perspectives on the draft affordability assessments

TRANSCRIPT

In SA Taxi Securitisation (Pty) Ltd v Mbatha

Levenberg J said:

“While one purpose of the NCA is to discourage

reckless credit, the Act is also designed to facilitate

access to credit by borrowers who were previously

denied such access. An overcritical armchair approach

by the courts towards credit providers when evaluating

reckless credit, or the imposition of excessive penalties

upon lenders who have recklessly allowed credit, would

significantly chill the availability of credit, especially to

the less affluent members of our society.”

Reckless Credit in terms of the NCA• Creditor wanting to conclude an agreement with a prospective consumer

must first do a compulsory pre-assessment of the consumer’s situation(eg, assessing his affordability, debt re-payment history, & generalunderstanding of the risks and obligations of the agreement).

• Provisions of over-indebtedness & reckless credit do not apply whereconsumer is a company, cc, partnership or certain trusts - apply only tonatural persons, stokvels & certain types of trusts.

• Provisions of reckless credit do not apply to certain loans:

– school, student, emergency loans;

– public interest credit agreement;

– incidental credit agreement;

– temporary increase in credit limit under a credit facility; or

– a pawn transaction.

• Consumer must fully and truthfully answer ANY REQUEST FOR INFORMATIONMADE BY CREDIT PROVIDER when application for a credit agreement is made(express duty of consumer).

Reckless credit (cont…)

Agreement was reckless if, at the time the agreement was made:

– Creditor provider failed to take reasonable steps to assess:

• the proposed consumer’s:

– general understanding/appreciation of risks & costs of credit & hisrights and obligations;

– debt re-payment history under credit agreements;

– existing financial means, prospects & obligations; and

– whether there is a reasonable basis to conclude that anycommercial purpose may be successful, if the consumer has sucha purpose for applying for credit.

– Or creditor provider made such assessment and entered intoagreement, despite the fact that:

• consumer did not understand/appreciate risks, costs or obligations; or

• entering into it would make consumer over-indebted.

Reckless Credit (cont…)

• Person making the determination must apply above criteria

as they existed at the time agreement was made.

• Complete defence for creditor to an allegation of reckless

credit if:

– creditor establishes that consumer failed to fully & truthfully answer

any request for info made by creditor as part of the compulsory

assessment; and

– a court or NCT determines consumer’s failure materially affected

creditor provider to make proper assessment.

(Thus onus on creditor to prove it has a valid defence and not every failure by

consumer to fully & truthfully answer any request for info will necessarily entitle

the creditor to this defence.)

• Delayed operation of the NationalRegister of Credit Agreements.

• Important Role of Credit Bureaux.

Background to Credit-Information Amnesties

• Pre-NCA – consumers were often blacklisted without their knowledgeand without an opportunity to challenge the correctness of adverse infobeing reported to credit bureaus.

• 2006 Credit-Information Amnesty Regulations were issued (“1st

Amnesty”)

– Generally welcomed.

– Limited application.

– Apparently at least 74% of consumers who benefited from the 1st amnestywere in default again on their credit payments.

• Initially thought to be a once-off provision of credit-information amnesty,

but resulted in a second and much more comprehensive amnesty (“2nd

Amnesty”).

• Came into operation on 1 April 2014.

• Strong opposition to 2nd Amnesty from banks and other credit providers.

Impact of 2nd Credit Amnesty Regulations

• Main purpose is to enable blacklisted consumers whose financialcircumstances have changed since they could not pay their debt in the pastto be able to access credit again.

• ONCE-OFF REMOVAL OF CERTAIN ADVERSE CONSUMER CREDITINFORMATION.

• ON-GOING REMOVAL OF INFORMATION RELATING TO “PAID UPJUDGMENTS” OF CONSUMERS (ie, civil court judgment debts, includingdefault judgments, where the consumer has settled the capital amountunder the judgment(s)).

• Registered credit bureaux had to remove all the listed adverse consumercredit information and the “paid up” data from their records within 2 monthsfrom the effective date (ie, on or before 1 June 2014). (Some extensionallowed.)

• Applicable to all consumers, irrespective of type of credit agreementinvolved and amount of debt (related to info kept by all the credit bureaus asat 1 April 2014).

• ONCE-OFF REMOVAL OF FOLLOWING ADVERSE INFO:

– adverse classifications of consumer behaviour are subjectiveclassifications of consumer behaviour and include classifications such as“delinquent’’, “default’’, “slow paying”, “absconded” or “not contactable”;

– adverse classifications of enforcement action, which are classificationsrelated to enforcement action taken by the credit provider, includingclassifications such as “handed over for collection or recovery”, “legal action”,or “write-off”;

– details and results of disputes lodged by consumers irrespective of theoutcome of such disputes;

– adverse consumer credit information contained in the payment profilerepresented by means of any mark, symbol, sign or in any manner or form.

• SUBJECTIVE LISTINGS VS OBJECTIVE LISTINGS.

• PAYMENT PROFILE IN A CREDIT REPORT NOT REMOVED (eg, number ofmonths to repay a debt – objective listings remain, but certain subjectivedeductions can be made from info).

• ROLE OF CREDIT SCORE BAND IN A REPORT.

Once-off and on-going removal of information relating to

“paid up judgments” of consumers

• Means civil court judgment debts, including default judgments, wherethe consumer has settled the CAPITAL AMOUNT under thejudgment(s).

• Unclear what is meant by the term “capital amount” or exactly whichamounts it includes - the NCA and its regulations silent on issue.

• The NCA refers to and defines only the term “principal debt”.

• Regulations silent about the payment (settlement) of the interestcomponent and any other costs (eg, legal costs) in connection with thejudgment debt.

• One of the drafters of the Amnesty Regulations states:

it does include interest; and

only reasons for term is to prevent credit providers from “piling on”the costs.

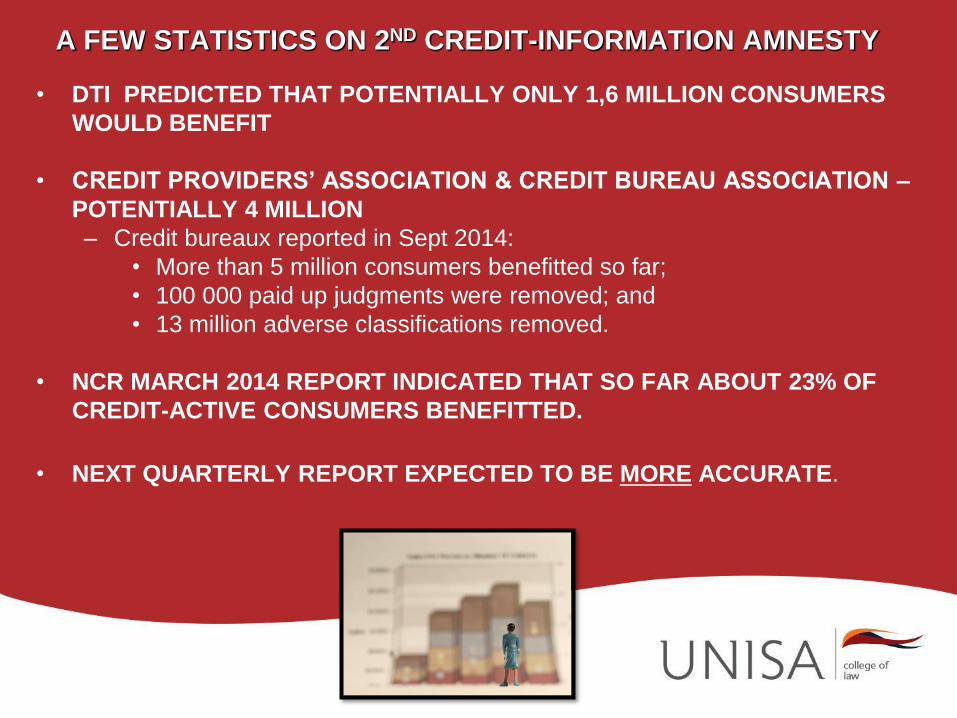

A FEW STATISTICS ON 2ND CREDIT-INFORMATION AMNESTY

• DTI PREDICTED THAT POTENTIALLY ONLY 1,6 MILLION CONSUMERS

WOULD BENEFIT

• CREDIT PROVIDERS’ ASSOCIATION & CREDIT BUREAU ASSOCIATION –

POTENTIALLY 4 MILLION

– Credit bureaux reported in Sept 2014:

• More than 5 million consumers benefitted so far;

• 100 000 paid up judgments were removed; and

• 13 million adverse classifications removed.

• NCR MARCH 2014 REPORT INDICATED THAT SO FAR ABOUT 23% OF

CREDIT-ACTIVE CONSUMERS BENEFITTED.

• NEXT QUARTERLY REPORT EXPECTED TO BE MORE ACCURATE.

Provision made for the on-going automatic removal of

adverse info & paid up judgments in the Amendment Act

• Pending National Credit Amendment Act 19 of 2014 also provides for an

automatic & on-going removal of adverse info and info ito paid up judgments – s

71A.

• Provides for duties of credit providers & credit bureaus.

• No distinction between objective or subjective adverse classifications and listings.

• Amnesty Regulations make reference only to adverse classifications of consumer

behaviour which are subjective.

• Important that objective listings remain in the payment profile.

• From a literal interpretation of s 71A it seems that the section aims to cater for the

automatic removal of both types of info.

• Draft regulations (see reg 19) relevant for s 71A also refer to the removal of

judgments where “capital is paid” without mentioning interest component.

A few questions arising• Which info may still be contained in the credit bureau report, despite the application of the

Amnesty Regulations and the pending s 71A?

• How do you assess repayment history with the Amnesty Regulations removing some parts

of the history? (No guidance in 2014 Draft Affordability Regulations how to deal with info in

report – only stressing the importance to get a report.)

• Clearly stated that credit provider is not permitted to use any of the info removed in terms

of these regulations for “any reason, including credit scoring and assessment” of

consumers.

o Credit provider in doing its statutory assessment may still use the same

removed info, if it was obtained from consulting its own records (eg, dealing with

existing customer).

o Only prohibited from using info if it was obtained from a credit bureau report.

o May credit provider ask questions, during the compulsory assessment,

regarding the type of adverse info that was removed? Eg, has a judgment ever

been taken against you for non-payment (even if it was latter fully settled)?

Current situation in terms of NCA• NCA seems to imply a duty on creditor to ask the correct

info/questions.

• Consumer under no duty to supply any info not specifically asked.

• Creditor determines his own assessment procedure/models – must be

fair.

• The NCR may publish non-binding guidelines proposing evaluative

mechanisms, models and procedures to be used to determine

whether credit is being granted recklessly in relation to credit

agreements.

• Creditor allowed to accept the info supplied as correct without

investigating it.

• Court/Tribunal must establish if incomplete or untrue info is material –

difficulty with this.

• No standardised guidelines as to how the assessment is to be done &

what the correct questions/info are.

Background to Draft Assessment Regulations• NCR’s public notice issued in May 2013 intending to issue affordability assessment guidelines.

• NCR issued “Affordability Assessment Guidelines” in Sept 2013.

• PENDING NATIONAL CREDIT AMENDMENT ACT 19 OF 2014

• Before registering a credit provider NCR will take following into consideration:

– Commitments to combating over-indebtedness;

– Compliance with prescribed code of conduct (provision made for Minister to prescribe acode); and

– Compliance with AFFORDABILITY ASSESSMENT REGULATIONS (issued byMinister on recommendation of the NCR).

• Minister may prescribe CODE OF CONDUCT & THE CRITERIA AND MEASURES TO DETERMINETHE OUTCOME of affordability assessments provided for in s 48.

• Credit provider may determine own assessment mechanisms, models and procedure, provided they arefair and objective and not inconsistent with the AFFORDABILITY ASSESSMENT REGULATIONS.

• Court and NATIONAL CONSUMER TRIBUNAL may declare an agreement to constitute reckless credit.

• 1 August 2014 a comprehensive set of DRAFT REGULATIONS on various matters including regulationson affordability assessment, were published for public comment.

2014 Draft Affordability Regulations

• An improvement on certain aspects of the Sept 2013 Guidelines.

• A few good things coming out of the regulations.

• Verification of allocatable & discretionary income by credit provider.

• Proving discretionary income & necessary expenses.

• Importance of credit bureau reports.

• Duties on credit provider and consumers (disclose all financial & otherobligations).

• Acknowledging maintenance payments.

• Definitions.

• Developmental credit agreements excluded from draft regulations, but NOTfrom reckless lending provisions in the NCA.

• Removal of distinction between secured and unsecured credit. Certain factorsare important:

• asset being obtained with credit may generate income and should befactored in;

• asset being obtained might bring with it more future expenses and thoseshould therefore be factored in.

2014 Draft Affordability Regulations

• Table of income, necessary expense norms, fixed factors (low-incomegroup vulnerable and might be marginalised).

• The important role of credit bureau reports in assessments &influence of credit amnesty in this.

• Long periods (7 & 14 business days) in which to do checks.

• Draft regulation 19(7) – adverse info only reported after threemonths. What if it is a large mortgage agreement that is involved,eg, where monthly instalment is R25 000–R50 000? If missed for 3months it will be a large amount.

• Draft regulation 19(11) – paid up judgment & admin order referonly to capital amount? What about interest?

• Given credit amnesty future adverse listings should be monitoredand reported.

2014 Draft Affordability Regulations

• Pending 71A in National Credit Amendment Act

o settlement of any obligation does it refer to the full outstandingamount or does it only refer to the amount in default/arrears?Acceleration clauses in agreements might confuse the matter.Possible interpretational problems – guidance should be given inregulations.

o In Amnesty Regulations reference is made to adverseclassification of consumer behaviour which are SUBJECTIVE, butin s 71A no such distinction. Important that OBJECTIVE listingsremain in payment profile, eg, if payment was missed for a monthor the number of months it took to pay the debt.

• Credit cost multiple – will it really offer assistance to a consumer?

Draft Affordability Regulations – Issues Needing Attention

• Explanation of calculation for the table – only guidance on how to do it foundin the Sept 2013 guidelines – should be in regulations themselves.Regulations should stand on their own.

• Not really catering for the individual, particularly one willing to cut down ondiscretionary expenses. Would like to see regulations catering fordiscretionary expenses a little more.

• Lack of mentioning of other expenses (lacking flexibility) – eg, telephone(necessary expense?), domestic worker/gardener, security levy (livingexpense?) insurance & annuities. Although definition of discretionary incomeprovides for it to some extent, still no clear distinction.

• Expenses for entertainment? Def of discretionary income states “OTHERCOMMITTED PAYMENT OBLIGATIONS”.

• Focused more on the low-income group than on the middle- and high-incomegroup.

• Declaration questionnaire more suitable for low income group should cater forall groups & some expenses left out. EVIDENCE REQUIRED?

• No guidance on how to deal with adverse info on credit reports from creditbureaux.

Draft Affordability Regulations – Issues Needing Attention

• Some guidance needed as to how credit providers should assess(deal with) consumer’s general understanding of risk, costs,obligations and rights.

• Amended regulation 17(1) – info on sequestration and rehabilitationcannot be left out of credit bureau report as they are paramount.Attention to be given to the shortened periods for adverse info andadmin orders.

• Grievances in reg 14 to be aligned with ss 60–62.

• Penalties for consumer – chapter 6.

• Little too complex – small micro-lenders will have difficultyunderstanding as well as front line employees of credit providers.

CLOSING COMMENTS• Final Affordability Regulations expected before the

end of the year.

• In essence be the same as current draft

Regulations.

• Developmental agreements still to be excluded from

Affordability Regulations, but not from the reckless

lending provisions in the NCA.

• Hopefully issues needing attention will be addressed

in the final Regulations.

• Hopefully final Regulations will be more flexible.