perusahaan umum listrik negara appraisal of the fourth...

TRANSCRIPT

Report No. 766-IND FILE COPYIndonesiaPerusahaan Umum Listrik NegaraAppraisal of the Fourth Power ProjectMay 20, 1975

East Asia and Pacific Projects DepartmentPower Division

Not for Public Use

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may notbe published, quoted or cited without Bank Group authorization. The Bank Group doesnot accept responsibility for the accuracy or completeness of the report

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

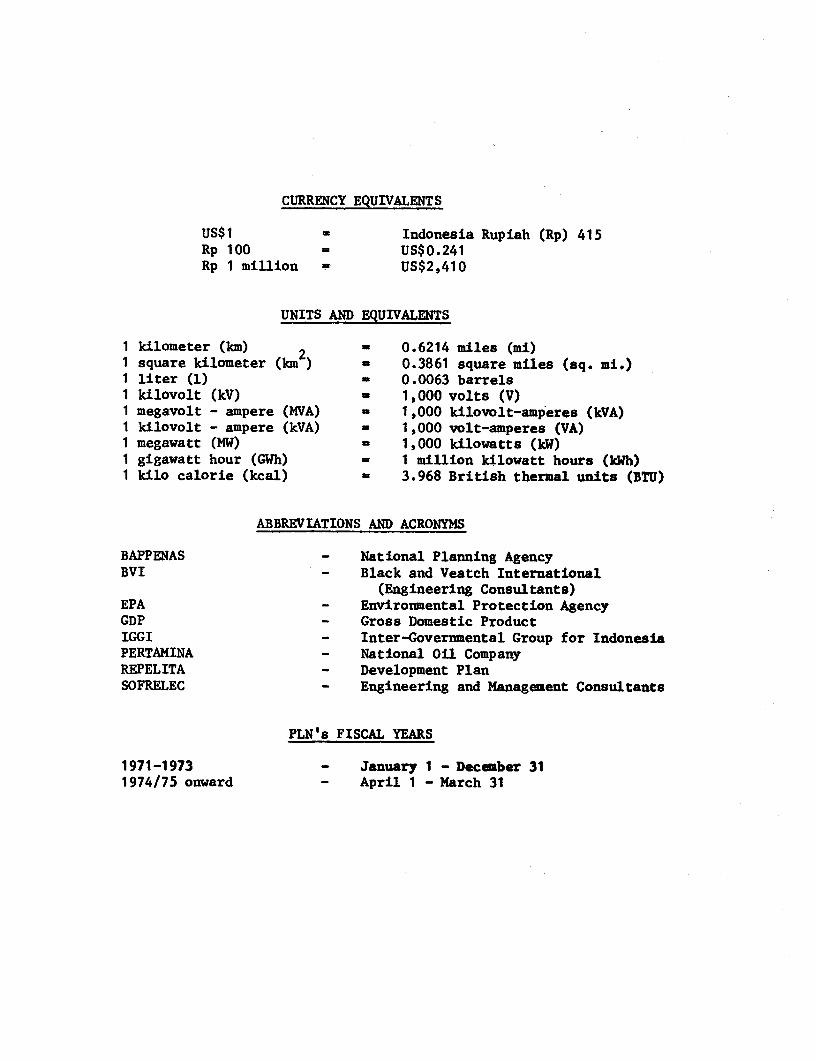

CURRENCY EQUIVALENTS

US$1 - Indonesia Rupiah (Rp) 415Rp 100 - US$0.241Rp 1 million - US$2,410

UNITS AND EQUIVALENTS

1 kilometer (km) 2 ' 0.6214 miles (mi)1 square kilometer (km ) - 0.3861 square miles (sq. mi.)1 liter (1) ' 0.0063 barrels1 kilovolt (kV) - 1,000 volts (V)1 megavolt - ampere (MVA) - 1,000 kilovolt-amperes (kVA)1 kilovolt - ampere (kVA) - 1,000 volt-amperes (VA)1 megawatt (MW) - 1,000 kilowatts (kW)1 gigawatt hour (GWh) - 1 million kilowatt hours (kWh)1 kilo calorie (kcal) - 3.968 British thermal units (BTU)

ABBREVIATIONS AND ACRONYMS

BAPPENAS - National Planning AgencyBVI - Black and Veatch International

(Engineering Consultants)EPA - Environmental Protection AgencyGDP - Gross Domestic ProductIGGI - Inter-Governmental Group for IndonesiaPERTAMINA - National Oil CompanyREPELITA - Development PlanSOFRELEC - Engineering and Management Consultants

PLN's FISCAL YEARS

1971-1973 - January 1 - December 311974/75 onward - April 1 - March 31

INDONESIA

PERUSAHAAN UMUM LISTRIK NEGARA

APPRAISAL OF THEFOURTH POWER PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS . . . i-ii

I. INTRODUCTION ....................... 1

II. THE POWER SECTOR ........................................ 1

Economic Background . . ........................ . 1Sector Organization ...... ...................... 2Existing Public Power Facilities ............... ... 2Sector Planning ................................... 3The Power Market *............................... 3Development Plan ........ ...................... 4

III. THE BENEFICIARY ................... 5 S

PLN's Corporate Existence ... ...................... 5Organization ....... ............................... 6Management Consulting Effort and

Recovery Plan ...... ........................ 6Government Procedures ..... ....................... 9

IV. THE PROJECT ......... ................................... 10

Description of the Project ..... ................... 10Cost Estimate ..................................... 11Amount of Loan .................................... 12Engineering and Construction .. ..................... 12Procurement and Disbursement . ..................... 13

Ecology ........................................... 14

V. JUSTIFICATION .......................................... 14

Power Market in West Java ....................... 14Economic Justification ...... ...................... 16

This report was prepared by Messrs. H. Maeda and K. Stichenwirth and isbased on information obtained with the cooperation of Mr. E. B. Arnoldduring the mission to Indonesia in November/December 1974.

- 2 -

VI. FINANCIAL ASPECTS ....... ............................... 16

PLN's Financial Situation .................... ..... 16Subsidiary Loan ................................... 19Debt Service Limitation ..... ...................... 19Tariffs ........................................... 20Audit ... 20Accounting, Billing and Collection ............. ... 21Insurance ......................................... 21

VII. AGREEMENTS REACHED AND RECOMMENDATION .................. 22

ANNEXES

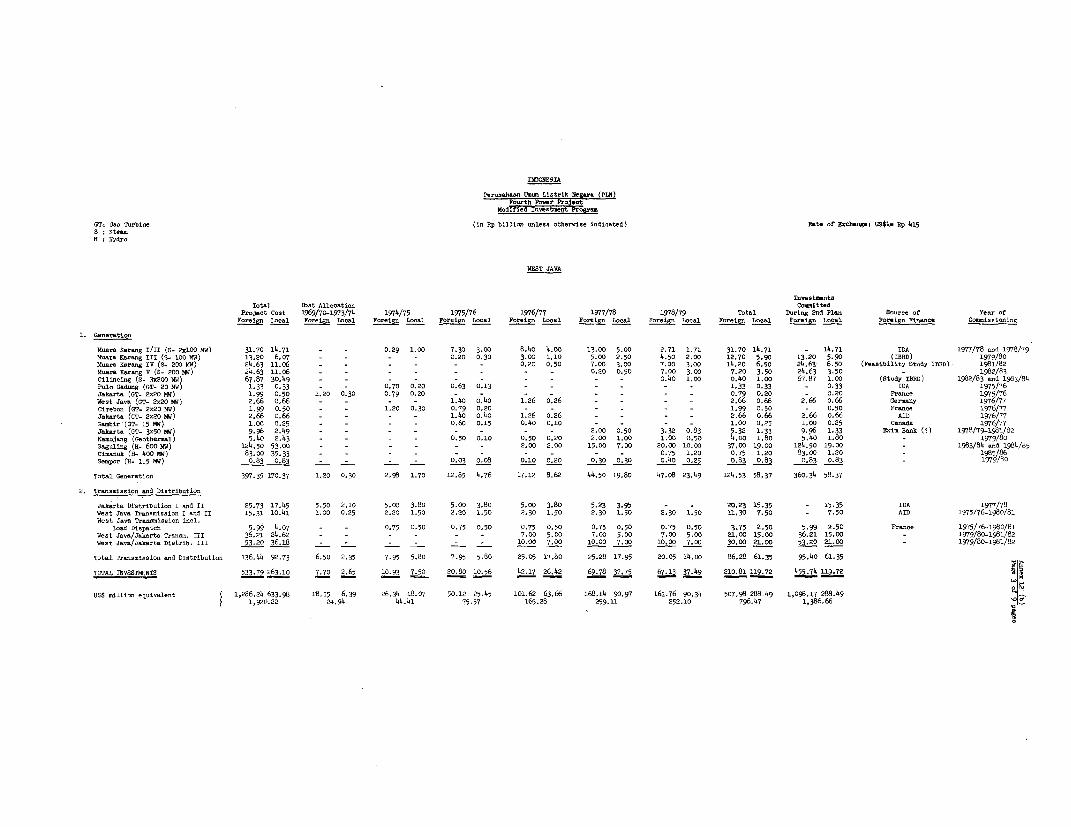

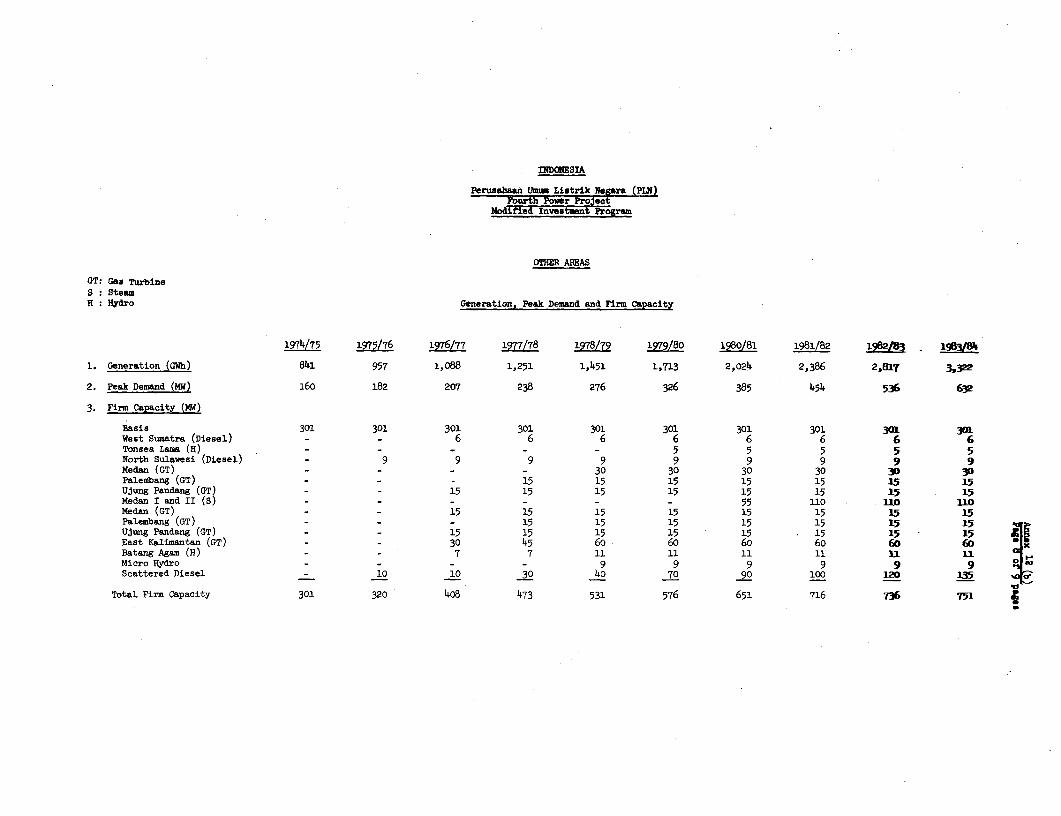

1. PLN's Organization Chart2. Installed Generating Capacity as of March 31, 19743. Peak Demand, Generation and Sales 19734. Energy Sales by Consumer Categories5. Actual and Forecast Generation (incl. Purchases) and Sales 1967-1978/796. Project Cost Estimate7. Economic Justification8. Construction Cost of Muara Karang Project (Units 1 and 2)-Analysis

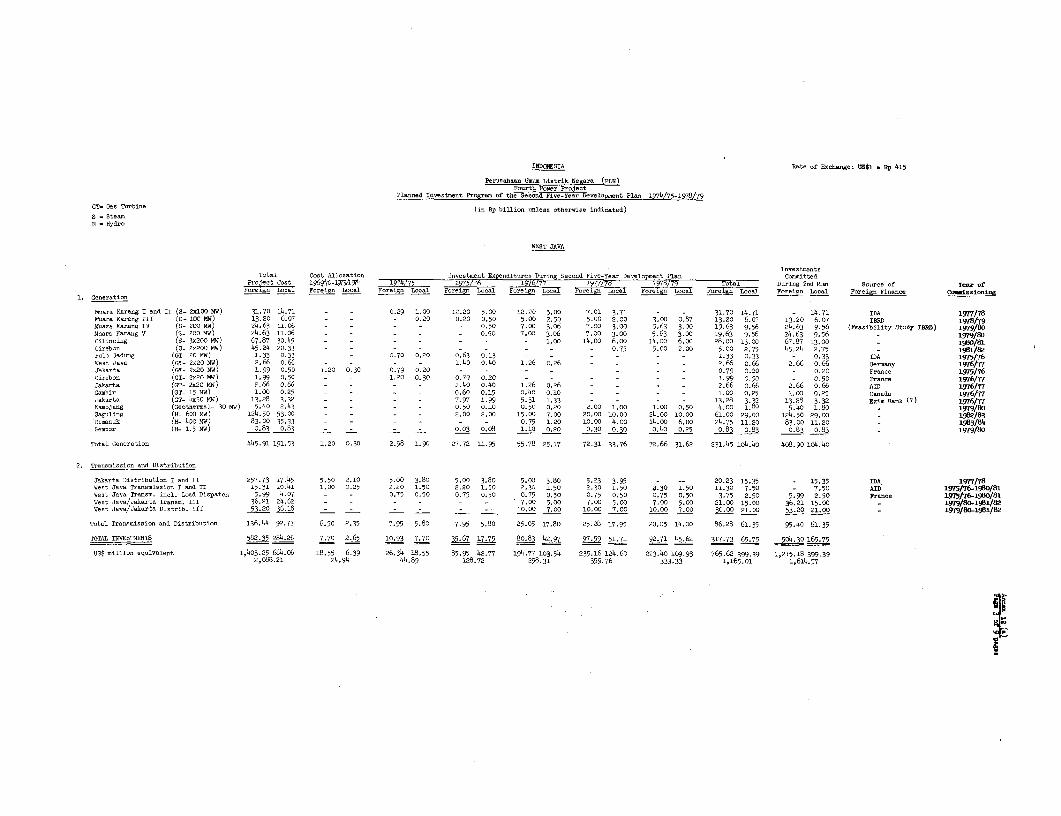

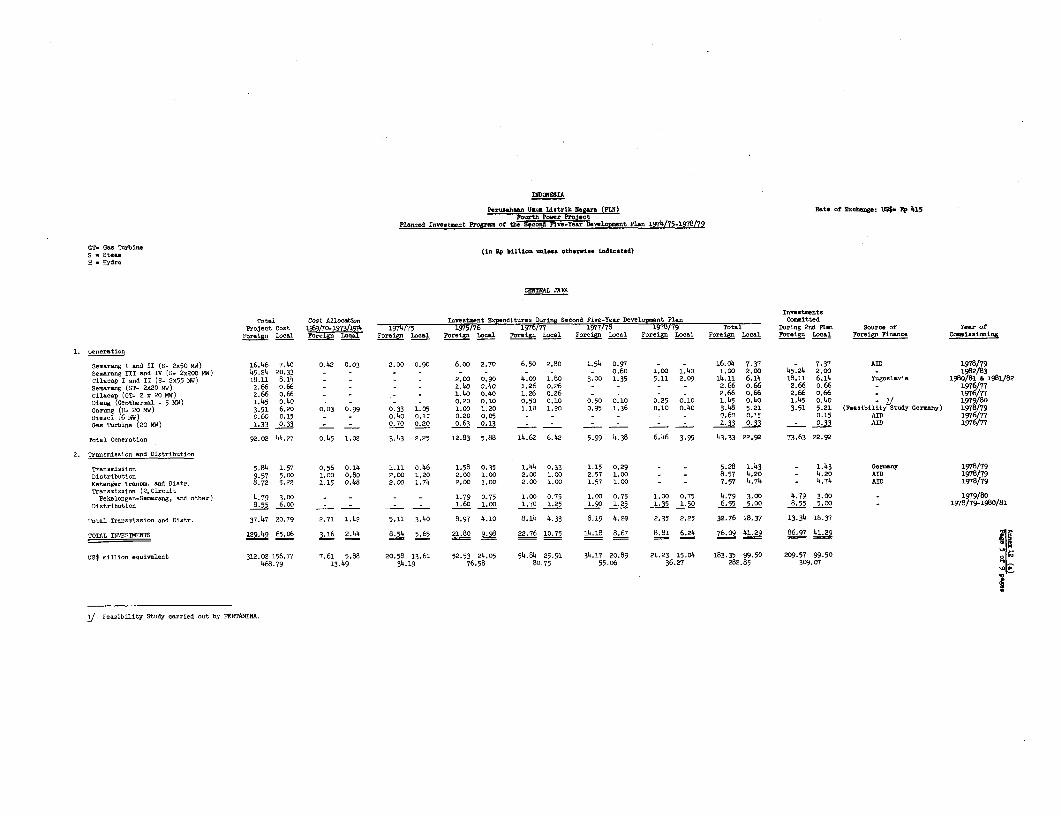

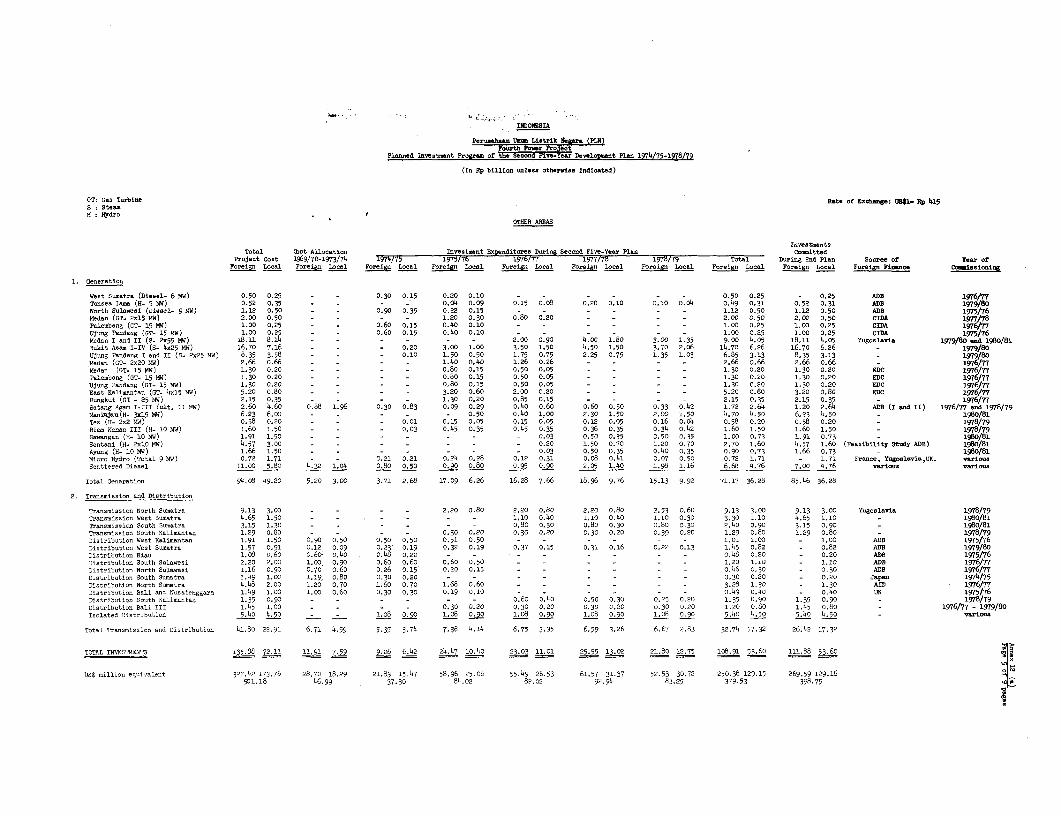

of Cost Overruns9. Schedule of Disbursements10. Tariffs11. Personnel12. Investment Program of the Second Five-Year Development Plan

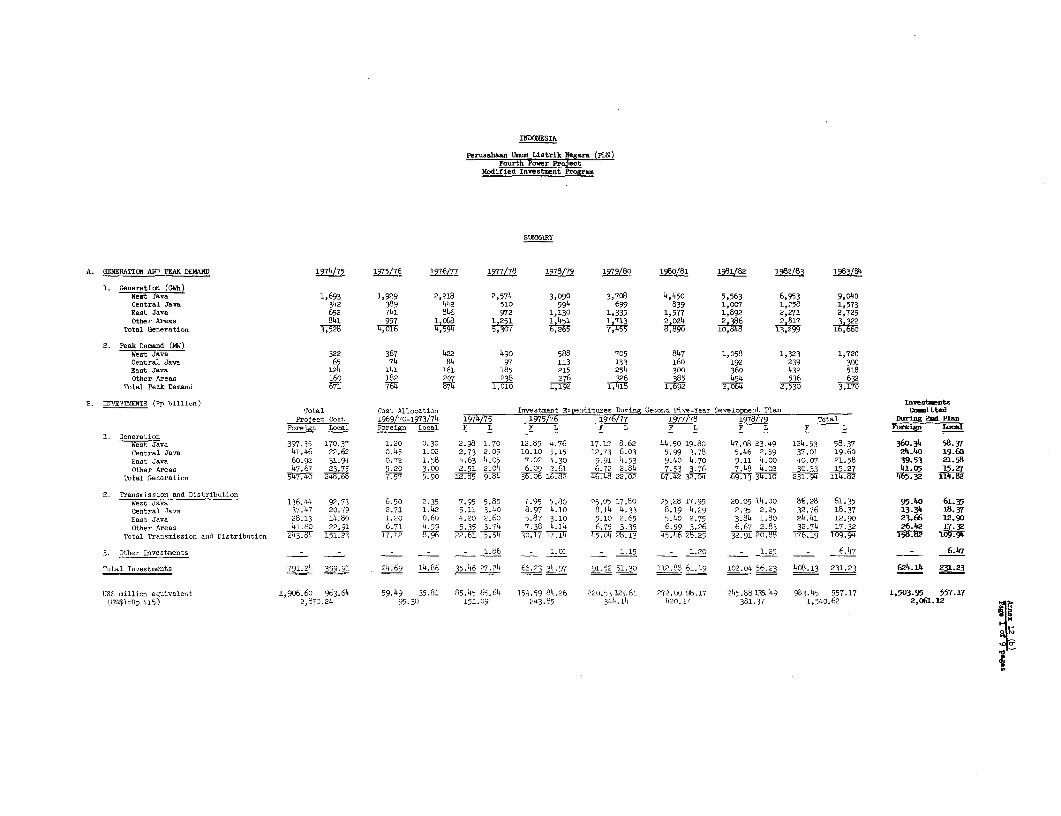

1974/75-1978/79(a) Planned(b) Modified

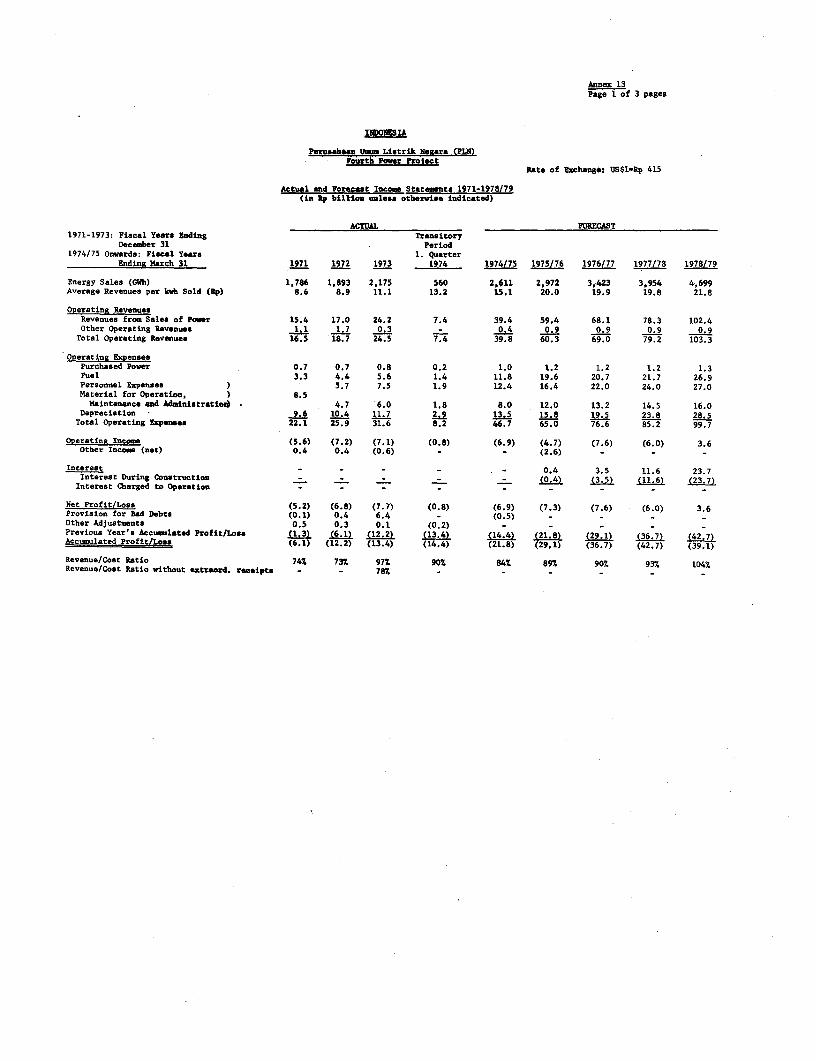

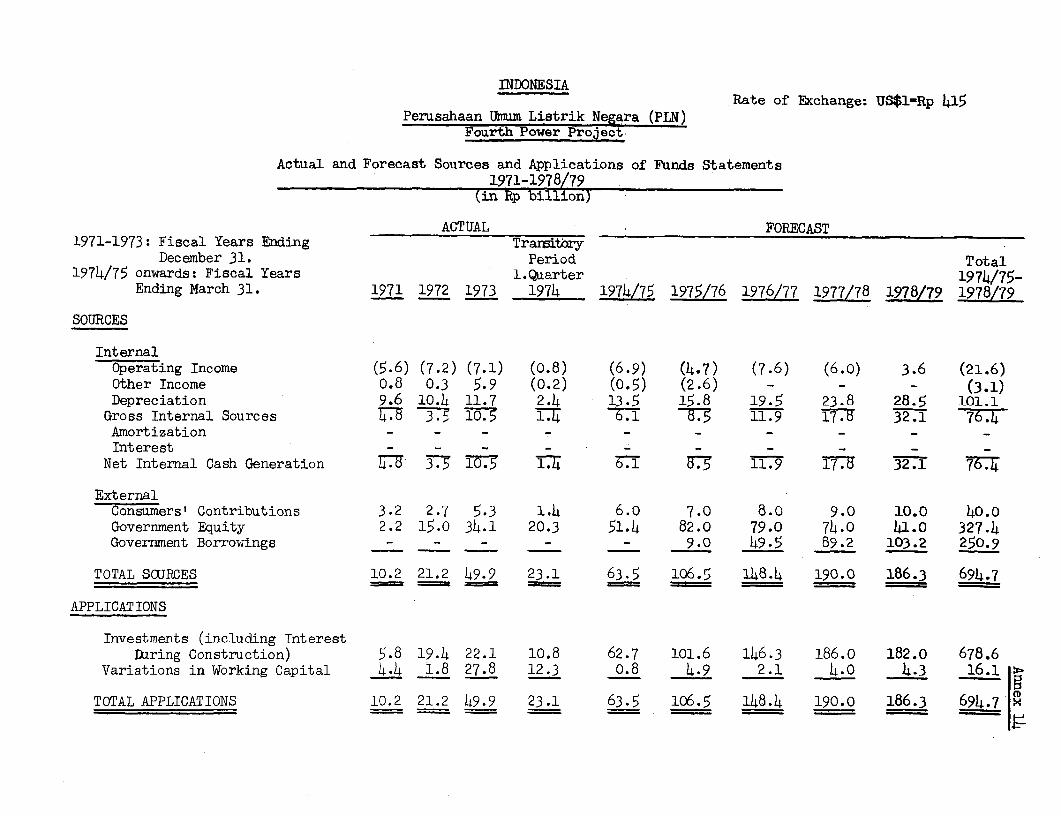

13. Actual and Forecast Income Statements 1971-1978/7914. Actual and Forecast Sources and Applications of Funds Statements

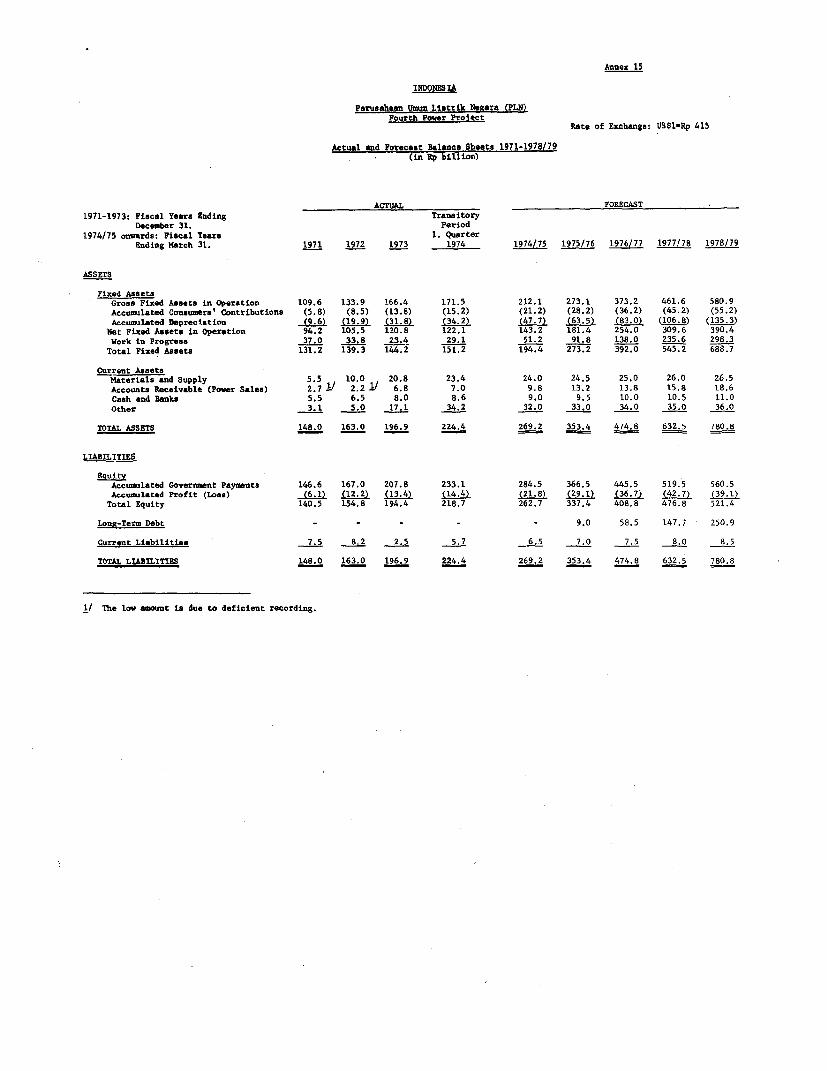

1971-1978/7915. Actual and Forecast Balance Sheets 1971-1978/7916. Status of Activities on Management Improvement

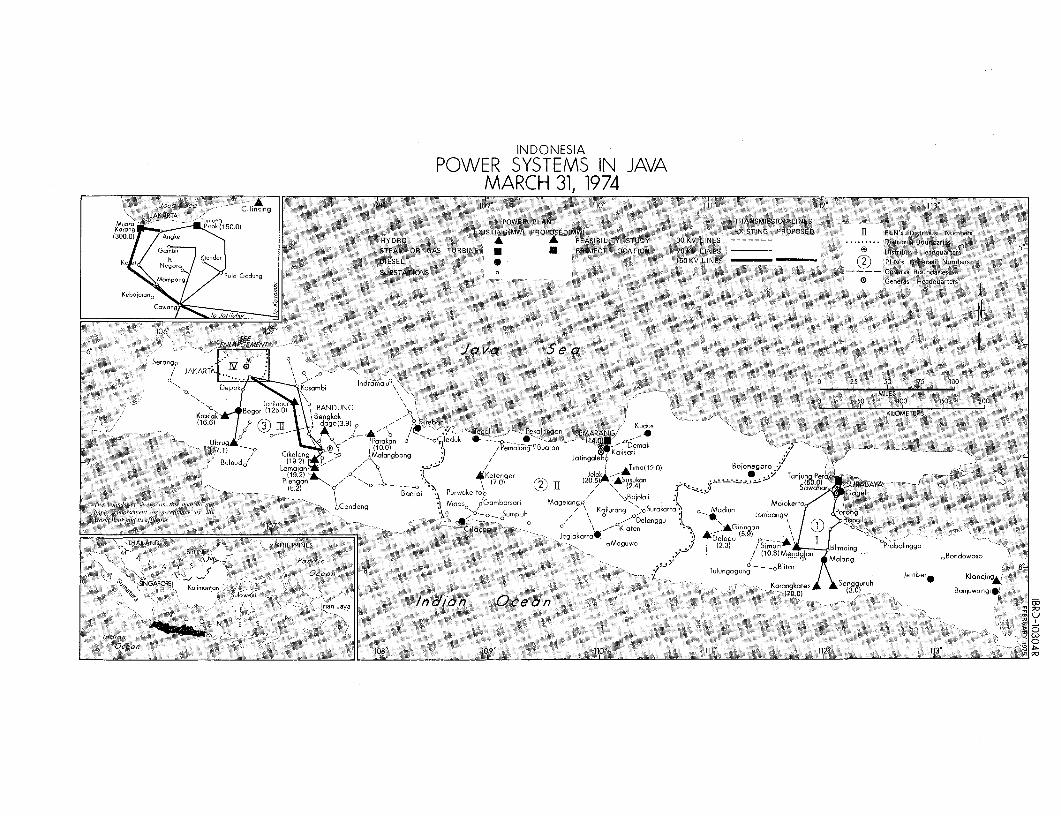

MAPS

IBRD-3912 RlIBRD-10304 R

INDONESIA

PERUSAHAAN UMUM LISTRIK NEGARA

APPRAISAL OF THE

FOURTH POWER PROJECT

SUMMARY AND CONCLUSIONS

(i) This report covers the appraisal of the Fourth Power Project con-sisting of the third 100 MW oil-fired generating unit of the Muara Karang

thermal power development, consulting services for the design of the fourthunit (200 MW) of the same station as well as for site investigation of afuture development, and advisory services and training. Total cost is

estimated at US$69.5 million equivalent, of which US$50.4 million is in theforeign exchange component. A Bank Loan of US$41 million equivalent isproposed representing the Project's foreign exchange cost excluding equip-ment for the training centers and interest on the Bank Loan during con-struction. Bank financing would cover 59% of the project cost.

(ii) The Project is the extension of the Muara Karang development,located on the bank of the Java sea in Jakarta, for which IDA had providedfinancing of the foreign exchange component of Units 1 and 2 through Credit399-IND (US$46 million equivalent). Since the appraisal of Credit 399 inlate-1972 dramatic cost increases have occurred. Based on results of bidsfor major equipment and a required design change of common facilities (inparticular the intake structure for cooling water), the total estimatedcost increased from $52 million to $106 million or by about US$54 millionout of which US$30 million are foreign exchange. It was decided that theBank Group would not finance any part of the cost overrun and the Governmentand PLN would have to raise the funds. Consequently, IDA financing ofUnits 1 and 2 represents 42% of the total cost. For all three units togetherBank Group financing amounts to 49%.

(iii) The potential growth of the power market is very high; it has been

estimated that PLN would have to increase sales by about 30% per year in theWest Java-area to catch up with the demand it is supposed to satisfy, whichpresently has to be covered through captive plant or is suppressed. Due tofinancial as well as physical constraints present assumptions are that PLN

is likely to be able to satisfy at most sales increases from about 14%(1974/75) to 30% (1983/84) in West Java (location of the Project) and 14% to25% in other areas.

(iv) The Muara Karang scileme is an essential element in the provisionof urgently required base load capacity in West Java. Despite the above-mentioned cost increases, the internal economic return of the first three100 MW units including investments required to market the station's output

- ii -

is about 17%. For the Project alone the respective return is 19%, reflectingthat investments for common facilities are included in Units 1 and 2. Further-more, the Project represents the least-cost solution for discount rates up to23%.

(v) Procurement of the goods and services financed from proceeds ofthe proposed Loan will be carried out on the basis of international com-petitive bidding under Bank Guidelines. Local preference in bid evaluationwill apply to purchases of equipment and material. It is expected that usecan be made of the options quoted for major equipment in the bidding forUnits 1 and 2.

(vi) The Financial Recovery Plan as included in the Credit 399-INDdocuments is underway and PLN is expected to achieve the financial targetsstipulated therein. Positive results have been achieved in most of themanagement improvement activities, particularly in the fields of training,operation and finance. Unfortunately the efforts to improve constructionmanagement activities are lagging behind. They will be the subject ofcontinued close supervision in future. Special training and managementconsulting efforts included in the proposed Loan are expected to furtherenhance PLN's development.

(vii) The engineering consultants' investigations indicate that noecological problems are foreseen. Design standards match the ones of theUS Environmental Protection Agency (EPA) since Indonesia has not yetestablished its own standards for environmental quality.

(viii) The proposed Loan would not only assist in financing badly neededexpansion of generating capacity, it would also provide the vehicle forcontinued Bank Group involvement in the process of institution building inPLN which started successfully with the previous Credits. Therefore,with agreements reached during negotiations, a loan of US$41 million witha 25 year term (including 5 years of grace) is recommended.

INDONESIA

PERUSAHAAN UMUM LISTRIK NEGARA

APPRAISAL OF THE

FOURTH POWER PROJECT

I. INTRODUCTION

1.01 The Government of Indonesia has requested financial assistance fora Project consisting of the third 100 MW unit for the oil-fired Muara Karangstation (Jakarta) including engineering consulting services for Unit 4, siteinvestigation of a future development, and advisory services and training.Consequently, a loan of US$41 million equivalent for a term of 25 years inclu-ding 5 years of grace covering the expected foreign exchange cost of theProject, exclusive of equipment for the training centers and interest on theBank Loan during construction, is proposed. The Loan would be granted tothe Government of Indonesia which will loan the funds to Perusahaan UmumListrik Negara (PLN), the Beneficiary, at terms equivalent to the Bank Loan.

1.02 The Loan would be the fourth Bank Group operation in the powersector with PLN as the beneficiary in all cases. The first two credits (165and 334-IND) were made to help finance the rehabilitation and expansion ofthe Jakarta electricity distribution system, whereas Credit 399-IND contri-buted to the construction of Units 1 and 2 of the Muara Karang development.

1.03 All three credits provide for a comprehensive managementand accounting consulting effort aimed at making PLN a sound public utility.Credits 165 and 334 provided the funds required for financing the consultantsand initiated the basic activities such as drafting laws and accountingsystems, and making a tariff study. With the successful completion of thesetasks, Credit 399-IND introduced an organized system of activities aimed atleading PLN to financial recovery in fiscal year 1978/79. The proposed Loancontinues the institution building effort through financing the foreign costof management advisers, training specialists and overseas fellowships.

1.04 This report was prepared by Messrs. H. Maeda and K. Stichenwirthand is based on information obtained with the cooperation of Mr. E. B. Arnoldduring the mission to Indonesia in November/December 1974.

II. THE POWER SECTOR

Economic Background

2.01 Indonesia has a total land area of approximately 1.9 million km2.But because the archipelago extends over a sea surface about 5 times larger,

- 2 -

distances are much longer than the country's size suggests-about 5,000 kmeast-west and 2,000 km north-south. Latest estimates place the populationat 130 million, growing at an annual rate of about 2.5%. The populationis distributed unevenly; almost two-thirds live on the island of Java whichrepresents only 7% of the total land area. The population density on Javais about 600 inhabitants per km2, one of the highest in the world.

2.02 The Second Five-Year Development Plan 1974/75-1978/79 (Repelita II)aimed originally at annual economic growth targets in real terms of 7.5%,with 13% for industry and 9% for mining and construction. With the increasein oil revenues and Indonesia's debt service capacity, the rate of invest-ment and consequent rate of growth are both likely to be reversed upwardduring the 5 year Plan period. With an estimated annual per capita GDPof US$125 in 1973, Indonesia ranks among the very poor countries in the world.Lasting improvements to the economy will require substantial and widespreadinvestment in agriculture and also in the industrial, mining and constructionsectors for which a well functioning power system will be crucial. Thepresent installed capacity of the public sector is only about 7 watts perinhabitant, and per capita annual consumption amounts to only 17 kwh (1973).These are among the lowest in the world.

Sector Organization

2.03 With certain exceptions (para. 2.04), the public power sector issynonymous with PLN, a Government-owned enterprise, responsible for genera-tion, transmission and distribution throughout the country. It was createdin 1961 through the merger of three nationalized utilities which in turn hadsucceeded Dutch owned private electricity corporations.

2.04 Although PLN has the exclusive right for generating, transmittingand distributing electric power, companies or individuals are allowed tobuild and operate generating stations for their own purposes if PLN isunable to provide service. In special cases, these auto-producers areallowed to distribute electricity to consumers in the surrounding areas.Generating stations below 50,000 kVA can be licensed by PLN but largerstations require approval by the Minister of Public Works and Power. Heacts upon PLN's recommendation.

2.05 Inadequate and unreliable public power supply has resulted incaptive plant installations representing an estimated 40% to 60% of the totalinstalled capacity (public plus captive). These installations representuneconomic investments, but despite PLN's very large investment program(para. 2.15), it will take years for this situation to normalize.

Existing Public Power Facilities

2.06 PLN's total installed capacity amounted to 792 MW by end-1973(exclusive of the 125 MW Juanda hydro station operated by the JatiluhurAuthority from which PLN purchases the output). Including Juanda, it con-sisted of 43% hydro, 25% steam and 32% diesel and gas turbine capacity.

-3-

The installations are scattered throughout the country, some in small unitsand stations. The system's largest plant is the 150 MW Tanjung Priok ins-tallation in Jakarta. Details are given in Annex 2.

2.07 With the exception of a 150 kV link between Jakarta and Bandung,even major load centers are not interconnected, resulting in high productioncosts and poor reliability. PLN's transmission facilities include about3,000 km of lines ranging from 25 kV to 150 kV, and an aggregate transformercapacity of about 1,350 MVA.

Sector Planning

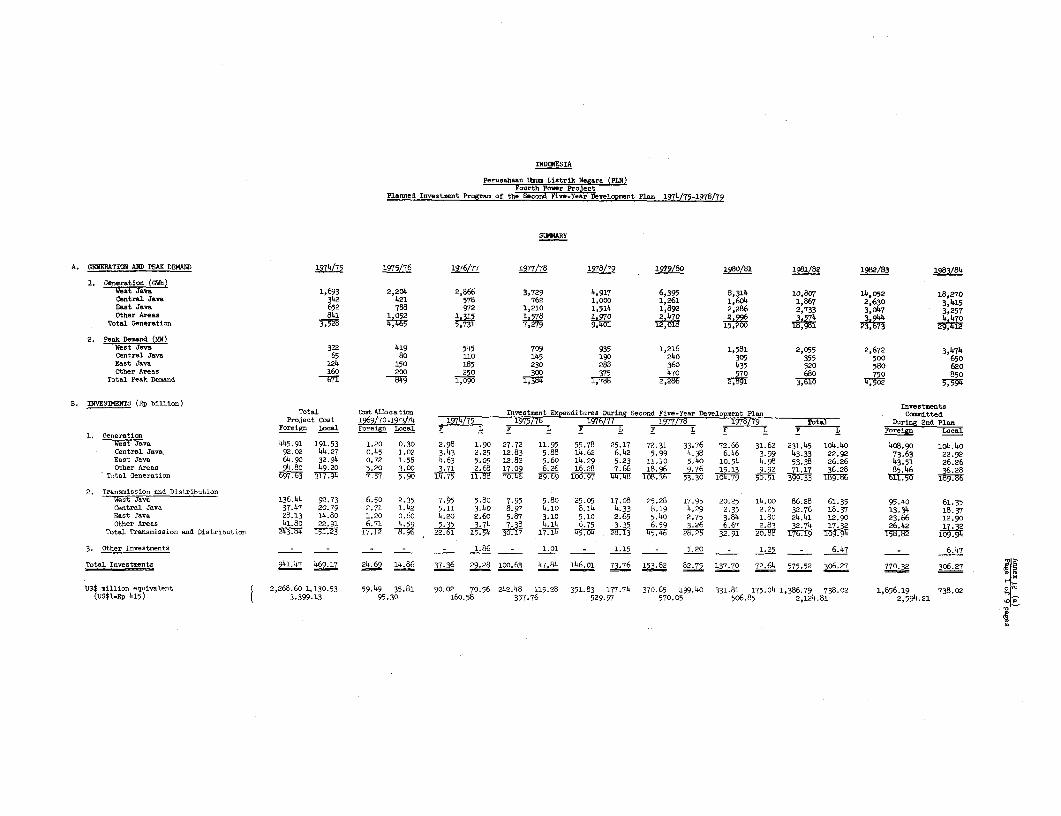

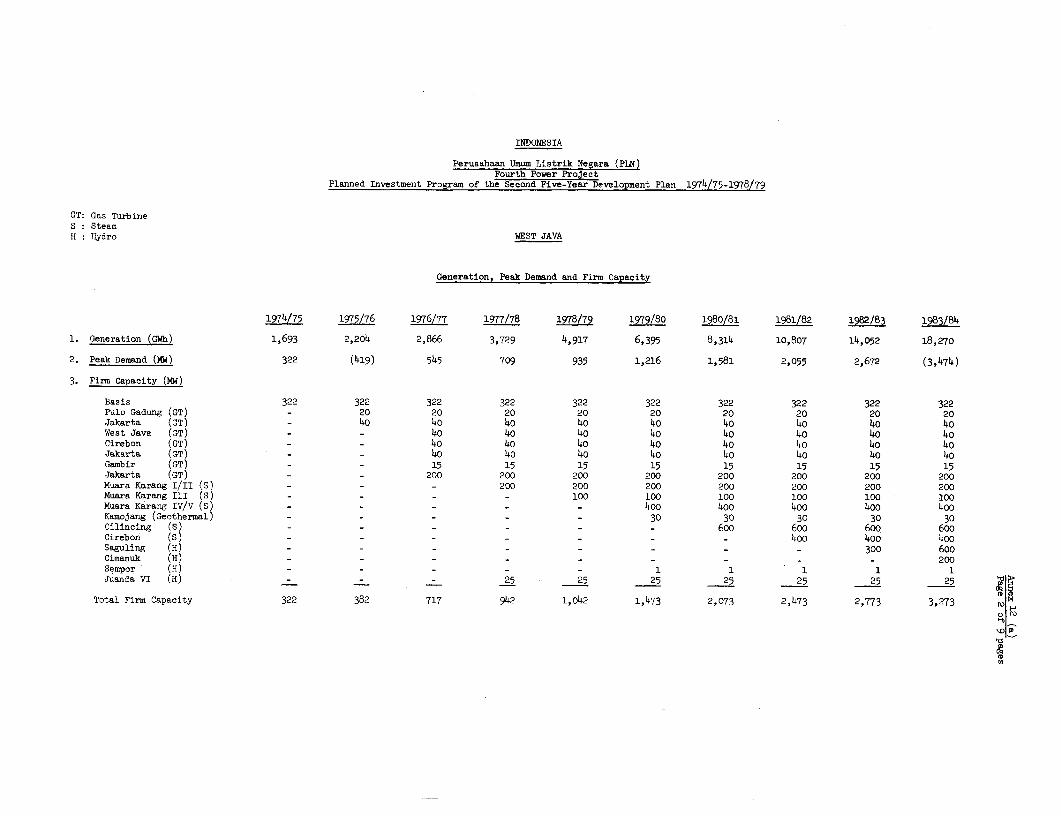

2.08 Past sector planning was partly determined by the foreign assistanceavailable and the domestic need to exchange capacity and gave insufficientemphasis to system standardization or the need for future interconnection.PLN's sector planning still needs strengthening. Apparently as a consequenceof the 1972 drought with subsequent blackouts due to lack of reserve capacity,PLN's development plan as incorporated in Repelita II (Annex 12 (a)) emphasizesgeneration investment but does not provide sufficient transmission anddistribution facilities to market the energy.

2.09 In order to create a sound basis for sector development on theimportant island of Java, Credit 399-IND includes funds for a system devel-opment study for the entire island. Consultants (Preece, Cardew and Rider)have been selected and the study started in November 1974. It is scheduledfor completion in July 1976. The objective is a system development planwhich will provide the guidelines for future power development and establishan appropriately balanced sector investment program.

The Power Market

2.10 As indicated in Annex 5, power consumption showed an increasinggrowth trend between 1967 and 1973, interrupted only in 1972, a severedrought year with generation cutbacks and blackouts. The first quarterof 1974 again indicates a slowdown, but this is because demand is approachingthe system's supply capability. New connections are severely repressed andthis situation is expected to continue until 1975/76 when new facilitieswill have been commissioned.

2.11 Development of power sales in the public power sector varied amongthe supply regions, with larger increases in West Java than in other areas;West Java, where the proposed Project is located, accounts for about 50%of the total market. Past results are summarized below:

-4-

TOTAL INDONESIA WEST JAVA

Generation 1/ Sales Annual Generation 1/ Sales Annual(GWh) (GWh) Sales Increase (Gwh) (GWh) Sales Increase

1967 1,607 1,158 - 789 529 -

1968 1,766 1,204 4% 846 537 2%

1969 1,872 1,454 21% 895 695 29%1970 2,084 1,589 9% 1,014 773 11%

1971 2,354 1,786 12% 1,175 898 16%1972 2,498 1,893 6% 1,268 960 7%

1973 2,932 2,175 15% 1,548 1,144 19%

1/ Including energy purchases.

2.12 By the end of the first quarter of 1974 PLN's customers totalled

about 1,031,000, of which about 90% were residential. The breakdown ofsales by consumer classes is shown in Annex 4. The strikingly low proportionof industrial sales underscores the extent of captive plant.

Development Plan

2.13 Future sales development will largely depend on PLN's capabilityto satisfy demand. Should it wish to meet by 1982 all the demand expectedby a recent West Java market study, installations to handle annual supplyincreases of about 30% would have to be commissioned during the next 7years. While this level of demand increase is entirely plausible, PLN isincapable of providing the necessary facilities due to physical as well asprobable financial constraints. The maximum satisfiable market developmentis judged to be about (Annex 5):

(i) West Java 14% annual increase in 1975/76 risinggradually to 30% in 1983/84; and

(ii) Other Areas : 14% annual increase in 1975/76 risinggradually to 25% in 1983/84.

These assumptions result in sales increases averaging about 14% (7% in1974/75) during Repelita II (1974/75 - 1978/79).

2.14 To permit the above sales increases, the following investments

will have to be made during the next several years (Annex 12 (b)):

-5 -

Total Cost of Investment Expendituresthe Program Before During Repelita II After

Repelita II (1974/75-1978/79) Repelita II

(1969/70-1973/74)3

(US$ million equivalent)

Foreign Cost 1,907 59 983 865

Local Cost 963 36 557 370

Total 2,870 95 1,540 1,235

This program would add about 3,000 MW to the existing 800 MW generation capa-city plus transmission and distribution. Although smaller than theinvestment planned by PLN (para. 2.15), it is very heavy and even if the moneybecomes available, it may be beyond PLN's capability to execute.

2.15 For the purpose of comparison, following is a summary of PLN'sinvestments as included in Repelita II (Annex 12(a)):

Total Cost of Investment Expendituresthe Program Before During Repelita II After

Repelita II (1974/75-1978/79) Repelita II(1969/70-1973/74) __

(US$ million equivalent)

Foreign Cost 2,268 59 1,387 822Local Cost 1,131 36 738 357

Total 3,399 95 2,125 1,179

This would add about 4,900 MW generation capacity and transmission/distribu-tion facilities.

III. THE BENEFICIARY

PLN's Corporate Existence

3.01 PLN's corporate existence is based on the 1972 Electricity Actwhich was issued as a Government decree within the framework of variousexisting laws. The charter does not provide the company with completelyindependent authority; important matters such as borrowing power, investmentpolicy, valuation of assets, personnel policy and salary structure and levelsare decided by the Government, represented in most cases by the Minister ofPublic Works and Power. However, such Government control over importantsectors of the economy and over Government enterprises is regarded as neces-sary and, with PLN's progressing impro-ement, the Government role in many

- 6 -

aspects of management i;as diminished. The covenant requiring Bank Groupconcurrence in material changes in governing laws affecting PLN has beenrepeated in the documents of the proposed Loan.

3.02 In matters of major importance the Minister is assisted by anAdvisory Board consisting of the Ministers of Finance, Industry, and NationalDevelopment Planning (Chairman of BAPPENAS, the Government planning agency).The Advisory Board provides a useful forum for officials concerned witheconomic matters to meet on problems of power sector development.

Organization

3.03 PLN's management (Board of Directors) is defined as the "represent-ative of the Minister, to carry out all basic management functions of theenterprise." It consists of a President Director and at least two otherDirectors. In addition to the President Director, there are presently four,responsible for planning, construction, operation,. and administration(including accounting and finances). The members of the Board are appointedand dismissed by the President of Indonesia upon recommendation by theMinister. They normally serve for a five-year term, but may be re-appointed.The President Director is responsible to the Minister and the Directors reportin their respective fields to the President Director. Decisions are commonlymade by consensus of the whole Board, a common feature in Indonesia.

3.04 PLN's regional organization (Annex 1) comprises 8 constructionregions (Construksi), 3 generation regions (Generasi), 4 distribution regions(Distribusi) and 11 operation tegions (Exploitasi); the latter cover areaswhere activities are too small to justify subdivision. The organizationalstructure is oriented towards practical needs.

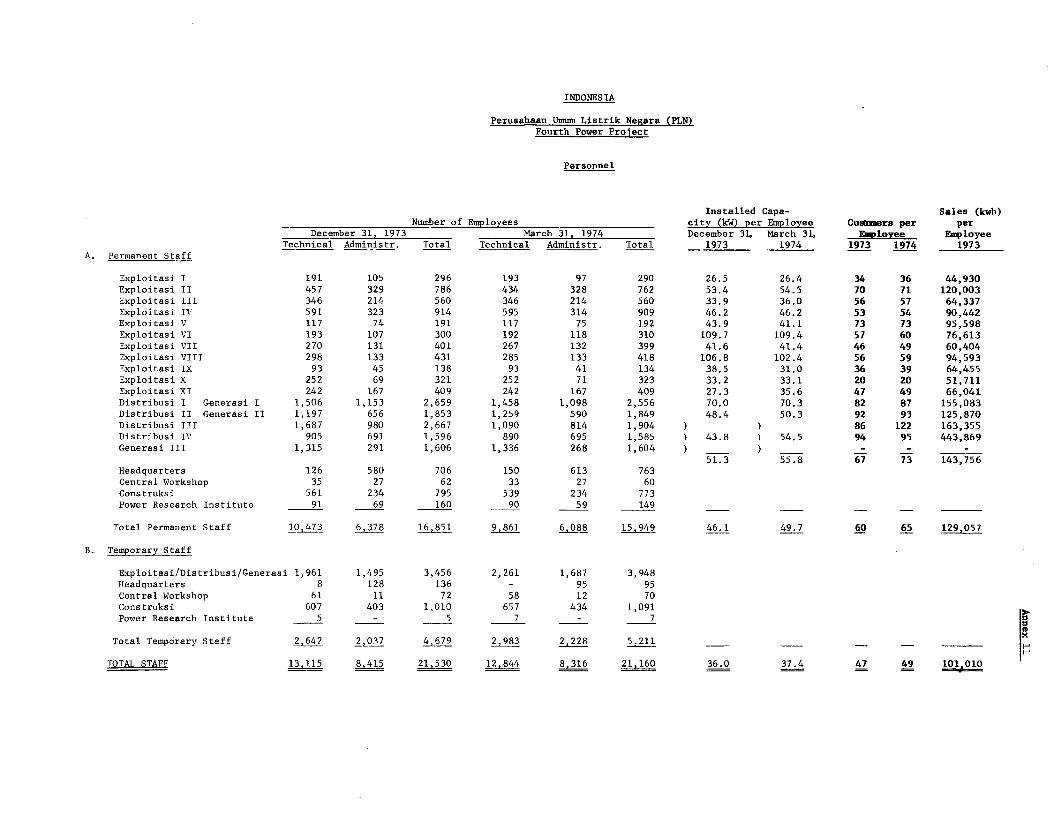

3.05 As of March 1974 PLN had a total staff of 21,160 (Annex 11), ofwhich 5,211 were temporary. Although the number of employees is high bynormal standards, reductions are unlikely because of the size of the supplyarea and the Government's employment-oriented policies. Despite the largenumber employed PLN suffers from a severe shortage of qualified staff; forinstance, its personnel upgrading program would require more civil andelectro-mechanical engineers annually than are presently graduating from alltechnical universities in Indonesia. The scholarship program included inthe Projec; is designed to alleviate this pressing problem by upgradingthe professional skill of graduated engineers (para. 3.11).

Management Consulting Effort and Recovery Plan

3.06 PLN was in a clearly chaotic state at the time of the Bank Group'sfirst involvement in the power sector (1969). The division of responsibilitybetween the Government and PLI was not defined, PLN's legal basis was un-satisfactory, records were unavailable and the financial situation, althoughconfused was clearly bad. To help remedy the situation, the Bank Grouphelped finance through Credits 165 and 334-IND a comprehensive managementconsulting effort, for which the French firm of SOFRELEC was selected.SOFRELEC was assisted in accounting matters by Peat, Marwick and Mitchell.

3.07 It took time before SOFRELEC could formulate recommendations withrespect to PLN's problems. Records had to be reconstructed and assetsphysically identified; large outstanding consumer accounts had to beverified and means found for their settlement; tariff levels and structurehad to be studied. The initial phase of the consultant's work took abouttwo years and consisted to a considerable degree of essential fact finding.The main accomplishments during the period included:

(i) draft of the Electricity Act (promulgated in 1972 after exten-sive discussions with representatives of the Bank Group);

(ii) recommendations on a new structure and level of tariffs(introduced with a general increase of 40% in June 1973);

(iii) draft of a functional organization (introduced with somemodifications in March 1973);

(iv) preparation of an accounting system and recommendations oncash management and control, inventory control, consumeradministration, mechanization and budgeting (in the processof implementation throughout the enterprise);

(v) revaluation of assets (introduced as of December 31,1971; and

(vi) recommendations on personnel regulations and administration,job analysis, salary'structure and training (some of therecommendations have been implemented, others are underdiscussion. A number of the recommendations meet withGovernment resistance since although suitable fora commercially oriented entity like PLN they often conflictwith regulations applicable to Government agencies).

3.08 At the time of appraisal for Credit 399-IND in late 1972 PLN'sproblems were better identified than previously and recommendations fortheir solution were in hand. SOFRELEC's investigations had revealed thatPLN's financial situation was worse than anticipated with high operatinglosses and very low internal cash generation. Consequently a "recoveryplan" designed to improve PLN's management capabilities and to overcome itsfinancial weaknesses over time was made a part of the project and incor-porated in the 399-IND documents. Its main features include:

(i) a detailed plan of activities designed to improve PLN'soperations and, as a consequence, its financial position;

(ii) annual programs of the activities to be taken towardsimprovement. These programs are discussed with andclosely supervised by Bank staff; and

-8-

(iii) improvement of PLN's finances to the point where alloperating expenses would be covered by revenues byFY 1978/79. PLN agreed to make all efforts to meetinterim targets of 80% revenue/cost coverage in FY 1974/75and 90% in FY 1976/77.

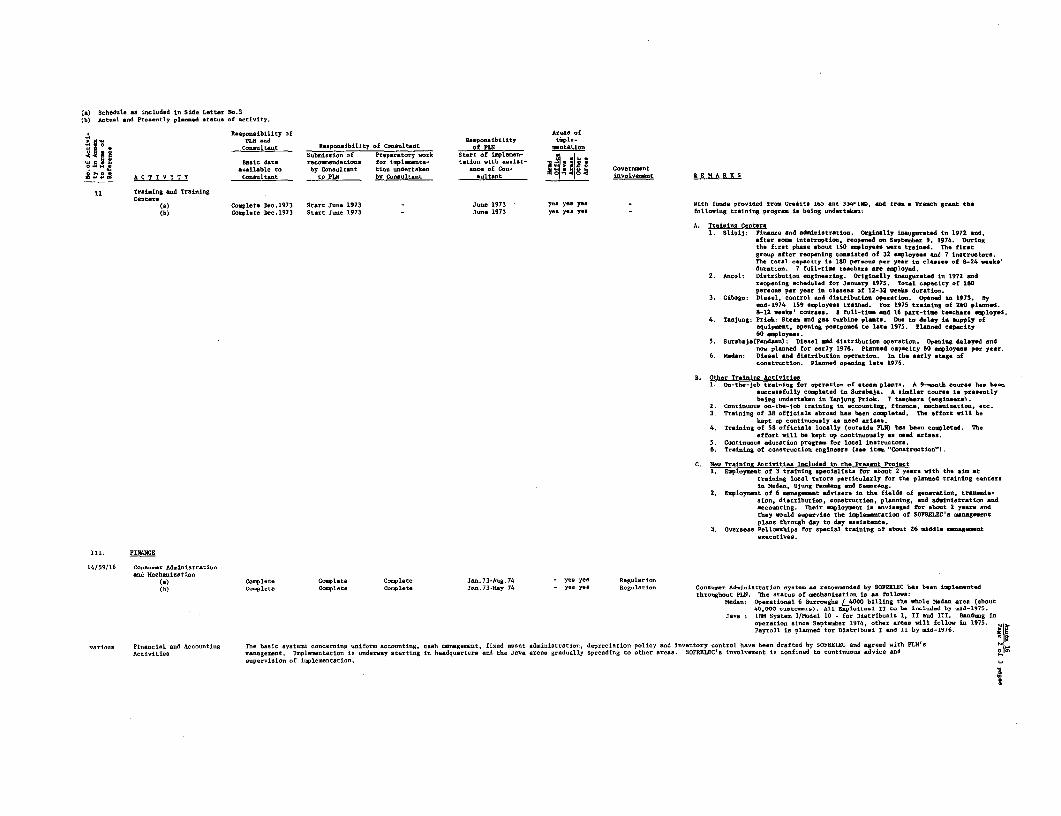

3.09 On July 16, 1974 the Association's Board received at its requesta status report on the recovery plan (Memorandum on the Progress under theRecovery Plan - IDA/SecM 74-230). Annex 16 describes the present situationand Annex 13 summarizes the prospects of meeting the financial targets.In summary:

(i) activities to strengthen system planning are underway.However, progress is slow as it is with personnel trainingin general because of a severe shortage of adequately qualifiedpersonnel to be trained. Problems also arise from Governmentregulations concerning salary levels and structures, andpromotions, which make incentive oriented plans difficult toimplement;

(ii) good progress has been made in improving accounting andfinancial control. Only occasional assistance by theconsultants is now required;

(iii) efforts to improve the management of construction activitieshave shown fewer results than the other activities. This isparticularly disappointing since improved project implement-ation capability is essential for PLN's full recovery. Whilenot entirely PLN's fault, as complex and cumbersome Governmentregulations seriously delay project implementation, there is stillmuch that could be done within PLN itself to overcome these prob-lems. They will be the subject of continued supervision;

(iv) good results have been achieved in operations (maintenanceprocedures and steam plant operation). Further progress incost economizing requires accelerated system improvements, andthis is directly linked to progress of the constructiongroup; and

(v) preliminary results indicate that the first 80% revenue/costtarget in EY1974/75 was reached and expectations are that fullfinancial recovery will be attained by FY1978/79 as scheduled.

3.10 The efforts made to date to turn PLN into a sound public utilityhave yielded positive resultj despite temporary setbacks. On balance theyhave been successful. Future activities will continue to concentrate onmanagement improvement largely through day to day assistance by the con-sultants, and on personnel training. Among other points, PLN will inaccordance with the recovery plan concentrate during the next year on (fordetails see Annex 16):

-9-

(i) training of about 500 employees in PLN-owned trainingcenters, and on-the-job;

(ii) introducing a comprehensive insurance system; and

(iii) improving the construction department (in particularprocurement and contract management, and streamliningof budget procedures) and strengthening the organizationin the regional construction offices (Construksi).

3.11 To help strengthen PLN's organization and to overcome at least toa certain degree the shortage of trained personnel, funds for financing theforeign exchange cost of the following management consulting and trainingelements in addition to those contained in the financial recovery plan havebeen included in the proposed Loan:

(i) employment of three training specialists for about twoyears with the aim of training local tutors particularlyfor the planned training centers in Medan, Ujung Pandangand Semarang;

(ii) employment of six management advisers in the fields ofgeneration, transmission, distribution, construction,planning, and administration and accounting. Theirassignment would be for about two years. After initiallyworking together with SOFRELEC, they would gradually takeover the responsibility of supervising the implementationof SOFRELEC's management plans through day-to-day assistance;and

(iii) overseas fellowships for special training of about 26 middlemanagement executives.

It has been agreed during negotiations that qualification, experience andterms and conditions of employment of the above-mentioned specialists shouldbe satisfactory to the Bank.

Government Procedures

3.12 Factors which severely hinder efficient project implementationinclude:

(i) customs clearance at Tanjung Priok harbor in about 50%of the cases investigated averaged about 70 days, in twocases about 250 days;

(ii) budget control procedures (see below); and

(iii) procedures for establishing letters of credit and issuingimport licenses which take up to 6 months.

- 10 -

Until mid-1974, budgeted local expenditure funds were disbursed to PLN itemby item through regional treasury offices, a most cumbersome process. How-ever, recently the Government agreed to advance budgeted funds quarterly toprovide PLN with more flexibility than before in fund management. This isa step in the right direction and this mechanism should be refined so as toincrease further PLN's financial flexibility.

3.13 The problems associated with the customs clearance procedureswere discussed during negotiations. An understanding was reached that inthe course of the next year the Ministry of Public Works and Power will developspecific recommendations for improvement which will be discussed with theBank and that an effort will be made to institute the recommended improve-ments. This improvement effort will in the end benefit all sectors of theeconomy.

IV. THE PROJECT

Description of the Project

4.01 The proposed Project consists of:

(a) construction of a third unit (100 MW) at the Muara Karangthermal power plant including engineering design for afourth unit (para 4.02);

A

(b) physical investigations of the site of a new thermal powerplant in West Java (para 4.03); and

(c) advisory services and training, including fellowships(para 3.11).

4.02 The project site, located in the northwest outskirts of Jakarta,will provide an ultimate capacity of 700 MW with five units installed. Thefirst two 100 MW units are being financed under Credit 399-IND and arepresently under construction. The severe inflation which has taken placesince project appraisal in late-1972 has doubled the project cost; theforeign comaponent is now expected to be about 70% higher than the originalestimate (Annex 8). However, no supplemental financing by the Bank isproposed. The No. 3 unit will be a non-reheat, oil-fired type, identicalto the first two units. It will supply the Jakarta area by 150 kV transmissionlines included in the first stage of the project (Units 1 and 2). Alsoincluded are engineering services for a detailed design of Unit 4 (200 MW)which should be initiated immediately.

4.03 PLN will need a new site for the next thermal power plant to becommissioned in the early 1980's when the Muara Karang site will have beenfully developed. The most probable sites presently under consideration are

- 11 -

Cilincing, in the eastern suburbs of Jakarta, and Cirebon, about 200 km eastof Jakarta. The consultants for the on-going Java System Development Studyfinanced under Credit 399-IND will determine the site priority and optimumdevelopment scheme for the station from the viewpoint of overall systemplanning. The proposed study would concentrate on physical investigationsof the first priority site such as geology, oceanography, environment andtransportation requirement and would include a preliminary design and costestimate of the plant.

Cost Estimate

4.04 The detailed cost estimate of the Project is given in Annex 6and summarized below:

Billions of Rupiahs Millions of US DollarsLocal Foreign Total Local Foreign Total

Muara Karang Unit 3

Site Development 1.46 - 1.46 3.52 - 3.52General Construction 1.74 3.62 5.36 4.19 8.72 12.91Equipment and Materials 0.05 7.76 7.81 0.11 18.71 18.82Engineering 0.13 1.48 1.61 0.31 3.57 3.88

Base Cost Estimate 3.38 12.86 16.24 8.13 31.00 39.13

Contingencies:Physical 0.32 0.83 1.15 0.77 2.00 2.77Price 1.44 2.24 3.68 3.48 5.40 8.88

Sub-total 5.14 15.93 21.07 12.38 38.40 50.78

Study 0.12 0.29 0.41 0.30 0.70 1.00

Advisory Services andTraining 2.68 1.35 4.03 6.45 3.25 9.70

Total 7.94 17.57 25.51 19.13 42.35 61.48

Interest cfuringConstruction on BankLoan - 3.32 3.32 - 8.00 8.00

Grand Total 7.94 20.89 28.83 19.13 50.35 69.48_ . = _

4.05 The cost estimate for the Muara Karang project was prepared byBlack & Veatch International (BVI) of U.S.A., the consultant retained for thefirst stage. The cost of the major equipment is based on bid prices forUnits 1 and 2 which included an option for Unit 3. Other costs of supplyand construction including the local component are based on recent experiencesof a similar project at Semarang, Central Java, and the local bidding on

- 12 -

civil works for the Muara Karang Units 1 and 2. They represent early-1975prices. About two-thirds of the engineering cost are for detailed designof Unit 4 which will be 200 MW. Since the project design is in an advancedstage, a physical contingency of 5% for equipment and 10% for constructionshould prove adequate. Price contingencies averaging about 8% for majorequipment supply are based on escalation provisions included in the proposals.Tnis is low because some suppliers offered firm prices for certain items.For other items annual inflation rates of 12% in 1975, 10% in 1976 and 8%thereafter for equipment and 16% in 1975, 14% in 1976 and 12% in later yearsfor civil works have been applied. The overall price contingency amounts to21% of the project cost including the physical contingency.

4.06 The estimated total cost of Unit 3 amounts to US$47.8 millionequivalent after deducting the engineering cost for Unit 4 and interest onBank loan during construction. This represents a unit cost of US$478/kWinstalled. Adding to this the revised cost of Units 1 and 2 (Annex 8) thetotal cost for 3 x 100 MW is now estimated at US$153.8 million. This includesthe cost of transmission and other common facilities required for the finalcapacity of 700 MW. If adjustments are made for the cost of common facilities,the average cost for the three 100 MW units is US$397/kW and US$442/kW in-stalled, , before and after price escalation. This is of the correct orderof magnitude for 100 MW and similar sized oil-fired units at early 1975 prices.

4.07 The cost estimates for the study, advisory services and traininghave been prepared by PLN based on man-months required for such activitiesand recent experiences of building similar training centers.

Amount of Loan

4.08 The Project's foreign exchange component of US$50.4 million equiv-alent represents 72% of the total cost of US$69.5 million equivalent includinginterest during construction on the Bank loan. This percentage is highbecause major civil works are included in the first stage project partiallyfinanced by Credit 399 IND. The proposed Loan would cover the foreign ex-change cost of the Project, except for the supply of the equipment for thetraining centers which is not suitable for international competitive biddingand the interest on the Bank Loan during construction; these items would befinanced by PLN and the Government. The total amount of the Loan would beUS$41 million, representing 59% of the total capital cost of the Project,including interest during construction on the Bank Loan.

Engineering and Construction

4.09 Credit 399-IND prov des financing for engineering services of Units1 and 2. PLN has retained BVI for this purpose and intends to extend thecontract to cover Units 3 and 4. The service for Unit 3 is for the detaileddesign and construction supervision with an estimated man-month requirementof 255. The service for Unit 4 will cover the detailed design, preparationof bidding documents and bid evaluation with an estimated man-month require-ment of 626; this is high because of a new design required for a larger unit.

- 13 -

This arrangement is satisfactory to the Bank and the proposed Loan includesfinancing of this contract extension.

4.10 Major items of site development such as site fill and buildingan intake canal are being carried out by local contractors under the firststage. The second stage site development including piling, minor mechanicalworks and some preparation works for Unit 4 will also be locally contracted.These works are financed by PLN. However, as with Units 1 and 2, generalconstruction contractor will be employed for structural, mechanical andelectrical construction including erection of major equipment. The contractsinclude sizeable foreign exchange costs which will be financed under theproposed Loan. In the interest of expediting and economizing the constructionwork, it was agreed during negotiations that the general constructioncontract(s) would cover the erection of all three units (paras 4.14-4.15).

4.11 PLN has established a construction team for the Project within itsheadquarters. Unit 3 is scheduled for completion in mid-1979, one year afterthe commissioning of Unit 2.

4.12 The study of the next thermal power site will be carried out byengineering consultants satisfactory to the Bank under a separate contract.The study is expected to take about one year with an estimated man-monthrequirement of 100.

Procurement and Disbursement

4.13 Bids for the supply of major equipment for Units 1 and 2 includedoption offers for Unit 3 valid until November 1975. PLN intends to exercisethe options since prices are reasonable under the present market situationand, more importantly, the construction period would be shortened by at leastsix months; additional advantages can be expected through equipment standard-ization and simplified engineering and construction work.

4.14 Assuming PLN exercises the option for major equipment, remainingitems to be procured are control equipment, structural equipment and thegeneral construction contract. Procurement will follow internationalcompetitive bidding in accordance with the Bank's Guidelines. During nego-tiations PLN agreed to let the general construction contract(s) covering allthree units under international competitive bidding since the Bank financesa portion of the foreign exchange cost of the contract(s). Since somestructural equipment could be supplied by local industries, the Loandocuments include the usual margin of preference for local manufacturers.Some civil works will be financed locally and the general construction con-tract, which will likely be beyond local capability, will largely be a supplyand erection type with some local subcontractor participation. Hence, thereare no grounds for a local preference for civil contractors and none isprovided.

4.15 Disbursement will be made against the full foreign exchange costof equipment, materials and consulting services. Should local manufacturers

- 14 -

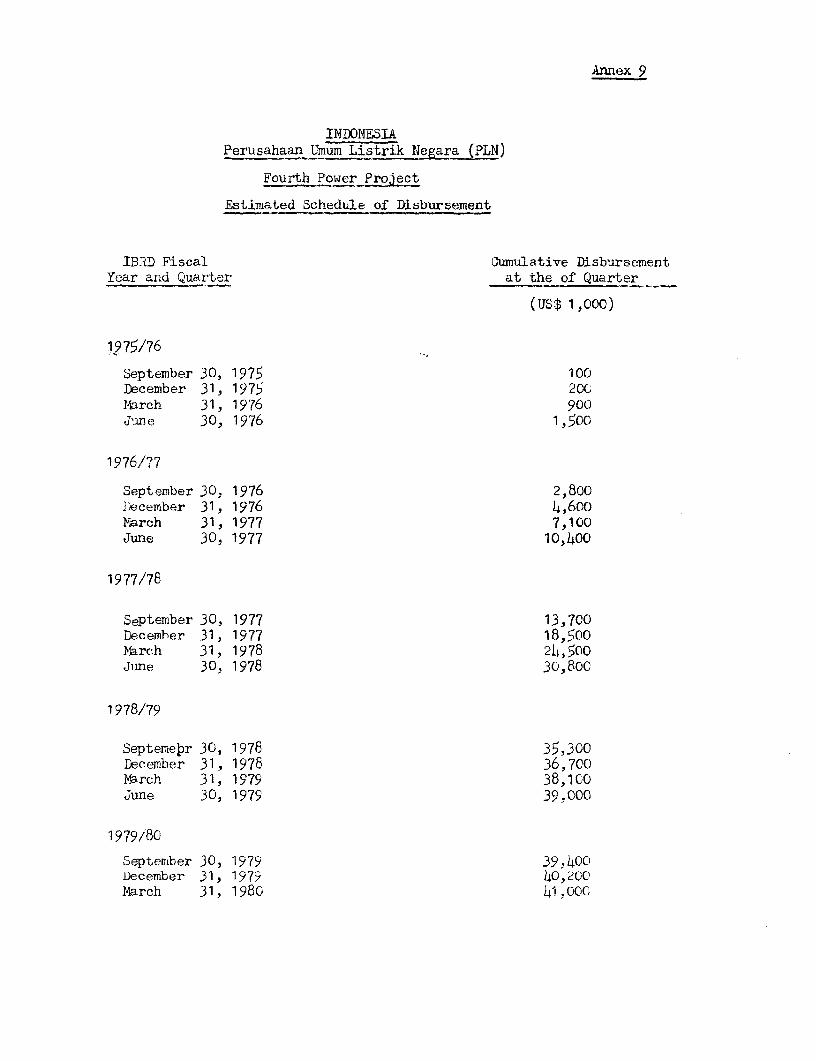

win contracts for equipment and materials, disbursement would be made against95% of the ex-factory price, the remaining 5% representing the estimatedaverage of local taxes. For the general construction contract(s) coveringall three units, disbursement will be made against 30% of the total expend-itures up to US$12.4 million. This would represent the full foreign exchangecost for Unit 3 included in the contract(s). No disbursement will be madefor expenditures prior to Loan signing. The estimated schedule of disburse-ments of the proposed Loan is shown in Annex 9. Any surplus funds remainingafter completion of the Project will be cancelled, unless there are goodreasons for applying savings to related works.

Ecology

4.16 No major ecological problems are expected. The consultants havecarried out surveys on meteorological and oceanographic conditions, andthe flora and fauna in the vicinity of the project area. Since Indonesiahas not yet ruled on matters of environmental quality, the US EnvironmentalProtection Agency (EPA) standards have been used as design criteria. Thecalculated maximum particulate concentration at ground level due to powerplant exhaust gases is well below the EPA standards and a mechanical preci-pitator will be sufficient to remove solid particles in the gas. Space isprovided for future installation of electrostatic precipitators, should itbecome necessary. A 75 meter stack will keep the sulphur dioxide pollutionbelow EPA ambient air standards even for the high-sulphur mid-eastern oilwhich PLN might use instead of more valuable low-sulphur indigenous oil.Cooling water from the plant will be discharged directly into the Java Seawhich forms a very shallow Area with a mudsilt for about one kilometer fromthe shoreline. The thermal plume of the discharged water is expected todissipate before it reaches the area where any consumable fish or shellfishof significant value exist.

V. JUSTIFICATION

Power Market in West Java

5.01 During the First Five-Year Plan period (1969-1973) electricitysales in West Java increased at an average rate of 16.3% per year. Thisgrowth rate, although high,does not reflect the economy's real needs forpower. It would have been much higher if PLN had been able to satisfy allthe potential demand. PLN severely restricts consumer connections in orderto keep the maximum demand within its capability. This has given rise to asubstantial installation of expensive self-generating plant by industries,commercial buildings, hotels and even by domestic consumers. Although exactfigures for these captive plants are not known, the total installed capacityis estimated to equal the supply capability of PLN. A 100 MW addition tosystem capability in 1972 was loaded in less than two years and at the endof 1974 maximum system demand was 300 MW against a total capability of325 MW, leaving little operating reserve.

- 15 -

5.02 As of November, 1974 PLN had applications for new connection inWest Java of 330 1VA for 1975 and 210 MIVA for 1976. This alone wouldrequire tripling of generating capacity in two years. It is apparent thatduring the next few years demand growth will depend entirely on PLN'scapability to supply. According to a study done by consultants (Chas. T.Main) PLN would have to increase its supply capability at an annual rateof 32% in Central and West Java, to fully satisfy suppressed demand by 1982.Based on this, PLN will try to fill the supply/demand gap as much as possibleby installing gas turbines until the first base-load Muara Karang unit iscommissioned in late 1977. PLN has already secured financing for 13 gasturbines with a total capacity of 284 MW; three have been commissioned.It is seeking financing for an additional 200 MW. However, consideringPLN's weakness in construction management and its inadequate distributionsystems, a more realistic assumption of satisfiable demand increase wouldbe 14-20%"o per year up to 1980 and 25-30% thereafter. The market forecastfor 1979 when Unit 3 will be commissioned would therefore be as follows:

Fiscal Year 1974 1979 Rate of Growth% p.a.

West Java

Energy Pequirement (GWh) 1,693 3,708 17.0Peak Demand (MW) 322 705 17.0

Central Java

Energy Requirement (GWh) 342 699 15.4Peak Demand (MW) 65 133 15.4

/1Combined-

Energy Requirement (GWh) - 4,407 -Peak Demand (MW) - 838 -

/1 The first interconnection between Central and West Java is expectedto be completed by December, 1978.

5.03 -The investment program based on this forecast (Annnex 12 (b)) showsthat generation capacity of the combined system at the end of 1978 will con-sist of 38% steam, 37% gas turbine and 25% hydro power. Heavy dependenceon gas turbines which consume about 50% more fuel than steam power toproduce the same amount of electric energy indicates the urgent need forbaseload steam power. Hydro alternatives presently under investigation willin the future replace gas turbines, which will then be transferred to othersmall, isolated systems.

- 16 -

Economic Justification

5.04 Although the proposed Project is the only realistic solution to

provide badly needed base-load capacity in 1979, a comparison was nevertheless

made of the Project with gas turbines as a possible alternative. The Muara

Karang project is more economic than gas turbines for discount rates up to

23%.

5.05 The economic value of alleviating acute power shortage by

investing in the proposed Project cannot be fully quantified and is thusnot expressed in any estimate of return on investment. Consumers are willing

to pay more for the power supplies. This is evidenced by the large amount

of expensive self-generation and by the number of applications for new

connection (paras 5.01-5.02). A minimum estimate of the economic return on

investment was calculated by comparing the costs attributable to the Project

(net of duties and taxes) -- including the cost of transmission/distributionassociated with the marketing of the project output -- to the additionalrevenues derived from it at tariffs expected to be in effect at the time of

project commissioning. In doing this the fuel cost was adjusted to reflectworld market prices which are about 65% higher than the controlled price in

Indonesia. On this basis the return of the Muara Karang project is 19% forUnit 3 and 17% for all three units (Annex 7). The return for Unit 3 ishigher than for three units combined because certain common facilities have

been included in Units 1 and 2.

VI. FINANCIAL ASPECTS

PLN' Financial Situation

6.01 Since 1971 when the first annual accounts based on SOFRELEC's

comprehensive inventory and revaluation program were available, gradualimprovement has been made in line with the objectives of the recovery program(paras. 3.06 - 3.10).

- 17 -

6.02 The following table illustrates PLN's actual finances 1971-1973

(for details see Annexes 13-15):

1971 1972 1973 Average

Energy Sales (GWh) 1,786 1,893 2,175 _

Increase in Energy Sales 12.4% 6.0 /1 14.9% 11.0%

Average Revenues per kwh Sold (Rp) 8.6 8.9 11.1 /2 -Operating Revenues (Rp billion) 16.5 18.7 24.5 -

Operating Expenses (Rp billion)/3 22.2 25.5 31.6 _

Operating Income (Rp billion) (5.7) (6.8) (7.1) _Revenue/Cost Ratio 74% 73% 78% -

Rate of Return on Net FixedAssets in Operation (6.3%) (6.8%) (6.3%) _

Internal Cash Generation(Rp billion) 4.8 3.5 4.1 /4 -

Investments (Rp billion) - /5 19.4 22.1

Percentage of InvestmentsFinanced through InternalCash Generation - /5 18% 19%

/1 Severe drought.

/2 Tariff increase (para. 6.09).

/3 Including provision for bad debts, but excluding lump sum settlement

of overdue Government accounts in 1973.-

/4 Before lump sum settlement of overdue Government accounts in 1973.

/5 Not included due to deficient recording.

6.03 Some information used for the above table is provisional due to

deficient data collecting before 1973. Nevertheless it provides an apprecia-

tion of PLN's unfavorable situation before the introduction of the recovery

plan. Operating revenues covered only slightly more than cash expenses.

Even in the absence of any debt service, less than 20% of the relatively

small investment program was financed through internal cash generation.

6.04 Annex 13 shows financial results expected for the future, based on

the following assumptions:

(i) all costs are valued at 1975 prices and no future escalation

has been assumed. This is reasonable since PLN's tariff

schedule permits fuel and other operating cost inflation

effects to be passed on through tariff adjustments (para 6.08);

(ii) revenues are based on present tariff levels plus one

assumed additional tariff increase of 10% in 1978/79;

- 18 -

(iii) PLN's progress in improving its finances permits on-lendingof funds provided by the Government rather than equity con-tribution as was required by the documents of Credit 399-IND.Consequently it was assumed that Government financing forinvestments committed after the date of signing of the proposedLoan would be in the form of loans rather than equity. This isthe most pessimistic assumption since it is likely that part ofthe Government funds will in fact be provided as equity. Inno case will PLN be liable to make debt service payments before1978/79 (end of the recovery period). Financing for projectscommitted before signing of the proposed Loan would continueto be provided as equity;

(iv) the modified investment program (para. 2.14) has been usedfor projecting capital costs;

(v) comparatively high personnel and material expenses have beenprojected. These are due to planned personnel upgradingprograms involving salary increases and termination payments,and a heavy equipment replacement program; and

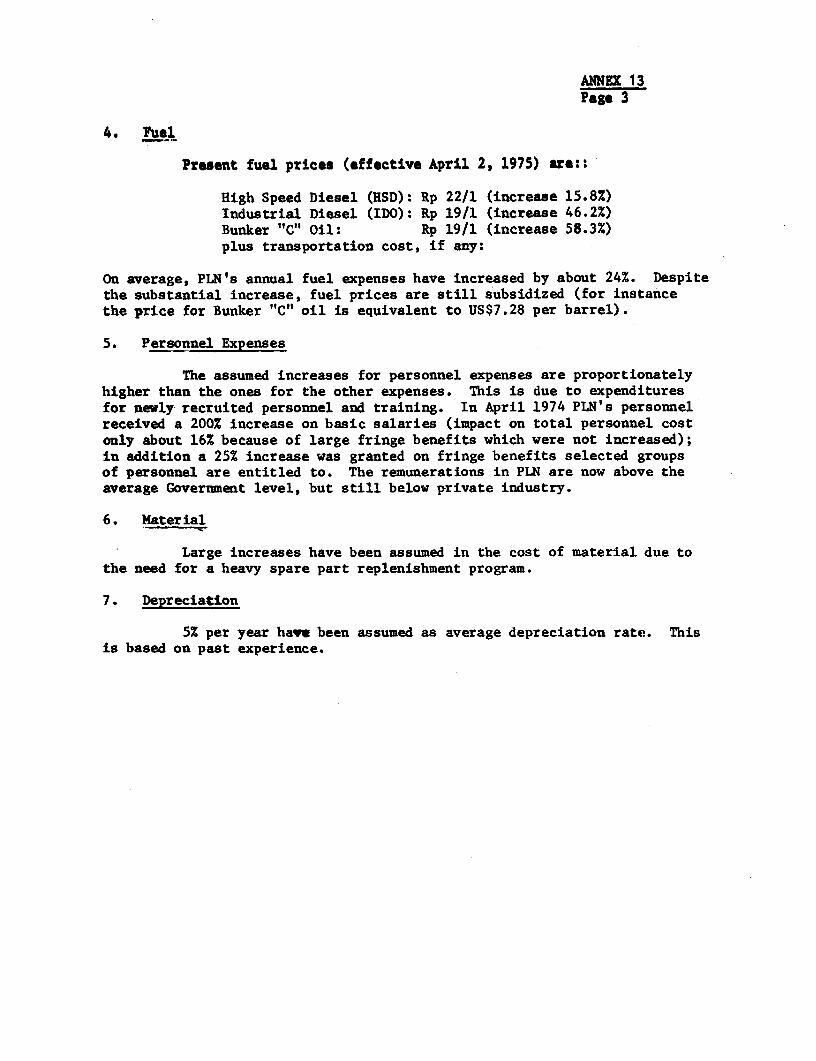

(vi) fuel expenses include the price adjustments effectiveApril 2, 1975 (Annex 13).

A summary of the projected financial results during the recovery period ispresented below (Annex 13-15):

/11974/75/ 1975/76 1976/77 1977/78 1978/79 Average

Energy Sales (GWh) 2,611 2,972 3,423 3,954 4,699 -Increase in Energy Sales 7.1% 13.8% 15.2% 15.5% 18.8% 14.0%Average Revenues perkwh Sold (Rp) 15.1 20.0 /3 19.9 19.8 21.8 -

Operating Revenues(Rp billion) 39.8 60.3 69.0 79.2 103.3 -

Operating Expenses(Rp billion) 47.2 67.6 /2 76.6 85.2 99.7 -

Operating Income(Rp billion) (7.4) (7.3) (7.6) (6.0) 3.6 -

Revenue/Cost Ratio 84% 89% 90% 93% 104% -Rate of Return on NetFixed Assets inOperation (5.6%) (4.5%) (3.5%) (2.1%) 1.0% -

/1 First semester actual.

/2 Including extraordinary personnel termination payments.

/3 Adjusted to reflect fuel cost increase effective April 2, 1975 (Annex 13).

- 19 -

1974/75- 11975/76 1976/77 1977/78 1978/79 Average

Internal Cash Genera-tion (Rp billion) 6.1 8.5 11.9 17.8 32.1 -

Investments (Rp billion) 62.7 101.6 146.3 186.0 182.0 -

Percentage of InvestmentsFinanced throughInternal CashGeneration 10% 8% 8% 10% 18% 11%

/1 First semester actual.

6.05 PLN is expected to meet the targets set in the financial recoveryplan despite sales lower than would be possible if all potential demandwere satisfied by the end of the recovery period. Nevertheless, even incontinued absence of debt service requirements up to 1978/79, internal cashgeneration is not expected to finance a significant portion of the investmentprogram. Government assistance will still be required for a number of yearsas equity or as loans with a grace period on interest and amortization atleast until 1978/79. Consequently the Government has agreed during negotia-tions to provide PLN in future the funds it needs in a form not requiringdebt service payments during the recovery period. Funds committed beforesigning the proposed Loan will continue to be provided as equity as stipulatedin Credit 399-IND.

6.06 To ensure PLN's financial recovery as planned, the financialperformance covenant as included in Credit 399-IND (para. 3.08) will becontinued. A change to a more conventional test (rate-of-return orcontribution-to-investment covenant) is expected to be made in connectionwith a subsequent loan. Intensive supervision will continue to monitorPLN's financial development.

Subsidiary Loan

6.07 Agreement was reached during negotiations that the Government willre-lend the proceeds of the proposed Loan to PLN at terms equivalent to theones charged by the Bank. In addition, PLN will be permitted to capitalizethe interest charges during Project construction to avoid debt service pay-ments during the recovery period. Signing of the Subsidiary Loan Agreementis a condition of effectiveness of the proposed Bank Loan.

Debt Service Limitation

6.08 To avoid excessive borrowing, or borrowing at unreasonably shortterm, an objective debt service limitation test was agreed on during negotia-tions. The covenant provides that PLN is permitted to incur debt as long asthe maximum future debt service is at least covered by the most recent actualnet revenues. In case debt service coverage is not provided, Bank concurrencehas to be sought for the borrowing.

- 20 -

Tariffs

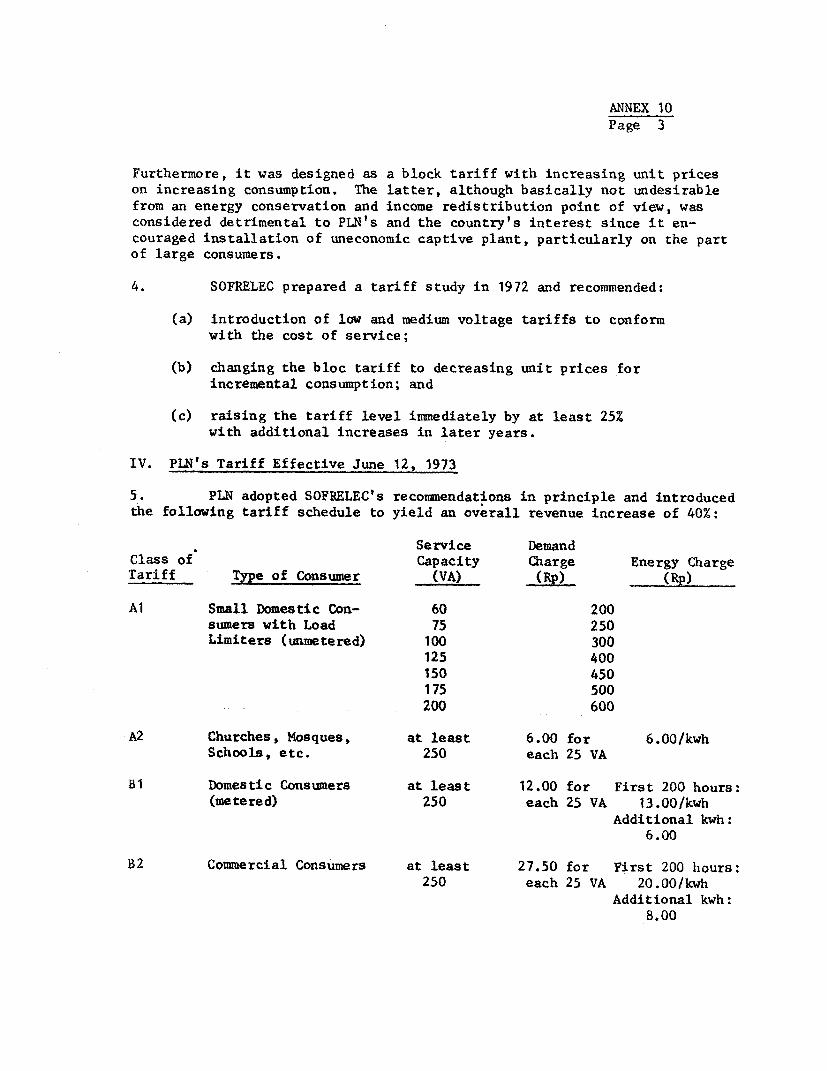

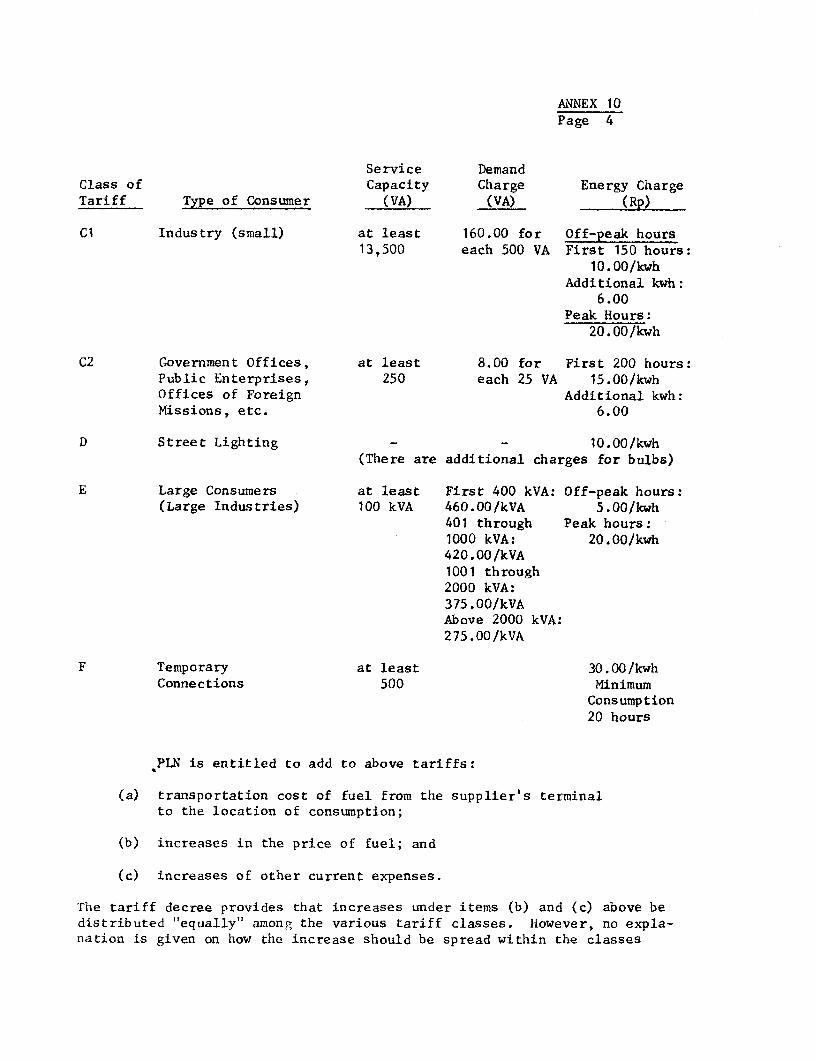

6.09 The tariff structure proposed by SOFRELEC introduced low and mediumvoltage charges to conform with the cost of service and changed the blockstructure from increasing to decreasing unit prices for incremental con-sumption. In addition, peak load tariffs were applied to a larger number ofconsumer classes than before. This was put in force on June 12, 1973 inslightly modified form. Annex 10 shows the new tariff and compares it tothe earlier one.

6.10 PLN's charges to its customers consist of:

(i) the basic tariff as shown in Annex 10;

(ii) transportation cost of fuel from PERTAMINA's terminal to thelocation of consumption; and

(iii) interim price adjustments for increases in the price of fueland other current expenses.

Government approval is required for adjustment of the basic tariff butcharges under (ii) and (iii) can be made after informing the Government.

6.11 Together with the introduction of the new structure, the tarifflevel was increased by 40% with the understanding that additional increaseswould be required for meeting the financial targets. However, the primeemphasis of the recovery plan is cost economizing and the need for tariffincreases will depend on the rate at which PLN is able to improve its opera-tional efficiency. This matter will be a subject of close and continuingreview to ensure that PLN will adjust its tariff level as may be necessary.

Audit

6.12 According to its Act, PLN must be audited by the DirectorateGeneral of State Financial Control. This is a sub-directorate of the Govern-ment's Supreme Audit Council in charge of auditing state enterprises operatedon a commercial basis. A second sub-directorate deals with Government ac-counting audits (for instance ministries and Government departments).

6.13 PLN is audited on a permanent basis with the help of local auditoffices (branches of the audit council) in the provinces and sometimessub-contracted local auditors in headquarters if sufficient audit staff isnot available. In addition to routine control special audits are carriedout irregularly upon request of the Government.

6.14 The state auditor's office has a staff of about 500 accountants.Judging from discussions which included the scope of the reports the Bankwishes to receive, and from a preliminary report, audits are carried outcompetently. Although PLN would not object to additional audit by aprivate firm, it is felt that such audit would not contribute substantiallyto the understanding and efficiency of PLN's operations. A private firm

- 21 -

would be particularly hampered by the long distances involved and lack of

regional offices. Consequently the standard audit covenant has been includedin the documents of the proposed Loan with the understanding that the DirectorateGeneral of State Financial Control is acceptable to the Bank. Audit reportswill be sent to the Bank annually not later than 6 months after the closeof the fiscal year.

Accounting, Billing and Collection

6.15 The consultants have designed a modern accounting system and thishas been introduced throughout PLN's operations. The important areas (Java

and parts of Sumatra) are in the process of mechanization and computeriza-tion with good results so far. The distances and sometimes primitivetransport facilities make it difficult to get records from outlying areas

to headquarters in time to permit timely closing of the books but this is

being overcome by dispatching accountants from headquarters to the regionaloffice to assist in finalizing the accounts and to handcarry the results

back to headquarters.

6.16 At the time of previous appraisals, large arrears in accountsreceivable posed a serious problem. This was particularly true for variousGovernment agencies. Consequently, in the course of negotiations for

Credit 334-IND, the Government agreed to settle its debt and has since doneso. Outstanding amounts from non-government consumers have been kept withinacceptable levels. By the end of FY 1973 accounts receivable representedabout 3-months billing. To ensure that billing and collection continue to

be handled efficiently:

(i) the covenant requiring the Government agencies to payits debts to PLN promptly when due has been repeated; and

(ii) PLN agreed during negotiations to restrict accountsreceivable of customers other than Government agenciesat the end of any month to not more than the amountbilled during the previous 3-months period.

6.17 PLN is generally slow in settling its accounts payable and this

has adversely affected its reputation with suppliers, very likely resultingin higher price quotations than would have otherwise been the case.Consequently the convenant requiring PLN to settle its debt within onemonth after they are due has been repeated. The one-month time allowanceshould be sufficient for settling most disputes.

Insurance

6.18 PLN does not presently insure its property in operation althoughinsurance against hazards of acquisition and transportation and delivery ofgoods is regularly arranged. However, SOFRELEC is preparing an insurance

- 22 -

proposal which is expected to form the general basis for asset insurance.As an interim measure agreement was reached in Credit 399-IND that theGovernment will provide PLN with the funds required to cover normallyinsurable damage minus an amount equivalent to US$100,000. This stipulationhas been repeated in the documents of the prospective Loan.

VII. AGREEMENTS REACHED AND RECOMMENDATION

7.01 During Loan negotiations, agreement was reached on the following:

(a) Bank concurrence will be sought before amendments to legis-lation affecting PLN are introduced (para. 3.01);

(b) consultants acceptable to the Bank will be retained fordesign, procurement and construction supervision of theMuara Karang 3 unit, design for Muara Karang 4, and siteinvestigation work for a new thermal power site (paras.4.09 and 4.12). Appointment of competent training specialistsand management advisers will be on terms and conditionssatisfactory to the Bank (para. 3.11);

(c) local preference will be taken into account in bid evaluationfor equipment (para 4.14);

(d) all future funds provided by the Government to PLN will bemade available in a form not requiring debt service paymentsduring the recovery period. Funds committed before Loansigning will continue to be provided as equity (para. 6.05);

(e) the financial recovery plan as included in the documentsof Credit 399-IND will continue to prevail (para. 6.06);

(f) the Government will re-lend the proceeds of the Loan to PLN.Signing of the Subsidiary Loan Agreement between the Governmentand PLN is a condition of effectiveness of the proposed BankLoan (para. 6.07);

(g) PLN will not incur debt without Bank concurrence unless itsmaximum future debt service is at least covered by historicnet revenues (para. 6.08);

(h) PLN will have its accounts audited annually by independentauditors acceptable to the Bank (para. 6.14);

(i) the Government and its agencies will pay their debts whendue (para. 6.16);

- 23 -

(j) the aggregate amounts outstanding from sales of power tonon-Government customers at the last working day of eachmonth will not exceed the amount of billing issued inrespect of the 3-months period terminating on such day(para. 6.16);

(k) PLN will pay its debts within one month after their respectivedue dates (para 6.17); and

(1) satisfactory insurance arrangements will be made by Governmentand PLN (para. 6.18).

7.02 With the agreements reached on the above, the Project would besuitable for a Bank Loan of US$41 million equivalent, on terms of 25 years,with a 5-year grace period.

_~~~~~~~~~~~~~~~~~~~~~ - - - - - - -L

s~~~~~~~~~~~~~~~~ ~ 5- -a52il3i - - -- -- -- -- - -- - -- i

35A 13=

' T _ r _ _ _ _ _ _ _ _ _ _ | _ =

3,,Q3,q,,5,,gg,,,.~~~~~~~~~~- -T-

Annex 2

INDONESIA

Penisahaan Umuim Listrik Negara (PLN)

Fourth Power Project

Installed Generating Capacity as of March 31, 1974

(kW)

Regions Hydro Steam Diesel Gas Turbine Total

Exploitasi I - - 7,644 - 7,644Exploitasi II 150 - 27,371 14,000 41,521Exploitasi III 70 - 20,097 - 20,167Exploitasi IV 1,320 - 26,694 14.,000 42,014Exploitasi V - - 7,890 - 7,890Exploitasi VI 20,000 - 13,923 - 33,923Exploitasi VII 8,940 - 7,561 - 16,501Exploitasi VIII - 25,000 17,802 - 42,802Exploitasi IX - - 4,165 - 4,165Exploitasi X - - 10,683 - 10,683Exploitasi XI 80 _ 14,498 - 14,578

Generasi I 109g,652 50,000 20,130 - 179,782Generasi II 42,300 - 36,642 14,000 92,942Generasi III 91,000 11150,000 14,564 20,000 275,564

Distribution I 572 - 895 - 1,467Distribution II - - 312 - 312

Total 274,o84 225,000 230,871 62,000 791,955

1/ Excluding the 125,000 kW Juanda hydro station owned and operated by theJatiluhur Authority.

INDONESIA

Perusahaan Umum Listrik Negara (PLN)

Fourth Power Project

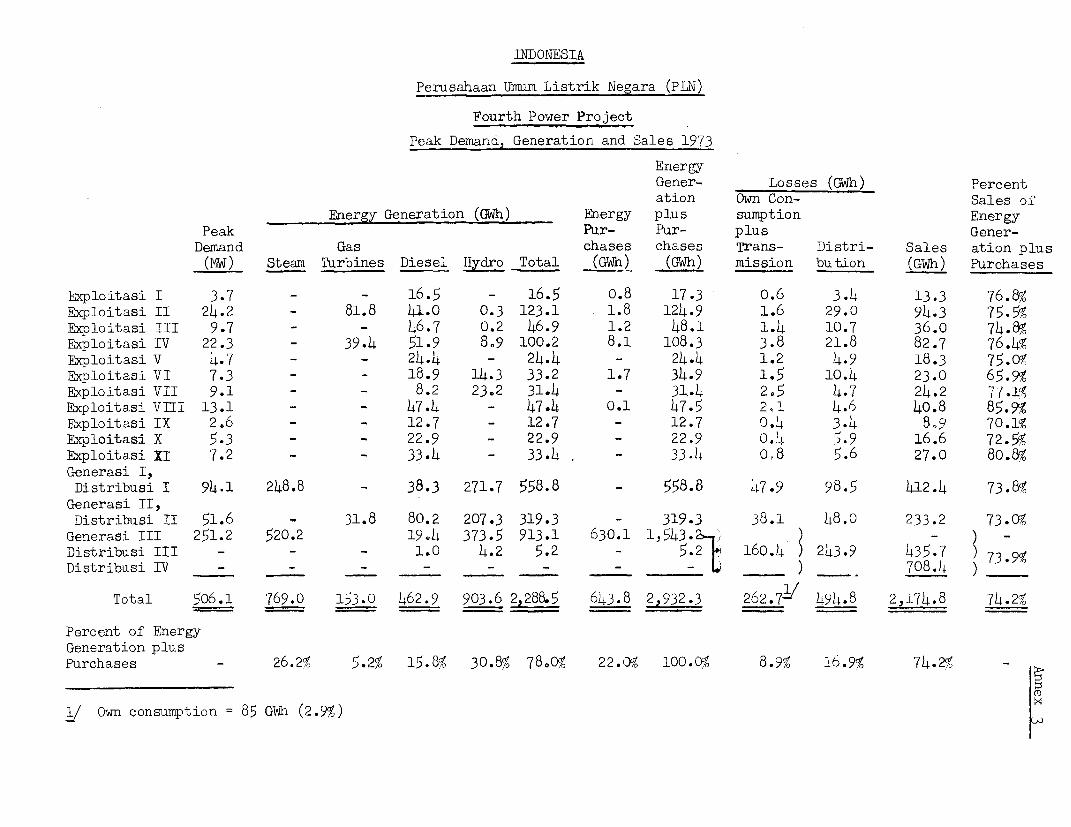

Peak Demand, Generation and Sales 1973

EnergyGener- Losses (GWh) Percent

ation Own Con- Sales of

Energy Generation (GWh) Energy plus sumption Energy

Peak Pur- Pur- plus Gener-

Demand Gas chases chases Trans- Distri- Sales ation plus

(MW) Steam Turbines Diesel Hydxo Total (GWh) (Gwh) mission bution (GWh) Purchases

Exploitasi I 3.7 - - 16.5 - 16.5 o.8 17.3 o.6 3.4 13.3 76.8%

Exploitasi II 24.2 - 81.8 41.0 0.3 123.1 1.8 124.9 1.6 29.0 94.3 75.5%

Exploitasi III 9.7 - - 46.7 0.2 46.9 1.2 48.1 1.4 10.7 36.0 74.8%

Exploitasi IV 22.3 - 39.4 51.9 8.9 100.2 8.1 108.3 3.8 21.8 82.7 76.4%

Exploitasi V 4.7 - - 24.4 - 24.4 - 24.4 1.2 4.9 18.3 75.0W

Exploitasi VI 7.3 - - 18.9 14.3 33.2 1.7 34.9 1.5 10.4 23.0 65.9%

Exploitasi VII 9.1 - - 8.2 23.2 31.4 - 31.4 2.5 4.7 24.2 77*14

Exploitasi VIII 13.1 - - 47.4 - 47.4 0.1 47.5 2,1 4.6 40.8 85.9%

Exploitasi IX 2,6 - - 12.7 - 12.7 - 12.7 0.4 3.4 8.9 70.l1?

Fxploitasi X 5.3 - - 22.9 - 22.9 - 22.9 04 5. 9 16.6 72. 5

Exploitasi XI 7.2 - - 33.4 - 33.4 - 33.4 018 5.6 27.0 80.8%

Generasi I,Distribusi I 94.1 248.8 - 38.3 271.7 558.8 - 558.8 47 .9 98.5 412.4 73.8%

Generasi II,Distribusi II 51.6 - 31.8 80.2 207.3 319.3 - 319.3 38.1 48.0 233.2 73.Q%

Generasi III 251.2 520.2 19.4 373.5 913.1 630.1 1,543. 2 ) - )

Distribusi III - - - 1.0 4.2 5.2 - 5.2 160.4 ) 243.9 435 ) 73 99

Distribusi IV - - - - -__ ) 708.4 )

Total 506.1 769.0 153.0 462.9 903.6 2,288.5 643.8 2n932.3 262.7-/ 494.8 2,174.8 74.2%

Percent of EnergyGeneration plusPurchases - 26.29 5.2% 15.8% 30.8%9 78.099 22.0O9 100.0% 8.9%9 16.9%9 74.29 _

(D

1/ Own consumption =85 GWh (2.9%) t

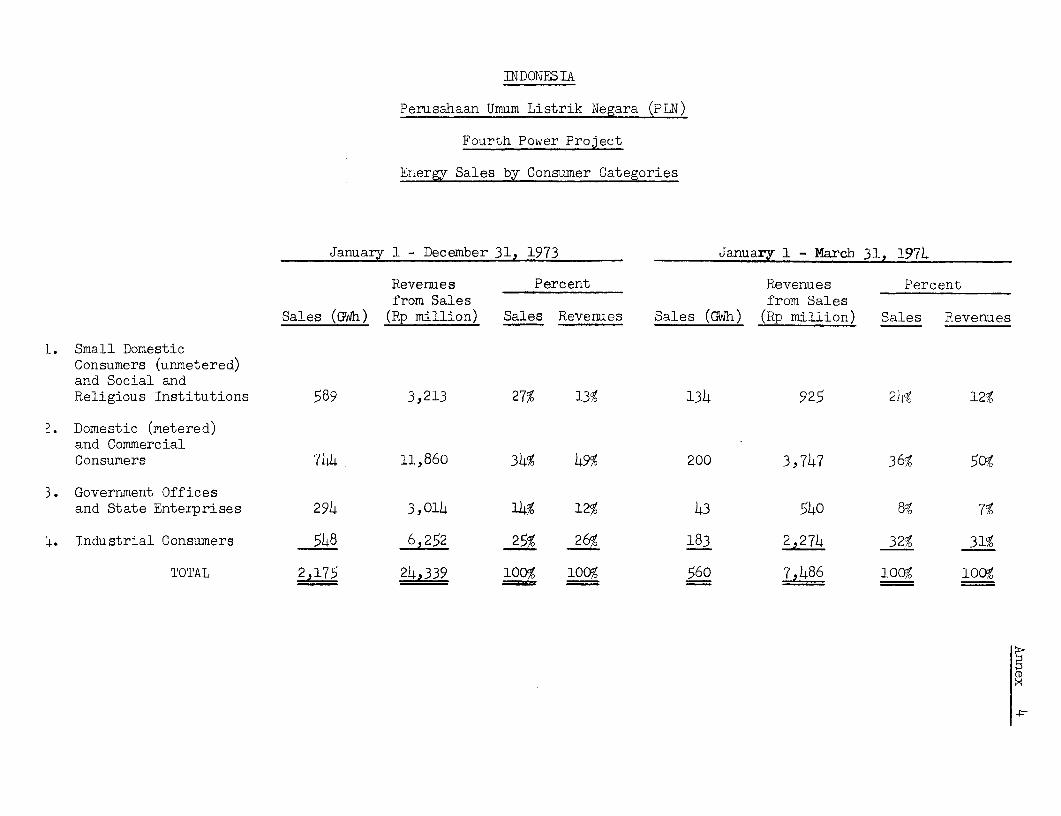

INDONESIA

Perusahaan Umum Listrik Negara (PLN)

Fourth Power Project

Energy Sales by Consumer Categories

January 1 - December 31, 1973 January 1 - March 31, 1974

Revenues Percent Revenues Percentfrom Sales from Sales

Sales (GWh) (Rp million) Sales Revenues Sales (GWh) (Rp million) Sales Revenues

l. Small DomesticConsumers (unmetered)and Social andReligious Institutions 589 3 ,213 27% 13% 134 925 2 4% 12%

Domestic (metered)and CommercialConsumers 744 11,860 34% 49% 200 3,747 36% 509

3. Government Officesand State Enterprises 294 3,014 14% 12% 43 540 8O 7%

4. Industrial Consumers 548 6,252 25% 26% 183 2,274 329 31%

TOTAL 2,175 24,339 lO0 lO0 560 7,486 100% lox,

(D

Annex 5

INDONESIA

Perusahaan Urnum Listrik Negara (PLN)Fourth Power Project

Actual and Forecast Generation (incl. Purchases) and Sales 1967-1978/79

Generation (incl.Purchases) SalesGWh Increase GWh Increase

Actual

1967 1,607 1,158 -

1968 1,766 5.7% 1,204 4.0%

1969 1,872 6.0% 1,454 20.8,

1970 2.084 11.3% 1,589 9.3-

1971 2,354 13,0% 1,786 12.4%

1972 2,498 6.1% 1,893 6.o%

1973 2,932 17.4% 2,175 14.9%

1974 (1. Quarter) .759 8.0% 560 707%

Forecast

1974/75 3,528 7.1% 2,611 7.1%

1975/76 4,016 13.8% 2,972 13.8%

1976/77 4,594 14.4% 3,423 15.2%

1977/78 5,307 15.5% 3,954 15.5%

1978/79 6,265 18.1% 4,699 18.8%

Annex 6

INDONESIAPerusahaan Umum Listrik Negara (PLN)

Fourth Power ProjectProject Cost Estimate

Billions of Rupiahs Millions of US DollarsLocal Foreign Total Local Foreign Total

1. Muara Karang No.3 Unit(1) Site Development 1.46 - 1.46 3.52 - 3.52(2) General Construction

Steam generator Construction 0.22 0.67 0.89 0.52 1.61 2.13Turbo generator Construction 0.04 0.37 0.41 0.10 0.89 0.99Mechanical Construction 0.30 1.56 1.86 0.73 3.76 4.49Electrical Construction 0.30 0.75 1.05 0.71 1.82 2.53Structural Construction 0.88 0.27 1.15 2.13 0.64 2.77

Sub-total 1.74 3.62 5.36 4.19 8.72 12.91

(3) Supply of EquipmentSteam Generator 0.02 2.08 2.10 0.05 5.01 5.06Turbo Generator - 3.96 3.96 - 9.54 9.54Electrical Equipment 0.01 0.84 0.85 0.02 2.02 2.04Transformer - 0.32 0.32 - 0.77 0.77Instrumentation 0.02 0.16 0.18 0.04 0.40 0.44Structural Equipment - 0.40 0.40 - 0.97 00.97

Sub-total 0.05 7.76 7.81 0.11 18.71 18.82

(4) EngineeringEngineering for Unit 3 0.02 0.40 0.42 0.05 0.97 1.02Engineering for Unit 4 0.11 1.08 1.19 0.26 2.60 2.86

Sub-total 0.13 1.48 1.61 0.31 3.57 3.88

Base Cost Estimate 3.38 12.86 16.24 8.13 31.00 39.13Physical Contingency 1/ 0.32 0.83 1.15 0.77 2.00 2.77Price Contingency 2/ 1.44 2.24 3.68 3.48 5.40 8.88

Total 5.14 15.93 21.07 12.38 38.40 50.78

2. Feasibility Study 0.12 0.29 0.41 0.30 0.70 1.00

3. Advisory Service and Training

Management Advisors 0.05 0.41 0.46 0.12 1.00 1.12Training Centers 2.63 0.77 3.40 6.33 1.85 8.18Fellowships - 0.17 0.17 - 0.40 0.40

Total 2.68 1.35 4.03 6.45 3.25 9.70

TOTAL PROJECT COST 7.94 17.57 25.51 19.13 42.35 61.48

Interest during Constructionon Bank Loan - 3.32 3.32 - 8.00 8.00

GRAND TOTAL 7.94 20.89 28.83 19.13 50.35 69.48AMOUNT OF LOAN 3/ 41.00

1/ 5% for foreign component of items (3), (4) and 10% for all other items are assumed.2/ Price contingency is based on the following rates of inflation:

1975 1976 1977-78

equipment 12% 10% 8%civil works/erection 16% 14% 12%

3/ The Loan will finance the full foreign exchange cost of the Project except foreducational equipment for training centers of US$ 1.35 million which will befinanced by PLN.

ANNEX 7Page 1

INDONES IA

PERUSAHAAN UMUM LISTRIK NEGARA (PLN)

FOURTH POWER PROJECT

Economic Justification

Economic viability of the Muara Karang project has been examinedin four different ways:

(1) least cost solution

(2) internal financial return

(3) internal economic return

(4) effect on economy

1. General Assumption

(a) Investment Cost

Muara Karang Unit 3

total project cost $50.78 millionless price contingency $(8.88)less engineering Unit 4 $(3.00) "

base cost $38.90 million

Muara Karang Unit 1 and 2

total project cost $106.0 millionless price contingency $(6.1) "

base cost $99.9 million

Gas Turbines

A recent international competitive bidding on a 20 MW unitfor the Pulo Gadung industrial project in Jakarta revealed avarying unit cost of $160-200/kW installed at a substation,

ANN4EX 7Page 2

excluding costs of site development, transmission lines,and engineering. A consultants' estimate indicates amuch higher unit cost of $350/kW for a complete unitincluding contingency. An informal quote obtained froma manufacturer shows $200/kW for a bunker C-fired unitincluding fuel treatment facilities, but excluding sitedevelopment, transmission lines and engineering. Hence,for the purpose of the study, a unit cost of $240/kW wasused as a today's unit cost for a complete set of gasturbines.

(b) Operation and Ilaintenance Cost

2% of the capital cost was assumed as an annual O/Mcost for both Muara Karang and gas turbines.

(c) Fuel Cost

PLN purchases its fuel oil at a controlled price whichwas raised as of April 2, 1975 from Rp 12/liter to Rp 19liter ($7.28/barrel) for Bunker C and from Rp 19/literRp 22/liter ($8.43/barrel) for diesel oil at Pertamina's(national oil company) terminal. For calculations of theinternal financial return, this controlled price was usedsince PLN's tariffs are based on it and fuel cost variationsare recoverable through fuel surcharges.

For calculations of the economic return and the leastcost solution, todays world market price for Indonesian oilof $12/barrel was used for both Bunker C and diesel oil.Although diesel oil prices are normally about 50% higher thanBunker C prices, this difference was not taken into accountsince no free market price exists in Indonesia. This wouldpenalize steam power generation against gas turbines.

(d) Heat Rate

Muara Karang: 2,300 kcal/kWh* Gas Turbine: 3,400 kcal/kWh

(e) Operating Pattern

The plant would be operated at a 75% plant factor forthe first 10 years and, thereafter, would be shifted to theupper portion of the load curve with decreasing operatinghours. A plant factor of 55% was assumed for the last 5years of the 30-year plant life. Gas turbines as an alter-native would follow the same operating pattern but with aplant life of 15 years.

ANNEX 7Page 3

(f) Incremental Revenues

PLN's average revenue per kWh sold is at presentRp 20.0 after adjustment for the increased price offuel. In order to financially break-even by 1978 asrequired in connection with Credit 399-IND, PLN will have toraise its tariffs to Rp 21.8/kWh, excluding any additionalincrease which might become necessary due to inflationarytrends. Incremental revenues from the Project based onthese tariff levels were used as the minimum benefits ofthe Project in calculations of the internal financialreturn. It was assumed that in the first year ofoperation only a half of the energy generated by theProject would constitute incremental sales and theremaining half would only replace existing gas turbinesand thus save fuel costs. From the second year, allenergies available from the Project would represent in-crenental sales. System losses of 20% were also assumedthroughout the period.

(g) Cost of Transmission and Distribution

Although the cost of transmission lines from the MuaraKarang plant to the grid is included in the project cost,additional investment to market the output of the Projectis required for the Iistribution system. During RepelitaII PLN plans to invest Rp 147.6 billion on transmissionand distribution in the West Java area for rehabilitatingexisting systems and for expanding new systems. Sincethe existing systems are old and in chaotic condition,about one half of the investment would be required forrehabilitation and only the remaining half (Rp 74 billion)would contribute to expanding the system capacity to meetan incremental generating capacity of 610 MW during thesame period. In the following calculations Rp 74 billionwas pro-rated as follows:

Unit 3 74 x 100/610 = Rp 12.1 billion ($29.2 million)

Unit 1-3 74 x 300/610 = Rp 36.3 billion ($87.5 million)

2. Least Cost Calculation

Although the proposed Project is the only realistic solution toprovide badly needed base-load capacity, a comparison was nevertheless madeof the Project with gas turbines as a possible alternative. The MuaraKarang project was proven to be more economic than gas turbines for dis-count rates up to 23%.

ANNEX 7Page 4

3. Internal Financial Return (IFR)

In view of sharply increased costs of Units 1 and 2, internalfinancial returns were calculated not only for Unit 3 but also for threeunits as a whole. Internal financial returns thus obtained are as follows:

tariffs at Rp 21.8/kWh at Rp 20.0/kWh

Unit 3 23.8% 21.5%.Units 1-3 22.0% 19.8%

4. Internal Economic Return (IER)

(a) Since no established methodology is available to quantify economicbenefits of electricity supply, incremental revenues from the Pro-ject were used as the minimum benefits as was the case for IFR.However, the fuel cost was shadow-priced by using the world marketprice of $12/barrel. IER's thus obtained are as follows:

tariffs at Rp 21.8/kWh at Rp 20.0/kWh

Unit 3 18.6% 16.1%Units 1-3 17.1% 14.7%

(b) As the most conservative economic evaluation, fuel replacementbenefits by substituting Muara Karang Unit 3 for existing gasturbines were compared to the project cost, disregarding allthe benefits to be derived from additional electricity avail-able to the economy. Benefits thus evaluated are found largerthan the cost for discount rates up to 11%. This would repre-sent the hypothetical lowest limit of the economic return onthe Project.

5. Effect on Economy

The consultants, Chas T. Main, made efforts to develop a methodto forecast future electricity demands based on the state of the economyat any given time and a probability assessment of its future potentials.In this method interrelationships between several economic sectors andtheir effect on power demands are determined by using multiple regressionand each sector's present state is defined by its present value and itsgrowth rate. Transition probabilities are assigned to each sector repre-senting the likelihood of increasing, decreasing or stable growth rate.The method thus gives a power demand forecast based not on past trends buton the future outlook of the economy. The methodology was consideredparticularly suitable for Indonesia where actual demands in the past do notrepresent the real demands. By using this method, the consultants predictedthat a 5% reduction in the growth rate of electric demand in Indonesia would

ANNEX 7

Page 5

result in a decline of approximately 1.5% in the growth rate of economy.Since the power demand in Central and West Java is expected to reach 1,000

MW in 1980, the Muara Karang No. 3 unit would represent about 10% of thetotal system demand and, according to this method, would affect the growthof economy by about 3%. Assuming that the combined area of Central-WestJava represents one-third of the country's economy (1972 actual), the Project

would have an effect of about 1.0% or about US$400-500 million, on thetotal expected GDP of US$40-45 billion in 1980. Although this amount doesnot necessarily represent the real benefit, it gives a good indication ofthe importance of electric power to the growth of the economy.

ANNEX 8Page 1

INDONESIA

PERUSAHAAN UMUM LISTRIK NEGARA (PLN)

FOURTH POWER PROJECT

Construction Cost of Muara Karang Project (Unit 1 &2)

Analysis of Cost Overruns

1. Introduction

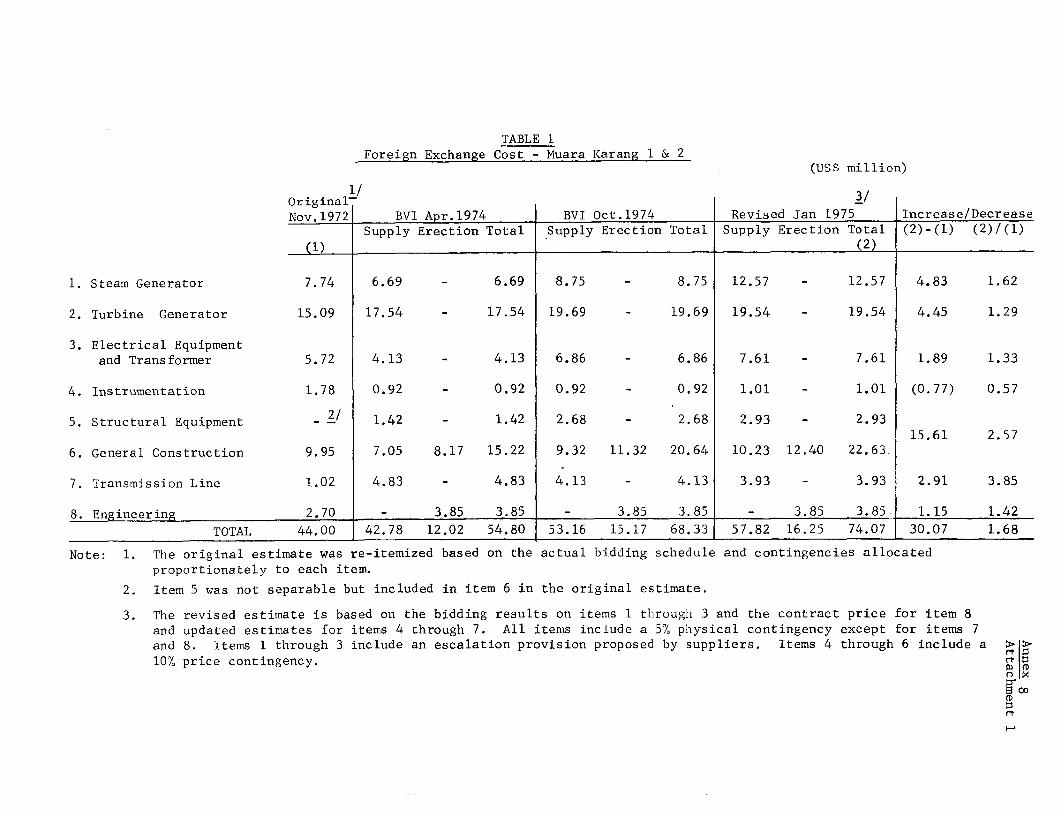

1.01 The Muara Karang project (Unit 1 & 2) was appraised in November1972. The cost estimate for the project, originally prepared by consultants(C.T. Main), was discussed with PLN and the consultants and accepted asadequate. The total cost of the project was estimated at US$52 million,US$44 million representing the foreign exchange portion and US$8 millionthe local cost, including necessary transmission facilities.

1.02 An IDA credit financing the foreign cost of the project wasapproved in May 1973, and in lovember 1973 Black & Veatch International(BVI) were appointed by PLN as the consultants for project engineering andsupervision. In April 1974, BVI reestimated the project cost based on theirpreliminary design. This increased both foreign and local cost to US$54.8million and US$16.3 million equivalent, respectively, resulting in thetotal cost of US$71.1 million.

1.03 Surprisingly high bidding prices received for the Semarangthermal power project (2 x 50 'IW), Central Java, in mid-1974 forced BVIto re-examine the cost estimate for the Mtuara Karang project. TheirOctober, 1974 revision further increased the estimate to US$68.3 millionand US$37.2 million for the foreign and local component, respectively,and the total to US$105.5 million.

1.04 Bids were received on November 15, 1974 for the supply of majorequipment. Although the response to the bid invitation was favorable withsixteen suppliers well spread throughout the world participating, pricesoffered revealed additional cost increases. The sum of the lowest evaluatedbid for each schedule is now US$37.8 million, which compares with US$22.8million in the appraisal for these items; US$27.2 million in BVI's estimatein April 1973 and US$34.4 million in their October 1974 estimate.

ANNEX 8Page 2