pierre-olivier gourinchas, thomas philippon, dimitri

TRANSCRIPT

Pierre-Olivier Gourinchas, Thomas Philippon, Dimitri Vayanos

The analytics of Greek crisis Article (Published version) (Refereed)

Original citation: Gourinchas, Pierre-Olivier and Philippon, Thomas and Vayanos, Dimitri (2017) The analytics of the Greek crisis. NBER Macroeconomics Annual, 31 (1). pp. 1-81. ISSN 0889-3365 DOI: 10.1086/690239 © 2017 by the National Bureau of Economic Research This version available at: http://eprints.lse.ac.uk/82433/ Available in LSE Research Online: June 2017 LSE has developed LSE Research Online so that users may access research output of the School. Copyright © and Moral Rights for the papers on this site are retained by the individual authors and/or other copyright owners. Users may download and/or print one copy of any article(s) in LSE Research Online to facilitate their private study or for non-commercial research. You may not engage in further distribution of the material or use it for any profit-making activities or any commercial gain. You may freely distribute the URL (http://eprints.lse.ac.uk) of the LSE Research Online website.

© 2017 by the National Bureau of Economic Research. All rights reserved.978- 0- 226- 39560- 9/2017/2017- 0101$10.00

1

The Analytics of the Greek Crisis

Pierre- Olivier Gourinchas, UC Berkeley, NBER, and CEPR

Thomas Philippon, NYU Stern and NBER

Dimitri Vayanos, London School of Economics, NBER, and CEPR

Gourinchas, Philippon, and Vayanos

I. Introduction and Motivation

The economic crisis that Greece has been experiencing from 2008 on-ward has been particularly severe. Real gross domestic product (GDP) per capita stood at approximately €22,600 in 2008, and dropped to €17,000 by 2014, a decline of 24.8%.1 The unemployment rate was 7.8% in 2008, and rose to 26.6% in 2014. The entire Greek banking system became insolvent during the crisis, and a large- scale recapitalization took place in 2013. In 2012, Greece became the first Organisation for Economic Co- operation and Development (OECD) member country to default on its sovereign debt, and that default was the largest in world history. Greece received financial assistance from other Eurozone (EZ) countries and the International Monetary Fund (IMF), and the size of this bailout package was also the largest in history.

The implications of the Greek crisis extended well beyond Greece. The bailout package that Greece received was large partly because of fears of contagion to other countries in the EZ and to their banking sys-tems. Moreover, at various stages during the crisis, the continued mem-bership of Greece in the EZ was put in doubt. This tested the strength and the limits of the currency union, and of the European project more generally.

This paper provides an “interim” report on the Greek crisis (“interim” in the sense that the crisis is still unfolding). We proceed in three steps. First, we describe the main macroeconomic dynamics that Greece experi-enced before and during the crisis. Second, we put these dynamics in per-spective by benchmarking the Greek crisis against all episodes of sudden stops, sovereign debt crises, and lending boom/busts in emerging and

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

2 Gourinchas, Philippon, and Vayanos

advanced economies since 1980. Third, we develop a dynamic stochas-tic general equilibrium (DSGE) model designed to capture many of the relevant features of the Greek crisis and help us identify its main drivers.

The global financial crisis that began in 2007 in the United States hit Greece through three interlinked shocks. The first shock was a sovereign debt crisis: investors began to perceive the debt of the Greek government as unsustainable, and were no longer willing to finance the government deficit. The second shock was a banking crisis: Greek banks had diffi-culty financing themselves in the interbank market, and their solvency was put in doubt because of projected losses to the value of their assets. The third shock was a sudden stop: foreign investors were no longer will-ing to lend to Greece as a whole (government, banks, and firms), and so the country could not finance its current account deficit.

To many observers, that last shock was a startling development. After all, the very existence of a common currency, and therefore of an auto-matic provision of liquidity against good collateral through its common central bank, was supposed to insulate member countries against a sudden reversal of private capital of the kind experienced routinely by emerging- market (EM) economies. Just like a sudden stop on California or Texas could not happen since Federal Reserve funding would substi-tute instantly and automatically for private capital, the common view was a sudden stop could not happen to Greece or Portugal since Euro-pean Central Bank (ECB) funding would substitute instantly and auto-matically for private capital.2 The belief that sudden stops were a thing of the past may have, in turn, contributed to the emergence of mount-ing internal and external imbalances, in Greece and elsewhere in the EZ (Blanchard and Giavazzi 2002). Yet, at the onset of the crisis, Greece and other EZ members did experience a classic sudden stop. The built- in defense mechanisms of the EZ were activated and the ECB provided much needed funding to the Greek economy. How much, then, did this sudden stop contribute to the subsequent meltdown and through what channels? And what was the contribution of other factors? These are among the questions that we seek to address in this paper.

The first main result that emerges from our macro- benchmarking ex-ercise is that Greece’s drop in output (a 25% decline in real GDP per capita between 2008 and 2013) was significantly more severe and pro-tracted than during the average crisis. This applies to the sample of countries that experienced sudden stops, to the sample that experienced sovereign defaults, to the sample that experienced lending booms and busts, and even to the sample that experienced all three shocks com-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 3

bined (we call these episodes “trifectas”). The collapse in investment (75% decline between 2008 and 2013) was even more severe. Impor-tantly, we find that the difference in output dynamics is not driven by the exchange- rate regime. Countries whose currency remains pegged experience a larger output drop, on average, than countries with float-ing rates. But unlike these countries, whose output rebounds after a few years, Greece’s output continued to drop to a significantly lower level.

One possible explanation for the severity of Greece’s crisis is the high level of debt—government, private, and external—at the onset of the crisis. Greece’s government debt stood at 103.1% of output in 2007, its net foreign assets at –99.9% of output, and its private- sector debt at 92.4% of output. On the former two measures, Greece fared worse than Ireland, Italy, Portugal, and Spain, the four other major EZ countries hit by the crisis. Greece fared worse than those countries also on its govern-ment deficit and current- account deficit, which stood at 6.5% and 15.9% of output, respectively, in 2007. And debt levels in Greece were more than twice as large than the average of the emerging- market economies, which account for most of the crisis episodes in our sample.

To identify the role of debt, as well as of other factors such as the sudden stop of private capital in driving the severity of the Greek cri-sis, we turn to our DSGE model. The model is designed to capture in a simple and stylized manner the three types of shocks that hit Greece. It also captures a rich set of interdependencies between the shocks. The model features a government, two types of consumers, firms, and banks. The government can borrow, raise taxes, spend, and possibly default on its debt. Consumers differ in their subjective discount rate. Impatient consumers are those who borrow in equilibrium, subject to a debt limit. Firms can borrow and invest and face sticky wages and prices. Consumers and firms can borrow from banks and can default on their debts. The rates at which the government, consumers, and firms can borrow depend on the probability with which these entities can default and on the losses given default. In turn, the expected costs of default (probability times losses) depend on the ratio of debt to income.

In the model, a sovereign risk shock increases the government’s fund-ing costs. The government responds by increasing taxes and reducing expenditures, which exerts a contractionary effect on the economy. In turn, the decline in output increases the expected costs of default on private- sector loans, causing funding costs for consumers and firms to rise and investment to drop. Conversely, a sudden stop increases directly the rate at which consumers and firms can borrow, causing in-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

4 Gourinchas, Philippon, and Vayanos

vestment, consumption, and output to decline. The decline in fiscal rev-enues pushes up sovereign yields and has an adverse impact on public debt dynamics. Hence, in our model, sovereign risks and private- sector risks are intertwined and shocks to one sector of the economy can affect funding costs and default rates throughout all sectors.

We estimate the model using Bayesian methods and annual data on government revenue and spending, household debt, nonperforming loans in the private sector, borrowing rates for the government and the corporate sector, as well as price and wage inflation. The model features eight stochastic shocks in each year, identical to the number of variables that we use in the estimation. We find that the model does an excel-lent job of matching additional variables such as output, investment, and the current account (which the model was not asked to replicate). We then perform two tasks with the model. First, we decompose the movements in output, investment, and other key variables into the con-tribution of each type of shock. This helps us determine which shocks were the most important in driving the crisis dynamics. Second, we use the model to perform a number of “counterfactuals” to identify the role played by different aspects of the institutional environment. We examine, in particular, how the dynamics of output and investment would have been different if debt levels in Greece were set at the av-erage of emerging- market economies, if banks’ funding costs had not increased during the crisis as a possible effect of a European banking union, if the Greek government had followed a more virtuous fiscal path in the years preceding the crisis, and if prices and wages had been more flexible.

As in Agatha Christie’s Murder on the Orient Express, our model indi-cates that many forces contributed to the “murder” of the Greek econ-omy. Yet a few factors stand out. First and most importantly, given the size of the fiscal imbalances, a substantial fiscal correction was inevi-table. According to our estimates, fiscal consolidation accounted for ap-proximately 50% of the output drop from peak to trough. Much of the remainder is explained by the increase in funding costs for the private sector (“sudden stop” in our model) and the sovereign (“sovereign risk shock”). The combination of the two shocks accounted for an additional 40% of the output drop from peak to trough, with the sudden stop driv-ing more than half of the effect.

Lastly, our estimates indicate that markup shocks in product mar-kets and a surge in nonperforming loans contributed significantly to the lack of recovery in 2014 and 2015: in the absence of these shocks,

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 5

output in 2014–15 would have recovered approximately 35% of its peak- to- trough drop. These findings indicate that the external dimen-sion of the crisis may slowly be fading, and that the forces holding back the Greek economy are now largely domestic and microeconomic: the recovery will entail cleaning up nonperforming loans and facili-tating the adjustment of prices relative to wages. The lack of a suffi-cient price adjustment may have been due to limited competition in goods and services markets, as well as to a rise in firms’ costs stemming from factors such as the uncertainty about EZ exit and the taxation of key inputs.

The effects of the shocks described above were made larger by high leverage and low price flexibility. Our counterfactual exercises allow us to examine more directly the effects of these factors. We find that if the levels of government, private, and external debt in Greece had been comparable to those in the average of the emerging- market economies (so smaller by about half), the peak- to- trough decline in output would have been smaller by about a third, and the same conclusion holds if the prices and wages had been twice as flexible.

II. The Greek Economy before and during the Crisis

This section describes the dynamics of key macroeconomic variables in Greece before and during the crisis. We focus on the behavior of output and investment, as well as on the accumulation of debt—government, private, and external. We also describe the three shocks through which the global financial crisis affected Greece (sudden stop, sovereign debt crisis, and banking crisis) as well as their interrelationships. This sets the stage for the empirical exercise in section III, and motivates some of the modeling choices and analysis in sections IV–VI.

A. Pre- crisis

Output

Figure 1 plots GDP per capita in 2014 US dollars, adjusted for purchas-ing power parity (PPP) and in a log scale from 1980 onward. In this figure, as well as in subsequent figures and tables in this section, we compare Greece to the four other major Eurozone (EZ) countries that were hit by the EZ crisis: Ireland (IE), Italy (IT), Spain (ES), and Por-tugal (PT).

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

6 Gourinchas, Philippon, and Vayanos

As of 1980, Greek GDP per capita was above that of Ireland, Por-tugal, and Spain. During the 1980s, Greece experienced relative stag-nation and was overtaken by Ireland and Spain. Greece grew faster during the period 1996–2000 and especially from 2001, when it entered the Eurozone (EZ), until 2008. By 2008, Greece had almost caught up with Spain.

Motivated by figure 1, we divide the period 1996–2014 into three subperiods: the period 1996–2000, during which Greece experienced a boom in anticipation of EZ entry; the period 2001–2008, during which the boom continued with Greece inside the EZ; and the crisis period 2009–2014. In the tables constructed in the rest of this section, we report averages of macroeconomic variables for the three subperiods. In some of the tables we also compare with the year 1995, which we take as in-dicative of the Greek economy before the (actual or anticipated) effects of EZ entry.3

Investment

Table 1 reports the level of investment in Greece during the periods 1996–2000, 2001–2008, and 2009–2014, and compares with 1995. The table also decomposes investment into corporate, residential, and public and compares with Ireland, Italy, Portugal, and Spain. Greece experienced the second- largest increase in corporate investment from

Fig. 1. GDP per capita for Greece and other EZ crisis countries, 1980–2014Source: The data come from the Conference Board Total Economy Database. The GDP is expressed in 2014 US dollars, is adjusted for PPP using 2011 weights, and is plotted in a log scale.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Tab

le 1

Inve

stm

ent i

n G

reec

e an

d o

ther

EZ

Cri

sis

Cou

ntri

es, 1

995–

2014

, as

Perc

enta

ge o

f GD

P

Tota

l Inv

estm

ent

95

96–0

0

01–0

8

09–1

4

ES

22.0

23.7

28.8

21.0

GR

20.4

23.1

23.7

14.6

IE18

.222

.326

.116

.2IT

19.0

19.4

21.1

18.6

PT

23.3

26

.5

23.9

17

.4

Cor

pora

te In

vest

men

tR

esid

enti

al In

vest

men

tPu

blic

Inve

stm

ent

95

96–0

0

01–0

8

09–1

4

95

96–0

0

01–0

8

09–1

4

95

96–0

0

01–0

8

09–1

4

ES

11.7

13.0

13.9

12.0

6.0

7.0

10.7

5.7

4.3

3.7

4.2

3.3

GR

8.4

10.5

10.3

7.7

8.6

8.8

9.2

3.7

3.4

3.8

4.2

3.2

IE10

.612

.311

.411

.05.

27.

110

.62.

72.

42.

94.

12.

5IT

11.3

11.8

12.9

10.8

5.1

4.8

5.3

5.1

2.6

2.8

2.9

2.7

PT

11.6

13

.8

13.7

11

.1

7.3

7.

7

6.1

3.

1

4.4

5.

0

4.1

3.

2

Sour

ce: T

he d

ata

com

e fr

om A

ME

CO

. Inv

estm

ent

is m

easu

red

by

the

seri

es “

gros

s fix

ed c

apit

al f

orm

atio

n: t

otal

eco

nom

y,”

and

doe

s no

t in

clud

e in

vent

orie

s. R

esid

enti

al in

vest

men

t is

mea

sure

d b

y “g

ross

fixe

d c

apit

al fo

rmat

ion:

dw

ellin

gs”;

cor

pora

te in

vest

men

t by

“gro

ss fi

xed

cap

ital

form

a-ti

on: p

riva

te s

ecto

r” m

inus

res

iden

tial

inve

stm

ent;

and

pub

lic in

vest

men

t by

“gro

ss fi

xed

cap

ital

form

atio

n: g

over

nmen

t.”

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

8 Gourinchas, Philippon, and Vayanos

Fig. 2. Net foreign assets in Greece and other EZ crisis countries, 1980–2014, as per-centage of GDP.Source: The data come from Lane and Milesi- Ferretti (2007).

1995 to 1996- 2000, after Portugal. Corporate investment remained at that elevated level during 2001- 2008. Thus, EZ entry and its anticipation was associated with a significant rise in corporate investment in Greece. That rise, however, occurred from a low base, and corporate investment remained significantly lower than in the other countries.

Unlike Ireland and Spain, Greece did not experience a significant increase in residential investment from 1995 to 1996–2008. Residential investment was already high in 1995, however, and the real estate boom in Ireland and Spain only meant that residential investment in those countries caught up with and exceeded somewhat that in Greece.

Net Foreign Assets

The fast growth of Greek GDP per capita during the period 1996–2008 was associated with an increase in external indebtedness. Figure 2 plots net foreign assets (NFA) from 1980 onward as percentage of GDP. The NFA for Greece were negative throughout that period. They were a relatively small fraction of GDP in absolute value until the mid- 1990s, and they subsequently declined to a much more negative fraction. Greece’s NFA position deteriorated at a comparable rate to Portugal’s and Spain’s, while Ireland experienced a more abrupt deterioration. The behavior of Greece’s NFA from the mid- 1990s onward is indicative of large current account deficits. Table 2 reports the level of the current

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Tab

le 2

The

Cur

rent

Acc

ount

in G

reec

e an

d o

ther

EZ

Cri

sis

Cou

ntri

es, 1

995–

2014

, as

Perc

enta

ge o

f GD

P

Cur

rent

Acc

ount

Sur

plus

Net

Exp

orts

Net

Cur

rent

Tra

nsfe

rs P

lus

Net

Pri

mar

y In

com

es

95

96–0

0

01–0

8

09–1

4

95

96–0

0

01–0

8

09–1

4

95

96–0

0

01–0

8

09–1

4

ES

–1.2

–2.0

–6.7

–1.6

–1.0

–1.1

–4.1

0.8

–0.2

–0.9

–2.6

–2.4

GR

–2.8

–5.7

–11.

7–7

.3–8

.3–9

.1–1

0.6

–5.9

5.5

3.4

–1.1

–1.4

IE2.

61.

2–2

.31.

710

.912

.012

.419

.2–8

.3–1

0.8

–14.

7–1

7.5

IT2.

01.

5–1

.1–1

.03.

72.

80.

10.

4–1

.7–1

.3–1

.2–1

.4PT

–3

.4

–7.7

–9

.8

–4.5

–6

.4

–9.1

–8

.5

–3.0

3.

0

1.4

–1

.3

–1.5

Sour

ce: T

he d

ata

com

e fr

om A

ME

CO

. Net

exp

orts

are

mea

sure

d b

y th

e se

ries

“ne

t exp

orts

of g

ood

s an

d s

ervi

ces”

; net

cur

rent

tran

sfer

s by

“ne

t cur

-re

nt tr

ansf

ers

from

the

rest

of t

he w

orld

”; a

nd n

et p

rim

ary

inco

me

by “

net p

rim

ary

inco

me

from

the

rest

of t

he w

orld

.” T

he c

urre

nt a

ccou

nt s

urpl

us

is th

e su

m o

f the

thre

e se

ries

.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

10 Gourinchas, Philippon, and Vayanos

account in Greece, Ireland, Italy, Portugal, and Spain during the periods 1996–2000, 2001–2008, and 2009–2014, and compares with 1995. The table decomposes the current account into (a) net exports and (b) the sum of net current transfers and net primary income.

Greece’s current account deteriorated from 1995 to 1996–2000, and deteriorated further from 2001 to 2008. The deterioration from 1996–2000 to 2001–2008 was particularly severe: 6.0% of GDP, larger than in the other countries. From 2001 to 2008, Greece was running an average current account deficit of 11.7% of GDP, also larger than in the other countries.

The deterioration of Greece’s current account from 1995 onward was primarily driven by a decline in net current transfers and net primary income. Net current transfers to Greece declined partly because of the drop in EU subsidies, especially after the 2005 EU enlargement, as funds were redirected to new entrants that were poorer than Greece. Net primary income also declined because workers’ remittances be-came smaller as Greece became a net immigration country and because of growing interest payments on Greece’s rising external debt. Greece’s trade balance also deteriorated through that period, reaching –10.6% of GDP during the period 2001–2008.

The increase in Greece’s current account deficit from 1995 to 1996–2000 was associated with an increase in corporate investment and, hence, in productive capacity. Indeed, the current account deficit in-creased by 2.9% of GDP, corporate investment increased by 2.1%, and public investment by 0.4%. The increase in the current account deficit from 1996–2000 to 2001–2008, however, was associated with an increase in consumption. Indeed, the current account deficit increased by 6.0% of GDP, total saving declined by 6.7%, and corporate investment dropped slightly. The decline in total saving from 1996–2000 to 2001–2008 was primarily driven by private saving, which declined by 4.3% of GDP.4

Government Debt

Figure 3 plots government debt from 1980 onward, as percentage of GDP. As of 1980, government debt in Greece was 21.4% of GDP, lower than in all other countries except for Spain. Debt rose sharply during the 1980s, and by 1993 it had reached 94.4% of GDP, a level larger than in all other countries except for Italy. A combination of fiscal tighten-ing to meet the criteria for EZ entry, and sharply lower interest rates in anticipation of that entry, helped stabilize and even reduce slightly

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 11

the ratio of debt to GDP to 88.5% in 1999. Budget discipline became looser after EZ entry, and especially after 2007. As a consequence, debt to GDP increased—to 103.1% in 2007 and 126.8% in 2009—despite the fast growth in GDP during the period 2001–2008.

While debt to GDP increased only mildly from 1999 to 2007, there was a sharp increase in the amount of the debt held by foreign entities and a consequent decrease in the amount held domestically. That trend was due mainly to the decline in private saving. Figure 4 plots gross government external debt for Greece, and compares with the same se-

Fig. 4. Gross government external debt for Greece, Portugal, and Spain, 1999–2013, as percentage of GDP.Source: The data come from the ECB, series “gross external debt: government.” The data are quarterly, and we report the average over each year.

Fig. 3. Government debt in Greece and other EZ crisis countries, 1980–2014, as per-centage of GDP.Source: The data come from AMECO, series “general government consolidated gross debt.”

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

12 Gourinchas, Philippon, and Vayanos

ries for Portugal and Spain, and with Greece’s NFA.5 Gross government external debt for Greece essentially coincides with the negative of NFA. By contrast, gross government external debt for Portugal and Spain is significantly lower than the negative of those countries’ NFA (which are not plotted, but are similar to Greece’s from figure 2). Figure 4 thus indicates that Greece’s current account deficit essentially financed gov-ernment borrowing.6

Figure 5 plots government deficit as percentage of GDP. The figure com-pares Greece to Italy, which was the most similar to Greece in terms of the size of its government debt until the crisis, and to the EU average. The figure shows that Greece’s public finances improved in the run- up to EZ entry, but worsened steadily post- entry. The pre- entry improvement was similar to that in Italy and the EU average. Unlike in Greece, however, the latter series remained relatively stable post- entry and until the crisis.

Banks and Credit

From the mid- 1990s until the crisis, Greece experienced a boom in private credit. An extensive program of financial liberalization that took

Fig. 5. Government deficit in Greece, Italy, and the EU average, 1985–2014, as percent-age of GDP.Source: The data come from the EC, series “surplus (net lending or net borrowing: general government).”

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 13

place in the late 1980s and the 1990s paved the way for the credit boom. It was also fueled by easier access to foreign capital following EZ entry (and the anticipation of it). Figure 6 plots bank loans to the nonfinancial private sector for Greece, Ireland, Italy, Portugal, and Spain, as percent-age of GDP.

Private- sector loans to GDP were significantly lower in Greece than in the other countries before EZ entry: they stood at 34.1% of GDP in 1998, compared to 60.8% in Italy, 74.6% in Spain, 80.31% in Portugal, and 82.8% in Ireland. Loans to GDP grew faster in Greece than in any other country, however, after EZ entry. As of 2008, they stood at 103.0%, a ratio smaller than Ireland’s, Portugal’s, and Spain’s, but larger than Italy’s.

To finance their increasing lending activity, Greek banks became more reliant on wholesale funding through the interbank market. Figure 7 plots gross external debt for Greek banks and compares with Italy, Por-tugal, and Spain. Gross external debt of banks consists mainly of inter-bank loans. Gross external debt of Greek banks increased from 12.3% of GDP in 1999 to 46.2% of GDP in 2008. As in the case of private- sector loans to GDP, the growth rate was higher than in the other countries, and the 2008 level was smaller than Portugal’s and Spain’s, but larger than Italy’s.

Fig. 6. Bank loans to the private sector excluding financial firms in Greece and other EZ crisis countries, 1998–2014, as percentage of GDP.Source: The loans data come from the Bank of Greece (BoG) in the case of Greece and from the European Central Bank (ECB) for the other countries. The loan data are monthly and are sampled in December of each year.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

14 Gourinchas, Philippon, and Vayanos

B. Crisis

The Three Shocks

The global financial crisis that began in 2007 found Greece in a highly vulnerable position. As of 2007, Greece’s current account deficit had reached 15.9% of GDP, NFA stood at –99.9%, government deficit at 6.5%, and government debt at 103.1%. On all four measures, Greece fared worse than Ireland, Italy, Portugal, and Spain. Greece’s bank-ing system was also vulnerable. While the ratio of private- sector loans to GDP in Greece was lower than in Ireland, Portugal, and Spain, the exposure of Greek banks to their sovereign was larger than in those countries.

Greece was hit by three interdependent shocks during the crisis. The first shock was a sovereign debt crisis: investors began to perceive the debt of the Greek government as unsustainable, and were no longer willing to finance the government deficit. The second shock was a bank-ing crisis: Greek banks had difficulty financing themselves, and their solvency was put in doubt because of projected losses to the value of their assets. The third shock was a sudden stop: foreign investors were no longer willing to lend to Greece as a whole (government, banks, and

Fig. 7. Gross external debt of financial firms for Greece and other EZ crisis countries, 1999–2013, as percentage of GDP.Source: The data come from the ECB, series “Gross External Debt: MFIs.” The data are quarterly and we report the average over each year. We exclude the series for Ireland, which rises up to 425% of GDP, so that the series for the other countries can be seen more clearly.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 15

firms), and so the country could not finance its current account deficit, nor roll over its maturing gross liabilities.

The three shocks were interlinked. The banking crisis made the gov-ernment’s fiscal problems worse. This was because the government had to inject equity capital into the banks and had to provide them with guarantees so that they could borrow in the interbank market. Moreover, because banks had to curtail their lending, the economy slowed down and the government’s tax revenues declined. These channels were at play starting from the fall of 2008, when Greek banks faced significant difficulties financing themselves in the interbank market. The Greek government passed a law in December 2008 that provided support to the banks in the form of guarantees and equity capital.

Conversely, the sovereign crisis made the banks’ liquidity and solvency problems worse. This was because concerns about default risk by the Greek government reduced the value of the Greek banks’ government- bond portfolio, and this put the banks’ solvency in doubt. Moreover, the government had to engage in significant fiscal tightening, and the ensuing recession meant that firms and house-holds had difficulty repaying their loans, adding to the banks’ sol-vency problems. Finally, the guarantees given by the government to Greek banks diminished in value. That applied both to the guarantees intended to help the banks borrow in the interbank market and to the government- supplied deposit insurance. Hence, banks had more dif-ficulties financing themselves and their liquidity problems worsened. These channels were at play beginning in September 2009, when in-vestors began to perceive the debt of the Greek government as unsus-tainable.

Both the sovereign and the banking crises were closely linked to the sudden stop. Indeed, most of government debt was held by foreign investors: out of government debt equal to 103.1% of GDP in 2007, the debt held by foreign investors was 76.1% of GDP. Greek financial firms also had significant foreign debt: their gross external debt was 41.8% of GDP in 2007. Since the Greek government and Greek banks intermedi-ated most of the flow of foreign capital to Greece, the withdrawal of foreign capital meant that both sectors’ access to funds was seriously impaired.

Ireland, Italy, Portugal, and Spain were hit by some or all of the same shocks. The shocks’ effects were more severe in the case of Greece, how-ever, given the country’s larger vulnerability.7

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

16 Gourinchas, Philippon, and Vayanos

Assistance to the Sovereign and Sovereign Default

In May 2010, Greece agreed to follow an adjustment program financed and monitored by European institutions and the IMF. Under the terms of the agreement, Greece received a loan so as to avoid a default on its private creditors and reduce its government deficit more smoothly. In exchange, it had to engage in significant fiscal tightening and imple-ment a battery of structural reforms. The agreed loan amount was 110 billion euros, or 44% of Greece’s 2010 GDP. Out of that amount 80 bil-lion came from other EZ countries, and the remaining 30 billion from the IMF. The first adjustment program was rolled over into a second, agreed to in February 2012. A third program began in August 2015.

In March 2012, Greece agreed to a debt restructuring with its private creditors. Under the terms of this private- sector involvement (PSI), pri-vately held government debt with face value of 199.2 billion euros was replaced by debt with a face value of 92.1 billion. Greece was the only EZ country to default on its creditors.

Assistance to the Banks, Recapitalizations, and Capital Controls

In addition to the loans made to the Greek government under the adjust-ment programs, assistance was provided to Greece through ECB loans to its banking system. These loans were administered either directly from the ECB, with a low interest rate and stringent collateral requirements, or indirectly via the Bank of Greece (BoG) as emergency liquidity assistance (ELA), with a higher interest rate and less stringent collateral requirements. The ECB loans were necessary to address the liquidity problems of Greek banks. They rose from 48 billion euros in January 2010 to a maximum of 158 billion euros in February 2012, then dropped to a minimum of 45 bil-lion euros in November 2014, and then rose again to a maximum of 122 bil-lion in September 2015. The ECB loans were at their maxima around times when there was a high- perceived risk of Greece exiting the EZ (Grexit). The risk of Grexit was high around the double election of May and June 2012, and during the first half of 2015 after a new Greek government op-posed to the adjustment programs had been elected in January 2015.

Greek banks went through a series of recapitalizations. Losses on the banks’ government- bond portfolio reduced the capital of all banks and rendered most of the large ones insolvent. Some of the banks were re-solved, and their deposits and some of the loans were transferred to the four largest banks. The latter were recapitalized. The resolution and re-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 17

capitalization process was completed in July 2013, and involved 38.9 bil-lion euros of public funds, which were loaned to Greece. An additional 3.1 billion euros were raised by private investors. That first, large- scale recapitalization was followed by a second in April and May 2014, when the banks raised 8.3 billion euros, solely from private investors. A third recapitalization took place in the fourth quarter of 2015. The total amount that was raised then was 13.7 billion euros, of which 8 billion euros was raised from private sources via new investment and debt- equity conver-sions. The second and third recapitalizations were made necessary be-cause of increased projected losses on banks’ loans to the private sector.

Macroeconomic Developments

We finally review the macroeconomic developments during the crisis period 2009–2014, following a roughly similar order as for the pre- crisis period. Greek GDP per capita declined sharply during the crisis, as shown in figure 1. The decline was 25.8% between 2008 and 2014. It was much sharper than in Ireland (6.1%), Italy (10.3%), Portugal (7.8%), and Spain (9.6%).

The decline in GDP was accompanied by a large decline in invest-ment. The latter decline can be seen in table 1 by comparing the crisis period with the pre- crisis one. It can be seen more sharply by compar-ing investment in 2014 to that in 2008. Investment in 2014 was less than half of its 2008 value, having dropped by 12.2% of GDP. Both the rela-tive and the absolute declines were larger than in Ireland, Italy, Portu-gal, and Spain. The level of investment in 2014 was also significantly lower than in the other countries.

During the crisis, Greece reduced and almost eliminated its current account deficit. That deficit stood at 2.2% of GDP in 2014, down from 16.5% in 2008. The adjustment occurred entirely through a drop in in-vestment. Total saving did not change: government saving increased as a result of the fiscal tightening that took place during the crisis, but that effect was offset by a decline in private saving. Private saving in Greece declined between 2008 and 2014, while it increased in Ireland, Italy, Portugal, and Spain. Conversely, government saving increased in Greece during the same period, while it declined in the other countries. Thus, the austerity undergone by Greece during the crisis was more severe than in the other countries.

During the crisis, public debt to GDP followed explosive dynamics, rising from 103.1% in 2007 and 126.8% in 2009 to 177.1% in 2014. The in-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

18 Gourinchas, Philippon, and Vayanos

crease resulted from the deficits run during the crisis and from the drop in GDP. The debt restructuring agreed to in 2012 countered these effects somewhat.8 Greece eliminated its primary budget deficit in 2014—it ran a primary surplus of 0.4% in that year.

The ratio of private- sector loans to GDP declined slowly during the crisis. As figure 6 shows, it stood at almost the same level as Portugal’s and Spain’s in 2014, and above Ireland’s and Italy’s. The slow decline of private- sector loans to GDP in Greece is due to the sharp decline in GDP and the relatively slow pace of resolving nonperforming loans.

III. Benchmarking the Greek Crisis

The previous section argued that Greece experienced three quasi- simultaneous and interlinked shocks: a sudden stop, with the abrupt withdrawal of private foreign capital starting in 2009; a sovereign debt crisis, with rapidly deteriorating fiscal accounts in 2008 and 2009, culminating in a sovereign default in 2012; and a banking crisis with the bursting of a boom in credit to the private nonfinancial sector in 2008 and 2009. This section provides a systematic comparison between Greece and other countries experiencing each type (and sometimes combinations) of similar shocks.

A. The Incidence of Crisis

We begin by identifying episodes of sudden stops, sovereign defaults, and lending booms/busts.

Sudden Stops

Starting with the work of Dornbusch and Werner (1994), Calvo et al. (2006), Adalet and Eichengreen (2007), and many others, an abundant literature has explored the macroeconomic consequences of a sudden reversal in foreign lending. Calvo et al. (2006), in particular, compiled a list of 33 sudden stop episodes between 1980 and 2004 for a sample of 31 emerging markets. In the authors’ classification, a sudden stop is identified by the combination of (a) a reversal in capital flows; (b) an increase in emerging- market bond spreads, capturing times of global stress on financial markets; and (c) a large drop in domestic output. Mendoza (2010) adopts a similar classification, while Korinek and Men-doza (2014) extend the Calvo et al. (2006) sample to 2012 and to ad-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 19

vanced economies.9 As in these earlier papers, we define the year t of a sudden stop episode as the year of a sharp reduction in foreign lending that coincides with a large decline in output.10 With this criterion, we identify 49 sudden stop events, 36 for emerging- market economies, and 13 for advanced economies (see table 3).

Sovereign Defaults

We identify sovereign debt crisis as in Gourinchas and Obstfeld (2012). The year t of a sovereign debt crisis corresponds to the year identified with a default on domestic or external public debt, as tabulated by Re-inhart and Rogoff (2009), Cantor and Packer (1995), Chambers (2011), Moody’s (2009) and Sturzenegger and Zettelmeyer (2007).11 Since 1980, we record 64 default episodes in emerging- market economies, and one in an advanced economy: Greece in 2012.

Lending Booms/Busts

Credit boom episodes are defined as in Gourinchas, Valdés, and Landerretche (2001), from the deviation of the ratio of credit to the nonfinancial sector to output from its trend.12 A lending boom episode is recorded when this cyclical deviation exceeds a given boom thresh-old. The year t of the lending boom then coincides with the year in which the maximum (positive) deviation of credit to GDP occurs. Our calculations identify 114 lending boom episodes, 96 of which are in emerging- market economies.

Finally, we identify “trifecta” episodes: sovereign defaults that coincide with a lending boom and a sudden stop.13 We find nine such crises for emerging markets, including well- known episodes such as Mexico in 1982, Chile and Uruguay in 1983, Indonesia and Russia in 1998, Ecua-dor in 1999, Argentina and Turkey in 2001, and Uruguay again in 2003. Again, Greece is the only advanced economy to have experienced a trifecta crisis in our sample.

Table 3 reports the incidence of each type of crisis for advanced and emerging- market economies. It illustrates the relative prevalence of sovereign defaults, lending booms, and trifecta crises among emerging economies. By contrast, sudden stops are roughly distributed in pro-portion to the number of countries in each group in our sample.

We compare each type of episode to the Greek crisis. For the purpose of this exercise, we consider that the Greek episode begins in 2010.14

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

20 Gourinchas, Philippon, and Vayanos

B. The Data

We construct a database of macrovariables for a large sample of ad-vanced and emerging economies between 1980 and 2014.15 The sample contains 22 advanced economies (including Greece) and 57 emerging- market economies, distributed across six broad regions. The list of emerging- market economies includes all countries classified as emerg-ing according to leading outlets and are therefore reasonably well inte-grated into global bond markets.16

In the spirit of a large literature in international macroeconomics, we examine the behavior of key macroeconomic variables around the three types of shocks discussed above: sudden stops, sovereign debt crises, and lending boom/busts episodes, as well as trifecta crises.17 Our event study considers the response of seven macroeconomic variables: out-put, consumption, investment, exports and imports of goods and ser-vices, the current account, credit to the nonfinancial sector, and public debt. The data is collected from the World Bank’s Development Indica-tors, the IMF’s International Financial Statistics, and Reinhart and Rog-off (2009) estimates of total (domestic and external) gross public debt for a large number of countries.18 In addition to these macroeconomic variables, we use the Reinhart and Rogoff (2004) and Ilzetzki, Reinhart, and Rogoff (2010) de facto exchange rate regime classification and sort countries into “pegs” or “floats” based on the exchange rate regime in the year preceding the episode. Further, we split pegs into “de- peggers,” that is, countries that abandon their peg within two years of the shock, and “strict peggers” who maintain their peg for at least two years. This will allow us to contrast the macroeconomic response of countries based on their post- shock exchange rate regime. This is an important consideration given the often- heard argument that the main constraint on the Greek economy is its lack of nominal exchange rate flexibility (e.g., see Krugman 2012).

Table 3Crises Incidence in Advanced and Emerging Economies, 1980–2014

Sudden

Stop Sovereign

Default Lending

Boom Trifecta No.

Countries

Advanced economies 13 1 18 1 22Emerging markets 36 64 96 9 57Total 49 65 114 10 79

Note: Details on how each type of episode is identified are in the appendix.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 21

C. Findings

Figure 8 reports the output response to a typical sudden stop across the 48 episodes (excluding Greece). It measures output per capita, relative to its pre- crisis level at t – 2, in 100 log points, so that a value of x indicates that output per capita is ex/100 times pre- crisis output. The figure also includes point- wise, one- sided 10% confidence intervals (the grayed area), as well as the trajectory of Greek output (bullet points) during the 2010 episode. As expected, since our definition of sudden stops requires a large output drop, the mean response indicates a sharp decline in output, marginally signifi-cant, close to 10% below its peak in the year of the sudden stop, followed by a gradual recovery. By year t + 2, output has typically recovered to its pre- crisis level and continues to expand. Two facts are relevant here. First, Greece experienced a strikingly worse output decline. By 2013, that is, t + 3, Greek output per capita was 25% below its pre- crisis level (e–0.29 = 0.75), significantly below the average response and showing few signs of re-covery. Second, unlike the typical sudden stop, Greece’s output path was “back loaded.” The initial recession in 2009 and 2010 (t – 1 and t) is similar to a typical sudden stop episode and milder than the subsequent

Fig. 8. The response of output to a sudden stopSource: See the appendix for data sources.Note: The figure reports real output per capita relative to period t – 2, in 100 log points for a typical sudden stop episode (with output collapse) and for Greece in the 2010 crisis.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

22 Gourinchas, Philippon, and Vayanos

decline in Greek output. By contrast, typical episodes are “front loaded” with a more pronounced “V” shape.19 This is not surprising if we con-sider that Greece’s sudden stop was of a particular nature. As discussed in the previous section, the sudden withdrawal of foreign lending was accommodated initially via ECB lending against collateral, and after 2010 via official assistance from the IMF and the European Union. Hence there was no sharp immediate downturn, as is typical when countries experi-ence sudden loss of market access.

Claim 1. The Greek crisis was significantly more severe, persistent, and back loaded than the typical sudden stop.

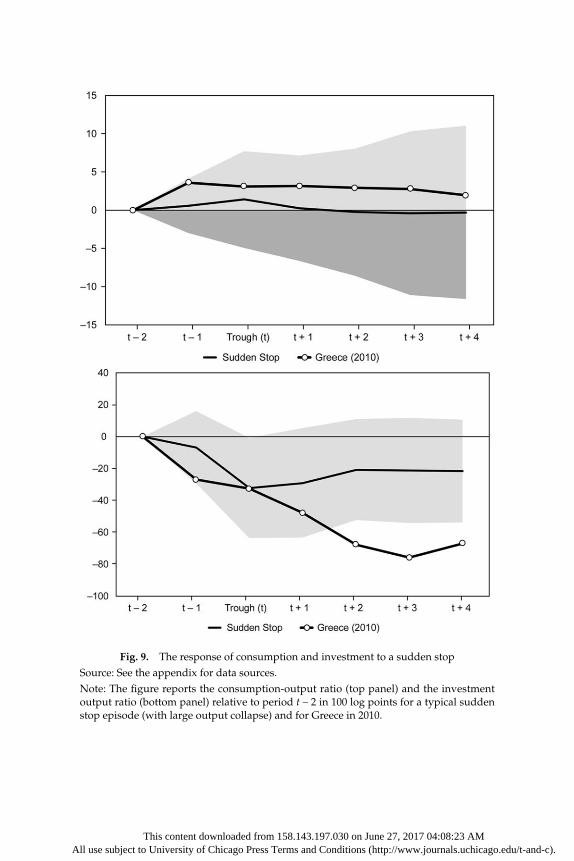

Figure 9 reports a similar analysis for the consumption and invest-ment ratios to output. As for output, each variable is expressed in 100 log points, relative to its value at t – 2, that is, at the beginning of the episode. Equivalently, this figure reports the growth differential be-tween consumption or investment and output since t – 2. The top panel reports the consumption- to- output ratio. In a typical sudden stop, con-sumption mostly moves in line with output. Instead, Greek consump-tion grew modestly faster than output, although not significantly so. The bottom panel reports the investment- to- output ratio. Greek invest-ment collapsed dramatically, much more so than in a typical sudden stop. By 2013, that is, t + 3, the investment- to- output ratio was less than half of its pre- crisis level (e–0.76 = 0.47), while a typical sudden stop sees a decline of 20% to 30%. Given the decline in output per capita docu-mented in figure 8, real investment per capita collapsed by almost two- thirds between 2008 and 2013 (0.75 × 0.47 = 0.35).

Claim 2. The collapse in Greek aggregate investment in this crisis was unprece-dented in its persistence and magnitude, in comparison to the typical sudden stop.

A sudden withdrawal of foreign capital is only one of the shocks that Greece experienced since 2009, and one might be concerned that the previous comparison might be too unfavorable to Greece. For instance, like Greece in 2010, Argentina in 2001, Chile in 1983, or Indonesia in 1998, among others, experienced a simultaneous drying- up of foreign capital, a sovereign default, and a collapse in lending, that is, a trifecta shock. These episodes are among the worst documented economic crises in postwar history, often accompanied by a banking crisis, and unprecedented levels of economic hardship and political turmoil. In light of the economic and political dislocation associated with it, one would expect the Greek crisis to be on a comparable scale. To investi-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Fig. 9. The response of consumption and investment to a sudden stopSource: See the appendix for data sources.Note: The figure reports the consumption- output ratio (top panel) and the investment output ratio (bottom panel) relative to period t – 2 in 100 log points for a typical sudden stop episode (with large output collapse) and for Greece in 2010.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

24 Gourinchas, Philippon, and Vayanos

gate this, figure 10 reports the average output response to each of the following shocks: a sovereign default, a lending boom/bust, as well as the trifecta shock that consists of these two shocks occurring during a sudden stop episode. As an additional point of comparison, the figure also includes the average output response for Ireland, Italy, Portugal, and Spain, that is, the other peripheral countries most affected by the Eurozone crisis (under the label IIPS). Finally, the graph also includes 10% point- wise, one- sided confidence intervals for the trifecta shocks.

The figure illustrates how much of an outlier the Greek crisis truly was. While output per capita initially declined in line with that of a trifecta crisis, by 2011 (i.e., t + 1) output had declined significantly more and kept falling. By contrast, in a typical trifecta crisis, output is back to its pre- crisis level by t + 3. The figure allows us to make a number of additional points. First, trifecta crises are more severe than a typi-cal default crisis, although the differences are small and often insignifi-cant. Second, following a lending boom, output keeps growing. This is because many lending booms in our sample are not always followed by an economic downturn or crisis, as noted also by Gourinchas et al.

Fig. 10. The response of output to various crisesSource: See the appendix for data sources.Note: The figure reports the mean output per capita relative to period t – 2 in 100 log points for various episodes, and for Greece in 2010; 10% one- sided, point- wise confidence intervals for trifecta episodes.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 25

(2001) and Ranciere, Tornell, and Westermann (2008). Lastly, the trajec-tory for the IIPS countries illustrates that, in these countries too, the crisis has been much more persistent then expected, with output still 7% below the pre- crisis level as of 2014 (t + 4).

Claim 3. The collapse in Greek output per capita has been significantly more severe and more persistent than the typical trifecta crisis.

Figure 11 makes the same point even more vividly. The panel on the left reports the output trajectory for all countries that experienced a sud-den stop in our sample. The panel on the right presents similar results for all trifecta episodes. Both panels also report the Greek 2010 episode. As is clear from both figures, Greece’s economic performance is cumu-latively much worse than all episodes from the last 35 years, including crises such as Argentina in 2001 or Uruguay in 1983, with the single exception of the United Arab Emirates crisis of 2009.20

We next consider the role of the exchange rate regime. Our data set includes information on the de facto exchange rate regime from Reinhart and Rogoff (2004) and Ilzetzki et al. (2010). We use this data to construct an indicator of the exchange rate regime in the year of the shock and the preceding year (peg/float). We further subdivide pegs based on whether countries maintain their peg for at least two years after the crisis (strict peggers) or abandoned it (de- peggers).21 Figure 12 contrasts the output response following an emerging market sudden stop for de- peggers, strict peggers, and floaters, together with that of Greece and of the IIPS countries. The figure also includes 10% point- wise, one- sided confidence intervals for strict peggers. Unsurprisingly, we find that strict peggers experience a worse adjustment than de- peggers, who in turn perform worse than floaters: by t + 4, output is still 4% below its pre- crisis level for strict peggers, while it is 3% (resp. 8%) above its trend for de- peggers (resp. floaters): a more flexible exchange rate regime is associated with a less severe and less persistent crisis. Greece’s experience is very singular in that respect as well: its output loss is much larger and significantly more persistent than for countries that maintained their exchange rate. By contrast, the experience of the IIPS countries is more in line with that of strict peggers, albeit less severe in 2010 and 2011 (t and t + 1).

There are two ways to think about this result. One possible inter-pretation is that the severity of the Greek crisis cannot be attributed entirely to the strictures of the common currency, since it significantly underperformed other “strict fixers.” This would direct our attention toward other features of the Greek economy than just the exchange rate

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Fig. 11. The distribution of output responses to sudden stops and trifecta crisesSource: See the appendix for data sources.Note: The figure reports output per capita relative to period t – 2 in 100 log points for each sudden stop episode (top panel), and for each trifecta crises (bottom panel), together with Greece in 2010.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 27

regime. This is not the only interpretation. Clearly, countries can and often choose their exchange rate regime in response to the economic environment. Therefore, the sample of strict fixers may consist precisely of countries who stand to lose relatively less from keeping the exchange rate pegged in the aftermath of a sudden stop. This could be the case in particular if these countries were experiencing a relatively modest decline in output. To investigate this question further, figure 13 reports the data for strict fixers alongside that for Estonia, Latvia, and Greece. Both Latvia and Estonia experienced severe recessions following their 2009 sudden stop episode. Estonia’s output per capita declined by 19% between 2007 and 2009, while that of Latvia declined by 17% between 2007 and 2010. Nevertheless, both countries chose to maintain their peg to the euro and “doubled down” by subsequently adopting the com-mon currency in January 2011 for Estonia and January 2014 for Latvia. Overall, both countries have an experience similar to that of the full sample of strict peggers. Yet, it could hardly be argued that the costs

Fig. 12. The role of the exchange rate regimeSource: See the appendix for data sources.Note: The figure reports output per capita relative to period t – 2 in 100 log points for emerging market sudden stops, by exchange rate regime, together with Greece in 2010; 10% one- sided, point- wise confidence intervals for strict peggers.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

28 Gourinchas, Philippon, and Vayanos

of maintaining a fixed exchange rate were small for either country. In-stead, their decision to carry forward and adopt the euro can be related to historical and geostrategic reasons, in particular the desire to anchor their country firmly in the West. Both countries, therefore, adopted the euro despite the large short- run costs associated with doing so: the comparison of their trajectory with Greece’s is unlikely to suffer from a strong selection bias. It is therefore interesting that the experience of Greece appears significantly worse than either country.22

Claim 4. The Greek crisis was significantly more severe than the typical emerg-ing market sudden stop, even for countries such as Latvia or Estonia that main-tained a fixed exchange rate in the aftermath of a sudden stop with large output collapse.

Figure 14 reports credit to the nonfinancial sector (left panel) and public debt (right panel), relative to output. The credit- to- output ratio is measured in deviation from a Hodrick- Prescott (HP) filter trend, while the debt- to- output ratio is measured relative to the country mean. Each

Fig. 13. Output response for strict peggersSource: See the appendix for data sources.Note: The figure reports output per capita relative to period t – 2 in 100 log points for emerging market strict peggers, together with Estonia (2009), Latvia (2009), and Greece (2010); one- sided 10% point- wise confidence intervals for strict peggers.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Fig. 14. Credit and government debt Source: See the appendix for data sources.Note: The left panel reports the ratio of credit to the nonfinancial sector to output, in deviation from a Hodrick- Prescott trend, in percent of GDP. The right panel reports the ratio of government debt to output, in deviation from a country mean, in percent of GDP. Both panels report the typical response over each type of episode, together with Greece in 2010; one- sided 10% point- wise confidence intervals for lending boom (top panel) and trifecta (bottom panel).

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

30 Gourinchas, Philippon, and Vayanos

variable is expressed in percent of GDP. The left panel reports 10% one- sided, point- wise confidence bands for lending boom/bust episodes, while the right panel reports similar confidence bands for trifecta epi-sodes, since these episodes witness the largest increase in public debt. Starting with the credit- to- output ratio, we see that the initial leverage was high, but not as high as in typical lending boom episodes, around 10% of GDP. The ratio of credit to GDP was gradually reduced, al-though at a more measured pace than in typical episodes. Overall, the contraction in credit to the economy is similar to what is observed in other countries. Confidence bands are quite large.

Turning to public debt, we observe an elevated level of public debt even before the crisis (18% of GDP above mean in 2008), increasing rapidly and remaining significantly more elevated than in other episodes. We can see on the graph the effect of the 2012 debt restructuring (in t + 2), reducing the debt- to- output ratio from 80% to 60% of GDP above its mean, but fol-lowed by a subsequent worsening, in part due to the collapse in economic activity in 2013 and 2014. Compared to trifecta or other episodes, levels of public debt remain extraordinarily high and it is clear from this figure that efforts to bring public debt back to sustainable levels have failed.

Claim 5. Domestic leverage in Greece was similar to other lending boom/bust episodes and evolved similarly. By contrast, public debt to output re-mained extremely elevated. Efforts to reduce the public debt burden mostly failed, despite a substantial debt restructuring in 2012.

Figure 15 reports the trade balance- to- output ratio as well as the consumer price index (CPI)- based multilateral real exchange rate com-piled by the IMF. As for domestic credit and public debt, the trade balance- to- output ratio is measured in deviation from country means and expressed in percent of GDP. The multilateral real exchange rate is expressed in percentage deviation from its country mean. The figure also reports 10% point- wise, one- sided confidence intervals for sudden stop episodes. The left panel (trade balance) illustrates the gradual but large improvement of the Greek trade balance between 2008 and 2014, in ex-cess of 10% of GDP, compared to the typical sudden stop episode. Unlike typical sudden stops, where loss of market access forces the trade bal-ance and current account to improve overnight, the overall improvement in Greece was spread out gradually. The cumulated improvement in the trade balance in a typical sudden stop represents 6.2% of output, 5% of which occurs in the year of the sudden stop itself. As discussed in the previous section, financial assistance and access to the liquidity facilities

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

Fig. 15. Net exports and real exchange rateSource: See the appendix for data sources.Note: The top panel reports the ratio of net exports on goods and services to output, in deviation from country mean, in percent of GDP. The bottom panel reports the multilat-eral real exchange rate in percentage deviation from a country mean. Both panels report the typical response over each type of episode, together with Greece in 2010; one- sided, point- wise confidence intervals for trifecta episodes.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

32 Gourinchas, Philippon, and Vayanos

of the European Central Bank allowed Greece to spread out a massive and necessary adjustment in its trade balance. The right panel indicates that most of this adjustment occurred without major movements in the real exchange rate. Like other countries experiencing a sudden stop, Greece’s real exchange rate was initially overappreciated by about 13%. Yet, while the real exchange rate depreciates by 10% in the aftermath of a typical sudden stop (and a massive 35% following a trifecta), Greece’s real exchange rate only depreciated by 4.5% between 2008 and 2014.23

Claim 6. The adjustment of external balances occurred more gradually, but was nevertheless very significant in size. The improvement in external accounts occurred despite any significant movement in the real exchange rate.

IV. Model

This section presents a stylized model of a small open economy in a currency union with rich macrofinancial linkages. The model is de-signed to shed light on two sets of issues. First, we want a realistic enough model that allows us to understand which shocks were respon-sible for the performance of the Greek economy, both before and during the crisis. Second, we want to use the model to perform some simple counterfactual exercises. To achieve these objectives, the model needs to remain stylized. In particular, while we introduce many macrofinance features, we abstract from a full microfounded model of the banking sector that would put excessive constraints on the data. The model fea-tures eight exogenous stochastic processes. They are labeled zs and each is assumed to follow an AR(1) process of the form:

zti = rizt−1

i + s iti, (1)

where the persistence and volatility parameters (ri, si) are estimated from the data, and the innovations ´t

i are i.i.d. with mean zero and unit variance, and i = {dg, spend, . .} is the name of the shock. We next specify the government, households, nonfinancial firms, and the financial sector.

A. Government

Budget Constraint

The government imposes a flat tax on income, spends Gt on goods and services, and makes social transfers Tt. Let B$,t−1

g be the face value (in

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 33

units of the common currency) of the debt issued at time t – 1 and due at time t. The nominal budget constraint of the government, conditional on not defaulting, is

B$,tg

Rtg + ttPH,tYt = PH,t Gt + Tt( ) + B$,t−1

g , (2)

where PH,t is the price index of home goods (so PH,tYt is nominal GDP), tt is a time- varying tax rate, and Rt

g is the gross interest rate on sover-eign debt. It will be convenient to work with real variables. We define real government debt Bt

g ≡ B$,tg / PH,t. We can then rewrite the budget

constraint (conditional on not defaulting) as

Btg

Rtg + ttYt = Gt + Tt +

Bt−1g

PtH, (3)

where PtH ≡ PH,t / PH,t−1 is the domestic (i.e., PPI) inflation rate from t – 1

to t. This formula makes clear that unexpected inflation at time t lowers the real debt burden. We use this convention for all other nominal assets.

Sovereign Default

Sovereign risk plays an important role in the Greek crisis.24 We do not model an optimal default decision by the government. Instead, we in-troduce a default shock ! t

dg and assume that the default happens when ! tdg < F(Bt−1

g / PtH ;Yt). We assume that the function F is increasing in the

real debt burden Bt−1g / Pt

H and decreasing in real GDP Yt. For instance, F could simply be the ratio of debt to GDP. The expected default rate is Et[ !dt+1] = Pr( ! t+1

dg < F(Btg / Pt+1

H ;Yt+1)|It), where It is the information set of investors at time t. Notice that the distribution of ! t+1

dg can be time varying. What matters most in our model, however, are expected credit losses, which take into account the probability of default and expected loss given default. Upon default, government debt is reduced by some haircut and we let dt

g denote expected credit losses. In our quantitative analysis, we adopt the following log- linear specification for expected credit losses at time t + 1:

dtg = dg

Bg

Y(bt

g − Et[yt+1] − Et[pt+1h ] + zt

dg), (4)

where Bg / Y is the average debt- to- GDP ratio, dg is a sensitivity param-eter, and lowercase variables (e.g., bt

g ) represent log deviations from

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

34 Gourinchas, Philippon, and Vayanos

steady- state values. The sovereign risk shock ztdg follows an AR(1) as

postulated in equation (1), with persistence rdg and volatility sdg. Equa-tion (4) states that expected default losses increase with the level of debt, decrease with the inflation rate since the latter reduces the real debt burden, and increase with the sovereign default shock zt

dg. We will use data on sovereign yields to estimate the parameters {dg, rdg, sdg}. The rate paid by the government on its debt is then (in log deviations)

rtg = rt + dt

g,

where rt is the international interest rate.

Fiscal Policy

The government’s spending policy and its social transfer policy are rep-resented by the same rule

gt = Flgt−1 − Fnnt − Frrtg − Fbbt

g + ztspend, (5)

where gt is the log deviation of spending, and nt, rtg, and bt

g are log devia-tions of employment Nt, government credit risk spread Rt

g, and govern-ment debt Bt

g from their steady- state values, Fl, Fn, Fr, and Fb are fixed parameters, and zt

spend is a spending shock that follows equation (1) with persistence rspend and volatility sspend.25 We have the same rule for trans-fers tt. We allow spending itself to be autoregressive (with Fl > 0) to cap-ture the fact that government programs are often scheduled for several years. This fiscal rule implies that the fiscal authorities respond to an increase in sovereign debt by tightening expenditures and reducing so-cial transfers. The term Fn captures automatic stabilizers: as the economy deteriorates, fiscal transfers and spending tends to increase. This formu-lation allows government expenditures and transfers to change both be-cause of macro and financial channels, and also because of spending shocks. Lastly, we specify the following process for the tax rate:

tt = t + zttax,

where ztax follows equation (1) with persistence rtax and volatility stax and t is calibrated to the steady state.

B. Households

Household debt dynamics played an important role during the Great Recession, so we need to introduce borrowers and savers in the model.

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 35

Households are heterogeneous in their time preferences, as in Eggerts-son and Krugman (2012) and Martin and Philippon (2014).26 There are two types of households: a measure 1 − x of patient households in-dexed by i = s (who will be savers in equilibrium), and a measure x of impatient households indexed by i = b (who will be borrowers in equilib-rium). These households have identical preferences over goods and hours worked, but differ in their discount factors: we assume that bs > bb. Household i maximizes expected lifetime utility

E0t=0

∞

∑bit Ct

i( )1−g

1 − g−

Nti( )1+f

1 + w

⎛

⎝⎜

⎞

⎠⎟ ,

where Cit is a bundle of home and foreign goods, defined in Gali and

Monacelli (2008) by

Cti ≡ [(1 − √)1/ehCH,t

i(eh−1)/eh + √1/ehCF,ti(eh−1)/eh]eh/(eh−1),

where eh is the elasticity of substitution between home and foreign goods and √ is the degree of openness of the economy. As usual, the home consumer price index (CPI) is

Pt ≡ [(1 − √)PH,t1−eh + √PF,t1−eh]1/(1−eh).

Household Default

Households borrow at the rate Rth and can default on their debts. Let dth

be the credit loss rate on household loans. Default is a loss for the banks and a positive transfer to borrowers, similar to the financial shock de-scribed in Iacoviello (2015). The borrowers’ budget constraint, following the same convention as with the government, is

PtCtb = (1 − tt)WtNt

b +PH,tBth

Rth

− (1 − dth)PH,t−1Bt−1h + PH,tTtb. (6)

where (1 − tt)WtNtb denotes after- tax labor income, Rt

h the gross interest rate faced by borrowers, Bth is the real face value of the household debt issued at t and due at t + 1, and Ttb the transfers received by borrowers. Borrowers are subject to the following borrowing limit:

Bth <Bth

x.

In our notations, Bth is a per capita measure, while Bth denotes the aggre-gate lending capacity of the financial sector to households. We later de-

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

36 Gourinchas, Philippon, and Vayanos

rive this lending limit from the lender’s problem, and we anticipate the result that only impatient households borrow in equilibrium. The credit loss rate is assumed to follow the process:

dth = −dhyyt + dhbbth + ztdh, (7)

where ztdh follows equation (1) with persistence rdh and volatility sdh. Equation (7) states that the credit loss rate on household loans increases with their debt level, decreases with output, and increases with a house-hold default shock zdh. We will use data on nonperforming loans to esti-mate {dhy, dhb, rdh, sdh}. Note that dth are realized credit losses at time t, un-like dt

g, which is an expected loss that may or may not materialize at t + 1.The savers’ budget constraint is

PtCts = (1 − tt)WtNt

s + !RtPH,t−1St−1 − PH,tSt + PH,tTts, (8)

where !Rt is the nominal after- tax gross return on savings PH,t–1St–1 at time t and Tts denotes real transfers to savers. This return is a complex object since savers are residual claimants: in equilibrium, they hold shares of firms and of banks, but also deposits, government bonds, and potentially foreign assets. Notice, however, that in equation (3) we have assumed a uniform tax rate on aggregate income, and this is what mat-ters in the end. The savers’ Euler equation is

Et bCt+1

s

Cts

⎛

⎝⎜

⎞

⎠⎟−g !Rt+1

Pt+1

⎡

⎣⎢

⎤

⎦⎥ = 1,

where Pt+1 = Pt+1 / Pt denotes the gross CPI inflation rate from t to t + 1. Finally, in the aggregate, we have

CH,t = xCH,tb + (1 − x)CH,t

s

Ct = xCtb + (1 − x)Ct

s.

Nominal Wage Rigidity

We assume a standard model of wage stickiness with a representative union setting wages à la Calvo. The wage equations are standard and satisfy:

ptw = bEtpt+1

w − lw(wt − gct − wnt) + ztw,

pt = (1 − √)pth + √pt

f ,

wt = wt−1 + ptw − pt

h,

This content downloaded from 158.143.197.030 on June 27, 2017 04:08:23 AMAll use subject to University of Chicago Press Terms and Conditions (http://www.journals.uchicago.edu/t-and-c).

The Analytics of the Greek Crisis 37

where ptw denotes wage inflation, wt is the real wage in terms of the CPI

(ln(Wt / Pt)), ztw is a wage- markup shock that follows equation (1) with persistence rw and volatility sw; pt denotes CPI inflation, pt

h is home inflation, pt