pages.wustl.edupages.wustl.edu/files/pages/imce/figueroa/slidesinforms2015.pdf · introduction the...

TRANSCRIPT

Optimally Thresholded Realized Power Variationsfor Stochastic Volatility Models with Jumps

José E. Figueroa-López1

1Department of MathematicsWashington University

INFORMS PhiladelphiaNov. 1, 2015

(Joint work with Jeff Nisen)

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 1 / 31

Introduction The Framework and the Statistical Problems

Framework

1 Finite-Jump Activity (FJA) Itô Semimartingales:

dXt = γtdt + σtdWt + dJt

• {Wt}t≥0 is a standard Brownian motion;• t → γt and t → σt are the drift and volatility functions;• Jt :=

∑Ntj=1 ζj :

t → Nt is the counting process of jumps s.t. Nt <∞, for all t > 0{ζj}j are the jump sizes;

2 FJA Lévy Model:

Xt = γt + σWt +∑Nt

j=1 ζj

• {Nt}t≥0 is a homogeneous Poisson process with jump intensity λ;• {ζj}j≥0 are i.i.d. with density fζ : R→ R+;• the triplet ({Wt}, {Nt}, {ζj}) are mutually independent.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 2 / 31

Introduction The Framework and the Statistical Problems

Framework

1 Finite-Jump Activity (FJA) Itô Semimartingales:

dXt = γtdt + σtdWt + dJt

• {Wt}t≥0 is a standard Brownian motion;• t → γt and t → σt are the drift and volatility functions;• Jt :=

∑Ntj=1 ζj :

t → Nt is the counting process of jumps s.t. Nt <∞, for all t > 0{ζj}j are the jump sizes;

2 FJA Lévy Model:

Xt = γt + σWt +∑Nt

j=1 ζj

• {Nt}t≥0 is a homogeneous Poisson process with jump intensity λ;• {ζj}j≥0 are i.i.d. with density fζ : R→ R+;• the triplet ({Wt}, {Nt}, {ζj}) are mutually independent.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 2 / 31

Introduction The Framework and the Statistical Problems

Classical Problems

Given a finite discrete record of observations,

Xt0 ,Xt1 , . . . ,Xtn , π : 0 = t0 < t1 < · · · < tn = T ,

the following problems are of interest under a high-frequency sampling setting(i.e., mesh(π) := maxi{ti − ti−1} → 0):

1 Estimating the integrated variance:

σ̄2T :=

∫ T

0σ2

t dt .

2 Estimating the jump features of the process:• Jump times: say, {τ1 < τ2 < · · · < τNT } if NT ≥ 1, or ∅, otherwise.• Corresponding jump sizes: {ζ1, ζ2, . . . , ζNT } if NT ≥ 1, or ∅, otherwise.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 3 / 31

Introduction The Main Estimators

Two main classes of estimators for σ̄2T

=∫ T

0 σ2sds

1 Multipower Realized Variations (Barndorff-Nielsen and Shephard (2004)):

BPV (X )T :=n−1∑i=0

∣∣Xti+1 − Xti

∣∣ ∣∣Xti+2 − Xti+1

∣∣ ,MPV (X )T :=

n−k∑i=0

∣∣Xti+1 − Xti

∣∣r1 . . .∣∣Xti+k − Xti+k−1

∣∣rk , (r1 + · · ·+ rk = 2).

2 Threshold Quadratic Realized Variations (Mancini (2001, 2003)):

TRV (X )[B]π

T :=n−1∑i=0

(Xti+1 − Xti

)2 1{|Xti+1−Xti |≤B}, (B ∈ (0,∞]).

(RQV :=

n−1∑i=0

(Xti+1 − Xti

)2 mesh→0−→ σ̄2T +

NT∑i=1

ζ2i

)

.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 4 / 31

Introduction The Main Estimators

Two main classes of estimators for σ̄2T

=∫ T

0 σ2sds

1 Multipower Realized Variations (Barndorff-Nielsen and Shephard (2004)):

BPV (X )T :=n−1∑i=0

∣∣Xti+1 − Xti

∣∣ ∣∣Xti+2 − Xti+1

∣∣ ,MPV (X )T :=

n−k∑i=0

∣∣Xti+1 − Xti

∣∣r1 . . .∣∣Xti+k − Xti+k−1

∣∣rk , (r1 + · · ·+ rk = 2).

2 Threshold Quadratic Realized Variations (Mancini (2001, 2003)):

TRV (X )[B]π

T :=n−1∑i=0

(Xti+1 − Xti

)2 1{|Xti+1−Xti |≤B}, (B ∈ (0,∞]).

(RQV :=

n−1∑i=0

(Xti+1 − Xti

)2 mesh→0−→ σ̄2T +

NT∑i=1

ζ2i

).

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 4 / 31

Introduction The Main Estimators

Advantages and Drawbacks of TRV

1 Pros:• Can exhibit reduced bias for estimating σ̄2

T , in the presence of jumps• Can be also be used to estimate the process’ jump features:

e.g., N̂[B]π

T :=n−1∑i=0

1{∣∣∣Xti+1−Xti

∣∣∣>B} mesh→0−→ NT .

2 Cons:Performance depends on a “good" selection of the threshold B;

e.g., for a FJA Lévy model and regular sampling (ti = ihn with hn = T/n),

F-L & Nisen (SPA, 2013):

(i) TRV (X )[Bn]π

T is consistent for σ̄2T iff Bn√

hn

n→∞−→ ∞ and Bn → 0;

(ii) E[TRV (X )[Bn]

π

T

]− σ̄2

T ∼ T hn(γ2 − λσ2)− 2Tσφ

(Bn

σ√

hn

)Bn√hn

+2TλB3

n C(fζ )

3

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 5 / 31

Introduction The Main Estimators

Advantages and Drawbacks of TRV

1 Pros:• Can exhibit reduced bias for estimating σ̄2

T , in the presence of jumps• Can be also be used to estimate the process’ jump features:

e.g., N̂[B]π

T :=n−1∑i=0

1{∣∣∣Xti+1−Xti

∣∣∣>B} mesh→0−→ NT .

2 Cons:Performance depends on a “good" selection of the threshold B;

e.g., for a FJA Lévy model and regular sampling (ti = ihn with hn = T/n),

F-L & Nisen (SPA, 2013):

(i) TRV (X )[Bn]π

T is consistent for σ̄2T iff Bn√

hn

n→∞−→ ∞ and Bn → 0;

(ii) E[TRV (X )[Bn]

π

T

]− σ̄2

T ∼ T hn(γ2 − λσ2)− 2Tσφ

(Bn

σ√

hn

)Bn√hn

+2TλB3

n C(fζ )

3

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 5 / 31

Introduction The Main Estimators

Advantages and Drawbacks of TRV

1 Pros:• Can exhibit reduced bias for estimating σ̄2

T , in the presence of jumps• Can be also be used to estimate the process’ jump features:

e.g., N̂[B]π

T :=n−1∑i=0

1{∣∣∣Xti+1−Xti

∣∣∣>B} mesh→0−→ NT .

2 Cons:Performance depends on a “good" selection of the threshold B;

e.g., for a FJA Lévy model and regular sampling (ti = ihn with hn = T/n),

F-L & Nisen (SPA, 2013):

(i) TRV (X )[Bn]π

T is consistent for σ̄2T iff Bn√

hn

n→∞−→ ∞ and Bn → 0;

(ii) E[TRV (X )[Bn]

π

T

]− σ̄2

T ∼ Thn(γ2 − λσ2)− 2Tσφ

(Bn

σ√

hn

)Bn√hn

+2TλB3

n C(fζ )

3

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 5 / 31

Introduction The Main Estimators

Advantages and Drawbacks of TRV

1 Pros:• Can exhibit reduced bias for estimating σ̄2

T , in the presence of jumps• Can be also be used to estimate the process’ jump features:

e.g., N̂[B]π

T :=n−1∑i=0

1{∣∣∣Xti+1−Xti

∣∣∣>B} mesh→0−→ NT .

2 Cons:Performance depends on a “good" selection of the threshold B;

e.g., for a FJA Lévy model and regular sampling (ti = ihn with hn = T/n),

F-L & Nisen (SPA, 2013):

(i) TRV (X )[Bn]π

T is consistent for σ̄2T iff Bn√

hn

n→∞−→ ∞ and Bn → 0;

(ii) E[TRV (X )[Bn]

π

T

]− σ̄2

T ∼ Thn(γ2 − λσ2)− 2Tσφ

(Bn

σ√

hn

)Bn√hn

+2TλB3

n C(fζ )

3

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 5 / 31

Introduction The Main Estimators

Popular thresholds B

• Power Threshold (Mancini (2003))

BPowα,ω := α hωn , for α > 0 and ω ∈ (0,1/2).

• Bonferroni Threshold (Bollerslev et al. (2007) and Gegler & Stadtmüller(2010))

BBFσ̃,C := σ̃h1/2

n Φ−1(

1− C hn

2

), for C > 0 and σ̃ > 0.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 6 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Optimally Thresholded Realized Variations

1 Aims• Introduce an objective “optimal" selection criterion for the threshold B• Develop a feasible implementation method for the optimal threshold B∗.

2 Loss Function

Lossn(B) := En∑

i=1

(1[|∆n

i X |≤B,∆ni N 6=0] + 1[|∆n

i X |>B,∆ni N=0]

),

where, as usual, ∆ni X := Xti − Xti−1 and ∆n

i N := Nti − Nti−1 .

3 InterpretationLossn(B) represents the Total Number of Jump Miss-Classifications:

• fail to identify the occurrence of a jump during [ti−1, ti ].• to flag that a jump occurred during [ti−1, ti ), when no jump occurred,

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 7 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Optimally Thresholded Realized Variations

1 Aims• Introduce an objective “optimal" selection criterion for the threshold B• Develop a feasible implementation method for the optimal threshold B∗.

2 Loss Function

Lossn(B) := En∑

i=1

(1[|∆n

i X |≤B,∆ni N 6=0] + 1[|∆n

i X |>B,∆ni N=0]

),

where, as usual, ∆ni X := Xti − Xti−1 and ∆n

i N := Nti − Nti−1 .

3 InterpretationLossn(B) represents the Total Number of Jump Miss-Classifications:

• fail to identify the occurrence of a jump during [ti−1, ti ].• to flag that a jump occurred during [ti−1, ti ), when no jump occurred,

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 7 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Optimally Thresholded Realized Variations

1 Aims• Introduce an objective “optimal" selection criterion for the threshold B• Develop a feasible implementation method for the optimal threshold B∗.

2 Loss Function

Lossn(B) := En∑

i=1

(1[|∆n

i X |≤B,∆ni N 6=0] + 1[|∆n

i X |>B,∆ni N=0]

),

where, as usual, ∆ni X := Xti − Xti−1 and ∆n

i N := Nti − Nti−1 .

3 InterpretationLossn(B) represents the Total Number of Jump Miss-Classifications:

• fail to identify the occurrence of a jump during [ti−1, ti ].• to flag that a jump occurred during [ti−1, ti ), when no jump occurred,

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 7 / 31

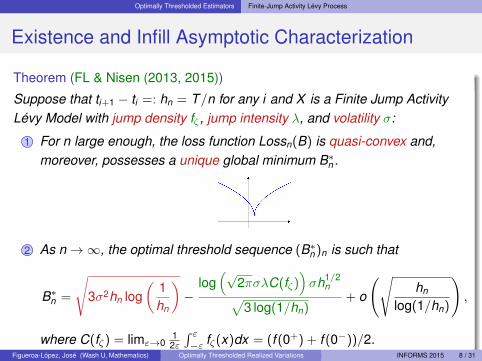

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Existence and Infill Asymptotic Characterization

Theorem (FL & Nisen (2013, 2015))

Suppose that ti+1 − ti =: hn = T/n for any i and X is a Finite Jump ActivityLévy Model with jump density fζ , jump intensity λ, and volatility σ:

1 For n large enough, the loss function Lossn(B) is quasi-convex and,moreover, possesses a unique global minimum B∗n .

2 As n→∞, the optimal threshold sequence (B∗n )n is such that

B∗n =

√3σ2hn log

(1hn

)−

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

+ o

(√hn

log(1/hn)

),

where C(fζ) = limε→012ε

∫ ε−ε fζ(x)dx = (f (0+) + f (0−))/2.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 8 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Existence and Infill Asymptotic Characterization

Theorem (FL & Nisen (2013, 2015))

Suppose that ti+1 − ti =: hn = T/n for any i and X is a Finite Jump ActivityLévy Model with jump density fζ , jump intensity λ, and volatility σ:

1 For n large enough, the loss function Lossn(B) is quasi-convex and,moreover, possesses a unique global minimum B∗n .

2 As n→∞, the optimal threshold sequence (B∗n )n is such that

B∗n =

√3σ2hn log

(1hn

)−

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

+ o

(√hn

log(1/hn)

),

where C(fζ) = limε→012ε

∫ ε−ε fζ(x)dx = (f (0+) + f (0−))/2.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 8 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Existence and Infill Asymptotic Characterization

Theorem (FL & Nisen (2013, 2015))

Suppose that ti+1 − ti =: hn = T/n for any i and X is a Finite Jump ActivityLévy Model with jump density fζ , jump intensity λ, and volatility σ:

1 For n large enough, the loss function Lossn(B) is quasi-convex and,moreover, possesses a unique global minimum B∗n .

2 As n→∞, the optimal threshold sequence (B∗n )n is such that

B∗n =

√3σ2hn log

(1hn

)−

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

+ o

(√hn

log(1/hn)

),

where C(fζ) = limε→012ε

∫ ε−ε fζ(x)dx = (f (0+) + f (0−))/2.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 8 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Remarks

1 The leading term of the optimal sequence is proportional to Lévy’smodulus of continuity of the Brownian motion:

lim suph→0

1√2σ2h log(1/h)

sup|t−s|<h,s,t∈[0,1]

|σWt − σWs| = 1, a.s.

2 The threshold sequences

B∗1n :=

√3σ2hn log

(1hn

), B∗2n := B∗1n −

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

,

are the first and second-order approximations for B∗n , and it can be shownthat the biases of their corresponding TRV estimators attain the “optimal"rate of O(hn) as n→∞.

3 They both provide “blueprints" for devising good threshold sequences!

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 9 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Remarks

1 The leading term of the optimal sequence is proportional to Lévy’smodulus of continuity of the Brownian motion:

lim suph→0

1√2σ2h log(1/h)

sup|t−s|<h,s,t∈[0,1]

|σWt − σWs| = 1, a.s.

2 The threshold sequences

B∗1n :=

√3σ2hn log

(1hn

), B∗2n := B∗1n −

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

,

are the first and second-order approximations for B∗n , and it can be shownthat the biases of their corresponding TRV estimators attain the “optimal"rate of O(hn) as n→∞.

3 They both provide “blueprints" for devising good threshold sequences!

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 9 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

Remarks

1 The leading term of the optimal sequence is proportional to Lévy’smodulus of continuity of the Brownian motion:

lim suph→0

1√2σ2h log(1/h)

sup|t−s|<h,s,t∈[0,1]

|σWt − σWs| = 1, a.s.

2 The threshold sequences

B∗1n :=

√3σ2hn log

(1hn

), B∗2n := B∗1n −

log(√

2πσλC(fζ))σh1/2

n√3 log(1/hn)

,

are the first and second-order approximations for B∗n , and it can be shownthat the biases of their corresponding TRV estimators attain the “optimal"rate of O(hn) as n→∞.

3 They both provide “blueprints" for devising good threshold sequences!

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 9 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.

2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A Feasible Implementation Algorithm Based on B∗1n

1 Key Issue: The threshold B∗1 would allow us to find an (approximately)“optimal" estimate σ̂2 for σ2 of the form

σ̂2 :=1T

TRV (X )[B∗1]n

but B∗1n := B∗1n (σ2) depends precisely on σ2.2 The previous issue suggests a “fixed-point" type of implementation:

(i) Get a “rough" estimate of σ2 via, e.g., the Realized Quadratic Variation:

σ̂2n,0 :=

1T

RQVT :=1T

n∑i=1

|Xti − Xti−1 |2

(ii) Use σ̂2n,0 to estimate the optimal threshold B̂∗1n,0 :=

(3 σ̂2

n,0hn log(1/hn))1/2

(iii) Refine σ̂2n,0 using thresholding,

σ̂2n,1 =

1T

n∑i=1

|Xti − Xti−1 |21[|Xti

−Xti−1|≤B̂∗1

n,0

]

(iv) Iterate Steps (ii) and (iii): σ̂2n,0 → B̂∗1n,0 → σ̂2

n,1 → B̂∗1n,1 → σ̂2n,2 → · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 10 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A numerical illustration I

(S2) Kou Model: 1-week / 5-minuteσ = 0.5, λ = 50, γ = 0

p = 0.45, α+ = 0.05, α− = 0.1

Method TRV STRV Loss SLoss

B̂∗1n,k∗n

0.5004 0.0186 0.2232 0.4706

Powω=0.495;α=1 0.4407 0.0142 13.5302 3.6392BF 0.4917 0.0193 1.180 1.0775

Table: Finite-sample performance of the threshold realized variation (TRV) estimatorsbased on 5, 000 sample paths of the Kou model:

fKou(x) = pα+

e−x/α+ 1[x≥0] + (1−p)α−

e−|x|/α−1[x<0].Loss represents the total number of Jump Misclassification Errors, while TRV , Loss,

STRV , and SLoss denote the corresponding sample means and standard deviations,respectively.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 11 / 31

Optimally Thresholded Estimators Finite-Jump Activity Lévy Process

A numerical illustration II

(S3) Kou Model: 1-year / 5-minuteσ = 0.4, λ = 1000, γ = 0p = 0.5, α+ = α− = 0.1

Method TRV STRV Loss SLoss

B̂∗1n,k∗n

0.4039 0.0028 139.6776 12.2193

Powω=0.495;α=1 0.3767 0.0019 230.0170 15.0308BF 0.6495 0.0315 375.5850 24.3999

Table: Finite-sample performance of the threshold realized variation (TRV) estimatorsbased on K = 5, 000 sample paths of the Kou model:

fζ(x) = pα+

e−x/α+ 1[x≥0] + qα−

e−|x|/α−1[x<0].Loss represents the total number of Jump Misclassification Errors, while TRV , Loss,

STRV , and SLoss denote the corresponding sample means and standard deviations,respectively.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 12 / 31

Extensions Additive Processes

Additive Processes and general sampling schemes

1 The model:

Xs :=

∫ s

0γ(u)du +

∫ s

0σ(u)dWu +

Ns∑j=1

ζj =: X cs + Js,

where ζji.i.d.∼ fζ and (Ns)s≥0 ∼ Poiss ({λ(s)}s≥0), independent of W , and

deterministic functions σ, λ : [0,∞)→ R+ and γ : [0,∞)→ R with σ andλ bounded away from 0.

2 Localized Optimal ThresholdingGiven a sampling scheme π : 0 = t0 < · · · < tn = T , determine the vector~Bπ,∗ = (Bπ,∗t1 , . . . ,Bπ,∗tn ) that minimizes the problem

inf~B=(Bt1 ,...,Btn )∈Rm

+

En∑

i=1

(1[|Xti−Xti−1 |>Bti ,Nti−Nti−1 =0] + 1[|Xti−Xti−1 |≤Bti ,Nti−Nti−1 6=0]

)

=n∑

i=1

infBti

{P (|∆iX | > Bti ,∆iN = 0) + P (|∆iX | ≤ Bti ,∆iN 6= 0)} ,

(∆iX := Xti−1+hi − Xti−1 , ∆iN := Nti−1+hi − Nti−1 , hi = ti − ti−1)

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 13 / 31

Extensions Additive Processes

Additive Processes and general sampling schemes

1 The model:

Xs :=

∫ s

0γ(u)du +

∫ s

0σ(u)dWu +

Ns∑j=1

ζj =: X cs + Js,

where ζji.i.d.∼ fζ and (Ns)s≥0 ∼ Poiss ({λ(s)}s≥0), independent of W , and

deterministic functions σ, λ : [0,∞)→ R+ and γ : [0,∞)→ R with σ andλ bounded away from 0.

2 Localized Optimal ThresholdingGiven a sampling scheme π : 0 = t0 < · · · < tn = T , determine the vector~Bπ,∗ = (Bπ,∗t1 , . . . ,Bπ,∗tn ) that minimizes the problem

inf~B=(Bt1 ,...,Btn )∈Rm

+

En∑

i=1

(1[|Xti−Xti−1 |>Bti ,Nti−Nti−1 =0] + 1[|Xti−Xti−1 |≤Bti ,Nti−Nti−1 6=0]

)

=n∑

i=1

infBti

{P (|∆iX | > Bti ,∆iN = 0) + P (|∆iX | ≤ Bti ,∆iN 6= 0)} ,

(∆iX := Xti−1+hi − Xti−1 , ∆iN := Nti−1+hi − Nti−1 , hi = ti − ti−1)

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 13 / 31

Extensions Additive Processes

Additive Processes and general sampling schemes

1 The model:

Xs :=

∫ s

0γ(u)du +

∫ s

0σ(u)dWu +

Ns∑j=1

ζj =: X cs + Js,

where ζji.i.d.∼ fζ and (Ns)s≥0 ∼ Poiss ({λ(s)}s≥0), independent of W , and

deterministic functions σ, λ : [0,∞)→ R+ and γ : [0,∞)→ R with σ andλ bounded away from 0.

2 Localized Optimal ThresholdingGiven a sampling scheme π : 0 = t0 < · · · < tn = T , determine the vector~Bπ,∗ = (Bπ,∗t1 , . . . ,Bπ,∗tn ) that minimizes the problem

inf~B=(Bt1 ,...,Btn )∈Rm

+

En∑

i=1

(1[|Xti−Xti−1 |>Bti ,Nti−Nti−1 =0] + 1[|Xti−Xti−1 |≤Bti ,Nti−Nti−1 6=0]

)=

n∑i=1

infBti

{P (|∆iX | > Bti ,∆iN = 0) + P (|∆iX | ≤ Bti ,∆iN 6= 0)} ,

(∆iX := Xti−1+hi − Xti−1 , ∆iN := Nti−1+hi − Nti−1 , hi = ti − ti−1)Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 13 / 31

Extensions Additive Processes

Well-posedness and Asymptotic Characterization

Theorem (FL & Nisen, 2014)

For any fixed T > 0, there exists h0 := h0(T ) > 0 such that, for each t ∈ [0,T ]

and h ∈ (0,h0], the function

Lt,h(B) := P(|Xt+h − Xt | > B,Nt+h − Nt = 0)

+P(|Xt+h − Xt | ≤ B,Nt+h − Nt 6= 0),

is quasi-convex and possesses a unique global minimum, B∗t,h, such that, ash→ 0,

B∗t,h =

√3σ2(t)h log

(1h

)− log(

√2πσ(t)λtC(fζ))σ(t)h1/2√

3 log(1/h)+ o

(√h

log(1/h)

).

Again, the leading term B∗1t,h =√

3σ2(t)h log( 1

h

)provides a blueprint to devise

a good threshold parameter.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 14 / 31

Extensions Additive Processes

Well-posedness and Asymptotic Characterization

Theorem (FL & Nisen, 2014)

For any fixed T > 0, there exists h0 := h0(T ) > 0 such that, for each t ∈ [0,T ]

and h ∈ (0,h0], the function

Lt,h(B) := P(|Xt+h − Xt | > B,Nt+h − Nt = 0)

+P(|Xt+h − Xt | ≤ B,Nt+h − Nt 6= 0),

is quasi-convex and possesses a unique global minimum, B∗t,h, such that, ash→ 0,

B∗t,h =

√3σ2(t)h log

(1h

)− log(

√2πσ(t)λtC(fζ))σ(t)h1/2√

3 log(1/h)+ o

(√h

log(1/h)

).

Again, the leading term B∗1t,h =√

3σ2(t)h log( 1

h

)provides a blueprint to devise

a good threshold parameter.Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 14 / 31

Extensions Additive Processes

Spot Volatility Estimation via Kernel Methods

Notation: hi = ti − ti−1, K θ(t) = 1θK( tθ

)(Kernel), θ = Bandwidth

Algorithm based on Kernel estimation (Fan & Wang(2008), Kristensen(2010))

1 Get a “rough" estimate for t → σ2t via the Kernel estimator:

σ̂20(ti ) :=

∑̀j=−`

|4i+jX |2 K θ(ti − ti+j ),

with θ chosen by a cross-validation type method (cf. Kristensen(2010)).2 Get an initial estimate for the leading term of the optimal threshold:

B̂∗10 (ti ) :=√

3σ̂20(ti )hi log (1/hi )

3 Refine the estimate σ̂20(ti ) using thresholding:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ (ti − ti+j ) 1[|4i+j X |≤B̂∗10 (ti+j )]

4 Iterate Steps 2 and 3 : σ̂20(·)→ B̂∗10 (·)→ σ̂2

1(·)→ B̂∗11 (·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 15 / 31

Extensions Additive Processes

Spot Volatility Estimation via Kernel Methods

Notation: hi = ti − ti−1, K θ(t) = 1θK( tθ

)(Kernel), θ = Bandwidth

Algorithm based on Kernel estimation (Fan & Wang(2008), Kristensen(2010))1 Get a “rough" estimate for t → σ2

t via the Kernel estimator:

σ̂20(ti ) :=

∑̀j=−`

|4i+jX |2 K θ(ti − ti+j ),

with θ chosen by a cross-validation type method (cf. Kristensen(2010)).

2 Get an initial estimate for the leading term of the optimal threshold:

B̂∗10 (ti ) :=√

3σ̂20(ti )hi log (1/hi )

3 Refine the estimate σ̂20(ti ) using thresholding:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ (ti − ti+j ) 1[|4i+j X |≤B̂∗10 (ti+j )]

4 Iterate Steps 2 and 3 : σ̂20(·)→ B̂∗10 (·)→ σ̂2

1(·)→ B̂∗11 (·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 15 / 31

Extensions Additive Processes

Spot Volatility Estimation via Kernel Methods

Notation: hi = ti − ti−1, K θ(t) = 1θK( tθ

)(Kernel), θ = Bandwidth

Algorithm based on Kernel estimation (Fan & Wang(2008), Kristensen(2010))1 Get a “rough" estimate for t → σ2

t via the Kernel estimator:

σ̂20(ti ) :=

∑̀j=−`

|4i+jX |2 K θ(ti − ti+j ),

with θ chosen by a cross-validation type method (cf. Kristensen(2010)).2 Get an initial estimate for the leading term of the optimal threshold:

B̂∗10 (ti ) :=√

3σ̂20(ti )hi log (1/hi )

3 Refine the estimate σ̂20(ti ) using thresholding:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ (ti − ti+j ) 1[|4i+j X |≤B̂∗10 (ti+j )]

4 Iterate Steps 2 and 3 : σ̂20(·)→ B̂∗10 (·)→ σ̂2

1(·)→ B̂∗11 (·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 15 / 31

Extensions Additive Processes

Spot Volatility Estimation via Kernel Methods

Notation: hi = ti − ti−1, K θ(t) = 1θK( tθ

)(Kernel), θ = Bandwidth

Algorithm based on Kernel estimation (Fan & Wang(2008), Kristensen(2010))1 Get a “rough" estimate for t → σ2

t via the Kernel estimator:

σ̂20(ti ) :=

∑̀j=−`

|4i+jX |2 K θ(ti − ti+j ),

with θ chosen by a cross-validation type method (cf. Kristensen(2010)).2 Get an initial estimate for the leading term of the optimal threshold:

B̂∗10 (ti ) :=√

3σ̂20(ti )hi log (1/hi )

3 Refine the estimate σ̂20(ti ) using thresholding:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ (ti − ti+j ) 1[|4i+j X |≤B̂∗10 (ti+j )]

4 Iterate Steps 2 and 3 : σ̂20(·)→ B̂∗10 (·)→ σ̂2

1(·)→ B̂∗11 (·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 15 / 31

Extensions Additive Processes

Spot Volatility Estimation via Kernel Methods

Notation: hi = ti − ti−1, K θ(t) = 1θK( tθ

)(Kernel), θ = Bandwidth

Algorithm based on Kernel estimation (Fan & Wang(2008), Kristensen(2010))1 Get a “rough" estimate for t → σ2

t via the Kernel estimator:

σ̂20(ti ) :=

∑̀j=−`

|4i+jX |2 K θ(ti − ti+j ),

with θ chosen by a cross-validation type method (cf. Kristensen(2010)).2 Get an initial estimate for the leading term of the optimal threshold:

B̂∗10 (ti ) :=√

3σ̂20(ti )hi log (1/hi )

3 Refine the estimate σ̂20(ti ) using thresholding:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ (ti − ti+j ) 1[|4i+j X |≤B̂∗10 (ti+j )]

4 Iterate Steps 2 and 3 : σ̂20(·)→ B̂∗10 (·)→ σ̂2

1(·)→ B̂∗11 (·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 15 / 31

Extensions Additive Processes

Illustration of Opt. Thresh. Spot Vol. Estimation Alg.

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

(A) Initial Estimates

Time Horizon

Actual Spot VolatilityEst. Spot Vol. (Uniform)Est. Spot Vol. (Quad)Sample Increments

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

(B) Intermediate Estimates

Time Horizon

Actual Spot VolatilityEst. Spot Vol. (Uniform)Est. Spot Vol. (Quad)Sample Increments

Figure: Estimation of Spot Volatility using Adaptive Kernel Weighted Realized Volatility.(A) The initial estimates. (B) Intermediate estimates. Parameters: γ(t) = 0.1t ,σ(t) = 4.5t sin(2πet2

)2 + 0.2, λ(t) = 25(e3t − 1), ζii.i.d.= D N (µ = 0.025, δ = 0.025).

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 16 / 31

Extensions Additive Processes

Illustration of Opt. Thresh. Spot Vol. Estimation Alg.

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

(C) Terminal Estimates

Time Horizon

Actual Spot VolatilityEst. Spot Vol. (Uniform)Est. Spot Vol. (Quad)Sample Increments

Figure: Estimation of Spot Volatility using Adaptive Kernel Weighted Realized Volatility.(C) The terminal estimates. (D) Estimation variability, based on 100 generated samplepaths, for the Quadratic Kernel based estimator. Parameters: γ(t) = 0.1t ,σ(t) = 4.5t sin(2πet2

)2 + 0.2, λ(t) = 25(e3t − 1), ζii.i.d.= D N (µ = 0.025, δ = 0.025).

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 17 / 31

Extensions Stochastic Volatility Processes

Stochastic Volatility Models with FJA

1 Motivation: In financial application, one usually encounters models like

Xs :=

∫ s

0γudu +

∫ s

0σudWu +

Ns∑j=1

ζj =: X cs + Js,

where {σt}t≥0 itself is erratic and not smooth.

2 Prototypical Example: Mean-reverting square-root process (CIR Model):

dσ2t = κ

(α− σ2

t)

dt+βσtdW (σ)t , (2κα−β2 > 0, Cov(dW (σ)

t ,dWt ) = ρdt)

3 Pitfalls of the Estimation Methods for σ:

• Spot volatility estimation has received comparatively much less attentionthan integrated variance estimation;

• Few bandwidth selection methods (e.g., Kristensen(2010))

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 18 / 31

Extensions Stochastic Volatility Processes

Stochastic Volatility Models with FJA

1 Motivation: In financial application, one usually encounters models like

Xs :=

∫ s

0γudu +

∫ s

0σudWu +

Ns∑j=1

ζj =: X cs + Js,

where {σt}t≥0 itself is erratic and not smooth.

2 Prototypical Example: Mean-reverting square-root process (CIR Model):

dσ2t = κ

(α− σ2

t)

dt+βσtdW (σ)t , (2κα−β2 > 0, Cov(dW (σ)

t ,dWt ) = ρdt)

3 Pitfalls of the Estimation Methods for σ:• Spot volatility estimation has received comparatively much less attention

than integrated variance estimation;• Few bandwidth selection methods (e.g., Kristensen(2010))

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 18 / 31

Extensions Stochastic Volatility Processes

A Proposed Bandwidth Selection Method

1 Technical Assumption (Kristensen, 2010):

|σ2t+δ − σ2

t | = Lt (δ)δυ + oP(δυ), ∀t , a.s., (δ → 0), (?)

where υ ∈ (0,1] and δ → Lt (δ) is slowly varying (random) function at 0and t → Lt (0) := limδ→0+ Lt (δ) is continuous.

2 Under (?), Kristensen(2010) proposes the following (asymptotically)“optimal" bandwidth:

bwlocopt,t = n−

12υ+1

(σ4

t ‖K‖22

υL2t (0)

) 12υ+1 (??)

3 Pitfall: In general, it is hard to check (?) with explicit constants υ andLt (0) 6= 0.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 19 / 31

Extensions Stochastic Volatility Processes

A Proposed Bandwidth Selection Method

1 Technical Assumption (Kristensen, 2010):

|σ2t+δ − σ2

t | = Lt (δ)δυ + oP(δυ), ∀t , a.s., (δ → 0), (?)

where υ ∈ (0,1] and δ → Lt (δ) is slowly varying (random) function at 0and t → Lt (0) := limδ→0+ Lt (δ) is continuous.

2 Under (?), Kristensen(2010) proposes the following (asymptotically)“optimal" bandwidth:

bwlocopt,t = n−

12υ+1

(σ4

t ‖K‖22

υL2t (0)

) 12υ+1 (??)

3 Pitfall: In general, it is hard to check (?) with explicit constants υ andLt (0) 6= 0.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 19 / 31

Extensions Stochastic Volatility Processes

A Proposed Bandwidth Selection Method

1 Technical Assumption (Kristensen, 2010):

|σ2t+δ − σ2

t | = Lt (δ)δυ + oP(δυ), ∀t , a.s., (δ → 0), (?)

where υ ∈ (0,1] and δ → Lt (δ) is slowly varying (random) function at 0and t → Lt (0) := limδ→0+ Lt (δ) is continuous.

2 Under (?), Kristensen(2010) proposes the following (asymptotically)“optimal" bandwidth:

bwlocopt,t = n−

12υ+1

(σ4

t ‖K‖22

υL2t (0)

) 12υ+1 (??)

3 Pitfall: In general, it is hard to check (?) with explicit constants υ andLt (0) 6= 0.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 19 / 31

Extensions Stochastic Volatility Processes

Heuristic alternative approach

1 Idea: Replace the “path-wise holder continuity assumption" with:

E[(σ2

t+δ − σ2t)2∣∣∣Ft

]= L2

t (0)δ2υ + oP(δυ), a.s. (δ → 0), (? ? ?)

for some positive adapted {Lt (0)}t≥0.2 Then, use (??):

bwlocopt,t = n−

12υ+1

(σ4

t ‖K‖22

υL2t (0)

) 12υ+1 (??)

3 Example: For the CIR model dσ2t = κ

(α− σ2

t)

dt + βσtdW (σ)t , it turns out

thatE((σ2

t+δ − σ2t)2∣∣∣Ft

)= β2σ2

t δ + o(δ).

Hence, (? ? ?) holds with υ = 12 and L2

t (0) = β2σ2t .

4 This in turn suggests the following local bandwidth selection method:

bwlocopt,t = n−1/2

(2σ2

t ‖K‖22

β2

)1/2

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 20 / 31

Extensions Stochastic Volatility Processes

Heuristic alternative approach

1 Idea: Replace the “path-wise holder continuity assumption" with:

E[(σ2

t+δ − σ2t)2∣∣∣Ft

]= L2

t (0)δ2υ + oP(δυ), a.s. (δ → 0), (? ? ?)

for some positive adapted {Lt (0)}t≥0.2 Then, use (??):

bwlocopt,t = n−

12υ+1

(σ4

t ‖K‖22

υL2t (0)

) 12υ+1 (??)

3 Example: For the CIR model dσ2t = κ

(α− σ2

t)

dt + βσtdW (σ)t , it turns out

thatE((σ2

t+δ − σ2t)2∣∣∣Ft

)= β2σ2

t δ + o(δ).

Hence, (? ? ?) holds with υ = 12 and L2

t (0) = β2σ2t .

4 This in turn suggests the following local bandwidth selection method:

bwlocopt,t = n−1/2

(2σ2

t ‖K‖22

β2

)1/2

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 20 / 31

Extensions Stochastic Volatility Processes

Estimation Method for the CIR model (No Jumps)

1 Get a “rough" estimate of σ2t ; e.g., using Alvarez et al. (2010):

σ̂20(ti ) =

RQVti +√

hi− RQVti√

hi=

1√hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2.

2 Estimate the vol vol β using the realized variation of {σ̂0(ti )}i=1,...,n since,for the CIR model, 〈σ, σ〉t = β2

4 ; denote such an estimate by β̂;3 Estimate the optimal local bandwidth based on σ̂2

0 and β̂:

θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

4 Apply kernel estimation with the estimated optimal local bandwidth:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )

5 Iterate steps 3 and 4 : σ̂20(·)→ θ̂0(·)→ σ̂2

1(·)→ θ̂1(·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 21 / 31

Extensions Stochastic Volatility Processes

Estimation Method for the CIR model (No Jumps)

1 Get a “rough" estimate of σ2t ; e.g., using Alvarez et al. (2010):

σ̂20(ti ) =

RQVti +√

hi− RQVti√

hi=

1√hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2.

2 Estimate the vol vol β using the realized variation of {σ̂0(ti )}i=1,...,n since,for the CIR model, 〈σ, σ〉t = β2

4 ; denote such an estimate by β̂;

3 Estimate the optimal local bandwidth based on σ̂20 and β̂:

θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

4 Apply kernel estimation with the estimated optimal local bandwidth:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )

5 Iterate steps 3 and 4 : σ̂20(·)→ θ̂0(·)→ σ̂2

1(·)→ θ̂1(·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 21 / 31

Extensions Stochastic Volatility Processes

Estimation Method for the CIR model (No Jumps)

1 Get a “rough" estimate of σ2t ; e.g., using Alvarez et al. (2010):

σ̂20(ti ) =

RQVti +√

hi− RQVti√

hi=

1√hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2.

2 Estimate the vol vol β using the realized variation of {σ̂0(ti )}i=1,...,n since,for the CIR model, 〈σ, σ〉t = β2

4 ; denote such an estimate by β̂;3 Estimate the optimal local bandwidth based on σ̂2

0 and β̂:

θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

4 Apply kernel estimation with the estimated optimal local bandwidth:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )

5 Iterate steps 3 and 4 : σ̂20(·)→ θ̂0(·)→ σ̂2

1(·)→ θ̂1(·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 21 / 31

Extensions Stochastic Volatility Processes

Estimation Method for the CIR model (No Jumps)

1 Get a “rough" estimate of σ2t ; e.g., using Alvarez et al. (2010):

σ̂20(ti ) =

RQVti +√

hi− RQVti√

hi=

1√hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2.

2 Estimate the vol vol β using the realized variation of {σ̂0(ti )}i=1,...,n since,for the CIR model, 〈σ, σ〉t = β2

4 ; denote such an estimate by β̂;3 Estimate the optimal local bandwidth based on σ̂2

0 and β̂:

θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

4 Apply kernel estimation with the estimated optimal local bandwidth:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )

5 Iterate steps 3 and 4 : σ̂20(·)→ θ̂0(·)→ σ̂2

1(·)→ θ̂1(·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 21 / 31

Extensions Stochastic Volatility Processes

Estimation Method for the CIR model (No Jumps)

1 Get a “rough" estimate of σ2t ; e.g., using Alvarez et al. (2010):

σ̂20(ti ) =

RQVti +√

hi− RQVti√

hi=

1√hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2.

2 Estimate the vol vol β using the realized variation of {σ̂0(ti )}i=1,...,n since,for the CIR model, 〈σ, σ〉t = β2

4 ; denote such an estimate by β̂;3 Estimate the optimal local bandwidth based on σ̂2

0 and β̂:

θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

4 Apply kernel estimation with the estimated optimal local bandwidth:

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )

5 Iterate steps 3 and 4 : σ̂20(·)→ θ̂0(·)→ σ̂2

1(·)→ θ̂1(·)→ σ̂22(·)→ · · ·

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 21 / 31

Extensions Stochastic Volatility Processes

Numerical Illustration (no jumps): Uniform Kernel

Model:CIR stochastic volatility dσ2

t = κ(α− σ2

t)

dt + βσtdW (σ)t .

Parameters:γt ≡ 0.05, λ = 0, ζi ∼ N (0,0.3), κ = 5, α = 0.04, β = 0.5,Cov(dWt ,dW (σ)

t ) = ρdt

Regular Sampling Scheme:T=1/12 (one month) and hn = 5 min

Monte Carlo results of MSE =∑n

i=1

(σ̂2(ti )− σ2(ti )

)2 based on 500 runs

Method ρ = −0.5 ρ = 0 ρ = 0.5Alvarez et al. Method 0.0741 0.0756 0.0766Iterated Kernel Est. with opt. loc. bw 0.0437 0.0441 0.0445Oracle1 Kernel Est. with opt. loc. bw 0.0463 0.0466 0.0472

1Using true parameters values for γ and σFigueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 22 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;

3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.

5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Outlined of Estimation Method (With Jumps)

1 Get a “rough" estimate of t → σ2t by σ̃2(ti ) = 1√

hi

∑j:tj∈(ti ,ti +

√hi ]

(∆n

j X)2

.

2 Using σ̃2, estimate the optimal threshold B̃(ti ) :=[3σ̃2(ti )hi ln(1/hi )

]1/2;3 Refine σ̃2(ti ) using thresholding,

σ̂20(ti ) =

1√hi

∑j:ti∈(ti ,ti +

√hi ]

(∆n

j X)2 1[|∆j X |≤B̃(ti )]

4 Estimate β using the realized variation of {σ̂0(ti )}i=1,...,n =⇒ β̂.5 Refine the estimates of the optimal threshold and local bandwidth:

B̂0(ti ) :=

(3σ̂2

0(ti )hi ln1hi

)1/2

, θ̂0(ti ) := n−1/2(

2σ̂20(ti )‖K‖2

2

β̂2

)1/2

6 Based on θ̂0(ti ) and B̂0(ti ), refine the estimate σ̂20(ti ):

σ̂21(ti ) :=

∑̀j=−`

|4i+jX |2 K θ̂0(ti )(ti − ti+j )1[|∆j X |≤B̂0(ti )]

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 23 / 31

Extensions Stochastic Volatility Processes

Numerical Illustration (with jumps): Uniform Kernel

Model:Normal jump sizes and CIR stochastic volatility.

Parameters:γt ≡ 0.05, λ = 120, ζi ∼ N (0,0.3), κ = 5, α = 0.04, β = 0.5.

Regular Sampling Scheme:T=1/12 (one month) and hn = 5 min

Monte Carlo results of MSE =∑n

i=1

(σ̂2(ti )− σ2(ti )

)2 based on 500 runs

Method MSEAlvarez et al. Method 2.3854Alvarez et al. Method with thresholding 0.8602Kernel Est. with thresholding and opt. loc. bw selection 0.0751Twice Kernel Est. with thresholding and opt. loc. bw selection 0.0652Oracle2 Kernel Est. with thresholding and loc. bw selection 0.0533

2Using true parameters values for γ and σFigueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 24 / 31

Conclusions

Main Contributions

1 Introduced an objective threshold selection procedure based onstatistically optimal criteria.

2 Developed the infill asymptotic characterization of the optimal threshold.

3 Proposed an iterative algorithm to find the optimal threshold sequence.

4 Proposed extensions to more general stochastic models, which allowstime-varying stochastic volatility and jump intensity.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 25 / 31

Conclusions

Ongoing and Future Work

1 Connection between the optimal threshold B∗1 and the data-basedthreshold B̂∗1 obtained by the iterative method

2 Implementation based on the second-order approximation B∗2 of B∗

3 Extensions to infinite-jump activity processes

4 Incorporation of a microstructure noise component

5 Extensions to other loss functions

6 Extensions to other estimation problems where parameter tuning isneeded.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 26 / 31

Appendix Bibliography

For Further Reading I

Figueroa-López & Nisen.Optimally Thresholded Realized Power Variations for Lévy Jump DiffusionModelsStochastic Processes and their Applications 123(7), 2648-2677, 2013.

Figueroa-López & Nisen.Optimality properties of thresholded multi power variation estimators. Inpreparation, 2015.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 27 / 31

Classical Path of a FJA Lévy Model Back Back 2

Figure: Classical Path of Xt = γt + σWt +∑Nt

i=1 ζi ; times and sizes of consecutivejumps are denoted by τ1 < · · · < τn and ζ1, . . . , ζn, respectively.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 28 / 31

Numerical illustration I Back Back 2

●

●●●

●●●●

●●●●●

●●

●●●

●●●●

●●●

●●●

●●●

●●●●

●●●

●

●●

●

●

●

●

●

●

●

●

●

●●

●●

●●

●

●

●

●●●●

●

●

●●

●

●

●

●●●●

●●

●

●●

●

●

●

●

●

●●

●

●

●●

●●

●●●●●

●●●●

●●

●

●

●

●●●

●●

●●●●

●●●

●●

●

●

●

●●

●●

●●●

●●●

●

●

●

●

●

●

●●

●

●

●

●●

●

●

●

●

●

●

●●

●●

●

●●

●

●●●

●

●●●

●●

●

●

●

●

●●●●

●

●

●

●

●

●

●●●

●

●

●

●●

●

●

●

●

●

●●

●

●

●

●●

●

●

●

●

●

●

●

●

●

●●●

●

●●●●●●●●●●●

●

●

●

●

●

●

●●

●●●

●

●

●

●●

●

●

●

●

●

●

●

●●

●

●

●

●

0.34

0.36

0.38

0.40

0.42

0.44

Diff

usio

n V

olat

ility

Par

amet

er E

stim

ates

TRV(GE)

TRV(Hist

)

TRV(BF)

TRV(Pow(0.

35))

TRV(Pow(0.

4))

TRV(Pow(0.

45))

TRV(Pow(0.

495))

MPV(1, 1

)

MPV(2

3, …, 2

3)

MPV(1

2, …, 1

2)

MPV(2

5, …, 2

5)

MPV(1

3, …, 1

3)M

inRV

Med

RV

Merton Model: Diffusion Volatility Parameter Estimates

Calibrated TRV EstimatorsUncalibrated TRV EstimatorsPower Variation Estimators

T = 6−months Freq. 5−min. σ = 0.35 λ = 197.55 δ = 0.037

Figure: Boxplots for Volatility Estimation: Based on 1,000 sample paths. Parameters:σ = 0.35, λ = 197.55, ζ =D N (0, 0.0372), T = 6-months, sampling frequency = 5-min.Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 29 / 31

Numerical illustration II Back

●

●

●

●

●

●●

●

●●

●

●

●●●●

●●●●

●

●

●●●●

●●●●

●

●

●●●●●

●●●●

●

●

●

●

●●

●●●●

●

●

●●

●

●●

●

●●●

●

●●

●

●

●

●

●

●

●

●

●

●●

●

●

●

●●●●

●

●

●

●●●●

●

●

●●

●●

●

●

●●●

●●●

●●

●● ●

●●●

●

●

●

●●

●

●

●

●●

●

●

●

●

●

●

●

●

●

●

●

●

●●●●●

●

●

●

●

●

●

●

●

●●

●

●

●

●

●

●

●●

●

●

●

●

●

●

●

●●

●

●

●●

●●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●●●●

●

●

●●●

●

●

●

●

●●

●

●●●

●●

●

●

●

●

●

0.40

0.45

0.50

0.55

0.60

Diff

usio

n V

olat

ility

Par

amet

er E

stim

ates

TRV(B1 )

TRV(B2 )

TRV(GE)

TRV(Hist

)

TRV(BF)

TRV(Pow)

MPV(1, 1

)

MPV(2

3, …, 2

3)

MPV(1

2, …, 1

2)

MPV(2

5, …, 2

5)

MPV(1

3, …, 1

3)M

inRV

Med

RV

Student's t Model: Diffusion Volatility Parameter Estimates

Oracle Optimal TRV EstimatorsEstimated Optimal TRV EstimatorsAlternative TRV EstimatorsMulti−Power Variation EstimatorsLocal Order Statistics Based Estimatorsσ = 0.45

Sparsity = 0.005 Signal−to−Noise Ratio = 30 T = 1−year Freq. = 15−min.

Figure: Boxplots for Volatility Estimators: Based on 1,000 sample paths. Parameters:σ = 0.45, λ = 32.84, ζ =D t-student(3 d.f.), T = 1-year, hn = 15-min.Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 30 / 31

Numerical illustration III Back

●●●●●

●● ●●●●●●●

●●

●●●●●●● ●

●

●●●●

●

●

●

●●

●

5010

015

020

0

Jum

p R

ate

Par

amet

er E

stim

ates

B1

B2

GEHist BF

Pow

Student's t Model: Jump Rate Parameter Estimation

Oracle Optimal TRV EstimatorsEstimated Optimal TRV EstimatorsAlternative TRV Estimatorsλ = 32.84

Sparsity = 0.005 Signal−to−Noise Ratio = 30 T = 1−year Freq. = 15−min.

Figure: Boxplots for rate estimators λ̂ := N̂[B]TT : Based on 1,000 sample paths.

Parameters: σ = 0.45, λ = 32.84, ζ =D t-student(3 d.f.), T = 1-year, hn = 15-min.

Figueroa-López, José (Wash U, Mathematics) Optimally Thresholded Realized Variations INFORMS 2015 31 / 31