payroll year end reporting: key consideration and...

TRANSCRIPT

Copyright © 2017 ADP, LLC. All rights reserved.

Sushma Tripathi, VP Strategic Advisory Services, ADP

Elena Redlich, VP Strategic Advisory Services, ADP

Payroll Year End Reporting: Key Consideration and Controls

October 13, 2017

Copyright © 2017 ADP, LLC. All rights reserved.2 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Sushma TripathiVP Strategic Advisory Services, ADP, LLC

• Prior to current role, served as Vice President Total Absence Management, ADP; Sr. Vice President of Product

Management, SHPS; Director, Product Development & Management, CIGNA

• 20+ years of experience in leadership, operations and product management; primarily in health and productivity

management, employee benefits administration and wellness outsourcing

• Recognized authority in workforce trends, leaves management, and DOL compliance including FMLA, FLSA, and ADA

• Widely published in outlets including CFO Magazine, SHRM and Employee Benefits News. Frequent speaker at

industry conferences and events

• MBA from Drexel University, Philadelphia, PA

• Prior to current role, worked in operations, consulting and service delivery roles for leading companies such as

General Electric, IBM, E&Y and Accenture

• Worked for 20 years assisting organizations in globally defining opportunities to align HR and payroll initiatives with

overall business strategies

• Created best-in-class methodology to support critical deliverables within the full global HCM and payroll

transformation lifecycle

• Delivered global HCM and payroll workshops for more than 25% of the FORTUNE 500 covering key areas such as

leading practices, market trends, model options and governance frameworks

Elena RedlichVP Strategic Advisory Services, ADP, LLC

Today’s Speakers

Copyright © 2017 ADP, LLC. All rights reserved.3 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Agenda

>HR and Business Challenges

>Compliance Trends and Considerations

>Year End Life-Cycle

>Payroll and Operational Indicators

>Key Considerations

>Next Steps

ADP does not practice law or give legal advice. ADP strongly recommends

that clients obtain qualified legal counsel prior to making any decisions.

4 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

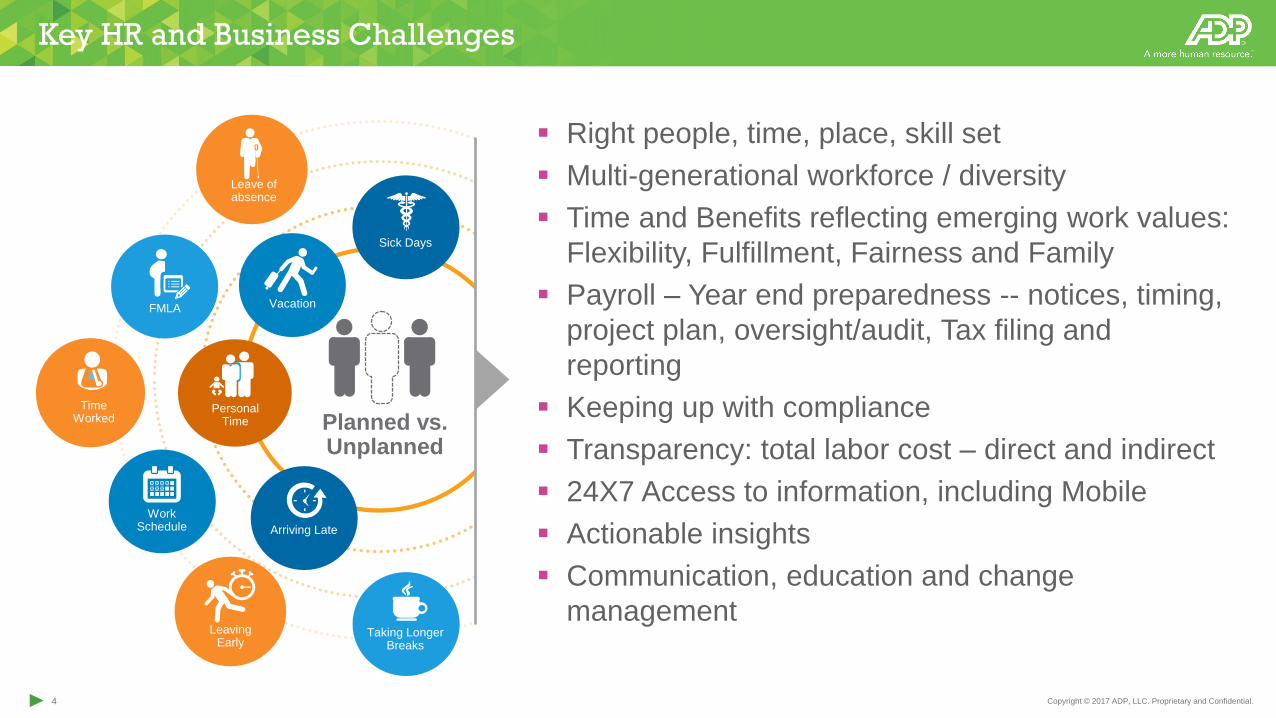

Key HR and Business Challenges

Planned vs. Unplanned

Sick Days

Arriving Late

Vacation

Taking Longer Breaks

Work Schedule

FMLA

Personal Time

Leave of absence

Leaving Early

Time Worked

Right people, time, place, skill set

Multi-generational workforce / diversity

Time and Benefits reflecting emerging work values:

Flexibility, Fulfillment, Fairness and Family

Payroll – Year end preparedness -- notices, timing,

project plan, oversight/audit, Tax filing and

reporting

Keeping up with compliance

Transparency: total labor cost – direct and indirect

24X7 Access to information, including Mobile

Actionable insights

Communication, education and change

management

Compliance Trends and Considerations

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Regulatory and Compliance Landscape

IRS increasingly focused on security and fraud prevention

– Accelerated deadline

States are increasingly adjusting their deadlines to reflect

IRS changes

Acceleration of new potential Federal and State/local

leave laws

– Hundreds of Private Sector, and Public Sector leaves

– Areas of concern include scrutiny by DOL

Proliferation of paid sick leave

– State / Municipal Trend

– New Trend – States Banning Local Paid Sick Leave Laws

Administrative burden and associated time erosion

Financial risks

It is not always easy to

know what is right…

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

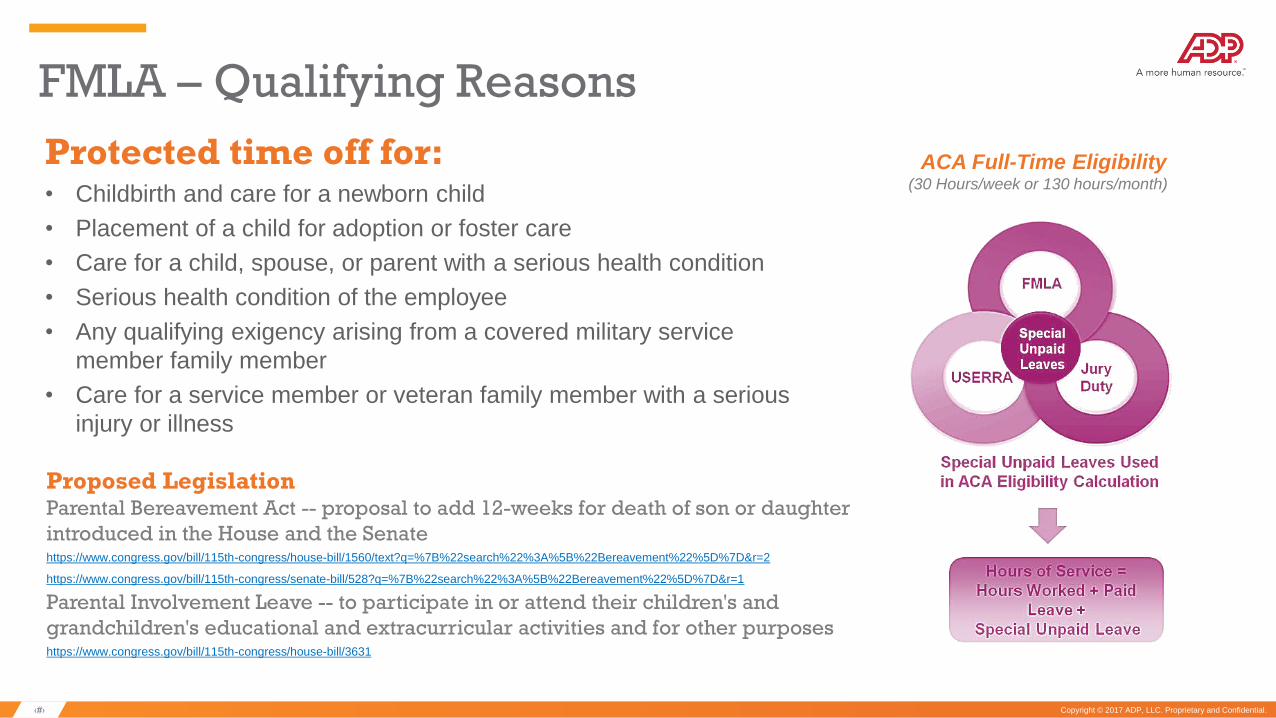

FMLA – Qualifying Reasons

Protected time off for:• Childbirth and care for a newborn child

• Placement of a child for adoption or foster care

• Care for a child, spouse, or parent with a serious health condition

• Serious health condition of the employee

• Any qualifying exigency arising from a covered military service

member family member

• Care for a service member or veteran family member with a serious

injury or illness

Proposed LegislationParental Bereavement Act -- proposal to add 12-weeks for death of son or daughter

introduced in the House and the Senatehttps://www.congress.gov/bill/115th-congress/house-bill/1560/text?q=%7B%22search%22%3A%5B%22Bereavement%22%5D%7D&r=2

https://www.congress.gov/bill/115th-congress/senate-bill/528?q=%7B%22search%22%3A%5B%22Bereavement%22%5D%7D&r=1

Parental Involvement Leave -- to participate in or attend their children's and

grandchildren's educational and extracurricular activities and for other purposeshttps://www.congress.gov/bill/115th-congress/house-bill/3631

ACA Full-Time Eligibility(30 Hours/week or 130 hours/month)

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

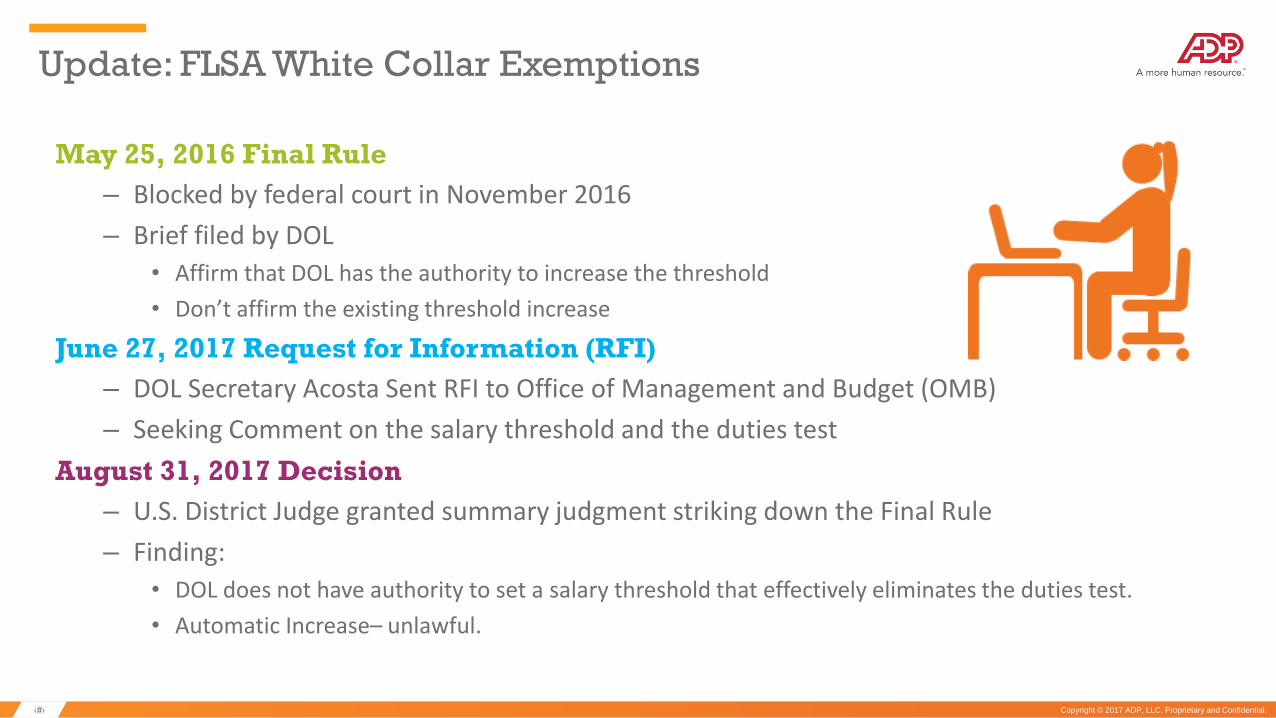

Update: FLSA White Collar Exemptions

May 25, 2016 Final Rule

– Blocked by federal court in November 2016

– Brief filed by DOL

• Affirm that DOL has the authority to increase the threshold

• Don’t affirm the existing threshold increase

June 27, 2017 Request for Information (RFI)

– DOL Secretary Acosta Sent RFI to Office of Management and Budget (OMB)

– Seeking Comment on the salary threshold and the duties test

August 31, 2017 Decision

– U.S. District Judge granted summary judgment striking down the Final Rule

– Finding:

• DOL does not have authority to set a salary threshold that effectively eliminates the duties test.

• Automatic Increase– unlawful.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

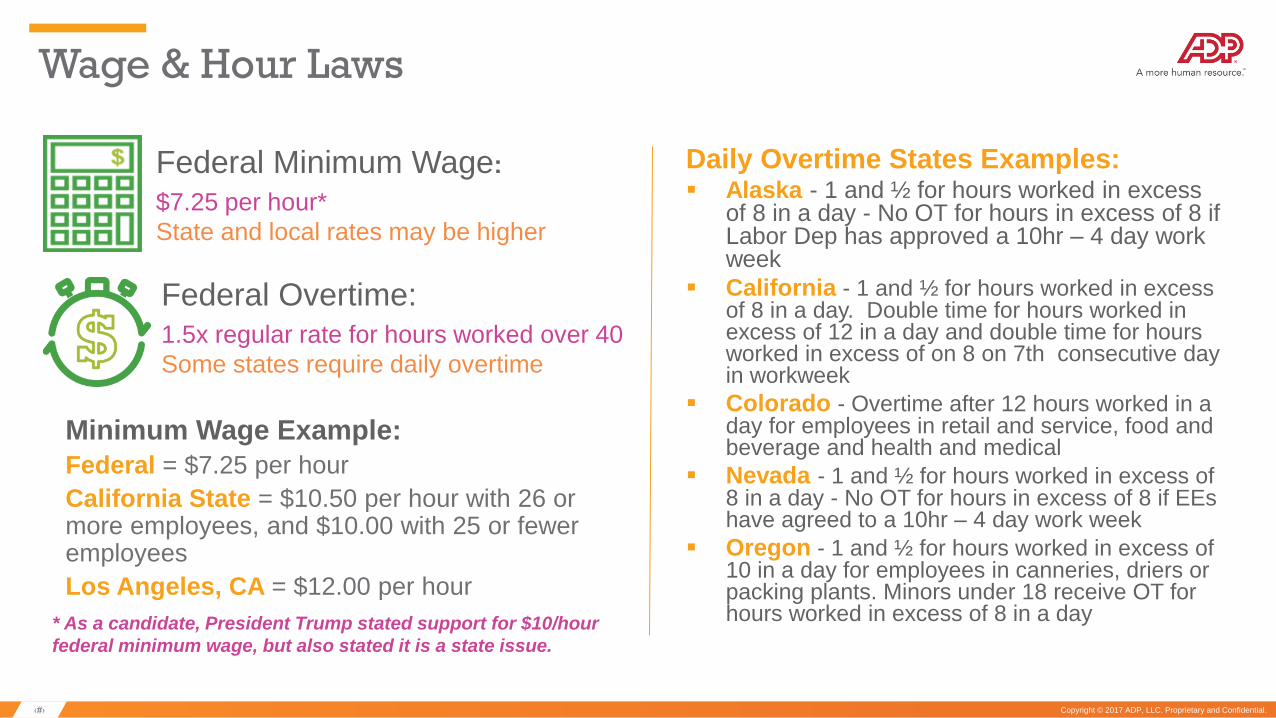

Wage & Hour Laws

Federal Minimum Wage:

$7.25 per hour*

State and local rates may be higher

* As a candidate, President Trump stated support for $10/hour

federal minimum wage, but also stated it is a state issue.

Federal Overtime:1.5x regular rate for hours worked over 40

Some states require daily overtime

Daily Overtime States Examples: Alaska - 1 and ½ for hours worked in excess

of 8 in a day - No OT for hours in excess of 8 if Labor Dep has approved a 10hr – 4 day work week

California - 1 and ½ for hours worked in excess of 8 in a day. Double time for hours worked in excess of 12 in a day and double time for hours worked in excess of on 8 on 7th consecutive day in workweek

Colorado - Overtime after 12 hours worked in a day for employees in retail and service, food and beverage and health and medical

Nevada - 1 and ½ for hours worked in excess of 8 in a day - No OT for hours in excess of 8 if EEs have agreed to a 10hr – 4 day work week

Oregon - 1 and ½ for hours worked in excess of 10 in a day for employees in canneries, driers or packing plants. Minors under 18 receive OT for hours worked in excess of 8 in a day

Minimum Wage Example:

Federal = $7.25 per hour

California State = $10.50 per hour with 26 or more employees, and $10.00 with 25 or fewer employees

Los Angeles, CA = $12.00 per hour

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

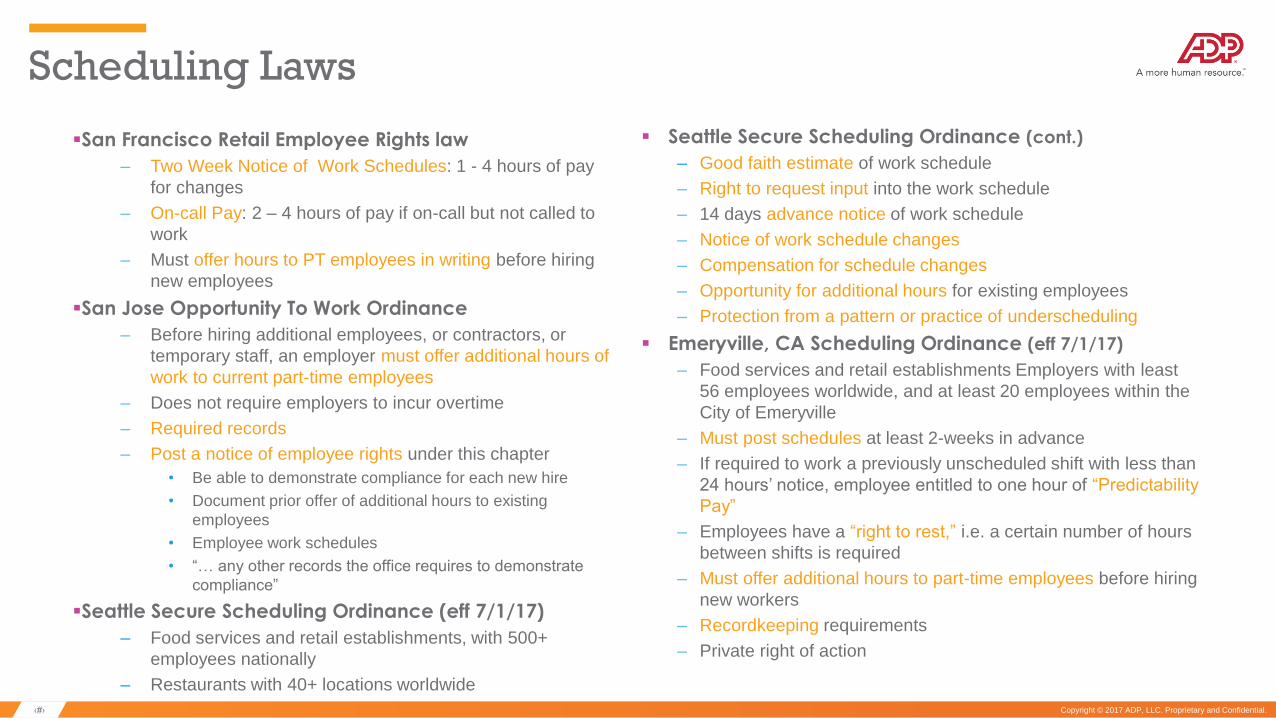

San Francisco Retail Employee Rights law

– Two Week Notice of Work Schedules: 1 - 4 hours of pay

for changes

– On-call Pay: 2 – 4 hours of pay if on-call but not called to

work

– Must offer hours to PT employees in writing before hiring

new employees

San Jose Opportunity To Work Ordinance

– Before hiring additional employees, or contractors, or

temporary staff, an employer must offer additional hours of

work to current part-time employees

– Does not require employers to incur overtime

– Required records

– Post a notice of employee rights under this chapter

• Be able to demonstrate compliance for each new hire

• Document prior offer of additional hours to existing

employees

• Employee work schedules

• “… any other records the office requires to demonstrate

compliance”

Seattle Secure Scheduling Ordinance (eff 7/1/17)

– Food services and retail establishments, with 500+

employees nationally

– Restaurants with 40+ locations worldwide

Scheduling Laws

Seattle Secure Scheduling Ordinance (cont.)

– Good faith estimate of work schedule

– Right to request input into the work schedule

– 14 days advance notice of work schedule

– Notice of work schedule changes

– Compensation for schedule changes

– Opportunity for additional hours for existing employees

– Protection from a pattern or practice of underscheduling

Emeryville, CA Scheduling Ordinance (eff 7/1/17)

– Food services and retail establishments Employers with least

56 employees worldwide, and at least 20 employees within the

City of Emeryville

– Must post schedules at least 2-weeks in advance

– If required to work a previously unscheduled shift with less than

24 hours’ notice, employee entitled to one hour of “Predictability

Pay”

– Employees have a “right to rest,” i.e. a certain number of hours

between shifts is required

– Must offer additional hours to part-time employees before hiring

new workers

– Recordkeeping requirements

– Private right of action

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

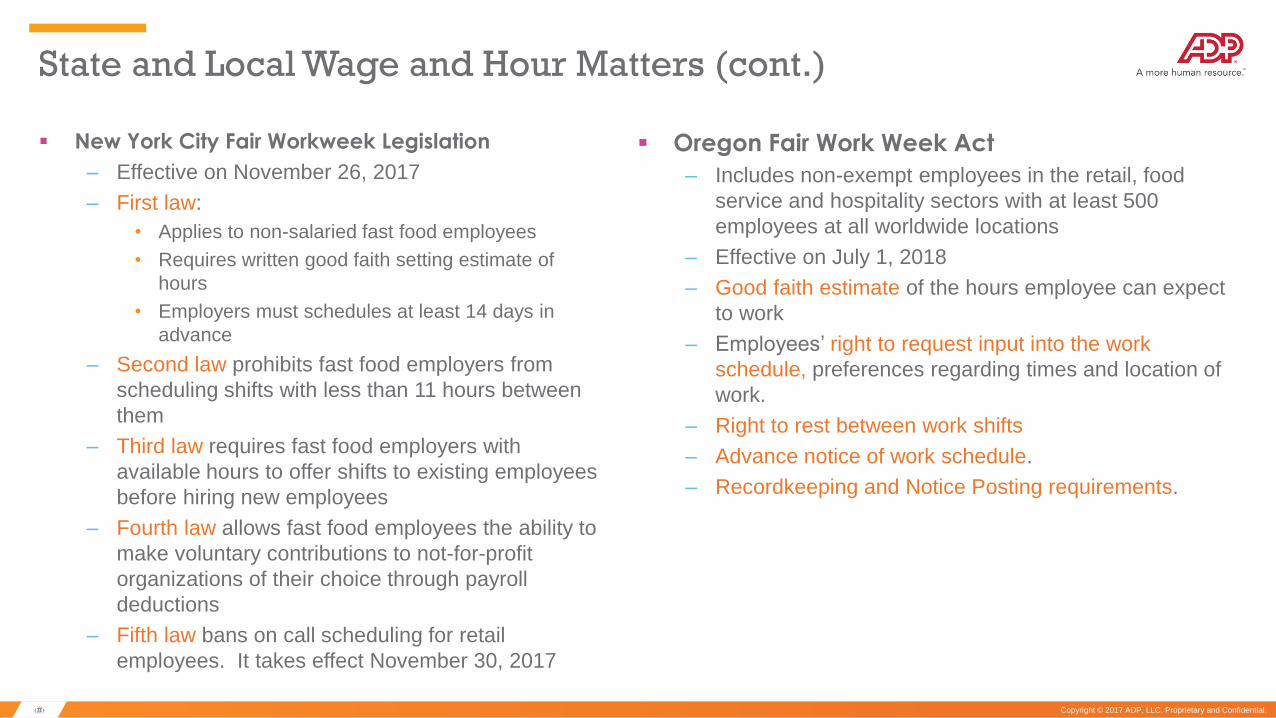

State and Local Wage and Hour Matters (cont.)

New York City Fair Workweek Legislation

– Effective on November 26, 2017

– First law:

• Applies to non-salaried fast food employees

• Requires written good faith setting estimate of

hours

• Employers must schedules at least 14 days in

advance

– Second law prohibits fast food employers from

scheduling shifts with less than 11 hours between

them

– Third law requires fast food employers with

available hours to offer shifts to existing employees

before hiring new employees

– Fourth law allows fast food employees the ability to

make voluntary contributions to not-for-profit

organizations of their choice through payroll

deductions

– Fifth law bans on call scheduling for retail

employees. It takes effect November 30, 2017

Oregon Fair Work Week Act

– Includes non-exempt employees in the retail, food

service and hospitality sectors with at least 500

employees at all worldwide locations

– Effective on July 1, 2018

– Good faith estimate of the hours employee can expect

to work

– Employees’ right to request input into the work

schedule, preferences regarding times and location of

work.

– Right to rest between work shifts

– Advance notice of work schedule.

– Recordkeeping and Notice Posting requirements.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Remind non-exempt employees and managers about

Timekeeping Policies and Prohibitions:

Policies and practices around timekeeping / flexible hours

Working off-the-clock

Meal and rest breaks

Exception time

Pre- and post-shift work activities

Meeting and training time

Travel time

Shift differentials

Overtime pay on bonuses and commissions

PTO tracking

Remote working provisions and home-shore policies

Payroll changes

Controlling overtime hours

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

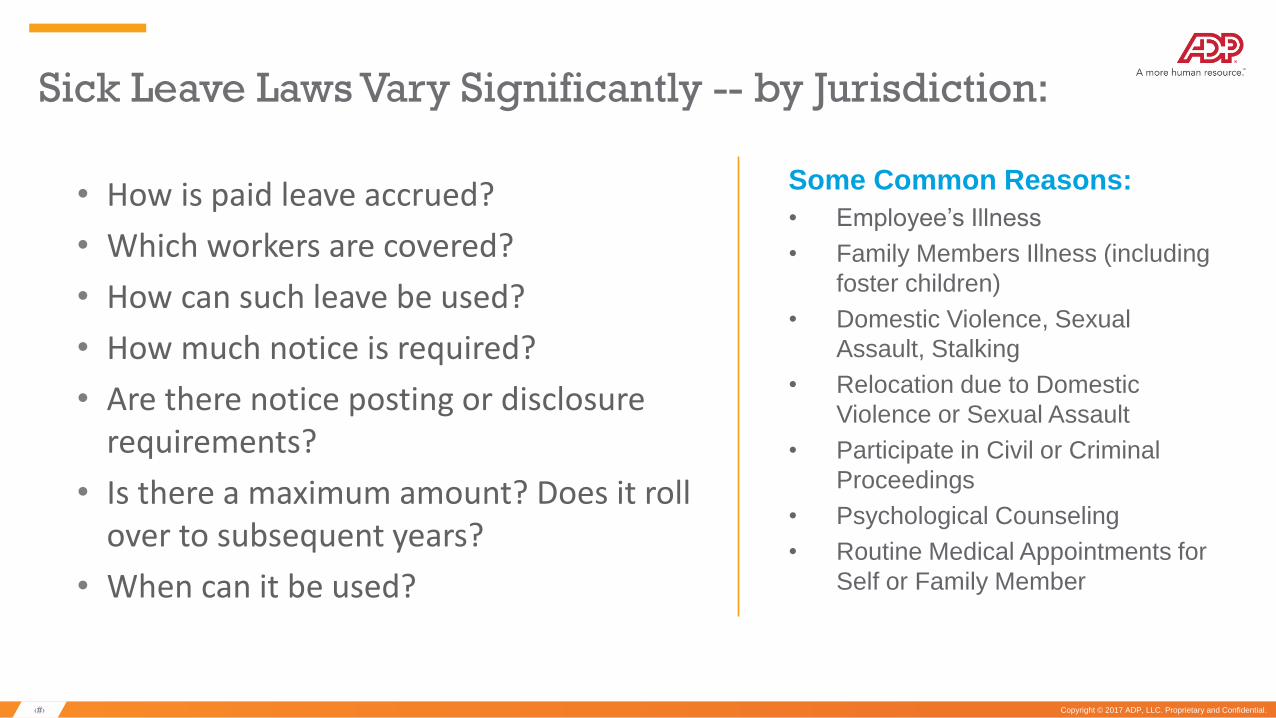

• How is paid leave accrued?

• Which workers are covered?

• How can such leave be used?

• How much notice is required?

• Are there notice posting or disclosure requirements?

• Is there a maximum amount? Does it roll over to subsequent years?

• When can it be used?

Some Common Reasons:

• Employee’s Illness

• Family Members Illness (including

foster children)

• Domestic Violence, Sexual

Assault, Stalking

• Relocation due to Domestic

Violence or Sexual Assault

• Participate in Civil or Criminal

Proceedings

• Psychological Counseling

• Routine Medical Appointments for

Self or Family Member

Sick Leave Laws Vary Significantly -- by Jurisdiction:

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

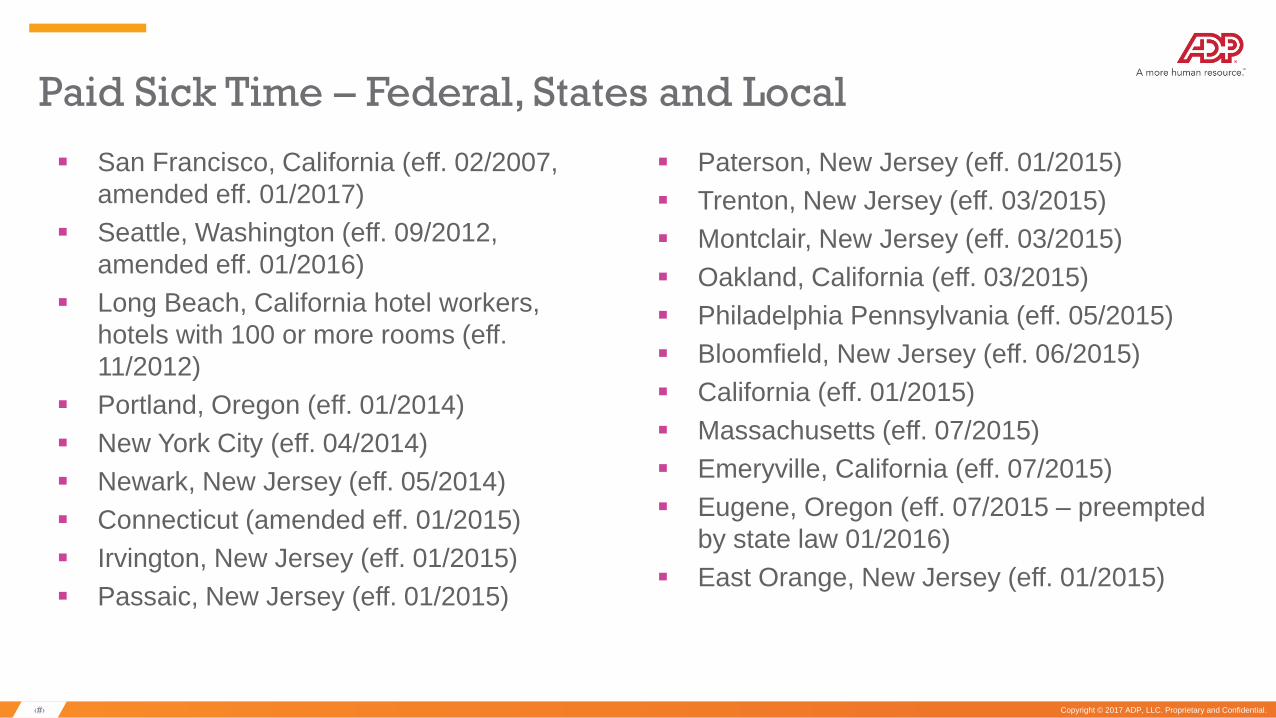

Paid Sick Time – Federal, States and Local

San Francisco, California (eff. 02/2007,

amended eff. 01/2017)

Seattle, Washington (eff. 09/2012,

amended eff. 01/2016)

Long Beach, California hotel workers,

hotels with 100 or more rooms (eff.

11/2012)

Portland, Oregon (eff. 01/2014)

New York City (eff. 04/2014)

Newark, New Jersey (eff. 05/2014)

Connecticut (amended eff. 01/2015)

Irvington, New Jersey (eff. 01/2015)

Passaic, New Jersey (eff. 01/2015)

Paterson, New Jersey (eff. 01/2015)

Trenton, New Jersey (eff. 03/2015)

Montclair, New Jersey (eff. 03/2015)

Oakland, California (eff. 03/2015)

Philadelphia Pennsylvania (eff. 05/2015)

Bloomfield, New Jersey (eff. 06/2015)

California (eff. 01/2015)

Massachusetts (eff. 07/2015)

Emeryville, California (eff. 07/2015)

Eugene, Oregon (eff. 07/2015 – preempted

by state law 01/2016)

East Orange, New Jersey (eff. 01/2015)

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

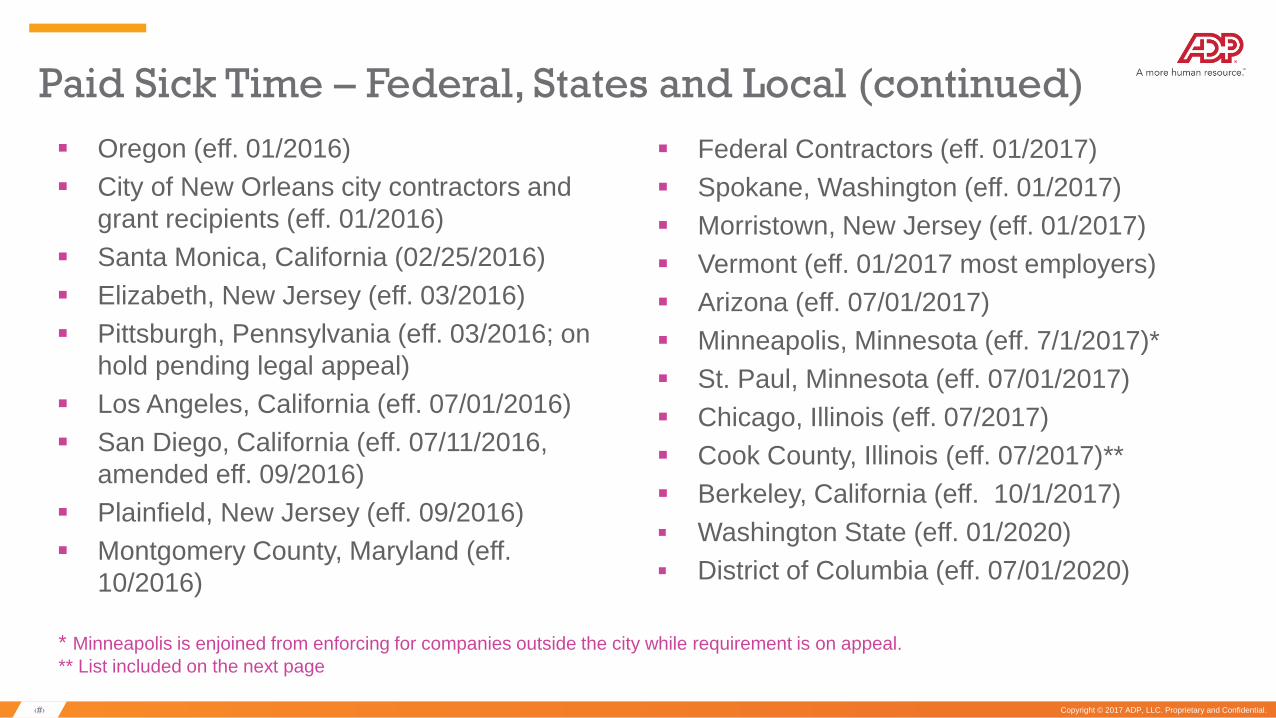

Paid Sick Time – Federal, States and Local (continued)

Oregon (eff. 01/2016)

City of New Orleans city contractors and

grant recipients (eff. 01/2016)

Santa Monica, California (02/25/2016)

Elizabeth, New Jersey (eff. 03/2016)

Pittsburgh, Pennsylvania (eff. 03/2016; on

hold pending legal appeal)

Los Angeles, California (eff. 07/01/2016)

San Diego, California (eff. 07/11/2016,

amended eff. 09/2016)

Plainfield, New Jersey (eff. 09/2016)

Montgomery County, Maryland (eff.

10/2016)

Federal Contractors (eff. 01/2017)

Spokane, Washington (eff. 01/2017)

Morristown, New Jersey (eff. 01/2017)

Vermont (eff. 01/2017 most employers)

Arizona (eff. 07/01/2017)

Minneapolis, Minnesota (eff. 7/1/2017)*

St. Paul, Minnesota (eff. 07/01/2017)

Chicago, Illinois (eff. 07/2017)

Cook County, Illinois (eff. 07/2017)**

Berkeley, California (eff. 10/1/2017)

Washington State (eff. 01/2020)

District of Columbia (eff. 07/01/2020)

* Minneapolis is enjoined from enforcing for companies outside the city while requirement is on appeal.

** List included on the next page

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

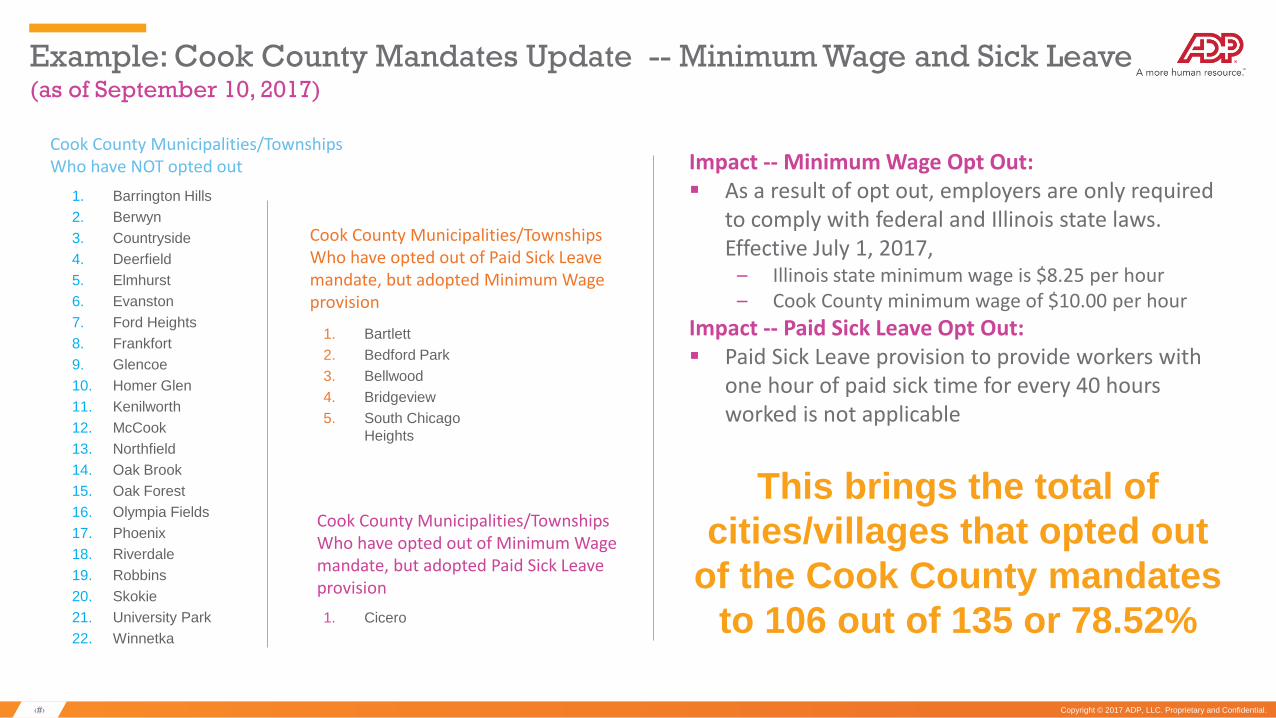

Example: Cook County Mandates Update -- Minimum Wage and Sick Leave (as of September 10, 2017)

1. Barrington Hills

2. Berwyn

3. Countryside

4. Deerfield

5. Elmhurst

6. Evanston

7. Ford Heights

8. Frankfort

9. Glencoe

10. Homer Glen

11. Kenilworth

12. McCook

13. Northfield

14. Oak Brook

15. Oak Forest

16. Olympia Fields

17. Phoenix

18. Riverdale

19. Robbins

20. Skokie

21. University Park

22. Winnetka

This brings the total of

cities/villages that opted out

of the Cook County mandates

to 106 out of 135 or 78.52%

Impact -- Minimum Wage Opt Out: As a result of opt out, employers are only required

to comply with federal and Illinois state laws. Effective July 1, 2017,

– Illinois state minimum wage is $8.25 per hour – Cook County minimum wage of $10.00 per hour

Impact -- Paid Sick Leave Opt Out: Paid Sick Leave provision to provide workers with

one hour of paid sick time for every 40 hours worked is not applicable

1. Bartlett

2. Bedford Park

3. Bellwood

4. Bridgeview

5. South Chicago

Heights

Cook County Municipalities/Townships Who have opted out of Paid Sick Leave mandate, but adopted Minimum Wage provision

Cook County Municipalities/Townships Who have NOT opted out

1. Cicero

Cook County Municipalities/Townships Who have opted out of Minimum Wage mandate, but adopted Paid Sick Leave provision

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

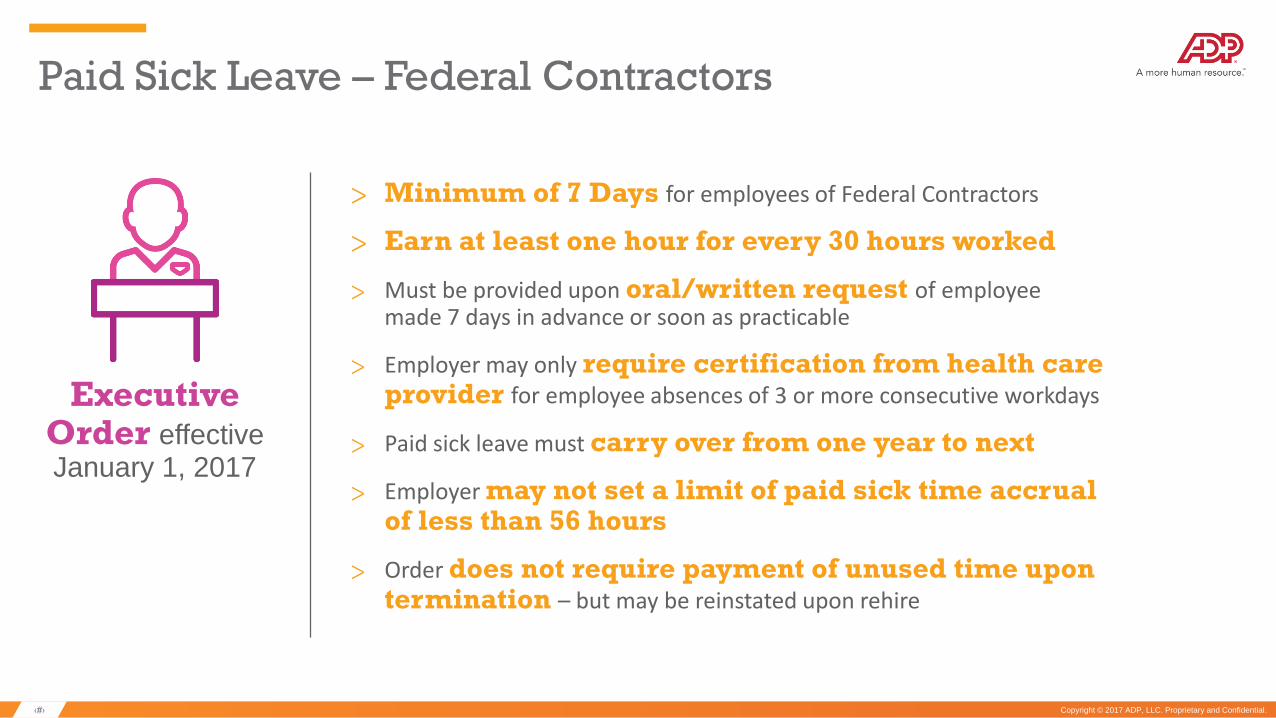

Paid Sick Leave – Federal Contractors

> Minimum of 7 Days for employees of Federal Contractors

> Earn at least one hour for every 30 hours worked

> Must be provided upon oral/written request of employee made 7 days in advance or soon as practicable

> Employer may only require certification from health care provider for employee absences of 3 or more consecutive workdays

> Paid sick leave must carry over from one year to next

> Employer may not set a limit of paid sick time accrual of less than 56 hours

> Order does not require payment of unused time upon termination – but may be reinstated upon rehire

ExecutiveOrder effective January 1, 2017

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

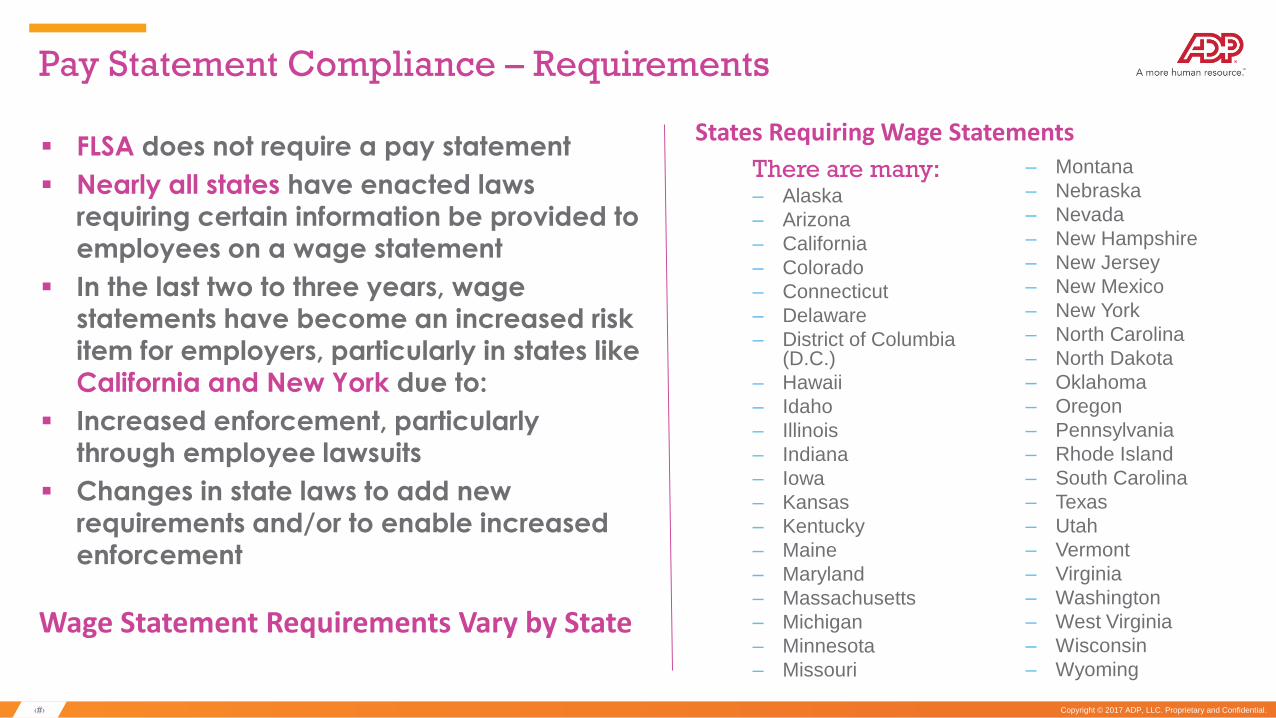

Pay Statement Compliance – Requirements

FLSA does not require a pay statement

Nearly all states have enacted laws

requiring certain information be provided to

employees on a wage statement

In the last two to three years, wage

statements have become an increased risk

item for employers, particularly in states like

California and New York due to:

Increased enforcement, particularly

through employee lawsuits

Changes in state laws to add new

requirements and/or to enable increased enforcement

States Requiring Wage Statements

There are many:– Alaska

– Arizona

– California

– Colorado

– Connecticut

– Delaware

– District of Columbia (D.C.)

– Hawaii

– Idaho

– Illinois

– Indiana

– Iowa

– Kansas

– Kentucky

– Maine

– Maryland

– Massachusetts

– Michigan

– Minnesota

– Missouri

– Montana

– Nebraska

– Nevada

– New Hampshire

– New Jersey

– New Mexico

– New York

– North Carolina

– North Dakota

– Oklahoma

– Oregon

– Pennsylvania

– Rhode Island

– South Carolina

– Texas

– Utah

– Vermont

– Virginia

– Washington

– West Virginia

– Wisconsin

– Wyoming

Wage Statement Requirements Vary by State

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

2017 Payroll and Tax-Related IRS Regulatory Requirements

By January 31, 2018, annual wage and tax reports must be furnished to employees (W-2s) and independent contractors (1099-MISC).

W-2s must be post marked to the Social Security Administration hard copy by January 31, 2018. This includes Form W-3, along with all W-2s and Form 1096, and all 1099 forms. The deadline to file electronically is January 31.

Both the monthly payment on federal unemployment (FUTA) taxes and the Federal Unemployment Tax Report for 2017 are due January 31, 2018.

Form 941 (Employer's Quarterly Federal Tax Form) for Fourth Quarter 2017 is due January 31, 2018.

State deadlines vary by state and are still being announced, but 21 states have moved up their deadlines for tax year 2017 and this trend will continue.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Form Descriptions

The Form W-2: Wage and Tax Statement, is used to report wages paid to employees and the taxes withheld from them Form W-3 is a summary page of all W-2 forms issued by the employer Form W-4 is used by employers to determine the amount of tax withholding to deduct from employees' wages. A 1099-MISC is a type of tax form. It is used to report miscellaneous income, such as income earned as a non-employee, as well as

fees, commissions, rents, or royalties paid during the last tax year. Payments for prizes, awards, legal services, and other non-employee activities may be reported on this form as well.

Form 940: Employer’s Annual Federal Unemployment (FUTA) Tax Return Form 941: Employer’s Quarterly Federal Tax Return Form 944: Employer’s Annual Federal Tax Return Form 945: Annual Return of Withheld Federal Income Tax (For withholding reported on Forms 1099 and W-2G) Form 1042-S is used to report amounts paid to foreign persons (including persons presumed to be foreign) that are subject to income

tax withholding, even if no amount is deducted and withheld from the payment because of a treaty or exception to taxation, or if any amount withheld was repaid to the payee.

1094-C and 1095-C are filed by employers that are required to offer health insurance coverage to their employees under the Affordable Care Act, also known as Obamacare.

Form 8027 is the Employer's Annual Information Return of Tip Income and Allocated Tips Form 5498 is sent if you made contributions to an IRA (Individual Retirement Account) in the preceding tax year. The "custodian" of

your IRA, typically the bank or other institution that manages your account, will mail a copy of this form to both you and the Internal Revenue Service.

Form 1099: Form 1099 series is used to report various types of income other than wages, salaries, and tips (for which Form W-2 is used instead). Examples of reportable transactions are amounts paid to a non-corporate independent contractor for services (in IRS terminology, such payments are nonemployee compensation).

Form 1096 is the Annual Summary and Transmittal of U.S. Information Returns. This form is used to transmit Forms 1097, 1098, 1099, 3921, 3922, 5498 and W-2G to the Internal Revenue Service.

Year End Life-Cycle

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

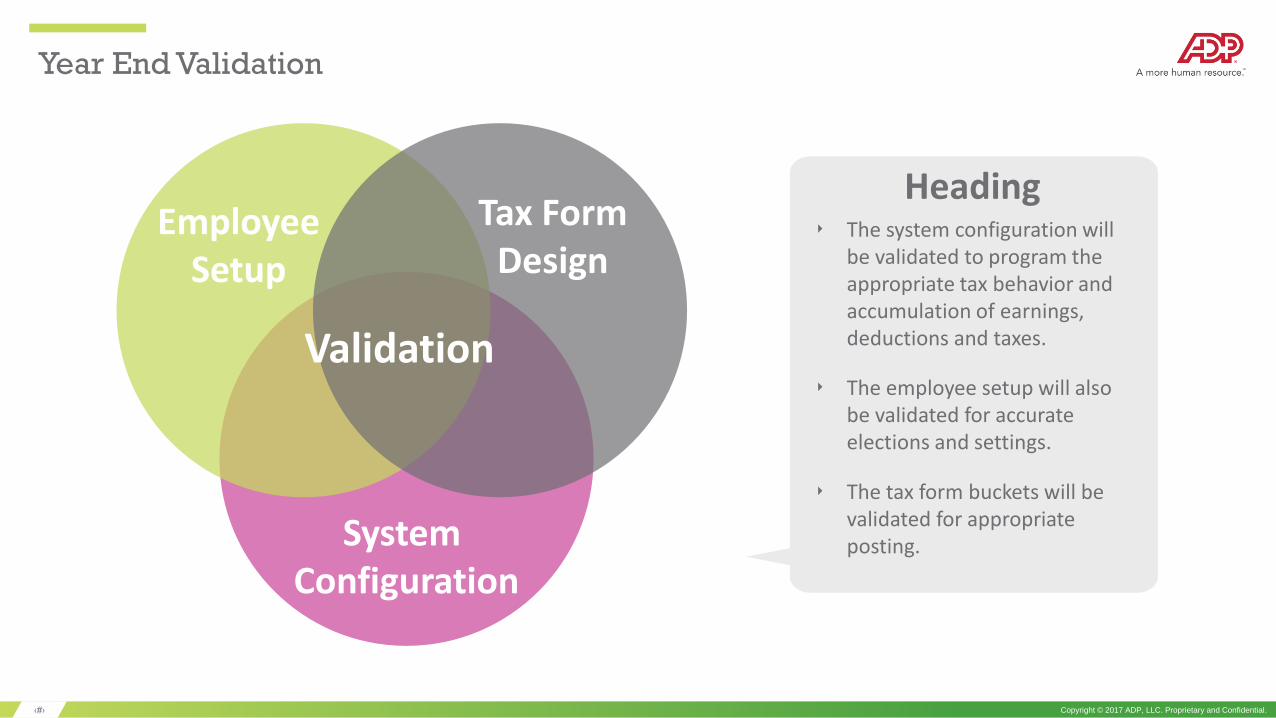

Year End Validation

Validation

EmployeeSetup

Tax FormDesign

System Configuration

‣ The system configuration will be validated to program the appropriate tax behavior and accumulation of earnings, deductions and taxes.

‣ The employee setup will also be validated for accurate elections and settings.

‣ The tax form buckets will be validated for appropriate posting.

Heading

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Audits Are Complex (Auditors Review)

Tax Attributes

Accumulators

Mapping

Balances

Employee Payroll Data (e.g. Exempt Status)

Limits (e.g. Social Security)

Percent Contribution (e.g. Social Security)

Adjustments

Employee Status (e.g. Terminated)

Resident and Work Location

Exceptions

Some of the key components evaluated in validating year end configuration and setup, as well as reconciling results, include:

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

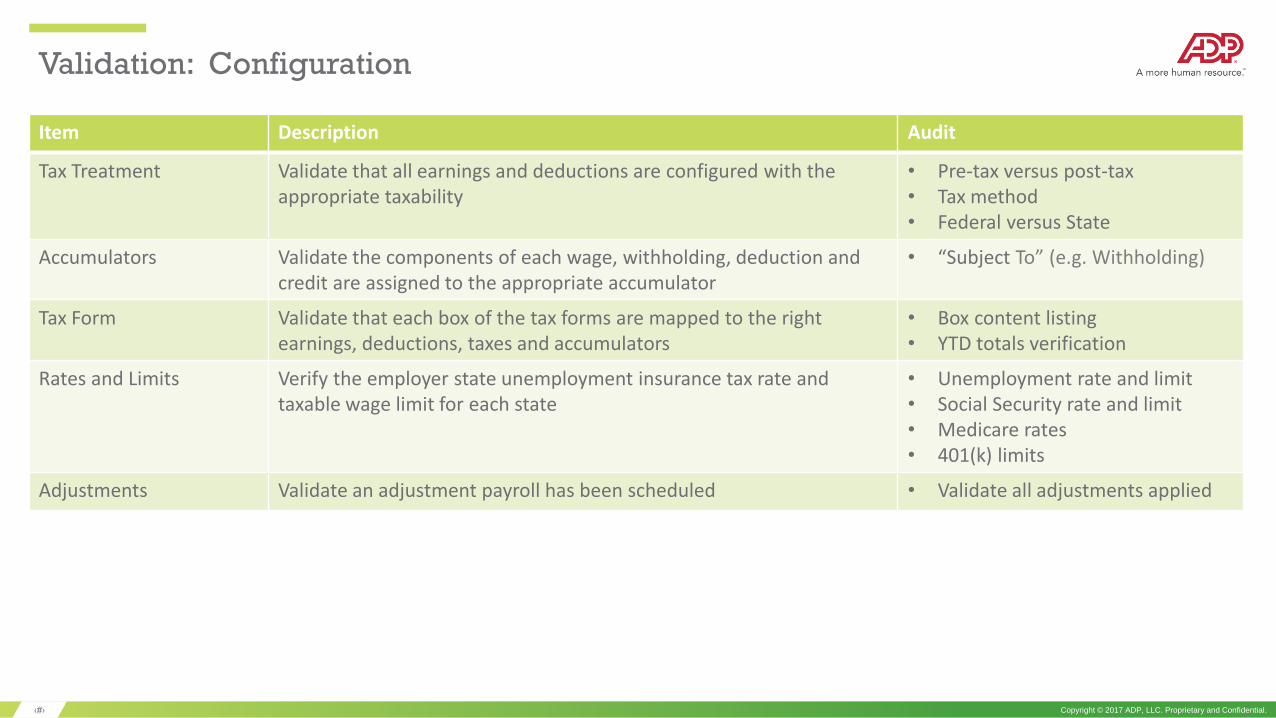

Validation: Configuration

Item Description Audit

Tax Treatment Validate that all earnings and deductions are configured with the appropriate taxability

• Pre-tax versus post-tax• Tax method• Federal versus State

Accumulators Validate the components of each wage, withholding, deduction and credit are assigned to the appropriate accumulator

• “Subject To” (e.g. Withholding)

Tax Form Validate that each box of the tax forms are mapped to the right earnings, deductions, taxes and accumulators

• Box content listing• YTD totals verification

Rates and Limits Verify the employer state unemployment insurance tax rate and taxable wage limit for each state

• Unemployment rate and limit• Social Security rate and limit• Medicare rates• 401(k) limits

Adjustments Validate an adjustment payroll has been scheduled • Validate all adjustments applied

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

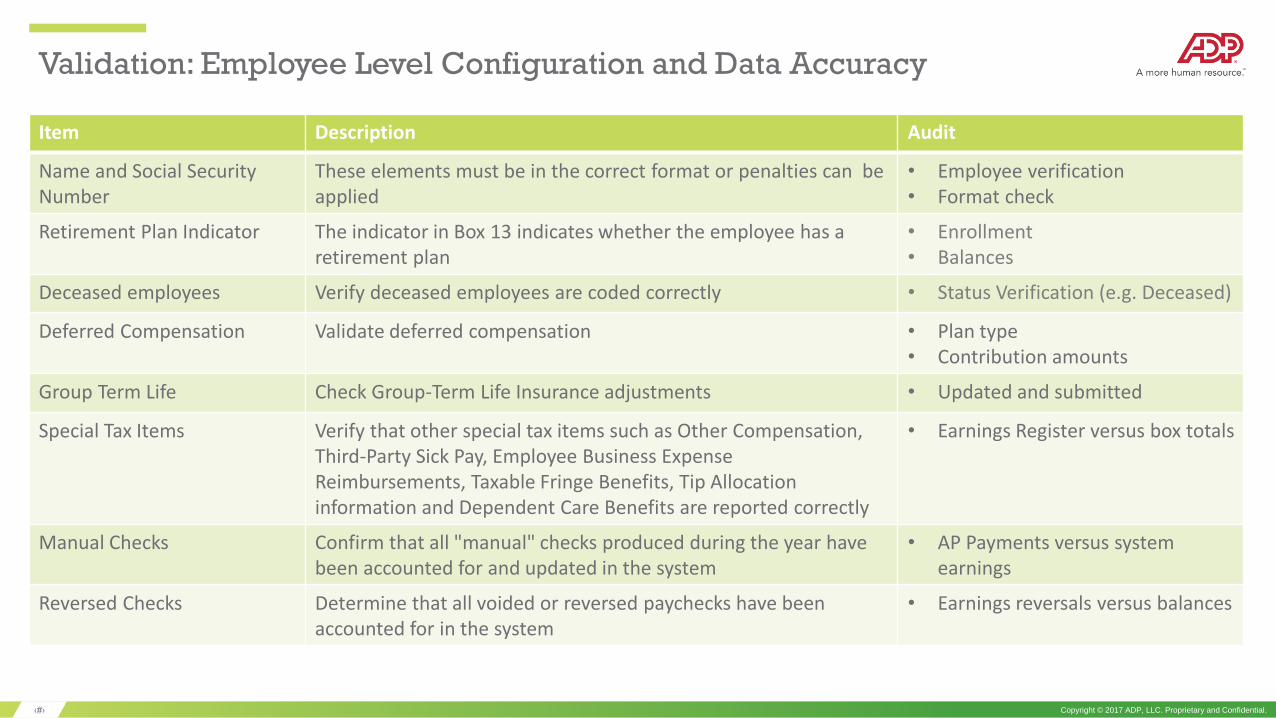

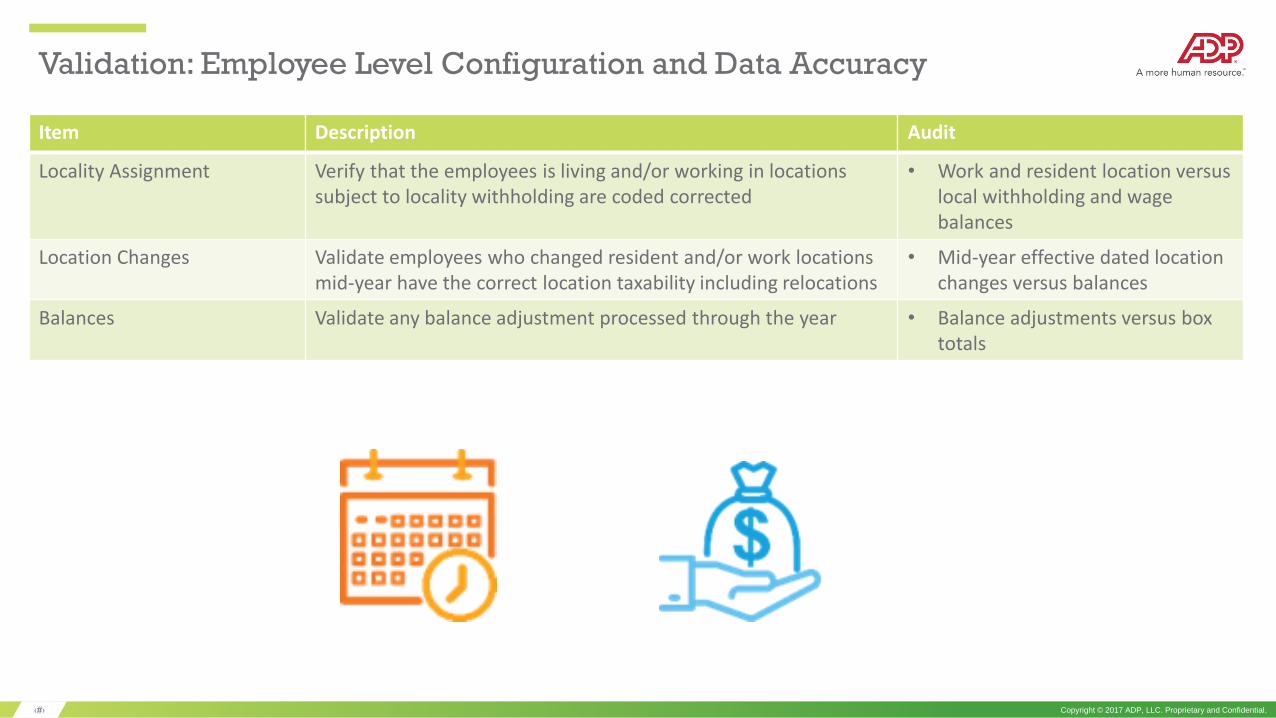

Validation: Employee Level Configuration and Data Accuracy

Item Description Audit

Name and Social Security Number

These elements must be in the correct format or penalties can be applied

• Employee verification• Format check

Retirement Plan Indicator The indicator in Box 13 indicates whether the employee has a retirement plan

• Enrollment• Balances

Deceased employees Verify deceased employees are coded correctly • Status Verification (e.g. Deceased)

Deferred Compensation Validate deferred compensation • Plan type • Contribution amounts

Group Term Life Check Group-Term Life Insurance adjustments • Updated and submitted

Special Tax Items Verify that other special tax items such as Other Compensation, Third-Party Sick Pay, Employee Business Expense Reimbursements, Taxable Fringe Benefits, Tip Allocation information and Dependent Care Benefits are reported correctly

• Earnings Register versus box totals

Manual Checks Confirm that all "manual" checks produced during the year have been accounted for and updated in the system

• AP Payments versus system earnings

Reversed Checks Determine that all voided or reversed paychecks have been accounted for in the system

• Earnings reversals versus balances

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

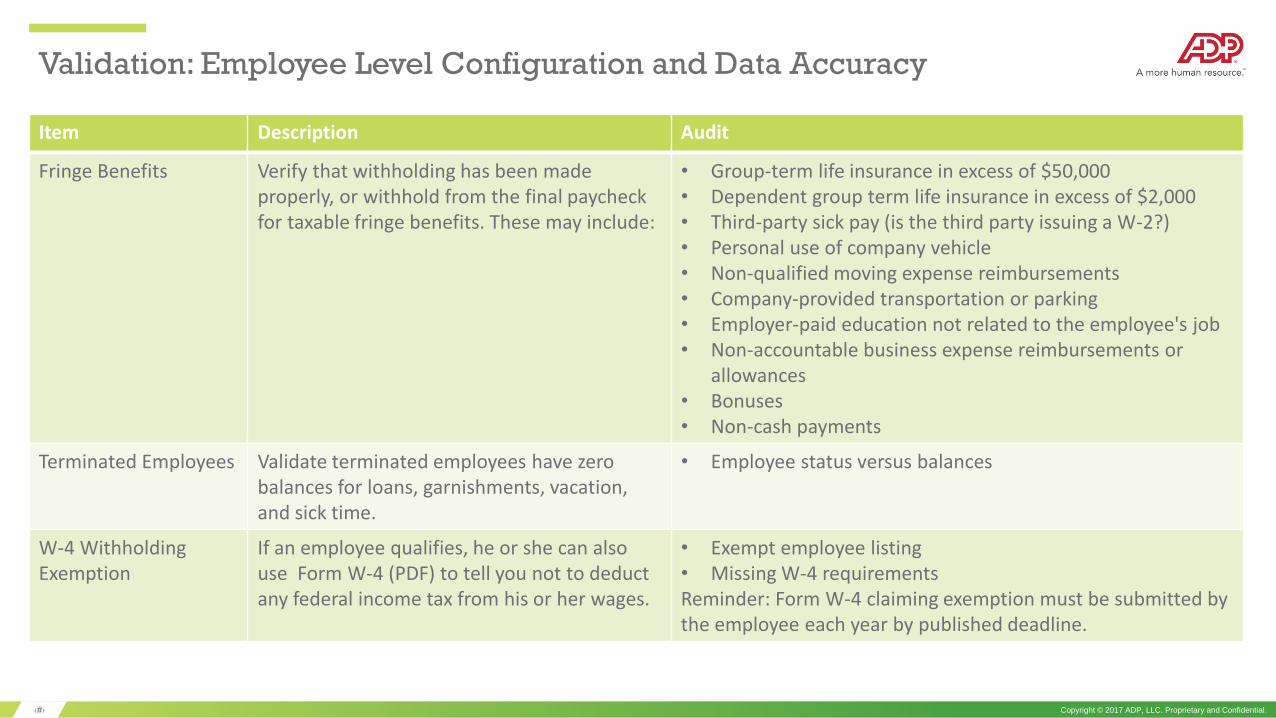

Validation: Employee Level Configuration and Data Accuracy

Item Description Audit

Fringe Benefits Verify that withholding has been made properly, or withhold from the final paycheck for taxable fringe benefits. These may include:

• Group-term life insurance in excess of $50,000• Dependent group term life insurance in excess of $2,000• Third-party sick pay (is the third party issuing a W-2?) • Personal use of company vehicle • Non-qualified moving expense reimbursements • Company-provided transportation or parking • Employer-paid education not related to the employee's job • Non-accountable business expense reimbursements or

allowances • Bonuses • Non-cash payments

Terminated Employees Validate terminated employees have zero balances for loans, garnishments, vacation, and sick time.

• Employee status versus balances

W-4 WithholdingExemption

If an employee qualifies, he or she can also use Form W-4 (PDF) to tell you not to deduct any federal income tax from his or her wages.

• Exempt employee listing• Missing W-4 requirementsReminder: Form W-4 claiming exemption must be submitted by the employee each year by published deadline.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Validation: Employee Level Configuration and Data Accuracy

Item Description Audit

Locality Assignment Verify that the employees is living and/or working in locations subject to locality withholding are coded corrected

• Work and resident location versus local withholding and wage balances

Location Changes Validate employees who changed resident and/or work locations mid-year have the correct location taxability including relocations

• Mid-year effective dated location changes versus balances

Balances Validate any balance adjustment processed through the year • Balance adjustments versus box totals

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

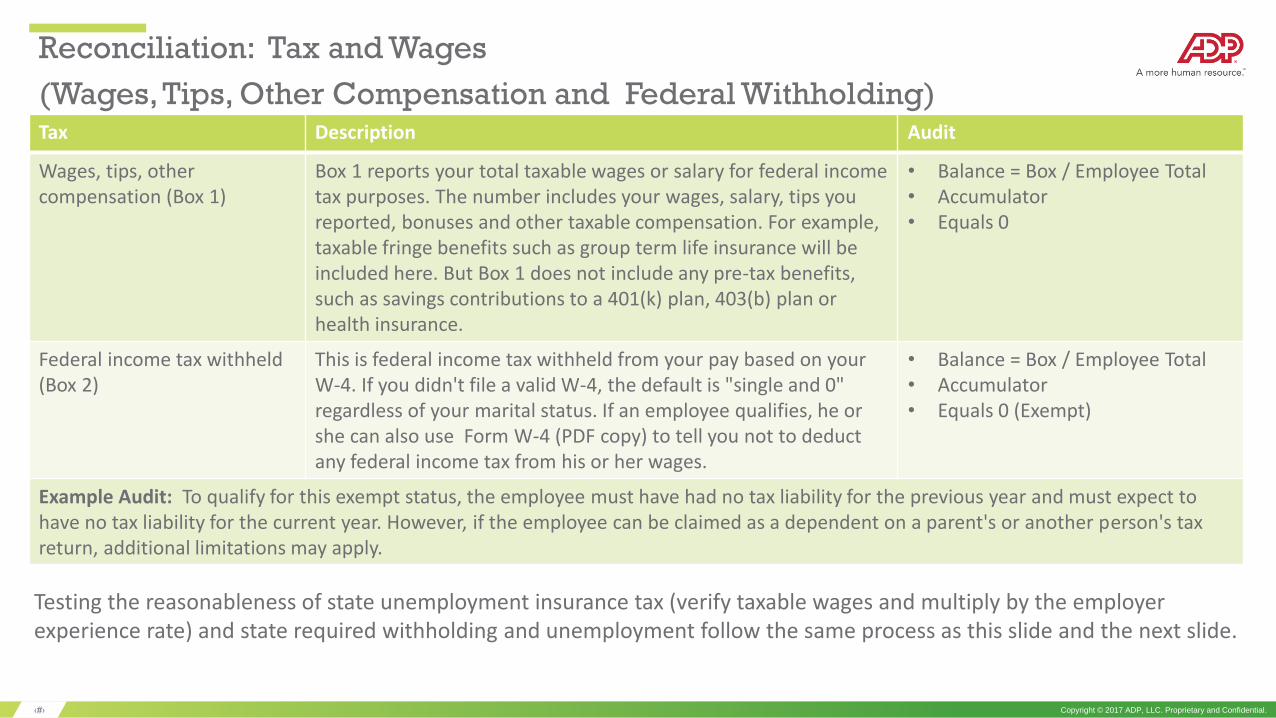

Reconciliation: Tax and Wages

(Wages, Tips, Other Compensation and Federal Withholding)Tax Description Audit

Wages, tips, othercompensation (Box 1)

Box 1 reports your total taxable wages or salary for federal income tax purposes. The number includes your wages, salary, tips you reported, bonuses and other taxable compensation. For example, taxable fringe benefits such as group term life insurance will be included here. But Box 1 does not include any pre-tax benefits, such as savings contributions to a 401(k) plan, 403(b) plan or health insurance.

• Balance = Box / Employee Total• Accumulator• Equals 0

Federal income tax withheld (Box 2)

This is federal income tax withheld from your pay based on your W-4. If you didn't file a valid W-4, the default is "single and 0" regardless of your marital status. If an employee qualifies, he or she can also use Form W-4 (PDF copy) to tell you not to deduct any federal income tax from his or her wages.

• Balance = Box / Employee Total• Accumulator• Equals 0 (Exempt)

Example Audit: To qualify for this exempt status, the employee must have had no tax liability for the previous year and must expect to have no tax liability for the current year. However, if the employee can be claimed as a dependent on a parent's or another person's tax return, additional limitations may apply.

Testing the reasonableness of state unemployment insurance tax (verify taxable wages and multiply by the employer experience rate) and state required withholding and unemployment follow the same process as this slide and the next slide.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

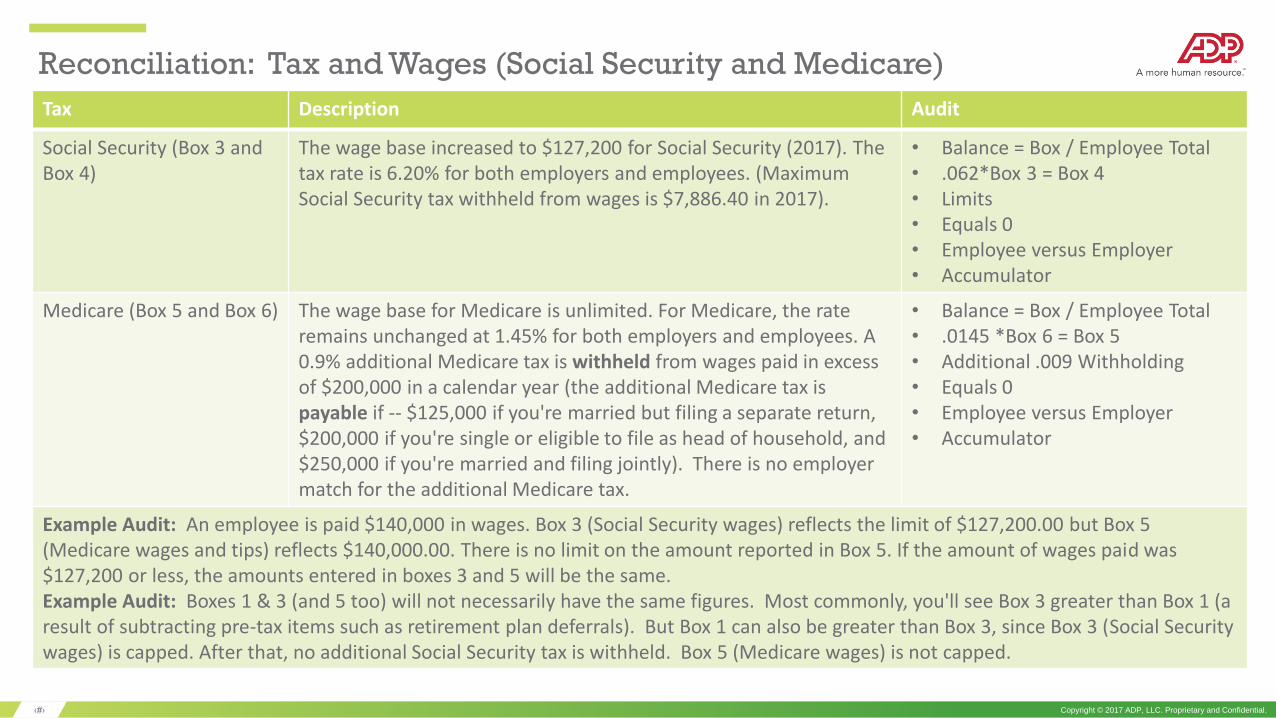

Reconciliation: Tax and Wages (Social Security and Medicare)

Tax Description Audit

Social Security (Box 3 and Box 4)

The wage base increased to $127,200 for Social Security (2017). The tax rate is 6.20% for both employers and employees. (Maximum Social Security tax withheld from wages is $7,886.40 in 2017).

• Balance = Box / Employee Total• .062*Box 3 = Box 4• Limits• Equals 0• Employee versus Employer• Accumulator

Medicare (Box 5 and Box 6) The wage base for Medicare is unlimited. For Medicare, the rate remains unchanged at 1.45% for both employers and employees. A 0.9% additional Medicare tax is withheld from wages paid in excess of $200,000 in a calendar year (the additional Medicare tax is payable if -- $125,000 if you're married but filing a separate return, $200,000 if you're single or eligible to file as head of household, and $250,000 if you're married and filing jointly). There is no employer match for the additional Medicare tax.

• Balance = Box / Employee Total• .0145 *Box 6 = Box 5• Additional .009 Withholding• Equals 0• Employee versus Employer• Accumulator

Example Audit: An employee is paid $140,000 in wages. Box 3 (Social Security wages) reflects the limit of $127,200.00 but Box 5 (Medicare wages and tips) reflects $140,000.00. There is no limit on the amount reported in Box 5. If the amount of wages paid was $127,200 or less, the amounts entered in boxes 3 and 5 will be the same.Example Audit: Boxes 1 & 3 (and 5 too) will not necessarily have the same figures. Most commonly, you'll see Box 3 greater than Box 1 (a result of subtracting pre-tax items such as retirement plan deferrals). But Box 1 can also be greater than Box 3, since Box 3 (Social Security wages) is capped. After that, no additional Social Security tax is withheld. Box 5 (Medicare wages) is not capped.

‹#› Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Reconciliation: GL, Bank and AP

General Ledger: A general ledger reconciliation must be performed before issuing the annual

information statements to verify that the employer’s financial statements accurately reflect the payroll

transactions of the business. This reconciliation can also be used to confirm that wages are reported

correctly and tax liabilities and payments are stated accurately.

Bank Reconciliation: Bank reconciliations should be performed through December 31st of the tax year.

Outstanding checks, voids and stop payments are identified and the posting is validated. Incorrect

wages can be reported and/or withholding an incorrect tax amount are key risks of not performing this

reconciliation.

Accounts Payable This is reviewed to verify that any payments made outside the payroll system to

employees are included in the tax update and unreported taxable items identified. According to

E&Y, an accounts payable reconciliation of this type includes, for example, a review of expense reports

and petty cash or impressed funds; the identification of non-accountable business expense

reimbursements and taxable payments made to individual employees or former employees, relocation

providers, stockbrokers, life insurance companies, and airlines and travel agents; and an accounting of

business and personal use of company vehicles, including cars and airplanes.

Payroll and Operational Indicators

32 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

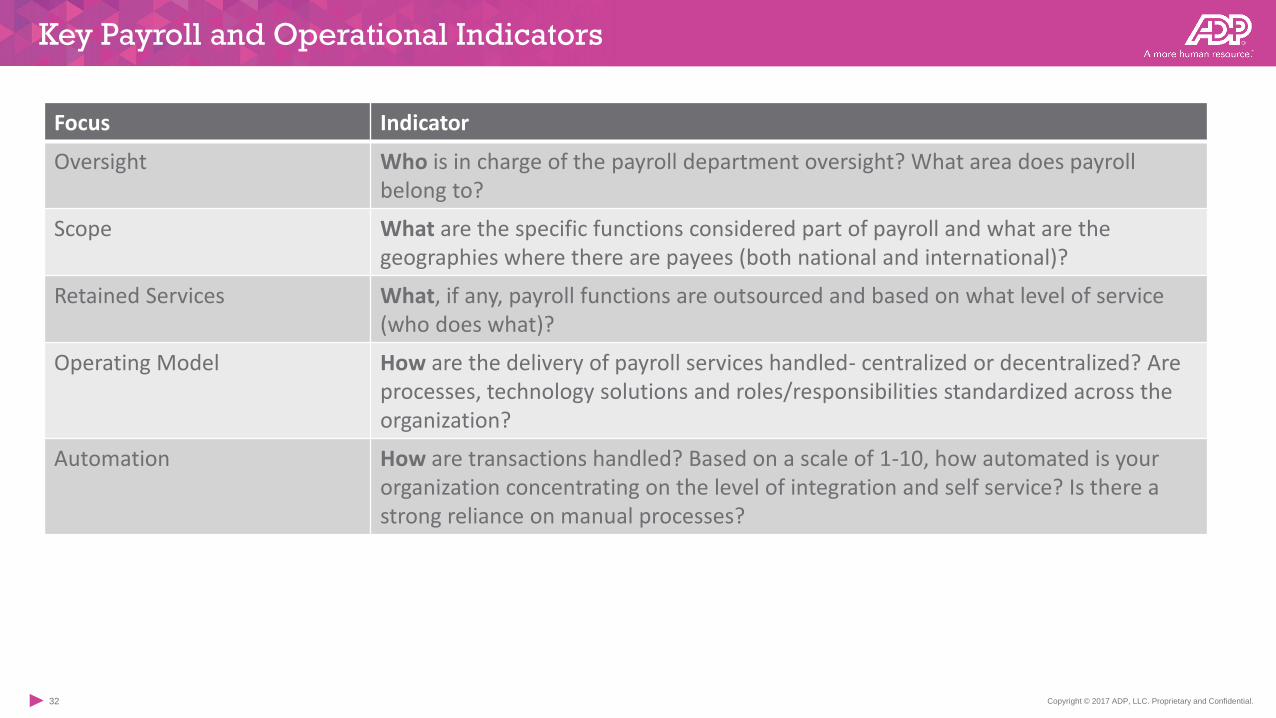

Key Payroll and Operational Indicators

Focus Indicator

Oversight Who is in charge of the payroll department oversight? What area does payroll belong to?

Scope What are the specific functions considered part of payroll and what are the geographies where there are payees (both national and international)?

Retained Services What, if any, payroll functions are outsourced and based on what level of service (who does what)?

Operating Model How are the delivery of payroll services handled- centralized or decentralized? Are processes, technology solutions and roles/responsibilities standardized across the organization?

Automation How are transactions handled? Based on a scale of 1-10, how automated is your organization concentrating on the level of integration and self service? Is there a strong reliance on manual processes?

33 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

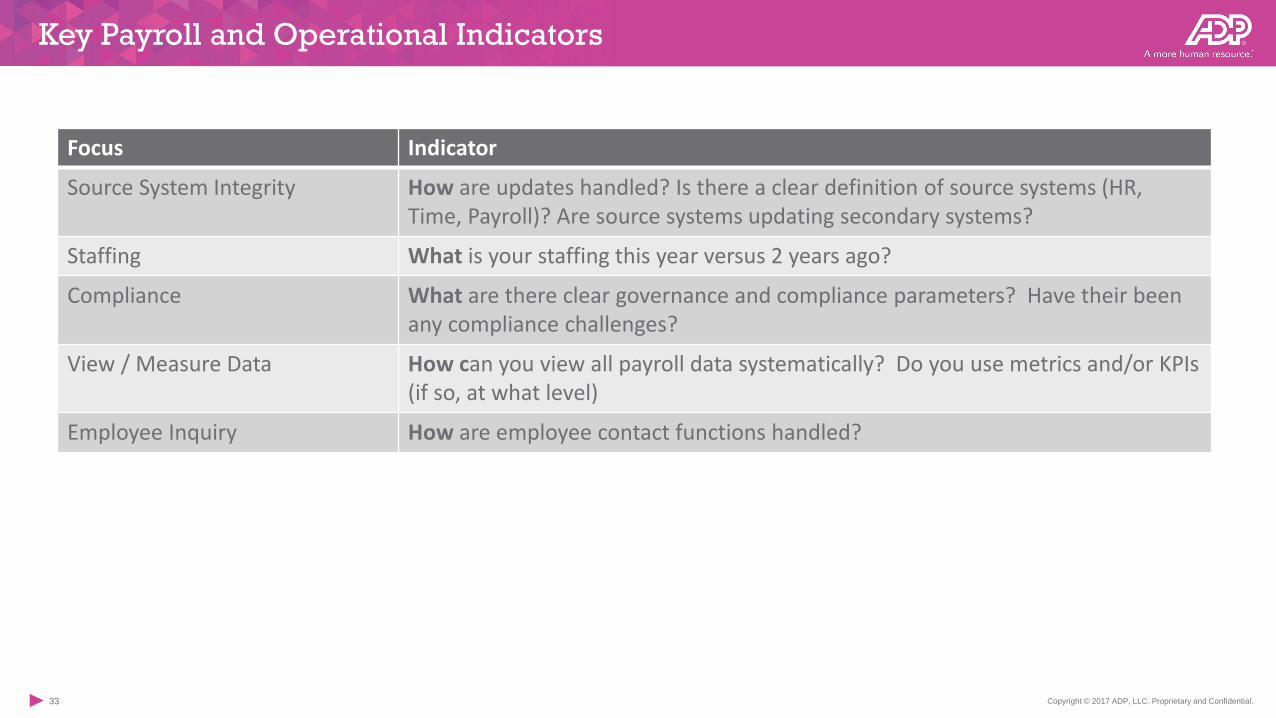

Key Payroll and Operational Indicators

Focus Indicator

Source System Integrity How are updates handled? Is there a clear definition of source systems (HR, Time, Payroll)? Are source systems updating secondary systems?

Staffing What is your staffing this year versus 2 years ago?

Compliance What are there clear governance and compliance parameters? Have their been any compliance challenges?

View / Measure Data How can you view all payroll data systematically? Do you use metrics and/or KPIs (if so, at what level)

Employee Inquiry How are employee contact functions handled?

34 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

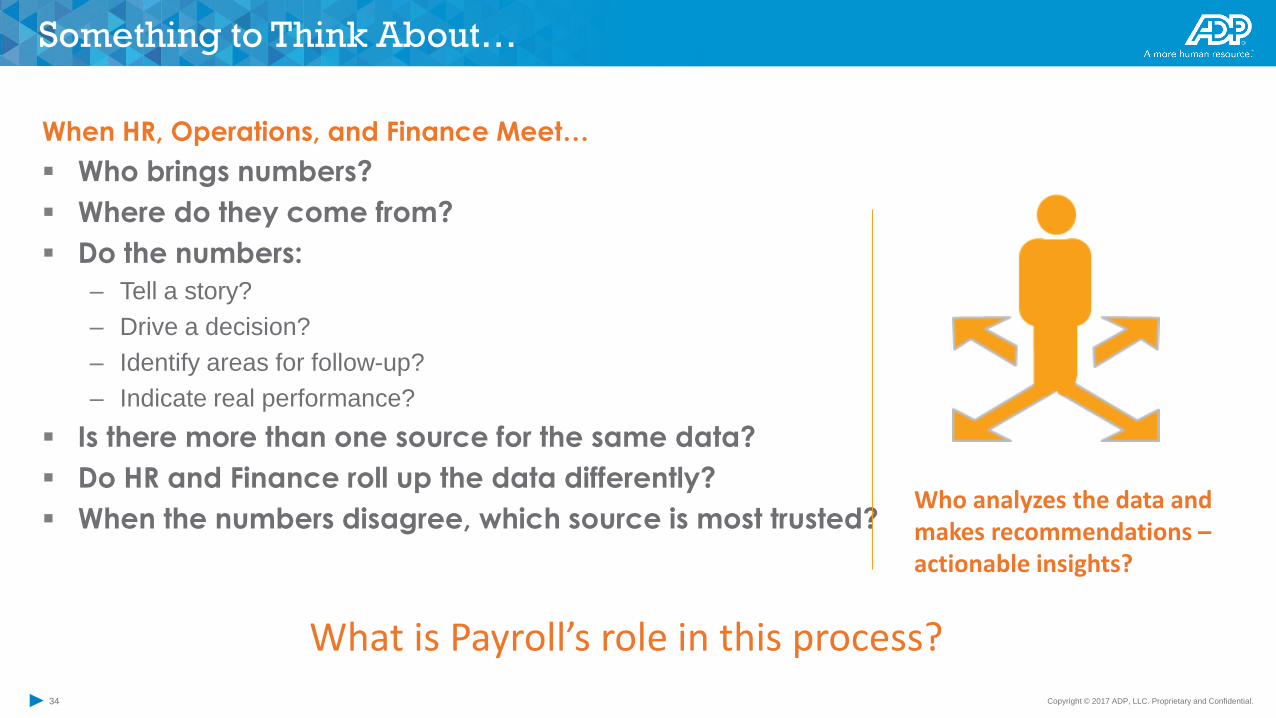

Something to Think About…

When HR, Operations, and Finance Meet…

Who brings numbers?

Where do they come from?

Do the numbers:

– Tell a story?

– Drive a decision?

– Identify areas for follow-up?

– Indicate real performance?

Is there more than one source for the same data?

Do HR and Finance roll up the data differently?

When the numbers disagree, which source is most trusted?Who analyzes the data and makes recommendations –actionable insights?

What is Payroll’s role in this process?

35 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Key Considerations

Payroll calendar for new year

Holiday schedule

FLSA/Wage and Hour changes

Paid sick leave laws related updates

Quarterly and year end audits and reconciliations

W-2s preparedness and mailing

Promote eW-2’s

New W-4s for employees exempt from withholding

Encourage direct deposits/pay card*

Understanding your paycheck -- Employee communication and education

ACA reporting/filing

Open enrollment

AND more…

36 Copyright © 2017 ADP, LLC. Proprietary and Confidential.

Next Steps

Evaluate your current policies, process, and compliance risks

Is there a need for change? If yes, determine steps to start

Create an execution plan

Manage and communicate change

Stay tuned for regulatory updates

Thank You!