pdf.usaid.govpdf.usaid.gov/pdf_docs/pnabe866.pdf · a loan is . overdue a penalty charge of 6% is...

TRANSCRIPT

- ~ Jt~ ~ ~ ~ AtKK~~k ~ cA1

Utft ~ t22t~j~tf ~

i ~A~ts- -~~ ft

55

S

to 2

t

ft 0

2

t

~

~ o~

~

ttt~

105~ 0

~

550 ft

~~0 0~ 5

0

tot S

tt 5 0-

~

~

05

5 0 tO

00~50

-1 - - t 55 tS ~ 5 ttj

~Vto SO

OS

to

S

tot

-5

A

5-55 5

St

o(t

05

SOt

- t~

F Ln~ir~s~amp

R31~U~ ~ (5

~i~o iecL Phwse

Nurnb~r I

II

- -

2 5

55

-

5

is

05 E

Forrest - Cook~on

5 5

to 0 Of 55~ -

jot

t~tyt ~

Oo5 - t~i

plusmn~oL)e3A H Nathan

t0d~bIILJJ~3 tofl

t

Associates

- -

0

0

I

O~ tobcu 1986 ~ S

---shy ft

~ ~j2~tlt ~

5i554i-5-- S o-2 04

Of

So~f

5-St 5

0

5

to 5of05

0550

~ ________________

5 5 50

2 t

J~f A~

S

t

St 2 55

~

55

t

~

foO55~ t0 -~

Table of Contents

Introduction 1

Portrait of- a Rural Branch Bank 4

Recovery Mt-asured by Branch Accounts 9

Loan Recovery Measured from Individual Loan Records 12

e tcI Iil IIIP ne I nq I oa n Recovery 17

Table List

Table 1 A Typica] Branch Bank Balance Sheet June 30 1985

2 A T vpi a I PuRra1 Bank Profit and Loss S I-almunt ]98o4

3 Estimated Returns on Assets and Liabilities 1984 8

4 Typical Disbursement and Recovery Ratios of Short Term Agricultural Loans 11

5 Disbursements and Recoveries of Short Term Agricultunral Loans Branch Means I1

6 Distribution of RecoveryOutstanding Ratio 12

7 Distribution of Loan Size of Short Term Ag riculLura[ loans ]

8 Loan Recovery Measures 14 9 Year of Disbursement and Loan Recovery 15

10 Distribution of Mean Recovery Ratios for 20 Short Term Agricultural Loans

11 Mean Recovery Rates by Bank for Short Term 21 Agricu]tural1 Loans

12 Nominal Ratio of Short Term Agricultural Credit by Bank 22

13 Nominal Rna ioof Short Term Agricultural c-ilIi y Prdaich Size 23

14 tWminal Recovery Ratio of Short Term AqricItu1 lr wr-it by Growth of Branch 253

15 N Iin I i tPtio of Short Termi Ag ii-tura l Cred it by Age of Branch

16 tmiI fmcovery Ratio of Short Term Aiiltural Crudit and Branch Remoteness 26

17 loan Recovery iI Interest Rates 30

18 P Patio for Short Term A rilturl IW s and the Collateral Ratio 3I

19 Nominol PcoveVr Ratio for Short Term Ac~r ltu-al QIuns and Size nf Principal 3

Accronyms

ACD AclriculiuvilVredit Department

BB ) )gL ~ l l a~

DPS l)|posi t PCnsion Scheme

110 ll(ad OfF ic -)fa bank

RBBUS NiiiralBk ind Bank User Survey

RFP RuLral Fiiace Project

Pecovery ofrm Agricultural Loans

1 Introduction Phit- paper pres(ents results from a survey uljl

taken as part I tLhe Rural Finance Project(RFP) of the Bangl ad(l

Bank financed by the Unitod States Agency for International

Development WitIin1 Hie ork program of the RFP the Rural

and Bnk ULsers ~livet (PBlII was udertaken to provide a detailed s of ctiri-e if l - il-inq wi th a number of issues of importanc ill

rural finance

Perhaps tHn meodv i mportant issue currently under discussion w ih

respect to ru-il ijiance is that of loan recovery There are two quesLi o s tliil r((l 1-o 1) addressed

1 What is the recovery rate of agricultural loans This fun lshyV (10 ii i I y to answer from available Lll

tiia plalje r detai Led evidence will be presented on recuvlfi

rates of short term agricultural loans

2 What factors influence recovery There are a number of possishy

bilities

a) The general social environment and the existence of free

riders a permissive environment will allow people to

default ()n I-leir loans leading to manywho are capabl of repaying willfully refusing to do so we call this

group the free riders

b) The pgterformance of the banks and bank branches Does ban]

or branch inainagcnen t made any difference

c) The choics miic-ade by a rational household willing to rly

the A-i th e oromic factors which inf uenc In

d) 1l tura dli asters and their impract on repayment capacit- P( hIf l- a mnjo impact on recovery

e) V I i I whctl result in no marlet

surplus AIC rural LLr(fers simply too poor to rt

The approach of this paper is to describe each of these fiv

factors and then consider what evidence is available from RBI3US or oth(er sou ( inidicate L e( which would oir mportance Howe vr relevant dat iK d I icl thtain for some factors The PkBIJ

data presented 1 no provids some information on b) and c) n

liMLUed data oni a) d) P)

It is commonplac and in onr view an unsatisfactory simplMI cation to at ti [rfri_nce by the political authoritVLr It in

as the root cause of poor loan recovery Now it certainly may be true that the i ti(-i]polt agivotion around issues of loan recovery

makes things difficult for the banksHowewer the real question is whether given the poitiical environment now extant it is possibl- ti [ rpv Lu lean recovery Whatever the viewpoints of the political authoLities there is considerable scope for action to improve loan recovery Howeverunderstanding should preco

action

The RBBUS data di scussed in this paper was collected from 100 branch banks whic h roprosiit a stratified random sample of tlh approximately 3000 rural branch banks From these banks some 60011 lit term anqri cullural loans were studied these ao-

represen t a proability sample of the short term agricultural loan portfolio of those loans disbursed during the period 1979-80

to 1983-84

Existing data on loan recovery of short term agricultural credit

is preparedlby oadeti Creditin L Bank Aqricul tural DepartmentI

based on returns by the five banks The bank level data is a compilation of Klie data ioiprted by individual branches Proceshydures torcompiliirg this data audit of the returns management

of non-reporting branches and octual branch coverage are a1 poorly defi ed To rmed th isthe B3ACD has been developing a detailed loan recory reporting system this system will soon be providing roports on loan recovery The RFP review of existiUg

reporting and a branch level review of loan ledger formats and procedures resulted grave that it toin doubts was feasible obtain accurate data from t1ic branch reporting of the entire loan universe ProvisLon of a bench mark for the loan recovery position r enle f the important purposes of RBBUS

What does measurinig loan recovery mean As this is not as s-iqp e an issue as it appears at first sight we describe the procediir used in Bangiladc Bank reporting and in RBBUS

1 An individLual liJOrI- Imm igricultural credit loan is dibu sed in kind and in cash

hoei cor2 Tieui i dce ii totality plus charges on a

dite Tlhe charges include the interest (currently 12) anid

a seryice charge (currently 4)

3 After the loan becomes due any unpaid interest or service charge is added to the original principal so that the loan on the books (blance outstanding) becomes larger (ie the unpaid interest is capitalized) Furthermore once a loan is overdue a penalty charge of 6 is added increasing the nominal interest rate to 22 This procedure makes it imposhyssible without a loan-by-loan calculation to identify payshyments made on interest or on principal

4 The usual way to measure the recovery rate for a specified period of time is to compare what should have been r)aid with what has been paid This ratio is in principle easy for the branch to comput-e retrospectively After the portshyfolio is brougLh up to date with interest accruals the total rce(vriF- diii i u the period are determined (R) Next tLhe

Tba [lce e-10I liug oF ry loan which is due prior to -ir end of tl perild is L II ] (1) The recovery ratio iF

then simpl y P P Se 1] as the interest accruals current at Ith t i me oII t reporting this poses no di I iIshyties Tis pr c-dure worlks perfectly for short term agricu]shy

tlra I vre I levor I hi precise procedures used by bnks

- I shy

to define amount due seem not will defined This ratio will be one of tho two measures used in this paper t

[4Y wAI il used if C1ye numuber of loans whcLch I 1K

or partial ly repaid a a percent of the total nu )e ni

loans disbursed T1 is is a good measure of branch perforshymance andin many ways a more useful indicator than the alternative value ratio described above The value ratio is influence0 d by interest rates and is difficult to interpret wvhen loans are several years overdue and inLerest

rates are high

This report describes first a typical rural branch bank This provi-des the reader with a snapshot of the rural branchs finaincial position Of course there is anot single type of branch balk and we have deliberately siinpshylified the complex spectrum into a single representative Next P13B3S results on recovery measurements are descrihLel Finally the factors influencing recovery are analyzed

2 Portrailt ol a ral Brainch Bank In this sectionfor ref-rr a fincc I portlrait of a rural branch bank in Bangladesh is asselfll)lcd fl a1pe r the rural branchs fin inr l I-ii tion ate ted irA 1gtlnice sheet a profit and mont and I ~L()

The profoin bailance sheet for June 30 1985 in summarized in T 1ab P ich m u-a- presented with medians summijri zd ai3 IWI)- l i llS

- 5 -

Table 1

A Typical Branch Bank Balance Sheet June 301985

(Thousand Taka bracketted figure give- percentof total advances in branches for assetspercent

of total deposits for liabilities)

Advances Deposits

Short len Agricultural loasL 4006 (40) Current Accounts 1(137 (19) Medium Tem Agricuturalamp Fishenr [inns 2011 (20) Saving(non-checking) 113 (13) lOflij O]I I I Ii i III11-a Deposits amp fifshr l I I (104) SavJing (cickiiig)Detx ii I31 H I1r (i Total -j-i-i 111 1 1 1-1ns 74 11) (74) Fixed deposits I

Other SiHl T- l1hs 824 ( 8) Other Short Tenmi IXcpn_-it )

Other 11k-diu Itim I ans 1122 (11) DPS -3 9) ( ) Othot I ruTg li n I)Ins 16) ( 7) Other Deposits 193 (4)

I 1o-I inI I jIi IlII I ( i6) 1(JL[ ILcx)sits 5465 (10) )

Grand To I of ilvii ices 1006 I(1()0)

towliij to tR 1 97 (19)

lolal JV-S J]P9t

1 Head O1li((

2 Balamcing itcm

3 [)ejjsitcIio-[iSchmuie

cui~tuid) dviu (nxnposition

Short TeIin 4830 (48)

MkRituu Tcnu 3133 (31)

long Teorm 2098 (21)

1BorromUi frn 110 I

Total Ii abiLities 1214

Ncudnal New Worth 2

- - 51

Mmuoranda Medians

Total Advances 578)

Lending to 110 0

Total assets 5780

Total deposits 329

Borrowing frail 110 277 Total liabilities 607

The balance sheeL indicates that measured by means Lhe typical branch Ii has Ltl idvlarces of 10 mill-ion Taka aniel lends 19 million Taka to its Ilead office It covers thi

with 55 mi i 1ic Tj-ka iii deposits and by borrowing 7 ti I I ii

laka f rom i I llo f ie on June 20 1985 deposits wef-re

50 of adwances the reminder was financed by transfers from t ilt lt (I ()f fice Ayri ctil tural loans amouLnted to 747A f total Loans (i the etiLire portfolio short term loans toQtaI lcd] 1H imdium term 31 and long term 21 However in agrl-i cuLI u slcort term loans were 54 medium term 21

and long term [9 somewhat more short term than for the non-aqrci l I t t A portfo)]io

From the port Felbo colposition we can see that the crediLI share is fairly close to the share of the labor force it

rural areas

Deposits averaged 5L million Taka per branch of which 15t were saving accounts 26 fixed deposits 19 current accounshy

ts and ]0 in various other deposits The sample branches reported a nominal average negative networth of 520 thousand

Taka This should be taken as a measure of the errors in the reported iaLa oiie hi rnihos have a number of other balitli- sheet items not reported in the survey which account foir tHie

difference

The median values are approximately half of the means inidishycating that tlhere are a tiumber of branches which are rather large and skew the statistical distribution

-7-

About half of the br-anch banks do not lend to their ilead

Office )n lr- hasis 11I h means net borrowing from the

head (4t ice is 9H (I(1posits on the basis of tHeitdiem i I

is 84 The iw-in ratii 1Finances 54 of its advances I

deposits i1o median liili 57

In Table 2 tt( fypica l profit and loss statement is r

The data i ci I tci F with current accounting policy so LI ii

income is usually (ove-sLated and there are no bad debt allowshy

ances maintLaiined at tie branch level Both the means and

mindian ar( 11rer income earned 77 accrues from ra rshy

nings (e ]lt)all and 157 from lending to head office Note tLhat

aht)iI lill IIf iaii lies lend to Head Office Other inceiiishy

reprs- - 8i lie total Of total costs 57~illy (A

in tercFee H- to and to offic)(22 depositors 36 head

wlmi II I i e- I cIa ociated administrative costs FiI- IP-r

are 26 (i I arpproximately 80 of the branches ripv I

Positi Vo pl()its

Table 2

A Tical Rural Bank Profit and Loss Statement 1984

(Thousand Taka percent of total income in brackets)

Mean Median

Interest earned from loans 1162 (77A) 734

Inte-est eaoi-d from 110 220 (146) 3

Other income 121 ( 81) 48 Total income 1503 1080

Interest paid to depositors 326 (217) 190

Interest paid to 110 538 (358) 217

Salary costs 147 ( 98) 129

Other costs 105 ( 70) 81

Total cost 1316 (743) 852

Profits 387 (257) 177

- 8 -

The various ratios releviinL t-o atnitig the branch are given in Table 3 Earnings on lodns avei-)p 162 while interest earned from lending to Hlead Wf[ic I 6_1 The average

return was then 146 Ij[ t cosls trk l interest

cost including transfers 1rcin H ave iged 86 Thus the

rural branches had a spread of 67 c Ii HhLt these

estimates do not questiol Cteamp11it 111iij p[Lactice but

reflect the rural finance system as il- Js reported today in

the accounts of he iead ()I ice

Estimated Returns on Assets and iiabilities (1984)

Assets

Interest t d on [2 IC1 Interest paid by lead tIi cu 6 3t

Average earnings 146 3

Interest paid on deposi[ 95 -

Interest )Lild Uo iead 01 ic- 1-

Average cost of funds 86

Other

Ratio of non-interest cost to loans 29

Ratio of profits to total 4sets413

1 Computed from average advances and reported earnings

2 Reported by branches

3 Asset composition of June 30 1985

4 As reported by branches

5 Liability composition on June 30 1985

-9shy

3 Recovery Measured Branchby Accounts

This section describes recovery rates estimated from branch data Tables 4 and 5 prusuiLt the hask- onicata disbursement and recovery In Table 4 we have reported the medians of ttie distributions of branch Values Use of the medians-has the advantage that it protects against some of the c- --eme mnireposhyrting errors by branches Over the five year period 1981-1985 the disbursements as a por-(t21 ofL I onot sHn gs at the beginning of the period lhve incrctnuXI I Fv-iidy pealltjng in 1983-1984 and then dcld i in iliij DisbursumiiL have continued to i I[V Inc-eI J190i L i of single disbursements has iru Lhi icmdaled over this period these increases are esstn il 1Iji tcl eses in input prices corresponding to iniiA]a t i (dIm 7] In real terms the typical short Lvitt agr loain has been consshytant or declining slightiy in size

The recovery ratio computed asis ilit noint recovered to the amount due The amount- due Ji ti1i iniLia] balance outstanshyding plus the interest charges assating tLhat the loans are repaid smoothly durinj the year an it_ ernative definition relates amount due to Vn] ()f the yai- ()tstand ng plus reco-shyveries less disbursements Limes an itltecst rate factor

The recovery rates have lI t a tc(t -Iim 31 in 1)81 and 1982 rising to 39 in 198j3 an ihten dcclini hg o 27 in 1984 and to 21 in 1985 There is li tile diit tht r ecove ry rates i 1986 are low and may I I I1c1I l -rtfrr m the lows o 1985 Repea Li tjg s kui IciiI atl-althe K I 1 t hbrnch means (Table 5) we sc-e essen il Iif 1t 101t1 1a recovery

- 10 -

The recovery ratio using the ul ian is sini lar to the recovery ratio

of the means The two metlic1i o pu Li ii L ( (M Iv01ry ra Li o give a( amp

similar result method 2 being systmatica]l Iv higher than method 1

There is an overall consistency in this daML indicating an increase in

the recovery rates upto 1983 followed by a shalrp decline to approximately

20

The size of a loan recovery deflated with an index of disbursement size

has developed as fol loMs

Real mean recovery (ndcex 1985=100) 1981 1982 1983 1984 1985

166 126 131 133 i0

Disbursenents in real terms using the same defLation (disburs(aent size

in Table 4) is as follcwqs

Real disLhisnents (index 1985=100) 1981 1982 1983 1981 1985

48 44 104 13] 100

Following the rapid rise in real terms (ie acreage covered by short

term credit) there was a substanial decl inu in 1985 a furt11her decline

will take place in 1986

Next we describe in Table 6 the distriltio oitf the ratio of recovery

outstanding ratio This indicates that th( c-L 30U of the branches have

very low recovery rates currently averagrwj 1esnq than 10 of the amount

due This effect of a substUantial niouixr (I I (upwt one third)with

very poor loan recovery records suggests tht a pr(opsa targetted at the

branches with such low recovery penrformance vould be tartictularly effective

in raising overall recover-y raTes The (l 1 ir VCV4)- I S ]S Seeni(t

in the deterioration of the median and 3C1i IWth 51-h fictiles ccawupred

by branch many branches havinj rlLainud st is factory recovery rates while

others deteriorated Tiie dewroration ot rc(2Jer rates has not been

uniform across the sample The icovery xceedi ng 100 result fraii1tt

a ccmbination of mi srerxrti j rt( c-ry oi I I t( - al oCC01iotstandi ng

canbined with loans less than one lear eg i I loans are for three months

and fully repaid then the roti recoveries 1-o the balance outstanding

would be Meurtlietimi ng (d LCOVe)fi s iii y reducealmost 500 [ne

the balance outstanding on the rcpiorting ct

- 11 shy

Tab]e 4

Typical Disbursement and Recovery Ratios for Short Tr Aqji- II_ [on ( Pcrcent)

(Branch m diitiws)

m _ _

1981 1982 1983 1984 1985

Disbursementoutstanding 50 54Th 119 93 25

Disbursement size (Taka) 1500 21() 2400 2700 3260

Recoverydue 1 315 307 39 269 21

Recovery size (Taka) 1913 203h 2420 2760 2500

I Method 1 for dues Due Outsl-andii kiLtcirc-sL vatl-e factor

Notes The value of Lhe vaL-iI-L is coiiputcd to - alL sampled branch the medians ar c-por-Led ij Lh1Js Labl e

Tolk-te 5

Disbursements and 1ecovurit is of Short Term Agricultural Lii- Branch lMeans

(Thou s n il Pla k a

981 1982 1983 1984 1989

Outstandings 1 606 750 1014 1874 3560

Disbursements 366 467 1260 1789 1650

Recoveries 272 26] 499 614 824

Disbursementsoutstandings 60 62 327 95 46

RecoveriesDue Method 1 39 305 43 275 195

Method 2 429 335 48 27 na

1 Start of year

Method 1 Duet = Outstandings tIiLerest rate factor

Method 2 Duet = Out tandingst+1 + Recoveriest- Disbursements

Interest rate factor

- 12 -

Table 6

Distribution of RecoveryOutstanding Ratio

(Percentage)

Fractile 1981 1982 1983 1984 l95

95 325 09 503 267 265

90 180 102 200 134 148

70 58 47 H7 44 53

50 36 35 45 32 25

30 19 22 29 20 13

10 8 11 14 3 4

5 6 8 3 2 2

4 Loan Recovery Measured from ndividual Loan Records

This section reports the results of analysis of 6000 plus

loans The ratio of the balance outst-anding at the time of

data collection to the loan principal was computed for each

loan We call this the nominal ratio Another ratio was compushy

ted deflating both the t tiltsiii iny and the original

principal to a common base year We call this the reel ratio

The short ter-m agriculLnii ln f)] i nLitutes sameI [)it

40 of the value of loans (usLutandi ng (se Table 1) The

distribution of loan sizes is given in Table 7

The nominal ratio takes on values mqing Iii zero Lo arbitrarily large

number When t h lan is reazid has been removedthe ratio is ZEfl-C) k fullV and

from the branch ix)rtfoio Ii up interest paynentsWhnriii rreiqc 1pt

and other charges then the noninal ratio is )nc_ wlict lieLio is less than

one some progress has been made in loan re(overy Finally whie the raLio is

greater than one then even the intf-rst paqueILs are not beirg met(ne

real ratio includes whatever recovery has been obtained through inflation

1

Ta b I e 7

DisLribution of Loan Size of Short ______erm A r iP(- I uir it Lodns shy

(Percentage of Loans D)IiLti1Lud JuJy 1978 - June 1985)

Class interval (Taka) Nomina] Real (1985 prices)

0 - 1000 32 15

1000 - 2000 36 32

2000 - 3000 16 27

3000 - 4000 10 11

4000 - 6000 4 12

6000 - 8000 1 2

8000 - 10000 0 1

10000 - 15000 0 1

Mean loan size(Taka) 1720 2570

The distribution of loan size indicates very clearly the type

of loans with which we are dealing There are no short term

agricultural loans greater than 1000() Ika in nominal terms

85 of the loans are less than 3000 TlVt in 19811 prices 8

are less than 4000 TPaka One is de -1inq with very small lrans

and collection effort per lo n could nver be very large

Using the direct data reported by B olies for 1984 and 1985

we find rather Ia-rger means (3400 Paand 3450 Taka respeshy

ctively) and medians(2700 Taka and Tka) There has been

onsiderable increase in the individual loan siz in nominal

terms over the period (1979-1985)

- 14 shy

The loan recovery measurement is summarized in Vabe 8 following

Ta b I e 8

Loan Recovery NlMea_sire-e (PercentL ()I foans)

Value of Ratio Normal a io Real Ratio

0 1 49 49 0- 4 2 3

4- 8 3 4

8 - 10 4 13 10 - 15 30 27 15 - 20 9 3 20 + 3 1

Repaid 49 49 Principal reduced 9 20 Total improved 58 69 Principal not reduced 42 31

1 Loan fully recovered

- 15 -

The nominal loan recovery ratio indicates that 49 of the

loans disbursed were fully recovered All of the loans were

due prior to the period of data coli clici Ano l ietr 9 of the loans had a balance otHt ldiilj in- thlan tir origina]

principal and hence should somu progrss towards recovery

However the remaining 42 haid a iInine oLtstanding greater than the Lgina1 princili l i Liatti interestor o payments

were not beiny met

When denominated in real terms we fIind Lhat 20 of the loans

had a balance outstanding less than original principal This

reflects the impact of intli ion ini dLi tile debt burden

felt by the borrower

We next examine the recoviy rate and the year of disburseshyment These results are prusented in ihle 9

Tahlu) 9 ]

Year of Disbursene and li Recovery 4

(Percentage ofi columioLotis)

(I j so( L Value of nominal ratio 79 80 81 82 83 84

0 66 70 63 43 28--

0- 4 2 Ii 0 2 5

4- 8 0 2 ] 3 4 4

8 shy 10 1 1 2 2 3 13

10 - 15 5 5 5 18 11 50

15 - 20 8 15 19 13 5 1

20 + 17 6 9 1 0 0

Repaid 66 70 63 63 43 28

Principal reduced 3 3 5 5 8 21

Total improved 69 73 68 68 51 49

Principal not reduced 31 27 32 32 49 51

- 16 -

Table 9 reports that loan recovery (fully repaid) measured

by the number of loans begins with 28 repaid in the first

year after disbursementrising to 43 in the second year 63 in the third year and then approaching 65-70 over the next two years The number of loans which show a reduced

principal ie interest charges are paid and some progress has been made in recovering principal begins at 21 one

year after disbursement and decreases to 3 after five years

Lhe number of loans for which there is no progress on prinshy

cipal repayment decreases from 51 one year after disbursement

towards 30 after 5 years

Examining the relationship between the recovery ratio and the

year of disburseient a numoer of conclusions are apparent

1) The recovery rate reachus 70 Hi i 11eis not

repaid

2) The loan portfolio car be separated into three categories

a) Repaid b) Repayment- underway or potential1y repayable

c) Non-recoverable We can simplit tLhu data in Table 9

as follows to indicate the four year pattern

Percent of loansyciLeqv

Year after isbn iInt~nt

1 2 3 4

Repaid

Potentially repa

Non-recoverable

id

30

70)

0

45

50

5

65

20

15

70

0

30

This suggests that 2 and 3 ifte-r di sbuirsment

are the critical times when many loa ns become non-recoshy

verab]e In year 2 two Lhirds )i Hie iiddle category

are repai-d one tiiI de non-i hivurjblein year 3

only 25 of the middle category are recovered 75 become

non-recoverable

- 17shy

3) Loans divide into two c(joups IiW)sc which are nver going to be repaid and those that- are If we subtract

out the 30 that are never repaid then we see the recoshy

very pattern as ()fl i

Recoverypatt ii for loim hil-i iro repaid

h-dr after d i sluruemenL I2 3 41

Repaid 43 64 93 100

In process of repayment 51 366 I 0

5 Factors Influencing Loan Recovery

This section presents data and analysis on the factors which

influence loan recovery The entire subject of loan recovery

is a very difficult one to investigate for there are strong opinions but limited facts This sectiot reviews five factors

which potentially influence loan recovery

51 The general souial C1avJronment There is widespread

informal expression of the vitw that the social and

political environment influences the rate of loan recoshy

very While thJ7 is a common--onse observation there is

no real evidence t support it A number of remarks are

of relevance

a) Different banks and branches how very different

loan recovery rates The vriations among branches

are very large () Iiht th l i i ulffect must be quite dii t1iriit I i (ltn( ld[ict2 [o anoth r

or it must be quiti weak

- 18 shy

b) There have been considerable variations in the

annual recovery rates (see Tables 4 and 5) Thure

is no obvious correlation of these rates with the

changes in the poiliLica] cvironmnnt

c) The immediate correlation that strikes one from

Table 4 is between the disb iirementoutstandings

ratio grd the recoverieshu Li Thete are only

five observation of this macrn le(vel data a but a

close relationship is suggested One would have

thought that politica] con( wit 1otildhe nianifest in a high growth of dit i sbursem rl Iltw-v1r he eidenice

is ambiguous A hicgh growth raLe in disbursements is

accompained by higher recvcry rates A large absoshy

lute volume of disinursement i accompained by lower

recovery rates

It appears from thesu iildicators that there is little

empirical suLtport tot the contention that changes in the

recovery level are int lmniuced by lI poli]tical environshy

ment However the a()s-I e 1t 1 t-ecove -y may will

be ifluenced by t he p i tica I lv i -onment Tho level of

70 recovery of a ortlroflio dishursed four years preshy

viously is not a very sct-isfacto y recovery rate (no

viable rural finance sfem ci Iki iL on this level of

recovery) The fai li 1 ra i Ili( -c(overy rate above

this 71 level may lt JiL ted withi i prolonged unshy

willingness of the soci-tt sys Wi- ccI Ictl more loans

This may also reflect a iiuitber of persons simply unable

to repair due to natural calamities What is evident is

thlt there is nio evidence which indicates a relationshy

ship between political and social otA i ttdes and short term

changes in rocovery rate3 Thu (ne should not look to a

stiffer political stance even as anecessa y much less

sufficient condition fo i imptrovinq rtovery rates from

say 20 to 40 of the amount due

- 19shy

52 Performance of banks i [id rc T aie signifishy

cant differences in loan recovury performance of differshy

ent branches and different banks Table 6 above indicated

the wide dispersion in Lhe ratio of recovery to outstanshy

dings a proxy for the recovery rate Table 10 gives the

distribution of mean recovery ratio for the branches

and also annual esLiuates Tie resulL is striking

loan recovery differs greatly from one branch to another

Table ]] presents the mean recovery rates by ban This

provides both the mean of branch means (unweighted) and

the recovery rate for the bank Again we see a considershy

able variation from one bank to inother

Turning to the individual lotns those are cross classishy

fied against a number of branch related variables in

Tables 12 13 14 15 16

i) Table Le records tLhe recovcry rates of banks This

indicates as does Tlb] e 1 taiti thvi-e ir signifishy

cant differLnces ii i- j ii It is t-1h existence

of such differences tLhat illdicates action is

possible to improve 1onn ivey

ii) Next we examine ba-ink si ze ii1 i rltnvery (Tab]e 13)

The RBBUS data shows that lhii i overy declines

with size of branch Sinall Iiiilh with total advanshy

ces less than 3million hl a have rccoe ry rates

of the range 65-70( This ii- Jcclines to 50 for

larger branches but incLuaii a fOL larycitddiin the

branches The upturn of the recovery rates for very

large branches is not sLa i a ly1 siqnificant

Although this ainilysis exntimesiWiiis I (lLt vari able

(branch size) it is highly suggestive of the conshyclusion that rwov ry will dec1 i iewith branch

- 20 -

Table 10

Distribution of Mean Recovery Ratios for Short Term Agricultural Loans

(Percent)

Fractile 81 82 83 84 85 Mean

5 94 113 99 71 85 92

10 64 71 79 43 44 60

30 39 33 41] 28 33 34

50 22 27 30 22 16 23

70 11 17 21 14 7 14

90 3 9 [0 2 2 5

95 0 6 5 1 0 2

Mean 30 33 36 24 22

Recovery Ratio Method 2

- 21 -

Tab] e I 1

Mean Recovery Rates by Bank for Short Term Agricultural] Loans

(Percen L)

Agrani Janata Rupali Sonali NCBs BKB Total

Branch Means

1981 3o9 186 172 I ()0 30()

1982 400 258 52 282 35 24 332

1983 442 267 537 287 346 408 362

1984 238 143 378 2h 8 241 233 239

1985 186 175 504 I7 215 243 222

Mean 315 206 489 2I90 294 291

Bank

1981 280 191 151 715 306 312 307

1982 214 120 265 9 245 259 248

1983 430 260 271 267 293 478 333

1984 280 73 156 241 207 282 232

1985 270 113 236 218 204 214 209

Mean 295 1514 216 268 250 309 266

Recovery Ratio Method 2

- 22 -

Tabl I 2

Nominal Ratio of Shuv-t Term Agr-icultural Cred i t l Iiink

Value of ratio AKa n j JanaLiai Upa Ii Sonali BKB

0 54 43 58 47 48 0- 4 1 1 1 3 3

4- 8 4 1 2 2 3 8 -10 8 6 2 4 2

10 - 15 26 24 26 31 36 15 -20 7 4 8 9 7 20 + 1 10 3 4 1

Repaid 54 43 58 47 48

Principal reduced 13 9 5 9 8

Total improved 67 52 63 56 56

Principal not reduced 33 48 37 441 44

- 23 shy

Table 13

Nominal Ratio of Short 1W nn Agqric ilt r li Credit bI wlc -_zu

(Percent of loans recoveit i by size cawegory)

~ l

Value of Ratio 0-1 1-2 2-1 3-4 4-- 6-8 8-10 10-20 20 +

0 66 59 4I 35 13 47 1 43 47 48

0- A 1 2 3 1 1 2 2 2 2 3

4- 8 4 3 3 3 2 2 3 2 2 2

8 - 10 3 4 5 I0 4 1 5 3 3 6

10 15 22 21 25 28 2( 37 35 38 36 35

15 - 20 4 7 1 15 i IH 9 9 9 5

20 + 1 4 5 8 I1 3 3 3 1 1

M wiW 66 59 48 35 41 i1 43 47 48

Principal reduced 7 9 1) 14 7 5 9 7 7 11

Total improved 73 68 58 19 50 2 53 50 54 59

Principal not reduced 27 32 42 51 50 48 47 50 46 41

Notes 1 Branch size measured by total advances outstanding in

million on June 30 1985

- 24 shy

size This is a reasonable conclusion As branch

operations expand the branch loses regular contact

with its customers and recovery rates decline At the branch level this suggests that the decline in recovery rates nay be a consequence of Lhe rapid

expansion of disbursements

iii) Another po~sible hrwLh chnL [rl i iK the rate

of growth of the ranch in lable 11 wc report tLhu

behavior of the in )nina] r- vhry iratio I)r branches

according to the rateoM growth of outstanding

loans This data i nJ icnIA no Mt a L -l 2hip betwoen

the growth rate and Lhe nominaii i ry ratio

Althogh large branches show poorer recovery than

smaller branchen rapidlv qrowinq hra-ancls do not

seem to be poorer at r Acvn I s I ow qjq br uihes

iv) The branch leia rnts iothi ng trom experience in loan recovery Table 10 sots out the nominal recovery

ratio by he agu oI Lhe 1ran t Altlhough there are

substantial variatiouns tlh r is no trend The older

branches do not improve tlhei- recovery rates

v) Very remote Qanuhrli- liavu pitrer recovery ratios

than do more accussible brinhes However for most branches accsii IiLy ha w influrence on the recoshyvery rate (td1n I )

l]e

Nominal Recovery RaLio i IiorL Term Agricultural Crccl i t n 3ranchBrawth

1) -11

Annua ro wL )wh I u Ot advances ( -25 Lo 0 0-10 ]10--20 20-30 30-40 40-50

Ioans repaid 61 63 33 58 47 49

Principal reduced 5 7 6 5 11 6

Total improved 65 70 38 63 58 55

Principal not reduced 35 30 62 37 42 45

Table 1

Nominal Recovery Ratio of Short Term Agriculural Credit by Age of Branch

(Percentage of loans)

Age of branch inye ars 4 5 6 7 0 q 10 ]0l1t

loans repaid 46 50 37 19 61 62 43 4q

Principal reduced 13 15 12 9 9 8 4 8

Total improved 59 65 49 58 70 70 48 57

Principal not reduced 41 35 51 2 30 30 52 43

- 26 -

Table ]6

Nominal Rucovery Ratio of Shout rl )n Agricultural Credit and Branch Reilotfenss

(Percentage of cases)

Remoteness index

1 2 3 4 5

Repaid 45 41 49 57 28

Principal reduced 8 11 10 7 11

Total improved 53 52 59 64 39

Principal not reduced 47 48 41 36 61

Note 1 is most accessablc 5 za sJhl] is Iccc

- 27 -

The conclusion to be dirawii r r-w 11 a I i L L Lhe ba-1t11

and the make Idi ll xcc hit loweverbranches e-i- Ii rt(cvury

the experience location (rcrmotceess) and growth of tile

bi ch do not infucICe r I ii does which is

strongly suggestive of d i a2ttL)nOl l 1i L 11l cove]7y Pile

major conclusion that o l II mpt banksis aI 1e the and

Lihe branchies f roi resomiailbi Ii Ly le - r ratesr recovery

53 Household conditiorIn I 111 11112 thi rd major aspeshy

ct of loani rucovery _ lI il I i iitI -I LI Iiw-laoid towards

repayi-i - IH th ii (ii I I WI_ I J I w ith L e

household that helI eve I t111 iilil i j-Piii uit throshy

ugh influence Instl ead wV c coi h iL LI aLc tiona]

farmer who faces the Itsi i I a orr to deferw

payment to thc future Pio j a iaaie aind we do

not examiie in this Vijw t Lii 1oan recovery A

numihrr of qtuestiors (i I in

i) One would expect recovery to I lavese]y related to the

availability of fresh credit Tie rrmer faced with unshy

certainly over availaIn lity ir Lrsi cr dit from the

banking system may preler tu defer repaymuiit the altershy

natives are no credilt or paying ligqi iiiI evest rates to

the informal sector versus a 22s banlk rate including the

penalty charge So long as the expected return from using

short term credit is gea ter l] ii 22[ but ting off repayshy

ment- would be the pic Feurred appi-oacl The data from the

branches supports the contenti on Llhat repayment is better

when loan sanctioiiinj is XpiniI g

ii) Another aspect of households aLti liide towards recovery

is the real interest rate The ic2a] iliterest rates for

the short term agiicultitira loans -r j i iii iihle16 The median

real interest rate is 107 Thi s is i le a hicih rea rate When the rate

- 28 -

Table 16

Real Interest Rates for Short TermAgricul tural 1ai

Interest rate interval Percent of loans

-50 to -10 11

-10 to 5- 2

- 5 to 0 6

0 to + 5 14

5 to 10 25

10 to 15 19

15 to 20 11

20 to 30 9

More than 30 10

Mean 108 Median 10

is high will the huwuhold LuLd to repay or defer

repayment The high real rates arises from the

decline in rice prices which has the simultaneous effect of raising the pricu inidex and reducing income from surplus rice sales The farmer on the one hand wishs to repay Lhe o oan sInc Lhe interest rate is higher and he pi-efeirs to dter current consumption

for future consumption which is now cheaper (this is the same effect 3 jvi j) ytuL Ills iicome may be

reduced and his ability to repay weak ened Table 17

gives the relationhip CLetUUH interest rates and both the nominal and real rucvery rate Thi- table

indicates that recovery rates declAine wvith riE-ing real raLs for the range -10 to +102 (approximately

half the loans) cind then incrieasu with real interet

rate Using the rel- recovry rilt ows essential ly

the same effect

For borrowers expticu i ng raIl rates less than 10

lowering the intc itae ni ( improve the recovery

rate whereas for the liiqlic ti rates thi recovery

rate would be rudic d

iii) The collateral used for short term agricultural credit has no impact- o ic i t tyili (i le If)

The conclusion of this brief JCrLipt ion Of household

response is that thert Js good _vikluiice tihat interest rates and the avaiIabii ty of l i 1()Li1s in luence the

willingnens to repay [Iowever late-al requirementsra have no influence Phis is no i ii i-iu ltis collateral

requirements are noi~inal and have no significance in the

recovery processr

- 3o -

Loan Recov-yrmand Ii l Ini s

(Percunt L)I loais)

-50 to -10 Lo -5 Lo 0 Lo UL 10 Lo 15 to 20 tc 30+ -10 - 5 C) 5- 1 15 20 30

Nominal

Repaid 55 77 70 51 35 17 51 58 62

hliincipal reduced 6 13 l1 7 9 9 12 8 6

IbLal improved 61 90 81 58 44 56 63 66 68

Ili icikil noL i-tducud 39 0 19 42 56 44 37 34 32

FRia 1

Repaid 55 77 70 51 35 47 51 58 62

Pri ncipal reduced 21 18 19 21 28 20 22 17 6 IYAdI improved 76 95 89 74 oi 67 73 75 68

Principal not reduced 24 5 11 16 T 33 27 25 32

- 31 -

Table 18

Nominal Recovery Ratio for Short Term Agricultural Loans and the Collateral Ratio

0-1

(ol 1ater-I Lit K

1-2 2-3 3-4 4-5 5-6 6-8 8-10 12 2 +

Repaid

Principal reduced

Total improved

Principal not reduced bull

40

11

51

49

36

8

44

56

35

10

45

55

43

9

52

48

16

10

56

44

46

12

58

42

57

7

64

36

63

5

68

32

46

0

46

54

31

8

39

61

1 Ratio of collateral to princilvd

5 4 Natural disasters and Lxi n rIc(( yf The branch data

from RBI3JS do H(t it )vidle any _iifo rilmiLion wiLh regard to

naturil disa r- i1i is liIt) I t)wve f Lhat natural

disasters are an im(F t L-ailt in tih management of

rural ci-li L in 1n [ 11 ii lC)51 of rice

acreage i gi l i i t il- iiti an occashyijt)L Iflhi

ssionl year greater thain 5 - nuh e Lect approxishy

mately 5A of the 1 i1w di sbn 1 a 4a r would on the

average b iiur|-rLt v jt i n L1ni-Il disasters

This is a suffi ci itl l-i iigtitlL tiLt lltlnce variashy

tions ldly lhave ai ]u is i ii I (-ii I I _ry Furthershy

more if these loans arer not pturq(d from the financial

systerm then the vali xmn blti 1 Iili) i ntou a considerable

amount as they are mliijliiwud (n Lhc books At present

no one has any relialie esLima te a1( ut the volume of

such loans in the short Lerm i i tI lios

5 5 Poverty and loan recovery The issue of poverty and

loan recovery is widely di scussed in Bangladesh This is

a particularly comp]2x problem as Lrut-h is very illusive rio repay any loan there must ho a surplus available for

sal [or the rural liousuhold tlhe usual argument is

to consider that there is a reasonably well defined

minimum level of consumpt ion Ill(e maximAm available

surplus is then production less this niiimum If the

extension of a loan resulLs -in iner--ased production but

the surplus availabl- tr t alt iiiiimui r(quirements

are met is not sufficient then thC ( ULnieII is thr

loan cannot be fully i Vid Ii i i available

then presunably mJiitilmt iictI li L L ( )(hLth W St

the availability of Lit 1oan1 WIII(i provide an increment

in producti on suI-i(ii I 1 [Fti- II 1l14 l) The household

with less the 1 Laij ti_I I in longthan I red 11li a

run decline in hea L and prod u L i wc cipac i L LThe evishy

dence on systemic de Lu i c)a Li oi I C i I ii Hiia ad eshi

health and nutritional sLaLus i (l ) ire not clear Cut

- 33 -

The one piece of evidun~ ziri si I iii l1 l i- that

small borrowers are not v I (i yAys t1101 ntLje borrshy

owes (all within the con xf of tlwu smalI short term

loans under discussioni) Table P) suLs out the repayment reccrd by loan size cot(gqory T mA 1 luns have a

better recovery rate l ini the 1 ij

The effect is not ]argc Lu iL is coinclusive that

smaller loan do not lu v a Jo( ru rrCOverY rite Most

of the loans are less ihuin 20011i i Ixiciji i of to a

common base year for the value i ci ani using tlhe real loan recovery ra[ti+ does no clha ge the conlusion

6 Conclusions

The preiminary nterpr(t it of the MiIl IS evidence on short term agricuLtural i i -covevy I uic+ls to the following

colic I uS i ou s

I) Some 70 of loans are riovered wi thiii three years of cofling duo- lIi s lt- l i- () +l Lohan

previousiy supposed

2) Recovery rates rose iiom 1981 t- 19HI ciiiJ then declined

In 1985 recoveiu-s wU 20 of Ow miount duu

3) The imporLanL I o th I inu probably

the reduction in sanctioning and thlu i icreas in real interest rate both fatois Iclj iij 1() borrowers buing

less likely to repay 11oviuvor thu decline ini disbursements

is probably most important

most iiiare

4) Branch banks and banks have very diferent recovery rates

large branches have poorer recovery rates than small branctes Greater efforts by banks and branches can improve

recovery rates

- 34 -

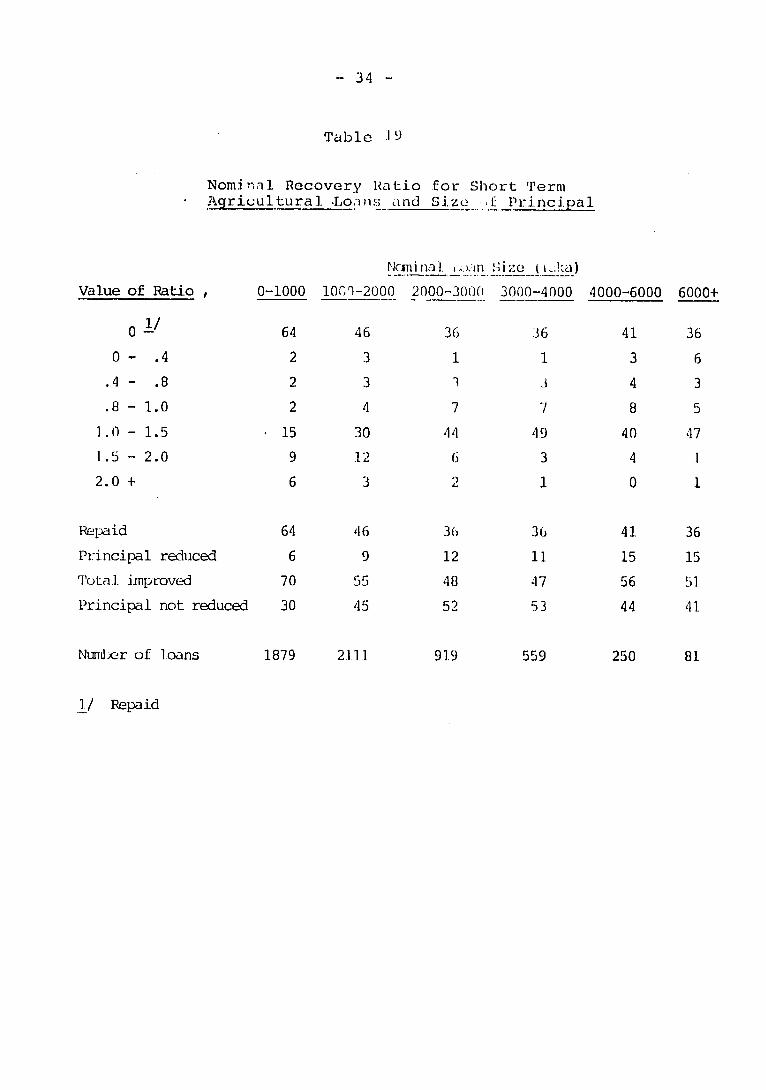

Table

Nominal Recovery Ratio for Short Perm Agriuultural Loins and Size f Principal

Value of Ratio

0 1

0- 4

4 8

8 -10

10 - 15

15 -20

20+

Repaid

Principal reduced

Total inproved

Principal not reduced

Nuiber of loans

J Repaid

0-1000

64

2

2

2

15

9

6

64

6

70

30

1879

NCmlina] ampin Size a

10r-2000 2000-3000 3000-4000 4000-6000 6000+

46 36 36 41 36

3 1 1 3 6

3 1 3 4 3

4 7 7 8 5

30 44 49 40 47

12 6 3 4 I

3 2 1 0 1

16 36 36 41 36

9 12 11 15 15

55 48 17 56 5]

45 52 53 44 41

2111 919 559 250 81

- 35 shy

5) Poverty and natural disnt-ers are significant factors

in rural Bangladesh It is not likely that either is responsible for the I)c)c-r loan rt r ery record

6) Although the social ad politicul ti vi ronment presently makes loan recovery rateo-s more di ti cult -here is no evidence that the loan raccovery t(s cire deteriorating

due to the politicilizLi i (f [ H ition The theme of

interf ronc by (AL IfI i i I I tI ()1 loction is nothing new in BanglacdL--ili

7) This paper has not addressed tLlit tiiestion of what to do

to improve loan recovery However some of the answers

follow directly from the analysis

a) The responsibility Cor recovery should rest squarely

with the banks It should itot be blamed on the

Government nature poverty etc

b) Collection of loans means greater resource inputs

Loth fiscal incentives anid manpower by the banks

More staff at the regional and branch level more

time in Lntact with the banks customers and a

greater commitment of bLaff to work in rural areas

Banks find all of these Lhings difficult Ivore

resources add to cocts but under present accounting

policy do not change revenues Programs requiring

g Late- resource Iup ts ret It i ri -wi l ok profits UltinmateJl -u u l o

requires a lot of by )raich f Athi ank sLa

present they sue lit tle reoao to make such effort

- 36 shy

c) Reduction of loan -vanctions as a stick to drive branch banks and hanks to ct_cover is self defeating Lower disbursement rates ](e I) more borrower resistance even i f branch sLafl would respond to

such a stick

d) Interest rates need to be miiiLtincid potsitive in real tu s for good economic management To improve recoshy

very rates from pruiunL level s reIuires either higher rates or lower rates The current meca real interest

rate is at the Iiinimum of tie relationship between

recovery and real rtLes ITn Wrest rate policy is

very complex and pLrhaps beyond prope- management

Interest rates ar- n L un pieW Uven for the same

nominal terms but arut very dependent upon the partishy

cular circumstances of the loan

Table of Contents

Introduction 1

Portrait of- a Rural Branch Bank 4

Recovery Mt-asured by Branch Accounts 9

Loan Recovery Measured from Individual Loan Records 12

e tcI Iil IIIP ne I nq I oa n Recovery 17

Table List

Table 1 A Typica] Branch Bank Balance Sheet June 30 1985

2 A T vpi a I PuRra1 Bank Profit and Loss S I-almunt ]98o4

3 Estimated Returns on Assets and Liabilities 1984 8

4 Typical Disbursement and Recovery Ratios of Short Term Agricultural Loans 11

5 Disbursements and Recoveries of Short Term Agricultunral Loans Branch Means I1

6 Distribution of RecoveryOutstanding Ratio 12

7 Distribution of Loan Size of Short Term Ag riculLura[ loans ]

8 Loan Recovery Measures 14 9 Year of Disbursement and Loan Recovery 15

10 Distribution of Mean Recovery Ratios for 20 Short Term Agricultural Loans

11 Mean Recovery Rates by Bank for Short Term 21 Agricu]tural1 Loans

12 Nominal Ratio of Short Term Agricultural Credit by Bank 22

13 Nominal Rna ioof Short Term Agricultural c-ilIi y Prdaich Size 23

14 tWminal Recovery Ratio of Short Term AqricItu1 lr wr-it by Growth of Branch 253

15 N Iin I i tPtio of Short Termi Ag ii-tura l Cred it by Age of Branch

16 tmiI fmcovery Ratio of Short Term Aiiltural Crudit and Branch Remoteness 26

17 loan Recovery iI Interest Rates 30

18 P Patio for Short Term A rilturl IW s and the Collateral Ratio 3I

19 Nominol PcoveVr Ratio for Short Term Ac~r ltu-al QIuns and Size nf Principal 3

Accronyms

ACD AclriculiuvilVredit Department

BB ) )gL ~ l l a~

DPS l)|posi t PCnsion Scheme

110 ll(ad OfF ic -)fa bank

RBBUS NiiiralBk ind Bank User Survey

RFP RuLral Fiiace Project

Pecovery ofrm Agricultural Loans

1 Introduction Phit- paper pres(ents results from a survey uljl

taken as part I tLhe Rural Finance Project(RFP) of the Bangl ad(l

Bank financed by the Unitod States Agency for International

Development WitIin1 Hie ork program of the RFP the Rural

and Bnk ULsers ~livet (PBlII was udertaken to provide a detailed s of ctiri-e if l - il-inq wi th a number of issues of importanc ill

rural finance

Perhaps tHn meodv i mportant issue currently under discussion w ih

respect to ru-il ijiance is that of loan recovery There are two quesLi o s tliil r((l 1-o 1) addressed

1 What is the recovery rate of agricultural loans This fun lshyV (10 ii i I y to answer from available Lll

tiia plalje r detai Led evidence will be presented on recuvlfi

rates of short term agricultural loans

2 What factors influence recovery There are a number of possishy

bilities

a) The general social environment and the existence of free

riders a permissive environment will allow people to

default ()n I-leir loans leading to manywho are capabl of repaying willfully refusing to do so we call this

group the free riders

b) The pgterformance of the banks and bank branches Does ban]

or branch inainagcnen t made any difference

c) The choics miic-ade by a rational household willing to rly

the A-i th e oromic factors which inf uenc In

d) 1l tura dli asters and their impract on repayment capacit- P( hIf l- a mnjo impact on recovery

e) V I i I whctl result in no marlet

surplus AIC rural LLr(fers simply too poor to rt

The approach of this paper is to describe each of these fiv

factors and then consider what evidence is available from RBI3US or oth(er sou ( inidicate L e( which would oir mportance Howe vr relevant dat iK d I icl thtain for some factors The PkBIJ

data presented 1 no provids some information on b) and c) n

liMLUed data oni a) d) P)

It is commonplac and in onr view an unsatisfactory simplMI cation to at ti [rfri_nce by the political authoritVLr It in

as the root cause of poor loan recovery Now it certainly may be true that the i ti(-i]polt agivotion around issues of loan recovery

makes things difficult for the banksHowewer the real question is whether given the poitiical environment now extant it is possibl- ti [ rpv Lu lean recovery Whatever the viewpoints of the political authoLities there is considerable scope for action to improve loan recovery Howeverunderstanding should preco

action

The RBBUS data di scussed in this paper was collected from 100 branch banks whic h roprosiit a stratified random sample of tlh approximately 3000 rural branch banks From these banks some 60011 lit term anqri cullural loans were studied these ao-

represen t a proability sample of the short term agricultural loan portfolio of those loans disbursed during the period 1979-80

to 1983-84

Existing data on loan recovery of short term agricultural credit

is preparedlby oadeti Creditin L Bank Aqricul tural DepartmentI

based on returns by the five banks The bank level data is a compilation of Klie data ioiprted by individual branches Proceshydures torcompiliirg this data audit of the returns management

of non-reporting branches and octual branch coverage are a1 poorly defi ed To rmed th isthe B3ACD has been developing a detailed loan recory reporting system this system will soon be providing roports on loan recovery The RFP review of existiUg

reporting and a branch level review of loan ledger formats and procedures resulted grave that it toin doubts was feasible obtain accurate data from t1ic branch reporting of the entire loan universe ProvisLon of a bench mark for the loan recovery position r enle f the important purposes of RBBUS

What does measurinig loan recovery mean As this is not as s-iqp e an issue as it appears at first sight we describe the procediir used in Bangiladc Bank reporting and in RBBUS

1 An individLual liJOrI- Imm igricultural credit loan is dibu sed in kind and in cash

hoei cor2 Tieui i dce ii totality plus charges on a

dite Tlhe charges include the interest (currently 12) anid

a seryice charge (currently 4)

3 After the loan becomes due any unpaid interest or service charge is added to the original principal so that the loan on the books (blance outstanding) becomes larger (ie the unpaid interest is capitalized) Furthermore once a loan is overdue a penalty charge of 6 is added increasing the nominal interest rate to 22 This procedure makes it imposhyssible without a loan-by-loan calculation to identify payshyments made on interest or on principal

4 The usual way to measure the recovery rate for a specified period of time is to compare what should have been r)aid with what has been paid This ratio is in principle easy for the branch to comput-e retrospectively After the portshyfolio is brougLh up to date with interest accruals the total rce(vriF- diii i u the period are determined (R) Next tLhe

Tba [lce e-10I liug oF ry loan which is due prior to -ir end of tl perild is L II ] (1) The recovery ratio iF

then simpl y P P Se 1] as the interest accruals current at Ith t i me oII t reporting this poses no di I iIshyties Tis pr c-dure worlks perfectly for short term agricu]shy

tlra I vre I levor I hi precise procedures used by bnks

- I shy

to define amount due seem not will defined This ratio will be one of tho two measures used in this paper t

[4Y wAI il used if C1ye numuber of loans whcLch I 1K

or partial ly repaid a a percent of the total nu )e ni

loans disbursed T1 is is a good measure of branch perforshymance andin many ways a more useful indicator than the alternative value ratio described above The value ratio is influence0 d by interest rates and is difficult to interpret wvhen loans are several years overdue and inLerest

rates are high

This report describes first a typical rural branch bank This provi-des the reader with a snapshot of the rural branchs finaincial position Of course there is anot single type of branch balk and we have deliberately siinpshylified the complex spectrum into a single representative Next P13B3S results on recovery measurements are descrihLel Finally the factors influencing recovery are analyzed

2 Portrailt ol a ral Brainch Bank In this sectionfor ref-rr a fincc I portlrait of a rural branch bank in Bangladesh is asselfll)lcd fl a1pe r the rural branchs fin inr l I-ii tion ate ted irA 1gtlnice sheet a profit and mont and I ~L()

The profoin bailance sheet for June 30 1985 in summarized in T 1ab P ich m u-a- presented with medians summijri zd ai3 IWI)- l i llS

- 5 -

Table 1

A Typical Branch Bank Balance Sheet June 301985

(Thousand Taka bracketted figure give- percentof total advances in branches for assetspercent

of total deposits for liabilities)

Advances Deposits

Short len Agricultural loasL 4006 (40) Current Accounts 1(137 (19) Medium Tem Agricuturalamp Fishenr [inns 2011 (20) Saving(non-checking) 113 (13) lOflij O]I I I Ii i III11-a Deposits amp fifshr l I I (104) SavJing (cickiiig)Detx ii I31 H I1r (i Total -j-i-i 111 1 1 1-1ns 74 11) (74) Fixed deposits I

Other SiHl T- l1hs 824 ( 8) Other Short Tenmi IXcpn_-it )

Other 11k-diu Itim I ans 1122 (11) DPS -3 9) ( ) Othot I ruTg li n I)Ins 16) ( 7) Other Deposits 193 (4)

I 1o-I inI I jIi IlII I ( i6) 1(JL[ ILcx)sits 5465 (10) )

Grand To I of ilvii ices 1006 I(1()0)

towliij to tR 1 97 (19)

lolal JV-S J]P9t

1 Head O1li((

2 Balamcing itcm

3 [)ejjsitcIio-[iSchmuie

cui~tuid) dviu (nxnposition

Short TeIin 4830 (48)

MkRituu Tcnu 3133 (31)

long Teorm 2098 (21)

1BorromUi frn 110 I

Total Ii abiLities 1214

Ncudnal New Worth 2

- - 51

Mmuoranda Medians

Total Advances 578)

Lending to 110 0

Total assets 5780

Total deposits 329

Borrowing frail 110 277 Total liabilities 607

The balance sheeL indicates that measured by means Lhe typical branch Ii has Ltl idvlarces of 10 mill-ion Taka aniel lends 19 million Taka to its Ilead office It covers thi

with 55 mi i 1ic Tj-ka iii deposits and by borrowing 7 ti I I ii

laka f rom i I llo f ie on June 20 1985 deposits wef-re

50 of adwances the reminder was financed by transfers from t ilt lt (I ()f fice Ayri ctil tural loans amouLnted to 747A f total Loans (i the etiLire portfolio short term loans toQtaI lcd] 1H imdium term 31 and long term 21 However in agrl-i cuLI u slcort term loans were 54 medium term 21

and long term [9 somewhat more short term than for the non-aqrci l I t t A portfo)]io

From the port Felbo colposition we can see that the crediLI share is fairly close to the share of the labor force it

rural areas

Deposits averaged 5L million Taka per branch of which 15t were saving accounts 26 fixed deposits 19 current accounshy

ts and ]0 in various other deposits The sample branches reported a nominal average negative networth of 520 thousand

Taka This should be taken as a measure of the errors in the reported iaLa oiie hi rnihos have a number of other balitli- sheet items not reported in the survey which account foir tHie

difference

The median values are approximately half of the means inidishycating that tlhere are a tiumber of branches which are rather large and skew the statistical distribution

-7-

About half of the br-anch banks do not lend to their ilead

Office )n lr- hasis 11I h means net borrowing from the

head (4t ice is 9H (I(1posits on the basis of tHeitdiem i I

is 84 The iw-in ratii 1Finances 54 of its advances I

deposits i1o median liili 57

In Table 2 tt( fypica l profit and loss statement is r

The data i ci I tci F with current accounting policy so LI ii

income is usually (ove-sLated and there are no bad debt allowshy

ances maintLaiined at tie branch level Both the means and

mindian ar( 11rer income earned 77 accrues from ra rshy

nings (e ]lt)all and 157 from lending to head office Note tLhat

aht)iI lill IIf iaii lies lend to Head Office Other inceiiishy

reprs- - 8i lie total Of total costs 57~illy (A

in tercFee H- to and to offic)(22 depositors 36 head

wlmi II I i e- I cIa ociated administrative costs FiI- IP-r

are 26 (i I arpproximately 80 of the branches ripv I

Positi Vo pl()its

Table 2

A Tical Rural Bank Profit and Loss Statement 1984

(Thousand Taka percent of total income in brackets)

Mean Median

Interest earned from loans 1162 (77A) 734

Inte-est eaoi-d from 110 220 (146) 3

Other income 121 ( 81) 48 Total income 1503 1080

Interest paid to depositors 326 (217) 190

Interest paid to 110 538 (358) 217

Salary costs 147 ( 98) 129

Other costs 105 ( 70) 81

Total cost 1316 (743) 852

Profits 387 (257) 177

- 8 -

The various ratios releviinL t-o atnitig the branch are given in Table 3 Earnings on lodns avei-)p 162 while interest earned from lending to Hlead Wf[ic I 6_1 The average

return was then 146 Ij[ t cosls trk l interest

cost including transfers 1rcin H ave iged 86 Thus the

rural branches had a spread of 67 c Ii HhLt these

estimates do not questiol Cteamp11it 111iij p[Lactice but

reflect the rural finance system as il- Js reported today in

the accounts of he iead ()I ice

Estimated Returns on Assets and iiabilities (1984)

Assets

Interest t d on [2 IC1 Interest paid by lead tIi cu 6 3t

Average earnings 146 3

Interest paid on deposi[ 95 -

Interest )Lild Uo iead 01 ic- 1-

Average cost of funds 86

Other

Ratio of non-interest cost to loans 29

Ratio of profits to total 4sets413

1 Computed from average advances and reported earnings

2 Reported by branches

3 Asset composition of June 30 1985

4 As reported by branches

5 Liability composition on June 30 1985

-9shy

3 Recovery Measured Branchby Accounts

This section describes recovery rates estimated from branch data Tables 4 and 5 prusuiLt the hask- onicata disbursement and recovery In Table 4 we have reported the medians of ttie distributions of branch Values Use of the medians-has the advantage that it protects against some of the c- --eme mnireposhyrting errors by branches Over the five year period 1981-1985 the disbursements as a por-(t21 ofL I onot sHn gs at the beginning of the period lhve incrctnuXI I Fv-iidy pealltjng in 1983-1984 and then dcld i in iliij DisbursumiiL have continued to i I[V Inc-eI J190i L i of single disbursements has iru Lhi icmdaled over this period these increases are esstn il 1Iji tcl eses in input prices corresponding to iniiA]a t i (dIm 7] In real terms the typical short Lvitt agr loain has been consshytant or declining slightiy in size

The recovery ratio computed asis ilit noint recovered to the amount due The amount- due Ji ti1i iniLia] balance outstanshyding plus the interest charges assating tLhat the loans are repaid smoothly durinj the year an it_ ernative definition relates amount due to Vn] ()f the yai- ()tstand ng plus reco-shyveries less disbursements Limes an itltecst rate factor

The recovery rates have lI t a tc(t -Iim 31 in 1)81 and 1982 rising to 39 in 198j3 an ihten dcclini hg o 27 in 1984 and to 21 in 1985 There is li tile diit tht r ecove ry rates i 1986 are low and may I I I1c1I l -rtfrr m the lows o 1985 Repea Li tjg s kui IciiI atl-althe K I 1 t hbrnch means (Table 5) we sc-e essen il Iif 1t 101t1 1a recovery

- 10 -

The recovery ratio using the ul ian is sini lar to the recovery ratio

of the means The two metlic1i o pu Li ii L ( (M Iv01ry ra Li o give a( amp

similar result method 2 being systmatica]l Iv higher than method 1

There is an overall consistency in this daML indicating an increase in

the recovery rates upto 1983 followed by a shalrp decline to approximately

20

The size of a loan recovery deflated with an index of disbursement size

has developed as fol loMs

Real mean recovery (ndcex 1985=100) 1981 1982 1983 1984 1985

166 126 131 133 i0

Disbursenents in real terms using the same defLation (disburs(aent size

in Table 4) is as follcwqs

Real disLhisnents (index 1985=100) 1981 1982 1983 1981 1985

48 44 104 13] 100

Following the rapid rise in real terms (ie acreage covered by short

term credit) there was a substanial decl inu in 1985 a furt11her decline

will take place in 1986

Next we describe in Table 6 the distriltio oitf the ratio of recovery

outstanding ratio This indicates that th( c-L 30U of the branches have

very low recovery rates currently averagrwj 1esnq than 10 of the amount

due This effect of a substUantial niouixr (I I (upwt one third)with

very poor loan recovery records suggests tht a pr(opsa targetted at the

branches with such low recovery penrformance vould be tartictularly effective

in raising overall recover-y raTes The (l 1 ir VCV4)- I S ]S Seeni(t

in the deterioration of the median and 3C1i IWth 51-h fictiles ccawupred

by branch many branches havinj rlLainud st is factory recovery rates while

others deteriorated Tiie dewroration ot rc(2Jer rates has not been

uniform across the sample The icovery xceedi ng 100 result fraii1tt

a ccmbination of mi srerxrti j rt( c-ry oi I I t( - al oCC01iotstandi ng

canbined with loans less than one lear eg i I loans are for three months

and fully repaid then the roti recoveries 1-o the balance outstanding

would be Meurtlietimi ng (d LCOVe)fi s iii y reducealmost 500 [ne

the balance outstanding on the rcpiorting ct

- 11 shy

Tab]e 4

Typical Disbursement and Recovery Ratios for Short Tr Aqji- II_ [on ( Pcrcent)

(Branch m diitiws)

m _ _

1981 1982 1983 1984 1985

Disbursementoutstanding 50 54Th 119 93 25

Disbursement size (Taka) 1500 21() 2400 2700 3260

Recoverydue 1 315 307 39 269 21

Recovery size (Taka) 1913 203h 2420 2760 2500

I Method 1 for dues Due Outsl-andii kiLtcirc-sL vatl-e factor

Notes The value of Lhe vaL-iI-L is coiiputcd to - alL sampled branch the medians ar c-por-Led ij Lh1Js Labl e

Tolk-te 5

Disbursements and 1ecovurit is of Short Term Agricultural Lii- Branch lMeans

(Thou s n il Pla k a

981 1982 1983 1984 1989

Outstandings 1 606 750 1014 1874 3560

Disbursements 366 467 1260 1789 1650

Recoveries 272 26] 499 614 824

Disbursementsoutstandings 60 62 327 95 46

RecoveriesDue Method 1 39 305 43 275 195

Method 2 429 335 48 27 na

1 Start of year

Method 1 Duet = Outstandings tIiLerest rate factor

Method 2 Duet = Out tandingst+1 + Recoveriest- Disbursements

Interest rate factor

- 12 -

Table 6

Distribution of RecoveryOutstanding Ratio

(Percentage)

Fractile 1981 1982 1983 1984 l95

95 325 09 503 267 265

90 180 102 200 134 148

70 58 47 H7 44 53

50 36 35 45 32 25

30 19 22 29 20 13

10 8 11 14 3 4

5 6 8 3 2 2

4 Loan Recovery Measured from ndividual Loan Records

This section reports the results of analysis of 6000 plus

loans The ratio of the balance outst-anding at the time of

data collection to the loan principal was computed for each

loan We call this the nominal ratio Another ratio was compushy

ted deflating both the t tiltsiii iny and the original

principal to a common base year We call this the reel ratio

The short ter-m agriculLnii ln f)] i nLitutes sameI [)it

40 of the value of loans (usLutandi ng (se Table 1) The

distribution of loan sizes is given in Table 7

The nominal ratio takes on values mqing Iii zero Lo arbitrarily large

number When t h lan is reazid has been removedthe ratio is ZEfl-C) k fullV and

from the branch ix)rtfoio Ii up interest paynentsWhnriii rreiqc 1pt

and other charges then the noninal ratio is )nc_ wlict lieLio is less than

one some progress has been made in loan re(overy Finally whie the raLio is

greater than one then even the intf-rst paqueILs are not beirg met(ne

real ratio includes whatever recovery has been obtained through inflation

1

Ta b I e 7

DisLribution of Loan Size of Short ______erm A r iP(- I uir it Lodns shy

(Percentage of Loans D)IiLti1Lud JuJy 1978 - June 1985)

Class interval (Taka) Nomina] Real (1985 prices)

0 - 1000 32 15

1000 - 2000 36 32

2000 - 3000 16 27

3000 - 4000 10 11

4000 - 6000 4 12

6000 - 8000 1 2

8000 - 10000 0 1

10000 - 15000 0 1

Mean loan size(Taka) 1720 2570

The distribution of loan size indicates very clearly the type

of loans with which we are dealing There are no short term

agricultural loans greater than 1000() Ika in nominal terms

85 of the loans are less than 3000 TlVt in 19811 prices 8

are less than 4000 TPaka One is de -1inq with very small lrans

and collection effort per lo n could nver be very large

Using the direct data reported by B olies for 1984 and 1985

we find rather Ia-rger means (3400 Paand 3450 Taka respeshy

ctively) and medians(2700 Taka and Tka) There has been

onsiderable increase in the individual loan siz in nominal

terms over the period (1979-1985)

- 14 shy

The loan recovery measurement is summarized in Vabe 8 following

Ta b I e 8

Loan Recovery NlMea_sire-e (PercentL ()I foans)

Value of Ratio Normal a io Real Ratio

0 1 49 49 0- 4 2 3

4- 8 3 4

8 - 10 4 13 10 - 15 30 27 15 - 20 9 3 20 + 3 1

Repaid 49 49 Principal reduced 9 20 Total improved 58 69 Principal not reduced 42 31

1 Loan fully recovered

- 15 -

The nominal loan recovery ratio indicates that 49 of the

loans disbursed were fully recovered All of the loans were

due prior to the period of data coli clici Ano l ietr 9 of the loans had a balance otHt ldiilj in- thlan tir origina]

principal and hence should somu progrss towards recovery

However the remaining 42 haid a iInine oLtstanding greater than the Lgina1 princili l i Liatti interestor o payments

were not beiny met

When denominated in real terms we fIind Lhat 20 of the loans

had a balance outstanding less than original principal This

reflects the impact of intli ion ini dLi tile debt burden

felt by the borrower

We next examine the recoviy rate and the year of disburseshyment These results are prusented in ihle 9

Tahlu) 9 ]

Year of Disbursene and li Recovery 4

(Percentage ofi columioLotis)

(I j so( L Value of nominal ratio 79 80 81 82 83 84

0 66 70 63 43 28--

0- 4 2 Ii 0 2 5

4- 8 0 2 ] 3 4 4

8 shy 10 1 1 2 2 3 13

10 - 15 5 5 5 18 11 50

15 - 20 8 15 19 13 5 1

20 + 17 6 9 1 0 0

Repaid 66 70 63 63 43 28

Principal reduced 3 3 5 5 8 21

Total improved 69 73 68 68 51 49

Principal not reduced 31 27 32 32 49 51

- 16 -

Table 9 reports that loan recovery (fully repaid) measured

by the number of loans begins with 28 repaid in the first

year after disbursementrising to 43 in the second year 63 in the third year and then approaching 65-70 over the next two years The number of loans which show a reduced

principal ie interest charges are paid and some progress has been made in recovering principal begins at 21 one

year after disbursement and decreases to 3 after five years

Lhe number of loans for which there is no progress on prinshy

cipal repayment decreases from 51 one year after disbursement

towards 30 after 5 years

Examining the relationship between the recovery ratio and the

year of disburseient a numoer of conclusions are apparent

1) The recovery rate reachus 70 Hi i 11eis not

repaid

2) The loan portfolio car be separated into three categories

a) Repaid b) Repayment- underway or potential1y repayable

c) Non-recoverable We can simplit tLhu data in Table 9

as follows to indicate the four year pattern

Percent of loansyciLeqv

Year after isbn iInt~nt

1 2 3 4

Repaid

Potentially repa

Non-recoverable

id

30

70)

0

45

50

5

65

20

15

70

0

30

This suggests that 2 and 3 ifte-r di sbuirsment

are the critical times when many loa ns become non-recoshy

verab]e In year 2 two Lhirds )i Hie iiddle category

are repai-d one tiiI de non-i hivurjblein year 3

only 25 of the middle category are recovered 75 become

non-recoverable

- 17shy

3) Loans divide into two c(joups IiW)sc which are nver going to be repaid and those that- are If we subtract

out the 30 that are never repaid then we see the recoshy

very pattern as ()fl i

Recoverypatt ii for loim hil-i iro repaid

h-dr after d i sluruemenL I2 3 41

Repaid 43 64 93 100

In process of repayment 51 366 I 0

5 Factors Influencing Loan Recovery

This section presents data and analysis on the factors which

influence loan recovery The entire subject of loan recovery

is a very difficult one to investigate for there are strong opinions but limited facts This sectiot reviews five factors

which potentially influence loan recovery

51 The general souial C1avJronment There is widespread

informal expression of the vitw that the social and

political environment influences the rate of loan recoshy

very While thJ7 is a common--onse observation there is

no real evidence t support it A number of remarks are

of relevance

a) Different banks and branches how very different

loan recovery rates The vriations among branches

are very large () Iiht th l i i ulffect must be quite dii t1iriit I i (ltn( ld[ict2 [o anoth r

or it must be quiti weak

- 18 shy

b) There have been considerable variations in the

annual recovery rates (see Tables 4 and 5) Thure

is no obvious correlation of these rates with the

changes in the poiliLica] cvironmnnt

c) The immediate correlation that strikes one from

Table 4 is between the disb iirementoutstandings

ratio grd the recoverieshu Li Thete are only

five observation of this macrn le(vel data a but a

close relationship is suggested One would have

thought that politica] con( wit 1otildhe nianifest in a high growth of dit i sbursem rl Iltw-v1r he eidenice

is ambiguous A hicgh growth raLe in disbursements is

accompained by higher recvcry rates A large absoshy

lute volume of disinursement i accompained by lower

recovery rates

It appears from thesu iildicators that there is little

empirical suLtport tot the contention that changes in the

recovery level are int lmniuced by lI poli]tical environshy

ment However the a()s-I e 1t 1 t-ecove -y may will

be ifluenced by t he p i tica I lv i -onment Tho level of

70 recovery of a ortlroflio dishursed four years preshy

viously is not a very sct-isfacto y recovery rate (no

viable rural finance sfem ci Iki iL on this level of

recovery) The fai li 1 ra i Ili( -c(overy rate above

this 71 level may lt JiL ted withi i prolonged unshy

willingness of the soci-tt sys Wi- ccI Ictl more loans

This may also reflect a iiuitber of persons simply unable

to repair due to natural calamities What is evident is

thlt there is nio evidence which indicates a relationshy

ship between political and social otA i ttdes and short term

changes in rocovery rate3 Thu (ne should not look to a

stiffer political stance even as anecessa y much less

sufficient condition fo i imptrovinq rtovery rates from

say 20 to 40 of the amount due

- 19shy

52 Performance of banks i [id rc T aie signifishy

cant differences in loan recovury performance of differshy

ent branches and different banks Table 6 above indicated

the wide dispersion in Lhe ratio of recovery to outstanshy

dings a proxy for the recovery rate Table 10 gives the

distribution of mean recovery ratio for the branches

and also annual esLiuates Tie resulL is striking

loan recovery differs greatly from one branch to another

Table ]] presents the mean recovery rates by ban This

provides both the mean of branch means (unweighted) and

the recovery rate for the bank Again we see a considershy

able variation from one bank to inother

Turning to the individual lotns those are cross classishy

fied against a number of branch related variables in

Tables 12 13 14 15 16

i) Table Le records tLhe recovcry rates of banks This

indicates as does Tlb] e 1 taiti thvi-e ir signifishy

cant differLnces ii i- j ii It is t-1h existence

of such differences tLhat illdicates action is

possible to improve 1onn ivey

ii) Next we examine ba-ink si ze ii1 i rltnvery (Tab]e 13)

The RBBUS data shows that lhii i overy declines

with size of branch Sinall Iiiilh with total advanshy

ces less than 3million hl a have rccoe ry rates

of the range 65-70( This ii- Jcclines to 50 for

larger branches but incLuaii a fOL larycitddiin the

branches The upturn of the recovery rates for very

large branches is not sLa i a ly1 siqnificant

Although this ainilysis exntimesiWiiis I (lLt vari able

(branch size) it is highly suggestive of the conshyclusion that rwov ry will dec1 i iewith branch

- 20 -

Table 10

Distribution of Mean Recovery Ratios for Short Term Agricultural Loans

(Percent)

Fractile 81 82 83 84 85 Mean

5 94 113 99 71 85 92

10 64 71 79 43 44 60

30 39 33 41] 28 33 34

50 22 27 30 22 16 23

70 11 17 21 14 7 14

90 3 9 [0 2 2 5

95 0 6 5 1 0 2

Mean 30 33 36 24 22

Recovery Ratio Method 2

- 21 -

Tab] e I 1

Mean Recovery Rates by Bank for Short Term Agricultural] Loans

(Percen L)

Agrani Janata Rupali Sonali NCBs BKB Total

Branch Means

1981 3o9 186 172 I ()0 30()

1982 400 258 52 282 35 24 332

1983 442 267 537 287 346 408 362

1984 238 143 378 2h 8 241 233 239

1985 186 175 504 I7 215 243 222

Mean 315 206 489 2I90 294 291

Bank

1981 280 191 151 715 306 312 307

1982 214 120 265 9 245 259 248

1983 430 260 271 267 293 478 333

1984 280 73 156 241 207 282 232

1985 270 113 236 218 204 214 209

Mean 295 1514 216 268 250 309 266

Recovery Ratio Method 2

- 22 -

Tabl I 2

Nominal Ratio of Shuv-t Term Agr-icultural Cred i t l Iiink

Value of ratio AKa n j JanaLiai Upa Ii Sonali BKB

0 54 43 58 47 48 0- 4 1 1 1 3 3

4- 8 4 1 2 2 3 8 -10 8 6 2 4 2

10 - 15 26 24 26 31 36 15 -20 7 4 8 9 7 20 + 1 10 3 4 1

Repaid 54 43 58 47 48

Principal reduced 13 9 5 9 8

Total improved 67 52 63 56 56

Principal not reduced 33 48 37 441 44

- 23 shy

Table 13

Nominal Ratio of Short 1W nn Agqric ilt r li Credit bI wlc -_zu

(Percent of loans recoveit i by size cawegory)

~ l

Value of Ratio 0-1 1-2 2-1 3-4 4-- 6-8 8-10 10-20 20 +

0 66 59 4I 35 13 47 1 43 47 48

0- A 1 2 3 1 1 2 2 2 2 3

4- 8 4 3 3 3 2 2 3 2 2 2

8 - 10 3 4 5 I0 4 1 5 3 3 6

10 15 22 21 25 28 2( 37 35 38 36 35

15 - 20 4 7 1 15 i IH 9 9 9 5