pilot investment climate assessment - world...

TRANSCRIPT

Pilot Investment ClimateAssessment

Improving theInvestment Climatein Bangladesh

An Investment Climate Assessment

Based on an Enterprise Survey

Carried Out by the Bangladesh Enterprise

Institute and the World Bank

June 2003

33689

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

© 2003 The International Bank for Reconstructionand Development / THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, USA

The material in this work is copyrighted. No part ofthis work may be reproduced or transmitted in anyform or by any means, electronic or mechanical,including photocopying, recording, or inclusion inany information storage and retrieval system, withoutthe prior written permission of the World Bank. TheWorld Bank encourages dissemination of its workand will normally grant permission promptly.

For permission to photocopy or reprint, pleasesend a request with complete information to theCopyright Clearance Center, Inc, 222 RosewoodDrive, Danvers, MA 01923, USA, telephone978-750-8400, fax 978-750-4470,

www.copyright.com All other queries on rights and licenses, including

subsidiary rights, should be addressed to the Office of the Publisher, World Bank, 1818 H Street NW,Washington, DC 20433, USA, fax 202-522-2422, e-mail [email protected]

Library of Congress Cataloging-in-Publication Datahas been applied for.

Acknowledgments iv

Acronyms and Abbreviations v

Executive Summary vi

1. Investment Climate Matters 1

Key Features of the Investment Climate 1

Governance 1

Infrastructure 2

Access to Finance 2

International Integration 3

Human Resources 3

Linking the Investment Climate with Growth 3

An Overview of the Bangladesh Economy 3

The Survey—and What Its Findings Reveal 8

2. Bangladesh’s Investment Climate in

International Perspective 10

A Strong Macroeconomic Performance 10

Poor Integration with the Global Economy 11

Serious Deficiencies in Infrastructure 13

Power 15

Transport, Ports, and Customs 16

Telecommunications 18

Governance Problems 20

Governance Quality 20

Entry 22

Access to Finance 23

Lagging in Human Resources 24

A Weak Record in Technological Innovation 26

3. The Effects of Bangladesh’s

Investment Climate on Firms 28

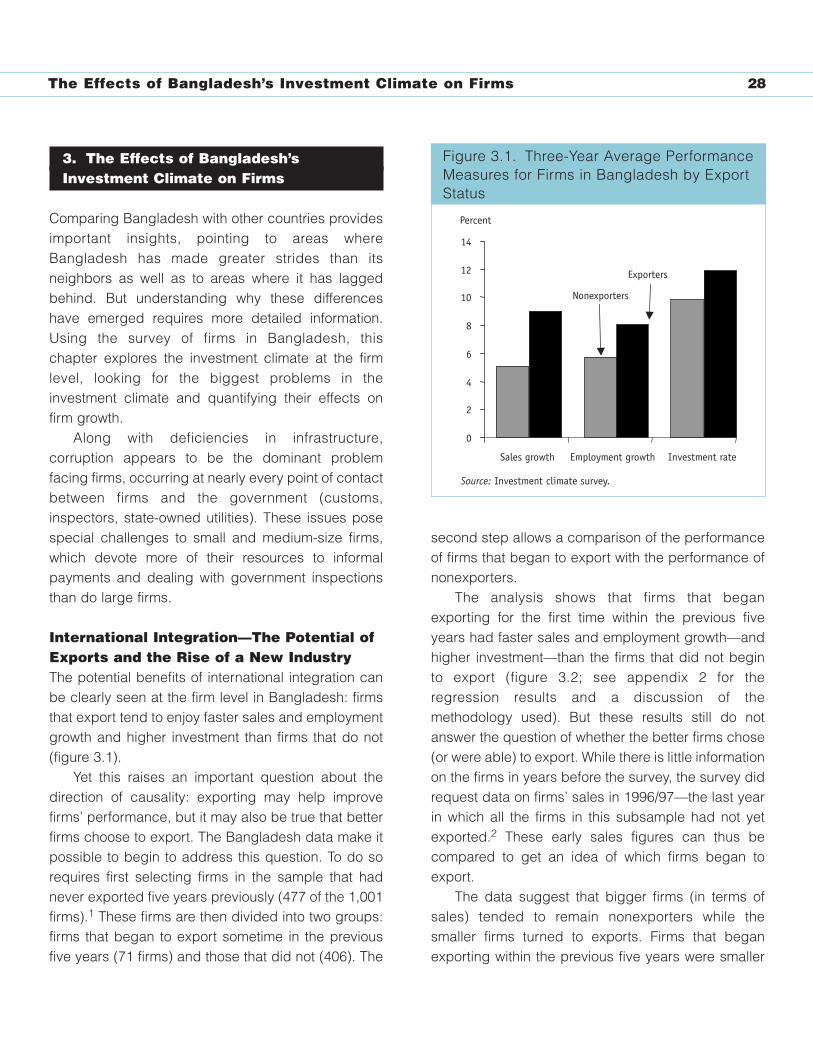

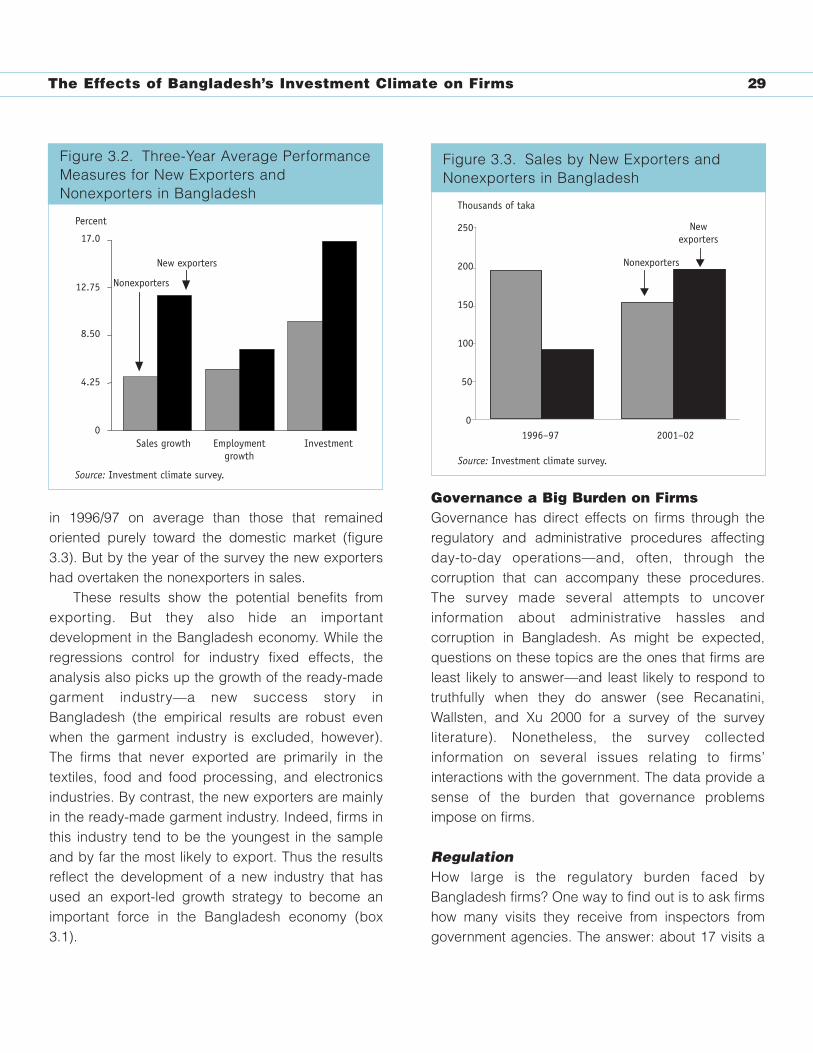

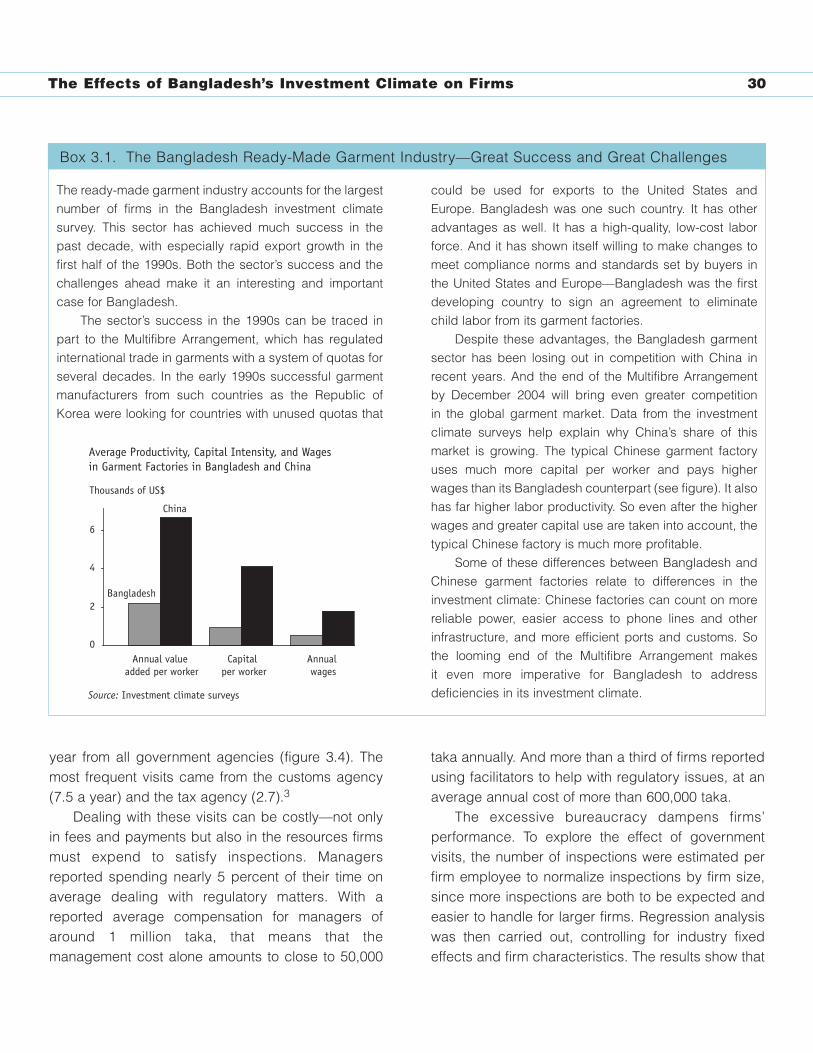

International Integration—The Potential of Exports and the Rise of a New Industry 28

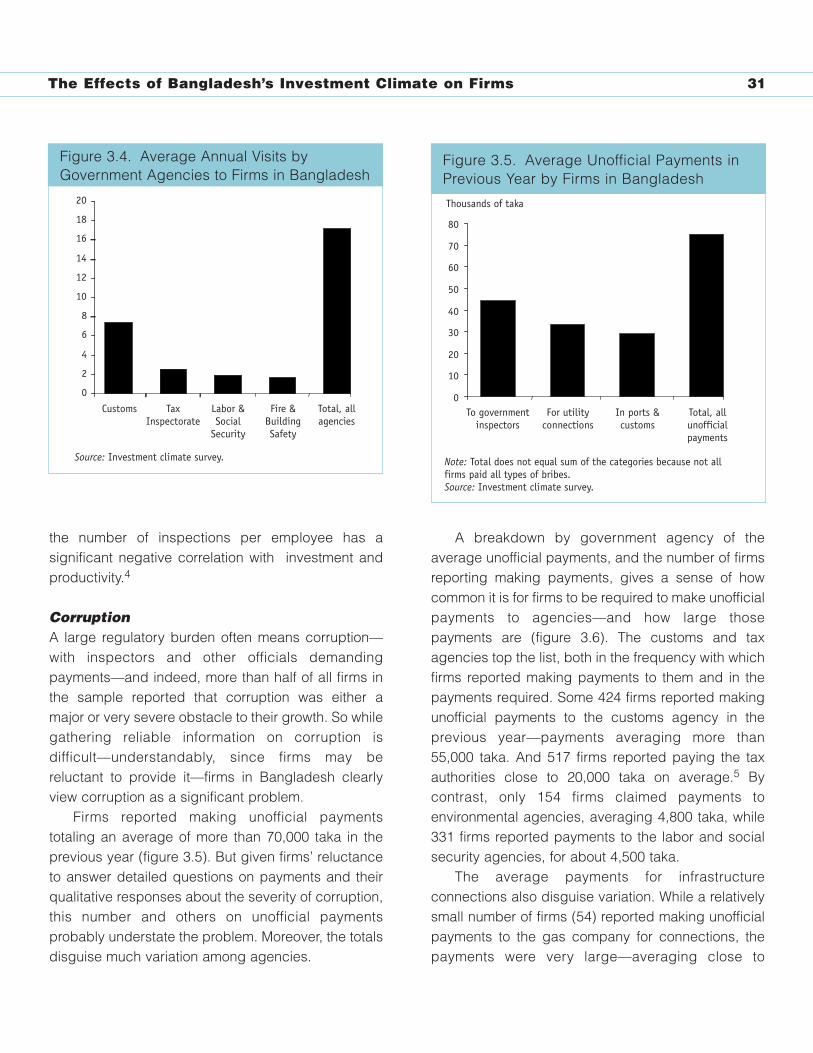

Governance a Big Burden on Firms 29

Regulation 29

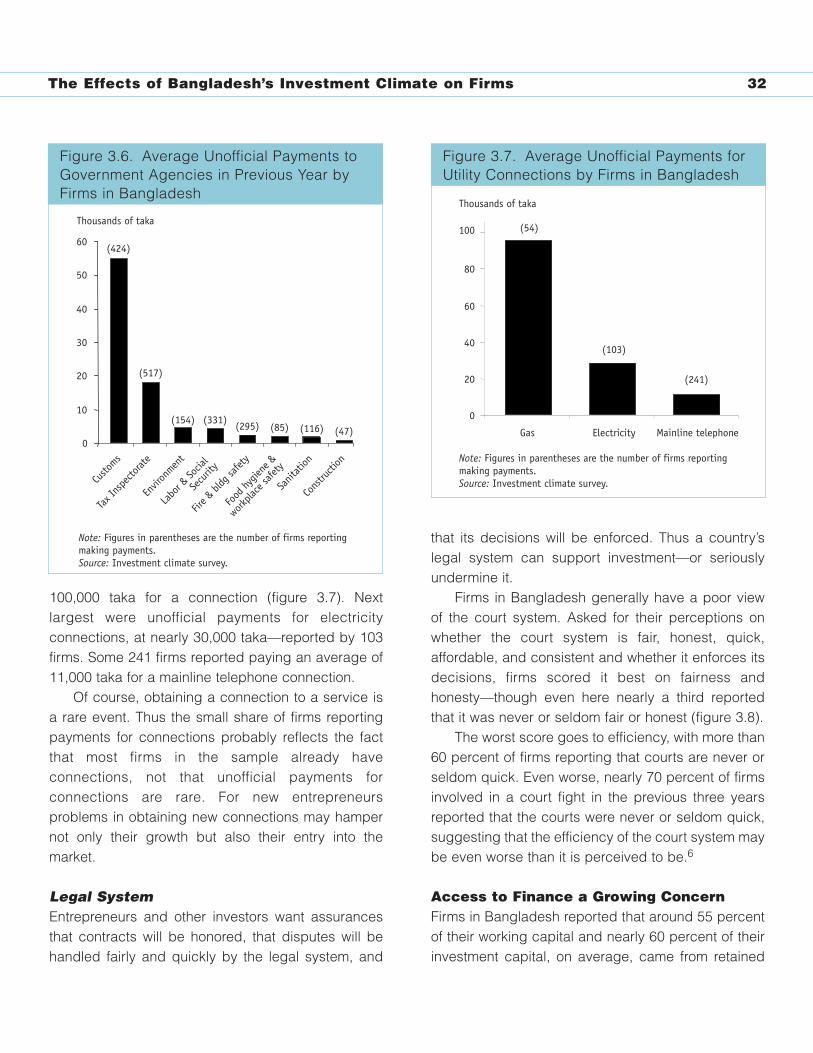

Corruption 31

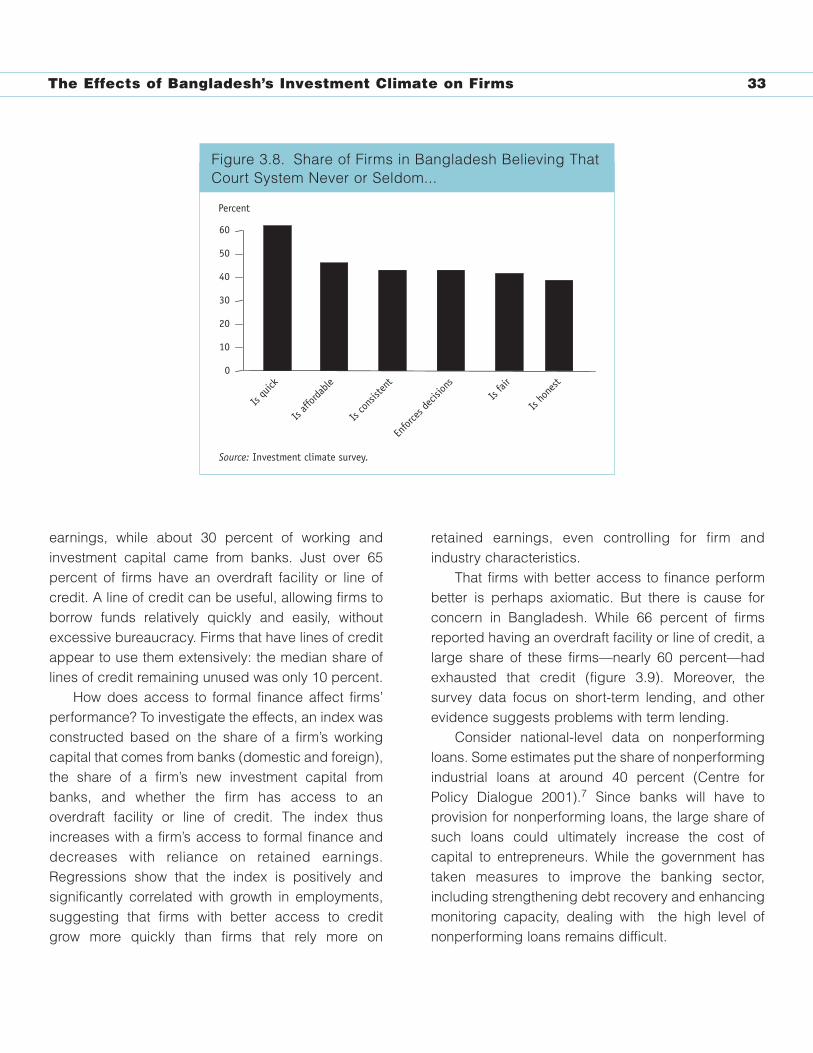

Legal System 32

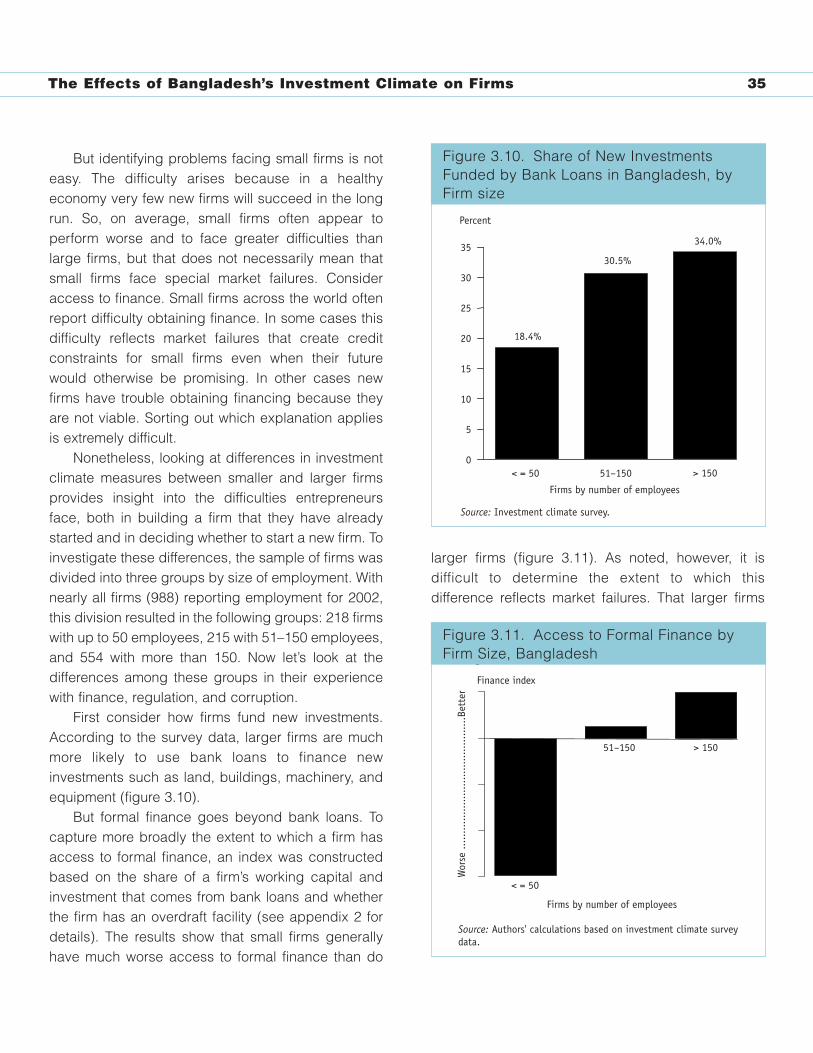

Access to Finance a Growing Concern 32

Flexible Rules for Labor 34

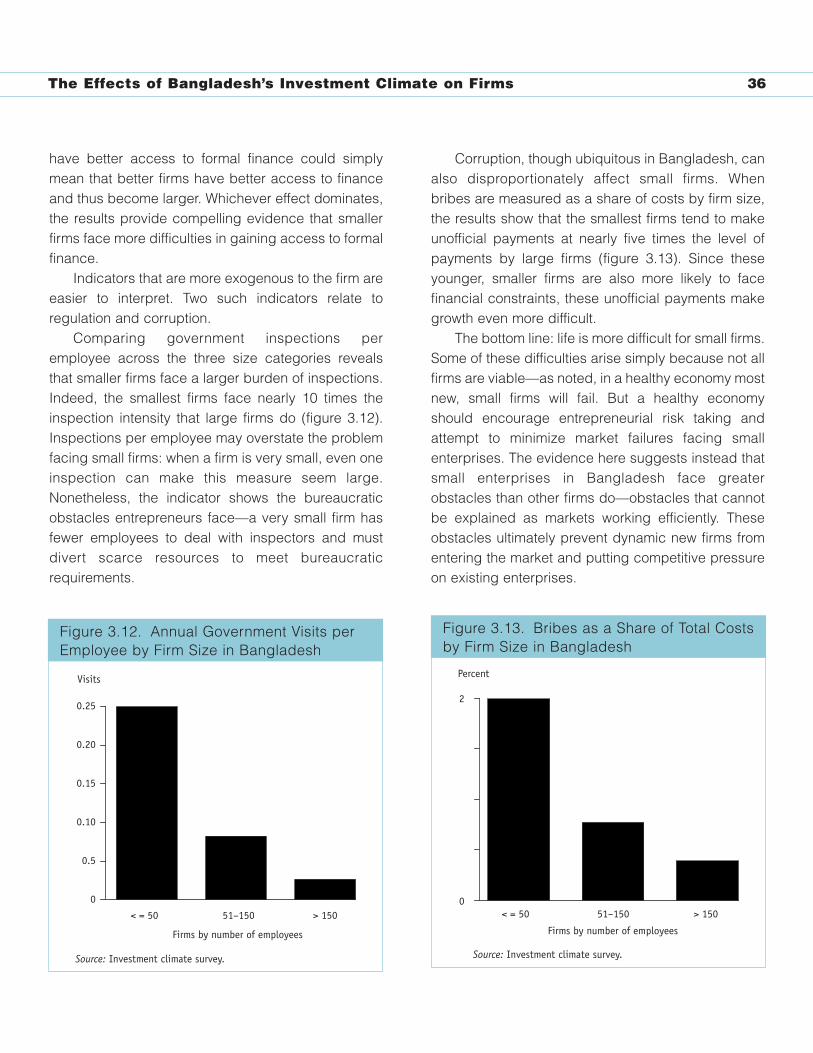

Greater Difficulties for Small- and Medium-Size Enterprises 34

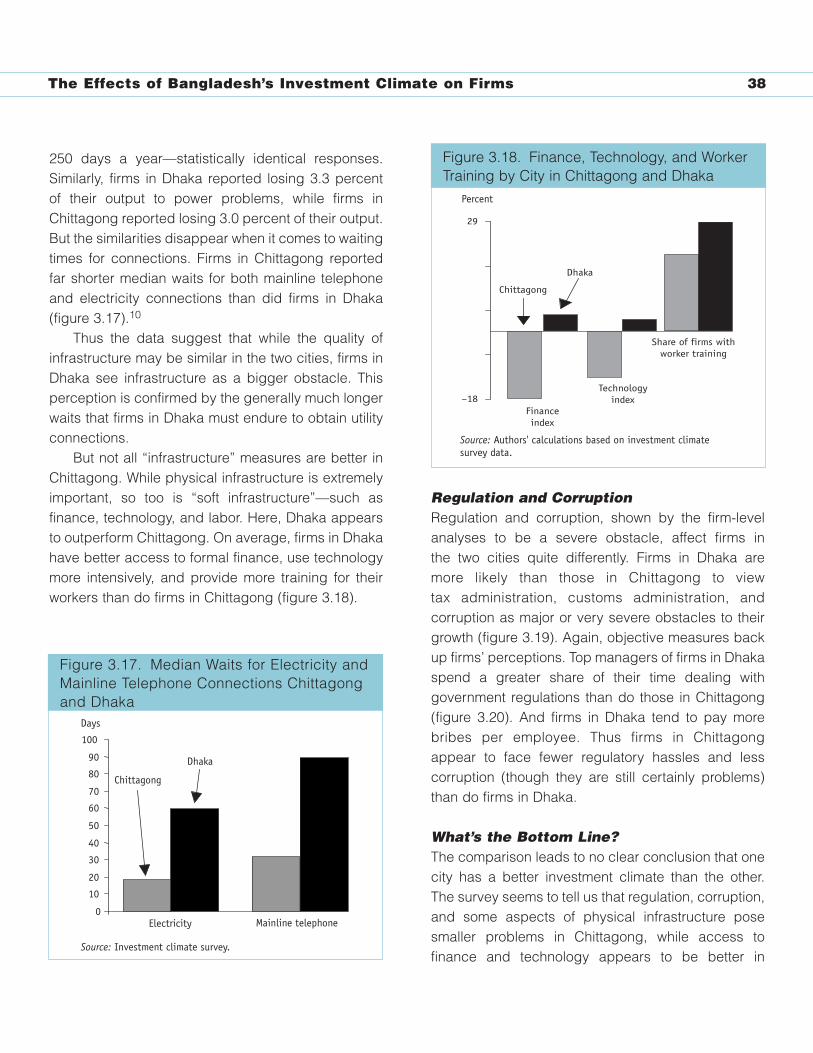

Comparing the Investment Climates in Chittagong and Dhaka 37

Infrastructure 37

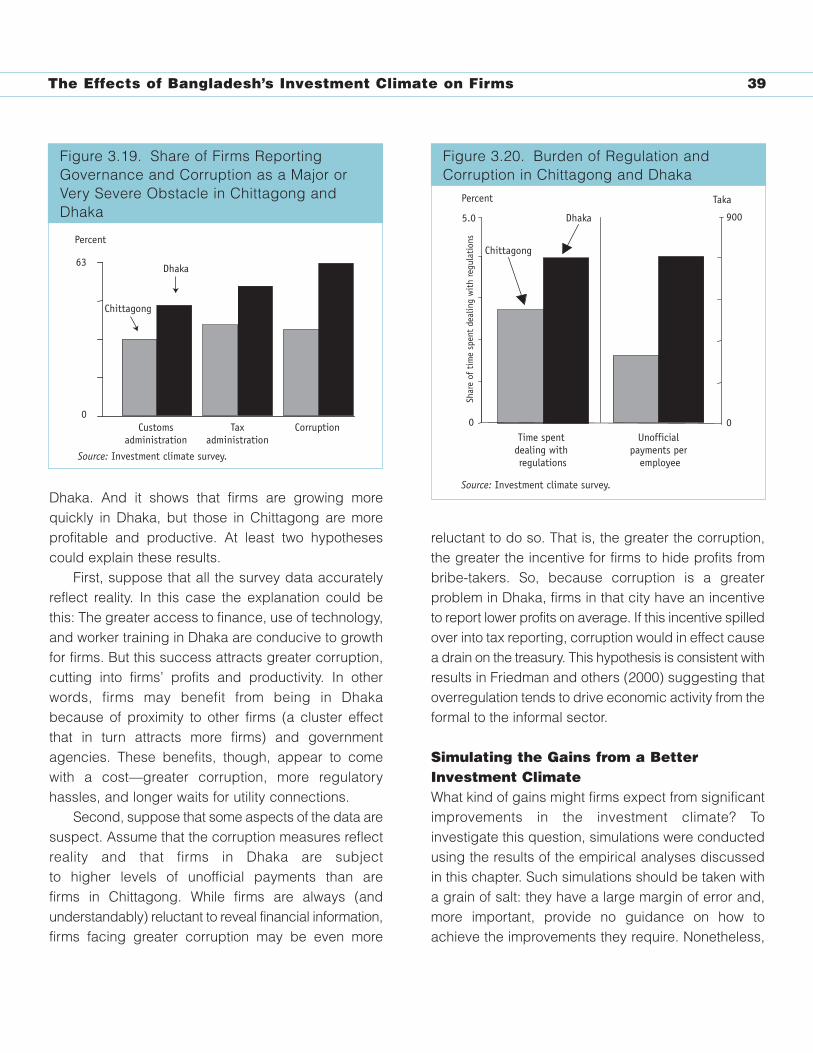

Regulation and Corruption 38

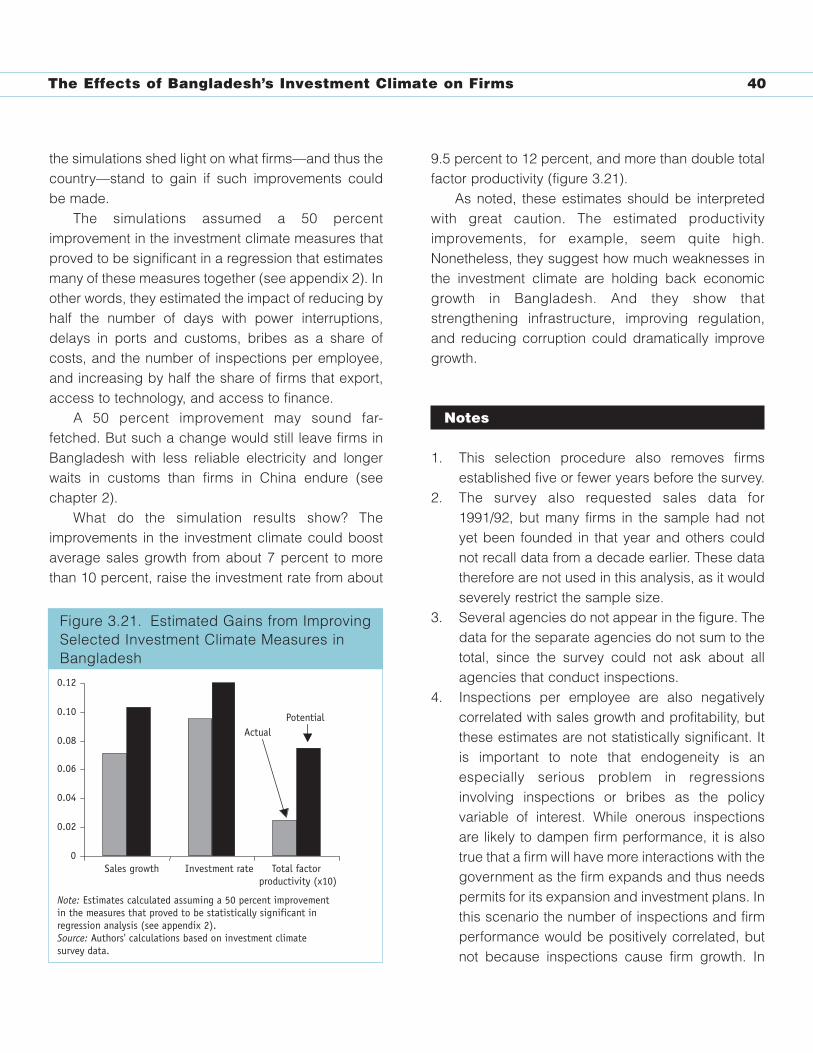

What’s the Bottom Line? 38

Simulating the Gains from a Better Investment Climate 39

4. Conclusions and PolicyRecommendations 42

Easing Bottlenecks in Infrastructure 42

Power 42

Telecommunications 45

Transport, Ports, and Customs 46

Strengthening Governance 46

Improving Access to Finance 47

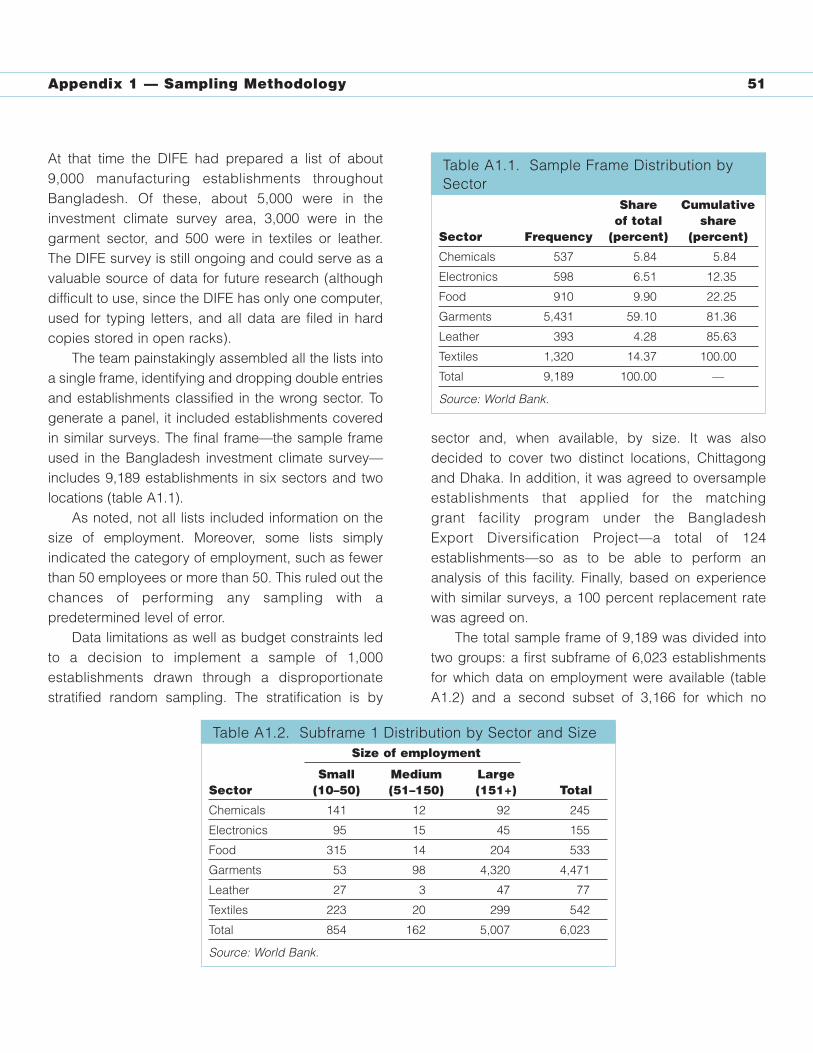

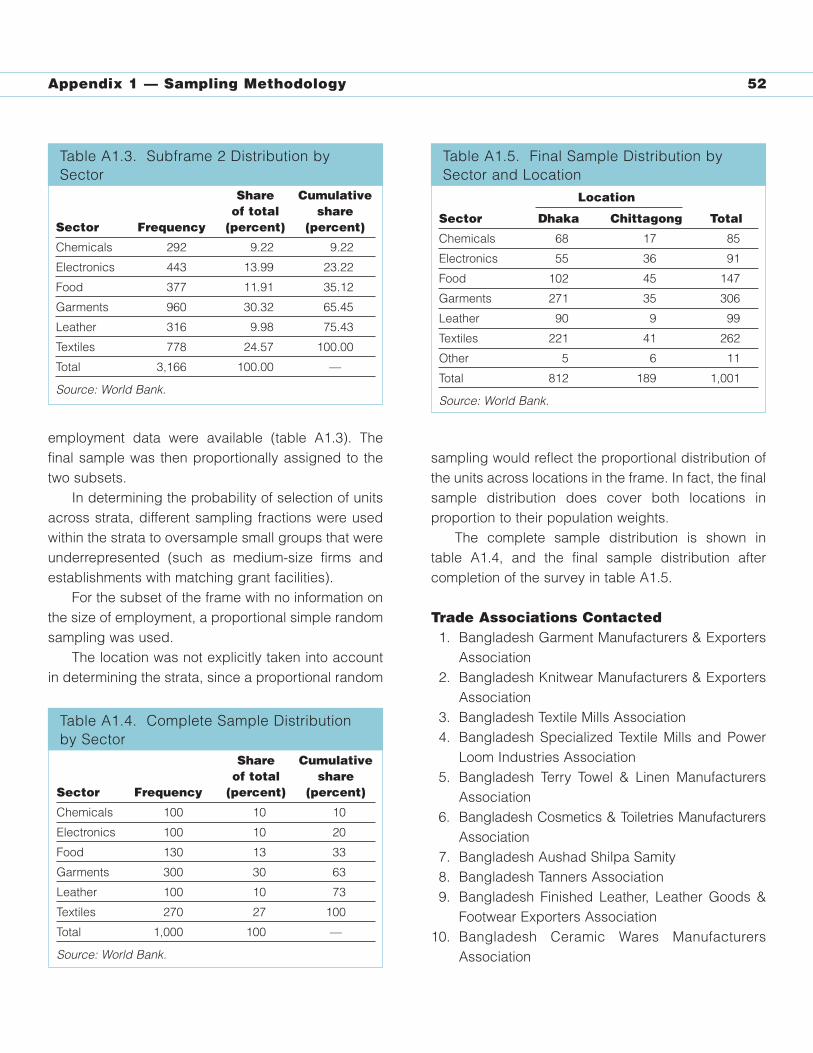

Appendix 1: Sampling Methodology 50

Trade Associations Contacted 52

Chambers of Commerce Contacted 53

Other Sources 53

Government Sources 53

Others 53

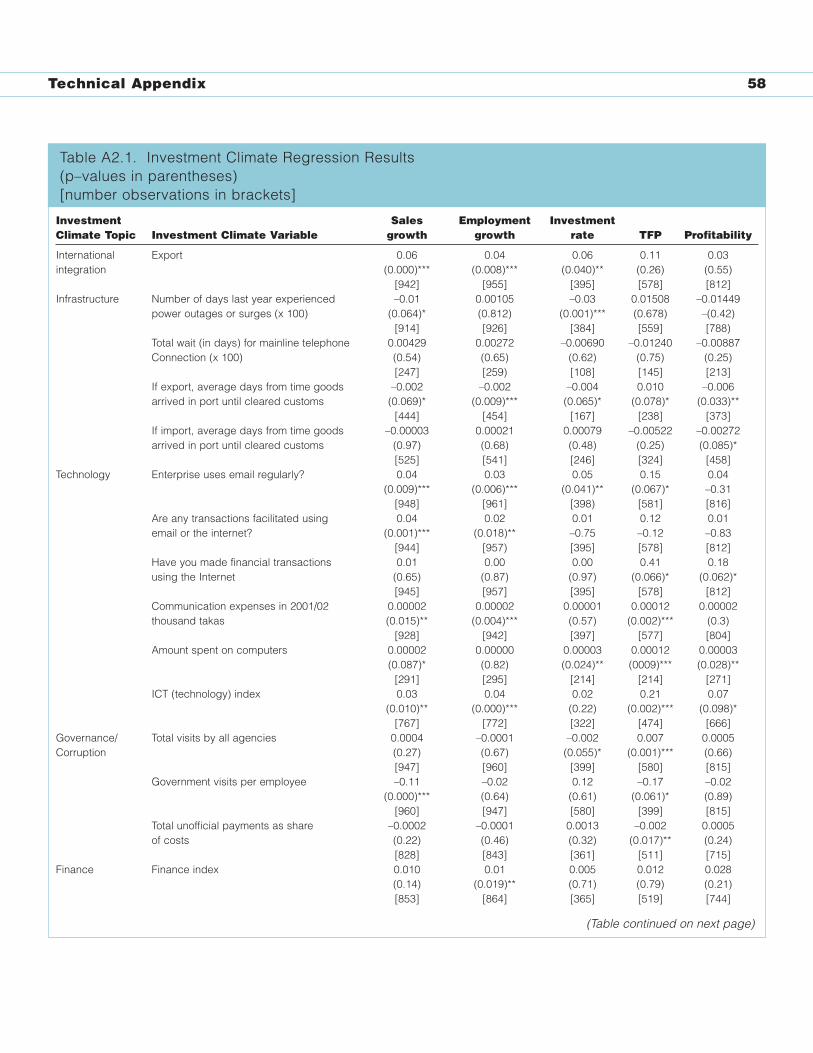

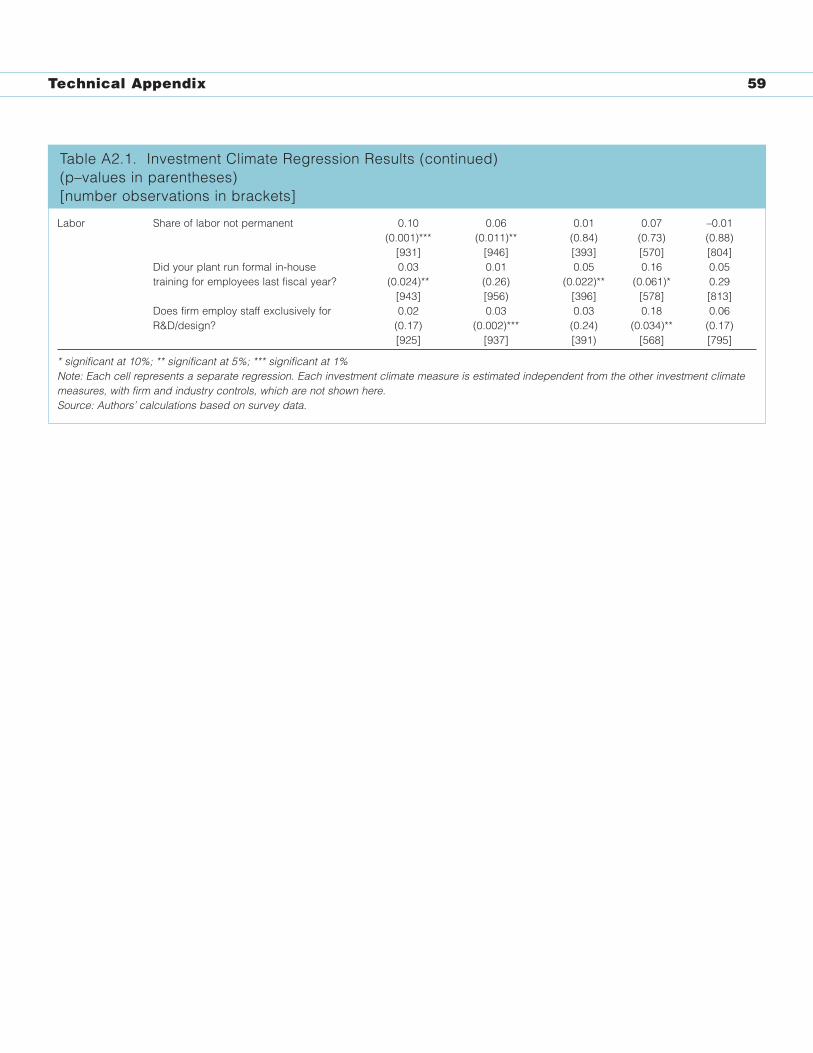

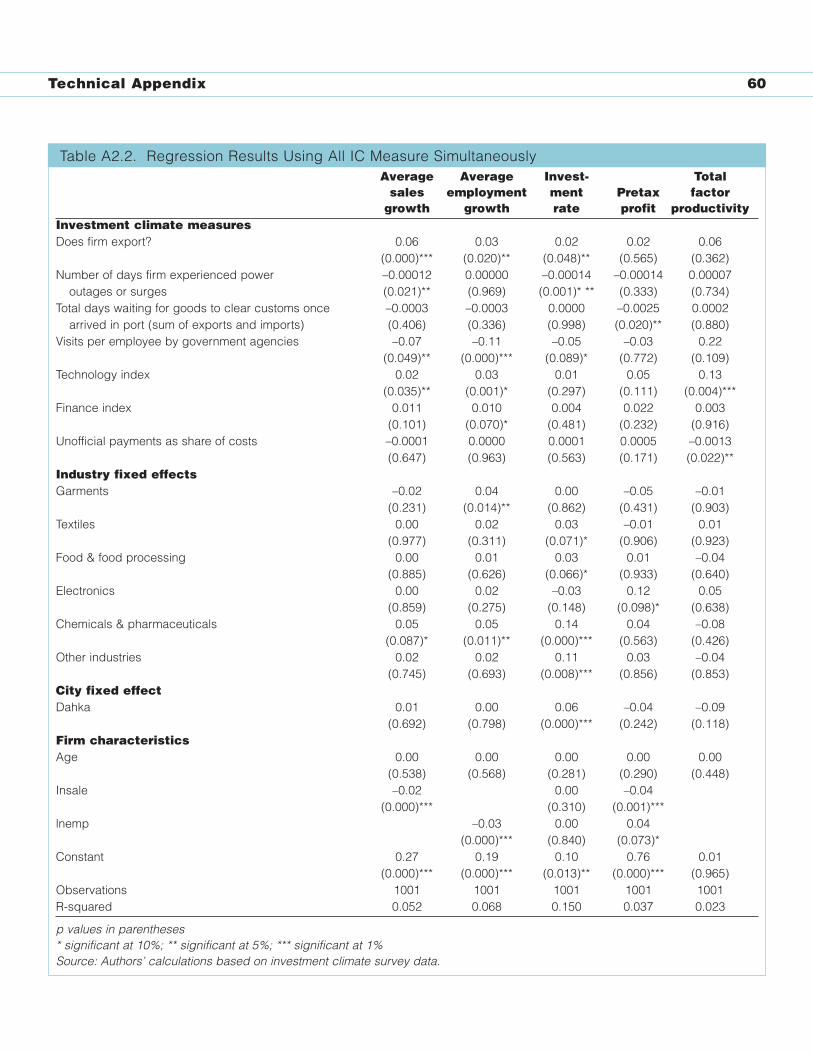

Appendix 2: Technical Appendix 56

Regression Analyses 56

Simulations 57

Indexes 57

Appendix 3: Standard Investment Climate Tables 62

References 73

Contents iii

Acknowledgments iv

The authors gratefully acknowledge financial supportfrom the United Kingdom’s Department forInternational Development (DFID), which supportedthe implementation of the survey and the collaborationwith the Bangladesh Enterprise Institute (BEI) in thesurvey and analytical work. BEI staff contributing tothis report include Farooq Sobhan and M. H.Khaleque. World Bank staff contributing to the reportinclude Khurshid Alam, George R. G. Clarke, DavidDollar, Giuseppe Iarossi, Esperanza Lasagabaster,Syed A. Mahmood, Giovanni Tanzillo, and Scott

Wallsten. The study team appreciates the efforts ofadvisors of the survey team. Members of the advisorypanel include Sayed Alamgir, F. Chowdhury,Ambassador Mustafa Faruque Mohammed,Ambassador M. Aminul Islam, Ambassador M.Shafiullah, Zahid Hussain, and M. Shamsur Rahman.The authors thank Arif Ahamed of World Bank, K. B. AlMasum, and Ayesha Novera for excellent researchassistance and the Survey and Research System inBangladesh for collaborating with the BEI inimplementing the survey.

Acronyms and Abbreviations v

ASYCUDA++ Automated System for CustomsData

BEI Bangladesh Enterprise Institute BPDB Bangladesh Power Development

Board BSIC Bangladesh Standard Industrial

ClassificationBTTB Bangladesh Telegraph and

Telephone Board DESA Dhaka Electric Supply Authority DESCO Dhaka Electric Supply Company DFID Department for International

Development DIFE Department of Inspection for

Factories and Establishments,Ministry of Labor andEmployment, Bangladesh

GDP gross domestic productNCBs national commercial banks PGCB Power Grid Company of

BangladeshUNCTAD United Nations Conference on

Trade and Development UNESCO United Nations Educational,

Scientific, and CulturalOrganization

R&D research and development TFP total factor productivity

Over the past decade Bangladesh performed well onmany macroeconomic indicators, became moreintegrated with the world economy, and achievedimpressive social gains. This progress in the 1990s isheartening. But the performance of other low-incomecountries suggests that Bangladesh has fallen shortof its growth potential. While Bangladesh hasmaintained fairly high per capita growth for the pastdecade, its growth has nonetheless lagged far behindthat in some countries. Take China and India. As aresult of the more rapid growth in these countries, abig gap has opened up in per capita income, thoughall three countries started out at similar income levelsin the 1980s.

Which features of Bangladesh’s investmentclimate pose particular obstacles to economic growthand development? To answer that question, thisinvestment climate assessment uses data from a 2002survey of a 1001 manufacturing firms in Bangladeshand from myriad publicly available sources. The hopeis that its results will help identify the reforms mostcritical to private sector development and facilitateconsensus on a more far-reaching agenda of reform.Some of the main findings:

• Infrastructure poses some of the most severeobstacles facing firms. Bangladesh fares worsethan its neighbors on general measures ofinfrastructure, and the vast majority of firms reportthat problems in infrastructure seriously hampertheir growth.

• Electricity problems plague firms in Bangladesh,which has less generation capacity per capitathan its neighbors. Firms report experiencingpower outages or surges nearly every day theyoperate. As a result, more than 70 percent rely on electric generators—at great expense. Onaverage, these generators cost more than$20,000 to purchase and 50 percent more perkilowatt-hour to operate than the price of powerfrom the public grid.

• Corruption is pervasive. Bangladesh ranks worseon measures of corruption than its neighbors—with more than half the firms reporting it as a majoror very severe obstacle.

• Firms view regulation as a serious problem.Starting a firm in Bangladesh is fairly difficult. Andonce firms are running, they receive frequent visitsfrom government agencies—about 17 a year onaverage.

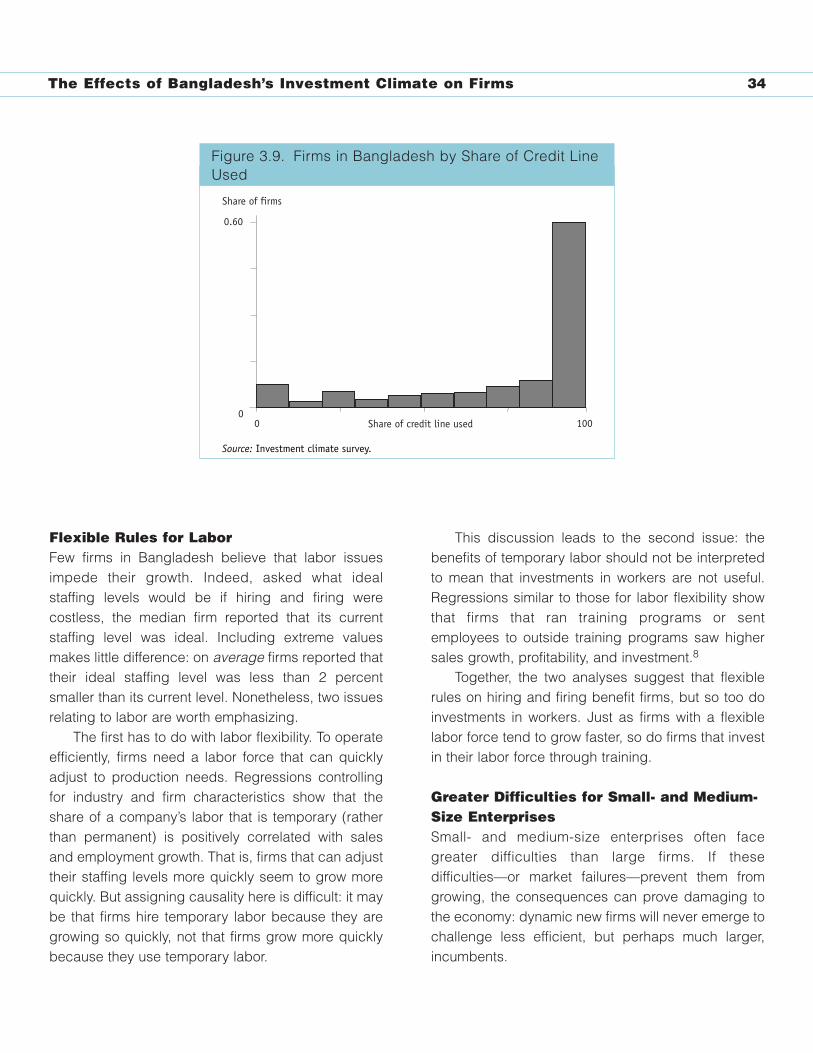

• Finance appears to be a looming problem. Whilemost firms appear to have access to finance, it is mostly short-term and nearly 60 percent of firms with a line of credit report having exhaustedthat credit. Moreover, the very large share of nonperforming loans portends potentialdifficulties.

• Small- and medium-size firms are disproportionatelyaffected by all these problems. The smaller the firm,the more of its resources it devotes to bribes andto dealing with government visits and inspections—and the less likely it is to have access to formalfinance. These problems can pose great barriers tomarket entry and growth for small firms.

Dealing with these problems is no simple matter.But their size and prevalence underscore the urgencyof reform. Among the potentially most importantreforms are unbundling electricity generation andtransmission, encouraging private investment in thepower sector, corporatizing the ports, increasingaccountability in the civil service, and streamliningregulatory procedures while eliminating unnecessaryones.

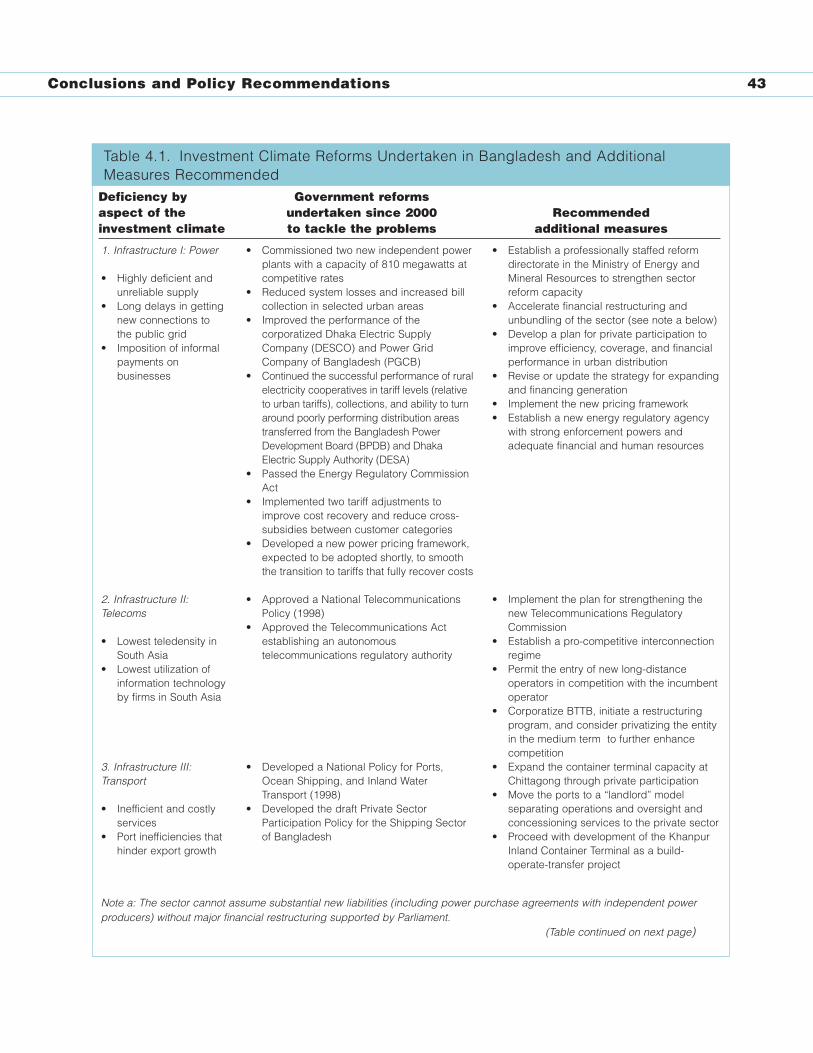

What would the private sector stand to gain fromsuch reforms? Simulations based on the surveyresults estimate the potential gains from a 50 percentimprovement in critical investment climate measures.While a 50 percent improvement may sound large,such a change would still leave Bangladesh with, forexample, less reliable electricity and longer waits incustoms than firms in China endure. The simulation

Executive Summary vi

results suggest that the improvements could boostsales growth from 7 percent to more than 10 percent,raise the investment rate from about 9.5 percent to 12 percent, and more than double total factorproductivity.

Carrying out the needed reforms may be difficult,but the costs of avoiding and delaying them are high.

And the urgency of reform will only increase as theMultifibre Arrangement is phased out by December2004, deepening the obstacles posed by a poorinvestment climate. The survey findings show, inrigorous, quantifiable ways, how much the poorinvestment climate costs firms—and how the voices ofthe thousand firms call out for reform.

Executive Summary vii

1. Investment Climate Matters

In recent years policymakers and multilateralorganizations have increasingly emphasized theimportance of a sound investment climate forpromoting economic growth in developing countries(Stern 2002b). Emphasizing investment used to meanadvocating greater quantities of investment, under theassumption that a financing gap was a barrier todevelopment. Today, few accept this simplistic view.Indeed, recent research shows surprisingly littlecorrelation between investment levels and growthrates, at least in the short run (Easterly 1999). Thuswhile this report is concerned with investment, it does not focus on its quantity. Instead, it focuses on the institutional and policy environment thatdetermines whether investments pay off in greatercompetitiveness for firms and in sustained growth forthe economy—that is, the investment climate.1 Aproductive investment climate can be broadly thoughtof as an environment in which governance andinstitutions support entrepreneurship and well-functioning markets in order to help generate growthand development.

Key Features of the Investment ClimateDefining investment climate precisely is difficult. Butone useful definition is the “policy, institutional, andbehavioral environment, both present and expected,that influences the returns, and risks, associated withinvestment” (Stern 2002b). This environment isgenerally seen as having three main features:macroeconomic conditions, governance, andinfrastructure. Macroeconomic (or country-level)factors include such issues as fiscal, monetary, andexchange rate policies and political stability.Governance relates to government interactions withbusiness, which typically mean regulation andcorruption, both of which affect the costs of starting andrunning a business. Infrastructure refers to the qualityand quantity of physical infrastructure (such as power,

transport, and telecommunications). More broadly, itcan also refer to financial infrastructure (such asbanking)—or access to finance. Beyond these featuresof the investment climate, this report also looks atinternational integration and human resources.

GovernanceA country’s general structure of governance and theinstitutions that govern interactions between businessand government determine the burden that firms facein complying with government regulations, the qualityof government services, and the extent to whichcorruption is associated with the procurement of these services. A large regulatory burden is oftenassociated with corruption, involving payments toinspectors who visit firms or to officials who grantpermits. Corruption can easily deter foreign anddomestic investors. Recent empirical researchconfirms, for example, that measures of corruption aresignificantly and negatively related to inflows offoreign direct investment (Smarzynska and Wei 2000;Wei 2000).

Finding quantitative measures of the quality ofgovernment regulation and the cost imposed bycorruption is generally difficult. But many researchersand practitioners have tried to produce aggregatestatistics that can be used for comparisons acrosscountries. One study looks at the regulatory andadministrative issues affecting firms’ day-to-dayoperations. Friedman and others (2000) compileindexes of taxation levels and “overregulation”(essentially, indexes of the business environment) in69 countries. While they find no evidence that highertax rates drive firms underground, they do find asignificant correlation between measures ofoverregulation and the size of the unofficial economy:“more overregulation is correlated with a largerunofficial economy” (Friedman and others 2000). Thuswhile higher tax rates do not appear to drive awayinvestors, the myriad obstacles to starting andrunning a business do.

1Investment Climate Matters

Investment Climate Matters 2

This does not mean that all regulations indeveloping countries are only onerous andunnecessary. On the contrary, regulations andregulatory agencies can play an important role inmitigating market failures (such as environmentalpollution), protecting consumers (for example, againstfirms that can exercise market power), and ensuringsafe working conditions. But regulations in developingcountries tend to be more complex and bureaucraticthan necessary, are associated with corruption, andoften are not intended to correct market failures orprotect consumers. Indeed, Djankov and others(2002) find that more regulations are generally notassociated with better societal outcomes indeveloping countries. This report focuses on the costsof regulatory inspections to firms, however; societaloutcomes are beyond its scope.

A particularly important aspect of governance isthe ease with which firms can enter and exit amarket—an important determinant of productivity,investment, and entrepreneurship (Lansbury andMayes 1996). Where entry and exit are relatively easy,poorly performing firms can leave the market—permitting their assets to be reallocated to moreproductive uses—and new, more productive andinnovative firms can emerge. The entrepreneurshipthat is unleashed accelerates economic growth andwelfare improvements in developing and transitioneconomies. New firms “have usually been the fastest-growing segment in transition countries” (McMillanand Woodruff 2002).

But the governments of many developing andtransition economies, failing to recognize that birthsand deaths of firms are an inevitable corollary ofentrepreneurial risk taking, have erected a maze ofadministrative obstacles to starting, operating, andclosing firms. Compiling data on entry regulations in85 countries, Djankov and others (2002) discoverenormous variation in the number of proceduresrequired to start firms, ranging from 2 in Canada to 20in the Dominican Republic (with Bolivia and the

Russian Federation also close to 20). The timerequired to establish a firm ranges from 2 businessdays to 214 in Mozambique. These procedures canbe extremely costly to the economy: in Mozambiquethe cost of official procedures (that is, excludingbribes) for setting up a new business amounts to 214 percent of per capita income. In Africa, Emeryand others (2000) find, “this whole maze of often duplicative, complex, and non-transparentprocedures can mean delays of up to two years to getinvestments approved and operational.” Moreover,Djankov and others (2002) find that stricter regulationof entry is correlated with more corruption and a largerinformal economy.

InfrastructureIn countries with poor infrastructure, businesses mustdevote more resources to such tasks as acquiringinformation, procuring inputs, and getting theirproducts to market. Especially for goods marketedinternationally, poor infrastructure can undermine thecompetitiveness of firms—at best making it morecostly for them to operate, and at worst deterring themfrom entering markets where they would otherwisehave been able to operate efficiently.

Infrastructure and firm performance interact inseveral ways. Established firms already connected toutilities are affected by the quality of the service. Newfirms or firms hoping to expand are concerned withdifficulties in connecting to utilities.

Access to FinanceEconomic theory holds that businesses will invest inprojects where the expected benefits exceed the costof investment. But this efficient outcome can beachieved only when entrepreneurs face no creditconstraints unrelated to their own performance. Creditconstraints are less likely in countries with well-developed and well-functioning financial systems.Indeed, a great deal of research has shown theimportance of financial sector development for growth

Investment Climate Matters 3

(Levine 1997; World Bank 2001b). A healthy financialsystem, by freeing firms from financial constraints,allows them to expand according to their expectedpotential rather than their current stock of cash. Thuscountries with well-developed financial systems(banks, stock and bond markets) tend to grow fasterthan countries with less well-developed systems.

International IntegrationResearch has shown that countries that aggressivelypursued integration with the global economy (such asBrazil, China, India, Malaysia, Mexico, the Philippines,and Thailand) grew more quickly in the 1990s thanthose that did not. Indeed, many studies find thatopenness to trade and foreign direct investmentaccelerates growth (for example, Dollar and Kraay2001; and Frankel and Romer 1999).

Studies using different measures of openness totrade—including the relative size of trade (asmeasured by imports and exports as a share of GDP)and the degree of trade distortion (as measured byaverage tariff rates and dispersion)—strongly suggestthat greater openness is associated with faster growthin both industrial and developing countries. Sachsand Warner (1995) find that openness is a highlysignificant determinant of growth and, whencombined with property rights, might even represent asufficient condition for growth in poor economies.Kang and Sawada (2000) find a similar effect ofopenness on growth, arguing that openness,combined with financial development, increasesgrowth in developing countries by reducing the costof investing in human capital.

Human ResourcesThe availability of inputs is a crucial element of theinvestment climate. For human resources, this impliesmore than just an abundant supply of workers. It also implies workers with sufficient education andtechnological know-how.

Linking the Investment Climate with GrowthStudies have found strong correlations betweenmeasures of investment climate and economic growth(see, for example, Kaufmann, Kraay, and Zoido-Lobatón 2000; and Knack and Keefer 1995). Thesestudies typically use data generated from surveys ofprivate businesses and reflect the extent to whichinvestors or firms perceive problems with harassment,corruption, and inefficient regulation. But most macro-level indicators of investment climate used in thesestudies are of little help to countries in identifyingexactly what needs to be done to create a betterinvestment climate. That requires delving much moredeeply, drawing on micro-level evidence from surveysof large numbers of firms, including small andmedium-size enterprises.

To begin to get an objective, empirical look at theinvestment climate at the firm level in Bangladesh, thisreport uses a new survey of 1,001 firms in Chittagongand Dhaka. Following a standard approach forinvestment climate assessments, it compares theinvestment climate in Bangladesh with that in othercountries—including its main competitors, China,India, and Pakistan—using similar surveys andpublicly available country-level data sets (box 1.1).And it explores the investment climate indicators fromBangladesh in more depth at the firm level, throughanalyses that include investigations of how theinvestment climate differs between Chittagong andDhaka and between small and large firms.

An Overview of the Bangladesh EconomyIn the 1990s Bangladesh became increasinglyintegrated with the global economy, with its tradedoubling over the decade to reach 31 percent of GDPby 2001. Efforts to increase integration had started inthe 1980s and continued into the early 1990s. As earlyas 1982 the country’s New Industrial Policy began to lift import controls and encourage exports. The

Investment Climate Matters 4

Revised Industrial Policy of 1986 furthered thesereforms, loosening more restrictions on imports,reducing antiexport bias by rationalizing tariffs, andeasing the import of inputs for production. By the endof the 1990s average nominal tariff rates inBangladesh had declined from more than 100 percentto about 20 percent, and tariff rates for manufacturedimports from 52 percent to 16 percent. The fixedexchange rate system was replaced with a moreflexibly administered system, foreign investment wasderegulated (with a few exceptions), and restrictionson repatriating profit and income from foreigninvestment were eliminated.

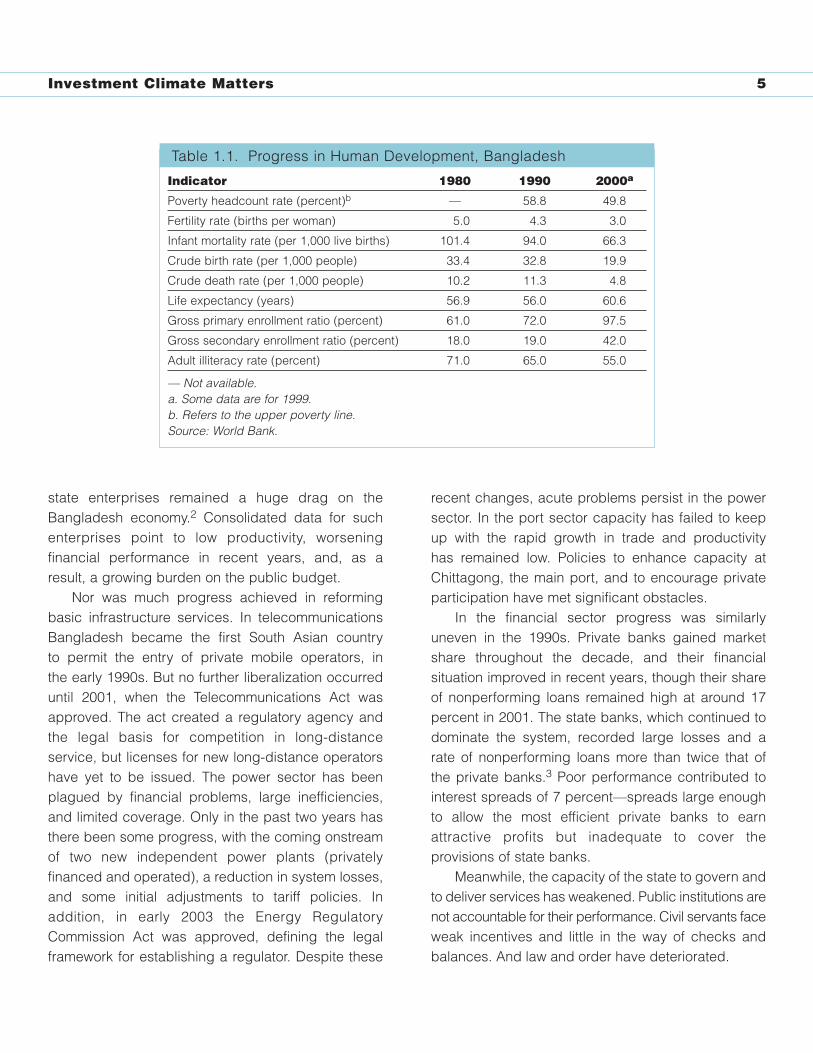

In parallel, the country undertook substantialinvestments in human development, making greatstrides in such areas as primary enrollment, girls’education, immunization, child nutrition, and fertilityreduction. Primary enrollment, for example, rose from61 percent in 1980 to 72 percent in 1990 and 97.5percent in 2000 (table 1.1).

By contrast, reforms in other areas, particularly inthe institutional and regulatory framework, were farless encouraging. Efforts launched in the early 1990sto deepen liberalization across economic sectorssoon lost momentum. The program to divest stateenterprises in manufacturing quickly stagnated, and

Investment climate assessments systematically analyzethe conditions for private investment and enterprisegrowth in a country, drawing on the experience of localfirms to pinpoint the areas where reform is most needed to improve the private sector’s productivity andcompetitiveness. By providing a practical foundation forpolicy recommendations and involving local partnersthroughout the process, the assessments are designed togive greater impetus to policy reforms that can speed theprivate sector’s growth, leading to faster economic growthand poverty reduction.

Produced by the World Bank Group in closepartnership with a public or private institution in eachcountry, the investment climate assessments are basedon a survey of private enterprises designed to find outwhat difficulties they encounter in starting and running abusiness—and, if the business fails, in exiting. Thesurvey captures firms’ experience in a range of areas—financing, governance, regulation, tax policy, laborrelations, conflict resolution, infrastructure services,supplies and marketing, technology and training. All these are areas where difficulties can addsubstantially to the costs of doing business. The surveyattempts to quantify these costs. Using a standardmethodology, the assessment then compares the surveyfindings with those in similar countries to evaluate how

the country’s private sector is faring and how well it cancompete.

The findings of the survey, combined with relevantinformation from other sources, provide a practical basisfor identifying the most important areas for reform aimedat improving the investment climate. The assessmentslook in detail at policy, regulatory, and institutional factorsthat hamper the provision of good-quality infrastructureservices and the functioning of product, financial, andother markets, linking the constraints to firms’ costs andproductivity.

In each country the investment climate assessmentsdraw on the guidance and expertise of local partners ingovernment and the business community. The findingsand policy recommendations emerging from theassessments are discussed extensively with the privatesector and other stakeholders in the country. This broaddissemination of the findings is aimed at engaging notonly policymakers but also business leaders, investors,nongovernmental organizations, and the donorcommunity in shaping the national private sectordevelopment strategy, forging consensus on the prioritiesfor reform of the investment climate, and laying thegroundwork for concrete responses to the problemsidentified. Updates of the assessment can help trackprogress in improving the investment climate.

Box 1.1. What Is an Investment Climate Assessment?

Investment Climate Matters 5

state enterprises remained a huge drag on theBangladesh economy.2 Consolidated data for suchenterprises point to low productivity, worseningfinancial performance in recent years, and, as aresult, a growing burden on the public budget.

Nor was much progress achieved in reformingbasic infrastructure services. In telecommunicationsBangladesh became the first South Asian country to permit the entry of private mobile operators, in the early 1990s. But no further liberalization occurreduntil 2001, when the Telecommunications Act wasapproved. The act created a regulatory agency andthe legal basis for competition in long-distanceservice, but licenses for new long-distance operatorshave yet to be issued. The power sector has beenplagued by financial problems, large inefficiencies,and limited coverage. Only in the past two years hasthere been some progress, with the coming onstreamof two new independent power plants (privatelyfinanced and operated), a reduction in system losses,and some initial adjustments to tariff policies. Inaddition, in early 2003 the Energy RegulatoryCommission Act was approved, defining the legalframework for establishing a regulator. Despite these

recent changes, acute problems persist in the powersector. In the port sector capacity has failed to keepup with the rapid growth in trade and productivity has remained low. Policies to enhance capacity atChittagong, the main port, and to encourage privateparticipation have met significant obstacles.

In the financial sector progress was similarlyuneven in the 1990s. Private banks gained marketshare throughout the decade, and their financialsituation improved in recent years, though their shareof nonperforming loans remained high at around 17percent in 2001. The state banks, which continued todominate the system, recorded large losses and arate of nonperforming loans more than twice that ofthe private banks.3 Poor performance contributed tointerest spreads of 7 percent—spreads large enoughto allow the most efficient private banks to earnattractive profits but inadequate to cover theprovisions of state banks.

Meanwhile, the capacity of the state to govern andto deliver services has weakened. Public institutions arenot accountable for their performance. Civil servants faceweak incentives and little in the way of checks andbalances. And law and order have deteriorated.

Indicator 1980 1990 2000a

Poverty headcount rate (percent)b — 58.8 49.8

Fertility rate (births per woman) 5.0 4.3 3.0

Infant mortality rate (per 1,000 live births) 101.4 94.0 66.3

Crude birth rate (per 1,000 people) 33.4 32.8 19.9

Crude death rate (per 1,000 people) 10.2 11.3 4.8

Life expectancy (years) 56.9 56.0 60.6

Gross primary enrollment ratio (percent) 61.0 72.0 97.5

Gross secondary enrollment ratio (percent) 18.0 19.0 42.0

Adult illiteracy rate (percent) 71.0 65.0 55.0

— Not available.a. Some data are for 1999. b. Refers to the upper poverty line.Source: World Bank.

Table 1.1. Progress in Human Development, Bangladesh

Investment Climate Matters 6

Despite this mixed picture in reform, Bangladeshachieved positive growth results. In 1991–2000 realGDP growth averaged about 4.8 percent a year (60percent for the period), and its volatility declined.Contributing to this higher growth trajectory washigher private investment and greater integration withthe global economy. Private investment increasedfrom a very depressed level of 4 percent of GDP in theearly 1970s to more than 15 percent of GDP in the late1990s (table 1.2). Investment growth has been themost stable stimulus to GDP growth during the lasttwo decades. Exports began to emerge as anothermajor source of growth in the late 1980s, becomingeven more important in the 1990s. The export stimuluscame mainly from woven garments and knitwear,which grew from $32 million in the early 1980s tonearly $5 billion in early 2000. Woven garments andknitwear now account for 75 percent of Bangladesh’stotal annual exports. The next largest items are frozen

food and raw jute, which respectively account for 5percent and 4 percent of total exports.

The new growth pattern is reflected in thestructure of the economy, which underwent significantchanges (table 1.3). The share of agriculture(including fisheries) declined from about 32 percent ofGDP in the early 1980s to slightly over 24 percent ofGDP in fiscal year 2002. The share of manufacturing,on the other hand, increased from less than 11percent of GDP in the early 1980s to 15 percent ofGDP in fiscal year 2002. However, the latter is stillsmall relative to the share of manufacturing in theSouth East Asian economies (around 25–35 percentof GDP). Also manufacturing activity remains heavilyconcentrated in Dhaka and Chittagong.

Bangladesh’s economic performance, combinedwith its notable success in slowing population growthover the past two decades, produced real per capitaGDP growth of 3.1 percent a year (36 percent over the

FY81 FY91 FY99 FY00 FY01 FY02

Investment 17.6 16.9 22.2 23.0 23.1 23.2

Private 12.4 10.3 15.5 15.6 15.8 16.8

Public 5.2 6.6 6.7 7.4 7.2 6.4

Gross Domestic Saving 12.5 14.6 17.7 17.9 18.0 18.2

Gross National Saving 17.8 19.7 22.3 23.1 22.4 23.4

Source: World Bank.

Table 1.2. Investment and Savings as Percent of GDP,Bangladesh (1981–2002)

FY81 FY91 FY99 FY00 FY01 FY02

Agriculture and fishing 32.3 28.7 24.3 24.3 24.6 24.1

Manufacturing 10.8 12.2 15.2 15.0 14.8 15.0

Other 56.8 59.1 60.5 60.7 60.6 60.9

GDP 100.0 100.0 100.0 100.0 100.0 100.0

Source: Bangladesh Bureau of Statistics

Table 1.3 GDP Composition of Selected Sectors, Bangladesh(1981–2002)

Investment Climate Matters 7

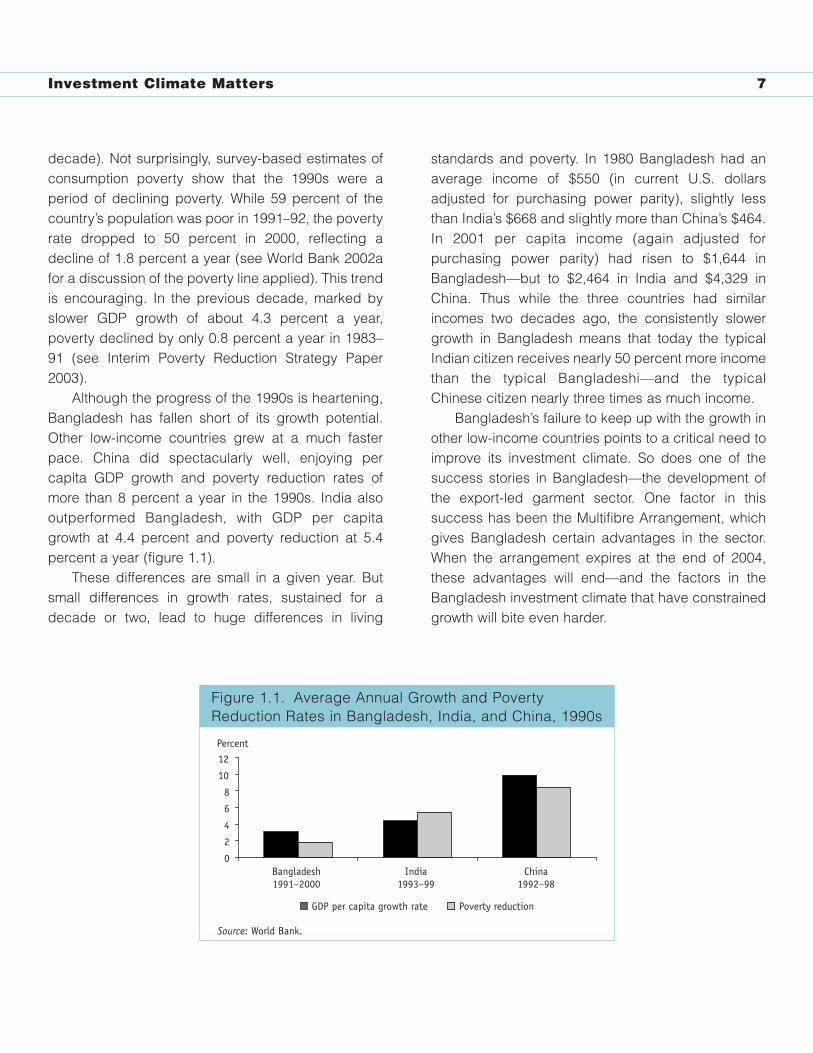

decade). Not surprisingly, survey-based estimates ofconsumption poverty show that the 1990s were aperiod of declining poverty. While 59 percent of thecountry’s population was poor in 1991–92, the povertyrate dropped to 50 percent in 2000, reflecting adecline of 1.8 percent a year (see World Bank 2002afor a discussion of the poverty line applied). This trendis encouraging. In the previous decade, marked byslower GDP growth of about 4.3 percent a year,poverty declined by only 0.8 percent a year in 1983–91 (see Interim Poverty Reduction Strategy Paper2003).

Although the progress of the 1990s is heartening,Bangladesh has fallen short of its growth potential.Other low-income countries grew at a much fasterpace. China did spectacularly well, enjoying percapita GDP growth and poverty reduction rates ofmore than 8 percent a year in the 1990s. India alsooutperformed Bangladesh, with GDP per capitagrowth at 4.4 percent and poverty reduction at 5.4percent a year (figure 1.1).

These differences are small in a given year. Butsmall differences in growth rates, sustained for adecade or two, lead to huge differences in living

standards and poverty. In 1980 Bangladesh had anaverage income of $550 (in current U.S. dollarsadjusted for purchasing power parity), slightly lessthan India’s $668 and slightly more than China’s $464.In 2001 per capita income (again adjusted forpurchasing power parity) had risen to $1,644 inBangladesh—but to $2,464 in India and $4,329 inChina. Thus while the three countries had similarincomes two decades ago, the consistently slowergrowth in Bangladesh means that today the typicalIndian citizen receives nearly 50 percent more incomethan the typical Bangladeshi—and the typicalChinese citizen nearly three times as much income.

Bangladesh’s failure to keep up with the growth inother low-income countries points to a critical need toimprove its investment climate. So does one of thesuccess stories in Bangladesh—the development ofthe export-led garment sector. One factor in thissuccess has been the Multifibre Arrangement, whichgives Bangladesh certain advantages in the sector.When the arrangement expires at the end of 2004,these advantages will end—and the factors in theBangladesh investment climate that have constrainedgrowth will bite even harder.

Figure 1.1. Average Annual Growth and Poverty Reduction Rates in Bangladesh, India, and China, 1990s

0

2

4

6

8

10

12

Bangladesh1991–2000

India1993–99

China1992–98

GDP per capita growth rate Poverty reduction

Percent

Source: World Bank.

Figure 1.1. Average Annual Growth and PovertyReduction Rates in Bangladesh, India, and China, 1990s

Investment Climate Matters 8

The Survey—and What Its Findings RevealWhat factors in the investment climate have preventedBangladesh from growing more quickly? To gather thefirm-level data imperative for answering this question,the Bangladesh Enterprise Institute and the WorldBank conducted a survey of manufacturingenterprises in late 2002. The lack of a reliable andrecent census of manufacturers made sampleselection especially difficult. The sample ultimatelywas drawn from a census of manufacturing industriesprovided by the Bangladesh Bureau of Statistics,combined with lists of firms provided by tradeassociations and chambers of commerce (seeappendix 1 for a detailed discussion of the samplingmethodology).4

Two criteria were used to choose industries for thesurvey: the industries had to be important to theBangladesh economy, and there had to be someoverlap with industries covered by surveys in othercountries to facilitate comparisons. The two criteriaare complementary in Bangladesh. For example, theready-made garment industry is especially importantto Bangladesh, and firms in this industry compete with

similar manufacturers in such countries as China,India, and Pakistan.

Six industries were included in the survey:garments, textiles, food and food processing, leatherand leather products, electronics, and chemicals andpharmaceuticals. The survey collected data from atotal of 1,001 firms in Dhaka (and surrounding areas)and Chittagong (see appendix 1 for a breakdown ofthe firms by industry, city, and other factors).

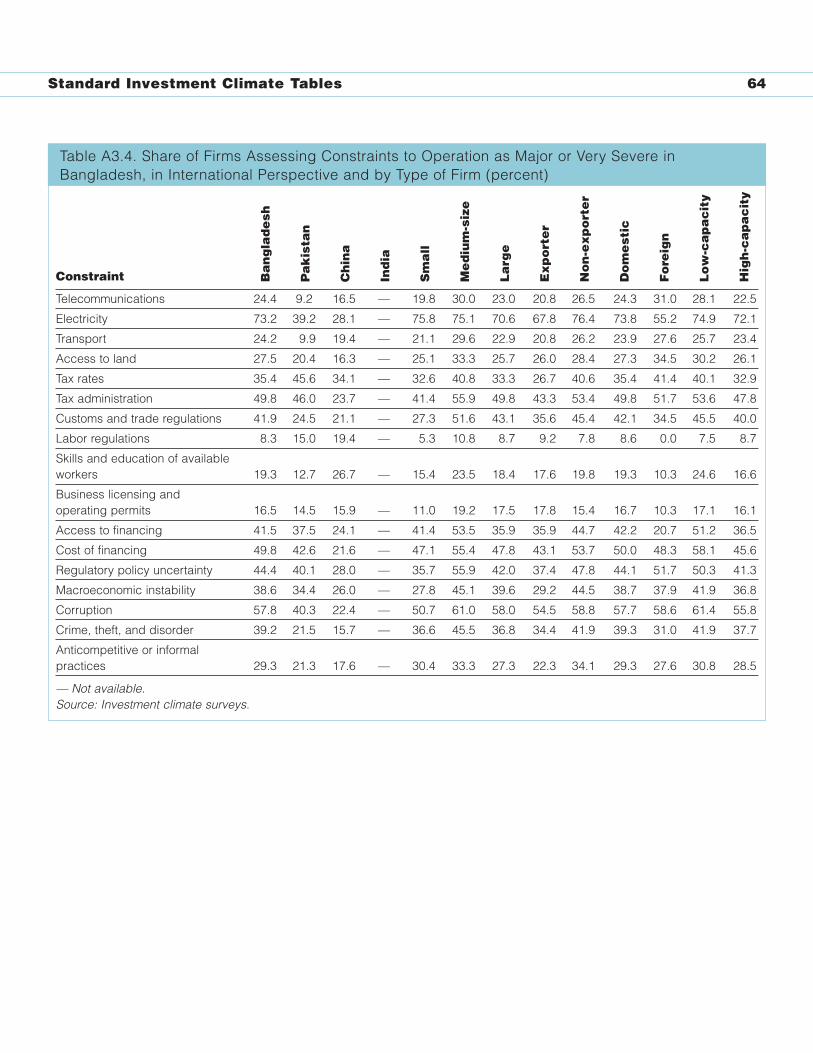

To get an initial sense of how firms view theinvestment climate, the survey asked firms to rate the extent to which a large number of factors in the investment climate constrain their operation andgrowth. By far the most frequent complaint was theconstraint imposed by the poor electricity system(figure 1.2). Ranked next highest were problemsrelating to corruption, governance, and finance.

The ranking results raise two issues. First, firmsranked economic policy uncertainty fifth, highlightingthe importance of stable macroeconomic policies.Since the importance of these issues is wellunderstood, this report focuses on microeconomicissues. Second, the rankings are subjective and may

0 10 20 30 40 50 60 70 80

Access tofinancing

Customs andtrade

Economic policyuncertainty

Cost offinancing

Taxadministration

Corruption

Electricity

Figure 1.2. Top Constraints to Business Operation and Growth in Bangladesh, as Viewed by Firms

Note: Percent of firms rating issues as major or very severe obstacles (percent).Source: Investment climate survey.

Figure 1.2. Top Constraints to Business Operation andGrowth in Bangladesh, as Viewed by Firms

Investment Climate Matters 9

not indicate actual economic problems. Mostentrepreneurs want cheaper financing, but that doesnot necessarily mean that the cost of financing is aneconomic problem.

Nonetheless, these rankings provide a startingpoint for the analysis, and the survey contains awealth of additional information to investigate theseand other issues more objectively and in greaterdepth. Most important, the analysis reveals that thegeneral constraints identified by the firms imposeserious costs on them.

The survey findings, while recording someremarkable improvements in Bangladesh in recentyears, also underscore many unfavorable features ofits investment climate. And they measure the seriouseffort that the country must undertake if it is tostimulate growth and catch up with faster-growingeconomies. Among the aims of this study is to aidBangladesh’s national Poverty Reduction StrategyProgram, one of whose objectives is to accelerategrowth to 7 percent a year—up from less than 5percent in the previous decade. But is this growthtarget realistic for Bangladesh? How will it beattained? The Interim Poverty Reduction StrategyPaper, recognizing the private sector as the mainengine of economic growth, encourages furtheropening of the trade regime and removal of theantiexport bias as well as improvements in a host offactors relating to the investment climate. The hope isthat this study, by shedding further light on the cost of

a poor investment climate, will help inform the nationaldebate on issues relating to private sectordevelopment and aid the consensus buildingnecessary to enact productive reforms.

Notes

1. While social infrastructure is recognized as noless important than its physical and financialcounterparts, a deliberate choice was made toexclude the provision of education and healthservices from the definition of investment climateused in this report. The issues involved inimproving social services are quite different fromthose involved in improving infrastructure andregulation of industry, the focus of the report.

2. In late 2001 state enterprises had physical assetsamounting to 35 percent of GDP, employmentsurpassing 250,000, and investment equal to 9percent of GDP (World Bank 2001a).

3. The market share of national commercial banks(NCBs) and specialized development banksremained at 58 percent at the end of 2001.

4. The survey and its analysis focus on theinvestment climate of the urban manufacturingsector and will therefore need to becomplemented with analytical pieces on ruraldevelopment.

Bangladesh’s Investment Climate in International Perspective 10

2. Bangladesh’s Investment Climate in International Perspective

Comparing the investment climate in Bangladesh withthose in other countries of East and South Asia, as thischapter does, might seem to diminish the progressthat Bangladesh has made, since these are countriesthat have performed relatively well in recent decades.But good performers provide more usefulbenchmarks than poor performers. If Bangladesh is to meet its Millennium Development Goals, recentestimates suggest, it will need to accelerate GDPgrowth to about 7 percent a year over the next decade(Bangladesh 2003). So comparing the performance ofBangladesh with that of economies that are doing wellprovides useful information—both on areas where itlags behind and on areas where it is doing well.

How well does Bangladesh fare in thiscomparison with other Asian countries? On somemeasures, quite well, especially given its lower percapita income. Bangladesh has recorded a relativelystrong performance in economic growth and inflation.It has greatly increased school enrollment, and in timethe improvements in enrollment should boost other

measures of human resources (such as literacy) thatremain low. Bangladesh also appears to performbetter than other low-income countries in somedimensions of governance, that is, regulatory qualityand government efficiency.

But Bangladesh performs less well in other areas.It is less integrated with the global economy thanother Asian countries, with low trade and foreigndirect investment and high formal and informalbarriers to trade. It has poor-quality physicalinfrastructure, especially in the power sector. It doespoorly on some measures of governance, with highcorruption, a weak rule of law, and a largeadministrative burden for starting a business. And itperforms poorly on technology-related issues, withrelatively low spending on research and developmentand weak basic research.

A Strong Macroeconomic PerformanceBangladesh has turned in a strong macroeconomicperformance in recent years. The country’s per capitaGDP growth, negative in the 1970s, rose to 1.7percent in the 1980s and to 3.1 percent in 1990–2001(figure 2.1). Its per capita growth in the 1990s

Figure 2.1. Average Annual Per Capita GDP Growth in Bangladesh and Comparator Countries, 1990–2001

–10123456789

Bang

lade

sh -

1970

s

Bang

lade

sh -

1980

s

Bang

lade

sh -

199

0-20

01

Phili

ppin

es

Low

inco

me

Paki

stan

Low

& m

iddl

e in

com

e

Indo

nesi

a

Indi

a

Sri L

anka

Thai

land

Mal

aysi

a

Chin

a

Source: World Bank 2002c.

Percent

Figure 2.1. Average Annual Per Capita GDP Growth inBangladesh and Comparator Countries, 1990–2001

Bangladesh’s Investment Climate in International Perspective 11

compared favorably with that in other low-incomecountries, where growth averaged 1.2 percent overthe decade. But Bangladesh lagged behind manyother countries in East and South Asia, where percapita growth in the 1990s averaged 3.5 percent in India, 3.7 percent in Sri Lanka, and 8.2 percent inChina.

Nonetheless, Bangladesh made strong gains inper capita income. Moreover, the growth wasaccompanied by—and contributed to—a host of otherachievements: a decline in the poverty rate (from 59percent in 1990–91 to 50 percent in 2000; Stern2002a), a significant drop in fertility (from 6.3 birthsper woman in 1975 to 3.3 in 1997–99), a reduction ininfant mortality (from 153 deaths per 1,000 live birthsin 1975 to 66 in 2000), and impressive gains incombating child malnutrition and starvation. All thesegains are consistent with recent evidence showingthat while GDP growth alone is not sufficient forreducing poverty, it does benefit the poor (Dollar and Kraay 2002), making it significantly easier for countries to achieve their poverty reduction goals.

In another positive trend, Bangladesh has keptinflation lower than most other countries in East andSouth Asia. Its consumer price inflation averaged 5.1percent in 1990–2001, compared with 7.1 percent inChina, 8.6 percent in India, and 9.2 percent inPakistan (figure 2.2). Moreover, although inflation inBangladesh remains higher than that in manyindustrial countries, it appears to be significantlybelow the level where it has a strong adverse impacton economic growth.1

The reasonably strong macroeconomic record inBangladesh, however, masks the underlying featuresof the investment climate that affect—and are affectedby—macroeconomic performance.

Poor Integration with the Global EconomyEvidence suggests that Bangladesh is not wellintegrated with the global economy, despite

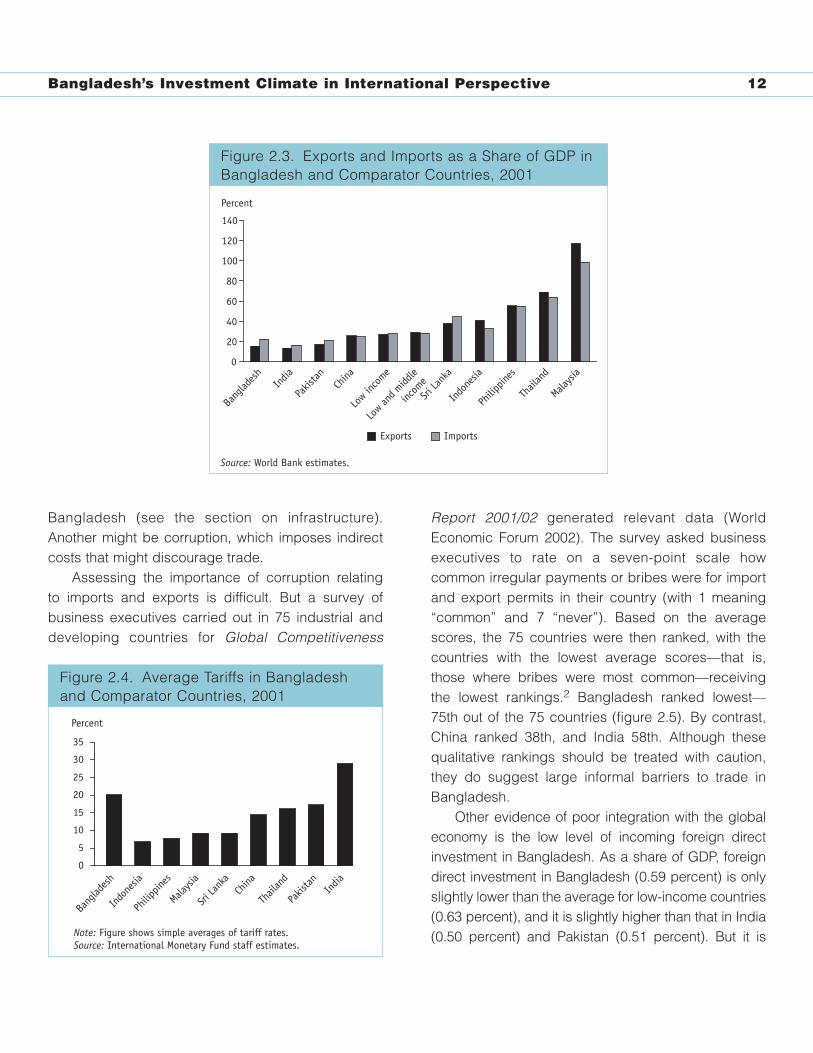

significant growth in trade in recent years. Thecountry’s exports rose from only 6 percent of GDP in 1980 to 15 percent in 2001, while its importsincreased from 18 percent of GDP to 23 percent.These shares compare favorably with those of Indiaand Pakistan but less so with those of other low- andmiddle-income countries, especially in East Asia(figure 2.3). Low-income countries as a group alsooutperform Bangladesh, with exports accounting for28 percent of GDP on average, and imports for 29percent.

What accounts for the trends in trade forBangladesh? One likely contributor to the largegrowth in trade over the past decade is the significantliberalization in tariffs, which fell from more than 100percent in 1990 to only about 20 percent in 2001. Thisliberalization, primarily in the early 1990s, left averagetariffs in Bangladesh in 2001 lower than those in India(29 percent), for example (figure 2.4). Even so,Bangladesh’s average tariffs remained higher thanthose in many other developing countries in Asia,including Pakistan (17 percent), China (14 percent),and Indonesia (7 percent).

So formal barriers to trade remain. And informalbarriers are also important. One such barrier is therelative poor performance of ports and customs in

Figure 2.2. Average Annual Inflation in Bangladesh and Comparator Countries, 1990–2001

02468

10121416

Malaysia

Thail

and

China

India

Philip

pines

Pakis

tan

Sri La

nka

Indo

nesia

Source: World Bank 2002c.

Percent

Bang

lades

h

Figure 2.2. Average Annual Inflation inBangladesh and Comparator Countries,1990–2001

Bangladesh’s Investment Climate in International Perspective 12

Bangladesh (see the section on infrastructure).Another might be corruption, which imposes indirectcosts that might discourage trade.

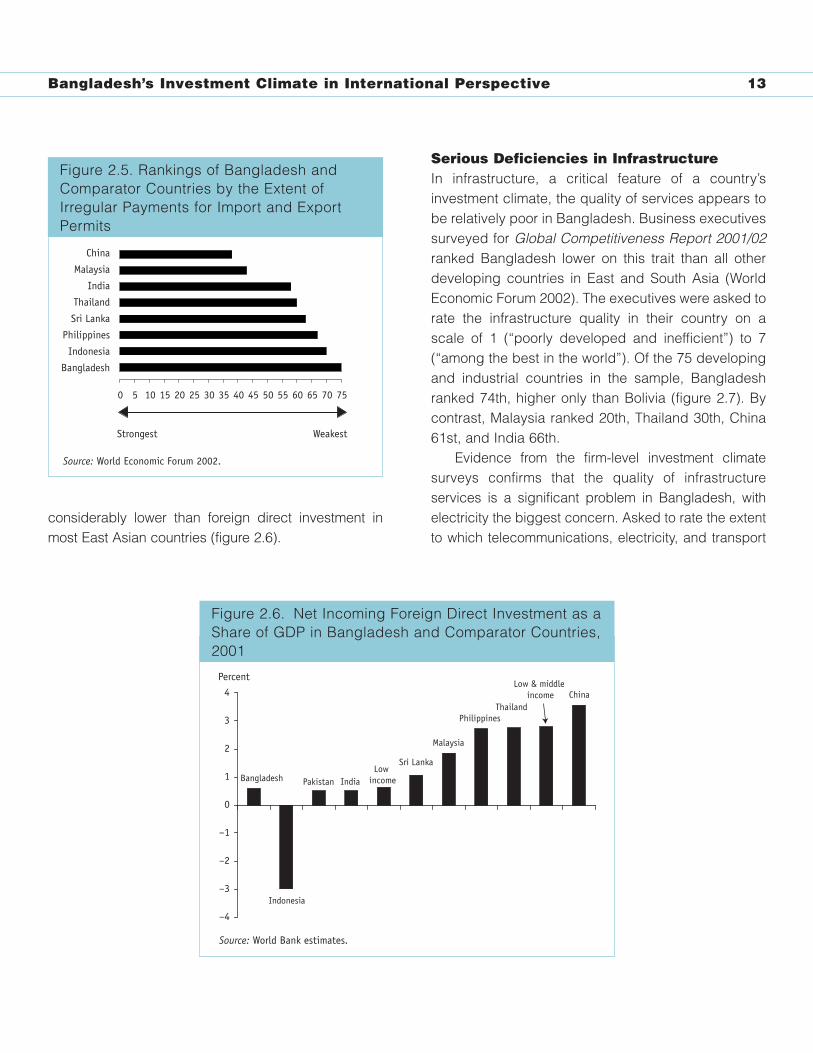

Assessing the importance of corruption relating to imports and exports is difficult. But a survey ofbusiness executives carried out in 75 industrial anddeveloping countries for Global Competitiveness

Report 2001/02 generated relevant data (WorldEconomic Forum 2002). The survey asked businessexecutives to rate on a seven-point scale howcommon irregular payments or bribes were for importand export permits in their country (with 1 meaning“common” and 7 “never”). Based on the averagescores, the 75 countries were then ranked, with thecountries with the lowest average scores—that is,those where bribes were most common—receivingthe lowest rankings.2 Bangladesh ranked lowest—75th out of the 75 countries (figure 2.5). By contrast,China ranked 38th, and India 58th. Although thesequalitative rankings should be treated with caution,they do suggest large informal barriers to trade inBangladesh.

Other evidence of poor integration with the globaleconomy is the low level of incoming foreign directinvestment in Bangladesh. As a share of GDP, foreigndirect investment in Bangladesh (0.59 percent) is onlyslightly lower than the average for low-income countries(0.63 percent), and it is slightly higher than that in India(0.50 percent) and Pakistan (0.51 percent). But it is

Figure 2.4. Average Tariffs in Bangladesh and Comparator Countries, 2001

0

5

10

15

20

25

30

35

Bang

lades

h

Indo

nesia

Philip

pines

Malaysia

Sri La

nka

China

Thail

and

Pakis

tan India

Note: Figure shows simple averages of tariff rates.Source: International Monetary Fund staff estimates.

Percent

Figure 2.4. Average Tariffs in Bangladeshand Comparator Countries, 2001

Figure 2.3. Exports and Imports as a Share of GDP in Bangladesh and Comparator Countries, 2001

0

20

40

60

80

100

120

140

Bang

lades

h

Pakis

tan

Low in

come

Sri La

nka

Philip

pines

Malaysia

Exports Imports

Source: World Bank estimates.

Percent

India

China

Low an

d midd

le

incom

e

Indo

nesia

Thail

and

Figure 2.3. Exports and Imports as a Share of GDP inBangladesh and Comparator Countries, 2001

Bangladesh’s Investment Climate in International Perspective 13

considerably lower than foreign direct investment inmost East Asian countries (figure 2.6).

Serious Deficiencies in InfrastructureIn infrastructure, a critical feature of a country’sinvestment climate, the quality of services appears tobe relatively poor in Bangladesh. Business executivessurveyed for Global Competitiveness Report 2001/02ranked Bangladesh lower on this trait than all otherdeveloping countries in East and South Asia (WorldEconomic Forum 2002). The executives were asked torate the infrastructure quality in their country on ascale of 1 (“poorly developed and inefficient”) to 7(“among the best in the world”). Of the 75 developingand industrial countries in the sample, Bangladeshranked 74th, higher only than Bolivia (figure 2.7). Bycontrast, Malaysia ranked 20th, Thailand 30th, China61st, and India 66th.

Evidence from the firm-level investment climatesurveys confirms that the quality of infrastructureservices is a significant problem in Bangladesh, withelectricity the biggest concern. Asked to rate the extentto which telecommunications, electricity, and transport

Figure 2.6. Net Incoming Foreign Direct Investment as a Share of GDP in Bangladesh and Comparator Countries, 2001

Bangladesh

Indonesia

Pakistan IndiaLow

income

Sri Lanka

Malaysia

Philippines

ChinaThailand

Low & middle income

–4

–3

–2

–1

0

1

2

3

4

Source: World Bank estimates.

Percent

Figure 2.6. Net Incoming Foreign Direct Investment as aShare of GDP in Bangladesh and Comparator Countries,2001

Figure 2.5. Rankings of Bangladesh and Comparator Countries by the Extent of Irregular Payments for Import and Export Permits

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75

Bangladesh

China

Malaysia

India

Thailand

Sri Lanka

Philippines

Indonesia

Source: World Economic Forum 2002.

Strongest Weakest

Figure 2.5. Rankings of Bangladesh andComparator Countries by the Extent ofIrregular Payments for Import and ExportPermits

Bangladesh’s Investment Climate in International Perspective 14

hampered enterprise operations and growth in theircountry, only 4 percent of enterprises in Bangladeshreported that electricity posed no obstacle (figure 2.8).Electricity was a smaller concern in China, where 37percent of enterprises reported that it was no obstacle,and in Pakistan, where 21 percent considered it noobstacle. Enterprises in Bangladesh rated services in

other infrastructure sectors higher, with transport posingno obstacle for 19 percent and telecommunications noobstacle for 30 percent. Still, these shares wereconsiderably smaller than those in China and Pakistan.

Although these responses suggest that the poorquality of infrastructure is a serious problem forenterprises in Bangladesh, the data are qualitative,

Figure 2.8. Share of Firms in Bangladesh and Comparator Countries Reporting That Infrastructure Is No Obstacle to Business Operations

30

4752

19

44 47

4

37

21

0

10

20

30

40

50

60

Bangladesh China Pakistan

Telecommunications Transport Electricity

Source: Investment climate surveys.

Percent

Figure 2.8. Share of Firms in Bangladesh andComparator Countries Reporting That Infrastructure IsNo Obstacle to Business Operations

Figure 2.7. Rankings of Bangladesh and Comparator Countries by Overall Quality of Infrastructure

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75

Bangladesh

Malaysia

Thailand

Indonesia

China

Sri Lanka

India

Philippines

Vietnam

Source: World Economic Forum 2002.

Strongest Weakest

Figure 2.7. Ranking of Bangladesh and ComparatorCountries by Overall Quality of Infrastructure

Bangladesh’s Investment Climate in International Perspective 15

and methodological issues make it difficult to drawstrong conclusions. For example, technologicallyadvanced enterprises might be more vulnerable toinfrastructure problems than less advanced ones,making them more likely to rate infrastructure as asignificant problem. Thus the average score in acountry depends on both the quality of infrastructureand the average level of technological advancement,making cross-country comparisons difficult. Thefollowing sections therefore explore severalquantitative measures of infrastructure developmentin addition to the qualitative measures.

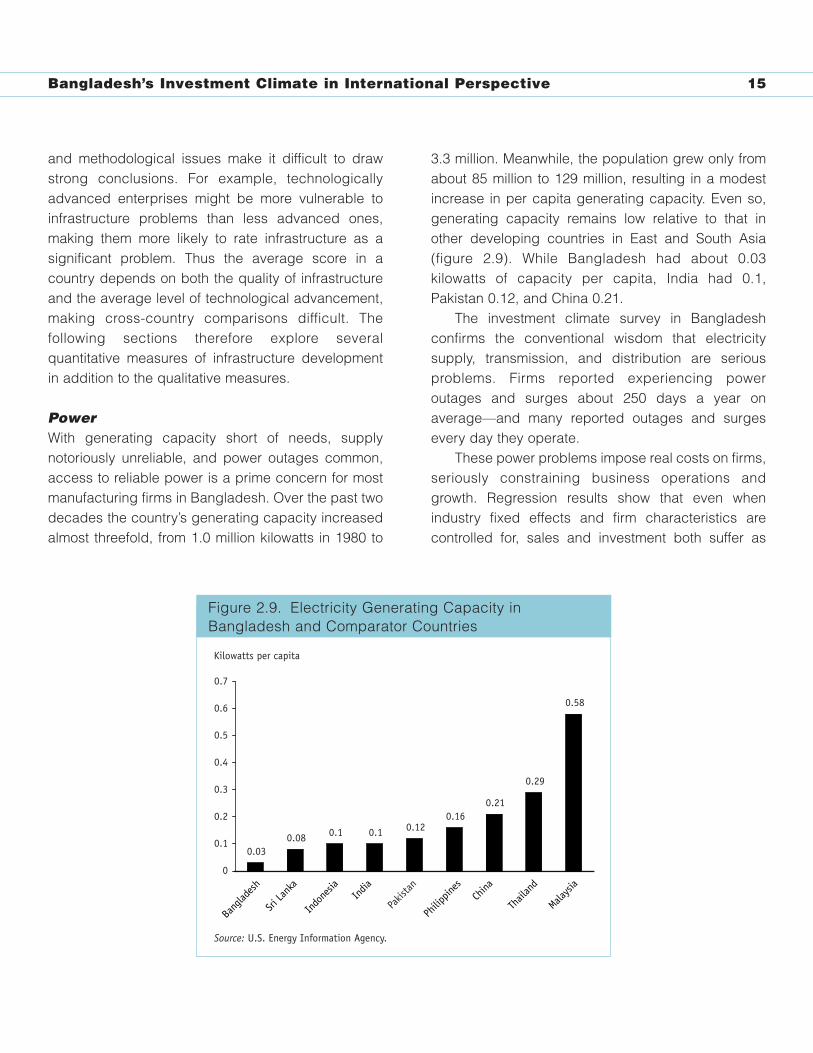

PowerWith generating capacity short of needs, supplynotoriously unreliable, and power outages common,access to reliable power is a prime concern for mostmanufacturing firms in Bangladesh. Over the past twodecades the country’s generating capacity increasedalmost threefold, from 1.0 million kilowatts in 1980 to

3.3 million. Meanwhile, the population grew only fromabout 85 million to 129 million, resulting in a modestincrease in per capita generating capacity. Even so,generating capacity remains low relative to that inother developing countries in East and South Asia(figure 2.9). While Bangladesh had about 0.03kilowatts of capacity per capita, India had 0.1,Pakistan 0.12, and China 0.21.

The investment climate survey in Bangladeshconfirms the conventional wisdom that electricitysupply, transmission, and distribution are seriousproblems. Firms reported experiencing poweroutages and surges about 250 days a year onaverage—and many reported outages and surgesevery day they operate.

These power problems impose real costs on firms,seriously constraining business operations andgrowth. Regression results show that even whenindustry fixed effects and firm characteristics arecontrolled for, sales and investment both suffer as

Figure 2.9. Electricity Generating Capacity in Bangladesh and Comparator Countries

0.030.08 0.1 0.1 0.12

0.160.21

0.29

0.58

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Source: U.S. Energy Information Agency.

Kilowatts per capita

Bang

lades

h

Malaysia

Thail

and

Indo

nesia

China

Sri La

nka

India

Philip

pines

Pakis

tan

Figure 2.9. Electricity Generating Capacity inBangladesh and Comparator Countries

Bangladesh’s Investment Climate in International Perspective 16

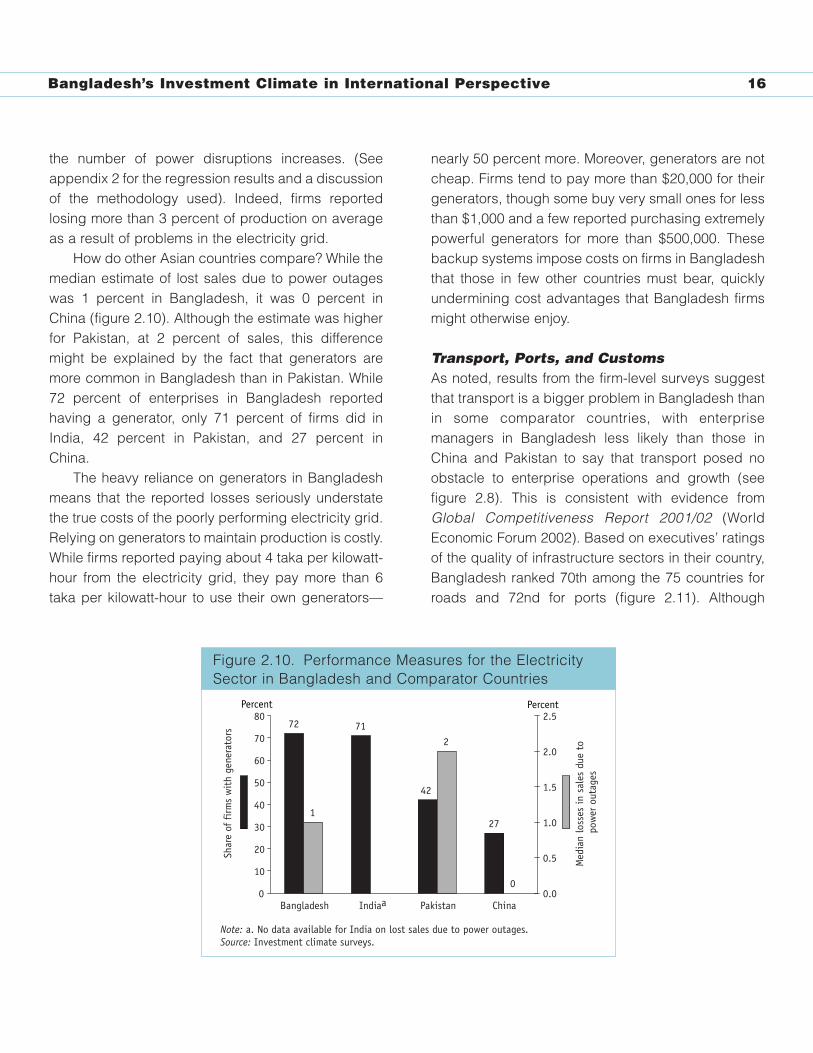

the number of power disruptions increases. (Seeappendix 2 for the regression results and a discussionof the methodology used). Indeed, firms reportedlosing more than 3 percent of production on averageas a result of problems in the electricity grid.

How do other Asian countries compare? While themedian estimate of lost sales due to power outageswas 1 percent in Bangladesh, it was 0 percent inChina (figure 2.10). Although the estimate was higherfor Pakistan, at 2 percent of sales, this differencemight be explained by the fact that generators aremore common in Bangladesh than in Pakistan. While72 percent of enterprises in Bangladesh reportedhaving a generator, only 71 percent of firms did inIndia, 42 percent in Pakistan, and 27 percent inChina.

The heavy reliance on generators in Bangladeshmeans that the reported losses seriously understatethe true costs of the poorly performing electricity grid.Relying on generators to maintain production is costly.While firms reported paying about 4 taka per kilowatt-hour from the electricity grid, they pay more than 6taka per kilowatt-hour to use their own generators—

nearly 50 percent more. Moreover, generators are notcheap. Firms tend to pay more than $20,000 for theirgenerators, though some buy very small ones for lessthan $1,000 and a few reported purchasing extremelypowerful generators for more than $500,000. Thesebackup systems impose costs on firms in Bangladeshthat those in few other countries must bear, quicklyundermining cost advantages that Bangladesh firmsmight otherwise enjoy.

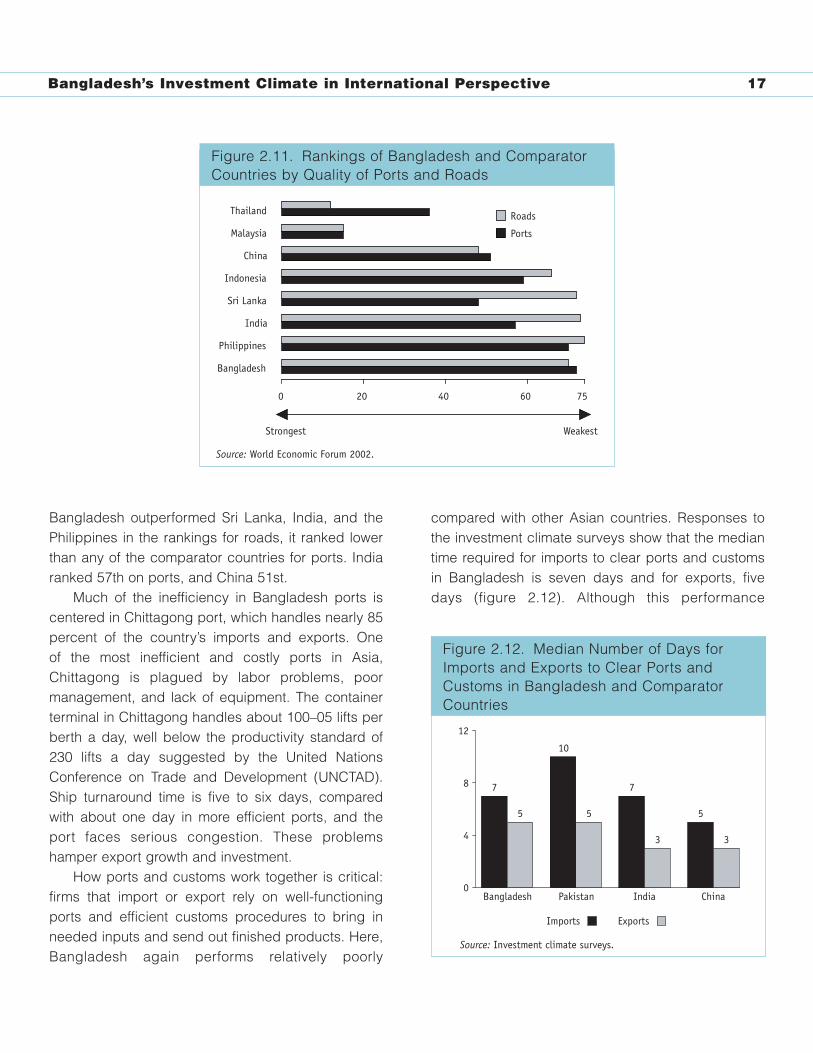

Transport, Ports, and CustomsAs noted, results from the firm-level surveys suggestthat transport is a bigger problem in Bangladesh thanin some comparator countries, with enterprisemanagers in Bangladesh less likely than those inChina and Pakistan to say that transport posed noobstacle to enterprise operations and growth (seefigure 2.8). This is consistent with evidence fromGlobal Competitiveness Report 2001/02 (WorldEconomic Forum 2002). Based on executives’ ratingsof the quality of infrastructure sectors in their country,Bangladesh ranked 70th among the 75 countries forroads and 72nd for ports (figure 2.11). Although

Figure 2.10. Performance Measures for the Electricity Sector in Bangladesh and Comparator Countries

72 71

42

271

2

00

10

20

30

40

50

60

70

80

Bangladesh Indiaa Pakistan China

Shar

e of

fir

ms

wit

h ge

nera

tors

0.0

0.5

1.0

1.5

2.0

2.5

Med

ian

loss

es in

sal

es d

ue t

o po

wer

out

ages

Note: a. No data available for India on lost sales due to power outages.Source: Investment climate surveys.

Percent Percent

Figure 2.10. Performance Measures for the ElectricitySector in Bangladesh and Comparator Countries

Bangladesh’s Investment Climate in International Perspective 17

Bangladesh outperformed Sri Lanka, India, and thePhilippines in the rankings for roads, it ranked lowerthan any of the comparator countries for ports. Indiaranked 57th on ports, and China 51st.

Much of the inefficiency in Bangladesh ports iscentered in Chittagong port, which handles nearly 85percent of the country’s imports and exports. One of the most inefficient and costly ports in Asia,Chittagong is plagued by labor problems, poormanagement, and lack of equipment. The containerterminal in Chittagong handles about 100–05 lifts perberth a day, well below the productivity standard of230 lifts a day suggested by the United NationsConference on Trade and Development (UNCTAD).Ship turnaround time is five to six days, comparedwith about one day in more efficient ports, and theport faces serious congestion. These problemshamper export growth and investment.

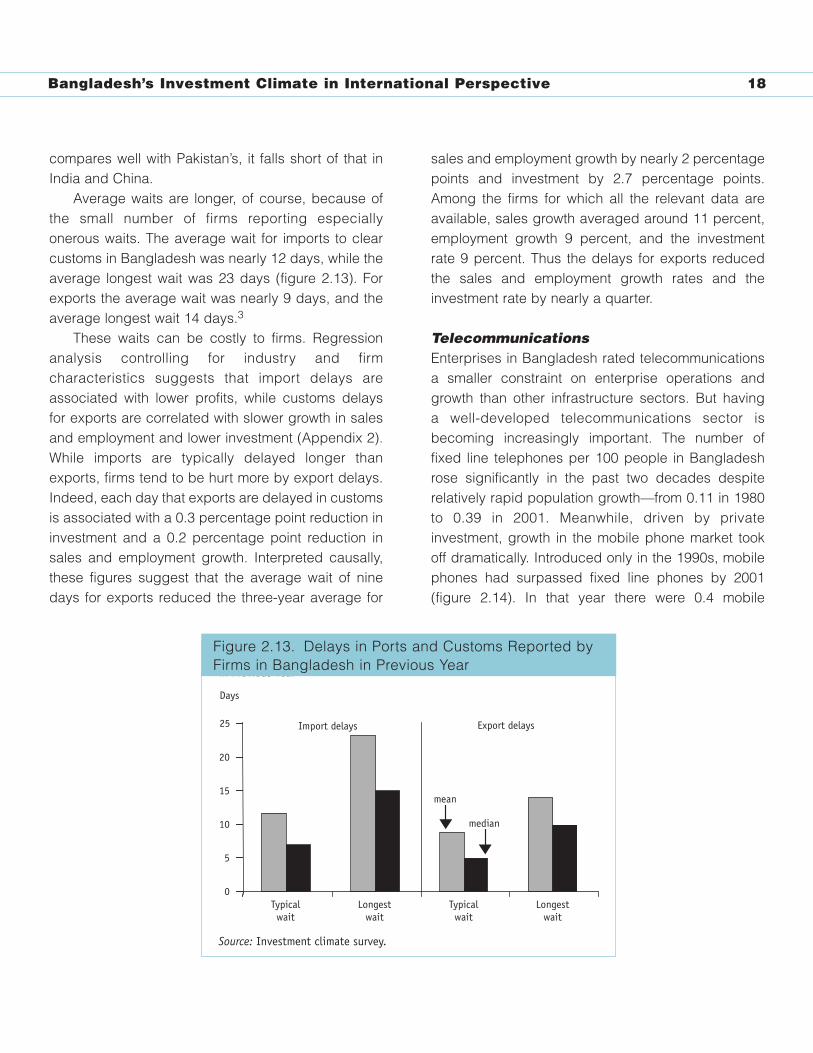

How ports and customs work together is critical:firms that import or export rely on well-functioningports and efficient customs procedures to bring inneeded inputs and send out finished products. Here,Bangladesh again performs relatively poorly

compared with other Asian countries. Responses tothe investment climate surveys show that the mediantime required for imports to clear ports and customsin Bangladesh is seven days and for exports, fivedays (figure 2.12). Although this performance

Figure 2.12. Median Number of Days for Imports and Exports to Clear Ports and Customs in Bangladesh and Comparator Countries

7

5

10

5

7

3

5

3

0

4

8

12

Bangladesh Pakistan India China

Source: Investment climate surveys.

Imports Exports

Figure 2.12. Median Number of Days forImports and Exports to Clear Ports andCustoms in Bangladesh and ComparatorCountries

Figure 2.11. Rankings of Bangladesh and Comparator Countries by Quality of Ports and Roads

0 20 40 60 75

Bangladesh

Thailand

Malaysia

China

Indonesia

Sri Lanka

India

Philippines

Roads

Ports

Source: World Economic Forum 2002.

Strongest Weakest

Figure 2.11. Rankings of Bangladesh and ComparatorCountries by Quality of Ports and Roads

Bangladesh’s Investment Climate in International Perspective 18

compares well with Pakistan’s, it falls short of that inIndia and China.

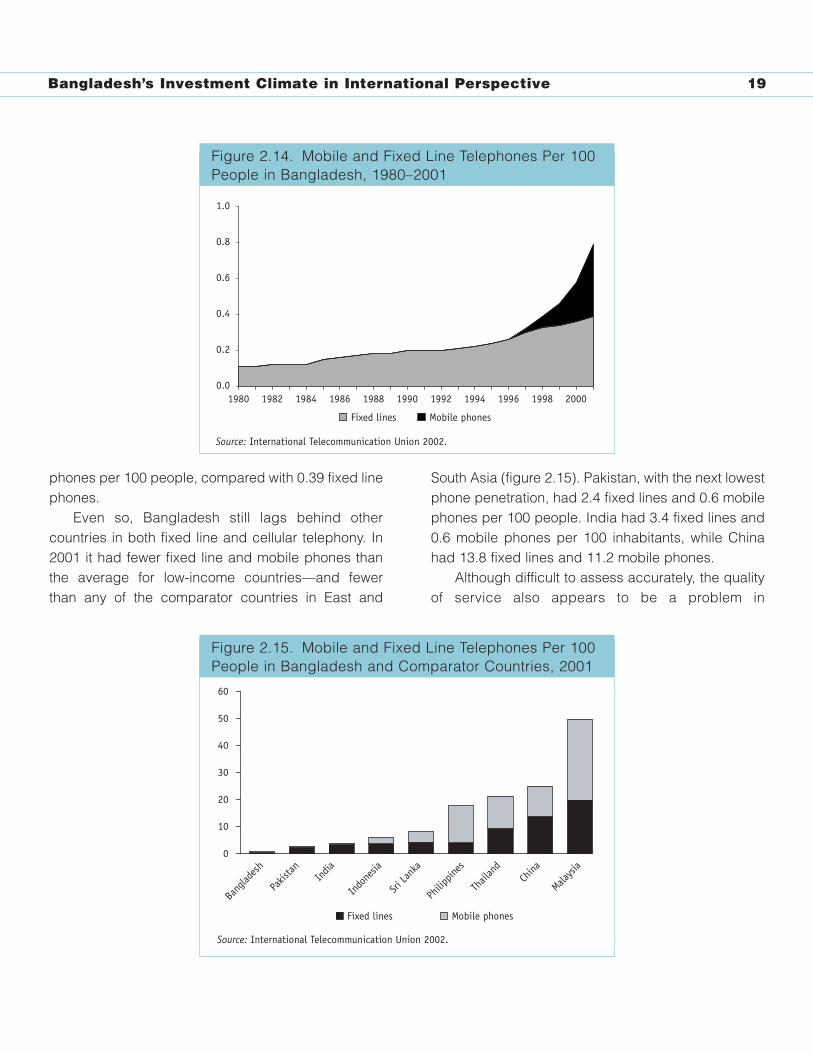

Average waits are longer, of course, because ofthe small number of firms reporting especiallyonerous waits. The average wait for imports to clearcustoms in Bangladesh was nearly 12 days, while theaverage longest wait was 23 days (figure 2.13). Forexports the average wait was nearly 9 days, and theaverage longest wait 14 days.3

These waits can be costly to firms. Regressionanalysis controlling for industry and firmcharacteristics suggests that import delays areassociated with lower profits, while customs delaysfor exports are correlated with slower growth in salesand employment and lower investment (Appendix 2).While imports are typically delayed longer thanexports, firms tend to be hurt more by export delays.Indeed, each day that exports are delayed in customsis associated with a 0.3 percentage point reduction ininvestment and a 0.2 percentage point reduction insales and employment growth. Interpreted causally,these figures suggest that the average wait of ninedays for exports reduced the three-year average for

sales and employment growth by nearly 2 percentagepoints and investment by 2.7 percentage points.Among the firms for which all the relevant data areavailable, sales growth averaged around 11 percent,employment growth 9 percent, and the investmentrate 9 percent. Thus the delays for exports reducedthe sales and employment growth rates and theinvestment rate by nearly a quarter.

TelecommunicationsEnterprises in Bangladesh rated telecommunicationsa smaller constraint on enterprise operations andgrowth than other infrastructure sectors. But having a well-developed telecommunications sector isbecoming increasingly important. The number offixed line telephones per 100 people in Bangladeshrose significantly in the past two decades despiterelatively rapid population growth—from 0.11 in 1980to 0.39 in 2001. Meanwhile, driven by privateinvestment, growth in the mobile phone market tookoff dramatically. Introduced only in the 1990s, mobilephones had surpassed fixed line phones by 2001(figure 2.14). In that year there were 0.4 mobile

Figure 2.13. Delays in Ports and Customs Reported by Firms in Bangladesh in Previous Year

0

5

10

15

20

Typicalwait

Longestwait

Typicalwait

Longestwait

Import delays Export delays

mean

median

Days

25

Source: Investment climate survey.

Figure 2.13. Delays in Ports and Customs Reported byFirms in Bangladesh in Previous Year

Bangladesh’s Investment Climate in International Perspective 19

phones per 100 people, compared with 0.39 fixed linephones.

Even so, Bangladesh still lags behind othercountries in both fixed line and cellular telephony. In2001 it had fewer fixed line and mobile phones thanthe average for low-income countries—and fewerthan any of the comparator countries in East and

South Asia (figure 2.15). Pakistan, with the next lowestphone penetration, had 2.4 fixed lines and 0.6 mobilephones per 100 people. India had 3.4 fixed lines and0.6 mobile phones per 100 inhabitants, while Chinahad 13.8 fixed lines and 11.2 mobile phones.

Although difficult to assess accurately, the qualityof service also appears to be a problem in

Figure 2.15. Mobile and Fixed Line Telephones Per 100 People in Bangladesh and Comparator Countries, 2001

0

10

20

30

40

50

60

Bang

lades

h

Pakis

tan India

Indo

nesia

Sri La

nka

Philip

pines

Thail

and

China

Malaysia

Fixed lines Mobile phones

Source: International Telecommunication Union 2002.

Figure 2.15. Mobile and Fixed Line Telephones Per 100People in Bangladesh and Comparator Countries, 2001

Figure 2.14. Mobile and Fixed Line Telephones Per 100 People in Bangladesh, 1980–2001

0.0

0.2

0.4

0.6

0.8

1.0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Fixed lines Mobile phones

Source: International Telecommunication Union 2002.

Figure 2.14. Mobile and Fixed Line Telephones Per 100People in Bangladesh, 1980–2001

Bangladesh’s Investment Climate in International Perspective 20

Bangladesh. In the most recent year for which dataare available, Bangladesh had 208 faults for every100 mainlines, according to the InternationalTelecommunication Union. In comparison, there were203 faults per 100 mainlines in India, 99 in Pakistan,38 in Malaysia, 29 in the Philippines, 15 in Sri Lanka,and 13 in Indonesia.

Getting a telephone connection also appears to berelatively difficult in Bangladesh. In the investmentclimate surveys, enterprises obtaining a telephoneconnection within the previous two years reported amedian wait of 90 days in Bangladesh, far longer thanthe 18 days in Pakistan and 7 days in China (figure 2.16).

Governance ProblemsHow does Bangladesh fare in comparisons ofgovernance across countries? Making suchcomparisons is not easy—because it is difficult to findquantitative measures of such aspects as the quality of government regulation and the cost imposed bycorruption. But analyses based on aggregate statisticssuggest a mixed performance in Bangladesh.

Governance Quality To assess governance in Bangladesh relative to that incomparator countries, six aggregate measures wereused that capture different aspects of governance,including regulation and corruption. Developed byKaufmann, Kraay, and Zoido-Lobatón (1999, 2002),these measures combine information on up to 60 (mostlysubjective) indicators from other sources.4 The sixindexes measure perceptions about:

• Voice and accountability—the extent to whichcitizens of the country are able to participate inthe selection of government.

• Political stability—the likelihood that thegovernment will be destabilized or overthrown bypossibly unconstitutional or violent means,including terrorism.

• Government effectiveness—the quality of publicservice provision and the governmentbureaucracy, the competence and independenceof the civil service, and the credibility of thegovernment’s commitment to adhering to

Figure 2.16. Median Wait for Fixed Line Telephone Connection in Bangladesh and Comparator Countries

90

18

7

0

10

20

30

40

50

60

70

80

90

100

Bangladesh Pakistan China

Note: Data refer only to firms receiving a fixed line connection within the two years before the survey. Source: Investment climate surveys.

Days

Figure 2.16. Median Wait for Fixed Line TelephoneConnection in Bangladesh and Comparator Countries

Bangladesh’s Investment Climate in International Perspective 21

announced policies. This measure focuses mainlyon “inputs” that governments need to implementgood policies and deliver public goods.

• Regulatory quality—the quality of governmentpolicies. This measure, based on “outputs” ratherthan “inputs,” focuses on the prevalence ofmarket-unfriendly policies (such as price controlsor inadequate bank supervision) as well asperceptions about the burden imposed onbusinesses by regulation.

• Rule of law—the extent to which individuals haveconfidence in and abide by the rules of society.This includes perceptions about the incidence ofcrime (violent and nonviolent), the effectivenessand predictability of the judiciary, and theenforceability of contracts.

• Control of corruption—the extent of corruption(that is, the illegal use of public power for privategain).

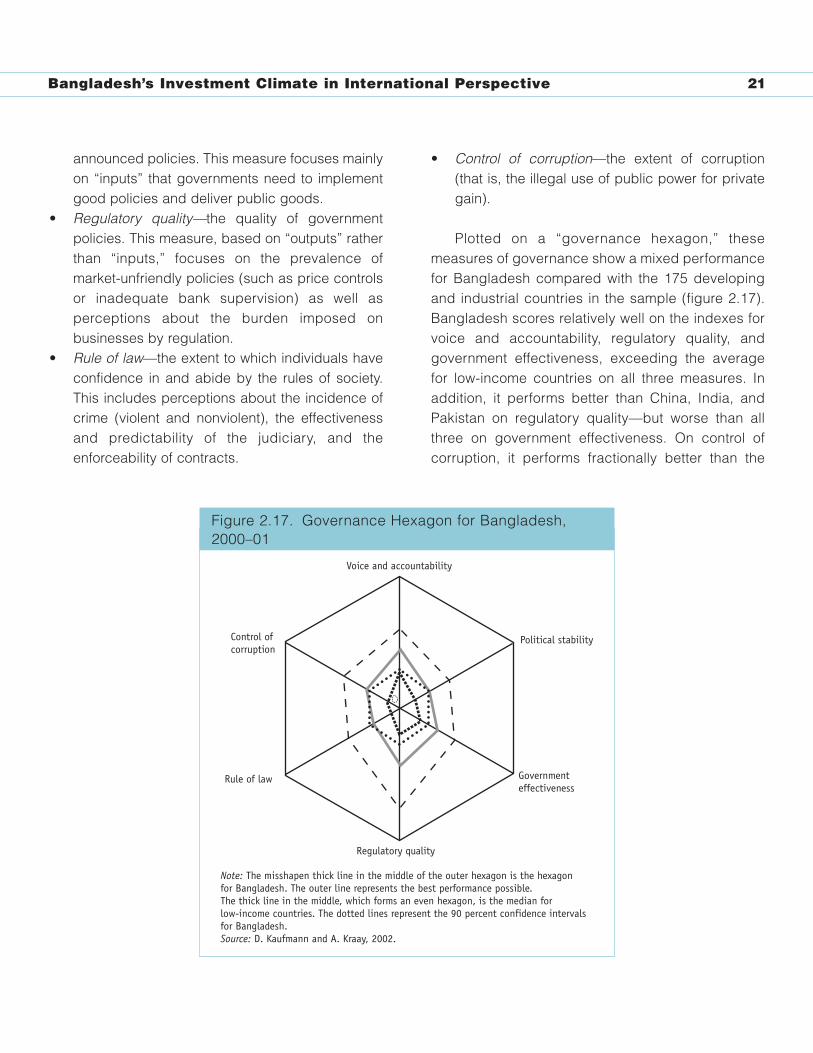

Plotted on a “governance hexagon,” thesemeasures of governance show a mixed performancefor Bangladesh compared with the 175 developingand industrial countries in the sample (figure 2.17).Bangladesh scores relatively well on the indexes forvoice and accountability, regulatory quality, andgovernment effectiveness, exceeding the averagefor low-income countries on all three measures. Inaddition, it performs better than China, India, andPakistan on regulatory quality—but worse than allthree on government effectiveness. On control ofcorruption, it performs fractionally better than the

Figure 2.17. Governance Hexagon for Bangladesh, 2000–01

Note: The misshapen thick line in the middle of the outer hexagon is the hexagon for Bangladesh. The outer line represents the best performance possible. The thick line in the middle, which forms an even hexagon, is the median for low-income countries. The dotted lines represent the 90 percent confidence intervals for Bangladesh.Source: D. Kaufmann and A. Kraay, 2002.

Voice and accountability

Control of corruption

Rule of law

Regulatory quality

Government effectiveness

Political stability

Figure 2.17. Governance Hexagon for Bangladesh,2000–01

Bangladesh’s Investment Climate in International Perspective 22

average for low-income countries but worse thaneither China or India. And on both political stabilityand rule of law, Bangladesh performs worse than theaverage for low-income countries and worse thanChina, India, and Pakistan.

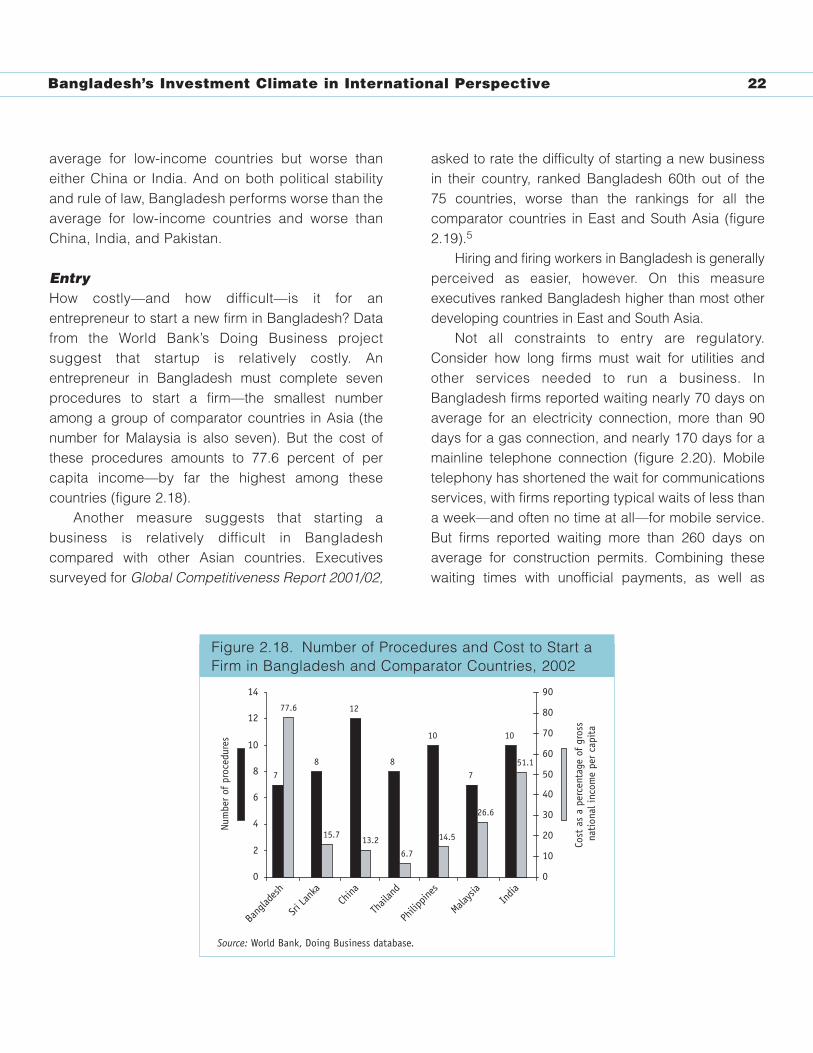

EntryHow costly—and how difficult—is it for anentrepreneur to start a new firm in Bangladesh? Datafrom the World Bank’s Doing Business projectsuggest that startup is relatively costly. Anentrepreneur in Bangladesh must complete sevenprocedures to start a firm—the smallest numberamong a group of comparator countries in Asia (thenumber for Malaysia is also seven). But the cost ofthese procedures amounts to 77.6 percent of percapita income—by far the highest among thesecountries (figure 2.18).

Another measure suggests that starting abusiness is relatively difficult in Bangladeshcompared with other Asian countries. Executivessurveyed for Global Competitiveness Report 2001/02,

asked to rate the difficulty of starting a new businessin their country, ranked Bangladesh 60th out of the 75 countries, worse than the rankings for all thecomparator countries in East and South Asia (figure2.19).5

Hiring and firing workers in Bangladesh is generallyperceived as easier, however. On this measureexecutives ranked Bangladesh higher than most otherdeveloping countries in East and South Asia.

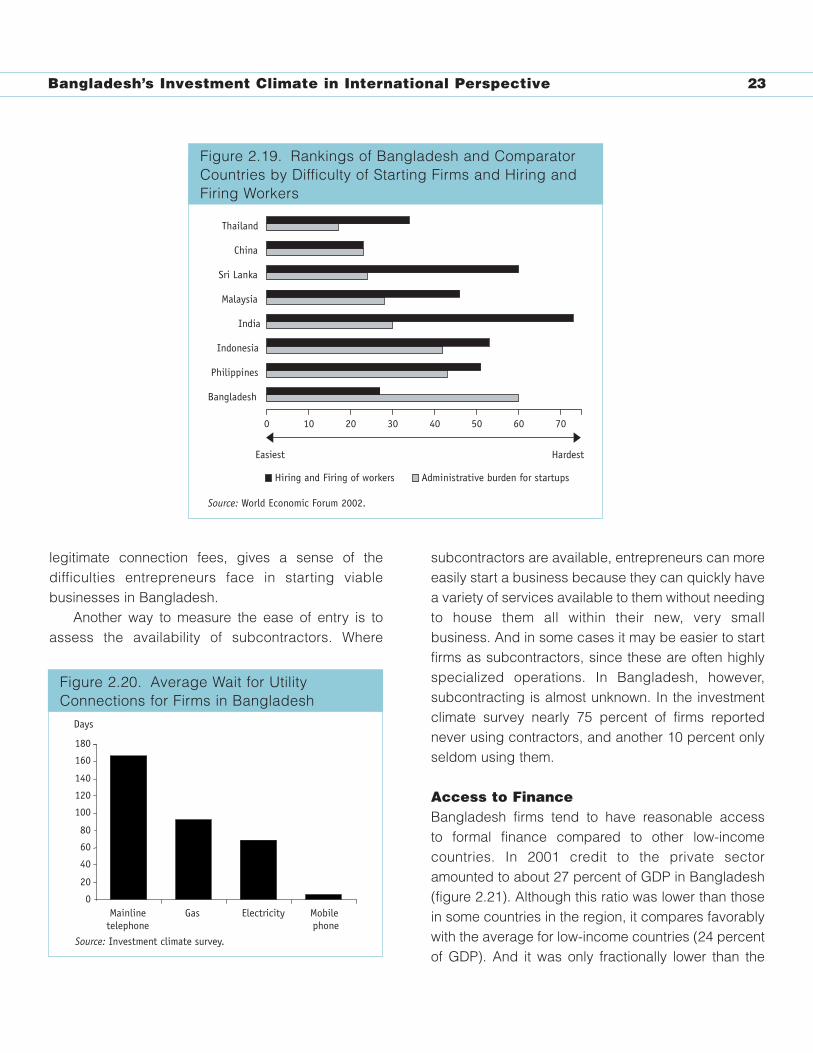

Not all constraints to entry are regulatory.Consider how long firms must wait for utilities andother services needed to run a business. InBangladesh firms reported waiting nearly 70 days onaverage for an electricity connection, more than 90days for a gas connection, and nearly 170 days for amainline telephone connection (figure 2.20). Mobiletelephony has shortened the wait for communicationsservices, with firms reporting typical waits of less thana week—and often no time at all—for mobile service.But firms reported waiting more than 260 days onaverage for construction permits. Combining thesewaiting times with unofficial payments, as well as

Figure 2.18. Number of Procedures and Cost to Start a Firm in Bangladesh and Comparator Countries, 2002

Bang

lades

h

Sri La

nka

China

Thail

and

Philip

pines

Malaysia

India

Num

ber

of p

roce

dure

s

Cost

as

a pe

rcen

tage

of

gros

s na

tion

al in

com

e pe

r ca

pita

Source: World Bank, Doing Business database.

78

12

8

10

7

10

77.6

15.713.2

6.7

14.5

26.6

51.1

0

2

4

6

8

10

12

14

0

10

20

30

40

50

60

70

80

90

Figure 2.18. Number of Procedures and Cost to Start aFirm in Bangladesh and Comparator Countries, 2002

Bangladesh’s Investment Climate in International Perspective 23

legitimate connection fees, gives a sense of thedifficulties entrepreneurs face in starting viablebusinesses in Bangladesh.

Another way to measure the ease of entry is toassess the availability of subcontractors. Where

subcontractors are available, entrepreneurs can moreeasily start a business because they can quickly havea variety of services available to them without needingto house them all within their new, very smallbusiness. And in some cases it may be easier to startfirms as subcontractors, since these are often highlyspecialized operations. In Bangladesh, however,subcontracting is almost unknown. In the investmentclimate survey nearly 75 percent of firms reportednever using contractors, and another 10 percent onlyseldom using them.

Access to FinanceBangladesh firms tend to have reasonable access to formal finance compared to other low-incomecountries. In 2001 credit to the private sectoramounted to about 27 percent of GDP in Bangladesh(figure 2.21). Although this ratio was lower than thosein some countries in the region, it compares favorablywith the average for low-income countries (24 percentof GDP). And it was only fractionally lower than the

Figure 2.19. Rankings of Bangladesh and Comparator Countries by Difficulty of Starting Firms and Hiring and Firing Workers

0 10 20 30 40 50 60 70

Bangladesh

Thailand

China

Sri Lanka

Malaysia

India

Indonesia

Philippines

Administrative burden for startupsHiring and Firing of workers

Source: World Economic Forum 2002.

Easiest Hardest

Figure 2.19. Rankings of Bangladesh and ComparatorCountries by Difficulty of Starting Firms and Hiring andFiring Workers

Figure 2.20. Average Wait for Utility Connections for Firms in Bangladesh

0

20

40

60

80

100

120

140

160

180

Mainlinetelephone

Gas Electricity Mobile phone

Days

Source: Investment climate survey.

Figure 2.20. Average Wait for UtilityConnections for Firms in Bangladesh

Bangladesh’s Investment Climate in International Perspective 24

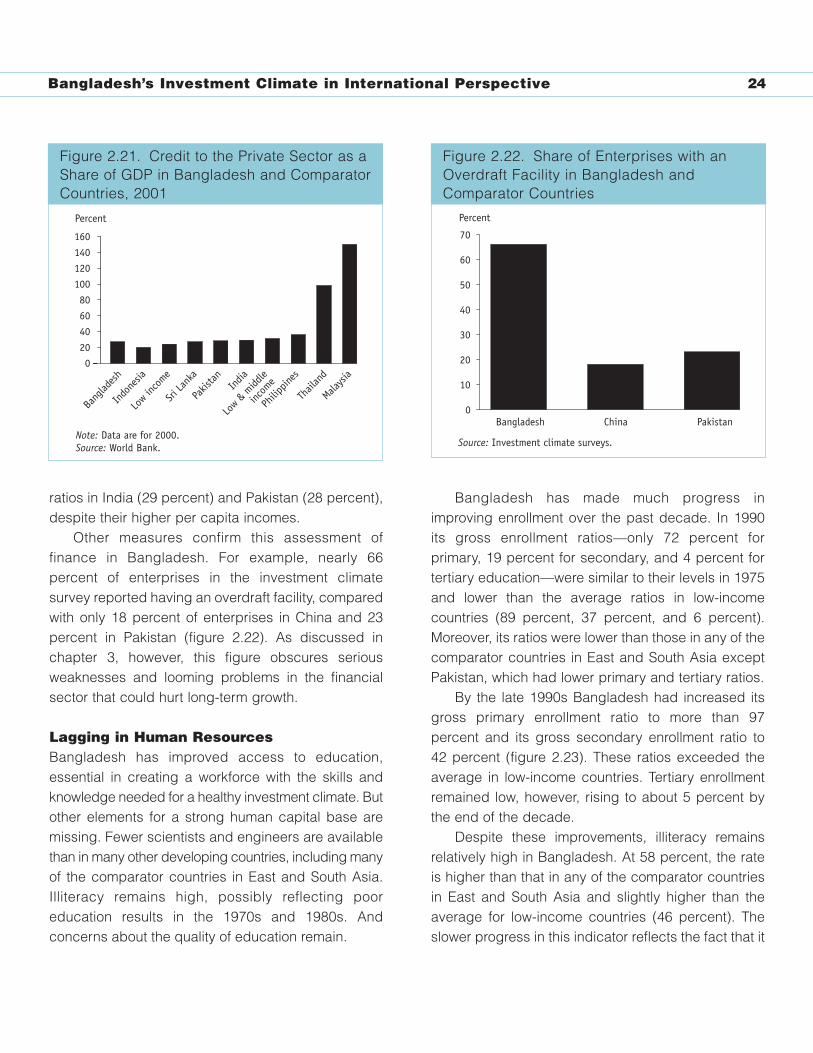

ratios in India (29 percent) and Pakistan (28 percent),despite their higher per capita incomes.

Other measures confirm this assessment offinance in Bangladesh. For example, nearly 66percent of enterprises in the investment climatesurvey reported having an overdraft facility, comparedwith only 18 percent of enterprises in China and 23percent in Pakistan (figure 2.22). As discussed inchapter 3, however, this figure obscures seriousweaknesses and looming problems in the financialsector that could hurt long-term growth.

Lagging in Human Resources Bangladesh has improved access to education,essential in creating a workforce with the skills andknowledge needed for a healthy investment climate. Butother elements for a strong human capital base aremissing. Fewer scientists and engineers are availablethan in many other developing countries, including manyof the comparator countries in East and South Asia.Illiteracy remains high, possibly reflecting pooreducation results in the 1970s and 1980s. Andconcerns about the quality of education remain.

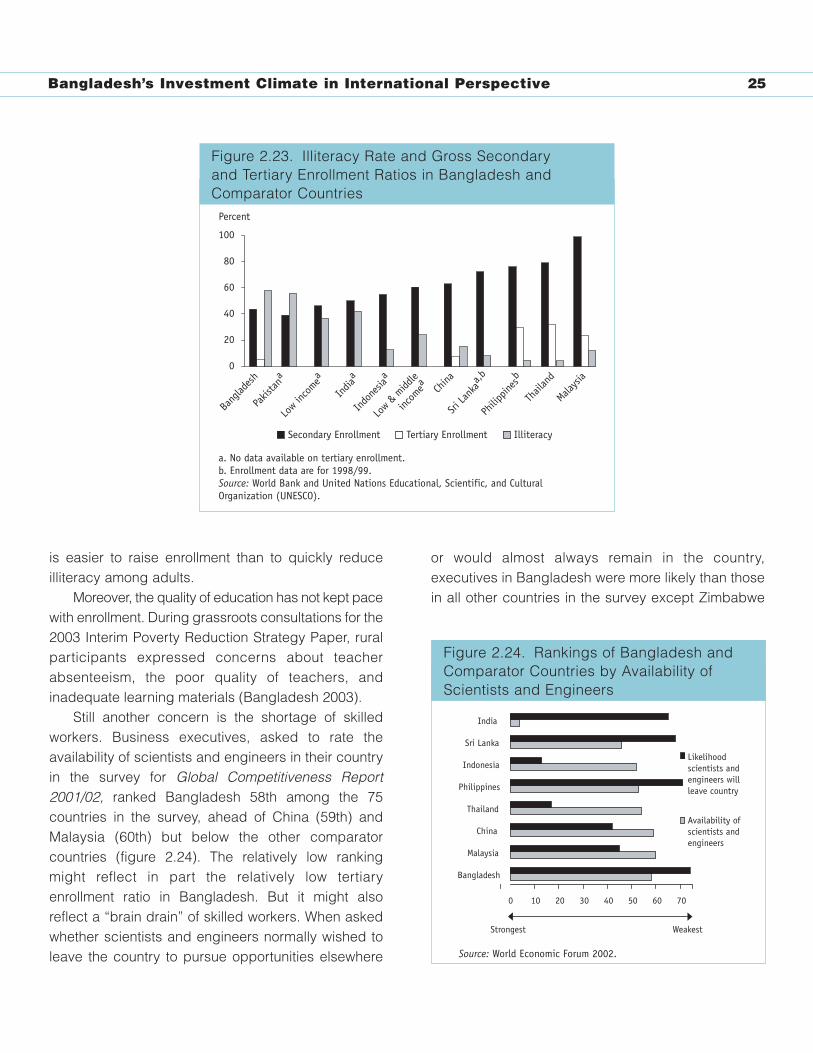

Bangladesh has made much progress inimproving enrollment over the past decade. In 1990its gross enrollment ratios—only 72 percent forprimary, 19 percent for secondary, and 4 percent fortertiary education—were similar to their levels in 1975and lower than the average ratios in low-incomecountries (89 percent, 37 percent, and 6 percent).Moreover, its ratios were lower than those in any of thecomparator countries in East and South Asia exceptPakistan, which had lower primary and tertiary ratios.

By the late 1990s Bangladesh had increased itsgross primary enrollment ratio to more than 97percent and its gross secondary enrollment ratio to 42 percent (figure 2.23). These ratios exceeded theaverage in low-income countries. Tertiary enrollmentremained low, however, rising to about 5 percent bythe end of the decade.

Despite these improvements, illiteracy remainsrelatively high in Bangladesh. At 58 percent, the rateis higher than that in any of the comparator countriesin East and South Asia and slightly higher than theaverage for low-income countries (46 percent). Theslower progress in this indicator reflects the fact that it

Figure 2.22. Share of Enterprises with an Overdraft Facility in Bangladesh and Comparator Countries

0

10

20

30

40

50

60

70

Bangladesh China Pakistan

Source: Investment climate surveys.

Percent

Figure 2.22. Share of Enterprises with anOverdraft Facility in Bangladesh andComparator Countries

Figure 2.21. Credit to the Private Sector as a Share of GDP in Bangladesh and Comparator Countries, 2001

0

20

40

60

80

100

120

140

160

Bang

lades

h

Indo

nesia

Low in

come

Sri La

nka

Pakis

tan India

Low &

midd

le

incom

e

Philip

pines

Thail

and

Malaysia

Note: Data are for 2000. Source: World Bank.

Percent

Figure 2.21. Credit to the Private Sector as aShare of GDP in Bangladesh and ComparatorCountries, 2001

Bangladesh’s Investment Climate in International Perspective 25

is easier to raise enrollment than to quickly reduceilliteracy among adults.

Moreover, the quality of education has not kept pacewith enrollment. During grassroots consultations for the2003 Interim Poverty Reduction Strategy Paper, ruralparticipants expressed concerns about teacherabsenteeism, the poor quality of teachers, andinadequate learning materials (Bangladesh 2003).

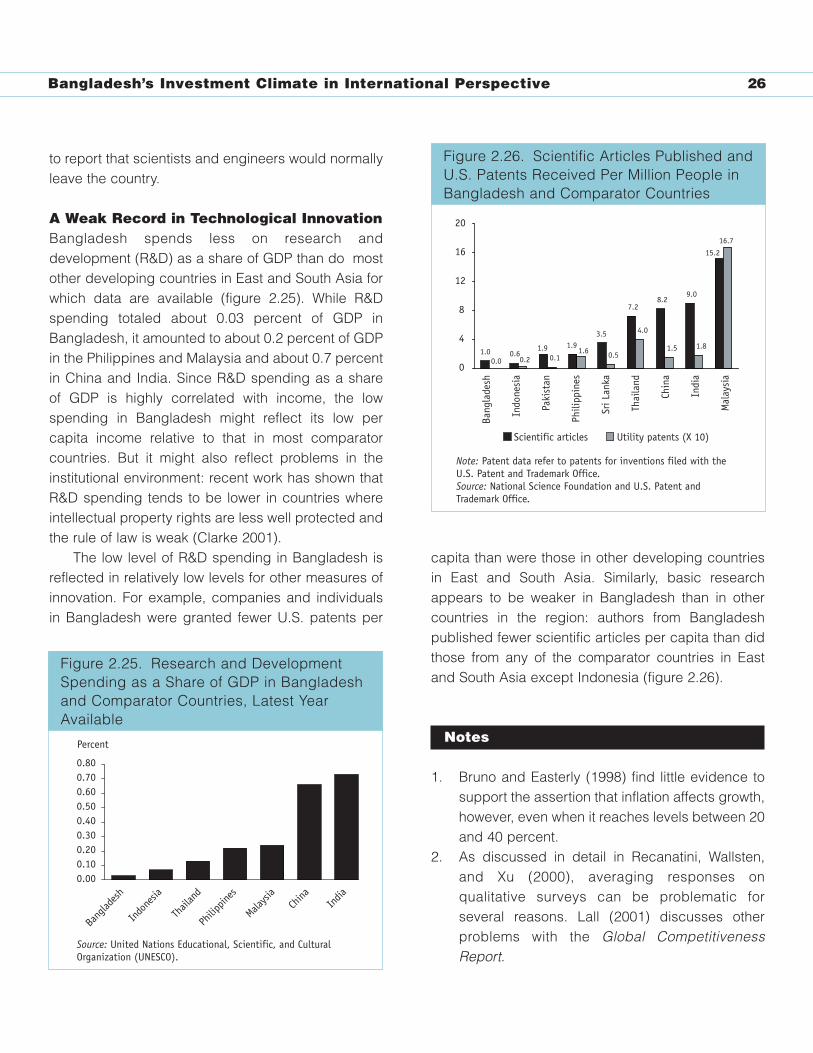

Still another concern is the shortage of skilledworkers. Business executives, asked to rate theavailability of scientists and engineers in their countryin the survey for Global Competitiveness Report2001/02, ranked Bangladesh 58th among the 75countries in the survey, ahead of China (59th) andMalaysia (60th) but below the other comparatorcountries (figure 2.24). The relatively low rankingmight reflect in part the relatively low tertiaryenrollment ratio in Bangladesh. But it might alsoreflect a “brain drain” of skilled workers. When askedwhether scientists and engineers normally wished toleave the country to pursue opportunities elsewhere

or would almost always remain in the country,executives in Bangladesh were more likely than thosein all other countries in the survey except Zimbabwe

Figure 2.24. Rankings of Bangladesh and Comparator Countries by Availability of Scientists and Engineers

0 10 20 30 40 50 60 70

Bangladesh

India