patient protection and affordable care act...

TRANSCRIPT

Patient Protection and Affordable

Care Act (PPACA)

Rex R. Schultze Perry Law Firm (402) 476-9200

Patient Protection and Affordable Care Act (PPACA)

• Patient Protection and Affordable Care Act (PPACA) Summary – after a series of debates, the Health Care Reform Bill was passed into law on March 23, 2010.

• Effective date of January 1, 2014 just under a year away.

• Employers (private and public) are “positioning” themselves to meet or “AVOID” the requirements (penalties) under the Act

PPACA Positioning

PPACA Positioning • Wendy’s • “A Wendy’s fast-food franchise in Nebraska is

cutting the hours of non-management employees so its owners won't be required to pay health benefits . . . because [the owner] cannot afford to pay health insurance for all his employees. ”

• MSN Money, January 9, 2013, http://money.msn.com/now/post.aspx?post=06a08990-82fd-47e6-bbd6-e23824f93591

PPACA Positioning •Wendy’s “has announced that all non-management positions will have their hours reduced to 28 a week.” •“Cuts are coming because the new Affordable Health Care Act requires employers to offer health insurance to [full-time] employees” •- WOWT, January 7, 2013, http://www.wowt.com/home/headlines/Fast-Food-Worker-Hours-Cut---185827392.html

PPACA Positioning •“About 100 Wendy’s workers in Omaha have been told their hours are being cut.” •Wendy’s spokesperson: "As small-business employers, our franchisees are facing rising food and operating costs and many new government regulations.“ •- Huffington Post, January 7, 2013, http://www.huffingtonpost.com/2013/01/07/wendys-obamacare_n_2425066.html?ncid=edlinkusaolp00000003&ir=Business

PPACA Positioning •Reportedly, “Wendy's restaurants in Arkansas and Idaho are undertaking similar measures as those taken in the Omaha Wendy's” •- Huffington Post, January 7, 2013, http://www.huffingtonpost.com/2013/01/07/wendys-obamacare_n_2425066.html?ncid=edlinkusaolp00000003&ir=Business

PPACA Positioning Taco Bell

“A Taco Bell in Guthrie, Oklahoma cut its full-time employees' hours down to 28 hours a week (and lower) in order to avoid paying for their health insurance under the Affordable Care Act” Opposing Views, January 8, 2013 http://www.opposingviews.com/i/money/jobs-and-careers/video-taco-bell-cuts-employees-hours-avoid-paying-health-care

PPACA Positioning • Today – Our objective is to:

– Inform School District employers of the current PPACA law and regulations;

– Discuss application of the requirements of the act and associated penalties; and,

– Provide approaches to positioning school district employers to make choices with regard to:

• Employee compensation, benefits, services and hours; • School district operation, including education

programming, and school schedule and term.

• IT’S ALL ABOUT THE ECONOMICS!!!

Patient Protection and Affordable Care Act (PPACA)

• Our presentation is a general analysis of the impact of the Patient Protection and Affordable Care Act (PPACA or “the Act”) on current health insurance plans and the provision of fringe benefits to both certificated and classified employees of Nebraska school districts.

• Each school district will need to conduct a specific analysis of the structure of compensation for both certificated and classified employees!!!!

Introduction: General Overview

• General Overview of Act: • As a point of beginning, PPACA’s shared responsibility

provisions require an applicable large employer (having 50 or more full-time employees, including full-time equivalent employees) to pay a penalty (called an “assessable payment” by the regulations) if either: – (1) the employer fails to offer its full-time employees (and their

dependents) the opportunity to enroll in minimum essential coverage under an employer-sponsored plan and any full-time employee is certified to the employer as having received a premium tax credit or cost-sharing reduction, or

– (2) the employer offers minimum essential coverage, but one or more full-time employees is certified to the employer as having received the premium tax credit or cost sharing reduction because the coverage is not “affordable” or does not provide “minimum value.”

Introduction: General Overview

• General Overview of Act: • Employers need only to cover full-time employees, not full-

time equivalent employees, for the purposes of the Shared Responsibility provisions. In other words, employers will only face penalties for not providing coverage to full-time employees. Employers will not be penalized for not covering non-full-time employees (any employees working less than, on average, 30 hours per week).

The Threshold Standards: Does the Act Apply to You?

• Number of Full-Time Employees: The threshold question for determining whether a school district employer is subject to the shared responsibility provisions of the PPACA is the following: “Does the school district have 50 “full-time” employees?”

• If a district does not meet the 50 employee threshold, the district will NOT be subject to the shared responsibility provisions.

The Threshold Standards: Does the Act Apply to You?

• The 50 Full-Time Employee Calculation: Under the PPACA, “full-time employee” is defined as an employee who has at least 30 hours of service per week, or under proposed guidance, 130 hours of service in a calendar month. – (1) Excluded from the calculation: full-time seasonal

employees who work less than 120 days during the calendar year;

– (2) Included in the calculation: part-time employees (i.e. those working less than 30 hours per week) on a monthly basis by taking their total number of hours worked and dividing by 120.

The Threshold Standards: Does the Act Apply to You?

• The Summary Information to the proposed PPACA regulations provide very specific and clear guidance on this issue: – “Solely for purposes of determining whether an employer is an applicable large

employer for the current calendar year, section 4980H(c)(2)(E) provides that the employer must calculate the number of full-time equivalent employees (FTEs) it employed during the preceding calendar year and count each FTE as one full-time employee for that year. The proposed regulations apply this provision using the calculation method for FTEs that was included in Notice 2011-36. Under that method, all employees (including seasonal workers) who were not full-time employees for any month in the preceding calendar year are included in calculating the employer's FTEs for that month by (1) calculating the aggregate number of hours of service (but not more than 120 hours of service for any employee) for all employees who were not employed on average at least 30 hours of service per week for that month, and (2) dividing the total hours of service in step (1) by 120. This is the number of FTEs for the calendar month.

The Threshold Standards: Does the Act Apply to You?

• The Summary Information to the PPACA regulations provide very specific and clear guidance on this issue: – “In determining the number of FTEs for each calendar month, fractions

are taken into account. For example, if for a calendar month employees who were not employed on average at least 30 hours of service per week have 1,260 hours of service in the aggregate, there would be 10.5 FTEs for that month. However, after adding the monthly full-time employee and FTE totals, and dividing by 12, all fractions would be disregarded. For example, 49.9 full-time employees (including FTEs) for the preceding calendar year would be rounded down to 49 full-time employees (and thus the employer would not be an applicable large employer in the current calendar year).”

See pages 21 ands 22 of the PPACA Supplemental Information.

The Threshold Standards: Does the Act Apply to You?

• For example – A school has 20 employees who all work 24 hours per week or 96 hours per month; these 20 part-time employees would be counted as 16 full-time equivalent employees (20 employees x 96 hours = 1920 ÷ 120 hours = 16).

• See, Appendix 1 – Large Employer or Small Employer Example Calculation

Seasonal Workers • What about seasonal workers?

– “Employment pertains to or is of the kind exclusively performed at certain seasons or periods of the year and which, from its nature, may not be continuous or carried on throughout the year.”

– Example: Non-Teacher Coaches, Summer Workers. – If your School District is close to at the 50

employee threshold, you should consult with your legal counsel as to how to deal with and possibly count the “seasonal employees.”

– See, Appendix 2 – Seasonal Workers discussion.

The Threshold Standards: Does the Act Apply to You?

• If a district does not meet the 50 full-time employee threshold, the district will not be subject to the requirement to provide affordable health coverage to full-time employees that provides minimum value, and will face no penalties.

The Threshold Standards: It Applies to You! Now What?

• For purposes of this presentation, we assume that the districts are “applicable large employers,” meaning the districts have at least 50 full-time employees, and will be subject to the PPACA.

• Appendix 3 - §4980H(a) Large Employer Determination Calculation

PPACA – Effective Date

• The requirements and potential penalty provisions of the Act become effective January 1, 2014.

• As noted above, employers are already positioning themselves to avoid the costs of providing health insurance coverage from some employees or the penalties for not providing same.

Acceptable /Minimum Value Health Care

• The PPACA’s primary purpose is to provide all Americans with adequate (acceptable and affordable) health insurance coverage: – The School District will need to ensure that the

coverage offered provides minimum (adequate) value.

– The “adequate” standard is described as health insurance coverage plan that pays for 60% or more of covered health care expenses.

– Insurance companies should inform Employers whether the insurance coverage provides minimum value.

Acceptable and Affordable Health Care

– The adequate component of the PPACA has been referred to as the “Essential Health Benefits Package.”

– The PPACA “essential health benefits package” must include coverage for specified services or care. – See, Appendix 1.

– Further, such plans may not have a deductible greater than $2,000 annually for self only coverage or $4,000 for any other level of coverage in 2014 (subject to adjustment thereafter), with cost sharing not in excess of that provided for health savings accounts under high deductible plan currently.

Offering Coverage • Offer of coverage: An applicable large employer

member will not be treated as having made an offer of coverage to a full-time employee for a plan year if the employee does not have an effective opportunity to elect to enroll (or decline to enroll) in the coverage no less than once during the plan year.

• The IRS will probably need to clean-up this language, as no insurance carrier provides open enrollment during a plan year,; rather open enrollments are offered within a short time prior to the plan year.

Offering Coverage • Whether an employee has an effective opportunity is

determined based on all the relevant facts and circumstances, including adequacy of notice of the availability of the offer of coverage, the period of time during which acceptance of the offer of coverage may be made, and any other conditions on the offer.

• Solved by EHA “Open Enrollment” period for 2013-2014.

Acceptable and Affordable Health Care

• We assume the current EHA “Employee” level coverage provides all of the essential health benefits required by the PPACA, but the District should seek confirmation from EHA.

• However, in discussions with the EHA liaison, it does not appear that the EHA has yet developed a “Bronze” plan at a lower cost than the current EHA plans that could be made available to non-certificated employee groups.

Acceptable and Affordable Health Care

• The PPACA calls for creation of varying levels of coverage denominated bronze, silver, gold or platinum, with Bronze level coverage providing for the lowest 60% of the actuarial value of essential health benefits.

• The actuarial value of a health plan is a measure of the percentage of health care costs, on average, that the plan is expected to cover.

Essential Health Benefits

Package • Essential Health Benefits Package

• PPACA requires that coverage include at least the following: • 1. ambulatory patient services; • 2. emergency services; • 3. hospitalization; • 4. maternity and newborn care; • 5. mental health and substance use disorder services,

including behavioral health treatment; • 6. prescription drugs; • 7. rehabilitative and habilitative services and devices;

Essential Health Benefits

Package • Essential Health Benefits Package

• 8. PPACA also requires health plans that offer insurance coverage in the individual and small group markets to ensure that such coverage

• 9. laboratory services; • 10. preventive and wellness services and chronic disease

management; and • 11. pediatric services, including oral and vision care. • PPACA also permits insurers to offer a catastrophic health

plan in the individual market for (1) young adults under age 30 and (2) people who are exempt from the individual mandate (discussed below).

Affordable Health Care Coverage

• Affordable Coverage: The health insurance plan offered by the School District must be affordable.

• The test for affordability evaluates whether the employee’s required contribution with respect to the plan exceeds 9.5% of the employee’s household income.

• The employee’s required contribution means the portion of the annual premium which would be paid by the individual, without regard to whether paid through salary reduction or otherwise, for self-only coverage.

Affordable Health Care Coverage

• Household income is measured by the modified adjusted gross income of employee and any members of the household who are required to file an income tax return.

• However, since an employee’s household income is likely unknown to the employer, the IRS has suggested the use of a safe harbor for determining whether coverage is affordable.

Affordable Health Care Coverage

• Under the safe harbor, each employee’s portion of the self-only premium for the lowest cost coverage (i.e., the employee contribution) would need to be less than 9.5% of the employee’s W-2 wages at the end of the calendar year.

W-2 Safe Harbor

To be affordable, an employee cannot contribute more than 9.5% of this amount

Federal W-2 Form

Affordability Line

• Salary > Affordability Line - Teachers: – Based upon 2013-2014 EHA rates for Employee

level health insurance coverage (without dental) the “Affordability Line” would be as follows:

Deductible Annual Health

Premium ÷ 9.5% Max. Employee Contribution

X 100 to annualize

Affordability Line Salary

$500 $6,515.28 ÷ 9.5 100 $68,581.89

$750 $6,177.60 ÷ 9.5 100 $65,027.37

$1,650 $5,212.20 ÷ 9.5 100 $54,865.26

Affordability Line

• Salary > Affordability Line – Classified Example: Based upon 2013-2014 EHA rates for Employee level health insurance coverage (without dental) the “Affordability Line” would be as follows assuming district pays ½ Employee (self-only) coverage:

Deductible Annual

Health Premium

District Contrib ½ Employee level coverage

÷ 9.5% Max. Employee Contribution

X 100 to annualize

Affordability Line Salary

$500 $6,515.28 $3,257.64 ÷ 9.5 100 $34,290.95

$750 $6,177.60 $3,088.80 ÷ 9.5 100 $32,513.68

$1,650 $5,212.20 $2,606.10 ÷ 9.5 100 $27,432.63

Affordable Health Care Coverage

• The employer could make the calculation based on budgeted income and contributions at the beginning of the year.

• For example, for 2014, the School District would determine whether it met the proposed affordability safe harbor for 2014 by looking at each employee’s anticipated W-2 wages for 2014 and comparing 9.5% of that amount to the employee’s 2014 employee contribution.

Full-Time Employee under PPACA

• The next inquiry is whether an individual employee is a “full-time employee” to whom the PPACA applies.

• Again, a “full-time employee” is defined as an employee who has at least 30 hours of service per week, or under proposed guidance, 130 hours of service in a calendar month.

The “Look-Back” Rule • The “Look-Back/Stability Period” (Look-Back) safe

harbor instructs employers on how to determine which employees are “full-time employees” under that Act and, therefore, must be provided “affordable” health insurance coverage that provides “minimum value” by the employer.

The “Look-Back” Rule • The Look-Back safe harbor allows an employer to

determine each ongoing employee’s full-time status (or not) by looking back at a defined period of not less than three but not more than 12 consecutive calendar months as chosen by the employer. Under the “look-back” test, any employee who works, on average, 30 hours per week, 130 hours per month and 1,560 hours per calendar year qualifies as a full-time employee. [Prop. Reg. 54.4980H-3(c)(1)(i)].

The “Look-Back” Rule • Again, employers need only to cover full-time

employees, not full-time equivalent employees, for the purposes of the Shared Responsibility provisions. In other words, employers will only face penalties for not providing coverage to full-time employees. Employers will not be penalized for not covering non-full-time employees (any employees working less than, on average, 30 hours per week).

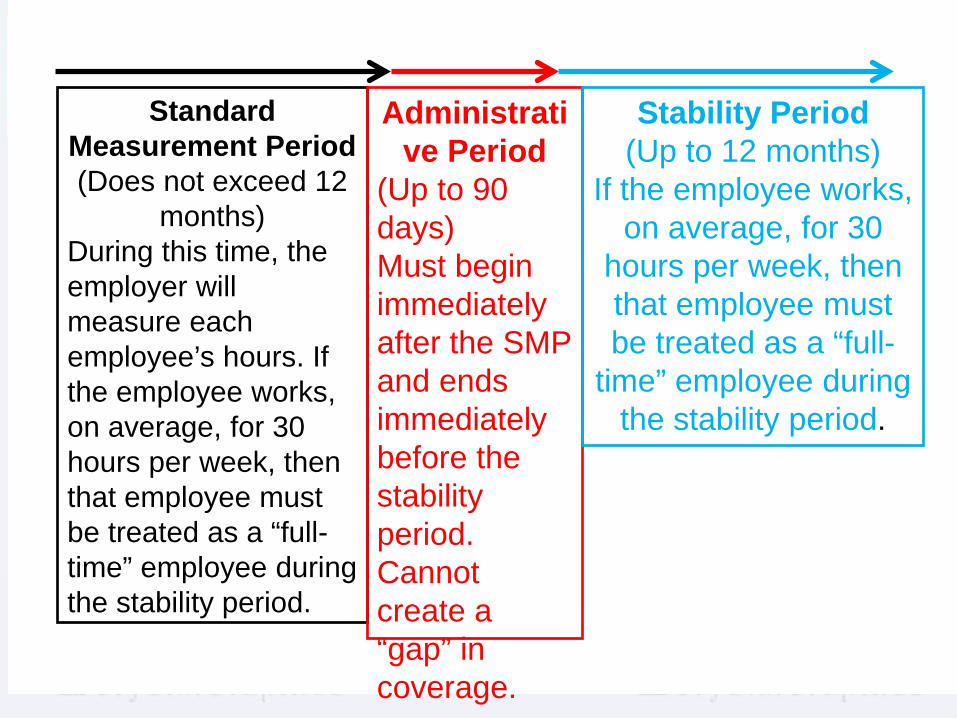

Standard Measurement Period (Does not exceed 12

months) During this time, the employer will measure each employee’s hours. If the employee works, on average, for 30 hours per week, then that employee must be treated as a “full-time” employee during the stability period.

Administrative Period

(Up to 90 days) Must begin immediately after the SMP and ends immediately before the stability period. Cannot create a “gap” in coverage.

Stability Period (Up to 12 months)

If the employee works, on average, for 30

hours per week, then that employee must be treated as a “full-

time” employee during the stability period.

The “Look-Back” Rule: Educational Employees

• Special Rules for Application of “Look-Back” Rule to Educational Institution Employers: – In the regulations and supplemental commentary

issued on December 28, 2012, the IRS identified the issue of teachers and other employees who work for part of the year, and have extended periods during a calendar year when school is not in session, e.g. summer months. In the proposed regulations, the IRS addressed these concerns. In fact, the IRS developed special rules for teachers and “other employees of educational organizations”.

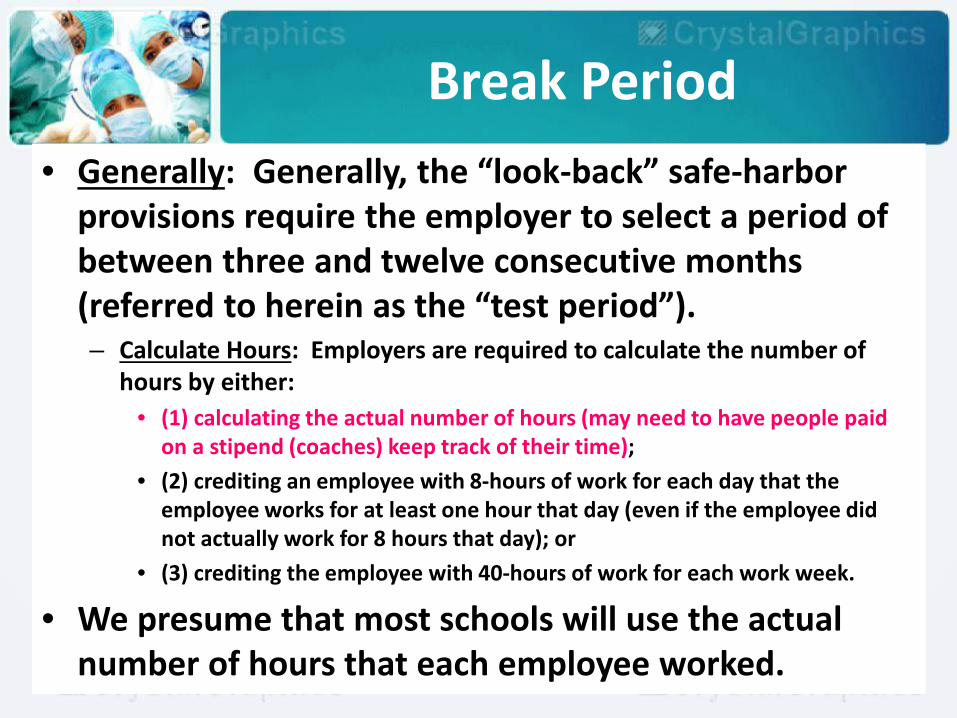

Break Period • Generally: Generally, the “look-back” safe-harbor

provisions require the employer to select a period of between three and twelve consecutive months (referred to herein as the “test period”). – Calculate Hours: Employers are required to calculate the number of

hours by either: • (1) calculating the actual number of hours (may need to have people paid

on a stipend (coaches) keep track of their time); • (2) crediting an employee with 8-hours of work for each day that the

employee works for at least one hour that day (even if the employee did not actually work for 8 hours that day); or

• (3) crediting the employee with 40-hours of work for each work week.

• We presume that most schools will use the actual number of hours that each employee worked.

Break Period • Can Use Different Method for Different Groups of Employees:

Employers are not required to use the same method for all employees, so long as the distinctions between employees are reasonable and consistently applied; e.g. treat teachers and para-educators differently.

• Calculate Actual Hours Worked During Test Period (3 to 12 months): Once the employer has selected a method for counting hours and chosen a test period, employers must then actually calculate each employee’s average number of hours worked during that test period.

• Break Period: “To Count or Not to Count – That is the Question”: In this calculation, schools will not be required to count “any employment break period” or could elect to count the “employment break period.”

Break Period • Break Period: The regulations define a “break period” as “a

period of at least four consecutive weeks . . . during which an employee of an educational organization is not credited with hours of service . . .”

• Work Weeks Excluded From Break Period: The definition of “break period” provides that a week where an employee performs work will not be included in the break period calculation. The proposed regulations provide examples, and one example confirms that break periods do not include weeks when an employee performs work.

• Appendix 4 – Supplementary Information and Proposed PPACA Regulations on “Break Period.”

Break Period – Therefore, school districts that start classes on a Thursday will be

allowed to count that entire week for purposes of each employee’s test period.

– Employers must use each employee’s average hours during the test period as the average for the entire measurement period.

• Winter/Spring Breaks: Still Can be Counted as Work Weeks: As they are not four consecutive weeks in durations, winter break, spring break, and other short-term breaks will still count in calculating each employee’s average hours of work per week during the test period.

The “Look-Back” Rule: Educational Employees

• For employees of educational organizations, the IRS determined in Prop. Treas. Reg. 54.4980H-3(e)(4), that when calculating whether an employee is a “full-time” employee subject to the PPACA shared responsibility provisions, an employer can either: – (A) elect to not count the Summer months (called a “break period,” as

defined above) by considering whether the employee averaged at least 30 hours per week during the school year rather than the full 12-month period; or

– (B) elect to calculate the average of the hours worked per week (a period decided at the discretion of the employer – which will be approved if reasonable) during the school term and deem the employee to have earned that average for the break period.

The “Look-Back” Rule: Educational Employees

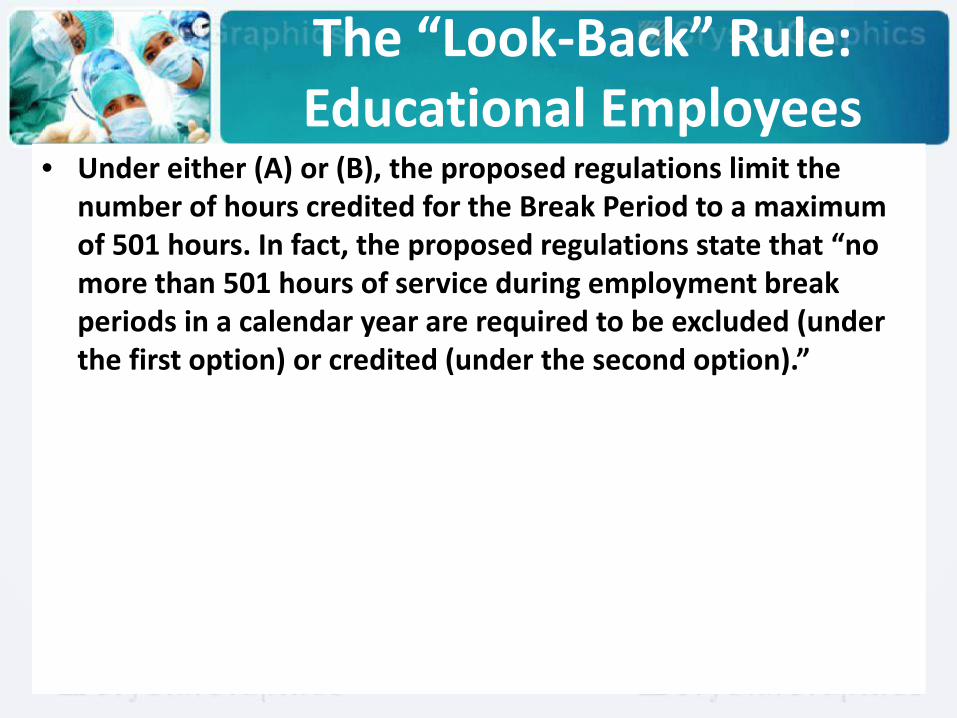

• Under either (A) or (B), the proposed regulations limit the number of hours credited for the Break Period to a maximum of 501 hours. In fact, the proposed regulations state that “no more than 501 hours of service during employment break periods in a calendar year are required to be excluded (under the first option) or credited (under the second option).”

The “Look-Back” Rule: Educational Employees

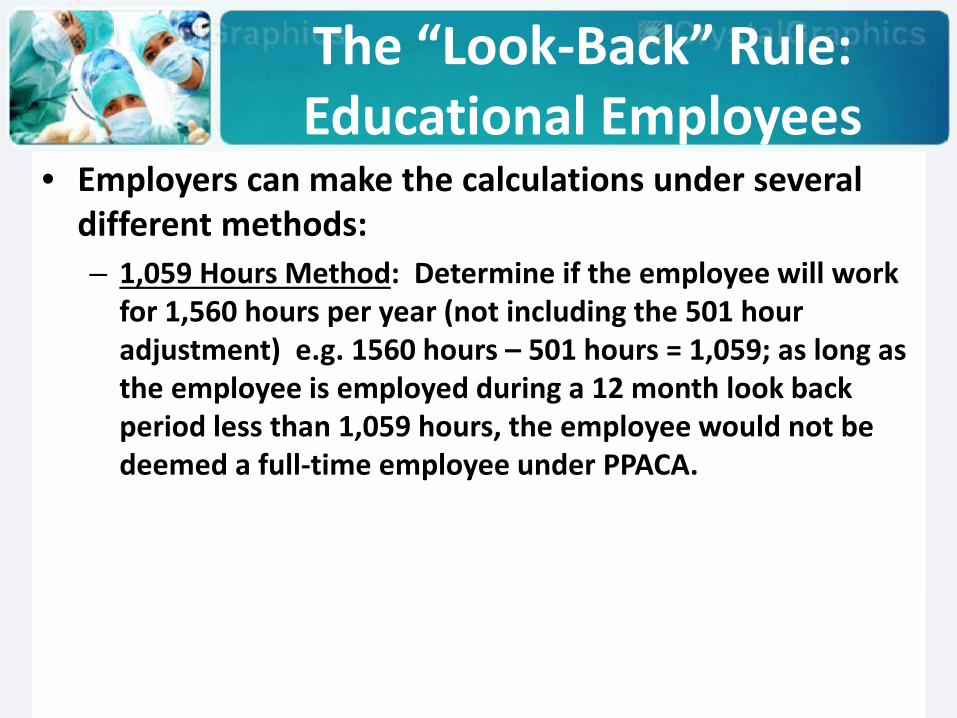

• Employers can make the calculations under several different methods: – 1,059 Hours Method: Determine if the employee will work

for 1,560 hours per year (not including the 501 hour adjustment) e.g. 1560 hours – 501 hours = 1,059; as long as the employee is employed during a 12 month look back period less than 1,059 hours, the employee would not be deemed a full-time employee under PPACA.

The “Look-Back” Rule: Educational Employees

• Employers can make the calculations under several different methods: – Hours Per Week Method: Determine whether an employee averages 30

hours per week. In order to calculate whether an employee averages 30 hours per week, the school district will first need to determine how many “working weeks” apply.

– If an employee works during a given week, that week will not be included in the break period. Instead, that entire week will be counted as part of the school year; e.g. school districts that start classes on a Thursday and finish the year on a Tuesday will be able to count those two full weeks in their school year “test period.”

NOTE: Why is this important? Because the regulations instruct employers to determine each employee’s full-time status based on average number of hours per week. Thus, the more weeks counted, the lower the average number hours per week.

Calculating Full-Time Employees

• How to calculate “full-time” employees under weekly hour method: – Add the number of weeks (from start to finish) from the

first day of work to the last day of work; – Count the total number of hours that the employee will

work during that period; – Divide the number of hours by the number of weeks; and, – If the number is less than 30 hrs/wk, that employee is not

full-time.

Calculating Full-Time Employees

• How to calculate “full-time” employees under 1,059 hour method: – Add the number of hours that an employee works during

the year: • If this number is less than 1,059: part-time. • If this number is more than 1,059: full-time, or,

– Number of weeks worked divided the number of hours worked = average per week to be used in the look-back period selected by the employer.

• Key - Addressing in 2013-2014 full-time employment status of classified employees (paras, food service, custodians, clerical, bus drivers) to provide result desired during look-back (3 month to 12 months).

The “Look-Back” Rule: Educational Employees Example 1: 40-week school year

Position Contract Days Hours

Per Day

Total Hours During School

Year

Number of Weeks in

School Year

Average Hours per

Week

Full-Time Employee Status?

Teacher 185 8 1,480 hours 40 37 Yes Teacher 182 8 1,456 hours 40 36.4 Yes Teacher 180 8 1,440 hours 40 36 Yes

Para 185 6 1,110 Hours 40 27.75 No Para 180 6 1,080 Hours 40 27 No Para 175 6 1,050 hours 40 26.25 No Cook 185 5 925 hours 40 23.13 No Cook 180 5 900 hours 40 22.5 No Cook 175 5 875 hours 40 21.88 No

The “Look-Back” Rule: Educational Employees Example 2: 37-week school year

Position Contract Days Hours

Per Day

Total Hours During School

Year

Number of Weeks in

School Year

Average Hours per

Week

Full-Time Employee Status?

Teacher 185 8 1,480 hours 37 40 Yes Teacher 182 8 1,456 hours 37 39.4 Yes Teacher 180 8 1,440 hours 37 38.9 Yes

Para 185 6 1,110 Hours 37 30 Yes Para 180 6 1,080 Hours 37 29.2 No Para 175 6 1,050 hours 37 28.4 No Cook 185 5 925 hours 37 25 No Cook 180 5 900 hours 37 24.3 No Cook 175 5 875 hours 37 23.6 No

Appendix 5 - §4980H(b) Full-Time Employee Determination Charts

New Employees • What about new employees?

– If a new hire is “reasonably expected” to work full-time, then the employer may wait up to three months from the date of hire to offer coverage.

– Employer will not be penalized during this three month period.

– Once a new employee has been employed for the entire measurement period (3 months), the employer must determine whether the employee is full-time.

New Employees • What about new employees?

– If employee is determined to be full-time employee during measurement period, that employee must be treated as full-time employee during the entire stability period (even if the employee does not work 30 hrs/wk during the stability period).

– If employee is determined not to be full-time employee during measurement period, but works 30 hrs/wk during stability period, then the employer must treat employee as full-time

– After the stability period: employer can determine the employee’s full-time status like all other employees.

New vs. Continuing Employee • Prop. Reg. 54.4980H-3(e)(1)(i) addresses whether employees

who return to work after an absence will be classified as either a “continuing” employee or “new” employee. For purposes of the regulations, a “new” employee will be treated as being “terminated and rehired” by the employer.

• This distinction is important because employers must take certain steps after hiring a “new” employee (the same steps that the employer must take when hiring other new employees).

New vs. Continuing Employee • The regulations set forth two bright-line tests for determining

whether an employee will qualify as a “new” or “continuing” employee. – The first test measures whether the employee worked at least one hour

over the 26-week period immediately preceding the employee’s return to work. If an employee does not work at least one hour during that period, that employee will automatically be treated as a “new” employee. Prop. Reg. § 54.4980H-3(b)(2).

– The second test measures whether an employee’s absence lasted for at least four weeks and the period of absence is longer than the amount of time the employee worked before the break. Prop. Reg. § 54.4980H-3(b)(2). In other words, under the second test, an employee will be deemed “terminated and rehired” if, for example, an employee worked for 8 weeks, then takes a 12-week break, then returns to work.

New vs. Continuing Employee • The break period rules for employees of educational

organizations only apply to “continuing” employees. In other words, no employer will need to worry about calculating break periods for employees who either (a) do not work for a consecutive 26-week period; or (2) take an absence of at least four weeks which is at least one week in excess of their employment immediately prior to the absence.

• For coaches who only coach for a limited period of time, many of these coaches would automatically considered to be “new” employees under the regulation’s first test if the coaches do not work for at least 26 weeks after their season ends.

New vs. Continuing Employee • The first test is not elective—employees who do not work for

26-consecutive weeks will automatically be deemed “new” employees. However, if a coach performs services during the off-season (or at some point during the 26-week period), then the School District must disregard the employment break periods and credit up to 501 hours of service. Prop. Reg. § 54.4980H-3(e)(4).

• These coaches would only be a full-time employee if he or she performed more than 1059 hours of service during the 12-month period (1,560 hours – 501 hours).

Look-Back Rule: Anti-Abuse Rule

• Anti-Abuse Rule: We should note that the regulations inform that employers are not allowed to force employees to work on sporadic days “for the purpose of avoiding or undermining the application” of the rules.

• The regulations provide an example of a school requesting its employees to work one hour in a week for the sole purpose of evading the rules.

• Absent these examples of obvious abuse of the rules, the proposed regulations provide that employers who make a good faith effort to comply with the provisions will not be deemed to have abused the rules. [Prop. Treas. Reg. 54.4980H-3(e)(6)]

Penalties - §4980H Assessable Payment

• Section 4980H generally provides that an applicable large employer is subject to an “assessable payment” if either: – 4980H(a) – Adequate/Minimum Value: The employer fails to offer to its

full-time employees (and their dependents) the opportunity to enroll in minimum essential coverage (MEC) under an eligible employer-sponsored plan and any full-time employee is certified to the employer as having received an applicable premium tax credit or cost-sharing reduction (section 4980H(a) liability); or,

– (2) The employer offers its full-time employees (and their dependents) the opportunity to enroll in MEC under an eligible employer-sponsored plan and one or more full-time employees is certified to the employer as having received an applicable premium tax credit or cost-sharing reduction (section 4980H(b) liability). . . . .

Penalties - §4980H – Generally, section 4980H(b) liability may arise because, with respect to

a full-time employee who has been certified to the employer as having received an applicable premium tax credit or cost-sharing reduction, the employer’s coverage is unaffordable within the meaning of section 36B(c)(2)(C)(i) or does not provide minimum value within the meaning of section 36B(c)(2)(C)(ii).

• As noted, an employer may be liable for an assessable payment under section 4980H(a) or (b) only if one or more full-time employees are certified to the employer as having received an applicable premium tax credit or cost-sharing reduction.

Penalties • Penalty for Not Offering Coverage:

– Beginning in 2014, if the School District did not offer coverage to its full-time employees (or group thereof, e.g. classified employees) and one or more employees receives a premium credit under the PPACA, the School District would be assessed a monthly penalty equal to the number of full-time employees minus 30 multiplied by one-twelfth of $2,000 for any applicable month.

– If all Nebraska schools offer all of their full-time employees the opportunity to purchase insurance through the EHA group plan, these penalties would not be applicable to those schools.

Penalties • Penalty for Not Offering Coverage:

– Scenario A = The large employer does not offer coverage, but no full-time employees receive credits for exchange coverage. No penalty would be assessed (This is very unlikely in the context of a large employer).

– Scenario B = The large employer does not offer coverage, and one or more full-time employees receive credits for exchange coverage. The annual penalty calculation is simply the number of full-time employees minus 30, times $2,000. In this example (i.e., 50 full-time employees), the penalty would not vary if only one employee or all 50 employees received the credit; the employer’s annual penalty in 2014 would be (50 full-time employees -30) x $2,000, or $40,000.

95% Relief from Offer of Coverage Requirement

• The IRS recognized that the Section 4980H(a) language could impose a huge penalty on an employer which intended to offer coverage, but failed to do so for a few full-time employees.

• For example, assume the School District intended to offer coverage to all “full-time employees,” as defined by the statute.

• However, a dozen part-time maintenance workers (who were not offered health insurance coverage) averaged more than 30 hours per week during a year because of additional snow-removal efforts, and one of those employees received a premium subsidy for his or her coverage through the exchange.

95% Relief from Offer of Coverage Requirement

• The specific language of Code Section 4980H would impose a penalty of $2,000 times the total number of the district's full-time employees (minus 30 full-time employees).

• The Proposed Regulations establish the 95% standard to give relief from the Code Section 4980H(a) penalty to employers who are substantially complying with the statutory language. [Prop. Reg. § 54.4980H-5(a)]

• The relief applies to a failure to offer coverage to 5 percent of employees and their dependents (or if greater, 5 employees), regardless of whether the failure to offer was inadvertent.

Penalties • Penalty for Offering Non-Acceptable and/or Non-Affordable

Coverage: Beginning in 2014, if the School District offers coverage to its full-time employees but the dollar amount the employee (or group thereof, e.g. classified employees) is/are required to contribute toward the premiums for self-only (Employee) level coverage exceeds 9.5% of the employee’s household income (or, under the IRS safe harbor, the employee’s W-2 wages in box “1”, “Wages, tips, other compensation”), OR

Penalties • Penalty for Offering Non-Acceptable and/or Non-Affordable

Coverage: If the plan offered by the School District pays for less than 60% of covered expenses (not a problem if the School District’s group plan is the current EHA plan – but see discussion below about the need for a cheaper “60% Bronze Plan”), . . . .

Penalties • Penalty for Offering Non-Acceptable and/or Non-Affordable

Coverage: The School District would be assessed a monthly penalty for each full-time employee who receives a premium credit in the amount of one-twelfth of $3,000 for any applicable month.

• However, the total penalty for an employer would be limited to the TOTAL number of the School District’s employees minus 30 multiplied by one-twelfth of $2,000 for any applicable month.

Penalties

• It is this penalty that is the most likely to be assessed against a Nebraska school district for those employees that pay more than 9.5% of their W-2 wages toward the cost of self only (employee) level coverage premiums.

Penalties • Penalty for Offering Non-Acceptable and/or Non-

Affordable Coverage: – Scenario C = The employer offers coverage and no full-time

employees receive credits for exchange coverage. No penalty would be assessed.

– Scenario D = The employer offers coverage, but one or more full-time employees receive credits for exchange coverage. The number of full-time employees receiving the credit is used in the penalty calculation for an employer that offers coverage. The annual penalty is the lesser of the following:

• the number of full-time employees minus 30, multiplied by $2,000—or $40,000 for the employer with 50 full-time employees (i.e., 50 minus 30, multiplied by $2,000); or,

• the number of full-time employees who receive credits for exchange coverage, multiplied by $3,000.

Penalties • There will literally need to be a cost benefit calculation of the

penalties versus the ramifications of changes in the compensation structure.

• Unfortunately, the “wild card” number in the penalty calculation is the number of employees receiving the “premium credit.” – Our thought is that employees whoa re eligible for the premium subsidy

will take it because (1) the subsidy is generous, and (2) the subsidy counts toward family coverage when all of employer provided coverage is based upon “self-only” coverage.

• (Note that after 2014, the penalty amounts would be indexed by the premium adjustment percentage for the calendar years, e.g. if EHA rates go up 4% so would the penalties).

Employer Penalty Flowchart

• See, Appendix 6, the flow chart for potential penalties.

• http://healthreform.kff.org/~/media/Files/KHS/Flowcharts/employer__penalty_flowchart_1.pdf.

• See, Appendix 7, Employer Penalty Examples

PPACA – Effective Date

• Transition Relief: – Because many employers have “fiscal year” rather than

calendar year health insurance plans, the January 1, 2014 may require terms and conditions of coverage to change in the middle of a plan year, and may require compliance with the Act for a fiscal year beginning in 2013.

• EHA plans have a fiscal year of September 1 through August 31.

– To address this concern, the IRS in the Supplemental Information to the proposed regulations provided for “transition relief” from the enforcement of the PPACA penalty provisions.

PPACA – Effective Date

– Specifically, the IRS is taking the position that they will not enforce the 4980H (a) and (b) penalties for fiscal year plans that meet certain requirements; the text of the comments is a follows:

– “If an applicable large employer member maintains a fiscal year plan as of December 27, 2012, the relief applies with respect to employees of the applicable large employer member (whenever hired) who would be eligible for coverage, as of the first day of the first fiscal year of that plan that begins in 2014 (the 2014 plan year) under the eligibility terms of the plan as in effect on December 27, 2012. If an employee described in the preceding sentence is offered affordable, minimum value coverage no later than the first day of the 2014 plan year, no section 4980H assessable payment will be due with respect to that employee for the period prior to the first day of the 2014 plan year.”

– NOTE: The question is whether under the EHA BC/BS plans current employees or newly hired employees would be eligible for the 2014-2015 fiscal year plan (which begins September 1, 2014) under the eligibility terms of such plan in effect as of December 27, 2012?

Transition Relief – Method #1

– There are three ways that an employer can benefit from the transition relief rules:

• Method 1 – Eligibility Terms on December 27, 2012 Relief only applies to the employees of an applicable large employer who - (A) Would be eligible for coverage under the health plan on the first day of the fiscal year of the plan in 2014 under the eligibility terms as in effect on December 27, 2012, and (B) Are offered affordable coverage that meets the minimum value requirements no later than the first day of the 2014 Plan Year. Relief is that no 4980H(a) or (b) penalties will be due for that employee prior to the first day of the 2014 Plan Year. Note that the relief doesn’t apply if the employee is not offered affordable coverage on the first day of the plan year in 2014. An employer who will need to change the eligibility terms of its plan to cover additional employees (e.g., the plan currently excludes coverage for paras, but will be changed to permit coverage for paras who work at least 30 hours per week) will not be able to rely on this transition method with respect to those employees who are currently excluded.

Transition Relief – Method #2 • Method 2 – 25% Employees Covered Relief applies to the employees of an applicable large employer if – (A) The employer has at least 25% of its employees covered under one or more fiscal year plans that have the same plan year as of December 27, 2012 (employer may determine this percentage as of any date between October 31, 2012 and December 27, 2012), and (B) Full-time employees are offered affordable coverage that meets the minimum value requirements no later than the first day of the 2014 Plan Year, and (C) Full-time employees are not eligible for coverage under any group health plan maintained by the applicable large employer as of December 27, 2012 that has a calendar year plan year. Relief is that no 4980H(a) or (b) penalties will be due for that employee prior to the first day of the 2014 Plan Year. Note that the relief doesn’t apply if the employee is not offered affordable coverage on the first day of the plan year in 2014.

Transition Relief – Method #3 • Method 3 – 1/3 Offered Coverage Relief applies to the employees of an applicable large employer if – (A) The employer offered coverage under one or more fiscal year plans that have the same plan year as of December 27, 2012 to one-third or more of its employees during the most recent open enrollment period before December 27, 2012, and (B) Full-time employees are offered affordable coverage that meets the minimum value requirements no later than the first day of the 2014 Plan Year, and (C) Full-time employees are not eligible for coverage under any group health plan maintained by the applicable large employer as of December 27, 2012 that has a calendar year plan year. Relief is that no 4980H(a) or (b) penalties will be due for that employee prior to the first day of the 2014 Plan Year. Note that the relief doesn’t apply if the employee is not offered affordable coverage on the first day of the plan year. The IRS guidance only says “most recent” open enrollment. It does not specify that the open enrollment has occurred within a certain period of time.

Transition Relief • Transition Relief is not a “Get Out of Jail Free

Card!!!!

Transition Relief • To access Transition Relief and the September 1, 2014 penalty

exemption, a School District Employer must: – Provide MEC and Affordable coverage to “all” full-time

employees; • If a School District employer fails to take these steps, when

(and if) a full-time employee who is not provided MEC and/or affordable coverage, and applies for insurance through a government exchange, then penalties will be assessed from January 1, 2014.

• As such, it is essential to plan prior to or at least during 2013-2014 to make sure to which employees are to be “full-time” employees and provided an MEC and affordable coverage.

PPACA and Teacher Compensation Structures

• Structure of Teacher Compensation in Nebraska: – Insurance only schools – Full compliance with PPACA – NO

PENALTY FOR TEACHERS! – Insurance or Cash-in-lieu Schools – Likely full compliance

with PPACA – NO PENALTY FOR TEACHERS! – Cafeteria Plan Schools and Flat Salary Schools – NOT in

compliance with PPACA as it does not meet the requirements of “minimum essential coverage” – PENALTY FOR TEACHERS UNLESS STRUCTURE OF COMPENSATION IS CHANGED.

Patient Protection and Affordable Care Act (PPACA)

• There is particular focus on the structure of certificated teacher compensation in light of the collective bargaining negotiations time line set forth at Neb. Rev. Stat. § 79-818.01, which requires negotiations for the 2013-2014 contract year to begin November 1, 2012 and be completed by February 8, 2013.

Classified Employees • Same rules as teachers.

– The key is whether the employees are “Full-Time Employees.”

– Of particular import is the 3 to 12 month look-back. – No policy required for the “look-back” period, but you

would want to document that the School District is applying the 12 month look-back calculation.

Section 125 (FSA) Provisions

• $2,500 Limitation on health flexible spending plans – Notice 2012-40 - **Employers need to amend their Section 125 Plans to make this change. – Internal Revenue Code § 125(i), added by § 9005 of the PPACA, is effective for

taxable years following December 31, 2012, and requires Flexible Spending Arrangements (FSA) to provide that an employee may not elect to have salary reduction contributions exceeding $2,500 to the FSA for any taxable year.

– The $2,500 limit does not apply to any plan year beginning before 2013. Additionally, the limit does not apply to certain employer non-elective contributions (flex credits), to contributions or amounts available through reimbursement under other FSAs, health savings accounts, or health reimbursement arrangements, or to salary reduction contributions to cafeteria plans that are used to pay an employee’s share of health coverage premiums.

NOTE: “Taxable year” refers to the plan year of the cafeteria plan. Plans may amend their requirements in order to conform to Code § 125(i) anytime through the end of the 2014 calendar year, as long as the plan operates in accordance with Code § 125(i) for plan years beginning after December 31, 2012. Unused salary reduction contributions to a Health FSA which are carried over into a grace period for the next plan year will not count against the $2,500 limit for the subsequent plan year.

Non-Discrimination • IRS, DOL and HHS have suspended compliance with the

nondiscrimination rules applicable to insured plans – Notice 2011-1. – The agencies issued Notice 2011-1 on December 22, 2010. Notice 2011-

1 and suspended the new provisions of the Public Health Service Act (“PHSA”) which make nondiscrimination requirements applicable to fully insured plans (EHA Plans). It states that the Agencies anticipate that any new guidance will not apply until plan years beginning a specified period after its issuance, and that before the beginning of those plan years, insured group health plans will not be required to file IRS Form 8928 to report excise taxes resulting from violations of the new PHSA rules.

• Non-Discrimination rules relating to Section 125 Plans remain in effect for highly compensated employees.

Action Steps • Action Steps to take to comply with Health Reform

Act. – Include a Summary of Benefits and Coverage with EHA open

enrollment materials (likely provided by EHA). – Amend your Health FSA (Section 125) Plan to limit

employee contributions to $2,500 per year. – Employers with at least 250 W-2s for 2012 (issued in

January 2013) must report in Box 12, under Code DD, the value of health plan benefits provided to each employee.

Action Steps • Action Steps to take to comply with PPACA:

– Provide Notice to employees that exchanges will be available in 2014. Employers will have to provide a notice about the insurance exchanges to existing employees by March 1, 2013 and to all new hires that begin on or after March 1, 2013.

– Make staffing changes and/or adjustments (workers/hours) for the 2013-2014 school year this Spring, so that you have considered the application of the Shared Responsibility provisions in light of the “look-back” process as you prepare for the effective date of the act – January 1, 2014 or possibly September 1, 2014.

IRS Disclosure • IRS Circular 230 Disclosure: The Internal

Revenue Service requires us to inform you that any federal tax advice contained in this communication (including attachments or enclosures) should not be used or referred to in promoting, marketing or recommending of any entity, investment, plan or arrangement, and such advice is not intended or written to be used and cannot be used by a taxpayer for the purpose of avoiding penalties under the Internal Revenue Code.

Patient Protection and Affordable Care

Act (PPACA)

Rex R. Schultze Perry Law Firm (402) 476-9200