perfil de la industria automotriz global— enfoque · pdf fileventas globales...

TRANSCRIPT

Perfil de la industria automotriz global—Enfoque Argentina

Guido VildozoManager, Latin America September, 2012

Copyright © 2010 IHS Inc. All Rights Reserved.

Agenda

• Global• Regional• Brasil• Argentina• Venezuela• Chile• Colombia• Conclusiones

Copyright © 2010 IHS Inc. All Rights Reserved.

-10

-5

0

5

10

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014

Real GDP Industrial Production

(Percent change)

La Economía Global Procede con Cautela

3

Copyright © 2010 IHS Inc. All Rights Reserved.

-4

-2

0

2

4

6

8

10

1990 1993 1996 1999 2002 2005 2008 2011 2014

World Advanced Countries Emerging Markets

(Real GDP, percent change)

Los Mercados Emergentes Lideran la Expansión Global, No Son Inmunes

4

Copyright © 2010 IHS Inc. All Rights Reserved.

-30 -20 -10 0 10 20

China (SSEA)

Emerging Markets* (MSCI)

Japan (Nikkei 225)

Eurozone (FTSE Euro 100)

Canada (S&P TSX)

World, Developed* (MSCI)

United Kingdom (FTSE 100)

United States (S&P 500)

2012 year-to-date (Aug. 15) 2011 2010

(Percent change)

* In US dollars

Mercados Presentan Ganancias en el 2012

5

Copyright © 2010 IHS Inc. All Rights Reserved.

(Index, over 50 indicates expansion)

25

30

35

40

45

50

55

60

65

2005 2006 2007 2008 2009 2010 2011 2012

United States Eurozone China Japan

Índices de Manufactura Anuncian un Estancamiento

6

Sources: Institute for Supply Management, Markit, China Federation of Logistics and Purchasing

Copyright © 2010 IHS Inc. All Rights Reserved.

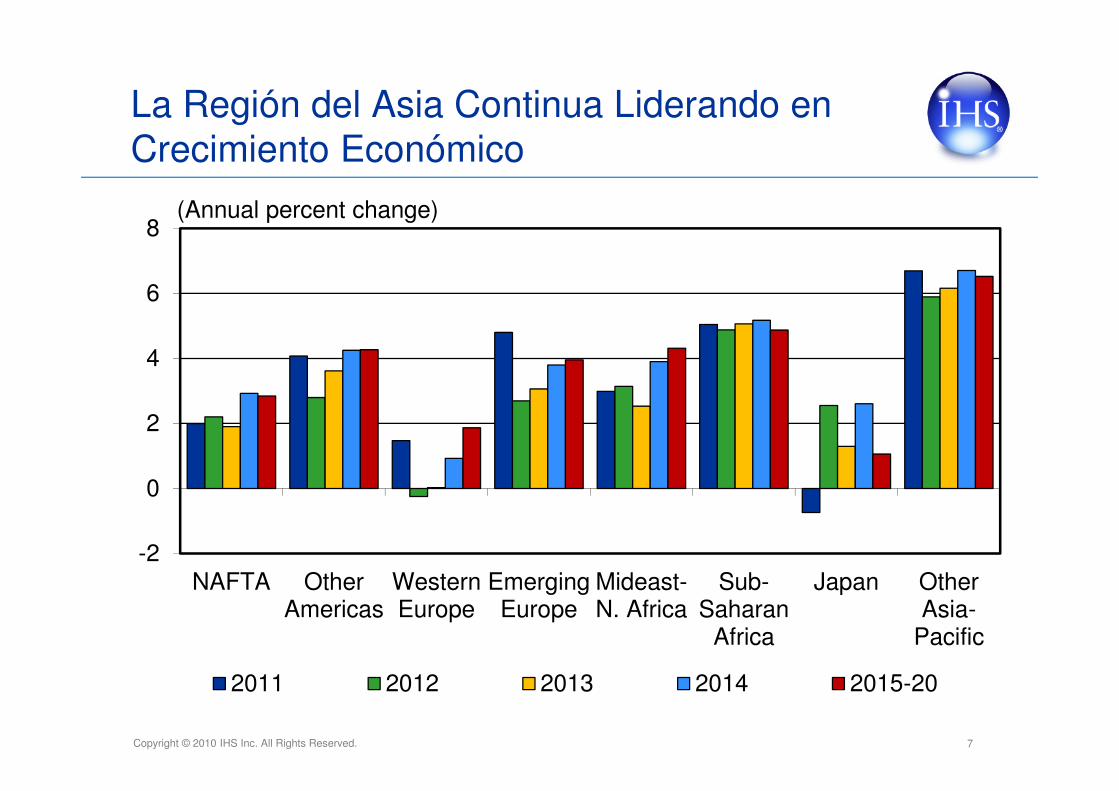

-2

0

2

4

6

8

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

2011 2012 2013 2014 2015-20

(Annual percent change)

La Región del Asia Continua Liderando en Crecimiento Económico

7

Copyright © 2010 IHS Inc. All Rights Reserved.

-2

0

2

4

6

8

10

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

2011 2012 2013 2014 2015-20

(Annual percent change)

Las Tasas de Inflación Varían Regionalmente

8

Copyright © 2010 IHS Inc. All Rights Reserved.

Shocks Externos a la Industria Automotriz

Spluttering Along

Spain & Italy Defaults, EurozoneBreaks ApartGlobal FinancialCrisis II(Early Vortex)

Greece Exits

RECOVERYRe-ignites

Sub-Prime CrisisBear Sterns

OilHits $147

Lehman Bros

Economies Rebound (inventory)

Libya, Arab Spring, Oil Surges

Japan Disasters

Greek Debt Crisis kicks off

Liquidity Freeze

Global Great Recession

US Debt Ceiling DebacleDowngraded

Is Greece Europe's Lehman Bros ?

Confidence Slumps

MarketsDrag Italy Into PIIGSClass

Inflation Surges in Emerging Markets

TARP China Stimulates

Banks Recapitalised,Nationalised, Guaranteed

Fiscal Pump Priming

Private Sector Debt => Sovereign Debt

Confidence Slumps

Banking System is Stabilized

Consumer De-leveraging

Mature EconomiesGrowth Fades

Consumer De-leveragingStill There

Po

lic

y R

es

po

ns

e

Event or Shock

QEIIInterest Rates Slashed, QEI

Auto Incentives Europe, China, Brazil, Japan, US India

Auto Incentives Ending

Auto Incentives Phasing out

Auto Bail Outs, Financing and Restructuring

World Auto Sales Track

Cooling Measures In EM

Japan Supply Chain Crisis

Fiscal TighteningAccelerated

Successive EU Summits-no silver bullet

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

ECB (LTRO)

ESM

Iranembargo

?

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales

50

60

70

80

90

100

110

120

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

BASE OPTIMISTIC PESSIMISTIC

.

% CHANGE 2011 2012 2013 2014 2015

BASE 4.3% 4.7% 3.1% 6.7% 5.9%

Copyright © 2010 IHS Inc. All Rights Reserved. 11

Ventas Globales — 10 Armadoras mas Grandes

0

2

4

6

8

10

12

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mil

lio

ns

Volkswagen-Porsche Toyota General Motors

Renault-Nissan Hyundai-Kia Ford

Fiat Auto-Chrysler Honda PSA

Suzuki

Units/MM Empresas buscan mayor cobertura global e eficiencia de costos

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales- El Nuevo Coloso Llamado China

0

5

10

15

20

25

30

35

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

% CHANGE 2011 2012 2013 2014 2015

BASE 3.6% 7.2% 8.7% 10.7% 8.9%

Sales struggling a bit this year, soft landing is key to long-term growth

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales – Japón

3.5

4.0

4.5

5.0

5.5

6.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

Tendencia de caída dada la edad de su población

% CHANGE 2011 2012 2013 2014 2015

BASE -15.6% 24.5% -7.8% -0.9% -0.1%

Copyright © 2010 IHS Inc. All Rights Reserved. 14

Ventas Globales — Europa Occidental

12

13

14

15

16

17

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Millio

ns

Units/MM

% CHANGE 2011 2012 2013 2014 2015

BASE -0.3% -8.8% -2.0% 5.5% 5.3%

Austeridad fiscal limita el potencial de ventas

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales – Europa Occidental

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

France Germany Italy Spain United Kingdom

% CHANGE 2011 2012 2013 2014 2015

France -1.4% -10.5% -4.2% 5.9% 2.7%

Germany 9.7% -2.2% -0.1% 4.1% 1.7%

Italy -9.9% -21.5% -1.0% 7.6% 11.8%

Spain -17.0% -16.7% -2.4% 13.1% 24.3%

UK -2.3% 1.1% -0.8% 5.6% 5.6%

El sur sufre, mientras que el norte aun paga los programas de incentivos

Copyright © 2010 IHS Inc. All Rights Reserved. 16

Ventas Globales — Europa Oriental y Central

2

3

4

5

6

7

8

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Millio

ns

Units/MM

% CHANGE 2011 2012 2013 2014 2015

BASE 23.8% 3.3% 3.0% 9.3% 6.0%

La nueva esperanza Europea

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales – Norte América

10

11

12

13

14

15

16

17

18

19

20

21

22

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

BASE OPTIMISTIC PESSIMISTIC

% CHANGE 2011 2012 2013 2014 2015

BASE 9.3% 10.3% 3.8% 5.2% 3.7%

EUA lidera la recuperación regional con el apoyo de México y Canadá

Copyright © 2010 IHS Inc. All Rights Reserved.

Ventas Globales - Sud América

1

2

3

4

5

6

7

8

9

10

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mil

lio

ns

BASE OPTIMISTIC PESSIMISTIC

% CHANGE 2011 2012 2013 2014

BASE 9.3% 5.5% -0.6% 6.1%

Copyright © 2010 IHS Inc. All Rights Reserved. 19

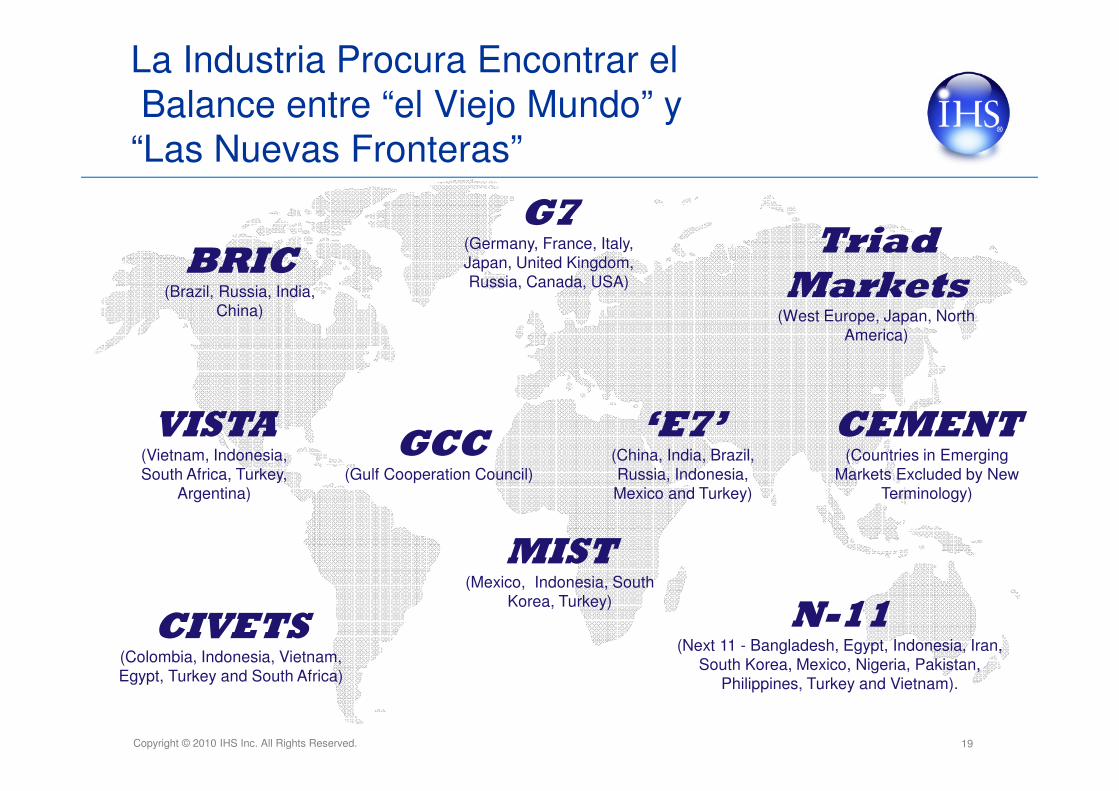

La Industria Procura Encontrar elBalance entre “el Viejo Mundo” y

“Las Nuevas Fronteras”

Triad

Markets(West Europe, Japan, North

America)

‘E7’(China, India, Brazil, Russia, Indonesia, Mexico and Turkey)

G7(Germany, France, Italy, Japan, United Kingdom, Russia, Canada, USA)

BRIC(Brazil, Russia, India,

China)

VISTA(Vietnam, Indonesia, South Africa, Turkey,

Argentina)

MIST(Mexico, Indonesia, South

Korea, Turkey)

GCC(Gulf Cooperation Council)

N-11(Next 11 - Bangladesh, Egypt, Indonesia, Iran,

South Korea, Mexico, Nigeria, Pakistan, Philippines, Turkey and Vietnam).

CEMENT(Countries in Emerging

Markets Excluded by New Terminology)

CIVETS(Colombia, Indonesia, Vietnam, Egypt, Turkey and South Africa)

Copyright © 2010 IHS Inc. All Rights Reserved. 20

Tasas de MotorizaciónV

ehic

les

In U

se P

er 1

000

Peo

ple

GDP Per Capita (in thousand 2005 US$)

US

Sweden

Russia

S Korea

Japan

Australia

Brazil

ItalySlovenia

Spain

China

PolandCzech Rep

Canada

UK

France

Germany

Taiwan

India

Thailand

Hungary

Mexico

TurkeyChile

Each $1000 increase in wealth leads to 15 more vehicles per 1000

people.

Source: CY2010 Data, IHS Data Insights

Copyright © 2010 IHS Inc. All Rights Reserved.

y = -0.0000003749x2 + 0.0272263164x - 76.5859828870

R2 = 0.7429749568-100

0

100

200

300

400

500

600

0 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000 55000

21

Ventas Globales Modelo de Saturación de Carros Pasajeros

GDP Per Capita PPP in USD (2005)

Car densityper 1000 pop

Copyright © 2010 IHS Inc. All Rights Reserved. 22

Ventas Globales –Triad vs BRICs vs ROW

0

20.000.000

40.000.000

60.000.000

80.000.000

100.000.000

120.000.000Beyond BRIC BRIC Mature

Realces:

• El 2000 aprox 80% de la ventasglobales era en los mercadosmaduros. Este año será el 48% ypara el 2019 se reduce a 40%.

• Los mercados maduros novolverán a los volúmenes previosa la crisis del 2007.

• China va contribuir cerca al28% del crecimiento global hastael 2019.

78.7 million

105.5 million

Copyright © 2010 IHS Inc. All Rights Reserved. 23

El “Viejo Mundo” cede a “Nuevas Fronteras”

0

5

10

15

20

25

30

35

40

45

50

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mil

lio

ns

TRIAD BRICS ROW

Units/MM

ROW = Rest of World

BRICS = Brazil, Russia, India, China

TRIAD = North America, Western Europe, Japan

ROW – Iran, Saudi Arabia, South Africa are the volume leaders

Copyright © 2010 IHS Inc. All Rights Reserved. 24

Ventas Globales: La próxima onda expansiva

Population in Mio.

GDP/Capita in Real US-$

Population in Mio.

GDP/Capita in Real US-$

PopulationChange

GDP/CapitaChange

BRIC China 1,347 3,142 1,385 5,547 3% 77%BRIC India 1,241 1,065 1,372 1,802 10% 69%BRIC Brazil 197 5,729 209 7,486 6% 31%BRIC Russia 143 6,872 141 8,849 -1% 29%

1 Indonesia 242 1,660 261 2,419 7% 46%2 Mexico 115 8,378 125 10,455 9% 25%3 Philippines 95 1,434 108 1,834 14% 28%4 Turkey 74 8,325 80 10,528 9% 26%5 Thailand 70 3,024 72 4,112 3% 36%6 South Africa 50 5,969 52 7,896 4% 32%7 Colombia 47 4,130 52 5,403 11% 31%8 Argentina 41 6,773 44 8,685 7% 28%9 Malaysia 29 5,735 33 7,979 13% 39%

10 Chile 17 8,568 18 11,490 6% 34%

2011 2019

Beyond BRIC Beyond BRIC

2011 vs. 2019

Beyond BRIC

Source: IHS – August 2012 Forecast

Copyright © 2010 IHS Inc. All Rights Reserved.

Producción en los BRICsA-Segment

0%

10%

20%

30%

40%

50%2007

2010

20132016

2019

BrazilChinaIndiaRussiaGlobal

25

El “share” cae globalmente excepto en Brasil

Domina en India y China pero declina a partir del 2013

Representado por OEMsChinas e Hindús y en menor escala en los OEMs Globales

Copyright © 2010 IHS Inc. All Rights Reserved.

Producción en los BRICsB-Segment

0%

20%

40%

60%

80%

100%2007

2010

20132016

2019

BrazilChinaIndiaRussiaGlobal

26

China es el mercado que menos acogida tiene para el segmento B

Domina en Brasil pero vera la presión de importados e dificultad para exportarlos

Crecimiento en Rusia en India capturando al consumidor primicio

India se fortalece con solidas exportaciones

Alta integración de plataformas globales

Copyright © 2010 IHS Inc. All Rights Reserved.

Producción en los BRICsC-Segment

0%

10%

20%

30%

40%

50%2007

2010

20132016

2019

Brazil

China

India

Russia

Global

27

Brasil e India están por debajo del estándar global

El segmento pierde mercado en Rusia

Segmento con mucho potencial en la China

Casi todas las plataformas en el segmento son global e tienen “economía de escala”

Copyright © 2010 IHS Inc. All Rights Reserved.

Producción en los BRICsD/E-Segment

0%

10%

20%

30%2007

2010

20132016

2019

Brazil

China

India

Russia

Global

28

Todos los BRICs están debajo del estándar global

Rusia se estabiliza conforme revisa sus aranceles de aduana

Brasil e India tienen presencia marginal

Plataformas globales donde hay una fuerte presencia de “Crossovers”

Copyright © 2010 IHS Inc. All Rights Reserved.

Producción en los BRICsFull-Frame

0%

10%

20%

30%2007

2010

20132016

2019

Brazil

China

India

Russia

Global

29

Cambio a “uni-body” afecta a todos los mercados

Solo India tiene planes de desarrolo en “mini” chassis

Porcentaje se contrae en China e Russia con el crecimiento de sistemas de transporte publico

Lenta integracion con plataformas globales

Copyright © 2010 IHS Inc. All Rights Reserved.

40%

50%

60%

70%

80%

90%

100%

0

2

4

6

8

10

12

14

Brazil China India Russia ROW

2019 Capacity U

tilization %S

trai

ght T

ime

Cap

acity

Cha

nge

(Mill

ions

)

2012-2019 Change 2012 Utilization 2019 Utilization

Straight-Time Capacity = Core shift set up 1, 2 or 3 shifts

Crecimiento en Capacidad 2012 vs. 2019

Copyright © 2010 IHS Inc. All Rights Reserved.

Expansión en Capacidad 2012 - 2019

0 100 200 300 400

Ford

Mitsubishi

PSA

GM

Jianghuai

Chery

Honda

Ren/Niss

VW

Fiat

Straight-time Capacity - Thousands

Brasil

0 30 60 90 120

Ren/Niss

PSA

GAZ Group

Fiat

VW

Straight-time Capacity - Thousands

Rusia

31

Copyright © 2010 IHS Inc. All Rights Reserved.

Expansión en Capacidad 2012 - 2019

0 250 500 750 1000

Honda

Ren/Niss

Tata

Hyundai

VW

GM

Ford

Bajaj Auto

Mahindra

Maruti/Suzuki

Straight-time Capacity – Thousands

India

0 300 600 900 1200

Geely

Dongfeng

FAW-VW

Dongfeng-Yueda-Kia

Great Wall

SAIC-GM-Wuling

**S-GM

Chery

Changan-Ford-Mazda

*S-VW

Straight-time Capacity - Thousands

China

32

* S-VW = Shanghai VW, ** S-GM = Shanghai GM

Copyright © 2010 IHS Inc. All Rights Reserved. 33

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

Millo

nes

Venezuela

Uruguay

Peru

Paraguay

Ecuador

Colombia

Chile

Brazil

Bolivia

Argentina

Venta Regional por País-Volumen

Copyright © 2010 IHS Inc. All Rights Reserved. 34

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

Millo

nes

Venezuela

Uruguay

Peru

Ecuador

Colombia

Chile

Brazil

Argentina

Producción Regional por País-Volumen

Copyright © 2010 IHS Inc. All Rights Reserved.

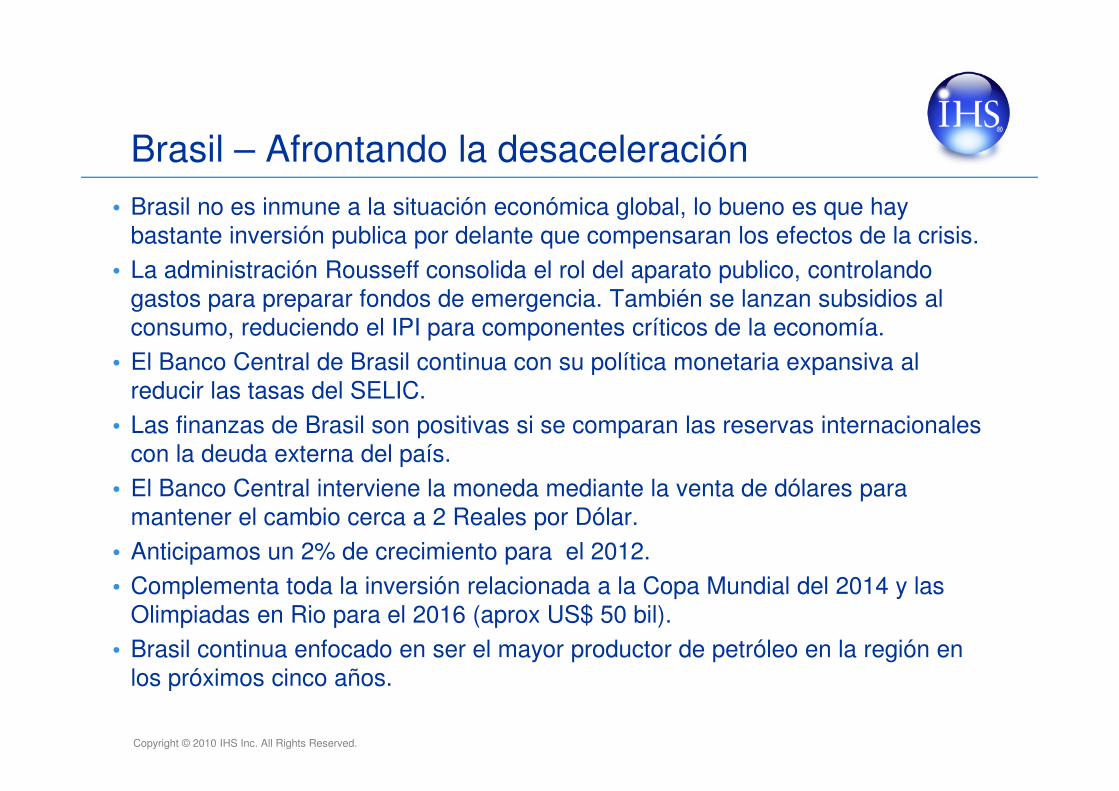

Brasil – Afrontando la desaceleración• Brasil no es inmune a la situación económica global, lo bueno es que hay

bastante inversión publica por delante que compensaran los efectos de la crisis.• La administración Rousseff consolida el rol del aparato publico, controlando

gastos para preparar fondos de emergencia. También se lanzan subsidios al consumo, reduciendo el IPI para componentes críticos de la economía.

• El Banco Central de Brasil continua con su política monetaria expansiva al reducir las tasas del SELIC.

• Las finanzas de Brasil son positivas si se comparan las reservas internacionales con la deuda externa del país.

• El Banco Central interviene la moneda mediante la venta de dólares para mantener el cambio cerca a 2 Reales por Dólar.

• Anticipamos un 2% de crecimiento para el 2012.• Complementa toda la inversión relacionada a la Copa Mundial del 2014 y las

Olimpiadas en Rio para el 2016 (aprox US$ 50 bil).• Brasil continua enfocado en ser el mayor productor de petróleo en la región en

los próximos cinco años.

Copyright © 2010 IHS Inc. All Rights Reserved.

*Annual average, **Billions of US dollars

-60

-40

-20

0

20

2004 2006 2008 2010 2012 20141,5

2,0

2,5

3,0

2004 2006 2008 2010 2012 2014

-202468

2004 2006 2008 2010 2012 2014

Real GDP Growth (%) Consumer Price Inflation (%)

Exchange Rate per USD* Current-Account Balance**

0

2

4

6

8

2004 2006 2008 2010 2012 2014

Brasil Perfil Económico

Copyright © 2010 IHS Inc. All Rights Reserved. 37

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

1990 1995 2000 2005 2010 2015 2020

Real GDP

(Percent Change)

PIB- Crecimiento Económico

El PIB creció 2.8% en promedio entre 1955-2005El PIB creció 2.8% en promedio entre 1955-2005

GDP Growth 2006-10 (4.45%) 2011-15 (3.48%) 2016-20 (4.51%)

Copyright © 2010 IHS Inc. All Rights Reserved. 38

60

70

80

90

100

110

120

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

LV Sales (left scale) Employment Index (right scale)

Ventas Mensuales– Promedio Trimestral vs Índice de Empleo Formal

El empleo formal genera consumoEl empleo formal genera consumo

Thousand Units

Copyright © 2010 IHS Inc. All Rights Reserved. 39

Ventas Mensuales – Promedio Trimestral vs Financiamiento

20

25

30

35

40

45

50

55

6050

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

LV Sales (left scale) APR Financing (right scale)

PercentThousand Units

Copyright © 2010 IHS Inc. All Rights Reserved. 40

Incremento en Mora Bancaria para Prestamos al Consumo Automotriz

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Percent

Copyright © 2010 IHS Inc. All Rights Reserved. 41

Brasil: tasas de empleo, financiamiento e salarios tienen un impacto histórico

-.15

-.10

-.05

.00

.05

.10

.15

13.2

13.6

14.0

14.4

14.8

15.2

90 92 94 96 98 00 02 04 06 08 10

Residual Actual Fitted

Copyright © 2010 IHS Inc. All Rights Reserved. 42

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Current Base Pessimistic (20%) Optimistic (20%)

Million Units

Perspectiva de Ventas Brasil

El IPI genera incertidumbre a corto plazoEl IPI genera incertidumbre a corto plazo

Copyright © 2010 IHS Inc. All Rights Reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2007 2009 2011 2013 2015 2017 2019

Others Chery Jianghuai Mitsubishi Honda

Toyota PSA Hyundai Renault/Nissan Ford

General Motors Volkswagen Fiat

Percentage

Brasil –Market Share

Los grandes pierdenLos grandes pierden

Copyright © 2010 IHS Inc. All Rights Reserved.

Brasil tiene una nueva estructura del IPI queimpacta vehículos importados

OEMs with local content

OEMs that don’t meet requirements

IPI IPI

Passenger Cars Fuel Type

Up to 1000cc Flex-Fuel 7 37

Up to 1000cc Gasoline 7 37

1001cc to 2000cc Flex-Fuel 11 41

1001cc to 2000cc Gasoline 13 43

2001cc Flex-Fuel 18 48

2001cc Gasoline 25 55

HCVs NA 30

Light Commercial Vehicles (PUPs/Vans)

NA 4 34

Copyright © 2010 IHS Inc. All Rights Reserved.

0

1000

2000

3000

4000

5000

6000

7000

8000

Investment OEMs Investment Suppliers

US $ 76 Billion 1980-2010US $ 26 Billion 2011-2026US $ 76 Billion 1980-2010US $ 26 Billion 2011-2026

US$ Millions

Inversion de la Industria Automotriz

Copyright © 2010 IHS Inc. All Rights Reserved. 46

0,50

1,50

2,50

3,50

4,50

5,50

6,50

7,50

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Light Vehicle Production Capacity

• 5 MM capacity by 2015 • Two new plants in 2012: Hyundai, Toyota

• 5 MM capacity by 2015 • Two new plants in 2012: Hyundai, Toyota

Million Units

Producción: Inversiones Para Atender Demanda de los próximos Diez Anos

Copyright © 2010 IHS Inc. All Rights Reserved. 47

Brasil Scorecard

Pluses:

• Estabilidad Economica• Inversion Directa Extranjera• Empleo• Financiamiento

• Rentabilidad/Lucratividad• Hasta 84 Meses• Reduccion de Tasas

• Cambio de Moneda (Importados)• Apoyo Gubernamental a la Industria• PIB per Capita• Baja Densidad de Motorizacion• Producto Nuevo• Inversion de la Industria

Minuses:• Capacidad Ociosa en plantas• Falta de Capacidad del Sector

Autopartista• Infraestructura Ineficiente• Cambio de Moneda (Exportaciones)• Precio de Vehiculos Nuevos• Riesgo de Credito Privado/PIB• Crecimiento Salarial vs Inflacion• Congestion Vehicular• Dependencia en commodities

Copyright © 2010 IHS Inc. All Rights Reserved.

*Annual average, **Billions of US dollars

-5

0

5

10

15

2004 2006 2008 2010 2012 20141,52,53,54,55,56,5

2004 2006 2008 2010 2012 2014

02468

10

2004 2006 2008 2010 2012 2014

Real GDP Growth (%) Consumer Price Inflation (%)

Exchange Rate per USD* Current-Account Balance**

0

5

10

15

2004 2006 2008 2010 2012 2014

Argentina Perfil Económico

Copyright © 2010 IHS Inc. All Rights Reserved. 49

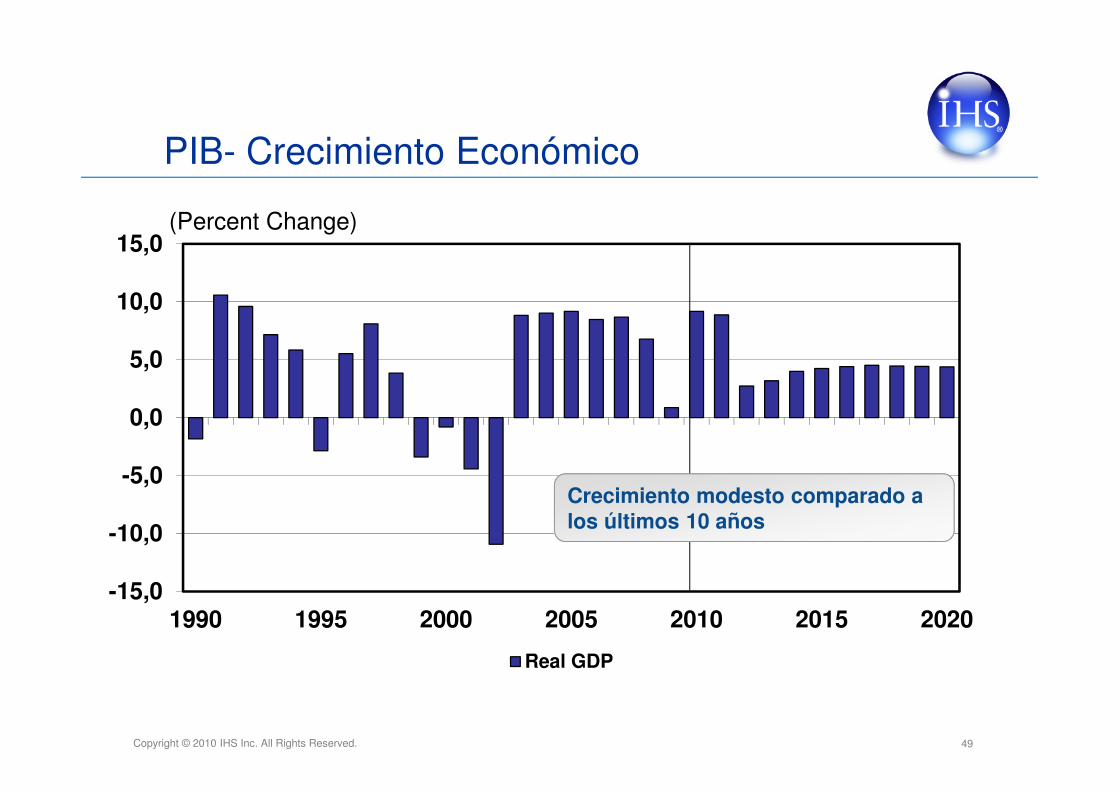

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

1990 1995 2000 2005 2010 2015 2020

Real GDP

(Percent Change)

PIB- Crecimiento Económico

Crecimiento modesto comparado a los últimos 10 añosCrecimiento modesto comparado a los últimos 10 años

Copyright © 2010 IHS Inc. All Rights Reserved. 50

Ventas Mensuales – Promedio Trimestral vs Índice de Confianza del Consumidor

30

35

40

45

50

55

60

65

70

0

15

30

45

60

75

90

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

LV Sales (left scale) Consumer Sentiment (right scale)

PercentThousand Units

Sector permanece robusto a pesar de caída en confianzaSector permanece robusto a pesar de caída en confianza

Copyright © 2010 IHS Inc. All Rights Reserved. 51

Ventas Mensuales – Promedio Trimestral vs Exportaciones

1

2

3

4

5

6

7

8

9

0

15

30

45

60

75

90

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

LV Sales (left scale) Exports (Right)

Billion US $Thousand Units

Las exportaciones impactan el movimiento economico

Las exportaciones impactan el movimiento economico

Copyright © 2010 IHS Inc. All Rights Reserved. 52

Argentina: crecimiento económico, población y balanza comercial

-.2

-.1

.0

.1

.2

11.0

11.5

12.0

12.5

13.0

13.5

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Residual Actual Fitted

Copyright © 2010 IHS Inc. All Rights Reserved. 53

0,0

0,2

0,4

0,6

0,8

1,0

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Current Base Pessimistic (20%) Optimistic (20%)

Million Units

Perspectiva de Ventas Argentina

Escenario incierto a causa del panorma politico e exportaciones

Exportaciones estables, pero controles de cambio preocupanExportaciones estables, pero controles de cambio preocupan

Copyright © 2010 IHS Inc. All Rights Reserved.

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00

Volume - L Market Share - R

Million Units

Argentina –Parque automotor

Units per ‘000

Copyright © 2010 IHS Inc. All Rights Reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2007 2009 2011 2013 2015 2017 2019

Others BMW Chery Daimler Hyundai

Honda Toyota Fiat Ford PSA

Renault/Nissan General Motors Volkswagen

Percentage

Argentina –Market Share

Los Asiaticos quieren crecerLos Asiaticos quieren crecer

Copyright © 2010 IHS Inc. All Rights Reserved. 56

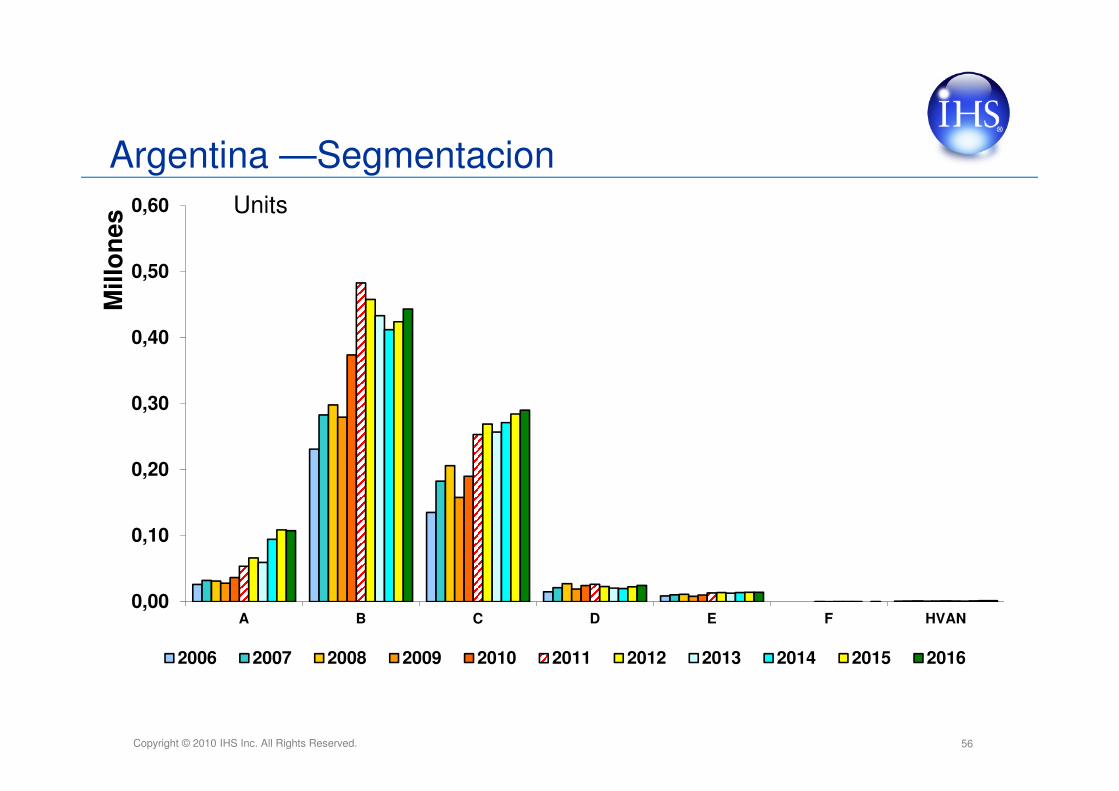

Argentina —Segmentacion

0,00

0,10

0,20

0,30

0,40

0,50

0,60

A B C D E F HVAN

Mil

lon

es

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Units

Copyright © 2010 IHS Inc. All Rights Reserved. 57

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

1,80

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Light Vehicle Production Capacity

• Capacidad: 1.2 million • No hay plantas adicionales• Capacidad: 1.2 million • No hay plantas adicionales

Million Units

Producción: Inversiones que Complementan el Crecimiento de MERCOSUR

Copyright © 2010 IHS Inc. All Rights Reserved. 58

Argentina Scorecard

Pluses:

• Commodities• Mayor exportador de oro• Estabilizacion de Finanzas Publicas• Infraestructura (Energia)• Empleo• Cambio de moneda (Exportaciones)• Apoyo Gubernamental a la Industria• Nueva gama de productos• Inversion de las terminales

Minuses:

• Inflacion• Confianza del Consumidor• Cambio de Moneda (Importados)• Demografias• Crecimiento de la Poblacion• Motorizacion• Dependencia en commodities

Copyright © 2010 IHS Inc. All Rights Reserved.

*Annual average, **Billions of US dollars

0

10

20

30

40

2004 2006 2008 2010 2012 20141,52,53,54,55,56,5

2004 2006 2008 2010 2012 2014

-505

101520

2004 2006 2008 2010 2012 2014

Real GDP Growth (%) Consumer Price Inflation (%)

Exchange Rate per USD* Current-Account Balance**

0

10

20

30

40

2004 2006 2008 2010 2012 2014

Venezuela Perfil Económico

Copyright © 2010 IHS Inc. All Rights Reserved. 60

0,0

0,1

0,2

0,3

0,4

0,5

0,0

0,1

0,2

0,3

0,4

0,5

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Current Base Pessimistic (25%) Optimistic (15%)

Million Units

Perspectiva de Ventas Venezuela

Mas un arte que cienciaMas un arte que ciencia

Copyright © 2010 IHS Inc. All Rights Reserved. 61

0,00

0,05

0,10

0,15

0,20

0,25

0,30

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Light Vehicle Production Capacity

• Capacidad 250K• Riesgo de nacionalización• Nuevos players?

• Capacidad 250K• Riesgo de nacionalización• Nuevos players?

Million Units

Producción: Limitados por políticas de cambio de moneda

Copyright © 2010 IHS Inc. All Rights Reserved. 62

Venezuela Scorecard

Pluses:

• Precios establecidos por orden Gubernamental

• Precio de usados• Tiendas “sociales”• Precio del petróleo• Elecciones• Potencial de 500K• Baja motorización

Minuses:• Quota de importacion• Acceso a moneda extranjera• Inflacion• Panorama Politico• Diferentes tarifas de cambio de

moneda• Sindicatos• Precios establecidos por el Gobierno• Perdidas de las terminales• Capacidad de sector de autopartes• Nacionalizacion• Dependencia del petroleo

Copyright © 2010 IHS Inc. All Rights Reserved.

*Annual average, **Billions of US dollars

-10

-5

0

5

10

2004 2006 2008 2010 2012 20141,5

201,5

401,5

601,5

801,5

2004 2006 2008 2010 2012 2014

-4-202468

2004 2006 2008 2010 2012 2014

Real GDP Growth (%) Consumer Price Inflation (%)

Exchange Rate per USD* Current-Account Balance**

02468

10

2004 2006 2008 2010 2012 2014

Chile Perfil Económico

Copyright © 2010 IHS Inc. All Rights Reserved. 64

Chile: economía, población y demografías salariales

-.3

-.2

-.1

.0

.1

.2

.3

11.2

11.6

12.0

12.4

12.8

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Residual Actual Fitted

Copyright © 2010 IHS Inc. All Rights Reserved. 65

0,0

0,1

0,2

0,3

0,4

0,5

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Current Base

Million Units

Perspectiva de Ventas Chile

Chile should post a negative 2012 given global economicsChile should post a negative 2012 given global economicsChile contraerá el 2012 dado el comportamiento económico global

Chile contraerá el 2012 dado el comportamiento económico global

Copyright © 2010 IHS Inc. All Rights Reserved.

*Annual average, **Billions of US dollars

-15

-10

-5

0

2004 2006 2008 2010 2012 20141500,0

2000,0

2500,0

3000,0

2004 2006 2008 2010 2012 2014

0

2

4

6

8

2004 2006 2008 2010 2012 2014

Real GDP Growth (%) Consumer Price Inflation (%)

Exchange Rate per USD* Current-Account Balance**

0

2

4

6

8

2004 2006 2008 2010 2012 2014

Colombia Perfil Económico

Copyright © 2010 IHS Inc. All Rights Reserved. 67

Colombia: economía, población y demografías salariales

-.6

-.4

-.2

.0

.2

.4

.6

10.5

11.0

11.5

12.0

12.5

13.0

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Residual Actual Fitted

Copyright © 2010 IHS Inc. All Rights Reserved. 68

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Current Base

Million Units

Perspectiva de Ventas Colombia

Colombia tiene el reto de incertidumbre en la economía global a corto plazo

Colombia tiene el reto de incertidumbre en la economía global a corto plazo

Copyright © 2010 IHS Inc. All Rights Reserved. 69

Conclusiones• Crecimiento económico y mejor disponibilidad de crédito

han generado ventas automotrices.

• Existe un cambio, donde los mercados “emergentes” generaran crecimiento.

• Hay que estar alerta al riesgo en Europa.

• La región tiene mucho potencial pero vemos medidas proteccionistas.

• La region se separa en dos grupos: Brasil, Chile, Colombia e Peru y Argentina, Ecuador, Venezuela

• Las OEMs Koreanas e Chinas quieren ser parte del crecimiento proyectado

Copyright © 2010 IHS Inc. All Rights Reserved. 70

Muchas Gracias por VuestraAtencion!

Guido VildozoManager, Latin AmericaSeptember, [email protected]