pension program and old age benefit system in...

TRANSCRIPT

KEMENTERIAN KEUANGANREPUBLIK INDONESIA

Pension Program and Old Age Benefit System in Indonesia

Washington DC, 6 May 2016

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Raja Ampat islands

Borobudur temple Bali

Mount Bromo

Bunaken Marine ParkSamarinda Mosque

Toba Lake

Indonesia

The total area : 5,193,250 km2Population 2015 : ±255 M The number of islands : ±17.504The number of Tribes : ± 300 (sub tribe 1340)The number of languanges : ± 15 (sub language 546 )

GDP 2015 : $862 BPopulation over age 65 : 5,4% of Population Public Pension Spending : 7,9% of GDPLife expectancy : at birth 70.7

at age 65 14,2

4

% population aged 65 and

older : 5,01%

Ages 0 – 64 :

94,99%

% population aged 65

and older : 9,23%

Ages 0 – 64 :

90,77%

% population aged 65

and older : 15,78%

Ages 0 – 64 :

84,22%

*) in 000.000 (hundred thousands)

(in million)

2000 2010 2030 2050

Population 208,94 240,68 293,48 321,38

0 - 14 64,06 71,79 65,50 60,69

15 - 64 135,13 156,83 200,90 209,96

65 - up 9,75 12,06 27,09 50,72

Dependency Ratio

Old-age 7,21% 7,69% 13,48% 24,16%

Total 54,62% 53,47% 46,09% 53,06%

Indonesia‘s Demographic Structure2010-2050

5

Expenditures Profile - Indonesia

5

The data of the expenses per family in retirementstill show a trend of high epenses

The Expenses* Before and After Retirement per Family

Before retirement

After retirement

% of expenses after retirement

Source: Adapted from BPS – National Social Economic Survey

*) Exclude health expenses

6

Indonesia’s

Social Security

Administrators

Health protection for

all citizens of Indonesia

Protection for all workers in Indonesia

(Law no. 24/2011)

Death Benefit (JKM)

Old Age Saving (JHT)

Occupational Accident

Benefit (JKK)

Pension Benefit(JP)

Indonesia Social Security Scheme has been reformed since 2014

7

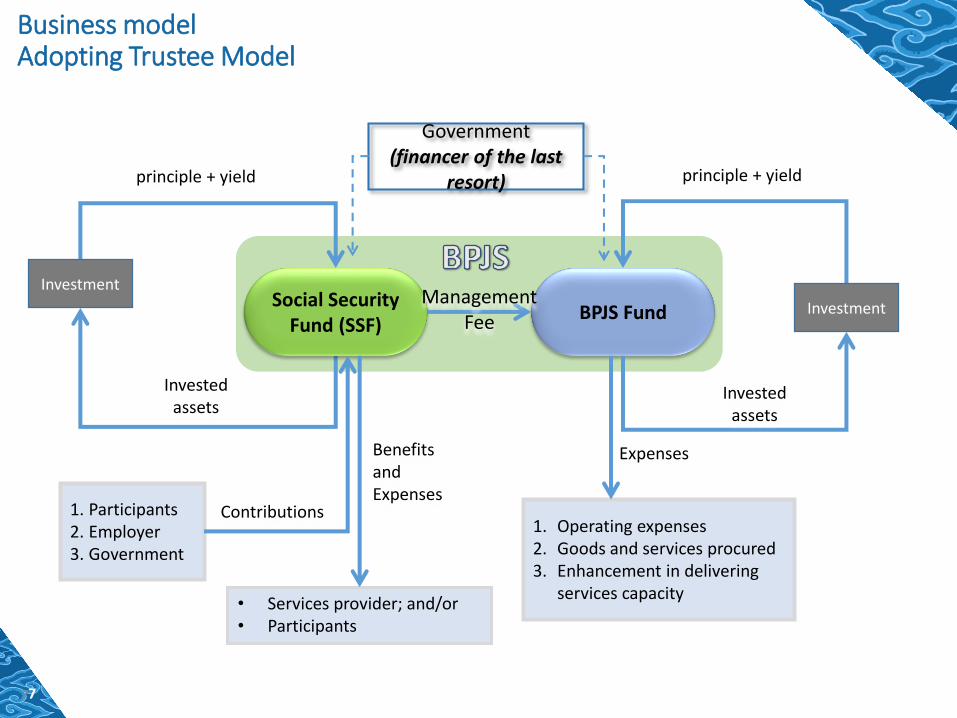

Business modelAdopting Trustee Model

7

Invested assets

Social Security Fund (SSF)

BPJS Fund

1. Operating expenses2. Goods and services procured3. Enhancement in delivering

services capacity• Services provider; and/or• Participants

Investment

1. Participants2. Employer3. Government

Investment

Invested assets

principle + yield principle + yield

Management Fee

Contributions

Benefits and Expenses

Expenses

Government(financer of the last

resort)

8

Implementation of Retirement Benefit System

04/20/1992

Civil servantPolice/army

Civil servantPolice/army

Voluntary

01/01/2014 07/01/2015

Civil servantPolice/army

Voluntary

Public Old Age Benefit,Working accident benefit, Death BenefitHealthcare

Civil servantPolice/army

Voluntary

Public Old Age Benefit,Working Accident benefit, Death Benefithealthcare

Public Pension Program

The Law No 40 Year 2004 on Nasional Social Security System

9

Retirement Benefit

Mandatory

Civil Servant

PT Taspen

Old Age Benefit

(DB)

Pension Program

(DB)

Policy&Army

PT Asabri

Old Age Beneft

(DB)

Pension Program

(DB)

All Workers

BPJS Employment

Old Age Benefit

(DC)

Working Accident Benefit

Death Benefit

Pension Plan

(DC+DB)

Voluntary

Workers (State Owned Ent. & Private Co.) & Self- employed

Employer Pension Fund

[259 EPF]

(DC&DB [80% DB]

Financial Institution PF

(DC)

[25: Bank & Life insurance]]

10

Pension Age

Pension Program (Annuity)

Early Retirement Normal Pension Age (NPA) Deferred Pension Age

Mandatory Civil Servant 50 and YoS 20 58 & 60

Army Forced 50 and YoS 20 58 & 60

Public 56, increase 1 year in every 3 years until reach age 65

Voluntarily EPF 10 Years before NPA 55 Maks 60

FIPF 10 Years before NPA Start at 40 to 55 Maks 60

Old Age Benefit(Lumpsum)

Early Retirement Normal Pension Age (NPA) Deferred Pension Age

Mandatory Civil Servant 50 and YoS 20 58 & 60

Army Forced 50 and YoS 20 58 & 60

Public 5 YoC (Govt Regulation) or1 month after lay-off

56 Gradually increase to 65

11

Benefit Formula

Old Age benefit(Lumpsum)

Pension Program(Annuity)

Mandatory Civil Servant 0,55 x YoS x Basic Salary 2,5% x YoS x Basic Salary

Policy/Army 0,55 x YoS x Basic Salary 2,5% x YoS x Basic Salary

Public 𝑐𝑜𝑛𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛 + 𝑅𝑂𝐼

If Participation < 15 years:

𝑐𝑜𝑛𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛 + 𝑅𝑂𝐼

For Participation ≥ 15 Years:1% x YoC x (Index Carrer Average, indexed to inflation (maks salary ± $700)

Maks Benefit: ±$300Min Benefit: ±$ 30

Benefit Indexed to inflation

Voluntarily

EPF (DB)

[1% – 2,5%] x YoS x Basic Pension Salary (some PF use full- salary)

Maks: 80% of Basic Pension Salary

EPF & FIPF (DC) 𝑐𝑜𝑛𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛 + 𝑅𝑂𝐼

12

Financing

Old Age benefit(Lumpsum)

Pension Program(Annuity)

Mandatory Civil Servant Govt: PAYG Govt: PAYG

Policy/Army Govt: PAYG Govt: PAYG

Public 3,7% 2%

Voluntarily EPF 5% - 20%

FIPF no limitation by regulation

Employer

Employee

Old Age benefit(Lumpsum)

Pension Program(Annuity)

Mandatory Civil Servant 3,25% 4,75%

Army Forced 3,25% 4,75%

Public 2% 1%

Voluntarily EPF 5% - 7,5%

FIPF no limitation by regulation

13

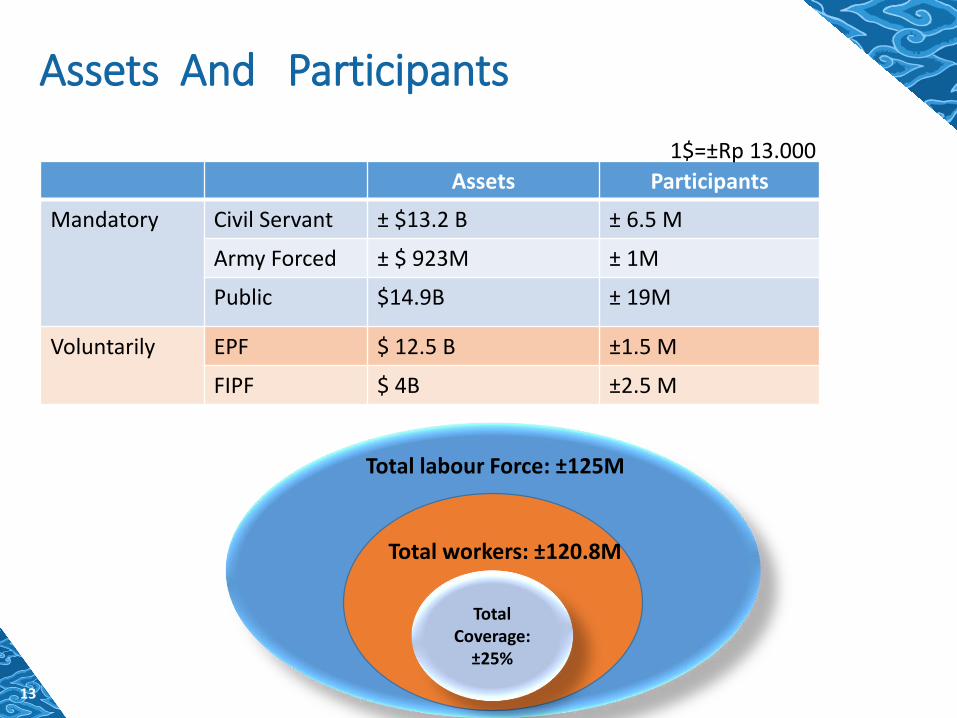

Assets And Participants

Assets Participants

Mandatory Civil Servant ± $13.2 B ± 6.5 M

Army Forced ± $ 923M ± 1M

Public $14.9B ± 19M

Voluntarily EPF $ 12.5 B ±1.5 M

FIPF $ 4B ±2.5 M

Total labour Force: ±125M

Total Coverage:

±25%

1$=±Rp 13.000

Total workers: ±120.8M

KEMENTERIAN KEUANGANREPUBLIK INDONESIA

Implementation challenges and Post Reform Plan

15

The Principles of Balance and Sustainability

15

1

2

3Affordability

Adequacy

Sustainability

Benefit has to be designed so that it is able to be funded by employers and employees

• The benefit has to be able to provide minimum replacement value of suitable income

• The amount of the output (benefit) should be in accordance with the amount of input (contribution rate and period)

Having long-term cost endurance to fund the program (actuarial fund life/AFL) in order to ensure macro economy stability

Image originally designed by www.freepik.com

Imbalance Funding may increase risk of failure on the funding program,

which is shown by the resilience of its life program.

16

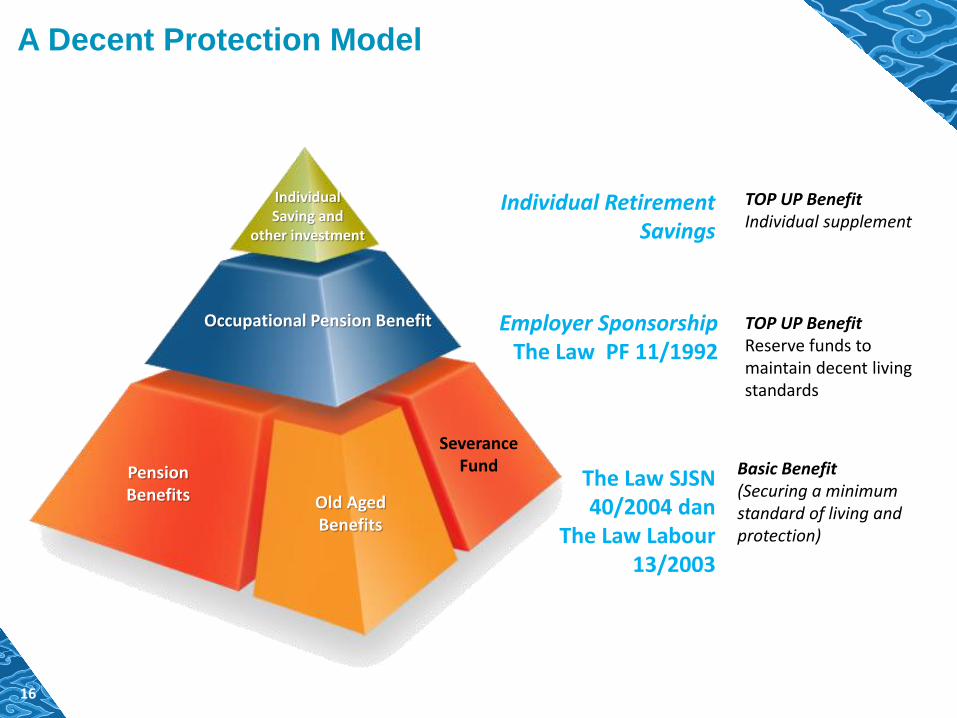

A Decent Protection Model

Pension Benefits Old Aged

Benefits

Occupational Pension Benefit

Individual Saving and

other investment

The Law SJSN40/2004 dan

The Law Labour13/2003

Employer SponsorshipThe Law PF 11/1992

Individual Retirement Savings

Basic Benefit(Securing a minimum standard of living and protection)

TOP UP BenefitReserve funds to maintain decent living standards

TOP UP BenefitIndividual supplement

Severance Fund

17

Implementation challengesThe program has just started... (1)

1. Affordability Employers have to face a burden of high contribution for the employee

benefits (about 30%)

2. Adequacy Small replacement rate (average 30%-40% of basic salary)

3. Sustainability

• Aging population

• Demographic dividend at the moment but soon it will aging rapidly

• Low real retirement age

• Investment

• The issue is more on the accumulated fund, how to utilize this fund to boost the economic growth

4. Administration system

• Unique ID and data sharing

The public Old Age Saving program has just started on Januari 1, 2014The public pension program has just started on July 1, 2015

18

Implementation challengesThe program has just started... (2)

5. Public education (low financial literacy)

6. Geographic condition

7. Economic challenges (affected by the global economic slowdown)

8. Unify the fragmented program (civil service and policy/army)

9. Expanding coverage for the informal sector

19

Government’s Concern

Administration’s Concern

Employer’s Concern

Employee’s Concern

Key factors of successful

implemenation

20

Employer’s Concern

• High Contribution

Program %

Public Pension program 2%

Old Age benefit 3,7%

Accident benefit 0.24%

Death Benefit 0,3%

Healthcare 4%

Voluntarily pension program (average)

±12.5%Range: 5% - 20%

Labour Law Severance Reserve(average)

±8%

Total ± 30.74%

21

Employee’s Concern

• High Contribution

• Promised by the Social Security Law No 40 Year 2004

“Public Program should keep decent life of elderly people”

[$170]

Program %

Public Pension program 1%

Old Age benefit 2%

Heathcare 1%

Voluntarily pension program (average)

5%

Total ± 9%

22

Government’s Concern

• During the first years of implementation, sustainability would not be an issue since there is 15 year vesting period

• Yet, periodical actuarial valuation (internal and external) is need to evaluate the balance of contribution and benefit

• Expansion to reach a large participants

23

Post reform plan

• Actuarial valuation • Review the sustainability the program

• Asses the adequacy of benefit and contribution

• Improvement in administration system• Unique ID

• Develop a robust database system merged with other social security program

• Harmonization with other employee benefit (old age saving and severence pay)

KEMENTERIAN KEUANGANREPUBLIK INDONESIA

Thank You

25

How to maintain the sustainability of pension program?

1. Massive expansion to reach a large participants (The more participants means the more premium collected).

2. Enforcing the law to employer as a result of strong legal basis.

3. Encouraging unemployed people to be integrated into workplace.

4. Review the amount of premium periodically

5. Redesigning the pension program and benefits by considering Intergenerational Faireness and Equity :

Demographic Structure

Number of young participant that is still productive

Number of participant towards retired.