page 2.6.7 major expenditures - lpswp.lps.org/bjames/files/2016/10/major-expenditures... ·...

TRANSCRIPT

Page | 1 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

RECOMMENDED GRADE

LEVELS AVERAGE TIME TO COMPLETE

EACH LESSON PLAN IS DESIGNED AND CONTINUALLY

EVALUATED “BY EDUCATORS, FOR EDUCATORS.” THANK YOU

TO THE FOLLOWING EDUCATORS FOR DEVELOPING

COMPONENTS OF THIS LESSON PLAN.

10‐12

Anticipatory Set & Facilitation: Housing – 55, Transportation – 40,

Food ‐ 30 Conclusion/Assessment Options: Housing: 20‐50, Transportation: 20‐

40, Food: 20‐65 Time does not include the vocabulary activity or potential modifications.

Kimberly Knoche, Family and Consumer Sciences Educator, Forsyth, Montana

NATIONAL STANDARDS LESSON PLAN OBJECTIVES

The curriculum is aligned to the following national standards: National Standards for Financial Literacy American Association of Family and Consumer

Sciences Council for Economic Education National Business Education National Jump$tart Coalition Common Core English Language Arts

Upon completion of this lesson, participants will be able to: Examine ways to maintain a food budget adequate to

income Compare the advantages and disadvantages of

renting and owning a home Identify the total cost of ownership for housing and

transportation Apply the planned buying process to major

expenditures

MATERIALS

MATERIALS PROVIDED IN THIS LESSON PLAN

MATERIALS SPECIFIC TO THIS LESSON

PLAN BUT AVAILABLE AS A SEPARATE

DOWNLOAD

MATERIALS TO ACQUIRE SEPARATELY

DEPENDING ON OPTIONS TAUGHT

Rental Agreement Checklist 2.6.7.A1 Housing Reinforcement 2.6.7.A2 Transportation Reinforcement 2.6.7.A3 Food Reinforcement 2.6.7.A4 Finding a Rental 2.6.7.A5 Eating on a Budget 2.6.7.A6 Major Expenditures Vocabulary List 2.6.7.E1 Sample Rental Agreement 2.6.7.E2 Major Expenditures: Housing, Transportation

and Food Information Sheet 2.6.7.F1 Major Expenditures: Housing, Transportation

and Food Note Taking Guide 2.6.7.L1

Major Expenditures: Housing, Transportation and Food PowerPoint 2.6.7.G1

Spending and Borrowing Unit Multiple Choice Test Bank and Answer Key 2.6.0.M1 & C1

Sheets of paper cut into squares

Fly swatters White board White board markers Music Chairs Rental Advertisements Timer Butcher paper Markers

MAJOR EXPENDITURES HOUSING, TRANSPORTATION AND FOOD

Advanced Level www.takechargetoday.arizona.edu

Page | 2 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

RESOURCES

EXTERNAL RESOURCES

External resources referenced in this lesson plan: Edmunds Tips on Buying a New Car Video www.youtube.com/watch?v=tOQLk4gQzNs Consumer Expenditure Survey www.bls.gov/cex Examples of apartment rental websites

o www.apartments.com o www.apartmentguide.com o www.rent.com o www.zillow.com (tablet application also available)

Kelly Blue Book Cost of Ownership www.kbb.com/new‐cars/total‐cost‐of‐ownership Consumer Reports www.consumerreports.org/cro/cars/index.htm Consumer Jungle www.consumerjungle.org Financial Calculators

o www.bankrate.com o www.mymortgagecalculator.org o www.practicalmoneyskills.com/calculators

My Plate www.myplate.gov NetGrocer www.netgrocer.com

TAKE CHARGE TODAY RESOURCES

Similar lesson plan at a different level: None available

Optional lesson plan resources: Vocabulary Reinforcement Activities Active Learning

Tool 3.0.36 Fly Swatter Facts Active Learning Tool 3.0.17 True or False Active Learning Tool 3.0.12 Musical Chairs Active Learning Tool 3.0.23 Life of…. 1.0.0 Guest Speaker Active Learning Tool 3.0.22 News Headline Active Learning Tool 3.0.54 Purchasing an Automobile Assessment 2.6.8

CONTENT

EDUCATOR MATERIALS PARTICIPANT READING

Materials to support educators when preparing to teach this lesson plan are available on the Take Charge Today website.

Major Expenditures: Housing, Transportation and Food Information Sheet 2.6.7.F1

OPTIONAL ADVANCE INSTRUCTION

This lesson is designed to be taught as a stand‐alone lesson. However, background content knowledge from the following lesson plans is directly related to this lesson and may be helpful for participants.

Basics of Taxes 2.2.2 Type of Insurance 2.6.5 Credit Basics 2.6.2 Credit Reports and Scores 2.6.1 Smart Consumer Spending 2.6.6

LESSON FACILITATION

Page | 3 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

PREPARE

Visual indicators to help prepare the lesson INSTRUCT

Instructions to conduct the lesson facilitation CUSTOMIZE

Potential modifications to lesson facilitation

VOCABULARY ACTIVITY

Mini Dictionary

Approximate time: 20 minutes prior to instruction and 15 minutes at the end

Materials to prepare: 1 sheet of paper per participant (must be cut square) Vocabulary Reinforcement Activities Active Learning Tool 3.0.36 for directions

for Mini Dictionary 3.0.36.J4

Before instruction:

1. Complete the mini dictionary vocabulary activity. Directions may be found in the Vocabulary Reinforcement Activities Active Learning Tool 3.0.36.

After instruction: 2. Conduct the mini dictionary activity again, but instead of defining the word

have participants use the word in a sentence.

ANTICIPATORY SET

Fly Swatter Facts Approximate time: 10 minutes Materials to prepare: Fly Swatter Facts Active Learning Tool 3.0.17

o Major Expenditures: Housing, Transportation and Food 3.0.17.E2 2 fly swatters White board and markers

1. Conduct the fly swatter facts activity to learn statistics about major

expenditures. Refer to the Fly Swatter Facts Active Learning Tool 3.0.17 for directions and materials.

a. Fly Swatter Facts is an activity that encourages participants to review terms or facts. The answers to review questions are written on the board and when a question is asked, a participant holding a fly swatter walks to the board and swats the correct answer.

RECOMMENDED FACILITATION OPTION There is one facilitation option provided for this lesson. The facilitation is broken into distinctive allowing an educator to teach housing, transportation and food individually or as a sequence.

PowerPoint Presentation Approximate time: 95 minutes Housing – 45 minutes Transportation – 30 minutes Food – 20 minutes Materials to prepare: Major Expenditures: Housing, Transportation and Food PowerPoint 2.6.7.G1

o Housing ‐ Slides 4‐23 o Transportation – Slides 24‐34

To avoid giving participants too many handouts at once, distribute each section of the note taking guide as it is discussed.

Show a video such as Edmunds Tips on Buying a New Car.

Page | 4 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

o Food – Slides 35‐40 1 Major Expenditures: Housing, Transportation and Food Note Taking Guide

2.6.7.L1 per participant (housing, transportation and food are in separate sections to use all or part)

Optional: o 1 Sample Rental Agreement 2.6.7.E2 per participant o 1 Rental Agreement Checklist 2.6.7.A1 per participant o 1 sheet of butcher paper and markers per group of 2‐3 o True or False Active Learning Tool 3.0.12

i. True or False Questions for Major Expenditures: Transportation 3.0.12.K2

o 1 chair per participant + 2 extra Present the Major Expenditures: Housing, Transportation and Food PowerPoint Presentation 2.6.7.G1. Distribute one Major Expenditures: Housing, Transportation and Food Note Taking Guide 2.6.7.L1 per participant. Part 1: Your Present Self Impacts Your Future Self 1. Slide 2: Food, Transportation and Housing: Over 60% of Average Spending

a. Housing, transportation and food are the largest expenses for most individuals.

i. Taxes and insurance are discussed in separate lesson plans: The Basics of Taxes 2.2.2 and Types of Insurance 2.6.5.

b. Ask participants what influences spending choices. i. The percentages are just averages. Consumers may spend

more or less in a category depending on multiple factors such as their values, goals, where they live, etc.

2. Slide 3: Your Present Self Impacts Your Future Self a. Using the planned buying process helps to maximize satisfaction;

especially with durable good purchases. b. Housing and transportation are often purchased with credit which

impacts net worth. Part 2: Renting Housing 3. Slide 4: Housing – Your Dream House

a. Have participants work in groups of 2‐3 to describe their dream house.

i. Encourage participants to do so by writing or drawing a picture.

ii. Ask participants to include details such as location, nearby facilities (such as a school), amenities, etc.

b. As a class, ask participants about the characteristics of this house. i. Do they rent or own? ii. Where is it located? iii. How big is it and who lives there? iv. What type of amenities does it have? v. Which characteristics are needs vs. wants?

4. Slide 5: Housing: Largest Expense for Most a. According to the 2011 Consumer Expenditure Survey, the average

Give participants play doh and have them use it to visually estimate how much they spend in each major expenditure category. Discuss why everyone’s spending will be different.

Show a variety of housing advertisements to illustrate factors that can impact pricing.

Page | 5 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

consumer spends 34% of their income on housing. b. Prices for houses vary greatly depending on several variables. For

example: i. Homes in cities are often more expensive than rural areas. ii. Homes near schools, shopping or other community areas can

be more expensive 5. Slide 6: Renting a Home – Important Terms

a. When individuals rent a home, they are paying to use property that a landlord owns.

6. Slide 7: What are common rental expenses? a. Stress that there are several expenses, in addition to rent, that

contribute to the total cost of housing. When creating spending plan, individuals must include all expenses.

i. According to the 2011 Consumer Expenditure Survey, the 34% the average consumer allocated to housing was broken down as follows:

1. 19.8% rent or mortgage 2. 7.5% utilities 3. 2.3% household operations 4. 1.2% household supplies 5. 3% furnishings and equipment

b. Renters insurance and communications are optional expenses. Stress that renters insurance is highly recommended as the landlord is not responsible for property loss or liability.

7. Slide 8: Where can you find a place to rent? a. When renting a home, there are several sources that advertise

available rentals. 8. Slide 9: When Comparing Properties

a. Individuals should make a list of essential vs. preferred features. b. If possible, visit properties of interest in person or online. c. It is important that individuals understand the rental policies and

calculate the total cost of living for each rental to truly compare properties and make sure it is an affordable location.

d. Have participants brainstorm what housing features would be essential vs. preferred for them.

9. Slides 10‐11: What types of questions would you ask when comparing rental properties?

a. Have participants brainstorm and then add to the discussion with slides 10‐11.

b. Direct costs i. Understand the rental length (typically renewed monthly or

yearly) and policies if an agreement is terminated early. ii. Some rentals will include certain utilities in the monthly

rental amount. iii. Some amenities may be provided including furnishings and

appliances. Check if laundry is available in the rental or an on‐site community laundry room. Learn if the machines are coin operated.

c. Policies

Conduct a class field trip a property management company and/or view several properties to learn about and practice asking questions about policies.

Have a panel of young adults discuss their experiences renting and living with roommates.

Page | 6 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

i. Each rental has different policies about how the property can be used and safety features. In advance of renting, individuals should get a copy of the policies to ensure it is a property they will be satisfied with.

ii. Repairs and maintenance are typically the responsibility of the landlord. But, individuals should be aware of policies regarding items such as lawn care that may be their responsibility and an added expense.

iii. It is important to know what constitutes a violation in the rental agreement and eviction terms.

10. Slide 12: What types of questions does a landlord ask on a rental application? a. When an individual is interested in renting a property, they will

typically complete a rental application. This helps the landlord compare potential tenants.

b. Landlords often review an individual’s credit history which is another reason to have a positive history.

11. Slide 13: Rental Agreement a. A rental agreement is a contract that protects both the landlord and

the tenant. b. Individuals should not rent a property without a written agreement.

12. Slide 14: What initial expenses may be required to rent a property? a. All or part of the security deposit may be returned when a renter

moves out depending on policies outlined in the rental agreement. 13. Optional: Rental Agreement Activity

a. Divide participants into groups of 2‐3. b. Provide each group with a Sample Rental Agreement 2.6.7.E2 and

Rental Agreement Checklist 2.6.7.A1. c. Have participants review the Sample Rental Agreement 2.6.7.E2 and

use the Rental Agreement Checklist 2.6.7.A1 to evaluate if the rental agreement is comprehensive. Then, respond to the reflection questions.

d. As a class, discuss: i. What was missing from the rental agreement and why does it

matter? ii. If they received this rental agreement, how would they work

with a landlord to address any missing information? iii. Stress that the agreement is designed to protect both them

and the landlord. iv. Have participants identify what expense categories should be

included in a spending plan for this rental. Part 3: Purchasing Housing 14. Slide 15: Purchasing a Home

a. When purchasing a home, many individuals work with a real estate agent.

15. Slide 16: Home Loan a. Depending on the type of loan and lender, different factors will be

evaluated to determine if an individual is eligible and the loan amount. Common factors include credit history, income, net worth

Show participants local rental agreements and applications.

Show the “Buying a House 101” video on the Consumer Jungle website to learn more about working with real estate agents.

Page | 7 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

and current expenses. b. There are several government programs that may help individuals

with the down payment or qualify for a home loan. Especially for first‐time home buyers. However, a positive credit history is still essential.

c. It is important to shop around for credit. Different lenders may offer different rates and closing costs vary.

16. Slide 17: Two Significant Initial Expenses a. The down payment and closing costs are significant initial expenses

when purchasing a property. b. If an individual does not have a 20% down payment, they will pay

private mortgage insurance as a part of their mortgage to protect the lender. This is different than homeowners insurance that provides for the home owner in case of property loss or liability.

17. Slide 18: Mortgage Payment a. A mortgage payment typically includes more than the cost of the

home. 18. Slide 19: What are typical home ownership expenses?

a. The maximum amount a lender will loan an individual could be more than they can afford.

b. Special assessments are fees charged by local government to pay for things like street lights, schools, roads, etc.

c. Some experts recommend that individual’s should plan on 2‐3% of the home’s value be allocated to maintenance and repairs each year.

19. Slide 20: Purchasing a $250,000 Home a. Show scenario one to illustrate the cost of mortgage insurance as a

result of a lower down payment. b. Scenario two illustrates how a low credit score can result in a higher

interest rate. Over time, the cost can be significant. 20. Slide 21: Statement of Financial Position

a. A home is an investment if it is worth more than what is owed on the home. This, along with the pride of ownership and tax benefits are advantages to home ownership.

b. However, home ownership can be a risk because the property value may decrease, it is a contractual expense and may be difficult to sell the home and there may be large unanticipated expenses.

Optional ‐ Part 4: Rent vs. Own Activity 21. Slide 22: Rent vs. Own Activity

a. Have participants work in groups of 2‐3 to brainstorm at least two advantages and two disadvantages of renting vs. owning on a piece of butcher paper.

b. As a class, share the answers and discuss. 22. Slide 23: Rent. Vs. Own Activity Answers

a. Add to the discussion with pros and cons from this slide. Part 5: Transportation 23. Slide 24: Transportation

a. Remind participants that the average consumer spends 17% of their income on transportation. The breakdown is:

Use a tablet or smartphone application to complete the pro and con list. Refer to the Tablet Applications for the Personal Finance Classroom Active Learning Tool 3.0.52 guide for examples.

Page | 8 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

i. Vehicle purchase – 5.4% ii. Fuel – 5.3% iii. Other expenses – 4.9% iv. Public transportation – 1%

b. Ask them to brainstorm transportation options in their community. c. Stress that transportation needs and access to different options

varies greatly between communities. 24. Slide 25: Public Transportation

a. Public transportation is often a cost effective way to get around, but the availability depends on the location and the trade‐offs may be convenience and time.

25. Slide 26: Purchasing an Automobile a. Most vehicles are purchased at a dealership or private sources such

as an individual. 26. Slide 27: Do Your Research

a. Before working with sales personnel, individuals should do their research to know what type of vehicle they want and how much they should expect to pay for that vehicle.

27. Slide 28: What are typical automobile ownership expenses? a. In addition to the monthly payment (if credit was used) there are

several out of pocket costs associated with owning a vehicle. 28. Slide 29: Marina’s Out‐of‐Pocket Expenses

a. Marina purchased a 2013 Honda Accord. She put 10% down on a 5‐year loan at a 2.84% interest rate. Her monthly payment is $347.09.

b. In addition, she used Kelly Blue Book Cost to Own Calculator and learned that, on average, she will pay a total of $19,402 in additional expenses over 5 years to own this vehicle.

c. While not all expenses will be monthly and the total will vary, Marina should plan on the vehicle costing her approximately $670.46 per month to own for the first five years.

29. Slide 30: Depreciation a. One of the most significant costs of owning a vehicle is depreciation.

All vehicles depreciate in value. b. In some cases, the vehicle may depreciate faster than the loan is paid

making an individual upside down on the loan. c. The Statement of Financial Position should record Market Value of a

Vehicle (what it is worth today). This can be found from sources such as Kelly Blue Book.

30. Slide 31: What features would you look for in an automobile? a. Expand on the participants list with examples from the slide.

31. Slide 32: Using Credit a. Vehicles are often purchased using credit. Most lenders will check an

individual’s credit history to determine if a loan will be granted and the terms.

b. It is important to shop around before negotiating. Loan terms may vary significantly between lenders.

32. Slide 33: Down Payment a. Not all vehicle purchases require a down payment. However, if this

occurs, individuals will pay more over the lifetime of the loan and are

Show the “5‐Year Cost to Own” video from the Kelly Blue Book website.

Have participants explore the Kelly Blue Book website to compare the 5‐year Cost to Own data on vehicles they are interested in owning or to determine the value of a used vehicle.

Discuss the impact to consumers of common advertising techniques such as no credit check or no down payment.

Page | 9 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

at greater risk of owing more than the vehicle is worth. b. Use resources, such as Kelly Blue Book, to know the vehicles worth

before negotiating with others. The retail value is not what consumers can typically expect to sell their vehicle for.

33. Slide 34: Leasing a. Individuals may choose to lease a vehicle. If doing this, they must

look closely at the contract to fully understand the terms.

Optional – Part 6: True False Chairs 34. Summarize key points form the transportation section by using the True or

False Active Learning Tool 3.0.12. a. True or False Questions for Major Expenditures: Transportation

3.0.12.K2 is available. Part 7: Food 35. Slide 35: Food

a. Have participants brainstorm if they prefer preparing food at home or eating out. Why?

i. Record participant responses on the white board to reference later.

b. Although food is a consumable item where individuals may spend less time in the planned buying process planning their purchases, the amount spent on food is significant. Especially because impulse buying can be common.

c. Remind participants that the average consumer spends 13% of their income on food. The breakdown is:

i. Food at home ‐ 7.7% ii. Food away from home – 5.3%

36. Slide 36: Two Primary Sources a. Food is a need. However, what is consumed and how it is purchased

can greatly impact the cost. b. Preparing food at home is a form of household production.

37. Slide 37: Burger Night a. Exact food prices will vary depending on the location and grocery

store. Food prepared at home is an average price from a large grocery chain.

i. 2 lb burger ‐ $5.98, package of buns $2.29, cheese slices $3.46, condiments $3, 5 lb potato ‐ $3.75 and a 12 pack of coke $4.88.

b. Not only is the food prepared at home less expensive, but there will be left overs.

c. Have participants brainstorm ways they could reduce the costs of either meal.

i. Order from the value meal. ii. Buy groceries on sale or use coupons. iii. Purchase meat in bulk. iv. Substitute Coke for water.

38. Slide 38: Nutrition a. Regardless of how the food was prepared, individuals should strive to

Illustrate food preparation methods and purchasing options by using cupcakes or chocolate chip cookie as the example.

Have participants create a pros and cons list of new vs. used, new vs. leased, or purchasing an automobile vs. public transportation.

Page | 10 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

eat well balanced meals that are high in nutrition. b. The United States Department of Agriculture provides this graphic

which illustrate what a well‐balanced plate would look like. c. Have participants brainstorm 2‐3 examples of foods from each group. d. An advantage to preparing food at home is the person has

opportunities to enhance nutrition and reduce calories. i. Ask participants how nutrition could be enhanced or calories

reduced with the burger night meal prepared at home. 1. Include a fruit. 2. Substitute Coke for water. 3. Use turkey burger instead of beef. 4. Use sweet potato fries instead. 5. Bake, not fry, potatoes.

39. Slide 39: Other Considerations a. In addition to cost and nutrition, there are several other variables

that impact an individual’s food choices. b. For each consideration, discuss it in the context of food prepared at

home vs. away from home. i. Time – eating out may be quicker. But, individuals should

factor in transportation time as well. ii. Skills – individuals may not have food preparation skills.

However, these skills can be gained from classes, peers, watching online tutorials, etc.

iii. Facilities and equipment – are required to cook at home. 40. Slide 40: Summary

CONCLUSION OPTIONS There are two conclusion options provided for this lesson. 1. Option 1: Musical Chairs 2. Option 2: Reinforcement Worksheets

Option 1: Musical Chairs Approximate time: 20 minutes Materials to prepare: Musical Chairs Active Learning Tool 3.0.23

o Musical Chairs Q and A for Major Expenditures 3.0.23.A2 Music 1 chair per participant 1. Conduct the musical chairs activity. Refer to the Musical Chairs Active

Learning Tool 3.0.23 for directions and materials. a. Musical Chairs encourages participants to introduce or review

concepts while working cooperatively to the tune of songs with a financial message.

Option 2: Reinforcement Worksheets

Approximate time: 20 minutes per worksheet Materials to prepare: 1 Housing Reinforcement 2.6.7.A2 per participant 1 Transportation Reinforcement 2.6.7.A3 per participant

Have participants explore the My Plate website to learn tips for eating on a budget, menu planning, calorie tracking, and much more!

Have participants create a spending plan using the Life of… 1.0.0 scenarios.

Invite a guest speaker to talk about insurance using the Guest Speaker Active Learning Tool 3.0.22.

Page | 11 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

1 Food Reinforcement 2.6.7.A4 per participant 1. Have participants complete one or all three of the worksheets as instructed.

ASSESSMENT OPTIONS There are three assessment options provided for this lesson. 1. Option 1: Finding a Rental 2. Option 2: Transportation News Headline 3. Option 3: Eating on a Budget

Option 1: Finding a Rental Approximate time: 30 minutes Materials to prepare: 1 Finding a Rental 2.6.7.A5 per participant Rental advertisements

o Participants may research them online o If internet access is not available, print 5‐10 apartment rental

advertisements or provide a local newspaper 1. Have participants complete the Finding a Rental 2.6.7.A5 handout as

instructed.

Option 2: Transportation News Headline

Approximate time: 20 minutes Materials to prepare: News Headline Active Learning Tool 3.0.54 1 timer for the facilitator 1 piece of butcher paper per group of 3‐5 1 printed news article or infographic for each group of 3‐5

o News articles may be the same or different for each group. o Short articles printed (or copied) with large font work best.

1 marker per participant 1. Conduct the News Headline activity. Refer to the News Headline Active

Learning Tool 3.0.54 for directions and materials. a. Use a variety of media sources and topics such as:

i. Articles from the Consumer Reports website ii. Articles from the Consumer Jungle website iii. Info graphics iv. Print or television advertisements (including those advertising

credit terms that may or may not be consumer friendly).

Option 3: Eating on a Budget Approximate time: 45 minutes Materials to prepare: 1 Eating on a Budget 2.6.7.A6 per participant Internet Access

o If Internet access is not available, provide weekly grocery advertisements.

Rather than providing articles, have participants find and evaluate their own article based on their previous experiences or questions they have about transportation.

Use the Purchasing an Automobile 2.6.8 unit assessment to have participants used the plan buying process for an automobile purchase.

Have participants work

in small groups.

Give participants a home purchase scenario and have them complete the research process.

Page | 12 2.6.7

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

1. Have participants complete the Eating on a Budget 2.6.7.A6 worksheet as instructed.

2. Once participants have completed the worksheet, discuss the reflection questions as a class comparing different menu ideas as well as strategies to save money, enhance nutrition and overcome potential obstacles.

Page | 13 2.6.7.E1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Major Expenditures Vocabulary List

TERM DEFINITION

1 Closing costs Fees and charges associated with the purchase of a property

2 Depreciation Decrease in the value of an asset associated with the decline in its remaining useful life

3 Down payment Portion of the purchase price that is not borrowed

4 Equity Monetary value of a property minus the amount owed on the property

5 Homeowner’s Association dues

Monthly or yearly fees that pay for the maintenance of shared areas and necessary repairs throughout the community

6 Homeowners insurance Covers damage or loss of the structure and contents, plus liability in case others are injured on the property

7 Landlord The person who owns the property

8 Leasing Renting a product while ownership title remains with the lease grantor

9 Mortgage insurance Protects the lender in case a mortgage loan payment cannot be made and the lender has to take the property back through a process known as foreclosure (also known as private mortgage insurance)

10 Mortgage A loan for the purchase or real estate

11 Real estate agent Licensed individual representing a buyer or seller in a contractual transaction to purchase real property

12 Rent The price paid for the use of someone else’s property

13 Rental agreement A contract specifying the tenant’s and landlord’s legal responsibilities

14 Renter’s insurance An optional (but important) purchase that covers damage and or loss of personal property and liability in a rental home

15 Security deposit Money paid to a landlord to cover potential cleaning costs at the end of the lease, as well as any damages the property suffered during occupancy

16 Special assessments Fees collected by the local city government for utilities, road maintenance and other services such as fire protection and street lighting

17 Tenant A person who rents the property

Page | 14 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

The person who owns the property:

The cost of using someone elses property:

The person who rents the property:

Housing rental expenses to include in a spending plan are:

Major Expenditures Note Taking Guide

Total Points Earned

Name

Total Points Possible

Date

Percentage

Class

Housing – Renting a Home

Two factors that can influence the price of

housing are:

1.

2.

When comparing properties, three questions to ask a landlord about direct costs include:

1.

2.

3.

Page | 15 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Describe the initial expenses that may be required when renting

a property.

A real estate agent is:

They help buyers by...

What are common rental application questions?

When comparing properties, why should you learn about policies?

Why is it important to read a rental

agreement closely?

Housing – Purchasing a Home

Page | 16 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

What types of information does a lender evaluate?

A mortgage payment typically includes:

Expenses to include in your spending plan when making a purchase are:

What is a down payment?

What are closing costs?

What is equity?

Page | 17 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Pros Cons

Transportation expenses to include in a spending plan are:

Transportation

What are pros and cons of public transportation?

Why is it important to do advanced research

before purchasing an automobile?

Why is it important to consider depreciation when purchasing a vehicle?

Page | 18 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

What are five features you would consider when purchasing an automobile?

How does shopping around for

an automobile loan benefit you?

Why is it important to have a

positive credit history when

using credit to purchase an

automobile?

Why is it important to have

down payment when purchasing

an automobile?

What is a resource you could use to learn about the value of a vehicle?

Describe what a consumer should be aware of when leasing a vehicle.

Page | 19 2.6.7.L1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Describe how each consideration can

impact an individuals food choices:

Time: Skills:Facilities and equipment:

Food

What are the primary sources of food?

Why is food prepared at home typically less expensive than food away from home?

What are three ways to eat meals that are well balanced and high in nutrition?

1.

2.

3.

Page | 20 2.6.7.E2

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Sample Rental Agreement By this agreement, made and entered into on June 1, 2013, between Barry Goetz, referred to as “landlord,” and Susan Smith and Debby Jones, are referred to as "tenant," landlord demises and lets to tenant, apartment no. 29 of the building The Missouri Apartments, situated at 350 North River Road, Clarkston, South Dakota, to be used and occupied by tenant as a residence and for no other use or purpose whatever, for a term of one year beginning on June 1, 2013, and ending on May 31, 2014, at a rental of $625 per month, payable monthly, in advance, during the entire term of this agreement, to landlord at 500 South Yellowstone Avenue, Clarkston, South Dakota, or to any other person or agent and at any other time or place that landlord may designate. THE TENANT FURTHER AGREES: 1. SECURITY DEPOSIT On the execution of this agreement, tenant deposits with landlord $500, receipt of which is acknowledged by landlord, as security for the faithful performance by tenant of the terms of this rental agreement, to be returned to tenant, without interest, on the full and faithful performance by tenant of the provisions of this rental agreement. 2. NUMBER OF OCCUPANTS Tenant agrees that the apartment shall be occupied by no more than two persons, consisting of two adults and no children under the age of 18 years without the prior, express, and written consent of landlord. 3. ASSIGNMENT AND SUBLEASING Without the prior, express, and written consent of landlord, tenant shall not assign this rental, or sublease the premises or any part of the premises. Consent by landlord to one assignment or subleasing shall not be deemed to be consent to any subsequent assignment or subleasing. 4. SHOWING APARTMENT FOR RENTAL Tenant grants permission to landlord to show the apartment to new rental applicants at reasonable hours of the day, within 25 days of the expiration of the term of this rental agreement. 5. ENTRY FOR INSPECTION, REPAIRS, AND ALTERATIONS Landlord shall have the right to enter the premises for inspection at all reasonable hours and whenever necessary to make repairs and alterations of the apartment or the apartment building, or to clean the apartment. 6. UTILITIES Electricity, gas, telephone service, and other utilities are not furnished as a part of this rental unless otherwise indicated in this rental agreement. These expenses are the responsibility of and shall be obtained at the expense of tenant. Charges for water and garbage service furnished to the apartment are included as a part of this rental and shall be borne by landlord. 7. REPAIRS, REDECORATION, OR ALTERATIONS Landlord shall be responsible for repairs to the interior and exterior of the building, provided, however, repairs required through damage caused by tenant shall be charged to tenant as additional rent. It is agreed that tenant will not make or permit to be made any alterations, additions, improvements, or changes in the apartment without in each case first obtaining the written consent of landlord. Consent to a particular alteration, addition, improvement, or change shall not be deemed consent to or a waiver of restrictions against alterations, additions, improvements, or changes for the future. All alterations, changes, and improvements built, constructed, or

Page | 21 2.6.7.E2

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

placed in the apartment by tenant, with the exception of fixtures removable without damage to the apartment and movable personal property, shall, unless otherwise provided by written agreement between landlord and tenant, be the property of landlord and remain in the apartment at the expiration or earlier termination of this rental agreement. 8. PARKING SPACE Tenant is granted a license to use parking space No. 2‐I in the apartment building for the purpose of parking one motor vehicle during the term of this rental agreement. 9. REDELIVERY OF PREMISES At the end of the term of this rental agreement, tenant shall quit and deliver up the premises to landlord in as good condition as they are now, ordinary wear, decay, and damage by the elements excepted. 10. DEFAULT If tenant defaults in the payment of rent or any part of the rent at the times specified above, or if tenant defaults in the performance of or compliance with any other term or condition of this rental agreement or of the regulations attached to and made a part of this rental agreement, which regulations shall be subject to occasional amendment or addition by landlord, the rental, at the option of landlord, shall terminate and be forfeited, and landlord may reenter the premises and retake possession and recover damages, including costs and attorney fees. Tenant shall be given written notice of any default or breach. Termination and forfeiture of the rental agreement shall not result if, within 10 days of receipt of such notice, tenant has corrected the default or breach or has taken action reasonably likely to affect correction within a reasonable time. 11. ATTORNEY FEES In the event that any action is filed in relation to this rental agreement, the unsuccessful party in the action shall pay to the successful party, in addition to all the sums that either party may be called on to pay, a reasonable sum for the successful party's attorney fees. In witness, each party to this rental agreement has caused it to be executed at B.T. Rentals on the date indicated below. Date: June 1, 2013 Keys Issued: 2 Landlord: Barry Goetz Automobile license, make and model kept on premises: Tenant(s): Susan Smith Blue Honda Accord KSO‐365 Debby Jones

Page | 22 2.6.7.A1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Rental Agreement Checklist

Directions: Compare the Sample Rental Agreement to the checklist below. If the item is described, put a checkmark in the box. If the term is not included, write ‘no’ then answer the reflection questions. (10 points for completion)

General Terms

Name of all tenants Length of agreement

What happens when agreement expires

Who is allowed to live in the rental

Rent

Total rent amount Rent charged to each tenant

Grace period before late charges assessed & amount charged

Who is responsible for paying utilities

Moving Out

Amount of time the tenant must give to landlord before moving out

Amount of time landlord must give tenant if they want tenant to leave

Rules for cleaning apartment Is subleasing allowed

Rules and Regulations

Noise restrictions Pets allowed

Decorating procedures How to hang items on the wall

Landlord’s right of entry Rules for using the rental

Maintenance

Who is responsible for yard work and clearing sidewalks

Who handles maintenance and repair problems

Furnishings

If laundry facilities are included and the price

Are recreational facilities included

Household items provided Parking rules

Extra Fees

Security deposit specifications Who is liable for accidents in unit

Is renter’s insurance required Are there utility connection fees

1. Identify three items missing in the rental agreement and describe why they need to be included (use the

back of this sheet if necessary). (3 points)

2. What expense categories should be included in a spending plan for this rental? (3 points)

Total Points Earned

Name

16 Total Points Possible

Date

Percentage

Class

Page | 23 2.6.7.A2

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Housing Reinforcement

Total Points Earned

Name

29 Total Points Possible

Date

Percentage

Class

Directions: Match the correct term with the definition. (1 point each) _____1. The price paid for the use of someone else’s property.

_____ 2. The person renting a property.

_____ 3. Monetary value of a property minus the amount owed on the property

_____ 4. A loan for the purchase of real estate.

_____5. Person who owns the property.

_____ 6. Contract specifying the tenant’s and landlord’s legal responsibilities.

_____ 7. Money paid to landlord to cover potential damage.

_____ 8. Portion of the purchase price that is not borrowed.

_____ 9. Fees and charges associated with the purchase of a property.

Directions: Fill in the blank with the appropriate word. (1 point each)

10. Housing is one of the _________________________ expenses for most people.

11. A typical down payment is ______ to _______ % of the purchase price of the home.

12. Rental applications may ask prospective tenants about their ______________, ____________and

______________.

13. Purchasing a property is complex and a real estate agent helps you find property that fits your

______________, ______________ and ________________.

Directions: Provide a short answer to the following questions. 14. Susan is trying to decide if she should purchase renter’s insurance. What would you say to advise her on

this topic? (1 point)

a. Landlord

b. Rent

c. Tenant

d. Rental agreement

e. Security Deposit

f. Mortgage

g. Down Payment

h. Closing Cost

i. Equity

Page | 24 2.6.7.A2

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

15. Explain four ways your personal financial condition can affect your housing choice. (4 points) 1. 2. 3. 4

16. Joel has recently accepted a job offer and is trying to decide whether he should rent or buy housing. He is

relocating to an urban area with public transportation although he does have a bike that he enjoys riding and would need to be able to store. This is his first position since graduating from college and he doesn’t know anybody in the area. Since he is an architect, he needs space for his drafting table and enjoys designing homes. In the area below list at least three reasons why he should choose either renting or buying as his housing choice. (6 points)

17. Now that Joel has looked at his options what are 3 resources for finding available homes to rent or

purchase? (3 points) 18. If viewing a possible rental what are 2 items to be looking for? (2 points)

Rent Buy

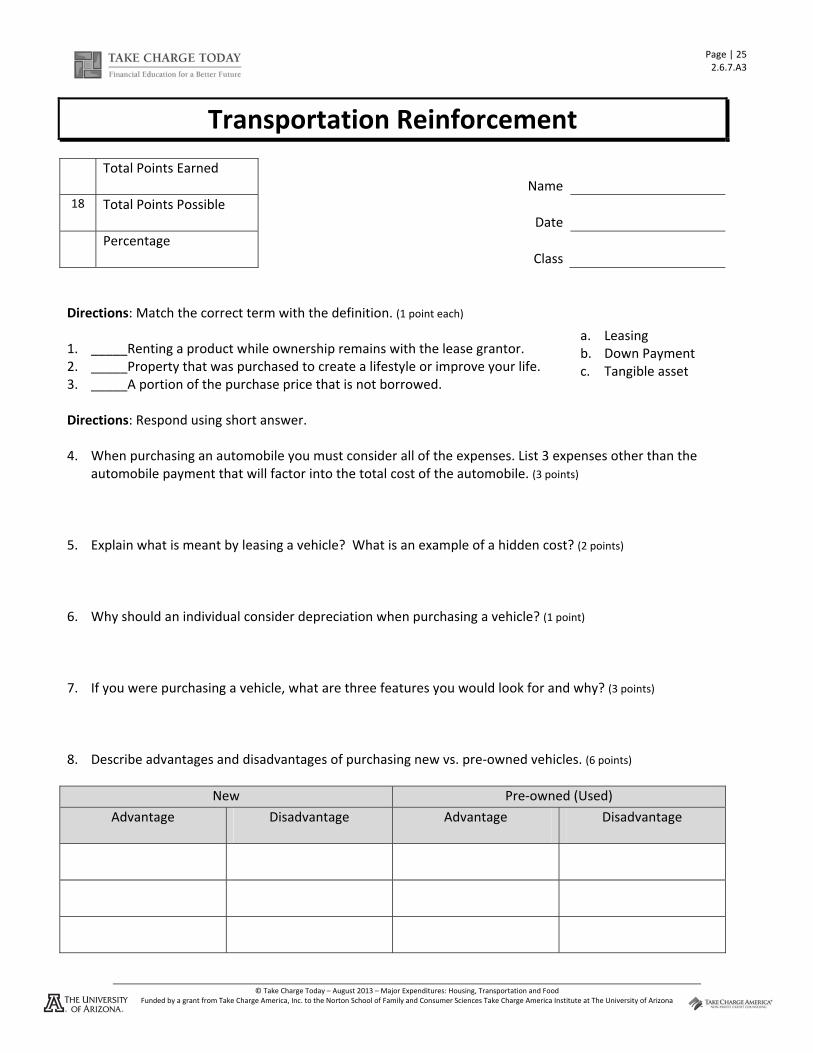

Page | 25 2.6.7.A3

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Transportation Reinforcement

Total Points Earned

Name

18 Total Points Possible

Date

Percentage

Class

Directions: Match the correct term with the definition. (1 point each) 1. _____Renting a product while ownership remains with the lease grantor. 2. _____Property that was purchased to create a lifestyle or improve your life. 3. _____A portion of the purchase price that is not borrowed. Directions: Respond using short answer. 4. When purchasing an automobile you must consider all of the expenses. List 3 expenses other than the

automobile payment that will factor into the total cost of the automobile. (3 points) 5. Explain what is meant by leasing a vehicle? What is an example of a hidden cost? (2 points) 6. Why should an individual consider depreciation when purchasing a vehicle? (1 point) 7. If you were purchasing a vehicle, what are three features you would look for and why? (3 points)

8. Describe advantages and disadvantages of purchasing new vs. pre‐owned vehicles. (6 points)

New Pre‐owned (Used)

Advantage Disadvantage Advantage Disadvantage

a. Leasing b. Down Payment c. Tangible asset

Page | 26 2.6.7.A4

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Food Reinforcement

Total Points Earned

Name

23 Total Points Possible

Date

Percentage

Class

Directions: Compare and contrast the following lasagna options.

Scratch Ready‐to‐Eat Full‐Service Restaurant

Brand Easy Lasanga III (beef and homemade

sauce)

Stouffers Family Size Lasagna with Meat and

Sauce

Olive Garden Lasagna Classico – lunch portion

Source www.allrecipes.com www.stouffers.com www.olivegarden.com Cost $10.50 $13.79 $10.75 Number of Servings 7 5 1 Approximate Preparation Time

30 minutes to prepare 30 minutes to cook

350 degree oven for 1 hour and 25‐30

minutes

Travel and time at the restaurant

Calories per serving 491 290 580 Sodium per serving 937mg 670mg 1930mg

1. Calculate the cost per serving for each option. (3 points)

Scratch Ready‐to‐eat Full‐Service Restaurant

2. What are 2 pros and 2 cons of each option? (12 points)

Pros Cons

Scratch

Ready‐to‐eat

Full‐Service Restaurant

Page | 27 2.6.7.A4

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

3. If you were to create a well‐balanced meal with lasagna as your entrée, what additional items would include? (3 points)

4. Which food source (scratch, ready‐to‐eat or full‐service restaurant) would be the easiest and most cost

effective to create a well‐balanced meal from. Describe why. (2 points) 5. Describe a situation when each food source option would be the most ideal for an individual. (3 points)

Scratch: Ready‐to‐eat: Full‐service restaurant:

Page | 28 2.6.7.A5

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Finding a Rental

Total Points Earned Name

28 Total Points Possible Date

Percentage Class

Scenario: You are searching for your first apartment. After reviewing your spending plan, you estimate that

you have up to $650 per month available for your total housing expenses.

Directions: Review rental advertisements, and identify two properties that you feel are a good fit for your

needs, wants and spending plan.

1. Rank, in order of importance, 5 features you would look for in a rental. (5 points)

Most important:

Least important:

1.

2.

3.

4.

5.

2. Review rental advertisements and identify two properties that are a good fit for you. Compare those

properties using the chart below. If the information is not provided in the announcement, indicate “not

included.” (10 points for completion)

Advertisement #1 Advertisement #2

Date advertisement

posted:

Source:

Address:

Rent:

Page | 29 2.6.7.A5

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Initial expenses:

What categories must

be planned for in a

spending plan?

Policies:

Advantages of the

property include:

Disadvantages of the

property include:

3. Describe, using at least three reasons, which rental is the best fit for you. (3 points)

o

o

o

4. What are five questions you would ask the landlord about your preferred property? (5 points)

o

o

o

o

o

5. What are three things you would look for in a rental agreement about your preferred property? (3 points)

o

o

o

6. What are two things you can do to be an ideal candidate on a rental application and tenant? (2 points)

o o

Page | 30 2.6.7.A6

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Eating on a Budget

Total Points Earned Name

44 Total Points Possible Date

Percentage Class

Scenario: Joleen is a college student living in an apartment. She is trying to keep the food portion of her spending plan at $30 a week. She plans to eat 3 meals daily with one small snack. She would like to eat out once a week if possible. Her refrigerator and pantry have the following items:

□ ½ pound deli sliced ham □ 3 eggs

□ 2 oranges □ 1 can of soup

□ 1 box mac n’ cheese □ 1 banana

□ 4 slices bread □ Ketchup

□ 1 Tomato □ Ranch dressing

□ 2 slices of cheese □ Variety of staples (butter, sugar, miracle whip, cooking spices)

The weekly ad lists the following sale items.

Item Quantity Cost Item Quantity Cost

□ Cheerios Box $2.50 □ Hashbrowns 32 oz $2.00

□ Strawberries 1 lb $2.00 □ Orange Juice ½ Gallon $2.99

□ Rib Steak 1 lb $5.99 □ Green Beans 12 oz $2.49

□ Red Peppers Each $1.50 □ Baby Carrots Bag $0.99

□ Shredded Cheddar 8 oz $1.50 □ Yogurt 6 oz $0.50

□ Pork and Beans can $0.79 □ Chips bag $3.99

□ Rice Roni Box $1.00 □ Pancake Mix Box $2.69

□ Pasta Bag $0.99 □ Pasta Sauce Jar $1.79

□ Chicken can $2.00 □ Spaghettio’s can $0.89

□ Hot Pockets Box $2.00 □ Pizza Box $3.50

□ Frozen Vegetable Bag $1.50 □ Bread loaf $1.48

□ Eggs 1 dozen $2.39 □ Apple 1 lb $1.79

□ Fresh Spinach 16 oz $2.45 □ Hamburger 1 lb $2.75

Other items (up to 8)

Item Quantity Cost Item Quantity Cost

□ □

□ □

□ □

□ □

Page | 31 2.6.7.A6

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Step 1: Create the Menu (20 points for completion) Help Joleen develop a meal plan for one week. Remember, her goal is to spend no more than $30 on groceries! For each meal, indicate the food needed such as spaghetti (pasta, hamburger, sauce), apple and slice of bread. When developing her meal plan, keep the following in mind: Use what she already has in her refrigerator and pantry (assume she has non‐perishable staple items) Up to eight items, in addition to the weekly ad of sale items may be purchased. Leftovers can be used Some items have enough quantity to be used for multiple meals Create well balanced meals high in nutrition

Breakfast Lunch Dinner Snack

Monday

Tuesday

Wednesday

Thursday

Friday

Saturday

Sunday

Step 2: Create a Grocery List and Evaluate the Budget Use the menu plan to create a grocery list by placing a check mark next to all items on page 1 that will be

used. (5 points for completion) Determine the price of items not on the grocery list using a website such as NetGrocer or visiting a local

grocery store. (5 points for completion) Calculate the total cost of the grocery list:____________________ (1 point)

Step 3: Reflection

1. Were you able to create a meal plan that was $30 or under? Why or why not? (2 points)

Page | 32 2.6.7.A6

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transportation and Food Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

2. What are three strategies you used to help Joleen stretch her food dollars as much as possible? (3 points)

o

o

o

3. If Joleen wanted to go out to dinner with friends, what advice would you give her to stick to her $30 weekly

food budget? (2 points)

4. Select two meals to evaluate. (5 points each)

a. Day and meal:________________________

i. Based on the MyPlate guidelines, does that meal include all of

the food groups? If not, what would you change about the

meal to be balanced?

b. Day and meal:_________________________

i. Based on the MyPlate guidelines, does that meal include all of the food groups? If not,

what would you change about the meal to be balanced?

5. When you were advising Joleen about the meal plan, she expressed the following concerns. Identify how you would respond to Joleen to help her overcome those challenges (this may include recommending modifications to the menu).

a. Three days per week she is on campus for class and cannot easily come home to eat lunch. (2 points)

b. In the evenings, she is often tired and needs to study. She estimates she only has 30 minutes to

spend preparing meals. (2 points)

c. Joleen’s cooking skills are limited. (2 points)

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 1 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

One of the biggest housing decisions you’ll make is whether to rent or

purchase a home. Plan on spending about 1/3 of your income on housing,

which is just about the na onal average. The size and loca on of the home,

ameni es within the community and the local real estate market will

influence the amount of money you’ll spend on your housing choice.

Ren ng Your Home

Rent is the price paid for the use of someone else’s property. A tenant rents

property from a landlord. The tenant pays the landlord “rent” (a fee, usually

paid monthly) to live in the landlord’s property. In large apartment

complexes or neighborhoods with large inventories of single‐family rental

homes you may find yourself working with a property manager or a property

management office. They’re the same as a landlord; they just have more

rental proper es to manage.

Informa on about exis ng rental proper es is available through many family and community resources.

How much of your income can you afford to pay towards a monthly rental payment? Here are some typical expenses your

spending plan should include when inves ga ng the rental market. Some of these items might be included in the monthly

rent.

Rent – Your regular payment to a landlord for the use of property.

U li es – How much will electricity, water, and garbage service, cost you if they’re not included in your rent?

Household furnishings include all items that make your home habitable.

Renter’s insurance ‐ An op onal (but important) purchase that covers damage and or loss of your personal property

and liability in your rental home. However, it doesn’t cover the loss of the dwelling if it is destroyed by fire or natural

disaster.

Communica on expenses include internet, television and phone service.

Your present self impacts your future self.

Housing, transporta on and food comprise over 60% of spending choices for most people. As a consumer, you have a range

of spending op ons in each of these categories. Decisions and tradeoffs you make here will have a big impact on your

budget and what you have le to spend on other things. Take the me to understand your op ons and apply the planned

buying process.

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 2 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

When ren ng a home, you may have some ini al expenses to pay before moving in:

Pre‐payment – You may be required to pay the first and last month’s rent

immediately upon signing your rental agreement.

Security deposit ‐ This is money you pay your landlord to cover cleaning costs

when you leave your unit at the end of the lease, as well as any damages the

property suffered during your occupancy. Damage repairs to be charged against your deposit must go beyond normal

wear and tear of a rental property. If you paid an addi onal month’s worth of rent upon signing your ini al contract,

your landlord typically has one month to return those funds to you. However, part or all of that deposit will be

withheld depending on the condi on of the property upon your departure. If your landlord holds back funds, he/she

must present you with a wri en list of the damages and the amount of money needed to clean and make repairs. If the

deposit is larger than the amount required for repairs and cleaning, the landlord must return the excess.

If you are approved to rent a property make sure you receive the rental

agreement before providing any deposits or rent payments. A rental agreement

(also referred to as a lease) is a contract specifying the tenant’s and the

landlord’s legal responsibili es. A rental agreement is a contract. Once signed,

you are responsible for the terms of the lease. Examine the rental agreement

closely making sure it clearly outlines informa on about expenses and policies.

The rental agreement is there to protect you and to outline your legal

responsibili es as a tenant.

You might be subject to financial penal es should you break any of the terms in

your lease. Most rental agreements state that the tenant (you) will pay rent for a

specific amount of me, usually 12 months from your signing date. If you break

the rental agreement before the contractual me period is over, you’ll probably

have to con nue to pay rent to the end of your contract or be assessed a

penalty charge. Check your rental agreement and don’t assume anything!

To begin comparing rental proper es, make a list of essen al vs. preferred features. Then, if possible make appointments to

view your favorite proper es. When comparing proper es it’s important that you ask a poten al landlord several ques ons:

Rent – How much is the rent, when is it due and what payment methods are available.

Length rental contract– Is the contract based on 12 months? If you want to shorten

the contract will that affect your rental payments? U li es – Learn who is responsible for paying each u lity bill.

Ameni es – Determine if any features such as furniture, appliances, on‐site laundry or a community pool are provided

and if so, whether there is an addi onal charge for usage.

Repairs and maintenance – If the dishwasher leaks or the furnace stops working are you responsible for the repairs?

Find out what maintenance is covered under your rental agreement and the associated fees for repair work.

Policies – Can you live with a restric on that says no overnight street parking? Do you have a pet and want to bring it to

your new home? What if you like to grill out? Check to see if there are restric ve policies related to the quality of life

you’d like to live. Be sure to ask for a wri en copy of all rental policies and restric ons before signing a lease.

Landlord/Property Manager’s Access Rights to the Property – Unless it’s an extreme emergency your landlord typically

must give you a 48‐hour no ce prior to entering your rental home. This varies from state to state. Make sure to read

and become familiar with your rights.

Evic on terms – Understand your rights and the policies associated with a landlord’s cause to evict you from your rental

property. Filling out a rental applica on is part

of the rental process. You may be

asked to verify Who will be living at the

property

Your current and past employers

and your income (don’t be

surprised if the landlord contacts

your employer to verify)

Your previous rental history

You’ll most likely also be asked to

supply addi onal character

references and approve your future

landlord’s request to pull your credit

reports.

Don’t rent without a rental

agreement ‐ A wri en rental

agreement protects the tenant.

Remember, your credit history

affects more than just credit. It

can also influence if a landlord

will rent a property to you.

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 3 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

Home Ownership

Homeownership provides a broad range of benefits including pride of ownership, tax benefits, and the opportunity to build

equity. Equity is the monetary value of a property minus the amount owed on the property. Building equity in your home

over me will increase your net worth. However, a home purchase and ongoing costs of home ownership also involve

expenses that you wouldn’t necessarily have if you decided to rent. A home purchase is a complicated transac on and

represents one of the largest single investments you’ll most likely ever make.

One of the first steps to take as a poten al homeowner is to find a good real estate agent. A real estate agent is a licensed

individual represen ng a buyer or seller in a contractual transac on to purchase real property. The agent should be

someone you can relate to, someone who understands your needs and has the exper se and know‐how necessary to help

you find the right home for you. A large part of a real estate agent’s job is to help guide you through the contract and

closing process.

Few people can buy a home for cash. According to the Na onal Associa on of REALTORS® (NAR), nearly nine out of 10

buyers finance their purchase, which means that virtually all buyers ‐‐ especially first‐ me purchasers ‐‐ require a loan.1 To

obtain a loan you’ll have to fill out a loan applica on and provide suppor ng documenta on. You’ll be asked to supply pay

stubs, rental checks and past tax returns. Loans are obtained through mortgage bankers, mortgage brokers, savings and

loan associa ons, commercial banks, credit unions and insurance companies.

If you finance (borrow money) your home purchase you will enter into a loan contract agreeing to repay the sum of money

borrowed. A loan for the purchase of real estate is called a mortgage. A mortgage is a special type of loan that is backed by

the property that it is used to purchase. Under a mortgage contract, the property is considered collateral on the loan and

the lender can take back the property if you do not repay as agreed. The repayment period for most home purchase loans

is either fi een or thirty years.

What can you begin doing today to qualify for a home loan with favorable terms?

Using a mortgage to purchase a home will involve two large ini al expenses.

Down payment is the por on of the purchase price that is not borrowed. A mortgage down payment is typically 5 –

20% of the purchase price of the home. If you can’t afford a full 20% down payment on a home, then the lender will

typically add mortgage insurance to the contract and include the cost as part of your monthly mortgage payment.

Also known as "Private Mortgage Insurance," PMI protects the lender in case you can’t make your mortgage loan

payments and the lender has to take the property back through a process known as foreclosure.2 In that event, the

insurance provider would reimburse the lender for any loss due to your failure to repay as agreed. Lenders o en

require PMI if a borrower provides less than a 20% down payment, because these loans are considered higher risk. The

PMI payment is usually paid monthly as part of the overall mortgage payment to the lender.

Closing costs are fees and charges associated with the purchase of a property. The exact amount depends on several

variables but can be 1‐4% of the purchase price.

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 4 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

Other home ownership expenses include:

U li es

Household furnishings

Special Assessments – fees collected by the local city government for u li es,

road maintenance and other services such as fire protec on and street

ligh ng.

Homeowner’s Associa on Dues – condos and residen al communi es may

charge monthly or yearly fees through a Homeowners Associa on (HOA) that

will pay for the maintenance of shared areas and necessary repairs throughout

the community

Communica on expenses including internet, television and phone service

The current market value of

your home is considered an

asset on your Statement of

Financial Posi on. However,

if you use a mortgage to

finance the purchase of the

home, the remaining

balance on your mortgage

loan is considered a liability.

In addi on to paying down the principal and interest on your mortgage loan, your monthly mortgage payment will also

include an amount to cover your property taxes and homeowner’s insurance costs. Homeowner’s Insurance covers

damage or loss of the structure and contents, plus your liability in case others are injured on your property. Most

lenders who provide a mortgage require the borrower to purchase homeowners insurance sufficient to cover loss of the

structure.

The average person spends 17% of their income on transporta on. As a

consumer you have several transporta on op ons.

Public Transporta on

Some ci es have limited public transporta on op ons (taxi, subway, bus, light

rail) and even in ci es with well‐developed networks, not all areas are

covered equally. However, if public transporta on is available this may be the

most cost‐effec ve op on because it doesn’t require you to pay the costs of

maintenance and repairs associated with vehicle ownership. The cost of using

the different modes of public transporta on varies significantly. Some public

transporta on systems offer passes (usually monthly or yearly) to help reduce

a user’s cost.

When purchasing an automobile you’ll discover there are two main sources of inventory: an automobile dealership and

vehicles offered for sale by other consumers. Dealerships sell a variety of new and used automobiles. Private owners usually

sell pre‐owned vehicles.

A major decision you’ll make before purchasing your automobile is whether you will buy new or used (also referred to as

pre‐owned). Before working with sales personnel, it is important that you carefully evaluate your needs and wants to

understand what vehicle op ons will meet your lifestyle.

Purchasing an Automobile

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 5 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

Here are some typical transporta on expenses to consider prior to

purchase:

Automobile loan payment – If you finance your purchase what

is your required loan payment?

Fuel costs – This expense will depend on vehicle performance

and how much you drive.

Maintenance and repairs –Do research to es mate the costs

associated with normal wear and tear based on how many

miles you expect to drive per year. Keep in mind that some

vehicle models (especially foreign imports) are much more

expensive to maintain and repair than others.

License and registra on – This is a yearly fee and varies greatly.

Insurance – Your age, sex and prior driving record all influence

this cost.

Parking – If your place of employment doesn’t provide free

parking during your workday how much will on street parking or

a local parking garage cost?

Costs associated with vehicle ownership vary

depending on the make and model of your

automobile and how much you drive it.

Newer automobiles have higher license and

registra on fees than older automobiles, but

older automobiles may also cost more to

maintain.

Consumer Reports

provides unbiased

informa on comparing

vehicle features, pricing,

safety ra ngs and much

more.

Kelly Blue Book Cost to Own (h p://www.kbb.com/new‐cars/total‐cost‐of‐ownership/) is an online es mator tool that

helps you understand how much it costs to own and operate a vehicle and how much money to allocate in your spending

plan.

The current market value of an automobile is considered a tangible asset (property purchased to create a lifestyle or

improve your present life) on your Statement of Financial Posi on. Each year the value of your automobile will decrease.

This is known as deprecia on (decrease in the value of an asset associated with the decline in its remaining useful life).

The deprecia on rate depends on the age of the vehicle as well as its make and model. If you used an automobile loan to

finance your purchase, the remaining balance on your loan is a liability on your Statement of Financial Posi on.

Depending on the amount borrowed, the car may depreciate faster than your loan balance declines. If the car’s value

becomes smaller than the remaining balance on your loan, you are considered “upside down with your loan.” This

doesn’t pose an immediate problem, but could present an obstacle to selling or trading your car for a different model, in

which case you would need to pay back the lender more than you would receive from the sale. You can reduce the

likelihood that you’ll have an upside down period during your loan payback if your original loan has a shorter loan term

(for example, 48 months instead of 60 months) and/or a larger down payment (for example, 20% instead of 10%).

What features would you want in an automobile?

2.6.7.F1

© Take Charge Today – August 2013 – Major Expenditures: Housing, Transporta on and Food – Page 6 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

Know what features you want in a car and the average price

for that vehicle. This will help you nego ate the best

possible price.

Examples of features that may be important to you include:

Cost – what can you afford?

Size – how many passengers will this car carry?

Usage – how will you use this vehicle?

Gas mileage – What’s the average MPG (miles per

gallon)?

Safety ra ngs – How safe is the vehicle compared to

other models?

Reliability – How reliable is the vehicle? What are the average maintenance and repair costs?

Environmental impact – Does the model have features (other than fuel economy) that reduce its environmental

impact?

Deprecia on – How quickly will the value of the vehicle depreciate? What did you learn from your research?

Upgraded features – What upgraded features would you consider adding to the price of your purchase? What are

some upgraded features you can live without?

Using Credit to Make Your Purchase

Automobile loans are available from depository ins tu ons or automobile dealerships. Most lenders check your credit

history to determine whether you can qualify for a loan. Loan rates vary significantly, so it is important to shop around in

advance of nego a ng your purchase.

Most lenders require a down payment (the por on of the purchase price that is not borrowed) be made. The down

payment amount depends on many factors including the price of the automobile and the lender’s specific terms. If you plan

to sell your current vehicle and use the money from its sale as your down payment, research your vehicle’s worth in

advance of working with a dealership. This helps determine whether the dealership is offering a good trade‐in value for your