pension basics for local officials teacher welfare education program 3f(n) edmonton catholic...

TRANSCRIPT

Pension Basics for Local Officials

Teacher Welfare Education Program 3F(n)

Edmonton Catholic Teachers’ Local #54

Defined Benefit Plan

• Benefit is defined by formula– A percentage of salary– Years of service

• Contributions are made to fund service

Sources of Retirement Income

• Government pension programs – Canada Pension Plan (CPP)– Old Age Security (OAS)

• Employment pensions – Alberta Teachers’ Pension Plan

• Individual savings– RRSPs– Tax Free Savings Accounts

DEFINED CONTRIBUTION (DC)

VERSUS

DEFINED BENEFIT (DB)

PENSION PLANS

Defined Contribution (DC) Plan

• Contributions are defined, pension is not• Contributions are invested for the member• Member makes some or all contribution

decisions• Investment risk is the responsibility of the

individual• Monthly pension received is total of

contributions plus earnings of the plan

DC Plan Continued

• Administration costs are in excess of 2%• Market fluctuations can have a negative

affect on your retirement security.

(NOTE: THIS IS NOT YOUR ALBERTA TEACHERS’ PENSION PLAN (ATTP) )

Benefits of a Defined Benefit (DB) Plan

• Pension amount is known and predictable• Pension is based on salary prior to

retirement including negotiated salary increases

• Risk is shared between employer (government) and all plan members

(NOTE: THIS IS YOUR AlbertaTPP)

Funding the Defined Benefit

• Prefunding – Funding future pensions as they are earned

• Actuaries estimate pensions – owed to all teachers over their lifetime – death benefits – pensions owed to teachers who quit prior to being

eligible for pension (salaries, age of retirement, mortality rates)

• Calculate amount needed today to pay pensions later depending on expected rate of return.

• Assign to each sponsor (government and teachers) depending on contribution agreement

Contribution Rates(What plan sponsors pay)

September 1, 2014 Teachers Government

Normal Cost (60%) 7.85% 7.85%10% COLA 0.50% 0%Post 1992 Deficiency 4.80% 4.80%Post 10% COLA 0.23% 0%

Total 13.46% 12.65%

Teachers: Up to Yearly Maximum Pensionable Earnings (YMPE) $53,600 - 11.44%; and over YMPE - 16.34%

COLA = Cost of Living Allowance (annual increase based on provincial averages)

Our Defined Benefit(What we get out of the plan)• Integrated with CPP• 1.4% of five year average salary up to the

YMPE (2015 amount is $53,600)• 2% salary over the YMPE• Add those two together and multiply by

years of service

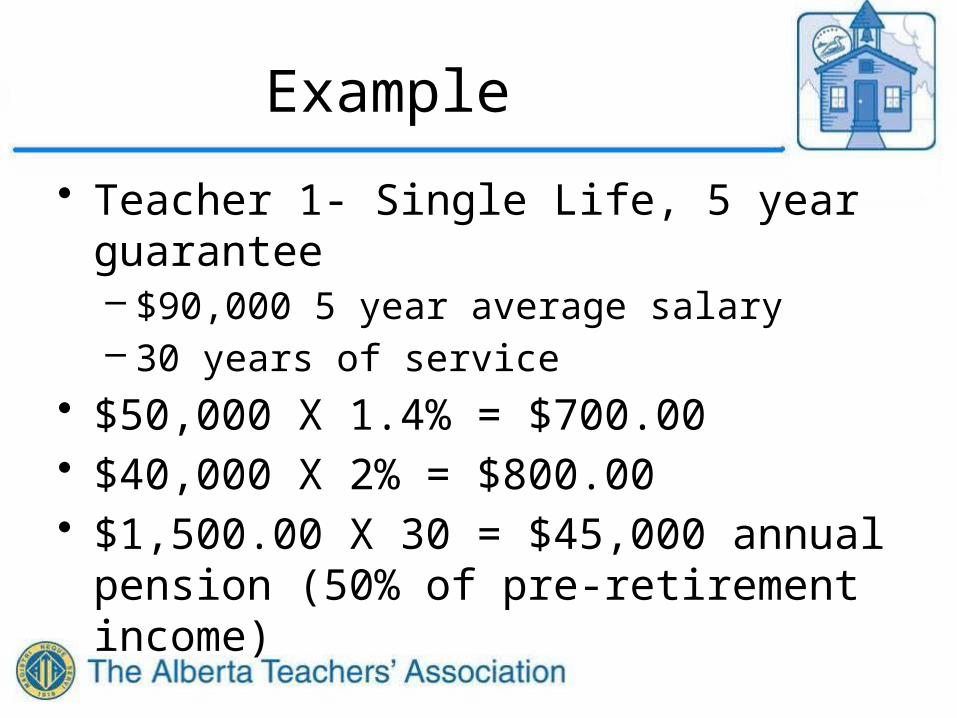

Example

• Teacher 1- Single Life, 5 year guarantee– $90,000 5 year average salary– 30 years of service

• $50,000 X 1.4% = $700.00• $40,000 X 2% = $800.00• $1,500.00 X 30 = $45,000 annual pension

(50% of pre-retirement income)

Eligibility

• For an unreduced pension– Age 65 or– Age plus service equals 85

• For a reduced pension– Age 55 and– Five years of pensionable service

• Reduction is 2% per year below 65 or 85 index, which ever is less

Accumulating Service

• Earn it - By earning salary• * Buy it (if you have Substitute Service or

Leaves of Absence) – use RRSP moneys• Transfer it (from other teacher plans or

other public sector plans)• Accumulation while on disability

* NOTE: CONTACT ATRF FOR BEST OPTION FOR YOU. DO IT NOW! THE LONGER YOU

WAIT, THE MORE IT WILL COST.

5 year average

• 60 best consecutive months• Periods of leave are dropped out unless

purchased– Do not count as 0 but are replaced by a

previous year• Part time by contract or assignment

– Annualized• Part time by leave of absence

– Not annualized

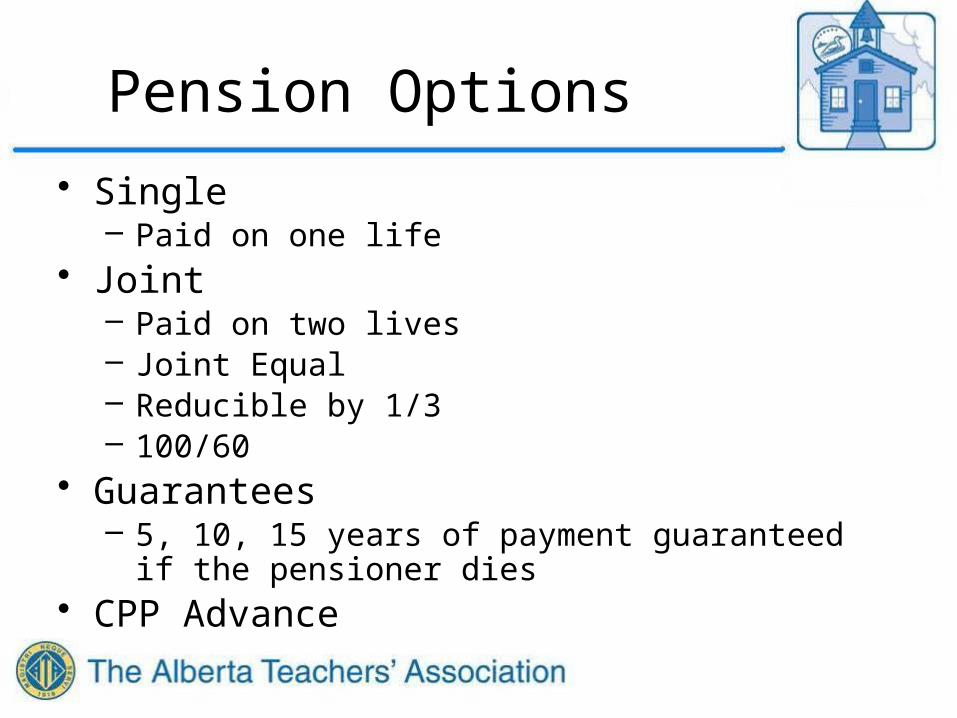

Pension Options

• Single – Paid on one life

• Joint – Paid on two lives– Joint Equal– Reducible by 1/3– 100/60

• Guarantees– 5, 10, 15 years of payment guaranteed if the

pensioner dies• CPP Advance

Pension and Marriage

• Pensions are marital property under the Marital Property Act

• Divorce– Sign off pension in the divorce agreement– Split pension

• Single pension– Pension partner must sign waiver

• Death – 1. Spouse– 2. Dependent minor children– 3. Beneficiary– 4. Estate

Who gets your pension?

• If still teaching:– Single - beneficiary receives contributions

plus interest• double for dependent minor children

– Married – pension partner receives pension based on years of service commencing the month following death, no index reduction

• Retired• according to option chosen

Who qualifies as a pension partner?

• Legally married• Common law couples who:

– live together for at least three years, and– publicly present themselves as a couple

• Same gender partners also eligible under common law terms

Pension and Taxes• RRSP room 18% of salary (to a maximum of

$24,930)• Pension benefit earned takes up RRSP room • Room taken up is called a Pension

Adjustment (PA); • PA=1.4% of YMPE + 2% of balance• ($1478 X 9) – 600 = $12,702• $90,000 X 18% = $16,200• Room = $3498

Improving the Plan• Last pension improvements were granted in

1992 (10% addition to COLA for teachers)• ATA objectives for improvements to the plan are

contained in long range policies 6.A.1 to 6.A.13 and current directives 6.B.1 to 6.B.7

• Government would have to agree to an improvement which are requested each year after ARA – Teachers contributions would rise as we pay one half– The 2007 unfunded liability agreement includes a

provision barring improvements retroactive prior to 1992.

Final Points

• Funding and Sustainability• Pension Envy• Overly rigorous application of ITA Caps • The current Alberta Government attention

to poor pension plan governance is not an issue for ATRF.