paper 5 : advanced accounting · (v) advances for tools/cranes etc. ` 1crore (vi) purchase of...

TRANSCRIPT

PAPER – 5 : ADVANCED ACCOUNTING

Question No.1 is compulsory.

Candidates are also required to answer any five questions from the remaining six questions.

Working notes should form part of the respective answers.

Wherever necessary, candidates are permitted to make suitable assumptions which should be

disclosed by way of a note.

Question 1

Answer the following questions:

(a) “While calculating diluted EPS, effect is given to all dilutive potential equity shares that

were outstanding during the period.” Explain this statement in the light of relevant AS.

Also calculate the diluted EPS from the following information:

Net Profit for the current year (After Tax) ` 1,00,00,000

No. of Equity shares outstanding 10,00,000

No. of 10% Fully Convertible Debentures of ` 100 each

(Each Debenture is compulsorily & fully convertible into 10 equity shares)

1,00,000

Debenture interest expense for the current year ` 5,00,000

Assume applicable Income Tax rate @ 30%

(b) M/s. Zen Bridge Construction Limited obtained a loan of ` 64 crores to be utilized as under:

(i) Construction of Hill link road in Kedarnath: (work was held up totally for a month during the year due to heavy rain which are common in the geographic region involved)

` 50 crores

(ii) Purchase of Equipment and Machineries ` 6 crores

(iii) Working Capital ` 4 crores

(iv) Purchase of Vehicles ` 1crore

(v) Advances for tools/cranes etc. ` 1crore

(vi) Purchase of Technical Know how ` 2 crores

(vii) Total Interest charged by the Bank for the year ending

31st March, 2016

` 1.6 crores

Show the treatment of Interest according to Accounting Standard by M/s. Zen Bridge

Construction Limited.

(c) While preparing its final accounts for the year ended 31st March, 2016, a company made

provision for bad debts @ 5% of its total debtors. In the last week of February, 2016 a

© The Institute of Chartered Accountants of India

2 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

debtor for ` 20 lakhs had suffered heavy loss due to an earthquake; the loss was not

covered by any insurance policy. In April, 2016 the debtor became a bankrupt. Can the

company provide for the full loss arising out of insolvency of the debtor in the final accounts

for the year ended 31st March, 2016?

Comment with reference to relevant Accounting Standard.

(d) A Company with a turnover of ` 375 crores and an annual advertising budget of ` 3 crores

had taken up the marketing of a new product. It was estimated that the company would

have a turnover of ` 37.5 croes from the new product. The company had debited to i ts

Profit and Loss account the total expenditure of ` 3 crores incurred on extensive special

initial advertisement campaign for the new product.

Is the procedure adopted by the Company correct? (5 x 4 = 20 Marks)

Answer

(a) As per AS 20 ‘Earnings per Share’, the net profit or loss for the period attributable to equity

shareholders and the weighted average number of shares outstanding during the period

should be adjusted for the effects of all dilutive potential equity shares for calculation of

diluted earnings per share. Hence, “in calculating diluted earnings per share, effect is

given to all dilutive potential equity shares that were outstanding during the period.”

Computation of diluted earnings per share=Adjusted net profit for the current year

Weighted average number of equity shares

Adjusted net profit for the current year

`

Net profit for the current year (after tax) 1,00,00,000

Add: Interest expense for the current year 5,00,000

Less: Tax relating to interest expense (30% of `5,00,000) (1,50,000)

Adjusted net profit for the current year 1,03,50,000

Weighted average number of equity shares

Number of equity shares resulting from conversion of debentures

=1,00,000 100

10

= 10,00,000 Equity shares

Weighted average number of equity shares used to compute diluted earnings per

share

= [(10,00,000 x 12) + (10,00,000 x 6)]/12 = 15,00,000 equity shares

Diluted earnings per share = ` 1,03,50,000 / 15,00,000 shares = ` 6.90 per share

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 3

Note: Interest on debentures for full year amounts to ` 10,00,000 (i.e. 10% of

` 1,00,00,000). However, interest expense amounting `5,00,000 has been given in the

question. It may be concluded that debentures have been issued at the mid of the year

and interest has been provided for 6 months.

(b) According to AS 16 ‘Borrowing costs’, qualifying asset is an asset that necessarily takes

substantial period of time to get ready for its intended use. As per the standard, borrowing

costs that are directly attributable to the acquisition, construction or production of a

qualifying asset should be capitalized as part of the cost of that asset. Other borrowing

costs should be recognized as an expense in the period in which they are incurred.

Capitalization of borrowing costs is also not suspended when a temporary delay is a

necessary part of the process of getting an asset ready for its intended use or sale.

The treatment of interest by Zen Bridge Construction Ltd. can be shown as:

Qualifying Asset

Interest to be capitalized ` in crores

Interest to be charged to Profit & Loss A/c ` in crores

Construction of hill road* Yes 1.25 1.6/64 x 50

Purchase of equipment and machineries

No

0.15

1.6/64 x 6

Working capital No 0.10 1.6/64 x 4

Purchase of vehicles No 0.025 1.6/64 x 1

Advance for tools, cranes etc. No

0.025

1.6/64 x 1

Purchase of technical know-how

No

0.05

1.6/64 x 2

Total 1.25 0.35

*Note: It is assumed that construction of hill road will normally take more than a year

(substantial period of time), hence considered as qualifying asset.

(c) As per AS 4 ‘Contingencies and Events Occurring After the Balance Sheet Date’,

adjustment to assets and liabilities are required for events occurring after the balance sheet

date that provide additional information materially affecting the determination of the

amounts relating to conditions existing at the Balance Sheet date.

A debtor for ` 20,00,000 suffered heavy loss due to earthquake in the last week of

February, 2016 which was not covered by insurance. This information with its implications

was already known to the company. The fact that he became bankrupt in April, 2016 (after

the balance sheet date) is only an additional information related to the condition existing

on the balance sheet date. However, bankruptcy of debtors is an adjusting event.

© The Institute of Chartered Accountants of India

4 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Accordingly, full provision for bad debts amounting ` 20,00,000 should be made, to cover

the loss arising due to the insolvency of a debtor, in the final accounts for the year ended

31st March 2016. Since the company has already made 5% provision of its total debtors,

additional provision amounting ` 19,00,000 shall be made (20,00,000 x 95%).

(d) According to AS 26 ‘Intangible Assets’, “expenditure on an intangible item should be

recognized as an expense when it is incurred unless it forms part of the cost of an intangible

asset”.

In the given case, advertisement expenditure of ` 3 crores had been taken up for the

marketing of a new product which may provide future economic benefits to an enterprise

by having a turnover of `37.5 crores. Here, no intangible asset or another asset is acquired

or created that can be recognized.

Therefore, the accounting treatment by the company of debiting the entire advertising

expenditure of `3 crores to the Profit and Loss account of the year is correct.

Question 2

X, Y and Z are in partnership sharing profits and losses in the ratio of 5:4:4. The Balance Sheet

of the firm as on 31st March, 2016 is as below:

Liabilities ` Assets `

X’s Capital 60,000 Factory Building 96,640

Y’s Capital 40,000 Plant and Machinery 65,100

Z’s Capital 50,000 Trade Receivable 21,600

Y’s Capital 18,000 Inventories 49,560

Trade Payable 66,000 Cash at Bank 1,100

2,34,000 2,34,000

On Balance Sheet date, all the three partners have decided to dissolve their partnership. Since the

realisation of assets was protracted, they decided to distribute amounts as and when feasible and

for this purpose they appoint Z who was to get as his remuneration 1% of the value of the assets

realised other than cash at bank and 10% of the amount distributed to the partners.

Assets were realised piecemeal as under:

`

First instalment 74,600

Second instalment 69,301

Third instalment 40,000

Last instalment 28,000

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 5

Dissolution expenses were provided for estimated

amount of

` 12,000

The creditors were settled finally for ` 63,600

You are required to prepare a statement showing distribution of cash amongst the partners by

"Highest Relative Capital Method". (16 Marks)

Answer

Statement showing distribution of cash amongst the partners

Trade Payable

Y’s Loan

Capitals

X (`) Y (`) Z (`)

Balance Due 66,000 18,000 60,000 40,000 50,000

On 1st Instalment amount with the firm ` (1100 + 74,600)

75,700

Less: Dissolution expenses provided for

(12,000)

63,700

Less: Z’s remuneration of 1% on assets realized (74,600 x 1%)

(746)

62,954

Less: Payment made to Trade Payables

(62,954)

(62,954)

Balance due Nil 3046

2nd instalment realised 69,301

Less: Z’s remuneration of 1% on assets realized (69,301 x 1%)

(693)

68,608

Less: Payment made to Trade Payables

(646)

(646)

Transferred to P& L A/c 2,400

67,962

Less: Payment for Y’s loan A/c

(18,000) (18,000)

© The Institute of Chartered Accountants of India

6 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Amount available for distribution to partners

49,962

nil

Less: Z’s remuneration of 10% of the amount distributed to partners (49,962 x 10/110)

(4,542)

Balance to be distributed to partners on the basis of HRCM

45,420

Less: Paid to Z (W.N.1) (2,000) (2,000)

43,420 48,000

Less: Paid to X and Z in 5:4 (W.N.1)

(18,000) (10,000) - (8,000)

Balance due 25,420 50,000 40,000 40,000

Less: Paid to X, Y & Z in 5:4:4

25,420

(9,778)

(7,821)

(7,821)

Nil

Amount of 3rd instalment 40,000 40,222 32,179 32,179

Less: Z’s remuneration of 1% on assets realized (40,000 x 1%)

(400)

39,600

Less: Z’s remuneration of 10% of the amount distributed to partners (39,600 x 10/110)

(3,600)

36,000

Less: Paid to X, Y, Z in 5:4:4 for (W.N.1)

(36,000)

(13,846)

(11,077)

(11,077)

Nil 26,376 21,102 21,102

Amount of 4th and last instalment

28,000

Less: Z’s remuneration of 1% on assets realized (28,000 x 1%)

(280)

27,720

© The Institute of Chartered Accountants of India

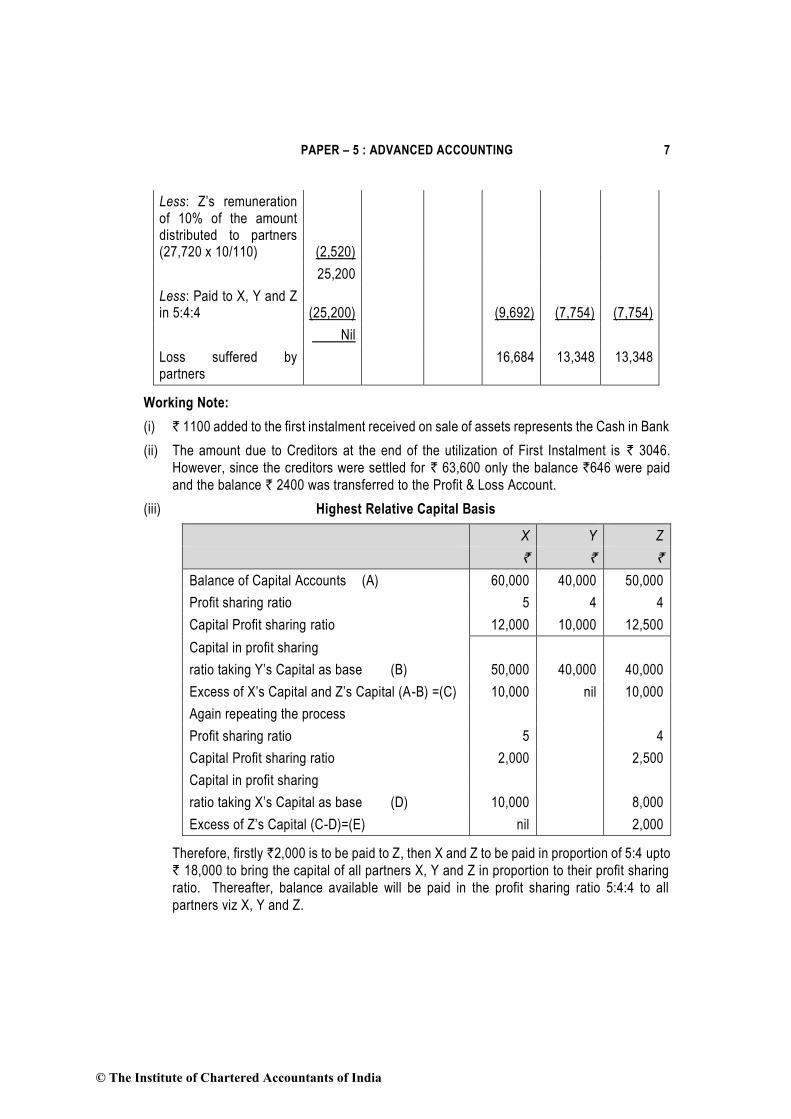

PAPER – 5 : ADVANCED ACCOUNTING 7

Less: Z’s remuneration of 10% of the amount distributed to partners (27,720 x 10/110)

(2,520)

25,200

Less: Paid to X, Y and Z in 5:4:4

(25,200)

(9,692)

(7,754)

(7,754)

Nil

Loss suffered by partners

16,684 13,348 13,348

Working Note:

(i) ` 1100 added to the first instalment received on sale of assets represents the Cash in Bank

(ii) The amount due to Creditors at the end of the utilization of First Instalment is ` 3046.

However, since the creditors were settled for ` 63,600 only the balance `646 were paid

and the balance ` 2400 was transferred to the Profit & Loss Account.

(iii) Highest Relative Capital Basis

X Y Z

` ` `

Balance of Capital Accounts (A) 60,000 40,000 50,000

Profit sharing ratio 5 4 4

Capital Profit sharing ratio 12,000 10,000 12,500

Capital in profit sharing

ratio taking Y’s Capital as base (B) 50,000 40,000 40,000

Excess of X’s Capital and Z’s Capital (A-B) =(C) 10,000 nil 10,000

Again repeating the process

Profit sharing ratio 5 4

Capital Profit sharing ratio 2,000 2,500

Capital in profit sharing

ratio taking X’s Capital as base (D) 10,000 8,000

Excess of Z’s Capital (C-D)=(E) nil 2,000

Therefore, firstly `2,000 is to be paid to Z, then X and Z to be paid in proportion of 5:4 upto

` 18,000 to bring the capital of all partners X, Y and Z in proportion to their profit sharing

ratio. Thereafter, balance available will be paid in the profit sharing ratio 5:4:4 to all

partners viz X, Y and Z.

© The Institute of Chartered Accountants of India

8 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Question 3

(a) A company had 40,000; 10 debentures of `100 each outstanding on 1 April, 2015

redeemable on 31st March, 2016.

On that day, sinking fund was ` 37,45,000 represented by 5,000 own debentures

purchased at average price of ` 99 and 9% stocks of the face value of ` 33,00,000. The

annual instalment was ` 1,42,000. On 31st March, 2016, the investments were realized at

` 98 and the debentures were redeemed.

Draw the following accounts for the year ending 31 st March, 2016 :

(i) 10% Debentures Account.

(ii) Debenture Redemption Sinking Fund Account (10 Marks)

(b) The following is the Summarized Balance Sheet of M/s. Vriddhi Infra Ltd. as on 31st March,

2016:

Equity & Liabilities Amount (`)

Assets Amount (`)

Shareholders Fund

1. (a) Share Capital: 1. Non Current Assets

1,00,000 Equity Shares of ` 10 each fully paid up

10,00,000 (a) Fixed (Tangible) Assets:

(b) Reserve & Surplus: Land & Building 21,50,000

Securities Premiums 3,00,000 Plant & Machinery 15,00,000

General Reserve 2,50,000 (b) Non- current Investment

2,00,000

Profit & Loss Account Surplus

1,50,000

2. Non-Current Liabilities 2. Current Assets

Long-Term Borrowings: (a) Trade Receivables 5,50,000

10% Debentures (Secured by floating charge on all assets)

20,00,000 (b) Inventories 1,80,000

Unsecured Loans 8,00,000 (c) Cash and Cash Equivalents

40,000

3. Current Liability & Provisions

Trade Payables 1,20,000

Total 46,20,000 46,20,000

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 9

On 21st April, 2016 the Company announced the buy back of 25,000 of its equity shares @

` 15 per share. For this purpose, it sold all its investment for ` 2.50 lakhs.

On 25th April, 2016, the company achieved the target of buy back. On 1st May, 2016 the

company issued one fully paid up share of ` 10 each by way of bonus for every five equity

shares held by the equity shareholders.

You are requested to pass necessary Journal Entries for the above transactions.

All necessary workings should form part of your answer. (6 Marks)

Answer

(a) 10% Debentures Account

Date Particulars ` Date Particulars `

31st March, 2016

To Own debentures A/c

5,00,000 1st April, 2015

By Balance b/d

40,00,000

To Bank A/c 35,00,000

40,00,000 40,00,000

Debenture Redemption Sinking Fund Account

Date Particulars ` Date Particulars `

31st March, 2016

To 9% Stock A/c (loss) (W.N.5)

16,000

1st April, 2015

By Balance b/d 37,45,000

To General reserve A/c (Bal. fig.)

40,00,000

31st March, 2016

By Profit and loss A/c

1,42,000

To Capital Reserve

2,23,000 By Interest on sinking fund A/c (W.N.3)

3,47,000

By Own debentures A/c (W.N.4)

5,000

42,39,000 42,39,000

© The Institute of Chartered Accountants of India

10 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Working Notes:

1. Amount of stock as on 1st April, 2015

`

Sinking fund balance as on 1st April, 2015 37,45,000

Less: Own debentures (4,95,000)

32,50,000

2. Sales value of 9% stock

= Face value / ` per stock

= `33,00,000 / `100 = 33,000 stock

Sales value = 33,000 stock x ` 98 per stock

= ` 32,34,000

3. Interest credited to Sinking Fund

(i) Interest on 9% stock (`33,00,000 x 9%) ` 2,97,000

(ii) Interest on own debentures (5,000 Debentures x `100 x 10%) ` 50,000

` 3,47,000

4. Own Debentures Account

` `

1st April, 2015

To Balance b/d

4,95,000 31st March, 2016

By 10% Debentures A/c

5,00,000

31st March, 2016

To Sinking fund A/c

5,000

5,00,000 5,00,000

5. 9% Stock Account

` `

1st April, 2015

To Balance b/d

(Face value `33,00,000) (W.N.1)

32,50,000

31st March, 2016

By Bank account (W.N.2)

32,34,000

By Sinking fund (loss on sales)

16,000

32,50,000 32,50,000

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 11

(b) In the books of Vriddhi Infra Ltd.

Journal Entries

Date 2016

Particulars Dr. Cr.

` `

April 21 Bank A/c Dr. 2,50,000

To Investment A/c 2,00,000

To Profit on sale of investment 50,000

(Being investment sold on profit)

April 25 Equity share capital A/c Dr. 2,50,000

Securities premium A/c Dr. 1,25,000

To Equity shares buy back A/c 3,75,000

(Being the amount due to equity shareholders on buy back)

Equity shares buy back A/c Dr. 3,75,000

To Bank A/c 3,75,000

(Being the payment made on account of buy back of 25,000 Equity Shares)

General Reserve A/c / P&L A/c Dr. 2,50,000

To Capital redemption reserve A/c 2,50,000

(Being amount equal to nominal value of buy back shares from free reserves transferred to capital redemption reserve account as per the law)

1st May Capital redemption reserve A/c Dr. 1,50,000

To Bonus shares A/c (W.N.1) 1,50,000

(Being the utilization of capital redemption

reserve to issue bonus shares)

Bonus shares A/c Dr. 1,50,000

To Equity share capital A/c 1,50,000

(Being issue of one bonus equity share for every five equity shares held)

It is assumed that there is bank overdraft amounting ` 85,000 [(40,000 + 2,50,000) less ` 3,75,000]

© The Institute of Chartered Accountants of India

12 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Working Note:

Amount of bonus shares = 105

1000,00,1

25,000 -

= 15,000 x ` 10 = ` 1,50,000

Question 4

The summarized Balance Sheet of M/s. X Limited as at 31st March, 2016 are as follows:

Equity & Liabilities Amount (`)

Assets Amount (`)

Shareholder Fund: Non-Current Assets 6,50,000

Share Capital Land & Building

50,000 equity shares of ` 10 each fully paid

5,00,000 Current Assets

75,000; 10% Preference Shares of ` 10 fully paid up

7,50,000 Sundry Current Assets 21,80,000

25,000 Equity Shares of ` 10 each, ` 8 per share paid up

2,00,000 Debenture issue expenses not written off

10,000

Profit & Loss Account (1,75,000)

Non-Current Liabilities:

13% Debentures 7,50,000

Mortgage Loan 3,50,000

Current Liabilities:

Bank Overdraft 1,50,000

Trade Creditors 1,90,000

Income Tax Arrears (Assessment completed in February, 2016)

1,25,000

28,40,000 28,40,000

Mortgage loan was secured against Land and Building. Debentures were secured by a floating

charge on all assets. The company was unable to meet the payments and therefore the

Debenture Holders appointed a Receiver for the Debenture Holders. He bought the L and &

Building to auction and realized ` 8,00,000. He also took charge of Sundry Assets of value of

` 11,80,000 and realized ` 10,00,000. Bank overdraft was secured by personal guarantee of

the Directors of the company and on the Bank raising a demand, the Directors paid off the due

from their personal resources. Cost incurred by the receiver were ` 9,750 and by the Liquidator

` 15,000. The Receiver was not entitled to any remuneration but the Liquidator was to receive

2% fee on the value of assets realized by him. Preference Shareholders have not been paid

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 13

Dividend for period after 31st March, 2014 and interest for the last half year was due to

Debenture Holders. Rest of the Assets were realized at ` 7,50,000.

Prepare the Accounts to be submitted by the Receiver and Liquidator. (16 Marks)

Answer

Receiver’s Receipts and Payments Account

Receipts ` ` Payments ` `

Sundry Assets realised 10,00,000 Costs of the Receiver 9,750

Surplus received from Mortgage loan: -

Sale Proceeds of land

Preferential payments:

Income Taxes (raised within 12 months)

-

1,25,000

and building

Less: Applied to

8,00,000 Debentures holders: Principal amount

7,50,000

Discharge mortgage loan

(3,50,000)

4,50,000

Interest for half year

Surplus transferred to the Liquidator

48,750 7,98,750

5,16,500

14,50,000 14,50,000

Liquidator’s Final Statement of Account

Receipts ` Payments `

Surplus received from Receiver

5,16,500 Cost of Liquidation:

Remuneration to Liquidator

(7,50,0000 x 2%)

15,000

Assets Realized 7,50,000 15,000

Calls on Contributories: Unsecured Creditors:

On holder of 25,000 Equity Shares at the rate of ` 1.38 per share

34,500 Trade

Directors for Bank O/D cleared

1,90,000

1,50,000

3,40,000

Preferential Shareholders:

Capital 7,50,000

Arrears of Dividends 1,50,000 9,00,000

Equity shareholders:

Return of money to holders of 50,000 equity shares at 62 paise each

31,000

13,01,000 13,01,000

© The Institute of Chartered Accountants of India

14 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Working Note:

Call from partly paid shares

Deficit before call from Equity Shares `

= ` (5,16,500+7,50,000) less ` (15,000+15,000+3,40,000+9,00,000) = (3,500)

`

(3500)

Notional call on 25,000 shares @ ` 2 each 50000

Net balance after notional call (a) 46500

No. of shares deemed fully paid (b) 75000

Refund on fully paid shares 46,500/ 75,000= ` 0.62

Call on partly paid share (2 – 0.62) = ` 1.38

Question 5

(a) From the following facts drawn from the records of Honest Bank for the year ended 31 st

March, 2015, prepare the accounts as mentioned below:

(i) On 1st April, 2015 Bills for Collection were ` 28,00,000. During 2014-15, bills

received for collection were ` 2,58,00,000. Bills collected were ` 1,88,00,000. Bills

dishonoured and returned were ` 22,00,000.

Prepare Bills for Collection (Assets) Account and Bills for Collection (Liability) Account.

(ii) On 1st April, 2014, Acceptance, Endorsement etc. not yet satisfied amounted to

` 58,00,000. During the year, Acceptances, Endorsements, Guarantees etc. were

` 1,76,00,000. The Bank honoured acceptances of ` 1,00,00,000 and a client paid

` 40,00,000 against guaranteed liabilities. The Bank paid `4,00,000 which clients

failed to pay.

Prepare "Acceptances, Endorsements and Other Obligations Account" in the General

Ledger.

(iii) A loan of ` 24,00,000 advanced by the Bank on 30 th August, 2014 @ 10 per annum,

whose interest is payable half-yearly. The loan was outstanding as on 31st March,

2015. Nothing was paid either towards Principal or Interest of this loan. The security

for the loan was 40,000 fully paid shares of ` 100 each. The shares were quoted on

the stock exchange on 30 th September, 2014 at ` 90 per share. Due to fluctuations,

the price fell to ` 50 per share in January, 2015. On 31st March, 2015 the share price

quoted on the stock exchange was ` 96 per share.

State giving reasons, whether the loan would be classified as secured or unsecured

in the Balance Sheet of the Company as on 31st March, 2015.

To be read as 1st April, 2014.

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 15

(iv) The following balances were taken from the Trial Balance as on 31 st March, 2015.

Dr. (`) Cr (`)

Interest & Discounts 3,92,00,000

Rebate for Bill Discounted 80,000

Bills Discounted & Purchased 16,00,000

Proportionate discounts not yet earned for Bills to mature in 2014-15 were ` 56,000.

Prepare the following Accounts:

(a) Rebate on Bills Account

(b) Interest and Discount Account. (10 Marks)

(b) From the following information given by M/s. Long Live Insurance Co. Ltd., you are required to pass necessary Journal Entries (with narration and required working notes) relating to Unexpired Risk Reserve. Also show "Unexpired Risk Reserve Account for 2015-16" in columnar form.

(i) On 31.03.15, it had reserve for unexpired risks amounting to ` 80 crores. Its composition was as under:

(a) ` 30 crores in respect of Marine insurance business

(b) ` 40 crores in respect of Fire insurance business and

(c) ` 10 crores in respect of Miscellaneous insurance business

(ii) M/s. Long Live Insurance Co. Ltd. reserves 100 of net premium income in respect of Marine insurance business and 50 of net premium income in respect of Fire and Miscellaneous income policies.

(iii) During 2015-16, the following business was conducted:

` In crore

Marine Fire Miscellaneous

Premium Collect from:

Insured in respect of Policies issued 36 86 24

Other Insurance Companies in respect of risks undertaken

14 10 8

Premium paid/payable to other insurance Companies on Business ceded.

20 10 15

(6 Marks)

To be read as 2015-16

© The Institute of Chartered Accountants of India

16 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Answer

(a) (i) Bills for Collection (Assets) A/c

` `

April 1, 2014

To Balance b/d 28,00,000 2014-15 By Bills for Collection

2014-15 (Liabilities) A/c 1,88,00,000

To Bills for Collection

By Bills for collection

(liabilities) A/c 2,58,00,000 (Liabilities) A/c 22,00,000

2015

Mar. 31 By Balance c/d 76,00,000

2,86,00,000 2,86,00,000

Bills for Collection (Liabilities) Account

` `

2014-15 To Bills for collection

(Assets) A/c

1,88,00,000 Apr. 1, 2014

By Balance b/d 28,00,000

To Bills for Collection

22,00,000 2014-15 By Bills for collection

2,58,00,000

(Assets) A/c (Assets) A/c

2015

Mar. 31 To Balance c/d 76,00,000

2,86,00,000 2,86,00,000

(ii) In the General Ledger

Acceptances, Endorsement & other Obligations Account

` `

2014-15 To Constituents’ Liability for Acceptance, Endorsement, etc.

1,00,00,000 1.4.2014 By Balance b/d 58,00,000

To Constituents’ Liability for Acceptances, Endorsement etc.

40,00,000 2014-15 By Constituents, Liabilities for Acceptances, Endorsements, etc.

1,76,00,000

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 17

To Constituents’ Liability for Acceptances, Endorsements, etc. (amount paid on failure of clients)

4,00,000

31.3.2015 To Balance c/d 90,00,000

2,34,00,000 2,34,00,000

(iii) For classifying loans as fully secured or otherwise, the value of the security as on the

last date of the year is considered. The value of the security is ` 38,40,000 (40,000

shares x ` 96 per share) covering the loan and the interest due comfortably. Hence

it is to be treated as good and fully secured loan.

(iv) Rebate on Bills Discounted Account

` `

2014-15 To Interest and Discount A/c

80,000 2014

Apr. 1

By Balance b/d

80,000

2015 Mar. 31

To Balance c/d 56,000

2015

Mar 31

By Interest and Discount A/c

56000

1,36,000 1,36,000

Interest & Discount Account

2015 ` 2014 `

Mar. 31 To Rebate on Bills Discount A/c

56,000 Apr. 1 By Rebate on Bills Discount A/c

80,000

To Profit & Loss A/c

3,92,24000 2014-15 By Bills Purchased & Discounted/Cash & sundries

3,92,00,000

3,92,80,000 3,92,80,000

(b) In the books of Long Live Insurance Co. Ltd.

Journal Entries

Date Particulars (` in crores)

Dr. Cr.

1.4.2015 Unexpired Risk Reserve (Fire) A/c Dr. 40.00

Unexpired Risk Reserve (Marine) A/c Dr. 30.00

© The Institute of Chartered Accountants of India

18 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

Unexpired Risk Reserve (Miscellaneous) A/c Dr. 10.00

To Fire Revenue Account 40.00

To Marine Revenue Account 30.00

To Miscellaneous Revenue Account 10.00

(Being unexpired risk reserve brought forward from last year)

31.3.2016 Marine Revenue A/c Dr. 30

To Unexpired Risk Reserve(Marine) A/c 30

(Being closing reserve for unexpired risk created at 100% of net premium income for marine)

Fire Revenue A/c Dr. 43

To Unexpired Risk Reserve(Fire) A/c 43

(Being closing reserve for unexpired risk created at 50% of net premium income for Fire)

Miscellaneous Revenue A/c Dr. 8.5

To Unexpired Risk Reserve(Misc) A/c 8.5

(Being closing reserve for unexpired risk created at 50% net premium income for Misc)

Unexpired Risk Reserve Account

Date Particulars Marine (`)

Fire (`)

Misc (`)

Date Particulars Marine (`)

Fire (`)

Misc (`)

1.4.2015 To Revenue A/c 30 40 10 1.4.2015 By Balance b/d 30 40 10

31.3.2016 To Balance c/d 30 43 8.5 31.3.2016 By Revenue A/c 30 43 8.5

60 83 18.5 60 83 18.5

Working Note:

Calculation of Closing balance of Reserve for Unexpired Risks

Marine Fire Misc

Premium Collected from:

a. Insured in respect of policies issued

36.00

86.00

24.00

b. Other ins co’s in respect of risks undertaken

14.00 10.00 8.00

Total (a+b) 50.00 96.00 32.00

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 19

Less Premium paid/payable to other insurance companies on business ceded

20.00

10.00

15.00

30.00 86.00 17.00

% of creation of unexpired Risk Reserve 100% 50% 50%

Amount of Closing Unexpired Risk Reserve 30.00 43.00 8.50

Question 6

(a) M/s Shyam Udyog, a retail store, has two departments, Department X and Department Y

for each of which stock account and memorandum 'mark-up' account are kept. All the

goods supplied to each department are debited to the stock account at cost plus a 'mark -

up', which together make up the selling price of the goods and in the account the sale

proceeds of the goods are credited. The amount of 'mark-up' is credited to the

Departmental Mark-up Account. If the selling price of any goods is reduced below its

normal selling price, the reduction 'marked down' is adjusted both in the Stock Account

and the Departmental Mark-up Account. The rate of 'Mark up' for X Department is 33-1/3%

of the cost and for Y Department it is 50% of the cost .

The following figures have been taken from the books for the year ended March, 2016 :

X

Department Amount

(`)

Y

Department Amount

(`)

Stock as on April 1st at cost 3,15,000 5,58,000

Purchases 22,77,000 28,02,000

Sales 28,68,000 37,50,000

(1) The stock of Department X on April 1, 2015 included goods the selling price of which

had been marked down by ` 37,800. These goods were sold during the year at the

reduced prices.

(2) Certain stock of the value of ` 2,07,000 purchased from the Department X was later

in the year transferred to the Department Y and sold for ` 3,10,5000. As a result

though cost of the goods is included in the Department X the sale proceeds have

been credited to the Department Y.

(3) During the year 2015-16 to promote the goods, they were marked down as follows:

Cost (`) Marked down (`)

Department X 1,68,000 10,800

Department Y 3,00,000 60,000

All the goods marked down, were sold except of Department Y of the value of

` 1,50,000 marked down by ` 30,000.

© The Institute of Chartered Accountants of India

20 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

(4) At the time of stock taking on 31st March, 2016, it was discovered that cloth of

Department X of the cost of ` 11,700 was missing and it was decided that the amount

be written-off.

You are required to prepare for both the departments for the year ended 31st March, 2016:

(a) The Memorandum Stock Account; and

(b) The Memorandum Mark-up Account. (8 Marks)

(b) Mr. Chena Swami of Chennai trades in Refined Oil and Ghee. It has a branch at Salem.

He despatches 30 tins of Refined Oil @ ` 1,500 per tin and 20 tins of Ghee ` 5,000 per

tin on 1st of every month. The Branch has incurred expenditure of ` 45,890 which is met

out of its collections; this is in addition to expenditure directly paid by Head Office.

Following are the other details:

Chennai H.O. Salem B.O.

Amount (`) Amount (`)

Purchases:

Refined Oil 27,50,000

Ghee 48,28,000

Direct Expenses 6,35,800

Expenses paid by H.O. 76,800

Sales:

Refined Oil 24,10,000 5,95,000

Ghee 38,40,500 14,50,000

Collection during the year (including Cash Sales)

20,15,000

Remittance by Branch to Head Office 19,50,000

Chennai H.O.

Balance as on 01-04-2015

Amount (`)

31-03-2016

Amount (`)

Stock:

Refined Oil 44,000 8,90,000

Ghee 10,65,000 15,70,000

Building 5,10,800 7,14,780

Furniture & Fixtures 88,600 79,740

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 21

Salem Brach Office

Balance as on 01-04-2015

Amount (`)

31-03-2016

Amount (`)

Stock:

Refined Oil 22,500 19,500

Ghee 40,000 90,000

Sundry Debtors 1,80,000 ?

Cash in hand 25,690 ?

Furniture &Fixtures 23,800 21,420

Additional information:

(i) Addition to Building on 01-04-2015 ` 2,41,600 by H.O.

(ii) Rate of depreciation: Furniture & Fixtures @ 10% and Building @ 5% (already

adjusted in the above figure)

(iii) The Branch Manager is entitled to 10% commission on overall organisational profits

after charging such commission.

(iv) The General Manager is entitled to a salary of ` 20,000 per month.

(v) General expenses incurred by Head Office is ` 1,86,000.

You are requested to prepare Branch Account in the Head Office books and also prepare

Chena Swami’s Trading and Profit & loss Account (excluding branch transactions) for the

year ended 31st March, 2016. (8 Marks)

Answer

(a) Department X Memorandum Stock Account

2015-16

` ` 2015-16

` `

To Balance b/d By Sales 28,68,000

(3,15,000 + 1,05,000 – 37,800)

3,82,200 X Deptt. 2,07,000

To Purchases 22,77,000 Mark-up A/c

69,000 2,76,000

Markup 7,59,000 30,36,000 By Loss of stock A/c

11,700

Mark-up A/c

3,900 15,600

© The Institute of Chartered Accountants of India

22 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

By Mark-up A/c

10,800

By Balance c/d

2,47,800

34,18,200 34,18,200

Department X Memorandum Mark-up Account

2015-16 ` 2015-16 `

To Stock A/c (transfer) 69,000 By Balance b/d

To Stock A/c (re-sale) 3,900 (1,05,000-37,800) 67,200

To Stock A/c (mark down) 10,800 By Stock A/c 7,59,000

To Profit & Loss A/c 6,80,550

To Balance (1/4 of ` 2,47,800)

61,950

8,26,200 8,26,200

Working Note:

Verification of Profit `

Sales as per books 28,68,000

Add: Mark-down (37,800+10,800) 48,600

29,16,600

Gross Profit on fixed selling price @ 25% on ` 29,16,600 7,29,150

Less: Mark down (48,600)

6,80,550

Department Y Memorandum Stock Account

2015-16 ` 2015-16 `

To Balance b/d By Sales A/c 37,50,000

To Cost 5,58,000 By Mark-up A/c 60,000

Mark-up 2,79,000 8,37,000 By Balance c/d 15,40,500

To Purchases 28,02,000

Mark-up 14,01,000 42,03,000

To X Deptt. A/c 2,07,000

Mark-up 1,03,500 3,10,500

53,50,500 53,50,500

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 23

Department Y Memorandum Mark Up Account

2015-16 ` 2015-16 `

To Stock A/c 60,000 By Balance b/d 2,79,000

To Profit & Loss A/c 12,30,000 By Stock A/c (28,02,000 x 50%)

14,01,000

To Balance c/d: [1/3(15,40,500+30,000)- ` 30,000]

4,93,500 By Stock A/c 1,03,500

17,83,500 17,83,500

Working Notes:

Verification of Profit `

Sales 37,50,000

Add: Mark down in goods sold 30,000

37,80,000

Gross Profit 1/3 12,60,000

Less: Mark down (30,000)

Gross profit as per books 12,30,000

(b) In the books of Mr. Chena Swami

Salem Branch Account

` `

To Balance b/d By Bank (Remittance to H.O.)

19,50,000

Opening stock: By Balance c/d

Ghee 40,000 Closing stock:

Oil 22,500 Refined oil 19,500

Debtors 1,80,000 Ghee 90,000

Cash on hand 25,690 Debtors (W.N. 1) 2,10,000

Furniture & fittings 23,800 Cash on hand (W.N. 2) 44,800

To Goods sent to Branch A/c Furniture & fittings 21,420

Refined Oil (30x1500x12) 5,40,000

Ghee (20x5000x12) 12,00,000

To Bank (Expenses paid by H.O.)

76,800

© The Institute of Chartered Accountants of India

24 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

To Net Profit transferred

to General P & L A/c 2,26,930

23,35,720 23,35,720

Mr. Chena Swami

Trading and Profit and Loss account for the year ended 31st March, 2016

(Excluding branch transactions)

` `

To Opening Stock: By Sales:

Refined Oil 44,000 Refined Oil 24,10,000

Ghee 10,65,000 Ghee 38,40,500

To Purchases: By Closing Stock:

Refined Oil 27,50,000 Refined Oil 8,90,000

Less: Goods sent to Branch (5,40,000)

22,10,000

Ghee 15,70,000

Ghee 48,28,000

Less: Goods sent to Branch (12,00,000)

36,28,000

To Direct Expenses 6,35,800

To Gross Profit 11,27,700

87,10,500 87,10,500

To Manager’s Salary 2,40,000 By Gross Profit 11,27,700

To General Expenses 1,86,000 By Branch Profit transferred

2,26,930

To Depreciation

Furniture (88,600-79,740) 8,860

Building (5,10,800+2,41,600- 7,14,780)

37,620

To Manager’s Commission @ 10% (8,82,150 x10/110)

80,195

To Net profit 8,01,955

13,54,630 13,54,630

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 25

Working Notes:

(1) Debtors Account

` `

To Balance b/d 1,80,000 By Cash Collections 20,15,000

To Sales made during By Balance c/d 2,10,000

the year: (Bal. Figure)

Refined oil 5,95,000

Ghee 14,50,000

22,25,000 22,25,000

(2) Branch Cash Account

` `

To Balance b/d 25,690 By Remittance 19,50,000

To Collections 20,15,000 By Exp. 45,890

By Balance c/d (Bal. Figure) 44,800

20,40,690 20,40,690

Note:

1. Branch managers generally get commission based on the Branch profits and not on

overall organizational profits. The answer given above is on the basis of the

information given in the question and the commission of branch manager is computed

as 10% on overall organizational profits after charging such commission.

2. Since the amount of cash sales was not given specifically in the question, total

amount of cash collections during the year amounting ` 20,15,000 has been

considered as collection from Debtors in the above solution.

Question 7

Answer any four of the following:

(a) With reference to AS 11, define the following:

(i) Integral Foreign Operation.

(ii) Non-Integral Foreign Operation.

(b) M/s. XYZ Ltd. is in a dispute with a competitor company. The dispute is regarding alleged

infringement of Copyrights. The competitor has filed a suit in the court of law seeking

damages of ` 200 lacs.

The Directors are of the view that the claim can be successfully resisted by the Company.

© The Institute of Chartered Accountants of India

26 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

How would the matter be dealt in the annual accounts of the Company in the ligh t of AS

29 ? Explain in brief giving reasons for your answer.

(c) Explain in brief, the alternative measurement bases, for determining the value at which an

element can be recognized in the Balance Sheet or Statement of Profit and Loss.

(d) Write short notes on Designated Partner in a Limited Liability Partnership and what are

their liabilities.

(e) From the following particulars of M/s. Tsunami Marine Insurance Limited for the year ending

31st March, 2016, find out the

(i) Net Premium earned

(ii) Net Claims incurred

Direct Business Re- Insurance

(`) lakhs (`) lakhs

PREMIUM:

Received 4,400 376

Receivable -01.04.2015 220 18

Receivable -01.04.2016 189 16

Paid 305

Payable - 01.04.2015 14

Payable - 01.04.2016* 9

CLAIMS:

Paid 3,450 277

Payable - 01.04.2015 45 8

Payable - 01.04.2016* 48 6

Received 101

Receivable - 01.04.2015 20

Receivable - 01.04.2016* 19

(4 x 4 = 16 Marks)

Answer

(a) Integral Foreign Operation (IFO): It is a foreign operation, the activities of which are an

integral part of those of the reporting enterprise. The business of IFO is carried on as if it

were an extension of the reporting enterprise’s operations. Generally, IFO carries on

These dates should be read as 31.3.2016.

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 27

business in a single foreign currency, i.e. of the country where it is located. For example,

sale of goods imported from the reporting enterprise and remittance of proceeds to the

reporting enterprise.

Non-Integral Foreign Operation (NFO): It is a foreign operation that is not an Integral

Foreign Operation. The business of a NFO is carried on in a substantially independent way

by accumulating cash and other monetary items, incurring expenses, generating income

and arranging borrowing in its local currency. An NFO may also enter transactions in

foreign currencies, including transactions in the reporting currency. An example of NFO

may be production in a foreign currency out of the resources available in such country

independent of the reporting enterprise.

(b) As per AS 29, 'Provisions, Contingent Liabilities and Contingent Assets’, a provision should

be recognized when

(a) an enterprise has a present obligation as a result of a past event;

(b) it is probable that an outflow of resources embodying economic benefits will be

required to settle the obligation; and

(c) a reliable estimate can be made of the amount of the obligation.

If these conditions are not met, no provision should be recognized.

In the given situation, since, the directors of the company are of the opinion that the claim

can be successfully resisted by the company, therefore there will be no outflow of the

resources. Hence, no provision is required. The company will disclose the same as

contingent liability by way of the following note:

“Litigation is in process against the company relating to a dispute with a competitor who

alleges that the company has infringed copyrights and is seeking damages of

` 200 lakhs. However, the directors are of the opinion that the claim can be successfully

resisted by the company.”

(c) The Framework for Recognition and Presentation of Financial statements recognises four

alternative measurement bases for the purpose of determining the value at which an

element can be recognized in the balance sheet or statement of profit and loss. These

bases are: (i)Historical Cost; (ii)Current cost (iii) Realisable (Settlement) Value and (iv)

Present Value.

A brief explanation of each measurement basis is as follows:

1. Historical Cost: Historical cost means acquisition price. According to this, assets

are recorded at an amount of cash or cash equivalent paid or the fair value of the

asset at the time of acquisition. Liabilities are recorded at the amount of proceeds

received in exchange for the obligation.

2. Current Cost: Current cost gives an alternative measurement basis. Assets are

carried out at the amount of cash or cash equivalent that would have to be paid if the

© The Institute of Chartered Accountants of India

28 INTERMEDIATE (IPC) EXAMINATION: NOVEMBER, 2016

same or an equivalent asset was acquired currently. Liabilities are carried at the

undiscounted amount of cash or cash equivalents that would be required to settle the

obligation currently.

3. Realisable (Settlement) Value: As per realisable value, assets are carried at the

amount of cash or cash equivalents that could currently be obtained by selling the

assets in an orderly disposal. Liabilities are carried at their settlement values; i.e. the

undiscounted amount of cash or cash equivalents paid to satisfy the liabilities in the

normal course of business.

4. Present Value: Under present value convention, assets are carried at present value

of future net cash flows generated by the concerned assets in the normal course of

business. Liabilities under this convention are carried at present value of future net

cash flows that are expected to be required to settle the liability in the normal course

of business.

(d) “Designated partner” means any partner designated as such pursuant to section 7 of the

Limited Liability Partnerships (LLPs) Act; 2008.

As per section 7 of the LLP Act, every limited Liability Partnership shall have at least 2

designated Partners who are individuls and at least one of them shall be a resident in India.

Provided that in case of Limited Liability Partnership in which all the partners are bodies

corporate or in which one or more partners are Individuals and bodies corporate, at least

2 individuals who are partners of such limited liability Partnership or Nominees of such

Bodies corporate shall act as designated partners

“Liabilities of designated partners”

As per Section 8 of LLP Act, unless expressly provided otherwise in this Act, a designated

partner shall be-

(a) responsible for the doing of all acts, matters and things as are required to be done by

the limited liability partnership in respect of compliance of the provisions of this Ac t

including filing of any document, return, statement and the like report pursuant to the

provisions of this Act and as may be specified in the limited liability partnership

agreement; and;

(b) liable to all penalties imposed on the limited liability partnership for any contravention

of those provisions.

(e) (i) Net Premium earned

` In lakhs

Premium from direct business received 4,400

Add: Receivable as 31.03.16 189

Less: Receivable as on 01.04.2015 (220) 4,369

© The Institute of Chartered Accountants of India

PAPER – 5 : ADVANCED ACCOUNTING 29

Add: Premium on re-insurance accepted 376

Add: Receivable as on 31.03.16 16

Less: Receivable as on 01.04.2015 (18) 374

4,743

Less: Premium on re-insurance ceded 305

Add: Payable as on 31.03.16 9

Less: Payable as on 01.04.15 (14) (300)

Net Premium earned 4,443

(ii) Net Claims incurred

` In lakhs

Claims paid on direct business

Add: Reinsurance

277

3,450

Add: Reinsurance outstanding as 31.03.16 6

Less: Reinsurance outstanding as on 01.04.2015 (8) 275

Less: Claims Received from re-insurance 101

Add: Receivable as on 31.03.16 19

Less: Receivable as on 01.04.2015 (20) 100

3,625

Add: Outstanding direct claims at the end of the year 48

3,673

Less: Outstanding Claims at the beginning of the year

(45)

Net Claims Incurred 3,628

© The Institute of Chartered Accountants of India