physics, economics and ecology

DESCRIPTION

Sorin Solomon, Hebrew University of Jerusalem. Physics, Economics and Ecology. Boltzmann, Pareto and Volterra. Pavia Sept 8 , 2003. Franco M.Scudo (1935-1998). Lotka. Volterra. +. + c i. ( X.,t ) ) X i + j a ij X j. d X i = ( a i. Lotka. Volterra. Boltzmann. (. ). +. x. - PowerPoint PPT PresentationTRANSCRIPT

Physics, Economics and Ecology

Boltzmann, Pareto and Volterra

Pavia Sept 8 , 2003

Franco M.Scudo (1935-1998)

Sorin Solomon, Hebrew University of Jerusalem

+

d Xi = ( ai

Lotka Volterra

+ ci (X.,t)) Xi +j aij Xj

x+( )d Xi = (randi

Lotka Volterra Boltzmann

+ ci (X.,t)) Xi +j aij Xj

x+( )

= P(Xi) ~ Xi –1- d Xi

Lotka Volterra Boltzmann

Pareto

d Xi = (randi + c (X.,t)) Xi +j aij Xj

Alfred Lotka

the number P(n) of authors with n publications is a power law P(n) ~ n with ~ 1.

No. 6 of the Cowles Commission for Research in Economics, 1941.

HAROLD T. DAVIS

No one however, has yet exhibited a stable social order, ancient or modern, which has not followed the Pareto pattern at least approximately. (p. 395)

Snyder [1939]:

Pareto’s curve is destined to take its place as one of the great generalizations of human knowledge

d x= (t) x + P(x) dx ~ x –

1- d xfor fixed distribution with negative drift < ln > < 0

Not good for economy !

d x= (t) x + P(x) dx ~ x –

1- d xfor fixed distribution with negative drift < ln > < 0

Herbert Simon; intuitive explanation

Not good for economy !

d ln x (t) = (t) + lower bound

= diffusion + down drift + reflecting barrier

Boltzmann (/ barometric) distribution for ln x

P(ln x ) d ln x ~ exp(- ln x ) d ln x

d x= (t) x + P(x) dx ~ x –

1- d xfor fixed distribution with negative drift < ln > < 0

Herbert Simon; intuitive explanation

Not good for economy !

d ln x (t) = (t) + lower bound

= diffusion + down drift + reflecting barrier

Boltzmann (/ barometric) distribution for ln x

P(ln x ) d ln x ~ exp(- ln x ) d ln x

~ x -1- d x

d x= (t) x + P(x) dx ~ x –

1- d xfor fixed distribution with negative drift < ln > < 0

Herbert Simon; intuitive explanation

Not good for economy !

d ln x (t) = (t) + lower bound

= diffusion + down drift + reflecting barrier

Can one

obtain stable power laws

in systems with variable growth rates

(economies with both recessions and growth periods) ?

Yes! in fact all one has to do is to recognize the statistical character of the

Logistic Equation

d Xi = (ai + c (X.,t)) Xi +j aij Xj

Montroll

almost all the social phenomena, except in their relatively

brief abnormal times obey the logistic growth.

Elliot W Montroll: Social dynamics and quantifying of social forces (1978 or so)

d Xi = (ai + c (X.,t)) Xi +j aij Xj

Volterra

Scudo

Lotka

MontrollEigen

almost all the social phenomena, except in their relatively

brief abnormal times obey the logistic growth.

Elliot W Montroll: Social dynamics and quantifying of social forces (1978 or so)

Stochastic Generalized Lotka-Volterra

d Xi = (rand i (t)+ c (X.,t) ) Xi +j aij Xj

for clarity take j aij Xj = a / N j Xj = a X

Stochastic Generalized Lotka-Volterra

d Xi = (rand i (t)+ c (X.,t) ) Xi +j aij Xj

Assume Efficient market: P(rand i (t) )= P(rand j (t) )

for clarity take j aij Xj = a / N j Xj = a X

Stochastic Generalized Lotka-Volterra

d Xi = (rand i (t)+ c (X.,t) ) Xi +j aij Xj

Assume Efficient market: P(rand i (t) )= P(rand j (t) )

=> THEN the Pareto power law P(Xi ) ~ X i –1-

holds with independent on c(w.,t)

for clarity take j aij Xj = a / N j Xj = a X

Stochastic Generalized Lotka-Volterra

d Xi = (rand i (t)+ c (X.,t) ) Xi +j aij Xj

Assume Efficient market: P(rand i (t) )= P(rand j (t) )

=> THEN the Pareto power law P(Xi ) ~ X i –1-

holds with independent on c(w.,t)

for clarity take j aij Xj = a / N j Xj = a X

Proof:

d Xi = (rand i (t)+ c (X.,t) ) Xi + a X

d X = c (X.,t) ) X + a X

Denote x i (t) = Xi (t) / X(t)

Then dxi (t) = dXi (t)/ X(t) + X i (t) d (1/X)

=dXi (t) / X(t) - X i (t) d X(t)/X2

= (randi (t) –a ) xi (t) + a

= [randi (t) Xi +c(w.,t) Xi + aX ]/ X

-Xi /X [c(w.,t) X + a X ]/X

= randi (t) xi + c(w.,t) xi + a

-x i (t) [c(w.,t) + a ] =

dxi (t) = (ri (t) –a ) xi (t) + a of Kesten type: d x= (t) x +

and has constant negative drift !

Power law for large enough xi : P(xi ) d xi ~ xi -1-2 a/D d xi

Even for very unsteady fluctuations of c; X

dxi (t) = (ri (t) –a ) xi (t) + a of Kesten type: d x= (t) x +

and has constant negative drift !

Power law for large enough xi : P(xi ) d xi ~ xi -1-2 a/D d xi

In fact, the exact solution is: P(xi ) = exp[-2 a/(D xi )] xi -1-2 a/D

Even for very unsteady fluctuations of c; X

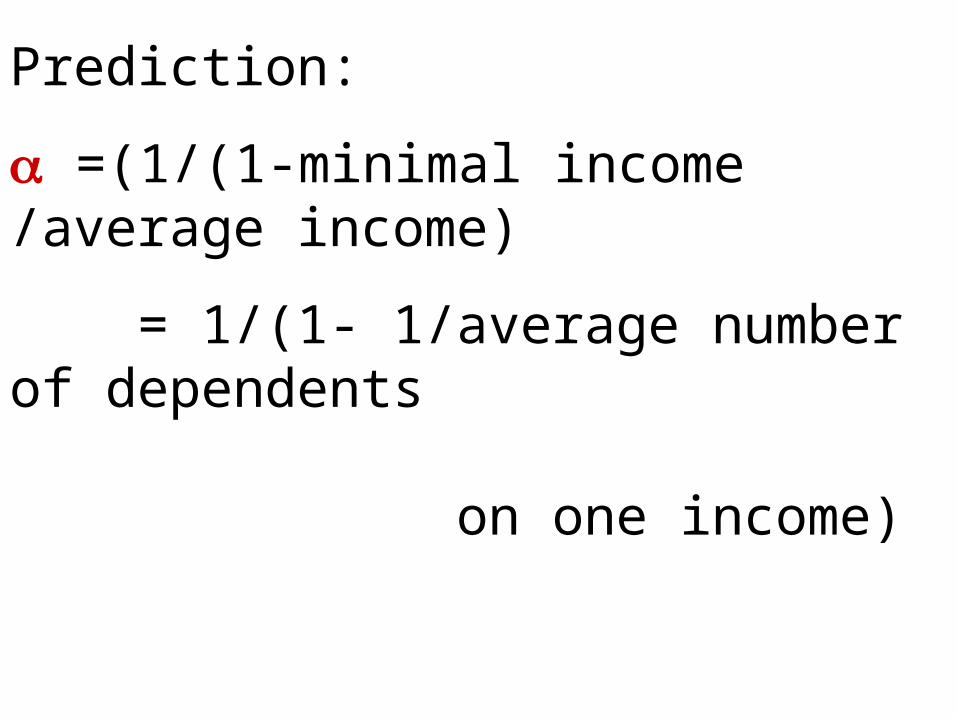

Prediction:

=(1/(1-minimal income /average income)

Prediction:

=(1/(1-minimal income /average income)

= 1/(1- 1/average number of dependents on one income)

Prediction:

=(1/(1-minimal income /average income)

= 1/(1- 1/dependents on one income)

= 1/(1- generation span/ population growth)

Prediction:

=(1/(1-minimal income /average income)

= 1/(1- 1/dependents on one income)

= 1/(1- generation span/ population growth)

3-4 dependents at each moment Doubling of population every 30 years minimal/ average ~ 0.25-0.33 (ok US, Isr)

Prediction:

=(1/(1-minimal income /average income)

= 1/(1- 1/dependents on one income)

= 1/(1- generation span/ population growth)

3-4 dependents at each moment Doubling of population every 30 years minimal/ average ~ 0.25-0.33 (ok US, Isr) => ~ 1.3-1.5 ; Pareto measured ~ 1.4

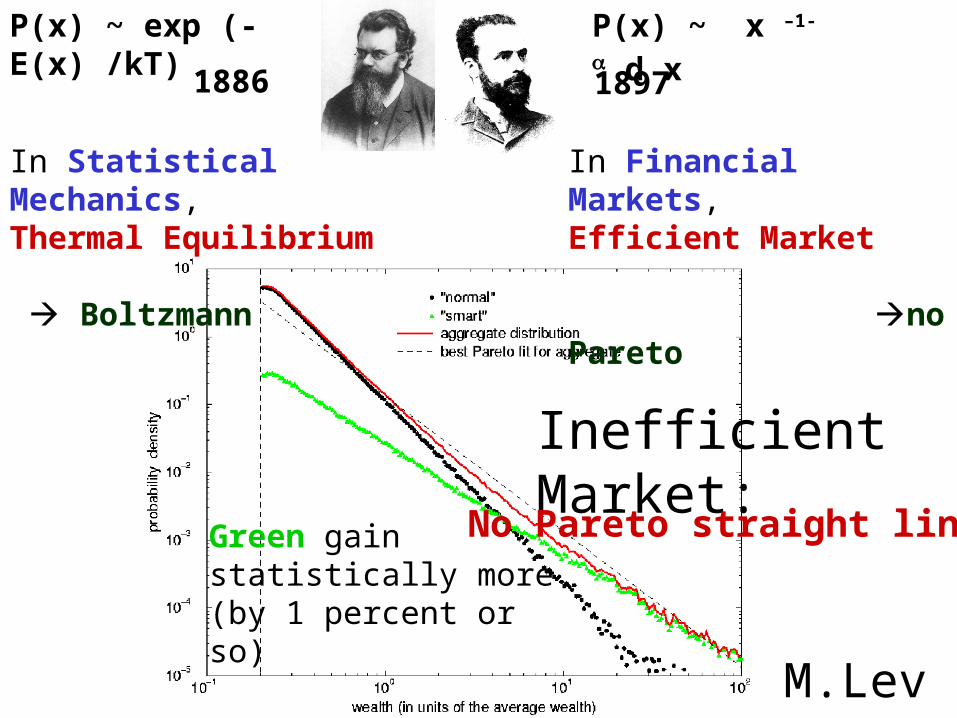

Inefficient Market:

Green gain statistically more (by 1 percent or so)

No Pareto straight line

In Statistical Mechanics, Thermal Equilibrium Boltzmann

In Financial Markets, Efficient Market no Pareto

P(x) ~ exp (-E(x) /kT)

1886

P(x) ~ x –1- d x

1897

Inefficient Market:

Green gain statistically more (by 1 percent or so)

No Pareto straight line

M.Levy

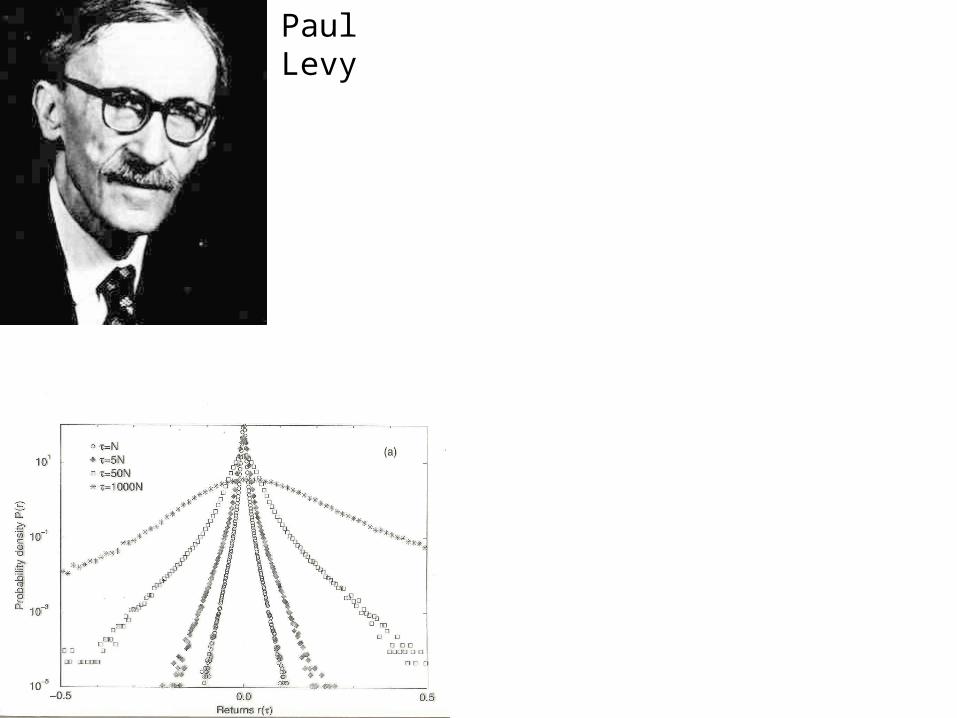

Market Fluctuations

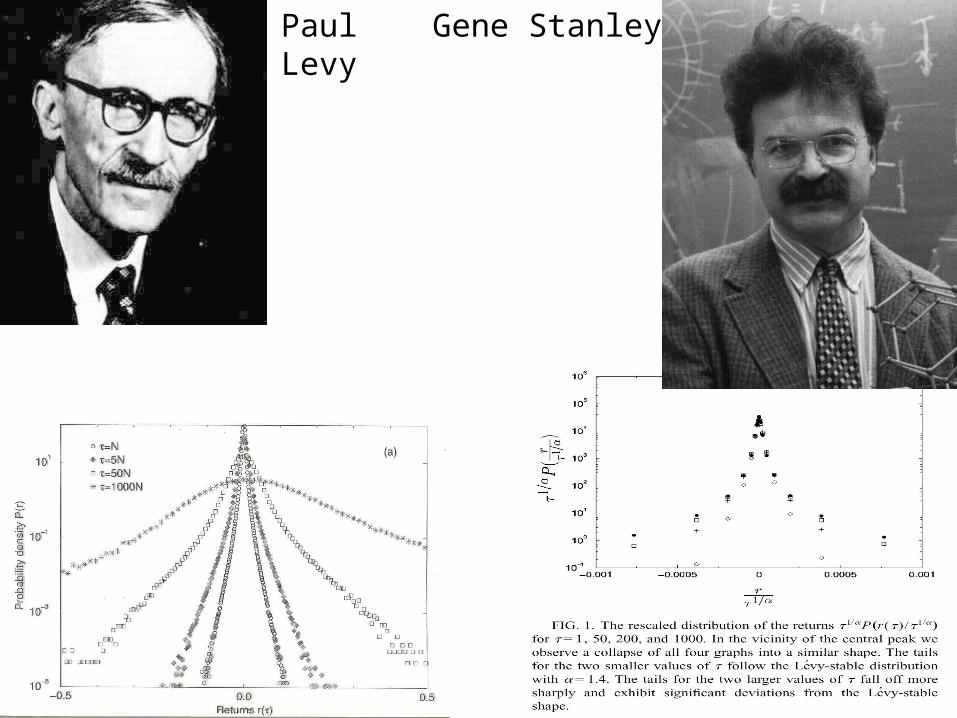

Paul Levy

Paul Levy Gene Stanley

Paul Levy Gene Stanley

(see him here in person)

M. Levy

One more puzzle:

For very dense (trade-by-trade) measurements

and very large volumes the tails go like 2

One more puzzle:

For very dense (trade-by-trade) measurements

and very large volumes the tails go like 2

Explanation:

Volume of trade = minimum of ofer size and ask size

P(volume > v) = P(ofer > v) x P(ask >v)

= v –2

P(volume = v) d v = v –1-2 d v as in measurement

Conclusion

The 100 year Pareto puzzle

Is solved

by combining

The 100 year Logistic Equation of Lotka and Volterra

With the 100 year old statistical mechanics of Boltzmann