paper p6 (mla) - association of chartered certified … not more than six years old 17% vehicle more...

TRANSCRIPT

The Association of Chartered Certified Accountants

The Malta Institute of Accountants

Professional Level – Options Module

Time allowedReading and planning: 15 minutesWriting: 3 hours

This paper is divided into two sections:

Section A – BOTH questions are compulsory and MUST be attempted

Section B – TWO questions ONLY to be attempted

Tax rates and allowances are on pages 2–5

Do NOT open this paper until instructed by the supervisor.During reading and planning time only the question paper may be annotated. You must NOT write in your answer booklet untilinstructed by the supervisor.This question paper must not be removed from the examination hall.

Advanced Taxation(Malta)

Friday 7 December 2012

Pape

r P6 (

MLA

)

SUPPLEMENTARY INSTRUCTIONS1. You should assume that the tax rates and allowances shown below will continue to apply for the foreseeable future2. Calculations and workings need only be made to the nearest Euro3. All apportionments should be made to the nearest month unless stated otherwise4. All workings should be shown

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

Individual income tax rates

Resident individual tax ratesMarried couples – joint computation Other individuals€ €

0 – 11,900 0% 0 – 8,500 0%Next 9,300 15% Next 6,000 15%Next 7,500 25% Next 5,000 25%Remainder 35% Remainder 35%

Non-resident individuals€

0 – 700 0%Next 2,400 20%Next 4,700 30%Remainder 35%

Returned migrants

Married couples Others€ €

0 – 5,900 0% 0 – 4,200 0%Remainder 15% Remainder 15%

Capital allowances – Income Tax Act rates

Industrial buildings and structuresInitial allowance 10%Wear and tear allowance 2%

Plant and machineryWear and tear allowance as indicated in the question where applicable

Capital allowances – Business Promotion Act rates

Investment allowances Industrial buildings and structures 20%Plant and machinery 50%

Corporate income tax

Standard rate 35%

2

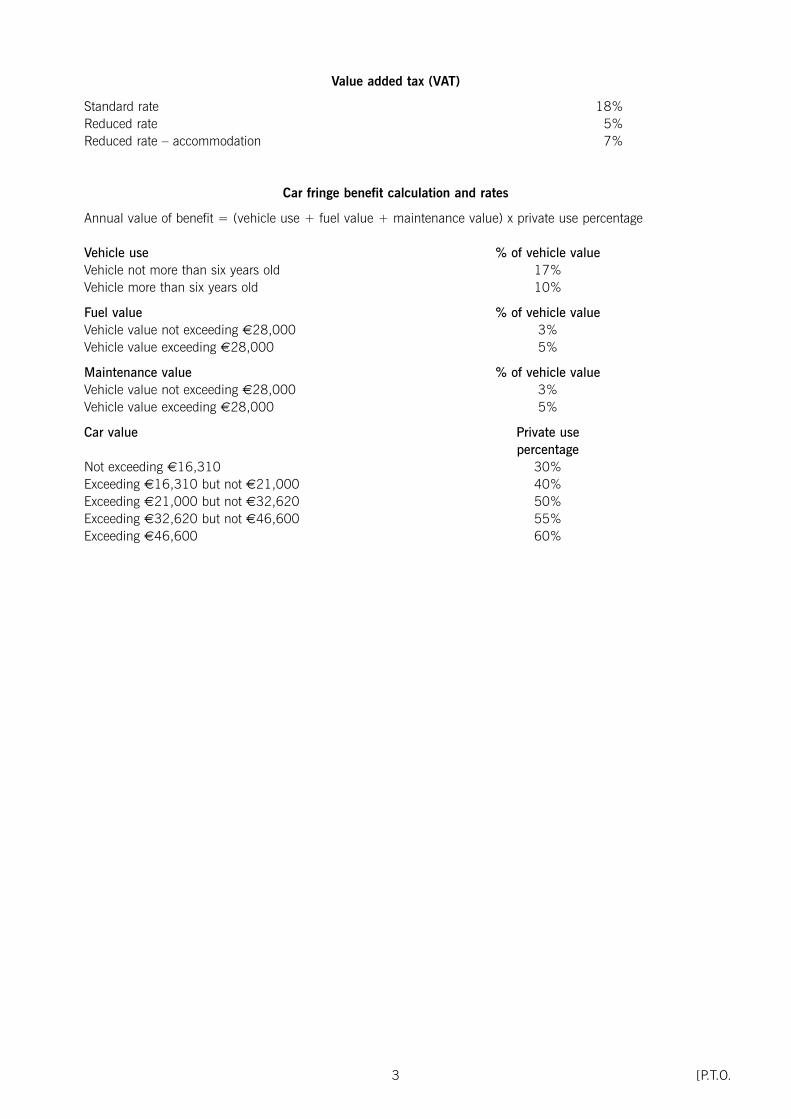

Value added tax (VAT)

Standard rate 18%Reduced rate 5%Reduced rate – accommodation 7%

Car fringe benefit calculation and rates

Annual value of benefit = (vehicle use + fuel value + maintenance value) x private use percentage

Vehicle use % of vehicle valueVehicle not more than six years old 17%Vehicle more than six years old 10%

Fuel value % of vehicle valueVehicle value not exceeding €28,000 3%Vehicle value exceeding €28,000 5%

Maintenance value % of vehicle valueVehicle value not exceeding €28,000 3%Vehicle value exceeding €28,000 5%

Car value Private usepercentage

Not exceeding €16,310 30%Exceeding €16,310 but not €21,000 40%Exceeding €21,000 but not €32,620 50%Exceeding €32,620 but not €46,600 55%Exceeding €46,600 60%

3 [P.T.O.

Capital gains

Index of inflation

1988 439·621989 443·391990 456·611991 468·211992 475·891993 495·601994 516·061995 536·611996 549·951997 567·951998 580·611999 593·002000 607·072001 624·852002 638·542003 646·842004 664·882005 684·882006 703·882007 712·682008 743·052009 758·582010 770·072011 791·022012 800·00 (est)

Applicability of increase for inflation

Cost of acquisition/improvementsx

index(yd) – index(ya)–––––––––––––––––––––––––––– ––––––––––––––––––

1 index(ya)

Where:index(yd) is the index for the year immediately preceding that in which the transfer is made;index(ya) is the index for the year immediately preceding that in which the property in question had been acquiredor completed, whichever is the later, or, when it relates to improvements, for the year immediately preceding that inwhich the cost of carrying out the improvements was incurred.

Transfer of value

Y = (A – B) + C – D

Where:‘Y’ represents the value transferred or acquired by a person‘A’ is the market value of the shares held in the company immediately before the change‘B’ is the market value of the shares held in the company immediately after the change‘C’ is the consideration paid by the person for the acquisition of shares or additional shares issued by the company,

where the change consists of an issue of share capital for consideration‘D’ is the amount paid by the company in respect of a cancellation of shares held by the person, where the change

consists of a reduction of share capital

4

Cost of acquisition of shares in the transfer of value

Z = ((A – B)/A) x E

Where: ‘Z’ represents the amount to be determined‘A’ is the market value of the shares held by the transferor immediately before the change‘B’ is the market value of the shares held by the transferor immediately after the change ‘E’ is the cost of acquisition of the shares held by the transferor immediately before the change

Business Promotion Act Incentives

Definition of a medium sized enterprise

An enterprise which is not a small enterprise and:

– has fewer than 250 employees; and– has an annual turnover not exceeding €40 million or total assets not exceeding €27 million; and– is to be treated as being independent.

Definition of a small enterprise

An enterprise which:

– has fewer than 50 employees; and– has an annual turnover not exceeding €7 million or total assets not exceeding €5 million; and– is to be treated as being independent.

Stamp duty

Standard rate €2 for every €100 in value or part thereofProperty companies (as defined) €5 for every €100 in value or part thereof

Annual market rent (tax accounting)

The annual market rent of immovable property situated in Malta owned and used by a company for the purpose ofits activities (excluding property which is rented by the said company to other parties) is calculated by multiplying theaggregate surface area in square metres of all floors of such premises so owned and used by €250 per annum.

5 [P.T.O.

This is a blank page.Question 1 begins on page 7.

6

Section A – BOTH questions are compulsory and MUST be attempted

1 Frank, an individual who is ordinarily resident and domiciled in Malta, owns 100% of the share capital of A Ltd, alimited liability company incorporated and managed and controlled in Malta. A Ltd carries on a business consistingof the importation and sale of electronic equipment. A Ltd owns a shop, situated in Mosta, from which it sells theequipment. The shop was acquired in 2005 for a consideration of €200,000 and stamp duty of €10,000 was paid;the shop has been used by A Ltd for the purpose of its business since its acquisition.

Frank has decided to set up a new company, B Ltd, to be owned equally by himself and his cousin Matthew, who isan electronics technician. A Ltd will transfer the shop situated in Mosta to B Ltd and B Ltd will use this shop for thepurpose of its new business, which is to consist of the repair and servicing of electronic equipment. B Ltd is to beincorporated on 5 January 2013 with a share capital of 10,000 fully paid-up ordinary shares of €1 each and theshop will be transferred to B Ltd on 15 January 2013.

The Mosta shop will be sold to B Ltd for €400,000. This price reflects its current market value, which is expected toremain unchanged until the time of transfer. The consideration of €400,000 payable by B Ltd to A Ltd is to remainoutstanding for the foreseeable future and there is no fixed date for repayment.

Separately, A Ltd has entered into a promise of sale agreement with third parties to acquire a shop in Valletta for€500,000, which A Ltd will use solely as an outlet to sell its equipment. The deed of transfer is to be signed on 30 June 2013.

Two options are being considered for the acquisition of Matthew’s shareholding in B Ltd:

Option 1: On incorporation, Frank will acquire 10,000 fully paid-up ordinary shares of €1 each in B Ltd. A Ltd willtransfer the Mosta shop to B Ltd for a consideration of €400,000 on 15 January 2013. Then, on 31 January 2013, Frank will transfer 5,000 ordinary shares in B Ltd to Matthew for a consideration of€5,000.

Option 2: Frank and Matthew will each acquire 5,000 ordinary shares in B Ltd on incorporation. A Ltd will transferthe Mosta shop to B Ltd for a consideration of €400,000 on 15 January 2013.

Required:

Prepare a letter to Frank advising on the income tax and stamp duty implications of each of the two options thatare being contemplated, as follows:

(a) The income tax and stamp duty implications under option 1, arising both from the transfer of the shopsituated in Mosta from A Ltd to B Ltd and from the subsequent transfer of shares to Matthew, including theapplicability or otherwise of any relevant options, exemptions or reliefs. (17 marks)

(b) The income tax and stamp duty implications under option 2 arising from the transfer of the shop situated inMosta from A Ltd to B Ltd, including the applicability or otherwise of any relevant options, exemptions orreliefs. (4 marks)

(c) The income tax implications that would arise under OPTION 2 if, subsequent to the transfers currentlyproposed, A Ltd transfers its Valletta shop to third parties without replacing it with another outlet.

(3 marks)

(d) Where relevant, calculations supporting the explanations provided. (6 marks)

Professional marks will be awarded in question 1 for the appropriateness of the format and presentation of theletter and the effectiveness with which the information is communicated. (4 marks)

(34 marks)

7 [P.T.O.

2 (a) BLUECO Ltd

HOLDCO Ltd

SUBCO A Ltd SUBCO B Ltd

Holdco Ltd, Subco A Ltd and Subco B Ltd are all limited liability companies incorporated and managed andcontrolled in Malta, having a 31 December year end. Holdco Ltd owns all of the ordinary share capital of Subco A Ltd and Subco B Ltd. Holdco Ltd is wholly (100%) owned by Blueco Ltd, a limited liability companyincorporated and managed and controlled in Country X, a member of the European Union (EU). Blueco Ltd iswholly (100%) owned by individuals who are neither resident nor domiciled in Malta. Holdco Ltd is registeredwith the Commissioner of Inland Revenue to be eligible for refunds of tax on dividend distributions.

Subco A Ltd’s business consists of the ownership and operation of a number of fast food outlets, all of which aresituated in Malta. The total area of these fast food outlets is 800 m2. The chargeable income of Subco A Ltd forthe financial year ending 31 December 2012, calculated in accordance with the Income Tax Act, amounts to€380,000. Capital allowances as per the Income Tax Act exceed accounting depreciation by €20,000; this isthe only tax adjustment required to the accounting profits.

On 30 June 2012, Subco B Ltd received a dividend of €180,000 from Blackco Ltd, a limited liability companyincorporated and resident in Country Z, a territory outside the EU with which Malta does not have a doubletaxation relief agreement. The dividend was not subject to withholding tax, but Blackco Ltd is subject tocorporation tax in Country Z at the rate of 10% on all of its profits and gains. Subco B Ltd’s investment in BlackcoLtd consists of fully paid-up 5% non-cumulative, non-participating preference shares redeemable in 2013. Thesepreference shares do not carry any right to vote or any other special rights and represent 5% of the total issuedshare capital of Blackco Ltd.

Subco A Ltd and Subco B Ltd have distributed all of their profits available for distribution and derived during thefinancial year ending 31 December 2012 by the end of 2012. Subco B Ltd does not own, directly or indirectly,any immovable property situated in Malta.

When determining their taxable income, Subco A Ltd and Subco B Ltd have as their main objective themaximisation of the return to Holdco Ltd, including the right to benefit from any tax refunds on the distributionof dividends.

Required:

(i) Explain the Maltese income tax treatment of Subco A Ltd’s income, indicating the manner in which theallocation to the tax accounts is to be made and calculate any tax refund that may be claimed by Holdco Ltd; (7 marks)

(ii) Explain the Maltese income tax treatment of the dividend received by Subco B Ltd from Blackco Ltd,including any options available in the computation of chargeable income to the extent that they canaffect the calculation of the tax refunds claimable by Holdco Ltd. Identify the most favourable optionand calculate the amount of the tax refund that can be claimed. (9 marks)

(b) Django Ltd is a limited liability company incorporated and managed and controlled in Malta, wholly (100%)owned by Wes Ltd, a limited liability company incorporated and managed and controlled in Redland, a territoryoutside the EU. A double taxation treaty based on the OECD Model Convention is in force between Malta andRedland. Wes Ltd is wholly owned by individuals who are neither resident nor domiciled in Malta.

Wes Ltd is interested in acquiring an office building situated in Malta and is considering the following two options:

Option 1: Wes Ltd will grant a loan amounting to €1 million to Django Ltd, charging an interest rate of 8% perannum. Django Ltd will use the money borrowed from Wes Ltd to purchase the office building.

Option 2: Wes Ltd will purchase the office building directly.

8

The office building is to be rented out to Burrell Ltd, a limited liability company incorporated and managed andcontrolled in Malta, for an annual rent of €100,000.

Required:

(i) Explain the Maltese income tax implications applicable to Django Ltd, under option 1, of the interestcharged by Wes Ltd; (5 marks)

(ii) Explain the Maltese income tax implications applicable to both Wes Ltd and Burrell Ltd, under option 2, of the rent received from Burrell Ltd. (5 marks)

Note: You are to assume that the rental income to be received from the letting of the office is chargeable totax as income, i.e. from property, and not derived from a trade or business.

(26 marks)

9 [P.T.O.

Section B – TWO questions ONLY to be attempted

3 (a) Aldo, his wife Sandra and their son Paul are ordinarily resident and domiciled in Malta. Aldo and Sandra haveowned, in equal proportions, all of the issued share capital of Alsan Ltd since its incorporation in 2003. AlsanLtd is a limited liability company incorporated and managed and controlled in Malta. The only fixed asset ownedby Alsan Ltd consists of a house situated in Hamrun, purchased in 2004 as a long-term investment for aconsideration of €150,000. The current market value of the house is €250,000.

Aldo and his wife have decided to dissolve Alsan Ltd and will be appointing a liquidator to wind up and dissolvethe company. Aldo and Sandra are considering the following options with regard to the house:

Option 1: Alsan Ltd transfers the house to Aldo and Sandra.

Option 2: Alsan Ltd transfers the house to Paul. Under this option, Paul will acquire the house for the purposeof establishing therein his sole, ordinary residence.

Required:

Comment on the stamp duty implications under each option being considered. Your answer should includean analysis of any potentially relevant exemptions, and the reasons why these should or should not apply.

(10 marks)

(b) Consider the following two scenarios:

Scenario 1S Ltd is a limited liability company established in Malta, which is registered in Malta under article 10 of the ValueAdded Tax Act (VAT Act). S Ltd supplies software packages and the software updates from its fixed establishmentin Malta. All of the software packages and updates are purchased online and supplied electronically. S Ltd’sturnover is made up of 70% generated from customers who are established within territories forming part of theEuropean Union (EU), and 30% from customers who are established in territories outside the EU. S Ltd’scustomers include both taxable and non-taxable persons.

Scenario 2R Ltd is a limited liability company established in Malta, which is registered in Malta under article 10 of the VATAct. R Ltd is an estate agent which also offers property valuation services. Its agency and valuation services areprovided for properties situated in Malta, Spain and Country X, which is a territory outside the EU. R Ltd’s clientsconsist only of non-taxable persons, all of whom are established within the territories forming part of the EU.

Required:

(i) Set out the general rule laid down in the Value Added Tax Act for determining where supplies of servicesare deemed to take place; (2 marks)

(ii) In the context of the Maltese VAT legislation for each of scenarios 1 and 2, giving reasons, state whetherthe services provided will be considered as taking place within or outside Malta and, if outside Malta,who is the person responsible for the payment of the value added tax (VAT) if applicable. (8 marks)

(20 marks)

10

4 John, an individual who is ordinarily resident and domiciled in Malta, owns 100% of the share capital of FoodstuffsLtd, which was incorporated in 2003. Foodstuffs Ltd used to carry on a business consisting of the wholesaling of foodproducts before it completely ceased operations during 2011. Foodstuffs Ltd did not derive any income during 2012.Foodstuffs Ltd has available unabsorbed tax losses amounting to €150,000 up to the year of assessment 2012.

John is now interested in starting a new business consisting of the operation of a restaurant and is in discussions withPaul who is the 100% shareholder of Diner Ltd, which is in the restaurant business. The only fixed asset owned byDiner Ltd consists of catering equipment which was purchased for €150,000 (net of value added tax) on 30 November 2010. Wear and tear allowances for the catering equipment are applied by Diner Ltd at the rate of16·67% per year (i.e. on a straight-line basis over a six year period). Diner Ltd’s taxable income before deductingwear and tear allowances in respect of the catering equipment for the year of assessment 2013 amounts to €75,000.Diner Ltd has fully claimed the annual wear and tear deductions allowed since 2010.

The following three options are being considered:

Option1On 15 January 2013, Foodstuffs Ltd acquires from Diner Ltd the restaurant business together with the assets, as agoing concern, for a consideration of €300,000. Foodstuffs Ltd will also assume all liabilities of Diner Ltd. John willinvest €300,000 in Foodstuffs Ltd by way of a shareholder’s loan charging interest at the rate of 8% per year, to beused by Foodstuffs Ltd to acquire the business and assets from Diner Ltd. The agreed price for the acquisition of thecatering equipment of €100,000 is included within the total consideration of €300,000.

Option 2On 15 January 2013, Foodstuffs Ltd acquires from Paul the entire share capital of Diner Ltd for a consideration of€300,000. John will invest €300,000 in Foodstuffs Ltd by way of a shareholder’s loan charging interest at the rateof 8% per year, to be used by Foodstuffs Ltd to acquire the entire share capital of Diner Ltd from Paul.

Option 3On 15 January 2013, John purchases from Paul the entire share capital of Diner Ltd for a consideration of€300,000.

Under each of the three options, John will take out a personal bank loan of €300,000 to finance the investment,which will be subject to annual interest at the rate of 8%. Any interest or dividends received by John will be taxed atthe marginal rate of 35%.

Foodstuffs Ltd and Diner Ltd are both limited liability companies incorporated and managed and controlled in Malta,having a 31 December year end.

Required:

(a) Under each of the options being considered, explain the tax treatment of the interest payable and receivableby Foodstuffs Ltd and John. (3 marks)

(b) Explain the income tax implications of the transfer of the catering equipment under option 1 for both DinerLtd and Foodstuffs Ltd. Support your explanation with calculations of the balancing charge or balancingallowance, if any, resulting from the transfer. (4 marks)

(c) Explain which of the options, 1, 2 or 3, would maximise the benefit of any potential losses for which reliefmay be claimed, and any available wear and tear deductions. Support your explanations with relevantcalculations taking into account a period of six years (years of assessment 2014 to 2019 inclusive) andclearly identify which option you would recommend.

Note: You should assume that the chargeable income from the restaurant business for the years of assessment2014 to 2019 will remain at €75,000 per year, before deducting wear and tear allowances in respect of thecatering equipment. (13 marks)

(20 marks)

11 [P.T.O.

5 (a) Lara is a qualified actuarial professional, with six years’ professional experience in the insurance business. Larais single and is domiciled and resident in Country Y, a jurisdiction that forms part of the European Union (EU).Lara is currently employed by GI Limited, a public limited liability company incorporated in Country Y.

With Lara’s consent, the directors of GI Limited have decided to transfer her to Malta to work for MT Limited. MT Limited is wholly (100%) owned by GI Limited, and is a limited liability company incorporated and managedand controlled in Malta which is licensed by the Malta Financial Services Authority and is authorised to carry onthe business of insurance from Malta.

Lara will take up employment in Malta with MT Limited as from 1 January 2013 and will exercise heremployment from MT Limited’s offices in Malta. Her contract of employment with MT Limited, which expiresafter three years, provides for an annual cash salary amounting to €90,000. In addition to the cash salary, theemployment contract also provides that MT Limited is to pay for her accommodation expenses in Malta. Afterthree years, it has been agreed that Lara will return to Country Y and resume her employment with GI Ltd.

A double taxation treaty based on the OECD Model Convention is in force between Malta and Country Y.

In accordance with Country Y’s domestic tax law, Lara will remain tax resident in Country Y during her stay inMalta and, in terms of the tie-breaker rules under the Residence Article of the double taxation relief treaty betweenMalta and Country Y, Lara will be treated as resident in Country Y for the purposes of that treaty.

Required:

(i) Explain the Maltese income tax implications relevant to Lara’s salary and benefits, including the effectof the Malta–Country Y double tax treaty; (5 marks)

(ii) Discuss whether Lara will or will not be entitled to benefit under the Highly Qualified Persons rules.(5 marks)

(b) (i) Explain the difference between economic double taxation and juridical double taxation; (2 marks)

(ii) Explain what is meant by a ‘full imputation system’ and state whether such a system eliminates/reducesthe distortions caused by economic double taxation in your opinion; (4 marks)

(iii) Briefly outline the relevant provisions of the Income Tax Acts which provide for the full imputationsystem. (4 marks)

(20 marks)

End of Question Paper

12