paper - alfred lerner college of business and economics

TRANSCRIPT

WORKING PAPER NO. 2013‐01

Evidence of Student Achievement in a

High School Personal Finance Course

By

Andrew T. Hill, Bonnie T. Meszaros and Brian Tyson

WORKING PAPER SERIES

The views expressed in the Working Paper Series are those of the author(s) and do not necessarily reflect those of the Department of Economics or of the University of Delaware. Working Papers have not undergone any formal review and approval and are circulated for discussion purposes only and should not be quoted without permission. Your comments and suggestions are welcome and should be directed to the corresponding author. Copyright belongs to the author(s).

Evidence of Student Achievement in a High School Personal Finance Course

Andrew T. Hill*† Economic Education Advisor

Federal Reserve Bank of Philadelphia Ten Independence Mall Philadelphia, PA 19106

Telephone: (215) 574‐4392 Fax: (215) 574‐2512

E‐mail: [email protected]

Bonnie T. Meszaros Associate Director

Center for Economic Education and Entrepreneurship University of Delaware 102 Alfred Lerner Hall Newark, DE 19716

Telephone: (302) 831‐1896 Fax: (302) 831‐6659

E‐mail: [email protected]

Brian Tyson‡ Graduate Student

University of Texas at Austin Austin, Texas 78712

December 7, 2012

* The views expressed in this paper are those of the authors and do not necessarily represent those of the Federal Reserve Bank of Philadelphia or the Federal Reserve System. The authors thank Susheela Patwari for valuable research assistance in the early stages of this project. †Corresponding author. ‡At the time this research was conducted, Brian Tyson was a research analyst at the Federal Reserve Bank of Philadelphia.

2

Evidence of Student Achievement in a High School Personal Finance Course

Abstract

This study investigates the effect of the “Keys to Financial Success” high school personal finance

curriculum on student achievement. It relies on multiple years of pre‐ and posttest data from 1,701

students who took a “Keys” course and from a comparison group of 261 students from the same

schools. The results from the pre‐ and posttests show that students who take the “Keys” course exhibit a

statistically significant increase in their personal finance achievement. These results contribute to the

growing literature showing the positive effects on the financial knowledge of high school students when

they take a well‐designed course taught by properly trained teachers.

Keywords: personal finance education, precollege, economic education, curriculum, assessment

JEL codes: A2, A21, D14

3

INTRODUCTION

Over the past decade, there has been increased attention on the need to include personal

finance in the high school curriculum. This perceived need has been fueled by articles from the popular

press, statistics on the impact of poor financial decisions made by young adults, and articles from the

academic community. In addition, the call for financial education has been reinforced by former Federal

Reserve Chairman Alan Greenspan (2001) and current Chairman Ben Bernanke (2006). While there has

been a growing interest in offering personal finance education in the K‐12 classroom, there is limited

evidence that personal finance instruction increases student personal finance achievement. This paper

explains the features of a high school personal finance curriculum – “Keys to Financial Success,” which is

offered by a consortium of partners in Delaware, New Jersey, and Pennsylvania – and the results from a

multiyear study of pre‐ and posttest scores from students in classrooms with teachers who use the

“Keys” materials.

LITERATURE

Today, more than any other time, individuals are expected to take more responsibility for

handling their personal finances and planning for their retirement. At the same time, the financial

services available to them have become more complex and specialized. Today’s consumers face an array

of sophisticated products. High levels of consumer debt, predatory lending, low savings rates, an

increase in nonbusiness bankruptcy filings, and expanded access to credit for younger populations are a

few of the factors contributing to the increased attention to the need for personal finance education

(Braunstein and Welch, 2002). With the recent financial crisis, the focus on a financially literate citizenry

has moved to center stage. Part of the responsibility to ensure that this goal is reached rests with

America’s K‐12 schools. Students leaving high school should be grounded in the fundamentals of

personal finance to be prepared for their roles as consumers, savers, and investors.

4

One of the impacts of the push for financial education in the schools has been an increase in

states’ mandates. In 2009, 44 states included personal finance to some extent in their state educational

standards and 34 states required that these standards be implemented. Thirteen states now require

students to take a personal finance course or include personal finance in an economics course as a high

school requirement for graduation (CEE, 2009). Having mandates does not necessarily translate into

student achievement. Tennyson and Nguyen (2001) found that in states that have broadly defined

personal finance mandates, students did not score higher on a personal finance test. However, those in

states that required a specific financial education course scored significantly higher than students in

states without mandates.

The Jump$tart Coalition of Personal Financial Literacy began conducting biannual national

testing of high school students in 1997. Mandell (2008) reports that results from the 2008 Jump$tart

survey were discouraging. The survey found that the financial literacy of high school seniors was at its

lowest level since the first Jump$tart survey was administered. The 2008 average score was 48.3

percent, down from a high of 57.3 percent in 1997. In fact, students who took a semester‐long high

school personal finance course did not do better on the Jump$tart examination than those who did not

take a personal finance course. These findings were cited by Willis (2008) as a reason against financial

literacy education. She argues that the move for more personal finance education in the schools should

be abandoned and suggests searching for policies that could lead more directly to good consumer

financial outcomes. Mandell and Klein (2009) drew similar conclusions and stated that until more

evidence was available that demonstrated that personal finance courses at the high school level

influenced subsequent financial behavior, the allocation of resources toward mandatory classes should

be reconsidered.

Mandell and Klein (2007) suggest that students retain little of what they learn in personal

finance because they don’t perceive that it is relevant to their lives. Motivation is a critical factor in

5

students becoming financially literate. The authors conclude that successful programs must include

instruction on setting clear and obtainable goals and helping students see how basic financial literacy

will allow them to reach their goals and add value to their lives. In addition, Mandell and Klein (2007)

conclude that the poor results on the Jump$tart surveys point out the need for teacher training and

better instructional materials. However, these surveys do show that high school students who play a

stock market game are more financially literate than students who do not (Mandell, 2006). A 2009

study to assess the impact of the Stock Market Game found that students who played the game scored

significantly higher on financial literacy tests than their peers who did not play (Hinojosa et al., 2008).

Mandell and Klein (2007) suggest that this implies that personal finance classes that are taught

interactively and are perceived by the students to be relevant to their lives may be more effective than

classes that use more traditional methods of instruction.

As the demand for personal finance education has increased so has the availability of

instructional materials. There has been a proliferation of nonprofit organizations, financial institutions,

congressional bills, and even a federal commission promoting financial literacy in recent years. Many of

these groups provide free or inexpensive instructional materials for children and adults. However,

limited research has been done on the effectiveness of these materials.

Hathaway and Khatiwada (2008) found that most research has not proven the effectiveness of

financial education programs. They conclude that there are two likely reasons for this. First, the

programs are not effective in transferring knowledge because of either their design or how they are

administered. Second, the programs are not being evaluated properly. Although the authors reviewed

research mainly on adult programs, their findings have implications for personal finance education.

Hathaway and Khatiwada (2008) conclude that a standard but adaptable framework for evaluation of all

types of literacy programs is needed. This is supported by Fox, Bartholomae, and Lee (2005) who

recommended Jacobs’s (1988) five‐tiered approach to evaluation with applications for personal finance.

6

Walstad, Rebeck, and MacDonald (2010) also stressed the use of Jacobs’s model when evaluating the

video‐based curriculum Financing Your Future. They outlined the five stages for personal finance

program evaluation. First, set a clear definition of content. Second, train teachers in content and use of

program materials. Third, specify knowledge outcomes that are measured with reliable and valid

instruments. Fourth, collect data on pre‐ and posttests. Fifth, rigorously analyze data using appropriate

forms of statistical analysis.

There are a number of studies that have shown a change in student achievement in personal

finance after exposure to a specific curriculum. In a survey of students who completed the High School

Financial Planning Program, Todd (2002) found that, following the training, 50 percent of the students

reported increases in financial knowledge. This supports findings from an earlier survey (Boyce and

Danes 1997–1998) that found that students feel more financially literate after the completion of the

personal finance course. Varcoe et al. (2005) used a 10‐item pre‐ and post‐ true/false test to determine

the impact of the Money Talks: Should I Be Listening? curriculum on student achievement. The results

from the true/false tests and the self‐reported data indicated that students who participated in Money

Talks seemed to improve their financial knowledge. However, these studies failed to include one or

more of the steps recommended in Jacobs’s (1988) five‐tier approach to evaluation.

Several studies have used a more rigorous approach to evaluation and have shown promising

results. All have used a quasi‐experimental design with treatment and comparison groups and have

provided teacher training using a specific curriculum package. Walstad and Rebeck (2005) developed a

50‐item multiple‐choice test to measure student achievement based on the content in Financial Fitness

for Life (FFL) (Morton and Schug, 2001) a personal finance and economics curriculum published by the

Council on Economic Education (formerly the National Council on Economic Education). After receiving

training in the FFL curriculum, high school teachers gave a pretest, taught the lessons, and administered

a posttest. The results showed that students receiving instruction from trained teachers using FFL had

7

higher achievement scores than students in the comparison group. Harter and Harter (2009) conducted

a study in eastern Kentucky to assess the effectiveness of the FFL lessons in elementary, middle, and

high school. Teachers participating in the study attended a workshop on the use of the FFL materials

prior to teaching with them in their own classrooms. At the high school level, student gains from the

pretest to posttest were significant when compared with the comparison group. Swinton et al. (2007)

examined student scores on Georgia’s economics end‐of‐course test. Students in classrooms with

teachers who attended a FFL workshop scored significantly higher on the required end‐of‐course test

than students taught by teachers who did not attend the workshop. Most recently, Walstad, Rebeck,

and MacDonald (2010) conducted a study on the effect of student achievement of Financing Your Future

(FYF), a series of five DVDs (CEE, 2009). Pre‐ and posttests were administered to treatment and

comparison groups. Students taught with FYF showed a statistically significant increase in their personal

finance knowledge over their peers in the comparison group.

KEYS TO FINANCIAL SUCCESS

In the spring of 2001, the University of Delaware Center for Economic Education and

Entrepreneurship (Center), the Federal Reserve Bank of Philadelphia, the Delaware Bankers Association,

and the Consumer Credit Counseling Service of Maryland and Delaware formed a partnership to provide

curriculum resources and teacher training to Delaware high schools interested in teaching a semester

personal finance course. Work commenced in the late spring and early summer of 2001 to compile a

90‐day instruction plan for a high school personal finance course that would make use of existing

curriculum resources, approach the teaching of personal finance using materials grounded in the

economic way of thinking, and allow the course to be flexible enough to be taught by teachers in the

social studies, family and consumer science, mathematics, and business departments. The resulting

course plan, called “Keys to Financial Success,” makes extensive use of lessons from the Council on

8

Economic Education’s widely distributed FFL (Morton and Schug, 2001) and Learning, Earning, and

Investing (LEI) (Caldwell et al., 2004) lesson books. These lessons make use of active and collaborative

learning and are engaging for the students. Since these two packages did not include lessons on specific

topics of importance to the partners, such as risk management, goal setting, and career planning,

lessons were developed by the staff at the Center and the Federal Reserve Bank of Philadelphia or were

taken from VISA’s Practical Money Skills (2000). To motivate students and add relevance to the course,

students are asked in the first two units to research different careers and set personal and financial

goals. Based on their research and goals, the students, with guidance from the teacher, select a career

for use during the course. The students’ goals and careers with entry‐level wages are revisited

throughout the remaining units in the course. Students are asked to apply what they have learned using

the income associated with their selected career and determine how their decisions impact their goals.

The intent of this approach is to help students see the relevance of being financially literate both now

and as adults.

The “Keys” course consists of 54 lessons built around nine themes: goals and decision‐making,

careers and planning, budgeting, saving and investing, credit, banking services, transportation issues,

housing issues, and risk protection. Throughout the course, students use the Internet for access to the

latest information on personal finance topics and financial products. This approach allows teachers to

update lessons from year to year to reflect changes in the financial marketplace. Using knowledge

gained from the lessons and information gleaned from the Internet, students create a personal portfolio

of tools and data. The students are encouraged to keep their portfolios as a reference when making

financial decisions after high school.

Participating schools commit to offering the course at least once per academic year. Teachers

attend a week‐long training course at the Federal Reserve Bank of Philadelphia taught by individuals

from the Center and the Federal Reserve Bank of Philadelphia. These economic educators have

9

advanced degrees in economics or economic education as well as extensive experience in teaching

classes for teachers.

In the 2001–2002 school year, the “Keys” course was piloted in one Delaware high school. As

shown in Table 1, the pilot year was followed by the addition of six schools in the 2002–2003 school

year, eight schools in 2003–2004, and six schools in 2004–2005. In this period, a total of 26 teachers

were trained to teach the course. In these first four years, only schools in Delaware were participating.

Beginning in the 2005–2006 academic year, schools in New Jersey and Pennsylvania were recruited to

participate in the program. In the six school years since recruiting began in New Jersey and

Pennsylvania, 97 schools were added to the program and 168 additional teachers were trained. While

new schools were continuing to adopt the “Keys” program over this period, a few schools left the

program each year. These attritions from the program were usually due to the retirement of the

teacher who had taught the course or due to school administrators realigning teachers’ schedules to

different areas.

[Insert Table 1 about here]

STUDY DESIGN

From the inception of the “Keys to Financial Success” program, the partners recognized the

importance of measuring the impact of the course on the personal finance achievement of the students.

A 50‐question personal finance test was developed based on the 50‐item high school multiple‐choice

test published by the Council for Economic Education to accompany the Financial Fitness for Life

personal finance curriculum.1 This test, developed by Walstad and Rebeck (2005), provided strong

internal consistency and was well suited to the content covered in the “Keys to Financial Success” course

since the course makes use of many lessons from the Financial Fitness for Life curriculum.

1. The test developed for this study omitted five questions from the FFL high school test and substituted five questions developed by the authors.

10

Initially, “Keys” teachers were asked to administer the 50‐item “Keys” test at the beginning of

the semester and at the end of the semester. They were also asked to administer, as a comparison, a

test with 10 questions drawn from the 50‐question “Keys” test to another section of students not taking

“Keys.” That section of comparison students could be either the “Keys” teacher’s own students or a

section of students taught in the same school by a colleague. The teacher was encouraged to choose a

comparison section of students who were about the same age and of the same ability level as the

students in his or her “Keys” course. During this early period in the study, no demographic information

was collected on the students in either the treatment or the comparison groups.

In subsequent years of the study, students in both the treatment and the comparison groups were asked

to self‐report whether they have a job currently or had one in the past, whether they have a checking

account, whether they have a savings account, their gender, and their age. The comparison test was

expanded from 10 to 20 questions. The 10 questions asked in the first comparison test were carried over

to the new 20‐question test, but 10 additional questions were added from the 50‐item test administered

to the treatment group.2 Also in the subsequent years of the study, students in both the treatment and

comparison groups were asked a set of affective questions about how they save and spend money, their

credit card use, and how they make decisions.3 All the data used in the analysis reported here are from

this later period.

2. Teachers indicated that they were unwilling to take the classroom time to administer a 50‐item test to a comparison group of students. In order to ensure that teachers were willing to administer a test to a comparison group, it was necessary to reduce the number of items to a subset of 20 questions drawn from the 50‐item test administered to the treatment group. While the difference in test length could result in differences in student performance due to more exam fatigue on the 50‐item test as compared to that on the 20‐item test, that bias would tend to cause the scores of the comparison group to be higher on the 20 items than those of their counterparts in the treatment group on those same 20 items. Given the large improvement from pre‐ to posttest exhibited by the treatment group as compared with the comparison group, this effect of exam fatigue does not seem to be much of a factor. 3. The results from the affective questions are not covered in this paper but are part of subsequent research to be published separately.

11

It is important to note that this study employs a quasi‐experimental design. Students in the

treatment group self‐selected themselves into their elective “Keys to Financial Success” course and

therefore the treatment group. Students in the comparison group are in other classes in the school and

are most often taught by the same teacher, but they are not receiving the “Keys” curriculum. The

comparison classes could be a business, social studies, or math class. As with many studies that examine

the effects of specific curriculum on student achievement, random assignment was not possible given

the specific circumstances present in the participating schools. Most significantly, schools are

overwhelmingly unwilling to allow researchers to randomly assign students to and require students to

take specific courses in the interest of research.

In Table 2, we present an overview of the content and cognitive level of the 20‐question “Keys

to Financial Success” knowledge test. Copyright restrictions prohibit us from reporting the specific

questions from the Financial Fitness for Life test, but we have summarized the content covered in each

question in the table. The related “Keys” and Financial Fitness for Life themes are also reported for each

question. The themes are listed beneath the table. The 20‐question test includes eight cognitive

questions, five analytical questions, and seven knowledge questions.

[Insert Table 2 about here]

In Table 3, we report the demographics for both the treatment group and the comparison

group. With respect to gender, age, history of employment, and checking and savings account

ownership, the comparison group is relatively representative of the treatment group. The treatment

group does have a larger percentage of students aged 15 or under and a smaller percentage of students

aged 17 than the comparison group. The treatment group and comparison group differ with respect to

the states in which the students are enrolled. The majority of students in the treatment group are from

Pennsylvania. The comparison group is more heavily weighted with students from Delaware and New

Jersey.

12

[Insert Table 3 about here]

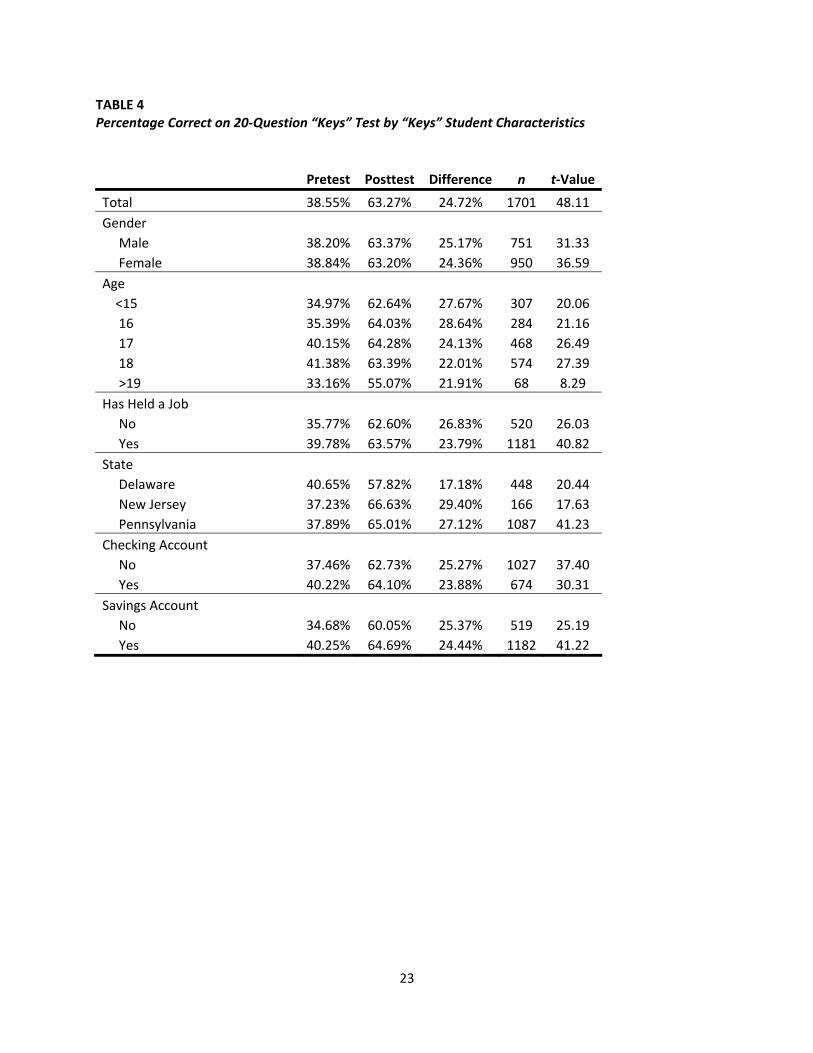

RESULTS In Table 4, we present the average pretest and posttest percentages correct on the 20‐question

test, sample sizes, and t‐values for the sample of “Keys” students (the treatment group). The increase in

average percentage correct from pretest to posttest was highly statistically significant for all subgroups

in the treatment sample. The gains in personal finance achievement for males and females were 25.17

percentage points and 24.36 percentage points, respectively.4 This result implies, as found by Walstad,

Rebeck, and MacDonald (2010), that instruction in the “Keys” course and the “Keys” test are “probably

not subject to conditions that produce gender differences in financial knowledge outcomes” (p. 349).

[Insert Table 4 about here]

Students who were 15 years of age or younger and students who were 16 showed the largest

improvement on the test (27.67 percentage points and 28.64 percentage points, respectively). They

started from about the same average percent correct (34.97 percent and 35.39 percent, respectively) on

the pretest and ended at about the same average percent correct (62.64 percent and 64.03 percent,

respectively) on the posttest. Likewise, students who were 17 and students who were 18 showed similar

starting points on the pretest (40.15 percent and 41.38 percent, respectively) and ended at similar

points on the posttest (64.28 percent and 63.39 percent, respectively). Seventeen‐year‐olds’ and 18‐

year‐olds’ achievement in personal finance as shown by the 20‐item “Keys” test increased by 24.13

percentage points and 22.01 percentage points, respectively. In this study the 17 and 18 year olds

started with a slightly greater understanding of personal finance but ended the course with roughly the

4. A test for attrition bias was conducted to investigate whether those students who took the pretest but did not take the posttest were significantly different from those who completed both the pretest and the posttest. Students from the treatment group who completed both the pretest and the posttest scored 1.07 questions higher on the 50‐question test than their counterparts who left the sample after the pretest. The t‐statistic comparing this difference to 0 was 5.60, implying that this difference is statistically significant. However, without a clear instrumental variable in our data set, we were unable to use the standard Heckman correction.

13

same level of personal finance knowledge as their younger counterparts. Students who were 19 years of

age or older, while representing a small portion of the sample, started with an average pretest score of

33.16 percent correct and ended with an average posttest score of 55.07 percent correct. The students

in the treatment group who were 19 years of age and older improved their personal finance knowledge,

on average, by 21.91 percentage points as measured by the 20‐question “Keys” test. On average, these

older students, who were older than average high school seniors, started their “Keys” courses with less

knowledge of personal finance than even their peers who were 15 years of age or younger and had

smaller gains in personal finance knowledge between the pre‐ and posttest.

“Keys” students who have held a job had pretest scores slightly over 4 percentage points higher

than those students who have never held a job. However, the posttest score for those who have held a

job was 63.57 percent correct as compared with 62.60 percent correct for those who have never held a

job. The personal finance knowledge gap between those students in the study who had held a job and

those who had not narrowed between the pretest and the posttest.

Students from New Jersey and Pennsylvania had pretest scores that were approximately the

same (37.23 percent correct and 37.89 percent correct, respectively). Students from Delaware, on

average, started with a higher pretest score of 40.65 percent correct. This pretest difference may reflect,

in part, that Delaware has a long‐standing economics requirement in elementary, middle, and high

school social studies. However, students in New Jersey and Pennsylvania gained significantly more in

their personal finance achievement when compared with their counterparts in Delaware. Between the

pretest and the posttest, Delaware students showed a 17.18‐percentage‐point increase in the number

correct on the 20‐question test, while students in New Jersey gained 29.40 percentage points and

students in Pennsylvania gained 27.12 percentage points.

Nearly 675 students in the treatment sample reported having a checking account. While those

students with checking accounts had pretest scores higher than their counterparts who did not, the

14

students without checking accounts increased their score on the test by 25.27 percentage points and

those students with checking accounts increased their score on the test by 23.88 percentage points.

Likewise, those students with a savings account had, on average, pretest scores that were 5.57

percentage points higher than those students without a savings account. Students with savings accounts

had average achievement gains of 24.44 percentage points after taking the course. Students without

savings accounts had average achievement gains of 25.37 percentage points after taking the course.

In Table 5, we present the pre‐ and posttest percentage correct results for the “Keys” students

and the students in the comparison group. We show the results for both the full 50‐item “Keys”

personal finance knowledge test as well as the 20‐item truncated test given to comparison students.

These results for the full 50‐question test are reported for just the “Keys” students, since they were the

only students to take the full 50‐item test. On average, the students gained 21.14 percentage points

between the pretest and the posttest on the 50‐item test. The increase was highly statistically

significant. Likewise, the “Keys” students gained, on average, 24.72 percentage points between the

pretest and the posttest on the 20 items given to the comparison group. On these same 20 questions,

the comparison group gained, on average, just 3.14 percentage points. Both gains are highly statistically

significant. These results imply that the “Keys” students’ performance on the 50‐question and 20‐

question tests is similar. Also, while there is some minor learning from the test exhibited by the

comparison group, that learning does not account for the majority of the achievement gains exhibited

by the “Keys” students between the pre‐ and posttest on the 20‐question instrument.

[Insert Table 5 about here]

While the results reported thus far show positive student achievement gains between the

pretest and the posttest, we estimated a regression model to further investigate the effect of the “Keys

to Financial Success” course while controlling for student characteristics and teacher effects. This

15

methodology mirrors the methodology used by Walstad, Rebeck, and MacDonald (2010) and is based on

the findings of Bosshardt and Watts (1990). The following linear model was estimated.

The dependent variable, , is the posttest raw score out of 20 for student of teacher . As

in both Bosshardt and Watts (1990) and Walstad, Rebeck, and MacDonald (2010), we controlled for

unobserved teacher effects by including , a fixed effect for each teacher. Ten independent variables

[X(1) through X(10)] were included in the regression. These independent variables were the students’

pretest raw score, a dummy variable that took the value 1 if the student was a member of the treatment

group and 0 if the student was a member of the comparison group; a dummy variable that took the

value 1 if the student was female and 0 otherwise; 0,1 dummy variables for the age groups (15 and

younger was the excluded group); a dummy variable that took the value 1 if the student reported

currently or in the past holding a job; a dummy variable that took the value 1 if the student reported

having a checking account; and a dummy variable that took the value 1 if the student reported having a

savings account.

The results for the unrestricted regression with teacher fixed‐effects, which includes all students

in both the treatment and comparison samples regardless of their teacher, are reported on the left side

of Table 6. As expected, the student’s pretest score was highly statistically significant, implying that prior

knowledge of personal finance was a good predictor of student knowledge on the posttest. The

estimated coefficient for the dummy variable that identified the treatment (“Keys”) students was 3.240

and highly statistically significant, implying that students who took the “Keys” course gained by 16.20

percentage points on average from the pretest to the posttest relative to the comparison students as

measured by the 20‐item test.

16

None of the estimated coefficients on gender or age were statistically significant. These results

imply that, counter to the results found by Danes and Haberman (2007) and Varcoe et al. (2005), there

is no gender‐specific effect of the “Keys” course on student achievement in personal finance.

Furthermore, the results imply that there are no age‐specific effects of the course on student

achievement in personal finance.

The estimated coefficient on the variable that captured whether the student currently held or

had ever held a job was statistically insignificant. This result implies that work experience did not impact

personal finance achievement.

The estimated coefficient on the variable that captured whether the student owns a checking

account was statistically insignificant. However, the estimated coefficient for whether the student owns

a savings account was positive and statistically significant at the 10 percent level.

On the right side of Table 6, we report the results from estimation of the same linear model with

teacher fixed‐effects conducted on a restricted sample of only those treatment and comparison

students’ tests collected by the same teacher. As in the unrestricted regression, the estimated

coefficient for the treatment group dummy variable implies a 16.17‐percentage‐point increase in

student achievement as a result of the “Keys” course. Like the results for the unrestricted regression,

gender, age, and job experience were all statistically insignificant. Checking account ownership is

positive and weakly statistically significant in the regression run on the restricted sample. In contrast to

the unrestricted regression, savings account ownership was highly statistically significant. The estimated

coefficient implies a 2.59 percentage point marginal effect of savings account ownership on the

student’s personal finance achievement. This positive effect may reflect the fact that students who have

savings accounts are likely to come from families in which there is more personal finance knowledge

passed from parents to children.

[Insert Table 6 about here]

17

CONCLUSIONS

The objective of this study was to investigate the effectiveness of a semester personal finance

course that uses a specific curriculum, “Keys to Financial Success,” taught by teachers who attended a

30‐hour training course. The results from the pre‐and posttests show that students who take the “Keys”

personal finance course exhibit a statistically significant increase in their personal finance achievement

as measured by the personal finance knowledge test. Students in a comparison group showed very little

gain in personal finance achievement over the same period. This study lends support to the notion that

students who are exposed to a specific personal finance curriculum and who receive instruction from

trained teachers experience achievement gains in their personal finance knowledge. Well‐known

limitations on conducting research on the effectiveness of semester courses in the U.S. meant that a

true experimental study design was impossible. Nevertheless, given the few opportunities afforded

researchers to collect pre‐ and posttest student data from semester‐long personal finance courses, our

findings, based on test results from nearly 2,000 students, lend support for the growing body of research

that shows that personal financial education, if well designed and properly implemented, can increase

students’ achievement in personal finance.

18

REFERENCES Bernanke, Ben. 2006. Financial Literacy: Testimony Before the Committee on Banking, Housing, and

Urban Affairs of the United States Senate. http://www.federalreserve.gov/newsevents/testimony/Bernanke20060523a.htm.

Bosshardt, William and Michael Watts. 1990. Education and Saving: The Long‐Term Effects of High School Financial Curriculum Mandates. Journal of Public Economics 85: 265‐276.

Boyce, Laurie and Sharon Danes. 1997‐98. Evaluation of the NEFE High School Financial Planning

Program, 1997‐1998. (report of a study sponsored by the National Endowment for Financial Education) http://www.nefe.org/pages/education.html.

Braunstein, Sandra and Carolyn Welch. 2002. Financial Literacy: An Overview of Practice, Research and

Policy. Federal Reserve Bulletin, Nov., 445‐457. Caldwell, Jean, J. Davis, Suzanne Gallagher, Jane Lopus, John Morton, Mark Schug, Mary Suiter, Phil

VanFossen, Donald Wentworth, and William Wood. 2004. Learning, Earning and Investing: High School. New York: National Council on Economic Education.

CEE (Council for Economic Education). 2009. Survey of the States 2009: Economic and Personal Finance

Education in Our Nation’s Schools. New York: CEE. http://www.councilforeconed.org/about/survey2009/.

Danes, Sharon M. and Heather R. Haberman. 2007. Teen Financial Knowledge, Self‐Efficacy, and Behavior: a Gendered View. Journal of Financial Counseling and Planning 18: 48‐60.

Fox, Jonathan, Suzanne Bartholomae, and Jankook Lee. 2005. Building the Case for Financial Education.

The Journal of Consumer Affairs 39: 195‐214.

Greenspan, Allan. 2001. Remarks by Chairman Alan Greenspan: The Importance of Education in Today’s Economy. Speech presented at the Community Affairs Research Conference of the Federal Reserve System. http://www.federalreserve.gov/boarddocs/speeches/2001/20011026/default.htm.

Harter, Cynthia and John Harter. 2009. Assessing the Effectiveness of Financial Fitness for Life in Eastern

Kentucky. Journal of Applied Economics and Policy 28: 20‐33.

Hathaway, Ian and Sameer Khatiwada. 2008. Do Financial Education Programs Work? Federal Reserve Bank of Cleveland Working Paper No. 08‐03. http://www.clevelandfed.org/research/workpaper/2008/wp0803.pdf.

19

Hinojosa, Trisha, Shazia Miller, Andrew Swanlund, Kelly Hallberg, Megan Brown, and Brenna O’Brien. 2008. The Stock Market Game Study: A Brief Report. DC: Learning Point Associates. http://www.learningpt.org/smg/SMG_Study.pdf.

Jacobs, Francine. 1988. The Five‐Tiered Approach to Evaluation: Context and Implementation. In

Evaluating Family Programs, ed. H. Weiss and F. Jacobs, 36‐68. New York: Aldine DeGruyter.

Mandell, Lewis. 2006. Financial Literacy: Improving Education Results of the 2006 National Jump$tart Survey Washington, D.C.: Jumpstart Coalition.

Mandell, Lewis. 2008. The Financial Literacy of Young American Adults: Results of the 2008 National

Jump$tart Coalition Survey of High School and College Students. DC: Jump$tart Coalition. Mandell, Lewis and Linda Klein. 2007. Motivation and financial literacy. Financial Services Review 16:

105‐116. _______________. 2009. The Impact of Financial Literacy Education on Subsequent Financial Behavior.

Journal of Financial Counseling and Planning 20: 14‐24. Morton, John and Mark Schug. 2001. Financial Fitness for Life: Bringing Home the Gold (Grades 9‐12). New York: National Council on Economic Education.

Swinton, John, Thomas DeBerry, Benjamin Scafidi, and Howard Woodard. 2007. The Impact of Financial

Education Workshops for Teachers on Students’ Economic Achievement. The Journal of Consumer Education 24: 63‐77.

Tennyson, Sharon and Chau Nguyen. 2001. State Curriculum Mandates and Student Knowledge of

Personal Finance. The Journal of Consumer Affairs 35: 241‐262. Todd, Richard. 2002. Financial Literacy Education: A Potential Tool for Reducing Predatory Lending? The

Region (Federal Reserve Bank of Minneapolis) December: 6‐13. Varcoe, Karen, Allen Martin, Zanna Devitto, and Charles Go. 2005. Using a Financial Education

Curriculum for Teens. Journal of Financial Counseling and Planning 16: 63‐71. VISA. 2000. Practical Money Skills. San Francisco: VISA, U.S.A., Inc. Walstad, William and Ken Rebeck. 2005. Financial Fitness for Life: High School Test Examiner’s Manual

(grades 9‐12). New York: Council for Economic Education. Walstad, William, Ken Rebeck, and Richard MacDonald. 2010. The Effects of Financial Education on the

Financial Knowledge of High School Students. The Journal of Consumer Affairs 44: 336‐357.

Willis, Lauren. 2008. Against Financial Literacy Education. University of Penn Law School. Public Law Research Paper No. 08‐10.

20

TABLE 1 Schools and Teachers in the Keys to Financial Success Program

School Year

Number of Schools Adopting

Number of Schools Leaving Total Schools

New Teachers Trained

Total Teachers Trained

2001‐2002 1 0 1 1 1 2002‐2003 6 0 7 7 8 2003‐2004 8 0 15 13 21 2004‐2005 6 1 20 5 26 2005‐2006 22 1 41 29 55 2006‐2007 24 9 56 40 95 2007‐2008 13 5 64 22 117 2008‐2009 12 3 73 17 134 2009‐2010 15 0 88 26 160 2010‐2011 31 1 118 34 194

21

TABLE 2 20‐Question Keys to Financial Success Test: Content and Cognitive Level KeysTest Item

FFL Test Item Content Cognitive Level

Keys Theme

FFL Theme

1 2 Reasons for saving and investing Comprehension 4 1 2 7 Opportunity cost Application 1, 2 1 3 9 Determinants of income Comprehension 1 1 4 10 Financial decision‐making Knowledge 1 1 5 18 Taxes and transfer payments Knowledge 3 2 6 19 Taxes and transfer payments Knowledge 3 2 7 20 Taxes and transfer payments Application 3 2 8 21 Saving and investing Comprehension 4 3 9 24 Rate of return on investment Application 4 3 10 27 Risk, return, and liquidity investment Comprehension 4 3 11 29 Buy and sell investments Comprehension 4 3 12 30 Buy and sell investments Knowledge 4 3 13 33 Credit history and records Knowledge 5 4 14 34 Credit history and records Knowledge 5 4 15 37 Sources of credit Comprehension 5 4 16 38 Rights and responsibilities of buyers,

sellers, and creditors Application 5 4

17 44 Use of money management tools Comprehension 6 5 18 48 Insurance, risk management Application 7, 9 5 19 NA Budgeting Comprehension 3, 8 5 20 NA Use of money management tools Knowledge 6 5

Note: Questions 19 and 20 were test items written by the authors.

Keys Themes 1. Goals and Decision‐Making 2. Careers and Planning 3. Budgeting 4. Saving and Investing 5. Credit

6. Banking Services 7. Transportation Issues 8. Housing Issues 9. Risk Protection

FFL Themes 1. The Economic Way of Thinking 2. Earning Income 3. Saving 4. Spending and Using Credit 5. Money Management

22

TABLE 3 Treatment and Comparison Sample Demographics

Treatment Group Comparison Group

Total 1701 261 Gender

Male 751 (44.15%) 123 (47.13%) Female 950 (55.85%) 138 (52.87%)

Age <15 307 (18.05%) 29 (11.11%) 16 284 (16.70%) 38 (14.56%) 17 468 (27.51%) 101 (38.70%) 18 574 (33.74%) 87 (33.33%) >19 68 (4.00%) 6 (2.30%)

Has Held a Job No 520 (30.57%) 92 (35.25%) Yes 1181 (69.43%) 169 (64.75%)

State Delaware 448 (26.34%) 96 (36.78%) New Jersey 166 (9.76%) 42 (16.09%) Pennsylvania 1087 (63.90%) 123 (47.13%)

Checking Account No 1027 (60.38%) 165 (63.22%) Yes 674 (39.62%) 96 (36.78%)

Savings Account No 519 (30.51%) 74 (28.35%) Yes 1182 (69.49%) 187 (71.65%)

23

TABLE 4 Percentage Correct on 20‐Question “Keys” Test by “Keys” Student Characteristics

Pretest Posttest Difference n t‐Value

Total 38.55% 63.27% 24.72% 1701 48.11

Gender

Male 38.20% 63.37% 25.17% 751 31.33 Female 38.84% 63.20% 24.36% 950 36.59

Age

<15 34.97% 62.64% 27.67% 307 20.06 16 35.39% 64.03% 28.64% 284 21.16 17 40.15% 64.28% 24.13% 468 26.49 18 41.38% 63.39% 22.01% 574 27.39 >19 33.16% 55.07% 21.91% 68 8.29

Has Held a Job

No 35.77% 62.60% 26.83% 520 26.03 Yes 39.78% 63.57% 23.79% 1181 40.82

State

Delaware 40.65% 57.82% 17.18% 448 20.44 New Jersey 37.23% 66.63% 29.40% 166 17.63 Pennsylvania 37.89% 65.01% 27.12% 1087 41.23

Checking Account

No 37.46% 62.73% 25.27% 1027 37.40 Yes 40.22% 64.10% 23.88% 674 30.31

Savings Account

No 34.68% 60.05% 25.37% 519 25.19 Yes 40.25% 64.69% 24.44% 1182 41.22

24

TABLE 5 Percentage Correct on “Keys to Financial Success” Knowledge Test: “Keys” Students and Comparison

Keys Students Comparison Students

Pretest(%) Posttest(%) Difference n Pretest Posttest Difference n

50‐Question Test 42.47% 63.60% 21.14%*** 1701 (13.56) (19.34)

20‐Question Test 38.55% 63.27% 24.72%*** 1701 41.72% 44.87% 3.14%*** 261

(13.96) (20.88) (14.17) (15.24)

***p < 0.01, two‐tailed t‐test

Note: Sample standard deviations are reported in parentheses.

25

TABLE 6 Fixed Effects Regression Results

Variable Unrestricted (n=1962)

Restricted (n=1117)

Keys Test Pretest Score 0.463 (0.047)*** 0.445 (0.066)*** Keys Students 3.240 (0.759)*** 3.233 (0.705)*** Gender (1 = female) 0.050 (0.126) ‐0.127 (0.159) Age = 16 ‐0.496 (0.653) 0.189 (0.561) Age = 17 ‐0.640 (1.021) 0.557 (0.532) Age = 18 ‐0.639 (0.991) 0.780 (0.527) Age = 19+ ‐0.906 (1.102) 0.325 (0.840) Job (1 = has worked) ‐0.126 (0.141) ‐0.156 (0.204) Checking Account (1 = Yes) ‐0.205 (0.139) ‐0.404 (0.208)* Savings Account (1 = Yes) 0.283 (0.152)* 0.518 (0.198)***

Constant 2.945 (1.340)** 2.324 (0.638)***

R2 0.429 0.486 F Value 30.60*** 33.11***

*p < 0.10, **p < 0.05, ***p < 0.01, two‐tailed test Note: Standard errors in parentheses