paper 2.4 - atc international

TRANSCRIPT

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 1/73

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 2/73

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (i)

ATC

ACCA

PAPER 2.4

FINANCIAL MANAGEMENT AND CONTROL

STUDY SYSTEM

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 3/73

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (ii)

No responsibility for loss occasioned to any person acting or refraining from action as aresult of any material in this publication can be accepted by the author, editor or

publisher.

This training material has been published and prepared by Accountancy Tuition Centre Limited

16 Elmtree RoadTeddington

TW11 8STUnited Kingdom.

Editorial material Copyright Accountancy Tuition Centre Limited, 2001.

All rights reserved. No part of this training material may be translated, reprinted or reproduced

or utilised in any form either in whole or in part or by any electronic, mechanical or other

means, now known or hereafter invented, including photocopying and recording, or in any

information storage and retrieval system, without permission in writing from the Accountancy

Tuition Centre Limited.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 4/73

CONTENTS

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (iii)

Page

Introduction (v)

MANAGEMENT ACCOUNTING

1 Management accounting and costing 0101

2 Activity based costing 0201

3 Costs for decision making 0301

4 Budgetary control systems 0401

5 Preparation of budgets 0501

6 Quantitative techniques for budgeting 0601

7 Standard costing and variance analysis 0701

8 Advanced variance analysis 0801

9 Costing methods 0901

FINANCIAL MANAGEMENT

10 Organisational objectives 1001

11 Working capital management 1101

12 Cash management 1201

13 Management of debtors and creditors 1301

14 Inventory management 1401

15 The financial environment 1501

16 The economic environment 1601

17 Equity finance 1701

18 Debt finance 1801

19 The capital structure decision 1901

20 Investment decisions 2001

21 Net present value and internal rate of return 2101

22 Relevant cash flows for DCF 2201

23 Applications of DCF 2301

24 Project appraisal under risk 2401

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 5/73

CONTENTS

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (iv)

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 6/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (v)

Introduction

This Study System has been specifically written for The Chartered Association of CertifiedAccountants Part 2 examination , Paper 2.4 Financial Management and Control .

It provides comprehensive coverage of the core syllabus areas and is designed to be used both as a reference text and interactively with the ATC Learning System to provide youwith the knowledge, skill and confidence to succeed in your ACCA studies.

SYLLABUS

Aim

To develop knowledge and understanding of financial management methods for analysing the benefits

of various sources of finance and capital investment opportunities and of the application of managementaccounting techniques for business planning and control.

Objectives

On completion of this paper students should be able to:

explain the role and purpose of financial management

evaluate the overall management of working capital

evaluate appropriate sources of finance for particular situations

appraise capital investment through the use of appropriate methods

identify and implement appropriate costing systems and techniques

prepare budgets and use them to control and evaluate organisational performance

critically assess the tools and techniques of financial management and control

demonstrate the skills expected in Part 2.

Position of the paper in the overall syllabus

Students must have a thorough knowledge of the material in Paper 1.2 Financial Information for Management and a good knowledge of other Part 1 papers. Financial Management and Control isintegrated with other Part 2 papers as it provides a management decision framework within whichaspects of the Part 2 syllabus are developed.

The effects of capital allowances and corporation tax on capital investment appraisal is examinable.Knowledge gained from Paper 2.3 Business Taxation (UK) will be useful in this respect.

Topics from Financial Management and Control are developed and advanced in Part 3 in Paper 3.3 Performance Management and Paper 3.7 Strategic Financial Management .

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 7/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (vi)

Financial Management

and Control

MANAGEMENTACCOUNTING

(40%)

FINANCIALMANAGEMENT

(60%)

MANAGEMENT ACCOUNTING

COST ANDMANAGEMENTACCOUNTING

METHODS

COSTING/PRICING OFPRODUCTS

AND SERVICES

Management accountingand costing

Activity based costing

Costs for decision making

Costing methods

INFORMATION FOR PLANNING

AND CONTROL

Budgetary control systems Preparation of budgets

Quantitative techniques

for budgeting Standard costing and variance

analysis

Advanced variance analysis

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 8/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (vii)

FINANCIAL MANAGEMENT

ORGANISATIONAL

OBJECTIVES

SOURCES OF

FINANCE

Organisational

objectives

MANAGEMENT OF

WORKING CAPITAL

CAPITAL EXPENDITURE

AND INVESTMENT

Equity finance Debt finance The capital structure

decision

Working capital

management Cash management Management of debtors

and creditors

Inventory management

Investment decisions Net present value and

internal rate of return Relevant cash flows for DCF Applications of DCF

Project appraisal under risk

FINANCIAL MANAGEMENT

FRAMEWORK

The financial environment

The economic environment

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 9/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (viii)

Syllabus Content

1 Financial management objectives

a The nature, purpose and scope of financial management.

b The relationship between financial management, management accounting andfinancial accounting.

c The relationship of financial objectives and organisational strategy.

d Problems of multiple stakeholders in financial management and the

consequent multiple objectives.

e Objectives (financial and otherwise) in not-for-profit organisations.

2 The financial management environment

a Financial intermediation and credit creation.

b Money and capital markets

i Domestic and international

ii Stock markets (both major markets and small firm markets).

c The Efficient Markets Hypothesis.

d Rates of interest and yield curves.

e The impact of fiscal and monetary policy on business.

f Regulation of business (for example, pricing restrictions, green policies andcorporate governance).

3 Management of working capital

a The nature and scope of working capital management.

b Funding requirements for working capital.

c Working capital needs of different types of business.

d The relationship of working capital management to business solvency.

e Management of stock, debtors, short term funds, cash, overdrafts andcreditors.

f Techniques of working capital management (including, inter alia, ratioanalysis, EOQ, JIT, credit evaluation, terms of credit, cash discounts,factoring and invoice discounting, debtors cycles, efficient short term fundinvesting, cash forecasting and budgets, Miller-Orr models, basic foreignexchange methods, probabilities and risk assessment, terms of trade withcreditors).

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 10/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (ix)

4 Sources of finance

a Sources and relative costs (including issue costs) of various types of financeand their suitability to different circumstances and organisations (large andsmall, listed and unlisted) including:

i access to funds and the nature of business risk

ii the nature and importance of internally generated funds

iii capital markets (types of share capital, new issues, rights issues,

loan capital, convertibles, warrants)

iv the effect of dividend policy on financing needs

v bank finance (short, medium and long term, including leasing)

vi trade credit

vii government sources: grants, regional and national aid schemes and

tax incentives.

viii problems of small company financing (collateral, maturity, funding

gap, risk)

ix problems of companies with low initial earnings (R&D, Internet,

and other high-technology businesses)

x venture capital and financial sources particularly suited to the smallcompany

xi international money and capital markets, including an introductionto international banking and the finance of foreign trade.

b Requirements of finance (for what purpose, how much and for how long) inrelation to a business’s operational and strategic objectives.

c The importance of the choice of capital structure: equity versus debt and basic analysis of the term profile of funds.

d Financial gearing and other key financial ratios and analysis of their significance to the organisation.

e Appropriate sources of finance, taking into account:

i cost of finance

ii timing of cash payments

iii effect on gearing and other ratios

iv effect on company’s existing investors.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 11/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (x)

5 Capital expenditure and investment

a Appraisal of domestic capital investment opportunities for profit and non- profit making organisations through the use of appropriate methods andtechniques

i the risk return relationship

ii return on capital employed

iii payback

iv internal rate of return

v net present value

vi single and multi-period capital rationing

vii lease or buy decisions

viii asset replacement

Including (in categories (i)-(viii)) the effects of taxation, inflation, risk anduncertainty (probabilities, decision trees, sensitivity analysis, simulation).

6 Costing systems

a The purpose of costing as an aid to planning, monitoring and control of

business activity.

b Information requirements of different approaches.

c Costing information requirements and limitations in not-for-profitorganisations.

d Behavioural implications of different costing approaches including

performance evaluation.

e Implications of costing approaches for profit reporting, the pricing of products and internal activities/services.

f The role of costing systems in performance evaluation and decision making.

7 Costing techniques

a Allocating/apportioning costs through the use of appropriate techniques

i absorption, marginal and opportunity cost approaches to theaccumulation of costs for specific orders (job, batch, contract) or operations (process, service)

ii activity based costing; use of cost drivers and activities

iii life cycle costing

iv target costing.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 12/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (xi)

8 Standard costing and variance analysis

a Standard costing

i determination of standards

ii identification and calculation of sales variances (including quantityand mix), cost variances (including mix and yield); absorption andmarginal approaches

iii significance and relevance of variances

iv operating statements

v interpretation and relevance of variance calculations to business

performance.

b Planning and operational variances.

c Behavioural implications of standard costing and variance reporting.

9 Budgeting and budgetary control

a Objectives of budgetary planning and control systems including aspects of

behavioural implications.

b Evaluation of budgetary systems such as fixed and flexible, zero based and

incremental, periodic, continuous and activity based.

c Development, implementation and coordination of budgeting systems:functional, subsidiary and master/principal budgets (including cash budgeting); budget review.

d Calculation and cause of variances as aids to controlling performance.

e Quantitative aids to budgeting and the concepts of correlation, basic timeseries analysis (seasonality) and forecasting; use of computer based models.

f Implications of costing systems on profit reporting.

g Behavioural implications of budgeting and budgetary control.

Excluded Topics

The following topics are specifically excluded from the syllabus:

Calculations involving the derivation of cost of capital in discounting problems. Candidates will always be supplied with an appropriate discountrate.

Calculations relating to Modigliani and Miller propositions.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 13/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (xii)

Key Areas Of The Syllabus

The core of the syllabus is aimed at developing the skills required in supporting managerial decisionmaking. They reflect the core competencies needed for students to satisfy the aim of the paper identified above. The core areas are:

financial management objectives

management of working capital

sources of finance

capital expenditure and investment

costing systems

standard costing and variance analysis

budgeting and budgetary control.

Approach To Examining The Syllabus

The examination is a three hour paper in two sections. Financial management issues will always, butnot exclusively, be examined in Section A. The Section A question will typically be a scenario based

question.

Most of the Section B questions will contain a mix of computation and discursive elements although it

is intended that at least one question will be entirely discursive. The balance between computation anddiscursive elements will remain largely constant from one examination to the next.

Section A: One compulsory scenario-based question 50

Section B: Choice of 2 from 4 questions (25 marks each) 50

Additional Information

Present value and annuity tables will be provided in the examination. The ACCA Study Guide providesmore detailed guidance on the syllabus. Wider reading is also desirable, especially regular study of relevant articles in the ACCA “student accountant” magazine.

EXAMINATION TECHNIQUE

Time allocation

Divide your time in proportion to the marks on offer. To allocate your time multiply themarks for each question by 1.8 minutes.

eg 25 mark question should take you 25 × 1.8 = 45 minutes

Stick to this time allocation.

The first marks are the easiest to gain in each question, so don’t overstep the time allocationon one question to tidy up a complicated answer, start the next question instead.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 14/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (xiii)

Numerical Questions

Before starting a computation, picture your route. Do this by jotting down the steps you aregoing to take and imagining the layout of your answer. For example an NPV calculation willrequire a cashflow table and workings for tax savings, working capital etc.

Set up a pro-forma structure to your answer before working the numbers. For example in an NPV calculation with tax it is important to maintain the distinction between the revenue andthe capital cashflows.

Use a columnar layout. This helps to avoid mistakes and is easier for the marker to follow.

Include all your workings and cross-reference them to the face of your answer. For example

ensure the marker can see where the entries for tax savings on your cashflow statement havecome from. In that way it is easy for your marker to identify your errors and give you themarks you deserve.

A clear approach and workings will help earn marks even if you make an arithmetic mistake.

If you do spot a mistake in your answer, often it is not worthwhile spending time amending

the consequent effects of it.

Don’t ignore marks for written recommendations or comments based upon your computation.

These are easy marks to gain. If you have been unable to complete the previous part of thequestion or your answer is obviously wrong then assume a sensible answer and base your comments on this. Do not try to justify the unjustifiable!

Case Study/Scenario based questions

Read the requirements carefully to identify

Instruction eg “outline, discuss .....”Content eg “the factors, the advantages ......”Vehicle/Format eg “report, memo, letter ......”Addressee eg “the board, the accountant ........”

Read the scenario quickly to identify

Company name, dates, nature of business, performance.

Recall the technical knowledge you have learned relating to the content from

the requirements and your quick read of the scenario. The different methodsof Investment Appraisal for example

Read the scenario again slowly and actively

highlighting key points, or noting implications in the margin, andnoting points on a plan of your answer.

Draw together your technical knowledge and the points from the scenario. Do this bythinking and rearranging your plan, before you write up your answer.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 15/73

INTRODUCTION

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 (xiv)

Written Questions

Planning

Read the requirements carefully at least twice to identify exactly how many areas you are being asked to address. Use the marking guide to establish how many points each section of your answer needs to make.

Jot down relevant thoughts on your plan. Make yourself generate sufficient points.

Give your plan a structure which you will follow when you write up the answer. Very often

the structure can be developed from the structure of the requirement.

Presentation

Use headings, indentation and bullet points to give your answer structure and to make itmore digestible for the marker.

Use short paragraphs for each point that you are making.

Separate paragraphs by leaving at least one line of space between each one.

Style

Pompous waffle does not impress markers. Concise, easily understood language scores marks.

Lots of points briefly explained tends to score higher marks than one or two points elaboratelyexplained.

GOOD LUCK!

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 16/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0101

OVERVIEW

Objectives

To consider the role of the management accountant.

To review various methods of product costing.

COSTACCUMULATION

ABSORPTION v MARGINAL

COSTING

LIFE CYCLECOSTING

TARGETCOSTING

Features Steps

Possible methods

Definition Features

MANAGEMENTACCOUNTING

FUNCTION

MA and FA

Financial management Planning, control and

decision-making

Allocation Apportionment

Service departments

Stock level changes Profit reconciliation Quick calculations

Comparison

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 17/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0102

1 MANAGEMENT ACCOUNTING – FUNCTION

1.1 Management accounting and Financial accounting

Management accounting is concerned with the preparation and presentation of

accounting information to management in order to help them plan, control and make

decisions about the operations of the business.

Financial accounting is concerned with the preparation and presentation of accounting

information on the performance and financial position of the business.

1.2 Comparison

Management accounting Financial accounting

Users of

information

Management Shareholders, banks, creditors,

potential investors, Customs &

Excise, Government, InlandRevenue

Format of

information

Can take any form Presentation regulated by law

and by the profession through

Accounting Standards and

European Directives

Purpose of

information

Useful to plan, control and make

decisions

Stewardship and investment

decisions

Bases of

valuation

Relevant costs Historical costs

1.3 Financial management

As well as a need for financial accounting and management accounting an organisation

will also require financial management. Financial management is concerned with:

the raising of long-term finance;

appraising potential investments or projects;

determining dividend policy ;

controlling working capital.

The financial manager will therefore determine the overall financing requirements of

the organisation and its investment policy. The management accountant will be

responsible for the control and reporting of these activities for management purposes

and the financial accountant will be responsible for reporting the activities for external

purposes.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 18/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0103

1.4 Planning, control and decision-making

1.4.1 Planning

Encompasses establishing objectives and evaluating policies and actions required to

achieve them.

Planning is the setting of goals and selecting the means of achieving them.

As businesses become large, these procedures will need to be formalised.

Short-term plans such as the annual budget show in detail the intended results

for the forthcoming year. (See Session 4)

Long-term plans are usually documents showing the long-term objectives of

the business.

1.4.2 Control

Control is the assessment of performance by comparing the budgeted results

with actual results.

This usually takes the form of an operating statement which breaks down the

difference into its component parts.

1.4.3 Decision-making

Decision-making usually involves using the information provided by the

costing system to make decisions.

2 COST ACCUMULATION

2.1 Approaches

Costs are recorded and accumulated in cost accounting systems using one of two main

approaches:

absorption costing;

marginal costing.

Under an absorption costing system overhead costs must be allocated, apportioned and

then absorbed.

2.2 Allocation

This is where costs that relate to a single cost centre are allocated to that cost centre.

2.3 Apportionment

Apportionment is where an overhead is common to more than one cost centre and

therefore needs to be shared out amongst the relevant cost centres using an appropriate

method of apportionment.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 19/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0104

Illustration

Cost Basis of apportionment

Rent, rates, heat − Floor area

Supervision, canteen costs − Number of employees

Depreciation, plant insurance − Book value of plant

2.4 Service department costs

Service departments are cost centres which exist to provide services to other

departments. The canteen is a common example.

Having allocated and apportioned the costs to the production and service departments,

the totals of the latter need to be reallocated and reapportioned to the former.

Three methods available:

Direct method – ignores work between service departments.

Step method – service department which does most work for other service

departments is reapportioned first. Other reciprocal services are ignored.

Reciprocal method – Full recognition is given for all work done by service

departments for each other. May be solved algebraically by simultaneous

equations.

Example 1

Production Service Pressing Assembly Canteen Main-

dept dept tenance£ £ £ £

Allocated costs specific toa department 10,000 20,000 5,000 6,000

Apportioned costs, eg rates

according to square footage 5,000 6,000 3,000 3,000 ——— ——— ——— ——— 15,000 26,000 8,000 9,000

Re-allocate service overheads to production departments

Use of canteen 50% 30% 20%Use of maintenance 55% 40% 5%

Required:

Reapportion the service department costs using:

(i) direct method;

(ii) step method;

(iii) reciprocal methods.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 20/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0105

Solution

(i) Direct method

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30)

Maintenance (55:40)

15,000 26,000 8,000 9,000

———

———

———

———

———

———

———

———

(ii) Step (down) method

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30:20)

15,000 26,000 8,000 9,000

——— ——— ——— ———

Maintenance (55:40)

———

———

———

———

———

———

———

———

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 21/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0106

(iii) Reciprocal method

Repeated distribution

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30:20)

15,000 26,000 8,000 9,000

——— ———

Maintenance (55:40:5) ____

———

Canteen (50:30:20) ____

____

Maintenance (55:40:5) ____

____

Canteen (50:30:20)

———

———

———

———

____

––––

____

––––

OR Algebraically

Let x be the total cost of canteen service department

Let y be the total cost of maintenance service department

x = y =

Rearranging

Solve simultaneously

~

y =

Substitute

x =

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 22/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0107

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30:20)

Maintenance (55:40:5)

15,000 26,000 8,000 9,000

———

———

———

———

———

———

———

———

As can be seen by the above results the differences between the methods are marginal

and generally insignificant. This is especially true when it is remembered that the

process of apportionment has already introduced subjective judgement into the

calculations.

What is the most appropriate apportionment basis?

2.5 Absorption

The total of the overheads in each production department must now be absorbed into

the units of production.

This is achieved using one of the following methods:

direct labour hour rate

direct material cost rate

direct labour cost rate

prime cost percentage rate

machine hour rate

unit of output rate.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 23/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0108

Example 2

X Ltd estimates that its factory costs for the coming year will be as follows:

£Direct material 40,000Direct wages 60,000

——— PRIME COST 100,000Factory overhead 30,000

——— Total factory cost 130,000

———

During the year there will be 100,000 direct labour hours, 50,000 machine hours and

200,000 units will be produced.

Required:

Work out the absorption rate using the following methods:

(i) direct labour hour rate;

(ii) direct material cost rate;

(iii) direct labour cost rate;

(iv) prime cost % rate;

(v) machine hour rate;

(vi) unit of output rate.

Solution

(i) Direct labour hour rate

(ii) Direct material cost rate

(iii) Direct labour cost rate

(iv) Prime cost % rate

(v) Machine hour rate

(vi) Unit of output rate

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 24/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0109

2.6 Pre-determined overhead rates

As the above figures have been calculated using estimates of costs for the coming year,

it is known as a pre-determined overhead absorption rate (POAR). This is then used to

apportion the overheads to the products. This rate is generally derived from the

budgeted overhead and the normal level of production figures, in order to avoid

distortion caused by seasonal fluctuations and to provide a consistent basis for

measuring costs.

Finally there are three relevant figures relating to overheads:

originally budgeted overhead;

actual overhead spent;

overhead absorbed (POAR × Actual activity level).

The difference between (2) and (3) is the under or over absorption which will be

adjusted for in the profit and loss account for the period.

> = under-absorption – debit to P&L

> = over-absorption – credit to P&L

2.7 Summary

The diagram below shows the process described above.

PRODUCTION OVERHEADS

PRODUCTION COST

PRODUCTION

DEPARTMENT B

SERVICE

DEPARTMENT

DIRECT

COSTS

Allocation

Apportionment

Reapportionment

Absorption

Charging of direct costs

PRODUCTION

DEPARTMENT B

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 25/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0110

3 ABSORPTION V MARGINAL

3.1 Methods

Absorption

costing Variable

production costs

Fixed

production costs

Selling

costs

Product

costs

Closing stock

⇒ Balance sheet

⇒ Profit and

loss account

period expenditure

Marginal costing Variable

production costs

Fixed

production costs

Selling

costs

Product

costs

Closing stock

⇒ Balance sheet

⇒ Profit and

loss account

period expenditure

period expenditure

These diagrams clearly show the difference between Total absorption costing (TAC)

and Marginal costing (MC). Under TAC fixed production costs are charged to the

products made and, to the extent that items remain in closing stock, a proportion of

those costs are carried forward as an asset in the balance sheet. Under MC all fixed

production costs are charged to the profit and loss account as a period charge.

Hence the reconciliation between TAC profits and MC profits (see later ) relates to

stock movement.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 26/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0111

Example 3

Budgeted sales and production are 10,000 items.

Standard/Budgeted figures

Selling price = £20 per unitMaterials = £3 per unitOther variable production costs = £2 per unitVariable selling costs = £3 per unitFixed production costs = £40,000Fixed selling costs = £20,000

Actual figures

Opening stock = 1,000 unitsSales = 9,000 units

Production = 11,000 units

Required:

Produce

(i) a marginal costing standard cost card;

(ii) an absorption costing standard cost card;(iii) a marginal costing profit and loss account;

(iv) an absorption costing profit and loss account.

(Produce profit and loss accounts assuming that revenues and costs are as originally budgeted.)

Solution

(i) Marginal costing standard cost card

£ £

Selling price

Materials

Other variable production costs

— Production costs – stock valuation

Variable selling costs

—

Cost of sales

Contribution

——

——

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 27/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0112

(ii) Absorption costing standard cost card

£ £

Selling price

Materials

Other variable production costs

Fixed production overhead —

Production costs – stock valuation

Variable selling costs

Fixed selling costs

—

Cost of sales

Profit

——

——

(iii) Marginal costing profit and loss

£000 £000

Sales

Less: Cost of sales

Opening stock †

Variable production costs

Closing stock †

——

——

Variable selling and administrative costs

—— Contribution

Fixed production costs

Fixed selling and administrative costs

Net profit

——

——

† Stocks valued at variable production cost per unit only.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 28/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0113

(iv) Absorption costing profit and loss

£000 £000

Sales

Less: Cost of sales

Opening stock*

Variable production costs

Fixed production costs

Closing stock*

——

——

Gross profit

Fixed selling and administrative costs

Variable selling and administrative costs

Net profit

——

——

* Stocks valued at variable production cost plus fixed production cost per unit.

An alternative layout of the absorption costing profit or loss account, which clearly

shows the over or under-absorption of overheads, would be as follows:

£000 £000

Sales

Opening stock

Total production costs

Closing stock

–––

––––

Under/over absorption

Overhead absorbed

Overhead spent

–––

Over absorption

––––

Gross profit

Fixed selling and administrative costs

Variable selling and administrative costs

Net profit

––––

––––

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 29/73

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 30/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0115

(b) Marginal costing

Month 1 Month 2 Month 3

£ £ £ £ £ £

Sales

Opening stock Variable production costs

Closing stock

——— ——— ———

Cost of goods sold

——— ——— ———

CONTRIBUTION

Fixed production costs

Gross profit

———

———

———

———

———

———

3.2 Stock level changes

Change in stock Effect on profit

(1)

(2)

(3)

Closing stock > Opening stock

Closing stock = Opening stock

Closing stock < Opening stock

TAC profit > MC profit

TAC profit = MC profit

TAC profit < MC profit

3.3 Profit reconciliation

Using Example 4 figures : Month 1 Month 2 Month3

£ £ £Marginal cost profit 38,000 70,500 64,000

Difference in profit

(Change in stock level × Fixed prodn o/h per unit)

2,000 × £5

500 × £5 10,000 (2,500) −

——— ——— ———

Absorption cost profit 48,000 68,000 64,000 ——— ——— ———

The above profit reconciliation assumes that the fixed overhead absorption rate per unit

remains constant. If this were to change, the reconciling difference would become the

difference between fixed production costs:

(i) b/f in opening stock; and

(ii) c/f in closing stock.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 31/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0116

3.4 Quick profit calculations

If there is no requirement to show a profit and loss account, quick profit calculations

can be used.

The calculations shown below are illustrated using the data from Example 3 .

(i) Marginal profit calculation

£000

Unit contribution × Units sold (12 × 9,000) 108Less Fixed production costs (40)

Fixed selling and administrative costs (20) ––––

Net profit 48 ––––

(ii) Absorption profit calculation£000

Unit profit × Unit solds (6 × 9,000) 54Adjust for:

Over/(under) absorption of fixed production overhead

((11,000 × 4) – 40,000) 4Over/(under) absorption of fixed selling and administrative

overhead ((9,000 × 2) – 20,000) (2) ––––

Net profit 56

––––

3.5 Comparison of methods

Total absorption costing Marginal costing

Stock valuation Conforms to accounting

standards

Prudent valuation

Profits Depends on sales and

production (manipulate it

by over-stocking)

Depends on sales

Costing procedures Avoids splitting semi-variable costs

Avoids allocation,apportionment and absorption

Decision-making Pricing More useful and relevant

Cost control Focuses on all costs Focuses on controllable costs

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 32/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0117

4 TARGET COSTING

4.1 Features

A target for product cost is derived by subtracting a desired profit margin from a

competitive market price.

A technique used to try to ensure that desired profit margins are achieved.

Used at the planning and design stage for a new product.

Particularly used in the car industry.

4.2 Steps

The sales department estimates the competitive market price for the new

product ie the estimated price that customers will be prepared to pay.

Management sets a required profit margin.

The target cost is calculated as

Target cost = Estimated selling price – required profit margin

The target cost is then given to the product and process designers who must

try to reduce budgeted costs to target.

4.3 Possible methods of meeting target cost

Value analysis

MRP/MRPII

5 LIFE CYCLE COSTING

4.1 Definition

A system which tracks and accumulates the actual costs and revenues attributable to

each product from development through to abandonment

4.2 Features

In the modern manufacturing environment a high proportion of a product’s

costs will be at the early stages in its life cycle eg development, design and

set-up costs.

This requires an accounting system that compares the revenue from a product

with all the costs incurred over the entire product life cycle.

Life Cycle Costing traces development, design and set-up costs to individual

products over the entire life cycle of that product.

Final profitability of a product is therefore determined at the end of the lifecycle.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 33/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0118

At any stage during the life cycle accumulated costs can be compared to life

cycle budgeted costs to aid control.

FOCUS

You should now be able to:

outline and distinguish between the nature and scope of management

accounting and the role of costing in meeting the needs of management

describe the purpose of costing as an aid to planning, monitoring and

controlling business activity

explain the potential for different costing approaches to influence cost

accumulation and profit reporting

explain the requirement to allocate overheads

describe, explain and apply absorption and marginal costing

reconcile the resulting profits/losses from absorption and marginal costing

explain the impact of life cycle costing on cost accumulation

describe and apply target costing methods

evaluate the relative advantages and disadvantages of the different costing

approaches

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 34/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0119

EXAMPLE SOLUTIONS

Solution 1 – Service departments

(i) Direct method

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30)

Maintenance (55:40)

15,000

5,000

5,211

26,000

3,000

3,789

8,000

(8,000)

9,000

(9,000)

———

25,211

———

———

32,789

———

———

–

———

———

–

———

(ii) Step method

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30:20)

15,000

4,000

26,000

2,400

8,000

(8,000)

9,000

1,600

——— ——— ——— ———

19,000 28,400 – 10,600

Maintenance (55:40) 6,137 4,463 (10,600)

———

25,137

———

———

32,863

———

———

–

———

———

–

———

(iii) Reciprocal method

Repeated distribution

Pressing Assembly Canteen Maintenance

£ £ £ £

Canteen (50:30:20)

15,000

4,000

26,000

2,400

8,000

(8,000)

9,000

1,600

——— ———

Maintenance (55:40:5) 5,830 4,240

–

530

10,600

(10,600)

——— ———

Canteen (50:30:20) 265 159530

(530) –

106

——— ———

Maintenance (55:40:5) 58 42

–

6

106

(106)

——— ———

Canteen (50:30:20) 3 3

6

(6) –

———

25,156

———

———

32,844

———

———

–

———

———

–

———

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 35/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0120

OR Algebraically

Let x be the total cost of canteen service department

Let y be the total cost of maintenance service department

x = 8,000 + 0.05 y

y = 9,000 + 0.20 x

Rearranging

x – 0.05 y = 8,000

–0.20 x + y = 9,000

Multiply by 0.2

0.20 x – 0.01 y = 1,600

– 0.20 x + y = 9,000

Add 0.99 y = 10,600 ~

y =10 600

0 99

,

.

y = £10,707

Substitute into

x – 535 = 8,000

x = £8,535

Pressing Assembly Canteen Maintenance£ £ £ £

Canteen (50:30:20)

Maintenance (55:40:5)

15,000

4,267

5,889

26,000

2,561

4,283

8,000

(8,535)

535

9,000

1,707

(10,707)

———

25,156

———

———

32,844

———

———

–

———

———

–

———

Solution 2 – Overhead absorption

(i) Direct labour hour rate

hrs10,000

£30,000= 30p

(ii) Direct material cost rate £30,

£40,

000

000= 75%

(iii) Direct labour cost rate £30,

£60,

000

000= 50%

(iv) Prime cost % rate £30,

£100,

000

000

= 30%

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 36/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0121

(v) Machine hour rate £30,

,

000

50 000 hrs= 60p

(vi) Unit of output rate £30 000

200 000 units

,

,= 15p

Solution 3 – MC vs AC

(i) Marginal costing standard cost card

£ £

Selling price 20

Materials

Other variable production costs

3

2

—

Production costs – stock valuation

Variable selling costs

5

3

—

Cost of sales (8)

Contribution

——

12

——

(ii) Absorption costing standard cost card

£ £

Selling price 20

MaterialsOther variable production costs

Fixed production overhead

32

4

—

Production costs – stock valuation

Variable selling costs

Fixed selling costs

9

3

2

—

Cost of sales (14)

Profit

——

6

——

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 37/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0122

(iii) Marginal costing profit and loss

£000 £000

Sales 180

Less: Cost of sales

Opening stock †

Variable production costs

Closing stock †

5

55

(15)

—— (45)

——

135

Variable selling and administrative costs (27)

——

Contribution

Fixed production costs

Fixed selling and administrative costs

108

(40)

(20)

Net profit

——

48 ——

† Stocks valued at variable production cost per unit only.

(iv) Absorption costing profit and loss

£000 £000

Sales 180

Less: Cost of sales

Opening stock*

Variable production costs

Fixed production costsClosing stock*

9

55

40(27)

—— (77)

——

Gross profit

Fixed selling and administrative costs

Variable selling and administrative costs

3 × 9,000

103

(20)

(27)

Net profit

——

56

——

* Stocks valued at variable production cost plus fixed production cost per unit.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 38/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0123

Alternative layout

£000 £000

Sales

Opening stock

Total production costs (11 × 9)

Closing stock

9

99

(27)

180

––– (81)

––––

99

Under/over absorption

Overhead absorbed (11 × 4)

Overhead spent

44

(40)

–––

Over absorption 4

––––

Gross profit

Fixed selling and administrative costsVariable selling and administrative costs

103

(20)(27)

Net profit

––––

56

––––

Solution 4 – Costing profit and loss accounts

(a) Absorption costing

Month 1 Month 2 Month 3

£ £ £ £ £ £

Sales 120,000 170,000 160,000

Opening stock

Variable production costs

Fixed production costs

Closing stock

12,000

56,000

40,000

(36,000)

36,000

56,000

40,000

(30,000)

30,000

56,000

40,000

(30,000)

——— ——— ———

Cost of goods sold 72,000 102,000 96,000

Gross profit

———

48,000

———

———

68,000

———

———

64,000

———

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 39/73

MANAGEMENT ACCOUNTING AND COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0124

(b) Marginal costing

Month 1 Month 2 Month 3

£ £ £ £ £ £

Sales 120,000 170,000 160,000

Opening stock

Variable production costs

Closing stock

7,000

56,000

(21,000)

21,000

56,000

(17,500)

17,500

56,000

(17,500)

——— ——— ———

Cost of goods sold 42,000 59,500 56,000

——— ——— ———

CONTRIBUTION

Fixed production costs

78,000

40,000

110,500

40,000

104,000

40,000

Gross profit

———

38,000

———

———

70,500

———

———

64,000

———

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 40/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0201

OVERVIEW

Objective

! To consider the differences between traditional costing systems and activity based costing.

COST DRIVERS

ACTIVITYBASED

COSTING

ADVANTAGES &DISADVANTAGES

CALCULATIONOF PRODUCT

COST

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 41/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0202

1 ACTIVITY BASED COSTING

Activity-based costing (ABC) is an approach to costing and activity monitoring which

assigns resources consumed to activities and activities to cost objects (based onestimated consumption). Cost drivers are used to apportion activity costs to output.

This approach for calculating product costs was developed by Cooper and Kaplan.

It recognises that traditional ideas of fixed and variable cost categorisations are notalways appropriate and that, as the proportion of overhead costs in manufacture hasincreased, there is a need for a more accurate method of absorbing these costs into costunits.

It looks for a clearer picture of cost behaviour and a better understanding of what

determines the level of costs – “cost drivers”.

In finding total product costs, overheads are traced to individual production

departments as usual – apportioning common costs according to suitable bases.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 42/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0203

Then

Identify major activities within each

department which create

cost

Determine

what causes the cost of each activity – the “cost

driver”

Create a cost

centre/cost poolfor each activity – the

“activity cost pool”

Step 1

Step 2

Step 3

Step 4

Examples

(1) Production scheduling

(2) Machining(3) Despatching of orders(4) Inspections

(1) Number of batch set-ups for production

scheduling(2) Machine hours for machining(3) Number of despatch orders for despatching(4) Number of inspections

Cost pool for:(1) all production scheduling costs(2) all machining costs

(3) all despatching costs

(4) all inspection costs

Cost per

(1) batch set up

(2) machine hour (3) despatch order (4) inspection

Eg Product Z(1) No of batch set ups for Product Z

× Cost per batch set up x(2) No of machine hours for Product Z

× Cost per machine hour x

(3) No of despatch orders for Product Z× Cost per despatch order x

(4) No of inspections for Product Z

× Cost per inspection x –––

y –––

Eg Product Z

Overhead cost per unit = producedZsof No

y

Calculate anabsorption rate

for each

“cost driver”

Calculate the totaloverhead cost

for manufacturing

each product

Calculate overhead

cost per unit

Step 5

Step 6

Having discovered the cost drivers within the business, it may well be decided to re-organise the original production departments.

2 COST DRIVERS

As can be seen, rather than use a single absorption rate, different types of overhead costare absorbed into units of production according to more appropriate rates based on costdrivers.

For example, for a particular production department find a warehousing cost/kg of material used, electricity cost/machine hour, production scheduling cost/production

order, etc. These can then each be costed for every product and aggregated to calculatean overhead cost per unit as described above.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 43/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0204

3 ADVANTAGES AND DISADVANTAGES OF ABC

3.1 Advantages

! Allotment of overhead is fairer and therefore product costs are more accurate.

! There is a better understanding of what causes cost.

! The company can concentrate on producing the most profitable items.

! Control of overheads is easier, as responsibility for incoming costs must beestablished before ABC can be implemented.

! Performance appraisal is more meaningful.

! Cost driver rates can be monitored and used to identify areas of weakness or inefficiency.

! Budget setting and sensitivity analysis are more accurate.

! Activity based budgeting (ABB) can be used.

Activity-based budgeting (ABB) is a budgeting method based on an activityframework which uses cost driver data in the processes of budget-setting and

variance feedback .

! New products can be designed to utilise efficient cost drivers. Cost can bedesigned out of products.

3.2 Disadvantages

! ABC may be based on historic information but could be used for futurestrategic decisions.

! Selection of cost drivers may not be easy.

! Additional time and cost of setting up and administering the system.

! Cost measurement may not be easy.

! Exclusion of non-production overheads can be difficult.

! Assessing the degree of completion of work in progress with respect to eachcost driver is difficult.

! Variance analysis is complicated.

! Many judgemental decisions still required in the construction of an ABCsystem.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 44/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0205

4 CALCULATION OF PRODUCT COST

Example 1

Total budgeted fixed overheads for a firm are £712,000. These have traditionally been

absorbed on a machine hour basis. The firm makes two products, A and B.

A B

Direct material cost £20 £60Direct labour cost £50 £40Machine time 3 hrs 4 hrsAnnual output 6,000 40,000

Required:

(a) Calculate the total cost for each product on the assumption that the firm

continues to absorb overheads on a machine hours basis.

The firm is considering changing to an Activity Based Costing system and hasidentified the following information:

Machine Annual Total No of No of hours/unit output machine hrs set ups purchase orders

Product A 3 6,000 18,000 16 52Product B 4 40,000 160,000 30 100

——— ——— —— —— 46,000 178,000 46 152

——— ——— —— ——

Cost pools: Cost driver:£

Machine related 178,000 Machine hoursSet-up related 230,000 Set-ups

Purchasing related 304,000 Purchase orders

———— Total overheads 712,000

————

Required:

(a) Calculate the cost per unit using traditional overhead absorption.

(b) Calculate the cost per unit using the ABC system.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 45/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0206

Solution

(a) Traditional

Total overhead =

Total machine hours =

Rate per hour =

A£

B£

Direct materialDirect labour

2050

6040

Fixed o/h

— —— Total

— ——

(b) ABC

Activities Machinerelated

Set-uprelated

Purchasing related

Overheads £178,000 £230,000 £304,000Consumption of activities

(cost drivers) 178,000 hrs 46 set ups 152 ordersCost per unit of consumption

Cost traced to products

AB

Cost per unit

A

B

A£

B£

Direct materialDirect labour Fixed overhead

20.0050.00

60.0040.00

_____

_____

Total

––––– –––––

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 46/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0207

FOCUS

You should now be able to

! understand some of the limitations of traditional cost allocation,apportionment and absorption.

! explain and apply activity based costing .

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 47/73

ACTIVITY BASED COSTING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0208

EXAMPLE SOLUTIONS

Solution 1 – Product cost

(a) Traditional

Total overhead = £712,000

Total machine hours = £178,000

Rate per hour =

000178

000712

,

,

= £4/hr

A£

B£

Direct material

Direct labour

20

50

60

40Fixed o/h

3hrs @ £44hrs @ £4

1216

— ——

Total 82 116 — ——

(b) ABC

Activities Machinerelated

Set-uprelated

Purchasing related

Overheads £178,000 £230,000 £304,000Consumption of activities

(cost drivers) 178,000 hrs 46 set ups 152 ordersCost per unit of consumption £1 per hour £5,000 per set up £2,000 per order Cost traced to products

AB

£18,000£160,000

£80,000£150,000

£104,000£200,000

Cost per unit

A

6,000

104,00080,00018,000 ++

= £33.67

B

40,000

200,000150,000160,000 ++

= £12.75

A£

B£

Direct materialDirect labour Fixed overhead

20.0050.0033.67

60.0040.0012.75

_____

_____

Total 103.67 112.75

––––– –––––

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 48/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0301

OVERVIEW

Objective

! To consider the information and costing requirements for managementdecision making.

BREAK-EVENANALYSIS

Break-even pointsBreak-even charts Margin of safety

INFORMATIONREQUIREMENTS

KEY FACTOR ANALYSIS

RELEVANTCOSTS

MeaningDifficultiesDeprival value

MISLevels of managementTypes of information

Limiting factors

MethodLimitations

MAKE OR BUYDECISIONS

MethodLimitations

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 49/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0302

1 INFORMATION REQUIREMENTS

1.1 Management information system

A management information system (MIS) is a set of formalised procedures designed to

provide managers at all levels with appropriate information from all relevant sources(internal and external) to enable them to make timely and effective decisions for planning and controlling the activities for which they are responsible.

Therefore a typical MIS:

! receives input data! processes the input data into information for output! communicates the output information.

The part of the accountant within the MIS will vary, depending on:

! the type of organisation and the type of costing system used! techniques used, eg budgets, standard costs! type and volume of information required.

1.2 Planning information

! Information is needed to decide the firm’s objectives and how they are to beachieved

! It pre-supposes that the current position of the firm is understood.Knowledge of the current position can be achieved through strategic analysis

of internal and external information (See Session 20).

1.2.1 Internal information

! Production and operations! Marketing and sales! Finance! Research and development! Personnel and organisation

1.2.2 External information

!

Markets and competitors! Economic conditions! Political situation! Technological change! Social trends

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 50/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0303

1.3 Levels of management and information needs

1.3.1 Strategic

! Investment appraisal! Potential markets! Forecasting and budgeting

In essence strategic planning looks at the “big picture” and is long-term and forward-looking in nature.

1.3.2 Tactical

Concerns effective and efficient resource utilisation to achieve specified objectives

encompassing:

! Purchasing decisions! Stock locations! Sales analysis! Cash flow projections

1.3.3 Operational

! Debtors and creditors! Payroll details! Customer complaints! Meeting schedules! Variances

In essence operational planning is concerned with detail and considers the immediate past and future; hence it is short-term in nature.

1.4 Control information

! Information which provides a comparison between actual results and the plan

! Only useful if it is timely, concise and reliable

! Useless if it:

− arrives too late;

− is unreliable;− concerns matters outside the control of the recipient

1.5 Decision-making information

! Must be relevant, up-to-date, as accurate as is necessary for the decision! Most important to use relevant costs.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 51/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0304

2 BREAK-EVEN ANALYSIS

2.1 Definition

Break-even point is the level of sales in units or revenue at which no profit or loss is

made.

Example 1

Selling price = 80p per unitVariable costs = 60p per unit

Total fixed costs = £2,000

Required:

What is the profit if sales are as follows?

10,000 units20,000 units30,000 units

Solution

Output 10,000

———

£

20,000

———

£

30,000

———

£SalesVariable costs

——— ——— ——— Contribution

Fixed costs

Profit ———

———

———

———

———

———

2.2 Determining the break-even point

units)in(expressed

pointevenBreak − =

unit per onContributi

costsFixed

Contribution margin=

unit per priceSelling

unit per onContributi=

ratioP/VratioumeProfit/Vol

ratioC/Sratioon/SalesContributi

−

−

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 52/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0305

revenue)salesof in terms (expressed

pointeven-Break =

ratioP/Vor

ratioC/Sor

marginonContributi

costsFixed

C/S ratio = contribution/sales ratio

Also in Cost Volume Profit (CVP) analysis :

Required profit (in units)=

unit per onContributi

profitRequiredcostsFixed +

revenue)salesof in terms(expressed

profitRequired =

marginonContributi

profRequired+costFixed

2.3 Break-even chart

Costs/Rev(£)

Sales revenue

Fixed andvariable costs

Currentoutput

Output (units)

L O S S

P R O F

I T

Safetymargin

Break-even

point

Margin of safety

Safety margin = Expected sales – Break-even sales

As a percentage =Expected sales Break-even sales

Expected sales

−×100

This can be expressed in terms of units or sales revenue.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 53/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0306

2.4 A contribution break-even chart

Costs/Rev(£) Sales revenue

Fixedcosts

Output (units)

Break-even point

L O S S

PROFIT

CONTRIBUTION

Total costs

Variable costs

2.5 Limitations of break-even analysis

! Assumes costs and revenues are linear (ie constant)

! Assumes all costs are either fixed or variable

! Assumes selling prices, variable cost per unit and fixed costs remain constant

! Cannot be used where more than one product is made and sold (unless the

sales mix is constant)

! Assumes all goods produced are sold (ie ignores changing stock levels).

2.6 Profit-volume (P/V) chart

Whilst break-even charts show details of costs and revenues, they do not illustrateeasily the sizes of profits and losses at different activity levels.

A P/V chart does show the net profit/(loss) at different activity levels.

Profit

Volume(sales units)

BEP

x y

Profit atvolume y

0

Loss atvolume x

£

Fixedcosts

!

The vertical axis shows the profit above and the loss below the horizontalsales axis

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 54/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0307

! When sales are zero, the loss is equal to the fixed costs

! If fixed costs and variable costs per unit are constant – then the P/V chart isrepresented by a straight line

! To draw a P/V chart – it is only necessary to know the profit/(loss) at onelevel of sales. Plot this point – then link it to fixed costs on the vertical axis – and draw a straight line through both points

! The slope of the line represents the contribution. The steeper the slope the

greater is the contribution per unit.

3 KEY FACTOR ANALYSIS

3.1 Method

Rule: Where resources are unlimited – make all those products which give“positive contribution”

Rule: Where a factor of production is limited – contribution (and profit ) will bemaximised by concentrating production on that product(s) which make(s)

“best use” of the scarce resource.

This is the product which gives the highest contribution per unit of key (limiting) factor

or resource, calculated as:

usedresourcescarceof Units

unit per onContributi

In order to decide which products to make, in order to maximise profit, where one of the factors of production is limited, the following approach should be undertaken:

(1) Calculate contribution per key factor for each product

(2) Rank the products according to the contribution per unit (CPU) of scarceresource calculated

(3) Concentrate production on those products with the highest CPU of scarceresource – until all of the scarce resource is used up

Example 2

Material I is restricted to 12,000 kg.

Product A B C

Contribution per unit 16 10 24 No of kg of I per unit 4 2 8

Required:

What is the maximum contribution which can be achieved?

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 55/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0308

Solution

Product A B C

Contribution per unit No of kg per unit

Contribution per kgRank

∴ Produce

Maximum contribution =

Example 3

Suppose in Example 2 above sales of B are restricted to 4,000 units.

Required:

What is the maximum contribution which can now be achieved?

Solution

kg 4,000 units of B uses up1,000 units of A uses up

———

———

∴ Maximum contribution £

From BFrom A

———

———

3.2 Limitations

! Assumes constant variable cost per unit and constant total fixed costs.

! Takes no account of loss of customer goodwill.

! Can deal with only one scarce resource.

! Applies only to situations where capacity constraints cannot be removed inthe short term.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 56/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0309

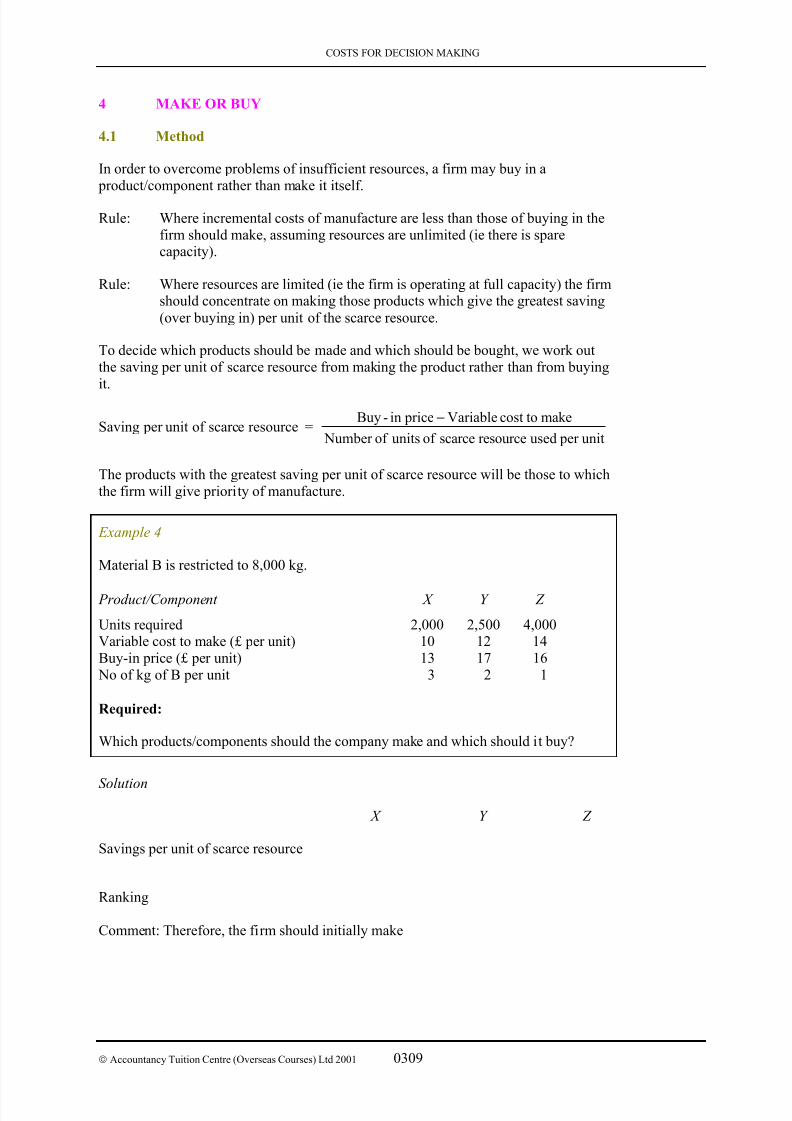

4 MAKE OR BUY

4.1 Method

In order to overcome problems of insufficient resources, a firm may buy in a product/component rather than make it itself.

Rule: Where incremental costs of manufacture are less than those of buying in thefirm should make, assuming resources are unlimited (ie there is sparecapacity).

Rule: Where resources are limited (ie the firm is operating at full capacity) the firmshould concentrate on making those products which give the greatest saving

(over buying in) per unit of the scarce resource.

To decide which products should be made and which should be bought, we work outthe saving per unit of scarce resource from making the product rather than from buyingit.

Saving per unit of scarce resource =unit per usedresourcescarceof unitsof Number

makecost toVariable pricein-Buy −

The products with the greatest saving per unit of scarce resource will be those to whichthe firm will give priority of manufacture.

Example 4

Material B is restricted to 8,000 kg.

Product/Component X Y Z

Units required 2,000 2,500 4,000Variable cost to make (£ per unit) 10 12 14Buy-in price (£ per unit) 13 17 16 No of kg of B per unit 3 2 1

Required:

Which products/components should the company make and which should it buy?

Solution

X Y Z

Savings per unit of scarce resource

Ranking

Comment: Therefore, the firm should initially make

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 57/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0310

Utilisation of B

kg of B

Total B overall ––––– 8,000

–––––

Comment:

4.2 Limitations

! Assumes constant unit variable cost and constant total fixed costs.! Ignores qualitative factors (eg reliability of supplier).

Therefore any decision to buy in a product or component should only be taken after aconsideration of other factors such as:

! suitability of component to be bought-in when compared with owncomponent;

! quality of proposed supplier;

! reliability of proposed supplier;

! reaction of workforce or customers.

5 RELEVANT COSTS

5.1 Meaning

Only those costs which will be affected by a decision are relevant to the decision-making process. Therefore

! only future costs are relevant

! sunk costs or committed costs can be ignored; research already carried outwould be a sunk cost and rental payments already agreed would be a

committed cost

! only incremental costs (costs which will change as a result of the decision)

are relevant

! fixed costs which are unaffected are therefore irrelevant

! only cash costs are relevant; book values and historic costs can be ignored

! all opportunity costs are relevant; an opportunity cost is the value of a benefitsacrificed in favour of an alternative course of action, eg the contribution lost

if a key worker is moved to a new project is a relevant opportunity cost whenassessing that new project.

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 58/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0311

5.2 Difficulties in using opportunity costs

! Estimating future costs/revenues and hence the benefit sacrificed can bedifficult

! Identifying alternative uses and hence the best alternative forgone can bedifficult

! Ignores effect on accounting profit

! Ignores the risk of each alternative

5.3 Deprival value

! This measures the value to a business of an existing asset in terms of the cost

incurred if the business were to be deprived of it

! Deprival value is calculated as follows

RC = Replacement cost NRV = Net realisable valuePV = PV of expected future earnings which the asset will generate

The lower of

RC and The hi her of

NRV PV

Example 5

Identify the deprival value in each case.

Case RC NRV PV

1 500 600 550

2 700 600 550

3 700 600 650

Solution

1

2

3

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 59/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0312

FOCUS

You should now be able to

! describe and distinguish between relevant and non-relevant costs

! apply and evaluate limiting factor analysis

! evaluate short run decisions e.g. make or buy.

! describe and apply cost-volume-profit (breakeven) analysis

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 60/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0313

EXAMPLE SOLUTIONS

Solution 1 – BEA

Output 10,000 ———

£

20,000 ———

£

30,000 ———

£Sales

Variable costs

8,000

(6,000)

16,000

(12,000)

24,000

(18,000) ——— ——— ———

ContributionFixed costs

2,000(2,000)

4,000(2,000)

6,000(2,000)

Profit ———

0 ———

——— 2,000

———

——— 4,000

———

Solution 2 – KFA

Product A B C Contribution per unit

No of kg per unitContribution per kg

Rank

£16

4£4

2

£10

2£5

1

£24

8£3

3

∴ Produce2

000,12= 6,000 units of B

Maximum contribution = 6,000 × 10 = £60,000

Solution 3 – KFA

kg

4,000 units of B uses up 4,000 × 21,000 units of A uses up

8,0004,000

———

12,000 ———

∴ Maximum contribution £

From B 1,000 × £16

From A 4,000 × £10

16,00040,000

——— 56,000

———

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 61/73

COSTS FOR DECISION MAKING

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0314

Solution 4 – Make or buy

X Y Z

Savings per unit of scarce resource

3

1013−= 1

2

1217 −=

2.5 1

1416−= 2

Ranking z y x

Comment: Therefore, the firm should initially make Ys and then make as many Zs as possible.

Utilisation of B:

kg of B

2,500 Ys × 2 kg each uses3,000 Zs × 1 kg each uses

5,0003,000

Total B overall ––––– 8,000

–––––

Comment: The additional 1,000 Zs and 2,000 Xs required should be bought in.

Solution 5 – Deprival value

Case RC NRV PV

1 500 600 550

2 700 600 550

3 700 600 650

7/27/2019 Paper 2.4 - ATC International

http://slidepdf.com/reader/full/paper-24-atc-international 62/73

BUDGETARY CONTROL SYSTEMS

Accountancy Tuition Centre (Overseas Courses) Ltd 2001 0401

OVERVIEW

Objectives

! To understand the purpose of budgeting and to appreciate the variety of different methods of budgeting.

! To appreciate the behavioural as well as the accounting aspects of budgeting.