philanthropic giving index - lilly family school of ... · in the december 2009 philanthropic...

TRANSCRIPT

Philanthropic Giving Index

December 2009

We gratefully acknowledge

The staff of the Center for Survey Research at Indiana University,

for survey administration and coding of data, and

to our panel of professional fundraisers who make this study possible.

2

In the December 2009 Philanthropic Giving Index (PGI) survey, fundraisers were slightly more

optimistic about the climate for fundraising than they were six months ago (8.7 percent) and

slightly more optimistic than they were this time last year (9.8 percent). The Present Situation

Index (PSI) shows a 1.7 percent decrease over last year‟s index, and fundraisers are slightly more

optimistic about future fundraising with the Expectations Index showing a 20.7 percent increase

from one year ago.

Key Findings for the December 2009 Philanthropic Giving Index, which included a series

of questions on the economy and giving:

The overall PGI was 71.1, an increase of 8.7 percent since Summer 2009 and up 9.8

percent from this time last year.

The PSI was 62.5, an increase of 7.7 percent from six months ago and down 1.7 percent

from one year ago. The Expectations Index, at 79.8, also increased 9.6 percent from six

months ago and 20.7 percent from a year ago.

Fundraisers from human services nonprofits are substantially less optimistic about the

current fundraising climate (PSI of 52.9) than other types of nonprofits.

Consultants who provide outside fundraising counsel to nonprofits are also less confident

about the current conditions for giving (PGI of 67.0) than other survey respondents.

Development officers from educational and religious organizations were the most

optimistic about the present climate.

The vast majority of the panel believes that the economy is having a negative impact on

fundraising, but fundraisers are less pessimistic about the impact of the economy on

fundraising six months from now (60.7 percent currently pessimistic and 42.5 percent six

months from now). Very few fundraisers (20 percent) have positive views about the

current economic impact compared to those expecting a positive economic impact six

months from now (45.9 percent).

With the exception of direct mail, fundraisers in the latest survey experienced less

success with all types of fundraising techniques in December 2009 than they predicted in

the first half of 2009.

Fundraisers reported statistically significantly less success with planned giving, corporate

gifts, Internet, and e-mail solicitations than they predicted just six months ago.

Approximately 63 percent of fundraisers said their organizations were projecting an

increase (31.2 percent) or no change at all (31.9 percent) in revenue generated from

fundraising when preparing the budget for the next fiscal or calendar year.

Just under 40 percent of fundraisers reported fewer repeat donors during the past two

years. One-third of fundraisers reported no shift either way in the number of donors that

gave year to year.

Most of the professional fundraisers reported that retaining current donors was a high

priority for their organization (92.5 percent). Nearly 70 percent of fundraisers made it a

medium to high priority for their organization to cultivate prospective donors. Only, 69.7

percent of fundraisers reported that cultivating prospective donors was a high priority for

their organization.

Philanthropic Giving Index December 2009

3

About the Philanthropic Giving Index

The Philanthropic Giving Index (PGI) is a semiannual study of the climate for charitable giving

and fundraising in the United States. It is similar to the Consumer Confidence Index, but for

charitable giving. The survey was fielded between October and November of 2009 and mailed to

a panel of 404 fundraising executives of nonprofits and fundraising consultants nationwide by

the Indiana University Center for Survey Research in Bloomington, Indiana, on behalf of the

Center on Philanthropy. Initially the panel was contacted by mail and then by follow-up e-mails.

Of the fundraisers and consultants receiving the survey, 146 returned the questionnaire, 1 was

not eligible, and 3 refused to participate; making the overall response rate 37.1 percent. The

panel represents a cross-section of the nonprofit sector in terms of subsectors (e.g., health,

education, or arts organizations), revenue size, and donor base.

The study produces three indexes. The Philanthropic Giving Index is the overall assessment of

the fundraising climate in the U.S. The Present Situation Index reflects professional fundraisers‟

view of the current fundraising climate, and the Expectations Index indicates what the panel of

fundraisers thinks the philanthropic climate will look like in the upcoming six months.

As with the Consumer Confidence Index, the PGI indexes range from 0 to 100, with higher

scores indicating more optimistic attitudes about the climate for giving. Table 1 lists the indexes

for the December 2009 wave and shows the percentage change from the two previous waves.

Table 2 shows the changes since the survey began; these changes are graphed in Figure 1.

Detailed Findings for the December 2009 Philanthropic Giving Index

The Philanthropic Giving Index for December 2009 is 71.1, an increase of 8.7 percent from six

months ago. These fundraisers are slightly more optimistic about the charitable giving climate

than they were last year (see Table 1). The Present Situation Index is 62.5, a 7.7 percent increase

from Summer of 2009 and a 1.7 percent decrease from one year ago. The Expectations Index is

79.8, a 9.6 percent increase from six months ago and a 20.7 percent increase from a year ago. All

indications suggest the fundraising climate is improving and is expected to remain this way for

the next six months.

Table 1 Values and Changes in Indexes Over the Past Year

December 2009

Change Since Summer 2009

Change Since December 2008

Philanthropic Giving Index (PGI) (overall assessment of climate for

fundraising) 71.1 8.7% 9.8%

Present Situation Index (PSI) (assessment of current climate for

fundraising) 62.5 7.7% -1.7%

Expectations Index (assessment of fundraising climate

in the next six months) 79.8 9.6% 20.7%

4

0

20

40

60

80

100

Philanthropic Giving Index Present Situation Index Expectations Index

Figure 1: Philanthropy Giving Index

Main Indexes Over Time

5

Table 2: Values of Philanthropic Giving Index Over Time

Report Date

Philanthropic

Giving Index

Present Situation

Index Expectations Index

Summer 98 88.8 87.2 90.4

December 98 87.1 86.2 87.9

Summer 99 86.8 85.5 88.0

December 99 94.6 93.6 95.6

Summer 00 94.5 93.7 95.3

December 00 92.0 90.5 93.5

Summer 01 91.1 89.9 92.3

December 01 83.6 79.0 88.2

Summer 02 89.0 83.8 94.1

December 02 77.7 69.7 85.8

Summer 03 72.3 63.0 81.6

December 03 83.3 75.5 91.1

Summer 04 90.6 87.4 93.8

December 04 89.7 88.2 91.3

Summer 05 85.2 82.2 88.2

December 05 86.3 84.9 87.6

Summer 06 88.9 86.6 91.2

December 06 87.6 85.8 89.5

Summer 07 87.5 85.4 89.7

December 07 88.8 88.0 89.7

Summer 08 82.8 81.7 83.9

December 08 64.8 63.6 66.1

Summer 09 65.4 58.0 72.8

December 09 71.1 62.5 79.8

6

Indexes by Subsector

Across all subsectors, development officers were noticeable more optimistic about the

fundraising climate in the next six months than the current fundraising climate (see Figure 2).

Fundraisers working in religious and educational organizations were the most optimistic about

the current fundraising climate and were also highly optimistic about the fundraising climate six

months from now. Nonprofit consultants and development officers working in human services

organizations were noticeably less optimistic about the current fundraising climate, rating the

Present Situation Index 8 to 10 points lower than their peers in other organizations. Fundraisers

working in public benefit, environment/animal, and international (PEAI) nonprofits were the

least optimistic about the future fundraising climate than their counterparts working in other

types of organizations.

Figure 2: Indexes by Subsector

December 2009

* PEAI: Public Benefit, Environment/Animal and International nonprofits

^ Arts: Results are not statistically meaningful because the sample size was less than 10

86.7

70.6

81.5

75.5

77.1

87.3

79.6

79.8

58.9

60.0

65.1

64.3

52.9

75.6

54.3

62.5

72.8

65.3

73.3

69.9

65.0

81.4

67.0

71.1

Arts^

PEAI*

Education

Health

Human Services

Religion

Consultants

Total

Index Values

Philanthropic Giving Index Present Situation Index Expectations Index

7

Effectiveness of Solicitation Techniques

As shown in Figure 3, fundraisers expect greater success with all solicitation techniques six

months from now, with the exception of direct mail. Fundraisers continue to report major gifts

and direct mail as the most successful fundraising techniques (69.7 percent and 66.7 percent

respectively). However, fundraisers believe that they will have more success with major gifts

(76.6 percent) and less success with direct mail in the next six months (65.1 percent). On the

other hand, development officers predict they will have more success with planned giving,

special events, foundation grants and telephone solicitations in the next six months than currently

reported. Few fundraisers report success with e-mail (21.3 percent), Internet (28.4 percent), or

corporate giving (29.2 percent).

76.6

69.9

55.9

46.9

65.1

45.1

34.0

35.0

37.1

69.7

61.4

54.7

44.8

66.7

34.8

29.2

28.4

21.3

Major Gifts

Planned Giving

Special Events

Foundations

Direct Mail

Telephone

Corporate Gifts

Internet

Percentage

Figure 3: Percentage of Respondents Who Rated Fundraising

Techniques as Successful or Somewhat Successful

December 2009

Current Future

8

Effectiveness of Solicitation Techniques Over Time

As Figure 4 shows, since the start of the recession in December 2007 the economy has affected

various types of solicitation techniques differently. Fewer fundraisers are reporting success with

major gifts, planned giving, and foundation grants. Development officers are reporting slight

increases in reported success with major gifts and planned giving compared to six months ago

(69.7 percent and 61.4 percent respectively) but they still remain at historic lows. In addition, the

reported success with foundation grants has fallen to 44.8 percent, one of its lowest levels. The

average reported success with foundation grants since the study began in summer of 1998 is

63.5. All indications suggest that direct mail still remains one of the most successful techniques

for raising philanthropic dollars for nonprofits. For this wave of the PGI, the reported success

with direct mail is 66.7; whereas the average reported success with direct mail since the study

began in Summer 1998 is 66.5.

0

20

40

60

80

100

Per

cen

tage

Figure 4: Percentage Reporting Success Over Time With

Major Gifts, Direct Mail, Foundation Grants, and

Planned Giving

Major Gifts Direct Mail Foundation Grants Planned Giving

9

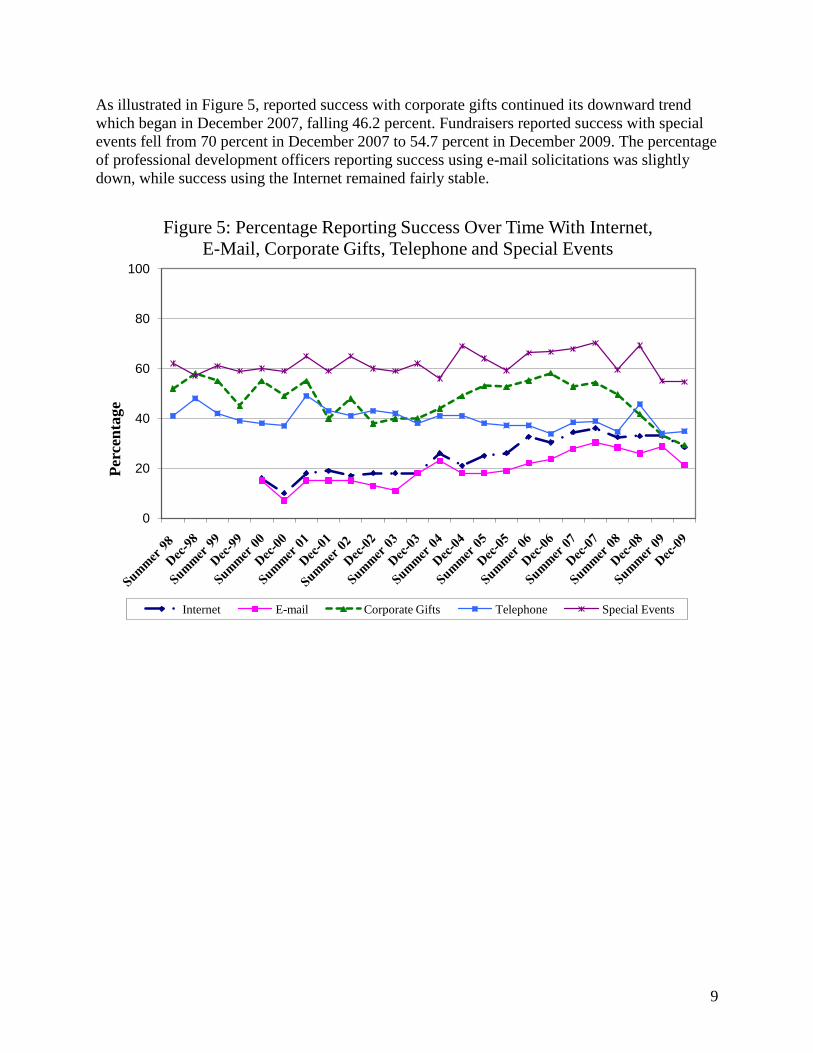

As illustrated in Figure 5, reported success with corporate gifts continued its downward trend

which began in December 2007, falling 46.2 percent. Fundraisers reported success with special

events fell from 70 percent in December 2007 to 54.7 percent in December 2009. The percentage

of professional development officers reporting success using e-mail solicitations was slightly

down, while success using the Internet remained fairly stable.

0

20

40

60

80

100

Per

cen

tage

Figure 5: Percentage Reporting Success Over Time With Internet,

E-Mail, Corporate Gifts, Telephone and Special Events

Internet E-mail Corporate Gifts Telephone Special Events

10

Predicted Versus Actual Levels of Success, by Fundraising Technique

The panel of professional fundraisers was asked six months ago (Summer 2009) to predict the

level of success they would have with various fundraising techniques. Here we examine their

predicted success with their current success as reported in December 2009 for those who

responded to both surveys. For nearly every type of fundraising technique, development officers

anticipated more success than they reported with the surprising exception of direct mail. Six

months ago, only 59.6 percent of fundraisers thought they would have success with direct mail in

the coming months, but in December of 2009, 66.7 percent of these same fundraisers reported

success. On the other hand, development officers anticipated much more success with corporate

gift fundraising than reported in December 2009. Fundraisers reported statistically significantly

less success with planned giving, corporate gifts, Internet, and e-mail solicitations than they

predicted just six months ago.

Note: Planned giving, corporate gifts, Internet, and e-mail solicitations are statistically significantly less successful

currently than predicted to be just six months ago.

69.7

61.4

66.7

44.8

54.7

29.2

34.8

28.4

21.3

73.9

66.5

59.6

44.5

54.6

34.8

38.8

42.7

37.4

Major Gifts

Planned Giving

Direct Mail

Foundation Grants

Special Events

Corporate Gifts

Telephone

Internet

Percentage

Figure 6: Predicted (Summer 2009) Versus Reported

(December 2009) Success of Fundraising Techniques

(of those that responded to both surveys)

Predicted Summer 2009 Reported December 2009

11

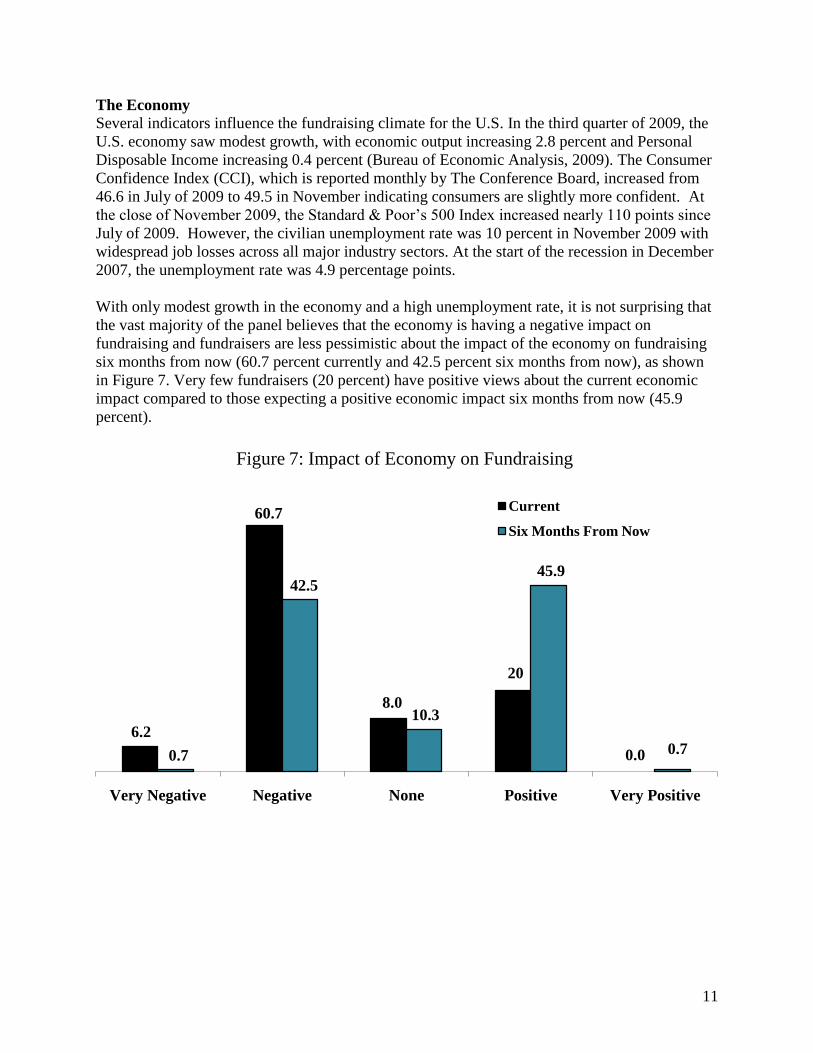

The Economy

Several indicators influence the fundraising climate for the U.S. In the third quarter of 2009, the

U.S. economy saw modest growth, with economic output increasing 2.8 percent and Personal

Disposable Income increasing 0.4 percent (Bureau of Economic Analysis, 2009). The Consumer

Confidence Index (CCI), which is reported monthly by The Conference Board, increased from

46.6 in July of 2009 to 49.5 in November indicating consumers are slightly more confident. At

the close of November 2009, the Standard & Poor‟s 500 Index increased nearly 110 points since

July of 2009. However, the civilian unemployment rate was 10 percent in November 2009 with

widespread job losses across all major industry sectors. At the start of the recession in December

2007, the unemployment rate was 4.9 percentage points.

With only modest growth in the economy and a high unemployment rate, it is not surprising that

the vast majority of the panel believes that the economy is having a negative impact on

fundraising and fundraisers are less pessimistic about the impact of the economy on fundraising

six months from now (60.7 percent currently and 42.5 percent six months from now), as shown

in Figure 7. Very few fundraisers (20 percent) have positive views about the current economic

impact compared to those expecting a positive economic impact six months from now (45.9

percent).

6.2

60.7

8.0

20

0.00.7

42.5

10.3

45.9

0.7

Very Negative Negative None Positive Very Positive

Figure 7: Impact of Economy on Fundraising

Current

Six Months From Now

12

Figure 8 shows the average assessments of the current impact of the U.S. economy on

fundraising during each of the past seven years. Between 2004 and 2007, fundraisers in general

reported a more positive influence of the economy on fundraising. However, just over 90 percent

of fundraisers reported that the economy had a negative or very negative impact on fundraising

in 2008. The panel of fundraisers was slightly less pessimistic in 2009, where 76.5 percent

reported that the economy had a negative or very negative impact on fundraising. Nearly 2

percent reported that the economy had a positive impact on fundraising in 2008. This compares

to 13 percent of fundraisers that reported the economy is having a positive impact on fundraising

in 2009, suggesting that the panel of fundraisers is slightly more optimistic about the impact of

the economy on fundraising.

71.2

36 3628.9

35.3

90.3

76.5

9.5

21.128.2

21.6

23.5

7.7

10.6

19.5

42.935.9

49.643.5

2.2

13

Average

2003

Average

2004

Average

2005

Average

2006

Average

2007

Average

2008

Average

2009

Per

cen

tag

e

Figure 8: Current Impact of the U.S. Economy on Fundraising

Negative None Positive

13

Questions related to the economy

In the December 2009 edition of the Philanthropic Giving Index, we asked a series of questions

related to the impact of the economy on organizations. Figure 9 shows the change, if any, that

fundraisers are projecting in revenue generated from fundraising when preparing the budget for

the next fiscal or calendar year. Approximately 28 percent of fundraisers are projecting a

decrease in revenue generated from fundraising when preparing their budgets. This is slightly

less than the 35 percent of fundraisers who projected a decrease in Summer 2009. Nearly 31.2

percent of fundraisers reported an increase in revenue when preparing their budgets, an increase

of more than 10 percentage points when compared to Summer 2009. In comparison, 31.9 percent

of fundraisers are projecting no changes at all.

Table 3 shows that the majority of fundraisers that project a decrease in revenue (75.7 percent)

reported a decrease in revenue of between 1 and 15 percent. Nearly 80 percent of fundraisers that

are projecting an increase in revenue reported an increase of between 1 and 15 percent.

Table 3: Reported Change in Projected Revenue for the Next Fiscal or Calendar Year

Decrease of: Increase of:

1 to 5 percent 18.9 44.1

6 to 15 percent 56.8 35.3

16 to 25 percent 16.2 17.6

26 percent or more 8.1 2.9

TOTAL 100.0 100.0

34.7

38.9

19.2

7.2

28.3

31.9 31.2

8.7

Decrease No change at all Increase Don‟t know

Figure 9: Percent of Fundraisers Reporting the Projected Change

in Revenue Generated from Fundraising when Preparing the

Budget for the Next Fiscal or Calendar Year

Summer 2009

December 2009

14

The panel of fundraisers was also asked about new activities or initiatives implemented in 2009

that increased organizational revenue (see Figure 10). The majority of fundraisers, 84 percent,

reported that a focus on stewardship and communication with donors led to increased

organizational revenue. In addition, 83.7 percent set organizational priorities and made tough

budget decisions that generated new revenue. Only 51.1 percent of fundraisers wrote grant

proposals for foundation and corporate grants. Whereas, 38.9 percent accepted in-kind donations

and 31.2 percent partnered with community organizations. However, only one-fifth of

fundraisers reported receiving American Recovery and Reinvestment Act funding in 2009.

Approximately 23 percent of fundraisers reported other activities or initiatives such as hiring

new staff with specific skill sets, increased solicitation of gifts and intensified communication

with donors.

20.5

22.6

24.4

31.2

38.9

51.1

83.7

84.0

Received American Recovery and

Reinvestment Act Funding

Other

Increase secondary sources of income

Partner with community organizations

Accept in-kind donations

Write grant proposals

Set organizational priorities and tough

budget decisions

Focus on stewardship and

communication with donors

Figure 10: Percent of Fundraisers Reporting the Types of New

Activities Implemented that Increased Organizational Revenue in

2009

15

Figure 11 shows the percentage of fundraisers reporting a change in the number of donors that

gave year to year, during the past two years. Just under 40 percent of fundraisers reported fewer

repeat donors during the past two years. One-third of fundraisers reported no shift either way in

the number of donors that gave year to year. About 27 percent, however, did report an increase in

the number of repeat donors during the past two years. This amounts to a decline in the number

of donors that gave year to year.

39.6

33.3

27.1

Fewer repeat donors No shift either way More repeat donors

Figure 11: Percentage of Fundraisers Reporting the Change in the

Number of Donors that Gave Year to Year

16

The panel of fundraisers was also asked about how much priority their organization has devoted

to retaining current donors, cultivating prospective donors, and reengaging lapsed donors in 2009

(see Figure 12). Most of the professional fundraisers reported that retaining current donors was a

high priority for their organization (92.5 percent). Nearly 70 percent of fundraisers made it a

high priority for their organization to cultivate prospective donors. Only, 69.7 percent of

fundraisers reported that cultivating prospective donors was a high priority for their organization.

In comparison, only 56.3 percent of development officers made reengaging lapsed donors a high

priority for their organization. This indicates that most fundraisers are focusing their primary

efforts on retaining current donors and cultivating prospective donors.

Most of the professional fundraisers reported that giving to their organization was down and that

they were experiencing uncertainty about the fundraising climate. However, a fair amount

reported the economy was having a mixed effect on fundraising for their organization.

Fundraisers on our panel said:

“Annual giving gift range donors have increased in number, but dollars per donation have

decreased. The number of major gift range donors, especially in the $1.0 million plus

range have dropped dramatically from prior years.”

“As fund raising has become more challenging we have invested more energy in fund

raising and donor cultivation. We had a development consultant assess our methods

which resulted in some improved techniques.”

0.75.5 6.8

92.5

0.75.5

24.1

69.7

1.4

13.4

28.9

56.3

Not a priority Low priority Medium priority High priority

Figure 12: Percentage of Fundraisers Reporting the Level of

Priority Their Organization has Devoted to Retaining Current

Donors, Cultivating Prospective Donors, and Reengaging Lapsed

Donors

Retaining Current Donors

Cultivating Prospective Donors

Reengaging Lapsed Donors

17

“Foundation funding is most directly impacted negatively. Also, corporations,

particularly banks, are avoiding high-end events.”

“Organizations that had strong relationships (good reporting and communication whether

by mail or in person) with donors prior to the economic downturn are doing well or at

least remaining stable.”

“We continue to see organizations with comprehensive, balanced development programs

that are committed to best practices are the ones that do well. The ones that struggle don't

embrace best practices. They often have a narrow donor base.”

“Planned Giving has improved (at least distributions of gifts) as the real estate market has

improved and homes are selling faster and for better prices than 12 months ago.”

“While we are not losing donors, the amount that individual donors are contributing is

less per donor than in the past.”

The Impact of the Economy by Subsector, Revenue, and Location of Donor Support

Overall, there were few differences in how the economy impacted fundraising among the various

types of nonprofits. Below we discuss those few differences.

Subsector

Fundraisers from PEAI and health organizations were the most likely to report that the

economy was having a negative impact on fundraising (93.3 percent and 73.7 percent,

respectively).

Fundraisers from educational and religious nonprofits were the most likely to report a

projected increase in revenue generated from fundraising when preparing the budget for

the next fiscal or calendar year.

Approximately 50 percent of consultants are projecting a decrease in revenue generated

from fundraising when organizations they consult with are preparing their budgets.

Consultants and fundraisers from educational organizations reported fewer repeat donors

during the past two years (62.5 percent and 40.6 percent respectively).

Religious organizations were more likely to report an increase in the number of repeat

donors during the past two years (40.9 percent).

Revenue

Small organizations, those with revenue between $1 and $5 million, were most likely to

report that the economy was having a negative impact on fundraising.

Medium organizations, those with revenue between $10 and $50 million were the most

likely to report a projected increase in revenue generated from fundraising when

preparing the budget for the next fiscal or calendar year.

Medium organizations, those with revenue between $10 and $50 million were the most

likely to report fewer repeat donors during the past two years (57.9 percent).

Larger nonprofit organizations, those with revenue more than $50 million were the most

likely to report more repeat donors during the past two years (45.8 percent).

18

Location of Donor Support

More than three-quarters of organizations with a regional donor base reported that the

economy was having a negative impact on fundraising (76.3 percent).

Nearly one-third of organizations with a national donor based report a projected decrease

in revenue generated from fundraising when preparing the budget for the next fiscal or

calendar year.

Nonprofit organizations with a national donor base were the most likely to report fewer

repeat donors during the past two years (43.3 percent).

Capital Campaign

Just one-third of nonprofits reported their organization was currently conducting a capital

campaign. Education and health organizations were the most likely to be involved in a capital

campaign (35.5 percent and 57.9 percent, respectively). Religious organizations (9.9 percent),

human services organizations (20.0 percent) followed by public-benefit, environment/animal,

and international (20.0 percent) were the least likely to be in a capital campaign. Local

organizations (36.2 percent) and organizations with more than $50 million in revenue were also

more likely to be involved in a capital campaign (54.1 percent).

19

Results of Fundraising Techniques by Subsector

Success with various fundraising methods differs widely by the type of organization. Table 4

shows the percentage of fundraisers that reported current success with various fundraising

techniques and Table 5 presents the predicted success rates six months from now. „*‟ Denotes

whether or not there were statistical differences within each column as well as the level of

significance.

Table 4: The Percentage of Respondents Reporting Success with Fundraising Techniques by Subsector

(%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

ACH^ 77.8 62.5 87.5*** 66.7 66.7 33.3 55.6 25 25

PEAI 64.3 13.3* 60 53.3 46.7 28.6 60 14.3 35.7

ED 84.4* 75.0*** 46.4 65.6 81.3 38.7 48.4 30 38.7

HE 55.6 12.5*** 64.7 66.7 52.6 42.1 42.1 11.1 22.2

HS 65 20 55 25.0*** 50 30 55 25 20

RE 77.3 27.3 31.8 86.4 85.7 13.6 36.4 13.6 27.3

CS 42.3* 20 65.4 57.7 80.8 23.1 30.8 23.1 28

Total 66.7 34.8 54.7 61.4 69.7 29.2 44.8 21.3 28.4

Note: ACH = Arts, Culture, and Humanities; PEAI = Public Benefit, Environment, Animal, and International;

ED = Education; HE= Health; HS = Human Services; RE = Religion; CS = Consultants

Note: Statistical significance tests determined by the means; *p<.05, **p<.01, ***p<.001

^ Results are not statistically meaningful since the sample size is less than 10

Table 5: The Percentage of Respondents Predicting Success with Fundraising Techniques Six Months

from Now by Subsector (%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

ACH^ 77.8 62.5 87.5** 77.8 100 44.4 33.3 50 37.5

PEAI 66.7 26.7** 53.3 53.3 57.1 42.9 60 28.6 46.2

ED 78.1 75.0*** 45.2 81.3 81.3 41.9 54.8 45.2 43.3

HE 52.6 23.5 61.1 63.2 63.2 42.1 47.4 15.8 26.3

HS 55 35 60 45.0*** 75 30 55 45 35

RE 72.7 45.5 45.5 86.4 81.8 18.2* 40.9 27.3 31.8

CS 53.8 36 65.4 69.2 76.9 26.9 30.8 34.6 40

Total 65.1 45.1 55.9 69.9 76.6 34.0 46.9 35.0 37.1

Note: ACH = Arts, Culture, and Humanities; PEAI = Public Benefit, Environment, Animal, and International; ED =

Education; HE= Health; HS = Human Services; RE = Religion; CS = Consultants

Note: Statistical significance tests determined by the means; *p<.05, **p<.01, ***p<.001

^ Results are not statistically meaningful since the sample size is less than 10

Arts, Culture, and Humanities

Fewer than 10 respondents from arts, culture, and humanities organizations responded to this

wave of the PGI. Therefore, the reader should exercise caution when interpreting these numbers

given the smaller sample size.

20

Public-Benefit, Environment/Animal, and International (PEAI)

Fundraising professionals from public-benefit, environment/animal, and international (PEAI)

nonprofits reported the most success with direct mail. This success is predicted to increase

slightly six months from now. Along with direct mail, fundraisers had the most success with

special events and foundation grants. However, the success with special events is expected to

decrease six months from now. PEAI fundraisers as a group were statistically significantly less

likely to report success with telephone solicitations; however, this success is expected to

statistically significantly increase in the future. The least successful fundraising techniques

reported were telephone solicitations, corporate gifts, and e-mail solicitations. PEAI fundraisers

are optimistic about their future success in major gifts and corporate fundraising. Finally, public-

society benefit, environment/animals, and international organizations as a group were the least

likely, 2.6 percent, to be involved in a capital campaign.

Education

Fundraisers from educational organizations reported statistically significantly more success than

their peers with using direct mail and telephone solicitations as fundraising techniques. This

success with direct mail solicitations is predicted to decrease six months from now, but

fundraisers still remain more confident than any other groups. Development officers from

educational organizations also reported planned giving and major gifts as their most successful

fundraising techniques. These fundraisers are optimistic about their future success with planned

giving. E-mail and Internet continue to be the least successful fundraising techniques reported by

these fundraisers.

Health

Fundraisers working in health organizations report the most success with special events and

planned giving, while they report statistically significantly less success with telephone

fundraising than their peers working in other types of organizations. Development officers from

health organizations reported their least successful fundraising techniques as the telephone, e-

mail and Internet. Health fundraisers are more optimistic about their fundraising success with

telephone solicitations, major gifts, foundation grants, e-mail and Internet solicitations six

months from now than they are currently experiencing. Finally, health organizations were the

most likely to be involved in a capital campaign (57.9 percent).

Human Services

Development professionals from human services organizations report the most success with

direct mail, special events and foundation grants. However, these fundraisers experienced

statistically significantly less success with planned giving than their peers working in other types

of organizations. These fundraisers also predict statistically significantly less success with

planned giving six months from now than their peers. In addition, human services fundraisers

predict more success with major gifts six months from now than they are currently experiencing.

Human service fundraisers are less optimistic about their success with telephone, e-mail and

Internet solicitations.

21

Religion

Fundraisers from religious organizations reported the most success with planned giving and

major gifts than their peers working in other types of organizations. Fundraisers predict less

success with major gifts six months from now. These fundraisers also reported success with

direct mail, however, the success with this technique is expected to decrease six months from

now. These fundraisers are the least likely to report fundraising success with corporate gifts,

though this is expected to statistically significantly increase in the future. Development personnel

from religious organizations also predict success with telephone and special events fundraising in

six months.

Consultants

Consultants working for all types of nonprofit organizations report the most success with major

gifts, and this success is expected to decrease six months from now. These fundraisers also had a

statistically significantly lower level of reported success with direct mail than their peers.

However, this success is expected to increase six months from now. Consultants report the least

success with telephone, corporate gifts, and e-mail fundraising. Consultants predict they will

have the most success with major gifts and planned giving six months from now and they also

predict low levels of success with corporate gifts, foundation grants and e-mail solicitations.

22

Results of Fundraising Techniques by Revenue

Success with various fundraising techniques also differs by the revenue size of the organization.

Table 6 shows the percentage of fundraisers that reported current success with various

techniques by revenue size. Table 7 details the predicted success of various techniques six

months from now. „*‟ Denotes whether or not there were statistical differences within each

column as well as the level of significance.

Table 6: Percentage of Respondents Reporting Success with Fundraising Techniques by Revenue Size

(%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

<$1 mil 79.2 21.7 66.7 54.2 66.7 26.1 45.8 19 36.4

$1-5 mil 71.4 42.9 47.6 28.6*** 42.9** 14.3 47.6 4.8 14.3

$5-10 mil 53.3 26.7 66.7 60 64.3 33.3 26.7 6.7 13.3

$10-50 mil 83.3 38.9 55.6 78.9 84.2 57.9 84.2** 47.4 52.6

> $50 mil 65.2 50.0 38.9 82.6*** 70.8 30.4 39.1 22.7 22.7

Total 71.2 36.3 55.2 60.7 65.6 31.6 49.0 20.4 28.2

Note: Statistical significance tests determined by the means

Note: * indicates statistical significance *p<.05, **p<.01, ***p<.001

Table 7: The Percentage of Respondents Predicting Success with Fundraising Techniques Six Months

From Now by Revenue Size (%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

<$1 mil 75 43.5 66.7 62.5 82.6 39.1 54.2 31.8 36.4

$1-5 mil 61.9 42.9 52.4 52.4** 52.4* 19 52.4 23.8 19

$5-10 mil 53.3 26.7 53.3 60 73.3 53.3 40 20 26.7

$10-50 mil 73.7 55.6 47.4 84.2 89.5 52.6 73.7* 52.6 61.1

> $50 mil 66.7 60.9 52.4 87.5** 83.3 34.8 47.8 43.5 34.8

Total 66.9 47.0 55 69.9 76.4 38.6 53.9 35 35.3

Note: Statistical significance tests determined by the means

Note: * indicates statistical significance *p<.05, **p<.01, ***p<.001

$1 million

Fundraisers from small organizations, those with revenues of less than $1 million, report more

success with direct mail, special events and major gifts fundraising. These organizations report

less success with these techniques six months from now, with the exception of major gifts, which

fundraisers predict more success in the future. Small-sized organizations are less optimistic

about their success with e-mail and Internet solicitations six months from now.

$1 million to $5 million

Fundraisers from medium-sized organizations, those with revenues in the $1 million to $5 million

range, report the most success with direct mail. The least successful techniques reported were e-

mail, telephone and Internet giving. Medium-sized organizations are expecting statistically

significantly less success with planned giving and major gifts. In addition, they are predicting

23

statistically significantly less success with these techniques than all other organizations six

months from now.

$5 million to $10 million

Development personnel from organizations with revenues between $5 million and $10 million

report the most success with special events and major gifts. The least successful techniques

reported were e-mail and Internet giving. These organizations predict less success with corporate

gifts than their peers from other types of organizations, however this is expected to increase six

months from now. These organizations predict more success with major gifts and planned

giving and less success with Internet, telephone and e-mail giving six months from now.

$10 million to $50 million

Fundraisers from organizations with revenues between $10 million and $50 million report

statistically significantly more success with foundations, followed by direct mail and major gifts,

as the most successful fundraising techniques. These fundraisers had the most success of all

organizations with direct mail and foundation grants. The least successful type of fundraising

reported was telephone solicitations. These organizations predict more success with major gifts,

planned giving, and foundations and less success with telephone and e-mail giving six months

from now.

$50 million and above

Fundraisers from the largest nonprofits, those with revenues of more than $50 million report

statistically significantly more success with planned giving than their peers from other types of

organizations. In fact, the very largest organizations expect this success to continue six months

from now. These organizations report success with major gifts and direct mail and less success

with Internet, corporate, and e-mail giving. Fundraisers from the largest nonprofits are the most

optimistic about their success with major gifts and planned giving and least optimistic about their

success with Internet and corporate giving six months from now.

24

Results of Fundraising Techniques by Donor Base

Success rates with fundraising techniques also vary by the location of the organization‟s donor

base. Table 8 outlines the percentage of fundraisers reporting success with various fundraising

techniques by where their donor base is located. Table 9 presents predicted success rates six

months from now. „*‟ Denotes whether or not there were statistical differences within each

column as well as the level of significance.

Table 8: The Percentage of Respondents Reporting Success with Fundraising Techniques by Location

of Donor Base (%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

Local 60 25 73.9*** 41.3*** 61.7 32.6 51.1 15.9 20.5

Regional 76.3 31.6 50 68.4 64.9 34.2 50 10.5 18.4

National 82.9 61.8 22.6 82.9 77.1 23.5 41.2 39.4 50

Total 72 37.9 52.2 62.2 67.2 30.5 47.9 20.9 28.4

Note: Statistical significance tests determined by the means

Note: * indicates statistical significance *p<.05, **p<.01, ***p<.001

Table 9: The Percentage of Respondents Predicting Success with Fundraising Techniques Six Months

from Now by Location of Donor Base (%)

Direct

Mail Telephone

Special

Events

Planned

Giving

Major

Gifts Corporate Foundation E-mail Internet

Local 55.3 35.6 68.1** 55.3** 71.7 41.3 46.8 35.6 34.1

Regional 68.4 44.7 54.1 71.1 76.3 36.8 57.9 23.7* 24.3*

National 82.9 64.7 33.3 88.6 82.9 26.5 47.1 47.1 52.9

Total 67.5 47 53.8 70 76.5 35.6 50.4 35 36.5

Note: Statistical significance tests determined by the means

Note: * indicates statistical significance *p<.05, **p<.01, ***p<.001

Local Donor Base

Fundraisers from organizations with a local donor base report statistically significantly more

success with special events, higher than all other organizations. However, they reported

statistically significantly less success with planned giving than their peers from other

organizations. They reported the least success with e-mail, telephone and Internet fundraising.

Development officers with a local donor base are expecting to have the most success with major

gifts and special events and the least success with e-mail and telephone fundraising six months

from now. In our sample, organizations with local donor bases were the most likely to be

involved in a capital campaign (36.2 percent).

Regional Donor Base

Development officers from organizations with a regional donor base report the most success with

planned giving and direct mail. The least successful techniques reported were e-mail and

telephone solicitations. They predict that e-mail and Internet giving will continue to be the least

successful techniques for fundraising; however this is statistically significant from what they are

currently experiencing. Planned giving and major gifts will continue to be the most successful

fundraising techniques in the next six months.

25

National Donor Base

Organizations with a national donor base had the most success of all organizations with direct

mail, major gifts and planned giving, and this success is expected to continue six months from

now. Fundraisers had more success with e-mail and Internet solicitations than corporate gifts.

Fundraisers from organizations with national donor bases predict that planned giving will

continue to be the most successful technique while corporate gifts and special events will be the

least successful six months from now.

For further information please contact:

Reema T. Bhakta

The Center on Philanthropy at Indiana University

550 West North Street, Suite 301

Indianapolis, IN 46202-3272

(317) 278-8996

http://www.philanthropy.iupui.edu

Also for a copy of previous PGI studies, please go to www.philanthropy.iupui.edu

PGI Summer 2009 – The Economy

PGI December 2008 – The Economy

PGI Summer 2008 – Special Events

PGI December 2007 – Planned Giving

PGI Summer 2007 – Internet Fundraising

PGI December 2006 – Pension Protection Act

PGI Summer 2006 – Fundraising after Gulf Coast Hurricanes