

Pulp, papper andprinting

Químicos | 2,7%

Chemical

Descartáveis | 2,5%

Disposable

Eletrônicos |1,8%

Electronics

Têxteis e vestuários| 1%

Textiles and clothes

Farmacêutico |0,9%

Pharmaceutical

Outros equipamentos

transportes | 0,6%

Other transport equipment

Exportações de resinas

termoplásticas

Exports ofthermoplastic resins

Produção de transformados

plásticos

Production ofprocessed plastics

Reciclagem pós-

industrial

Post-industrialrecycling

US$

1,8bilhãoUSD 1,8billion

Consumo aparente

de transformados

plásticos

Apparent consumption of

processedplastics

R$

91,7bilhõesBRL 91,7billion

Reciclagem mecânica

de material plástico

pós-consumo(2018)

Mechanical recycling ofpost-consumption

plastic material (2018)

757,6 mil

toneladas757,6 thousand tons

Importações de resinas

termoplásticas

Imports of thermoplastic resins

US$

2,5bilhõesUSD 2.5billion

Exportações de

transformados plásticos

Exports ofprocessed plastics

US$ 1,1 bilhãoUSD 1,1 billion

R$

82 bilhõesBRL 82 billion

Importações de

transformados plásticos

Imports ofprocessed plastics

US$

3,5bilhõesUSD 3.5billion

Parcela exportada

Portionexported

5,2%

Parcela Importada:Portion imported

15,2%

Setores consumidores

de produtosplásticos (2017)Consumer sectors of plastic articles (2017)

ConsumidorfinalFinal consumer

FONTE: ABIPLAST

Empresasna indústria de transformadosplásticosCompanies in the processedplastics industry

315

360

347

345 344

356 356353

330

325

306

300

312 314315

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: RAIS, Caged/ Min is tér io da Economia.

Source:RAIS,Caged/Ministry of Economy.

Empregosna indústria de transformadosplásticos–em mil empregosJobsin the processed plastics sector – in thousandjobs

2

4

6

12

10

8

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: Pesquisa Indust r ia l Anual – Produto, Pesquisa Indust r ia l Mensal – Produção Física/ PIM-PF, Comexstat / M in is tér io

da Economia. Elaboração: ABIPLAST.

Source:Annual IndustrialSurvey - Product, Monthly IndustrialSurvey -PhysicalProduction / PIM-PF,Comexstat / Ministry of Economy. Preparedby

ABIPLAST.

Produçãode transformadosplásticos9–em milhõesde toneladasProductionof processedplastics9 – in million tons

11.250

11.000

11.750

12.000

11.524

11.690 11.67011.590

11.559

11.459

11.312

11.500 11.127

11.018

2010 2011

Fonte: RAIS/ Min is tér io da Economia.

Source:RAIS/Ministry of Economy

2012 2013 2014 2015 2016 2017 2018

8,7

11PERFIL 2019 |ABIPLAST

PROFILE 2019 | ABIPLAST

8,6 8,6 8,68,4

7,6

7,07,1 7,2 7,1

FONTE: ABIPLAST

Produçãode transformadosplásticos–em R$ bilhões–preçosconstantes

de 2019.Productionof processedplastics – in BRL billion –constantprices of 2019

Consumoaparente de transformadosplásticos–em milhõesde toneladas10Apparent consumption of processedplastics – in million of tons10

PERFIL 2019 |ABIPLAST

10,0

20,0

30,0

40,0

50,0

60,0

70,0

90,0

80,0

100,0

0,0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: Pesquisa Indust r ia l Anual – Produto, Pesquisa Indust r ia l Mensal – Produção Física/ PIM-PF/ IBGE. Elaboração: ABIPLAST.

Source:Annual IndustrialSurvey-Product, Monthly IndustrialSurvey-PhysicalProduction / PIM-PF/IBGE.PreparedbyABIPLAST.

81,485,8

91,6

84,7 84,579,6 80,9

82,9 82,0

93,41,0

2,0

3,0

4,0

5,0

6,0

8,0

7,0

9,0

10,0

0,0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: Pesquisa Indust r ia l Anual – Produto, Pesquisa Indust r ia l Mensal – Produção Física/ PIM-PF,

Comexstat / M in is tér io da Economia. Elaboração: ABIPLAST.

Source:Annual IndustrialSurvey - Product, Monthly IndustrialSurvey -PhysicalProduction / PIM-PF,Comexstat / Ministry of Economy. Preparedby

ABIPLAST.

9,0 9,0 9,1 9,1

8,0

7,37,6 7,7 7,6

8,9

Consumoaparente de transformados plásticos–emR$bilhões–preços

constantesde 2019Apparent consumption of processedplastics – in BRL billion –constantprices of 2019

80,0

85,0

95,0

90,0

75,0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: Pesquisa Indust r ia l Anual – Produto, Pesquisa Indust r ia l Mensal – Produção Física/ PIM-PF, Comexstat / M in is tér io

da Economia. Elaboração: ABIPLAST.

Source:Annual IndustrialSurvey - Product, Monthly IndustrialSurvey -PhysicalProduction / PIM-PF,Comexstat / Ministry of Economy. Preparedby

ABIPLAST.

85,4 85,787,1

91,191,7

89,6

92,3 92,1

105,0

101,2

100,0 99,0

43 FONTE: ABIPLAST

Exportaçõese importaçõesde transformadosplásticos (em mil toneladas)Processedplastics exportsand imports (in thousandtons)

Fonte: Comexst at / M in is tér io da Economia

Source:Comexstat/ Ministry of Economy

Exportaçõese importaçõesde transformadosplásticos (nominalem US$

milhões)Processedplastics exportsand imports (nominal in USDmillion)

Fonte: Comexst at / M in is tér io da Economia.

Source:Comexstat/ Ministry of Economy.

200

0

400

600

800

615,9

309,8

659,7

267,8

708,5

237,9

731,9

246,2

768,8

235,9

659,4

256,6

585,6

256,0

685,8

264,9

747,1

278,6

770,7

283,8

2010 2011 2012 2013 2014

Exportações

Exports

2015 2016 2017 2018 2019

Importações

Imports

2.834,1

1.474,7 1.512,2

1.283,6

3.228,8

3.001,0

1.206,7 1.213,1

3.389,4 3.366,2

1.083,5

3.542,1

1.112,3

1.338,3 1.394,6 1.345,91.000

0

1.500

500

2.000

3.000 2.707,4

2.500

3.500

4.000 3.844,5 3.888,1

3.590,1

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Exportações Importações

Exports Imports

Faturamento de transformadosplásticos–em R$ bilhões–preçosconstantes

de 2019Revenuesof processedplastics – in BRL billion –constant pricesof 2019

Exportaçõese importaçõesde transformadosplásticos

(nominalem R$milhões)Processedplastics exportsand imports (nominal in BRL million)

Fonte: Comexst at / M in is tér io da Economia.

Source:Comexstat/ Ministry of Economy.

2.000

4.000

6.000

8.000

10.000

12.000

14.000

9.154,2

10.782,0

3.012,6 3.168,8

4.286,5

9.579,8

3.852,1

12.304,9

4.434,6

13.976,5

4.275,2

9.367,9

3.848,7

8.305,0

7.017,6

5.674,7

4.983,9

2.593,3 2.531,9 2.615,9

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Exportações Importações

Exports Imports

85

75

80

95

70

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Fonte: Pesquisa Indust r ia l Anual – Produto, Pesquisa Indust r ia l Mensal – Produção Física/ PIM-PF/ IBGE. Elaboração: ABIPLAST.

Source:Annual IndustrialSurvey-Product, Monthly IndustrialSurvey-PhysicalProduction / PIM-PF/IBGE.PreparedbyABIPLAST.

13PERFIL 2019 |ABIPLASTPROFILE 2019 | ABIPLAST

80,3

83,684,6

90,8

90

83,3

79,380,2

82,281,3

92,7

FONTE: ABIPLAST

Saldocomercial de transformadosplásticos (em mil toneladas)Commercialbalance of processedplastics (in thousandtons)

2010

0-150-300

2011

2012

2013

2014

2015

2016

2017

2018

2019

-600 -450

Fonte: Comexst at / M in is tér io da Economia.

Source:Comexstat/ Ministry of Economy.

-306,0

-392,0

-470,7

-485,7

-532,8

-402,8

-329,6

-420,9

-468,5

-486,9

0-2500-5000

Saldocomercial de transformadosplásticos (nominalem R$milhões)Commercialbalance of processedplastic (nominal in BRLmillion)

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

-10.000 -7.500

Fonte: Comexst at / M in is tér io da Economia.

Source:Comexstat/ Ministry of Economy.

-2.390,6

-3.142,8

-4.401,7

-5.292,4

-5.985,4

-6.495,5

-5.519,2

-5.727,7

-7.870,3

0-650

-1.300

Saldocomercial de transformadosplásticos (nominalem US$milhões)Commercialbalance of processedplastics (nominal in USDmillion)

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

-2.600 -1.950

Fonte: Comexst at / M in is tér io da Economia.

Source:Comexstat/ Ministry of Economy.

-486-4.-9264.4845.4,588,63,4

-1.359,4

-1.877,1

-2.251,8

-2.450,0

-2.542,2

-1.945,2

-1.595,1

-1.794,3

-2.153,0

PERFIL 2019 |ABIPLAST

PROFILE 2019 | ABIPLAST

FONTE: ABIPLAST

-9.701,3

www.cbplastico.com.br

Informações confidenciais e de uso restrito da Abiplast e Braskem (Equipe PICPlast), sendo proibida a sua reprodução, salvo com autorização prévia e expressa dessas instituições.

OBRIGADO