pharma's new productivity challenge: cost and - pharmafutures

TRANSCRIPT

FuturesPharma

Pharma’s NewProductivity Challenge:Cost and Choice in the US Market

PharmaFutures: Cost and Choice in the US Market

What is PharmaFutures?

PharmaFutures was created in 2003 as a dialogue between pharmaceutical executives,institutional investors and societal stakeholders to explore long-term value drivers for thepharmaceutical industry and its evolving social contract. e dialogues are based on thepremise that the industry and its investors thrive when it is seen as socially useful andthat if that perception falters, so does the business model. e fih PharmaFuturesdialogue began in November 2011 and focuses on one of the greatest challenges facingthe pharmaceutical industry today: that of persuading purchasers of pharmaceuticalproducts that these products offer value, not just to patients, but also to cash-strappedhealth systems seeking productivity gains and health improvements. is is a two yearglobal dialogue focusing on three major markets: Europe, emerging markets and the US.It will conclude with the publication of a global report on its findings in June 2013.

PharmaFutures provides insights for pharmaceutical executives and investors froma wide range of stakeholders and experts whose views about the social utility of theindustry help shape the industry’s licence to operate. PharmaFutures is based on theassumption that while pharmaceutical development lies in the hands of publicly quotedcompanies, it is imperative that investors, companies and global health experts betterunderstand one another’s viewpoints, the constraints each faces, and their room formanoeuvre when seeking to reconcile unmet need for medicines with the commercialimperatives of a business.

Methodology

e PharmaFutures dialogues are run by not-for-profit company, Meteos Ltd. eanalysis produced by PharmaFutures is drawn from an extensive process of research,interviews, synthesis and dialogue among participants. It relies on the willingness ofa wide-ranging group of experts to share their time and insights in semi-structuredinterviews, and of the members of the PharmaFutures Working Group to engage inopen and frank discussions. We would like to thank all those who contributed to thisprocess. A list of those interviewed appears in the Appendix. is report is written bySophia Tickell, with invaluable contributions from Charis Gresser, Becky Buell, JohnSchaetzl, Constance Mackworth-Young and Cassie Painter.

Disclaimer:

As a multi-stakeholder and collaborative project, the findings, interpretations and conclusionsexpressed herein may not necessarily reflect the views of all members of the Working Groupwho took part in this project in their personal capacity. e report was compiled for informationpurposes only and it is not a promotional material in any respect. e material does not offeror solicit the purchase or sale of any financial instrument. e report is not intended to provide,and should not be relied on for accounting, legal or tax advice or investment recommendations.

PharmaFutures: Cost and Choice in the US Market

1

Introduction

e US market is changing.Gone is the “golden age”in which insurers acceptedphysicians’ seemingly limitlessappetite to prescribe newproducts, irrespective of cost.In its place is a new era in whichthe 18% of GDP spent on healthin the US is under scrutiny asnever before.2 e country mayremain content to pay a muchhigher percentage of its GDPon health than others in theOECD. Nevertheless, it is clearthat growing anxiety over thesustainability of growing levelsof spending is leading both publicand private payers to seek tocontain costs and to focus onproven clinical benefit in a waythat is transforming the market.And they are being helped to doso by advances in technology thatpermit them to aggregate andinterpret data in ways that havenever before been possible.

Economics are one powerfuldriver of this change, particularlyin light of the huge federalbudget deficit. Another driver isthe combination of demographic

and epidemiological changes.As the population ages,increasing numbers of olderAmericans need and expect morehealthcare, including ever moreexpensive health technologies.At the same time, America’sgrowing burden of chronicdisease and disappointing healthoutcomes relative to otherOECD countries add to thepressure to change the status-quo.

How the changes will unfoldis open to question. e USmodel of healthcare is highlyfragmented as a result of itscommitment to individualchoice and market forces, and thelegacy of World War Two wagecontrols which led to employer-sponsored health coverage.ese characteristics led to theevolution of a decentralisedand diversified system in whichhealthcare was first and foremostthe responsibility of individualsand their employers. Only laterdid it become the responsibilityof government to provide forelderly, disabled and poor peopleunder Medicare and Medicaid.

Unlike the European model,which starts with a commitmentto healthcare for all, and anacceptance that this brings withit in-built resource constraints,the US healthcare market reflectsa belief that the best healthcareis achieved by allowing theinterplay of multiple strong andcompeting interests. Hundredsof health plans and a mix ofprivate and public sector payers– which vary from state to state– compete to offer multiple,tiered offerings, ranging fromthe very best of care to its totalabsence, except in direstemergencies. e resultingsystem has proved remarkablydurable and, until now, resistantto change.

e government’s health reform,the Patient Protection andAffordable Care Act (ACA)will test the resilience of thesystem as never before. On theone hand, it gives unprecedentedinfluence to the government inhealthcare, at federal and statelevels, through insurancesubsidies, new insurance

is PharmaFutures report focuses on the US – the world’s largest and most profitablemarket for the pharmaceutical industry. e country has historically been the mostsignificant source of pharmaceutical growth, driven largely by price increases (nine-foldaverage real price rises since 1980) and expanding volumes.1 Europe’s growth is currentlysluggish, Japan’s moderate, and while the emerging markets offer great potential, there arealso significant price and margin challenges. Consequently, in the near-to-medium term,at least, the fortunes of the industry will continue to be shaped by what happens in the US.

PharmaFutures: Cost and Choice in the US Market

2

exchanges and expandedMedicaid eligibility. It alsolooks likely to change howother players in US healthcareoperate as new incentives andcosts alter the behaviours of largeemployers, healthcare providers,insurers and patients. On theother hand, however, the multi-actor US health system hashistorically proved remarkablyresilient. And it is preciselybecause it is highly fragmented,crowded and complex that thisis the case. Recent reforms donot change its basic characteristicas a free-market, consumer-ledmodel in which fragmentationis a defining feature. What thereforms do change is the balanceof power between the system’smajor protagonists.

e implications of thesechanges for the pharma industryspecifically are not yet entirelyclear. Industry optimists arguethat changes to the system,including the use of neweffectiveness metrics, willallow pharma companies todemonstrate how, when usedappropriately, innovativemedicines can offer payerssignificant tertiary care savings.A more pessimistic view arguesthat the introduction of costcontainment measures willfocus attention on the readilyidentifiable upfront costs of

medicines (especially higher-priced new ones), and thatpharma will struggle to persuadethe system that it is offeringsufficient value in the newenvironment.

It is likely that two criticalfactors will overshadow othersin determining the impactof health reform on pharma.e first is how the increasinglysophisticated use of data indefining value will play out, andwhether the industry will be ableto be an active participant in thisprocess. New data managementcapabilities are allowingproviders and payers to linkinputs to health outcomes andto use this analysis to guidereimbursement. If pharma is notat the table, new definitions ofvalue will be made in its absence.e second is how – and indeedwhether – the industry choosesto address the thorny issue ofpricing. Difficult choices needto be made in the face ofincreasingly cost-consciouspatients, payers and providers,facing mounting economicconstraints. e choices theindustry makes will, in turn,influence the future forinnovation, since investmentin the next generation of R&Dis dependent on the industry’sconfidence in a long-termsustainable market for its

products. And the challengeis made harder by the fact thatthe changes will take place overyears of trial and error, requiringdifficult judgement calls onstrategy and tactics alongthe way.

Investors will play an influentialrole in determining pharma’s nextsteps, as they anticipate – and inthe process to some extent pre-determine – the winners andlosers. e financial markets aretoday more upbeat about pharmathan they have been for sometime. e industry’s recent trackrecord on R&D is likely to havecontributed to this. Last year,some big pharma stocksoutperformed the S&P 500 index– which itself rose over 10%.3

ere are a number of reasonsfor this return to favour. Pharmastill produces a high dividendyield (between 3% - 4%) relativeto the market; the industryappears to be addressing someinvestor concerns on costs andovercapacity and, finally, theshort-term impact of the ACAis viewed by many as expandingthe market for drugs becauseof wider insurance coverage.To this list of potential valuedrivers investors are adding anassessment of increasinglydifferentiated company strategieson pricing and reimbursement.

Economic Pressures

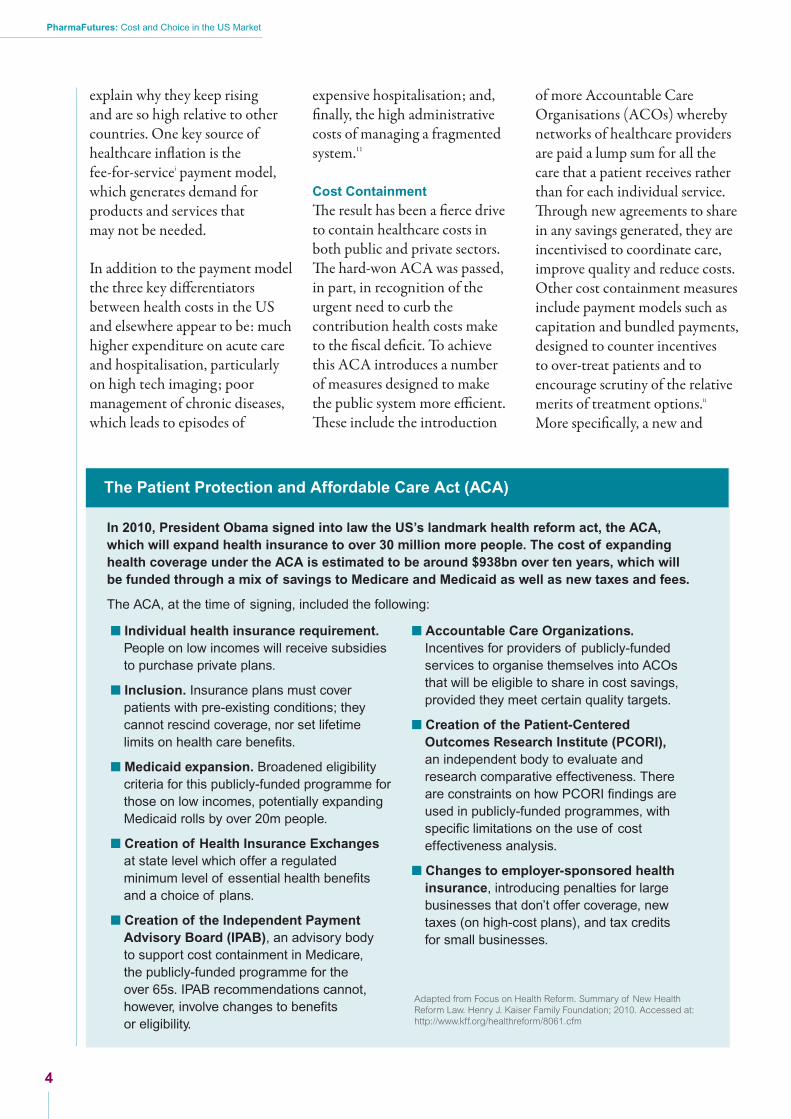

At 18% of GDP and rising fasterthan economic growth, healthcosts are making a significantcontribution to the US deficit,which for 2012 stood at an eye-watering $1.1 trillion.4 Inevitably,much of the debate has focusedon those areas of healthcare thatare publicly financed. Federalhealth spending is forecast togrow from 5.6% of GDP in 2011to over 9% by 20355 and, despiterecent signals that growth inhealth costs is slowing, manyworry about the long-termsustainability of parts of theseprogrammes (see Fig. 1).6

Escalating health costs are notjust a government problem. eyalso place a heavy burden on USemployers who provide the lion’sshare of private health insurance.For some time, economists havespeculated about the impact thismay have on US competitivenessin terms of jobs and economicoutput.7 Investor Warren Buffetthas likened the US healthsystem to a tapeworm insidethe economy that drags downits global competitiveness.8

Health costs also exact a highpersonal toll on the millionsof uninsured or under-insuredAmericans; over 60% ofbankruptcies in 2007 stemmedfrom medical debt9 and a fullthree-quarters of people who

go bankrupt because of unpaidbills have insurance.10

Drivers of Cost

Health costs in the US are drivenby a number of complex factorsand many theories have tried to

PharmaFutures: Cost and Choice in the US Market

US Healthcare Market Fundamentals

e US health system is changing, with implications for all its protagonists: governmentat the federal and state level; providers; insurers; hospitals; doctors; pharma and devicecompanies; and patients. e biggest impulse behind this change is the need to expandaccess to healthcare, with the ACA as the expression of this. But change in the system isalso being driven by the need to urgently address America’s spiralling healthcare costs aswell as to improve on its relatively poor health outcomes.

3

Source: OECD Health Data. 2010. Cited in: Squires D. The US health system inperspective: a comparison of 12 industrialized nations. Issues in internationalhealth policy. The Commonwealth Fund. 2011.

Figure 1:

International comparison of total expenditureson Health as a percentage of GDP, 1980-2008

0

2

USFRSWZGERCANNETHNZDENSWE

UKNORAUS

4

6

8

10

12

14

16

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

PharmaFutures: Cost and Choice in the US Market

4

explain why they keep risingand are so high relative to othercountries. One key source ofhealthcare inflation is thefee-for-servicei payment model,which generates demand forproducts and services thatmay not be needed.

In addition to the payment modelthe three key differentiatorsbetween health costs in the USand elsewhere appear to be: muchhigher expenditure on acute careand hospitalisation, particularlyon high tech imaging; poormanagement of chronic diseases,which leads to episodes of

expensive hospitalisation; and,finally, the high administrativecosts of managing a fragmentedsystem.11

Cost Containment

e result has been a fierce driveto contain healthcare costs inboth public and private sectors.e hard-won ACA was passed,in part, in recognition of theurgent need to curb thecontribution health costs maketo the fiscal deficit. To achievethis ACA introduces a numberof measures designed to makethe public system more efficient.ese include the introduction

of more Accountable CareOrganisations (ACOs) wherebynetworks of healthcare providersare paid a lump sum for all thecare that a patient receives ratherthan for each individual service.rough new agreements to sharein any savings generated, they areincentivised to coordinate care,improve quality and reduce costs.Other cost containment measuresinclude payment models such ascapitation and bundled payments,designed to counter incentivesto over-treat patients and toencourage scrutiny of the relativemerits of treatment options.ii

More specifically, a new and

The Patient Protection and Affordable Care Act (ACA)

� Individual health insurance requirement.People on low incomes will receive subsidiesto purchase private plans.

� Inclusion. Insurance plans must coverpatients with pre-existing conditions; theycannot rescind coverage, nor set lifetimelimits on health care benefits.

� Medicaid expansion. Broadened eligibilitycriteria for this publicly-funded programme forthose on low incomes, potentially expandingMedicaid rolls by over 20m people.

� Creation of Health Insurance Exchangesat state level which offer a regulatedminimum level of essential health benefitsand a choice of plans.

� Creation of the Independent PaymentAdvisory Board (IPAB), an advisory bodyto support cost containment in Medicare,the publicly-funded programme for theover 65s. IPAB recommendations cannot,however, involve changes to benefitsor eligibility.

� Accountable Care Organizations.Incentives for providers of publicly-fundedservices to organise themselves into ACOsthat will be eligible to share in cost savings,provided they meet certain quality targets.

� Creation of the Patient-CenteredOutcomes Research Institute (PCORI),an independent body to evaluate andresearch comparative effectiveness. Thereare constraints on how PCORI findings areused in publicly-funded programmes, withspecific limitations on the use of costeffectiveness analysis.

� Changes to employer-sponsored healthinsurance, introducing penalties for largebusinesses that don’t offer coverage, newtaxes (on high-cost plans), and tax creditsfor small businesses.

In 2010, President Obama signed into law the US’s landmark health reform act, the ACA,which will expand health insurance to over 30 million more people. The cost of expandinghealth coverage under the ACA is estimated to be around $938bn over ten years, which willbe funded through a mix of savings to Medicare and Medicaid as well as new taxes and fees.

The ACA, at the time of signing, included the following:

Adapted from Focus on Health Reform. Summary of New HealthReform Law. Henry J. Kaiser Family Foundation; 2010. Accessed at:http://www.kff.org/healthreform/8061.cfm

controversial IndependentPayment Advisory Board (IPAB)is planned, designed to containrising Medicare costs, withoutusing direct price controls onmedicines.

e ACA has resulted in somecost concerns shiing fromfederal to the state level. e Act’sexpansion of Medicaid, whichcould add over 20m people toits rolls by 202212, is a state-runprogramme; and it is at statelevel that the ACA’s momentousconsumer reforms – the settingup of insurance exchanges and thebenefits packages they offer – willplay out. e impact of the ACAon individual state budgets isunclear; incremental costs willbe minimal compared to federalspending and there could evenbe small net budget gains.13

However, states have alreadydemonstrated their appetite forcontrolling healthcare costs ina number of ways – throughlimiting rises in insurancepremium rates and, in someplaces, cutting reimbursementrates for Medicaid. Other movesinclude preferred drugs listsand managed Medicaid plans.

Despite these public sectormoves, many believe that greatestinnovation to contain costs willcome from the private sector.e private sector has sought tocontain rising healthcare costs,and the drugs bill in particular,for some time. Efforts havefocused on the design ofinsurance plans to promotegenerics and preferred brandsvia the use of tiers in formularies,

and to steer beneficiaries towardslower cost drugs through theuse of step therapyiii and therequirement for priorauthorisation. Negotiations overthe place of drugs on formularieshave involved complex pricingand rebate deals. With theintroduction of the ACA, privateinsurers and providers have a newreference point for developmentsin quality measures and costcontainment and new modelsin the payment and deliveryof services that they may seekto emulate.

Demographic andEpidemiological Pressures

A second driver of change in UShealthcare is the fact that, withthe exception of oncology, the USunderperforms on many measuresof health outcomes comparedwith international peers.Although at the top end of thescale US healthcare is secondto none, life expectancy for theaverage American is lower thantheir counterparts in almost allother high-income countries.14

Nearly half of all Americanshave at least one chronic disease,which cause seven out of tendeaths in America.15 e seconddriver of change in the US systemis therefore the desire to improvehealth outcomes.

Expansion of Health Coverage

Poor population health outcomeshave partly been the result ofmillions of Americans lackinghealth insurance. e ACAseeks to address this through itsfederally mandated insurance

coverage which will add over30 million people to those whoalready have health insuranceby 2019.16 By 2014 each stateis to have a Health InsuranceExchange – either set up bythe state or run by the federalgovernment. ese will bemarketplaces where individualscan purchase an essential healthbenefits package that providesa comprehensive set of services.Some of the recently insured willcome from among the poorest ofAmerica’s communities, meaningthey may have complex andexpensive health requirements.While the health reform has beendesigned to be paid for by a rangeof new taxes and savings, thisrapid expansion in coverageis likely to add further impetusto the desire both to improveoutcomes and contain costswithin the public system.

Improving Outcomes

A key part of the ACA reformis therefore the introduction ofmeasures to assess and improvehealth outcomes. e ACOs arenot only designed to encouragesavings, but, by encouraging themove to integrated care, theyare also intended to achievebetter coordination of patientcare and better health outcomes.ey will be accompanied by theintroduction and evaluation ofspecific new quality measures.Another ACA creation, thePatient-Centred OutcomesResearch Institute (PCORI),seeks to produce independentresearch on comparativeeffectiveness.

PharmaFutures: Cost and Choice in the US Market

5

i Fee for service, refers to payment for each service a patient receives.

ii Capitation payments are lump sum payments to cover any care a patient might need. A bundled payment – someway between fee for service andcapitation payments – refers to payments linked to an episode of care (range of treatment for a particular health episode).

iii Step therapy is an approach set out in a patient’s health plan: it works by putting patients on a first-step drug treatment for their condition (often ageneric) and only moving to a second-step therapy (which may be more expensive) if medically required.

PharmaFutures: Cost and Choice in the US Market

6

e private sector has also rampedup its ability to hold healthcareproviders to account for improvedperformance and outcomes.Payers, ranging from health plansto employers, are using key assets,such as vast amounts of claimsdata, to innovate with newmodels of primary care.17 eyare also experimenting with value-based insurance design, whichuses cost-sharing to steer patientstowards more efficient and high-value health services. Providers,in turn, are carrying this agendathrough their own organisationsby influencing the prescribingbehaviours of physicians intheir networks.

Pharma has been a partner in someof the newer outcomes-focusedinitiatives. Risk-sharing deals oncertain drugs, for instance, havelinked part of the payment for

a drug to specific outcomes, suchas blood sugar control in the caseof diabetes or non-spinal fracturesin the case of osteoporosis.18

Amid the welter of pilots andexperiments, the system isundergoing a quiet revolutionin which major players areobtaining and acting on a newunderstanding of population-based health outcomes.

The Enabler of Change:Big Data

e scaling up of efforts torationalise and streamline costsand to evaluate outcomes has beenmade possible by dramaticadvances in technology. It is nowpossible to aggregate and analysevast amounts of claims data, whichprovide an indication of drugutilisation. e ambition is

to integrate this data with therelevant clinical data, whichwould provide insights intopatient outcomes. If successful,these changes offer the prospectof revolutionising definitionsof value by accelerating newapproaches to comparativeeffectiveness. e task ofintegrating such complex setsof data is difficult and time-consuming, and remains animperfect science, but is likelyto evolve rapidly as more isinvested in this area. A highprofile example of this trendis the recent agreement betweenUnitedHealth and the MayoClinic, which, between them,will bring together millionsof health insurance claims andclinical patient records forresearchers to analyse.19

PharmaFutures: Cost and Choice in the US Market

7

Although the majority of recentapprovals were for specialtypharma, they ranged across manytherapeutic categories, includingthe first new treatment for TB in40 years, as well as an anticlottingdrug. Other disease areas thathave been in focus in the pastcouple of years include HepatitisC, auto-immune and oncology.e therapeutic landscape is alsochanging with growing interest inusing combinations of drugs, useof diagnostics and a shi frominjectable to oral specialist drugs.How any successful medicinewill fare in the changing UShealthcare market will, however,be determined by the evolutionof the following hallmarks ofhealth reform and relatedreimbursement trends.

Expansion of Drug Market

e ACA is almost certainto increase the volume ofpharmaceutical sales, as aresult of expanded coverage.

e market is likely to expandfurther if ACOs succeed inoffering more integratedtreatment of chronic diseasesin a primary care setting, andfocus on greater adherenceto avoid expensive hospitaladmissions and re-admissions.e focus on primary care alsoprovides an opportunity formedicines (anti-hypertensives,anti-diabetics and osteoporosis,for example) to be used to avoidthe expense of poorly managedchronic conditions.

ComparativeEffectiveness Research

Comparative EffectivenessResearch (CER) is likely to bestrengthened and to become morewidely used by private providersand payers. It is not clear, however,whether this makes things easieror more difficult for pharma.ere are many interpretationsand sources of CER – withcompanies, payers and research

bodies all potentially coming upwith their own versions. ACAalso raises the profile of CER,via the creation of a new researchbody, PCORI, which willgenerate and review existingevidence on effectiveness.e long-term impact of PCORIon the market is unclear, as, atpresent, its findings cannot beused to mandate or denypayment or coverage of healthcaretreatments across Medicare.

The Rise of the Patient

e patient voice is becomingincreasingly important in UShealthcare. Patients’ views onwhere and how they want to betreated will be more influential,as has been shown in diabetesprogrammes in the contextof Patient Centred MedicalHomes.20 As patients emergeas an independent force in thepurchasing of healthcare, theirviews on quality of care and valuefor money will acquire moreresonance. eir choices will be

Hallmarks of Change

e core value proposition of the global pharma industry continues to be the developmentof innovative medicines that offer improvements on existing therapies or breakthroughtreatments. Aer a long drought in R&D productivity, there are signs of a turnaroundfor pharma. Last year the FDA approved over 30 new drugs, the highest level since 1996.Coming aer a good year in 2011, the pick-up in approvals is prompting hopes of asustained improvement over the last decade, when drug approvals were much lower.

“Realistically, comparativeeffectiveness is ten yearsaway, or more. ”

“My fear is that CER will be costly and time-consumingand dependent on regular data from thousands ofindividuals, and because of that CER will fall backinto the hands of pharma.”

*

* Direct, unattributed quotes drawn from conversations and interviews during the course of the PharmaFutures project.

felt more clearly in the marketas they select which health plansthey want through the variableofferings available on theinsurance exchanges. eywill also have a direct influenceon the ACOs, whose qualityperformance will be measured,in part, on how patients ratetheir experience.

Consolidation

e previous sales model in whichindustry reps knew who they

needed to influence (key peoplewithin Pharmacy BenefitsManagers (PBMs) and insurers aswell as individual prescribers) hasbeen replaced by multiple newplayers – providers, hospitals,patients – as well as the doctorsand PBMs. e push to integrate

care and the scope for cost savingshas already led to significantconsolidation, which isstrengthening the bargainingpower of payers and providers,and leading some in the industryto express fears of an ‘oligopoly’,distorting the US marketplace.

PharmaFutures: Cost and Choice in the US Market

8

“Pushing more cost onto the consumer is a megatrend.”

“Payers are taking less risk, and increasingly functionas an intermediary. This means the patient will have moreat risk themselves. ”

PharmaFutures: Cost and Choice in the US Market

9

Linking Data andOutcomes in Regulationand Reimbursement

ere is widespread agreementthat the narrow regulatory focuson efficacy and safety data,generated by clinical trials, isinsufficient to determine the valueof a medicine. ere is a growingdisconnect between the approvalprocess for innovative drugsand their reimbursement bypayers. e Food and DrugAdministration (FDA) hasintroduced greater flexibilityon oncology, and recently onAlzheimer’s Disease, but more isneeded for other therapeutic areas.ere is a need to explore the

potential for alternative regulatoryprocesses, such as adaptivelicensing, to allow real-worlddata (data from normal clinicalsettings) to build on clinical trialdata. is would require moreinstitutional dialogue between theFDA and CMS (Centers forMedicare and Medicaid Services),and a wider dialogue with

stakeholders about the natureof the evidence that wouldbe required and would beconsidered relevant.

e most significant change is thatproviders and payers now requiredata that helps them to measureclinical and quality outcomes.is includes a growing needfor real world data on specificpopulations, oen with complexdisease profiles. New measuresof accountability are beingintroduced for both payers and

providers, and data therefore hasto help them demonstrate howinterventions are helping meettargets. Can a drug demonstrablyimprove the overall costs ofdelivering care, for example;or can it be shown to avoiddownstream complicationssuch as hospital readmissionsor to improve adherence rates?

Electronic medical records will bea key source of this data, althoughit will take time before they arewidely embedded in the UShealthcare system.

e role of pharma in contributingto new types of data is thesubject of debate and has manydimensions. First, it is not clearhow credible pharma will be ingenerating or disseminating realworld data, given the legacy ofmistrust that dogs the industryregarding more established formsof data such as clinical trial data.Second, pharma faces considerablechallenges in communicating thisdata. For instance, there isregulatory uncertainty over howfar pharma will be allowed to go,in using new types of evidence indiscussions with payers. irdly,there is the question of how suchdata will translate into improvedclinical practice. ere may be arole here for independent thirdparties, such as medical societies,to analyse the data in a credibleand relevant way to inform clinicalguidelines. Pharma’s role here may

“ It is completely and utterly wrong that someone coulddo a trial and not publish it, on an ethical, moral, no, fromevery basis.”

Transparency of data is accelerating and that’s generally agood thing, but I can see schisms in the industry about howyou make the data transparent.

“”

UncertaintiesReforming the highly complex, fragmented US health system, across the public andprivate sectors, is likely to mean several additional waves of reform and adjustmentover the coming decade. is makes predictions of what is to come highly problematic.However, for pharma, it is nevertheless possible to identify two key uncertaintiesthat are likely to be critical determinants of its ability to generate value over time.

involve a conversation with awhole new set of stakeholders.Lastly, the industry is unlikelyto be united in its approachto any of these issues, whichwill add to the complexity.

Pricing

e crucial question for pharmaand its investors is what impactthese changes are likely to haveon the pricing of its products– especially the launch price ofnew drugs. ere are conflictingviews – from both within andoutside the industry – on whetherpharma will be able to retainpricing power in the medium term.Some support for high and risingprices is likely to come from thesystem itself: a fragmented systemwhere pricing is not transparent.In addition, some of the reformmeasures might take a long timebefore they have any effect oncosts (such as bundled paymentmodels). Lastly, pharma’s pricingpower may be bolstered if it wereable to communicate the value ofits products better, and convincepayers that pharmaceuticals cansave on hospitalisation expenses.

However, an alternative viewargues that payers and providerswill become increasinglyaggressive, introducing measures

to “bend the cost curve” in acontext of growing demand.is line of argument asserts thatthe combined impact of the ACAand other changes in healthcarewill lead to inexorable andpermanent downward pricingpressure. ere is a discerniblepathway that would lead to thisoutcome: first, plans offered byhealth insurance exchanges arelikely to be lower-value thanemployer-sponsored schemesbecause they are competing

for more budget-constrainedconsumers. Second, it is likelythat companies who carry highhealth insurance costs will seekto shi some of the employeesin their health plans onto theexchanges. ird, the lower valueof what is offered in Medicaidcould affect pricing elsewherein the system (Medicaid paysapproximately 30% less, on aweighted basis, for healthcareservices and products than thecommercial sector, though in thecase of some drugs it could beless).21 Fourth, the adoptionof new processes by payers andproviders, such as disease pathwaysand protocols, could prioritisesome drugs over others,generating savings withoutharming outcomes.22 Finally,despite current prohibitions, overtime, economic pressures could

PharmaFutures: Cost and Choice in the US Market

10

“For the last 3-5 years the US has been the only place whereyou can raise drug prices. Price increases in the US will continuefor at least 5-10 years.

“

”The industry is under-prepared for the big pricing cuts that

are coming their way.“

”

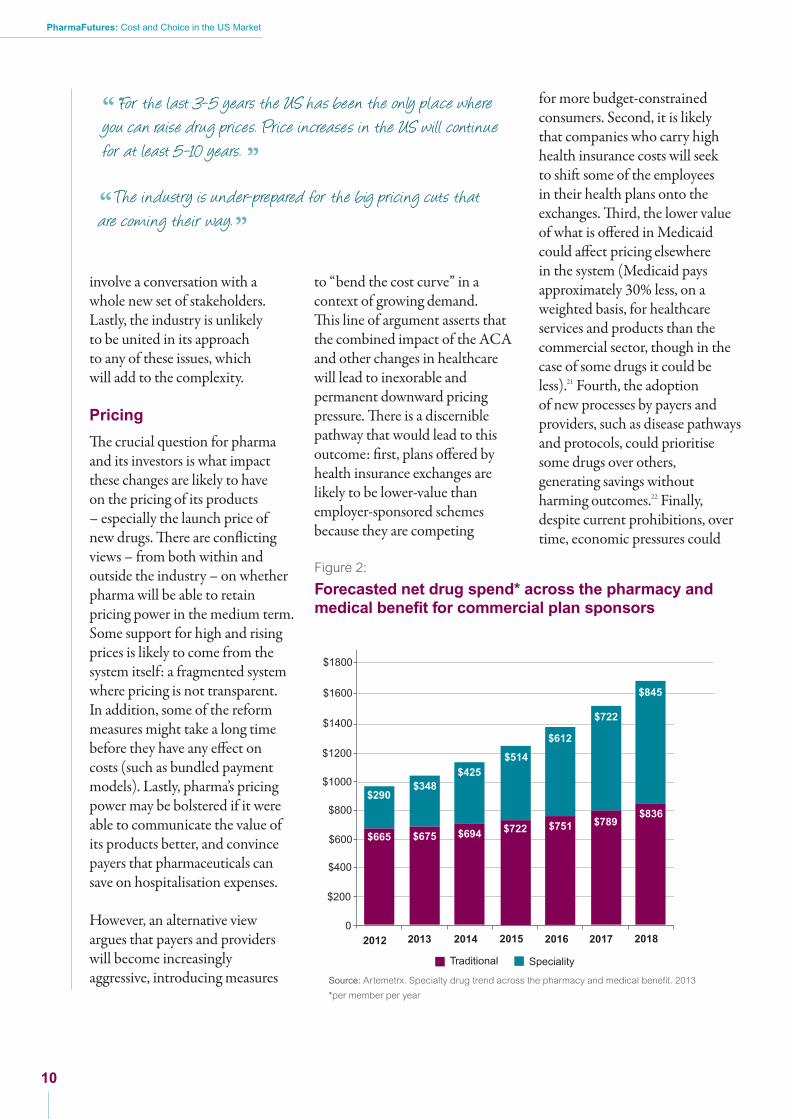

Figure 2:

Forecasted net drug spend* across the pharmacy andmedical benefit for commercial plan sponsors

0

$200

$400

$600

$800

$1000

$1200

$1400

$1600

$1800

2012 2013 2014 2015 2016 2017 2018

$665

$290$348

$675 $694 $722 $751 $789$836

$425$514

$612

$722

$845

Traditional Speciality

Source: Artemetrx. Specialty drug trend across the pharmacy and medical benefit. 2013

*per member per year

PharmaFutures: Cost and Choice in the US Market

11

make it acceptable for IPAB torecommend cost control measuresin Medicare spending that focuseson originator products.

A number of factors could serveto accelerate these trends. First,the multiple patent expiries thathave shielded payers from theimplications of the increasing drugbill for the last ten years are comingto an end. e cost of innovativemedicines will no longer be quiteso cushioned by savings fromgeneric substitution, leading payersto seek to reduce the highly visibledrugs line item in the budget.Even though this may only be asmall percentage of the whole, itmay prove easier for providers tocut pharmaceuticals than endurethe highly politicised fall-out ofcutting costs at hospitals, forinstance, which are sometimesseen as bastions of local economies.

Second, providers are increasinglyaligning with payers to push backon prices, with the private sectormoving quickly and aggressivelyon this. ird, there is a change inpatient expectations and providerbehaviours that could combine toreduce healthcare utilisation andtemper expectations in the longterm. Some experts argue thatpatients have been “conditioned”by several years of recession toaccept constraints on theirhealthcare choices and are moresensitive to high prices throughco-pays and co-insurance. is mayaffect the price point at which newdrugs come to market. ere is alsoevidence to suggest that the trendtowards engaging patients in shareddecision-making can lead to themopting for less intervention.23

However, the most importanttrigger for private healthcareproviders and insurers to takeradical action on pricing is likelyto be the inexorable increase inthe prices of specialty medicinesand biologics (with attentionfocusing on certain disease areassuch as autoimmune, cancer, HIVand MS). Prices for these medicinesare rising much faster than othermedicines: 17% in 2011 comparedwith overall trend of 2.7%.24

Although these medicines accountfor only 1% of total prescriptionvolume for private insurers, theyaccount for 17% of totalprescription spending, and theproportion is growing.25 Somepredict that insurers could bespending more on specialty drugsthan on traditional drugs by2018.26 It is little wonder thatthe sustainability of the specialtyand biologic prices has comeunder intense scrutiny (see Fig. 2).

PharmaFutures: Cost and Choice in the US Market

12

Conclusion

For some, these changes do notchange the industry’s strongposition. In a market characterisedby choice, if pharma succeeds inbringing innovative drugs throughdevelopment, it will continue tofind a lucrative market for them.And it has multiple potentialpartners for demonstrating thevalue of prescription drugs, andthe resources and skills to succeedwithin the changed system,however complex. For others,the cost containment challengesfundamentally change theindustry from being a pricemaker to a price taker. In thiscontext, innovation is a hardersell, contingent on how value isperceived by a much wider groupof stakeholders. And the situationis made more difficult by thefact that the industry starts witha trust deficit.

Which opinion proves correctwill depend on the interplay ofmany things. What is clear is thatindustry executives and investorsalike face difficult questions aboutwhat a strategic response lookslike – and whether that response

should be company by companyor an industry-wide – in theface of a dramatically changedUS health system.

e PharmaFutures dialoguebrought together industry,investors and societal stakeholdersto share analysis and perspectivesabout the US market.

Investor participants in thedialogue reaffirmed their cautiousoptimism about pharma pipelines,but acknowledged that theprospects for pharma wouldincreasingly be determined byreimbursement trends. It maybe that investors come todifferentiate between companieson the basis of their distinctivereimbursement strategies, as wellas comparing them on R&D,pipeline and choice of therapeuticcategory. In addition, investors areincreasingly interested in thesustainability of specialty pricing,approaches to data managementand the growing demands fortransparency as well as the natureof the industry’s response toprovisions of the ACA.

For payer and providerparticipants bending the all-important cost curve in the faceof the “silver tsunami” of olderpatients is of paramount concern.For them too, specialty productsare of particular of interest due toannual price hikes that they deemunsustainable.

Patient participants sharedthis concern, and highlightedthe growing trend to acceptconstraints on choice as anacceptable trade-off for costreductions, though this is nottrue for rare disease treatments.

Industry participants acceptedthat there will be winners andlosers in this transition. eyacknowledged that their industryfaces a strategic decision aboutwhether to adopt a defensiveposition, seeking to maximisereturns in the short-term,irrespective of the long-termconsequences, or to take a morecollaborative approach, whichthough costly and complex, willultimately position pharma as partof the solution to the problem ofoutcomes and costs.

e US health system is in flux and high levels of uncertainty will remain as healthcaremarkets adjust to the expansion of publicly funded programmes, the advent of theinsurance exchanges, the growing voice of patients, the greater focus on the valueof medicines, and the shi to outcomes-based reimbursement.

PharmaFutures: Cost and Choice in the US Market

13

PharmaFutures discussionsconcluded with a sense ofopportunity for the industry.As the health system adoptsgreater understanding of theimpacts of health interventions,the outlook for medicines thatcan help to save the system money,

at the same time as preventingdisease progression is bright.To achieve this end, however,will require the industry tocollaborate with payers andproviders, understand theconstraints they face and committo reframing the relationship to

one of negotiation, rather thanan all-or-nothing stand-off on aprice. ere is no guarantee thatthe pharma sector as a wholewill do this. It is likely, however,that tomorrow’s successfulcompanies will be thosewho chose this path.

PharmaFutures: Cost and Choice in the US Market

14

PharmaFutures US Participantsand External Interviewees

Stewart Adkins, Director, Stewart Adkins Advisors LtdJack Bailey, Senior Vice President, Policy, Payers & Vaccines,GlaxoSmithKlineLauren Barnes, Senior Vice President, Avalere HealthProf Ernst Berndt, Louis E. Seley Professor in AppliedEconomics, MIT Sloan School of ManagementDr Scott Braunstein, Managing Director, JP Morgan AssetManagementKathy Buto, Vice President Health Policy GovernmentAffairs, Johnson & JohnsonJoseph Canzolino, Deputy Chief Consultant, PharmacyBenefits Management, Veterans AffairsDr Benjamin Chu, Group President Southern California andHawaii, Kaiser PermanenteDr Molly Coye, Chief Innovation Officer, UCLA HealthSystemProf Patricia Danzon, Celia Moh Professor of HealthcareManagement, Wharton School, University of PennsylvaniaDave Domann, Director Health Care Quality, Johnson& JohnsonDr Robert Dubois, Chief Science Officer, NationalPharmaceutical CouncilSusan Edgman-Levitan, Executive Director of John DStoeckle Center for Primary Care Innovation,Massachusetts General HospitalJoel Emery, Vice President, Analyst Fred Alger Management,Inc.Charlotte Ersbøll, Corporate Vice President, GlobalStakeholder Engagement, Novo NordiskDr Richard Evans, Founder and General Manager,Sector & Sovereign ResearchWilliam Fleming, President, Humana Pharmacy Solutions,Humana Inc.Jason Fletcher, Head of American Equities, UniversitiesSuperannuation Scheme Investment ManagementLiz Fowler, Vice President Global Health Policy, Johnson& JohnsonDr Chester Good, Co-Director, VA Center for MedicationSafety, Veterans AffairsMary Grealy, President, Healthcare Leadership CouncilDavid Green, Social Entrepreneur, Oxford Lotus Health FundDr Jane Griffiths, Company Group Chairman, JanssenPharmaceuticals, EMEA, Johnson & JohnsonJohn Haney, Vice President Immunology Marketing,Johnson & JohnsonGraham Hetherington, Chief Financial Officer, Shire PlcRoger Longman, Chief Executive Officer, Real Endpoints

Chris McGowen, Director of Government Affairs,Novo NordiskLaurence McGrath, Executive Director, US HealthcareAnalyst, JP Morgan Asset ManagementDr Neil Minkoff, Founder, Fountainhead HealthPenny Mohr, Senior Vice President, Program DevelopmentCenter for Medical Technology PolicyAndy Oh, Research Analyst and Portfolio Manager,Fidelity PlcProf Gilbert Omenn, Professor of Internal Medicine,Human Genetics and Public Health, University of MichiganValerie Paris, Economist, Health Division, Organisationfor Economic Co-operation and DevelopmentJoseph Piemont, Chief Operating Officer, CarolinasHealthCare SystemsSteve Phillips, Director, Health Policy and Reimbursement,Johnson & JohnsonGinny Proestakes, Director of Health Benefits,General Electric CompanyProf Sir Michael Rawlins, Chairman, National Institute forHealth and Clinical Excellence (NICE)Dr Roger Ray,Executive Vice President and Chief MedicalOfficer, Carolinas HealthCare SystemProf Dennis Ross-Degnan, Associate Professor, Departmentof Population Medicine, Harvard Medical SchoolProf Leonard Schaeffer, Judge Robert Maclay WidneyProfessor and Chair, Sol Price School of Public Policy,University of Southern CaliforniaJohn Schaetzl, Industry Commentator, IndependentAd Schuurman, President, e Medicine EvaluationCommittee (MEDEV)Carl Seiden, President, Seiden Pharmaceutical StrategiesNorman Selby, Executive Chairman, Real EndpointsMark Skinner, President/CEO, Institute for PolicyAdvancementDaniel Summerfield, Co-Head Responsible Investment,Universities Superannuation Scheme Investment ManagementJennifer Taubert, Company Group Chairman, NorthAmerica Pharmaceuticals, Johnson & JohnsonPhil ompson, Senior Vice President, GlobalCommunications GlaxoSmithKlineJulie Trocchio, Senior Director, Community Benefit andContinuing Care, Catholic Health AssociationDr Sean Tunis, Founder and Director, Center for MedicalTechnology PolicyMike Valentino, Chief Consultant, Pharmacy BenefitsManagement, Veterans AffairsDr Giorgia Valsesia, Healthcare Analyst, RobecoSAMStijn Vanacker, Analyst, Global Healthcare, Robeco

Appendix

nia

PharmaFutures: Cost and Choice in the US Market

15

1. Evans R. Large Cap Pharma’s Dependence on US List Price Growth is Unsustainable. Stamford: Sector & Sovereign Research; 2012.

2. Martin A.B; Lassman D; Washington B; Catlin A, and the National Health Expenditure Accounts Team. Growth in US health spendingremained slow in 2010; Health share of gross domestic product was unchanged from 2009. Health Affairs Jan 2012; 31 (1): 208-219.

3. Mourdoukoutas P. Should Investors Buy into Big Pharma Rally? Forbes; 2012 [cited 19 Mar 2013]; Accessed at:http://www.forbes.com/sites/panosmourdoukoutas/2012/11/01/should-investors-buy-into-big-pharma-rally/

4. Congressional Budget Office. Monthly Budget Review; 2012 [cited 19 Mar 2013]; Accessed at: http://www.cbo.gov/publication/43656.

5. Henry J Kaiser Family Foundation. Health Care Costs: A Primer. Key Information on health care costs and their impact; 2012[cited 19 March 2013]; Accessed at: http://www.kff.org/insurance/upload/7670-03.pdf

6. Henry J Kaiser Family Foundation. Medicare – A Primer. Kaiser Family Foundation; 2010 [cited 19 Mar 2013];Accessed at: http://www.kff.org/medicare/upload/7615-03.pdf

7. Johnson T. Healthcare Costs and U.S. Competitiveness. Council on Foreign Relations; 2012 [cited 19 Mar 2013]; Accessed at:www.cfr.org/health-science-and-technology/healthcare-costs-us-competitiveness/p13325.

8. Milstein A. Code Red and Blue – Safely Limiting Health Care’s GDP Footprint. New England Journal of Medicine 2013; 368:1-3.

9. Daemmrich A. US healthcare reform and the pharmaceutical industry. Harvard Business School; 2011 [cited 19 Mar 2013]; Accessedat: http://hbswk.hbs.edu/item/6832.html.

10. Himmelstein D, Thorne D, Warren E, Wollhandler S. Medical Bankruptcy in the United States, 2007: Results of a National Study.The American Journal of Medicine; 2009.

11. Squires DA. Explaining high health care spending in the United States: an international comparison of supply, utilization, prices andquality. The Commonwealth Fund; 2012. and Cutler DM, Ly DP. The (paper) work of Medicine: understanding international medical costs.Journal of Economic Perspectives; 2011.

12. Holahan J, Buettgens M, Carroll C, Dorn S. The Cost and Coverage Implications of the ACA Medicaid Expansion. Washington D.C.:Kaiser Commission on Medicaid and the Uninsured. The Henry J Kaiser Family Foundation and The Urban Institute; 2012 [cited 19 Mar2013]; Accessed at: http://www.kff.org/medicaid/upload/8384_ES.pdf.

13. ibid

14. Woolf SH, Aron L (eds.) US Health in International Perspective: Shorter Lives, Poorer Health. National Research Council. WashingtonDC: The National Academies Press; 2013.

15. Centers for disease control and prevention. Chronic diseases and health promotion. [cited 19 march 2013]; Accessed at:http://www.cdc.gov/chronicdisease/overview/index.htm

16. Henry J Kaiser Family Foundation. How People Get Coverage under the Affordable Care Act. Health Reform Source. Kaiser FamilyFoundation; 2012 [cited 19 Mar 2013]; Accessed at: http://healthreform.kff.org/the-basics/access-to-coverage-flowchart.aspx.

17. Vojta D, De Sa J, Prospect T and Stevens S. Effective interventions for stemming the growing crisis of diabetes and prediabetes:a national payer’s perspective. Health Affairs Jan 2012; 31 (1): 20-26.

18. Garrison L. Performance-based risk sharing arrangements. Experiences, challenges and directions. University of Washington.Novartis en la Academia III. Bogota, Colombia July 13 2012. [cited 19 Mar 2013]; Accessed at:http://www.novartis.com.co/pdf/GarrisonNovartisColombiaPBRS2012.pdf.

19. Wilde Mathews A. Researchers mine data from clinic, big insurer. The Wall Street Journal; January 15 2013. Accessed at:http://online.wsj.com/article/SB10001424127887324595704578242011727443992.html

20. Patient-Centered Primary Care Collaborative. Practices in the Spotlight. The Medical Home and Diabetes Care. Washington D.C.:2011 [cited 19 Mar 2013]; Accessed at: http://www.pcpcc.net/files/diabetes_guide_2011.pdf.

21. Evans R, Hinds S, Baum R. US Healthcare Demand – Reform Effects. ACA look like a headwind. Stamford: Sector & SovereignResearch; 2012.

22. Baum A, Abraham L et al. Pharma: I pay, you pay, he pays, won’t pay? Citi Research Equities; 2012.

23. Coulter A and Ellins J. Effectiveness of strategies for informing, educating and involving patients. BMJ July 7 2007; 335 (7609): 24-27.

24. Express Scripts. Drug Trend Report 2011. Express Scripts [cited 19 Mar 2013]; Accessed at:http://www.drugtrendreport.com/traditional/a-closer-look-at-2011-trend.

25. PricewaterhouseCoopers. Unleashing Value – The Changing Payment Landscape for the US Pharmaceutical Industry. PwC HealthResearch Institute; 2012.

26. Specialty Drug Trend across the Pharmacy and Medical Benefit. Artemetrx. Quoted in Comer, B. PharmExec. Specialty Drugs andReimbursement. 2013 [cited 19 Mar 2013]; Accessed at: http://blog.pharmexec.com/2013/01/21/specialty-drugs-and-reimbursement/.

References

PharmaFutures: Cost and Choice in the US Market

16

Meteos is a not for profit company, which runs dialogues andnetworks to explore how to achieve long-term economic, socialand environmental stability. Meteos dialogues provide a forumfor senior figures in the corporate, public sector and investmentworlds to discuss the major trends that will shape the market andregulatory landscape in coming years. e dialogues analyse thespeed and direction of these trends and provide an opportunityfor those who will determine future outcomes to work togetherto achieve an alignment of interests.

Meteos is funded by participants in the dialogues, who pay a fee to participate. Meteos seeksto ensure diversity in its dialogues and therefore provides some spaces to participants on ano-fee basis.

Meteos Ltd, 267 Banbury Road, Oxford, OX2 7HT, UK

[email protected] • www.meteos.co.uk

© Meteos, April 2013

Front cover photograph: Sandeep K. Bhat