pact

DESCRIPTION

PACT responseTRANSCRIPT

Response to BBC Strategy Review

May 2010

BBC strategy review

2

Executive summary

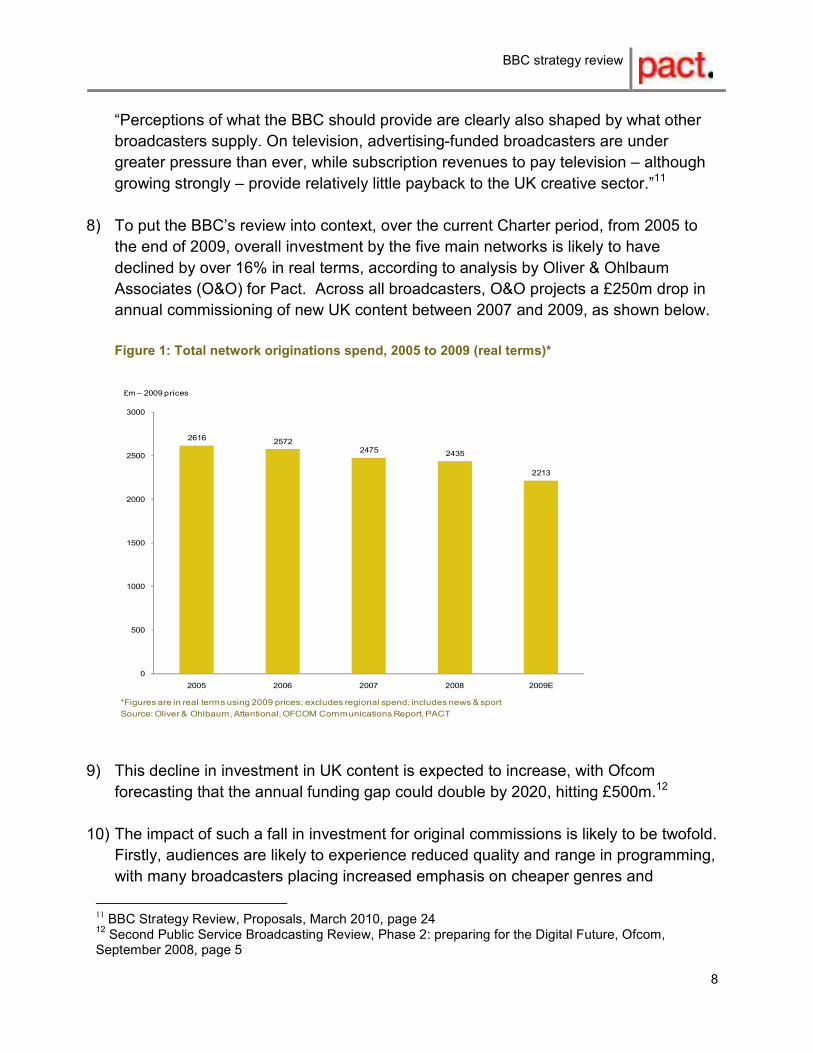

1) UK-made content is vital to public service broadcasting and other services,

representing, challenging and, at its best, uniting our society in a way that

imported programmes never can. However, investment in UK programmes by

commercial sector broadcasters is under severe pressure. Over the current

Charter period, from 2005 to the end of 2009, overall investment by the five main

networks is likely to have declined by over 16% in real terms, according to

analysis by Oliver & Ohlbaum Associates (O&O) for Pact. Across all

broadcasters, O&O projects a £250m drop in annual commissioning of new UK

content between 2007 and 2009.1

2) This is likely to have two negative effects: reduced quality and range of content

for UK audiences as broadcasters move to cheaper genres and imports (the BBC

is already a near monopoly broadcaster of UK-made programming for older

children, for example); and an undermining of the recent growth of the UK

content sector on a global level (exports of UK television programmes have risen

by 39% since 2003,2 but initial investment by a broadcaster through a

commission is vital to enabling the producer to generate further export sales).

3) We therefore broadly welcome the focus in the strategy review on UK content, in

particular the commitment by BBC Management to maintain a level of content

spending and, through allocating a set proportion of resources to content, a

capping of non-content spending. We also welcome the principle of reducing and

capping spending on foreign acquisitions as part of a focus on UK-made content

that fulfils public service values. In light of the market conditions that we have

highlighted above, the proposed focus on content is particularly relevant to the

BBC’s fulfilment of its Public Purpose under the Charter of stimulating creativity.

4) However, the BBC’s proposals do raise a number of issues that Pact requests

the Trust and Management consider and, if appropriate, address. These fall into

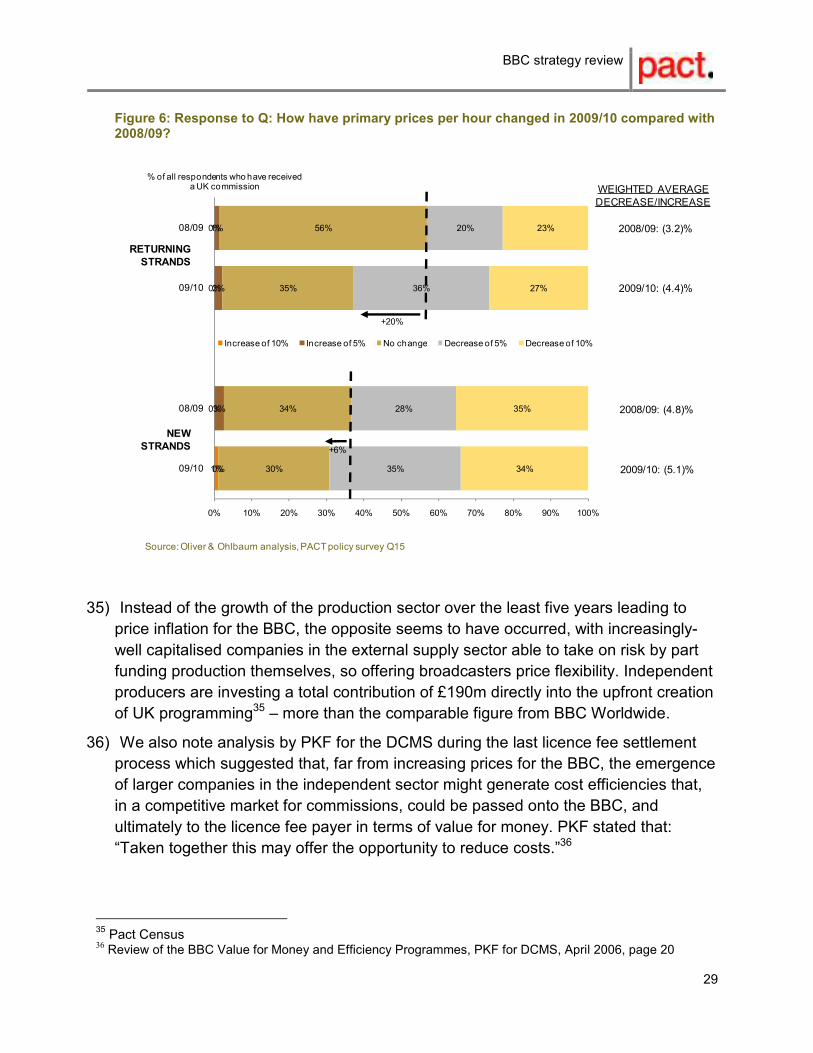

the following areas:

1 Oliver & Ohlbaum Associates for Pact 2 Annual Export Figures, TRP for Pact/UKTI

BBC strategy review

3

Clarity over figures and definitions: Several headline proposals in the strategy

paper lack detail in key areas that risk potentially misleading industry and the

licence fee payer, and raise difficulties in measuring the implementation of the

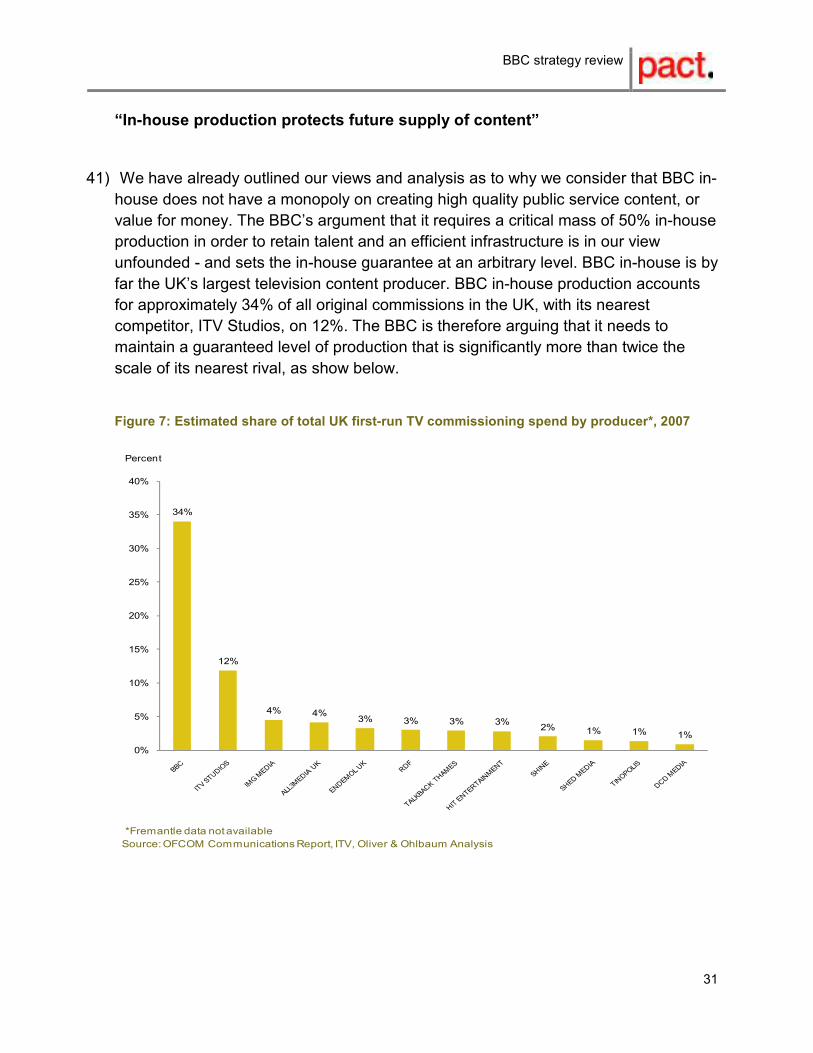

proposals, and thereby holding BBC Management to account.

In this area, we propose that the BBC should:

• Clarify the time frame for achieving its 90% target for spending on content/distribution.

• Guarantee a level of spending on first-run originations.

• Adopt a definition of content consistent with that used by Ofcom.

• Break down planned spending on television, radio and online content.

• Measure the target of 90% on content/distribution against income.

• Make public the cost of in-house and external commissions per hour, as well as by service.

• Clarify whether dividends paid to the BBC by BBC Worldwide will be included in its 90% target

for content/distribution.

• Make public BBC spending on content/distribution as a proportion of total group expenditure

(or preferably income). This would include BBC Worldwide.

• Only buy imports where there is a clear public service rationale and where the BBC does not

have to compete against the market to acquire such content. To ensure this it should only buy

overseas series after their first season has aired in their domestic market.

• Clarify why it has set its proposed reduction in imports at just 20%, and look to reduce imports

further.

• Benchmark spend on imports against other UK broadcasters and BBC originations.

Putting quality at the heart of commissioning: the BBC strategy proposals

have rightly considered how much and on which type of programming the BBC

should invest, but they do not look at whether the BBC’s commissioning

framework ensures it commissions programmes on a meritocratic and cost-

efficient basis, regardless of whether they originate in-house or externally. In-

house currently benefits from a 50% guarantee of all qualifying BBC

commissions, plus BBC news, despite the case for this guarantee being in our

view fundamentally flawed, and despite the fact that the guarantee increasingly

risks distorting commissioning by placing an artificial restraint on BBC

commissioners that prevents commissioning from external companies after a

fixed point – potentially preventing them from commissioning the best ideas on

merit.

BBC strategy review

4

In this area, we propose that the BBC should:

• Review whether current commissioning structures are optimal on a strategic basis, with a

view to removing the in-house guarantee or setting it an appropriate level as soon as

possible.

• Demonstrate publicly why the in-house guarantee should be maintained and at what level.

Online: the strategy paper does not consider the negative impact of proposed

cuts in online investment on the nascent online content sector, which is likely to

undermine the BBC’s fulfilment of its Public Purpose under the Charter of

stimulating UK creativity.

In this area, we propose that the BBC should:

• Limit negative market impact through a clear remit, not cutting 25% of spending.

• Introduce an online WOCC of 25%, in addition to the 25% external quota.

• Address concerns over the inclusion of services in the external quota; if this is not possible, it

should introduce a 50% WOCC.

Content priorities: The BBC strategy review has rightly indentified UK children’s

content as one of its five content priorities, but its proposals do not in our view

address this issue in a meaningful way. In feature film, the BBC is required under

the Charter Agreement to have “a film strategy” in place,3 yet this is not

addressed in the strategic review. The Trust is in the final stages of a separate

review of BBC Films’ strategy and, in being mindful of BBC Charter requirements,

this overarching strategy review should take account of its findings.

In this area, we propose that the BBC should:

Children’s:

• Increase annual investment in first-run originations by £50m.

Film:

• Increase the share of revenues from the BBC corridor to the producer. The majority of these

revenues could be placed in a “lock-box” so that they can be accessed only for future

development and production.

• Reduce the overall licence period for film and the exclusive window to five years.

• Over time double the annual budget of BBC Films to around £20m.

3 BBC Charter Agreement, 8 (2) (a)

BBC strategy review

5

Introduction

1) Pact is the trade association that represents the commercial interests of the

independent production sector. We have more than 600 member companies,

involved in creating and distributing television, film and interactive content.

2) The independent production sector creates around half of all new UK television

programmes each year,4 as well as acclaimed UK films. The sector’s turnover is

£2.2 billion per year5 and it employs 20,950 people – more than the terrestrial

broadcasting and the cable and satellite sectors respectively.6

3) For further information, please contact Pact’s director of policy, Adam Minns, at

[email protected] or on 020 7380 8232.

4 Ofcom, Communications Market Report, 2008

5 Pact Census

6 Employment Census 2006, Skillset

BBC strategy review

6

Section 1: Prioritising content

1) Pact welcomes in principle the strategy review’s commitment to content through the

five content priorities and related proposals. As the trade association for the

independent production sector, Pact has consistently championed UK-made content

as crucial to delivering the public service values enshrined in the BBC Charter and

highlighted in the strategy paper – i.e. informing, educating and entertaining

audiences through high quality, original and cost-efficient programmes and content.

2) In recent years, the BBC has emphasised digital projects and infrastructure, such as

the build out of the digital terrestrial network, developing a satellite service, and

relocating to Manchester and Glasgow. The strategy paper points out that a larger

share of licence fee income has come to be used for digital projects and

infrastructure, and the “amount able to be used for the BBC’s primary purpose of

informing, educating and entertaining has been reduced in proportion.”7

3) With the culmination of digital switchover and the BBC’s geographical restructuring, it

is timely for the BBC’s strategy review to focus on content. Content is clearly a

priority for the licence fee payer: the BBC’s consumer research for this review found

that, amongst licence fee payers who valued the BBC highly, the top reason for

supporting the BBC was “great programmes and content”.8

4) Crucially, it is UK-made content, as opposed to imports, that is at the heart of

delivering public service broadcasting, and should be at the heart of the BBC’s

commitment to content. UK content represents, questions and, at its best, unites our

society in a way that imported programming never can. We welcome in particular the

strategy paper’s inclusion of “originality” and “building on British talent” as two of the

four characteristics by which it seeks to define the distinctiveness of BBC output. The

strategy paper’s emphasis that this entails a commitment to “original production

providing range and depth; fresh and new ideas,” and “focusing on content made for

the UK...and helping support UK creative industries across the country.”9

5) We see this commitment to UK content as absolutely consistent with – and indeed

fundamental to the delivery of – the BBC’s Public Purposes under the Charter,

notably:

7 BBC Strategy Review, Proposals, March 2010, page 32 8 Ibid, page 20 9 Ibid, page 24

BBC strategy review

7

• Sustaining citizenship (e.g. through UK-made news and factual content).

• Promoting educating and learning (e.g. through factual content that explores and

reflects diverse UK culture and history).

• Stimulating creativity and cultural excellence (e.g. stimulating creative growth and

the best UK talent by commissioning the best ideas on a meritocratic basis,

whether they come from in-house or external suppliers).

• Representing the UK (e.g. through a wide range of genres, drawn from creators

across the country, reflecting the diversity of UK culture and society).

• Bringing the UK to the world and the world to the UK (e.g. representing world

events them in a way that is accessible to UK audiences; supporting a UK content

sector that is globally competitive and able to exploit its programming

internationally).

• Delivering the benefits of digital technology (as part of this, high quality UK content

can help drive the take up of new services providing the appropriate rights to that

content are made available on a reasonable basis).

6) The importance of UK content in a public service context was also confirmed by

Ofcom’s consumer research for its recent Public Service Broadcasting Review, which

found that UK-made content was crucial to reflecting UK cultural identity and

representing diverse viewpoints.10

The market context for public service content

7) The strategy review’s commitment to high quality UK content is important at a time

when commercial sector broadcasters are reducing recent investment in home-grown

content. The review rightly notes this, stating that its commitment to content is, in part

at least, a response to certain market trends:

10 PSB Review Phase 1: The Digital Opportunity, Ofcom

BBC strategy review

8

“Perceptions of what the BBC should provide are clearly also shaped by what other

broadcasters supply. On television, advertising-funded broadcasters are under

greater pressure than ever, while subscription revenues to pay television – although

growing strongly – provide relatively little payback to the UK creative sector.”11

8) To put the BBC’s review into context, over the current Charter period, from 2005 to

the end of 2009, overall investment by the five main networks is likely to have

declined by over 16% in real terms, according to analysis by Oliver & Ohlbaum

Associates (O&O) for Pact. Across all broadcasters, O&O projects a £250m drop in

annual commissioning of new UK content between 2007 and 2009, as shown below.

Figure 1: Total network originations spend, 2005 to 2009 (real terms)*

26162572

24752435

2213

0

500

1000

1500

2000

2500

3000

2005 2006 2007 2008 2009E

£m– 2009 prices

Source: Oliver & Ohlbaum, Attentional, OFCOM Communications Report, PACT

*Figures are in real terms using 2009 prices; excludes regional spend; includes news & sport

9) This decline in investment in UK content is expected to increase, with Ofcom

forecasting that the annual funding gap could double by 2020, hitting £500m.12

10) The impact of such a fall in investment for original commissions is likely to be twofold.

Firstly, audiences are likely to experience reduced quality and range in programming,

with many broadcasters placing increased emphasis on cheaper genres and

11 BBC Strategy Review, Proposals, March 2010, page 24 12 Second Public Service Broadcasting Review, Phase 2: preparing for the Digital Future, Ofcom,

September 2008, page 5

BBC strategy review

9

imported content. Core public service genres are already under particular pressure.

ITV has already made widely-reported cuts in public service programme budgets

such as programming from the devolved nations and English regions. In some areas,

such as programming for school-age children, the BBC is already close to a

monopoly provider of first-run originations, and the quality and breadth of its output is

therefore all the more important.

11) Secondly, decreased commissioning in the domestic market may undermine the UK

creative content sector’s successful growth on a global level. In recent years, the UK

television content sector has been one of the success stories of the creative

industries, with an increase in overseas exports of UK television content of 39%

(external and in-house programmes).13 The success of the UK television content

sector in the global market is closely linked to the public service broadcasting system

in the UK – and the BBC in particular as the single biggest commissioner of UK

content. A BBC commission will typically represent only a portion of the production

budget, but it enables the producer to raise the remaining production funding through

exploiting IP rights in secondary and ancillary markets around the world. In this way,

the independent sector raises up to £190m per year in investment in the development

and production of UK content.14 In effect, therefore, BBC commissioning of domestic

content acts as seed capital for driving export growth.

12) Any significant reduction in overall levels of funding provided by public service

broadcasters - over and above that which can be absorbed by content producers

from rising secondary and ancillary rights revenue – would be likely to reduce the

competitive advantages of the UK content sector in the global market place. In the

current climate, the role of the BBC as an engine for the growth of the content sector

is likely to become increasingly important as original commissioning by broadcasters

in the commercial sector comes under more and more pressure.

13) There are already signs that the independent content sector is under pressure, with

producer margins remaining flat or falling as broadcasters decrease their payments

for programmes and production companies raise more of the production costs from

other sources. As we have noted, O&O is projecting a £250m drop in total new UK

content commissioning between 2007 and 2009. According to O&O, growth in rights

income will not be sufficient to make up for this loss in new content spend, with the

whole independent sector declining by £100m between 2007 and 2011 in real terms,

as shown below.

13 Annual export figures, TRP for Pact/UKTI, indicate that total television exports have risen by 39% since

2003. 14 Pact Census

BBC strategy review

10

Figure 2: Total TV revenues of UK independent sector (real terms), 2008 to 2011

15401395 1376 1343

109

115 121126

64

70 70 71

285

369 371 373

3932 31 30

2217 17 16

2,0601,998 1,986 1,960

0

500

1000

1500

2000

2008 2009 2010F 2011F

£m

OTHER INT’L

INCOME*

PRIMARY UK

COMMISSIONS

OTHER UK

PRE-PRODUCTION

UK RIGHTS INCOME*

INT’L SALES OF UK

FINISHED PROGRAMMES*

*Definitions: ‘Other international income’ - revenue from companies overseas operations and any primary commissions received from non-UK broadcasters; ‘Int’l sales of UK finished programmes’ - sales of first run UK programming sold as finished product abroad; ‘UK rights income’ – UK secondary sales, publishing, formats, DVD sales etc.; 2009 prices

Source: Oliver & Ohlbaum analysis, PACT census

75%

69%

14) We therefore broadly welcome the focus in the strategy review on UK content, in

particular the commitment by BBC Management to maintain a level of content

spending and, through allocating a set proportion of resources to content, a capping

of non-content spending. We also welcome the principle of reducing and capping

spending on foreign acquisitions as part of a focus on UK-made content that fulfils

public service values. In light of the market conditions that we have highlighted

above, the proposed focus on content is particularly relevant to the BBC’s fulfilment

of its Public Purpose under the Charter of stimulating creativity.

BBC strategy review

11

15) However, the BBC’s proposals do raise a number of issues that Pact requests the

Trust and Management consider and, if appropriate, address. These fall into the

following areas:

• Clarity over figures and definitions: Several headline proposals in the strategy

paper lack detail in key areas that risk potentially misleading industry and the

licence fee payer, and raise difficulties in measuring the implementation of the

proposals, and thereby holding BBC Management to account.

• Putting quality at the heart of commissioning: the BBC strategy proposals have

rightly considered how much and on which type of programming the BBC should

invest, but they do not look at whether the BBC’s commissioning framework

ensures it commissions programmes on a meritocratic and cost-efficient basis,

regardless of whether they originate in-house or externally. In-house currently

benefits from a 50% guarantee of all qualifying BBC commissions, plus BBC news,

despite the case for this guarantee being in our view fundamentally flawed, and

despite the fact that the guarantee increasingly risks distorting commissioning by

placing an artificial restraint on commissions that prevents them from

commissioning from independents after a set point, even if that means not

commissioning on a meritocratic basis.

• Online: the strategy paper does not consider the negative impact of proposed cuts

in online investment on the nascent online content sector, which is likely to

undermine the BBC’s fulfilment of its Public Purpose under the Charter of

stimulating creativity.

• Content priorities: The BBC strategy review has rightly indentified UK children’s

content as one of its five content priorities, but its proposals do not in our view

address this issue in a meaningful way. The proposal to increase investment in

children’s by £10m per year represents less than 2% of the total proposed content

re-prioritisation of £600m, and may not even replace declines in BBC investment in

children’s over recent years, let alone the market failure in the wider commercial

sector. In feature film, the BBC is required under the Charter Agreement to have “a

film strategy” in place, yet this is not addressed in the strategic review. The Trust is

in the final stages of a separate review of BBC Films’ strategy and, in being

mindful of BBC Charter requirements, this overarching strategy review should take

account of its findings.

16) We detail our concerns and proposals in this order in the subsequent sections.

BBC strategy review

12

BBC strategy review

13

Section 2: Clarity issues

1) As we have outlined in the preceding section, Pact welcomes in principle the BBC’s

commitment in the strategy proposals to prioritise funding for high quality UK content

that meets public service values. However, there are several areas of the BBC’s

proposals that lack clarity, making them potentially misleading for industry, and

indeed for the licence fee payer, and creating difficulties in measuring progress and

holding Management to account.

Commitment to original content

2) As we noted in the preceding section of this paper, we welcome the strategy review’s

inclusion of “originality” and “building on British talent” as two of the four ways of

defining BBC distinctiveness. The level of spending on first-run originations, as

opposed to repeats and imports, should therefore be an explicit part of the BBC’s

public commitment to spend 90% on content/distribution. We note that the BBC’s

commitment to broadcast a minimum level of original content under the Charter

Agreement is based on hours, not value.15

Definition of content and distribution

3) We are concerned that the BBC’s strategy paper does not offer a clear definition of

either content or distribution, despite these two being at the heart of key proposals.

Ofcom’s analysis of spending on content by broadcasters, based on figures supplied

by broadcasters including the BBC, excludes spending that is not directly part of the

programme production costs – such as costs for interstitials and promotions, support

and IT. We understand that the BBC does not do this. For example, in the BBC

Trust’s review of the service licence for its children’s channels, it presented a

“Breakdown of the expenditure of CBBC and CBeebies content.” Of the total spend of

£114.3m, around 15% went on areas not directly related to programme production.

£6.8m went on “presentation”, including interstitials, and £10.7m on “other costs”,

including support staff and IT.16

15 BBC Charter Agreement, Programming quotas for original productions, 49 (1) (a)

16 Review of children’s services and content, BBC Trust, February 2009, page 49

BBC strategy review

14

4) The different definitions of content used by Ofcom and the BBC have led to confusion

around BBC spending in children’s. According to Ofcom figures, BBC spending on

first-run originations of children’s programming fell by 20% from 2004 to 2008, from

£97m to £77m.17 Even factoring in the increase of £25m over three years (around

£8m per year) that the BBC announced last year would mean BBC spending on first-

run children’s originations had fallen substantially over this period, based on Ofcom’s

figures. Yet the BBC has stated in the media and to Pact that it has never spent more

on children’s programming, including first-run originations.

5) To be clear about the BBC’s spending on content, the BBC should provide figures

that are consistent with those of Ofcom (and thereby with the rest of the industry). For

the same reason, the BBC should also provide more details as to what will constitute

distribution spending.

Clarity on investment by content area

6) We call on the BBC to clarify what proportion of its content spending it proposes

investing in each of television, radio and online going forward. This would help

provide certainty to respective sectors, encouraging companies to develop their

businesses accordingly and invest on a strategic basis. This might be done via three-

year business plan commitments to industry.

Income, not expenditure

7) The BBC is proposing to benchmark spending on content/distribution against

expenditure rather than income. Total group income in 2008/09 was £4.6 billion,

while expenditure was more than £100m lower, at just under £4.5 billion.18 In addition

to the lack of clarity that this creates, we are concerned that pegging

content/distribution spending to expenditure would enable the BBC to reduce the

proportion of spending that is eligible for the 90% target without this being

immediately transparent. This could create uncertainly in measuring performance

going forward. To be clear to industry and the licence fee payer about the proportion

of BBC activities classified as content/distribution, and hold BBC Management to

account fully, the BBC’s target of 90% should be measured against income.

17 Public Service Broadcasting: Annual report 2009, Ofcom PSB report, July 2009, page 147

18 BBC annual report and accounts 2008/09

BBC strategy review

15

Comparing in-house and external value for money

8) The BBC’s accounting for production costs creates difficulties in monitoring and

demonstrating efficiency in commissioning. The BBC does not disclose programme-

by-programme costs for in-house commissions, meaning it can allocate backroom

and fixed costs for production staff to departmental budgets even though they may

not be directly involved in on-screen production. This means that it is impossible to

compare in-house production and external commissioning costs. The BBC should

make public the total cost of in-house and external commissions on a per hour basis.

BBC Worldwide dividends

9) We would welcome clarification as to whether the proposed 90% target for

content/distribution would include the annual dividends returned to the BBC by BBC

Worldwide. While BBC Worldwide’s investment in programmes at production stage

by definition goes on content, it is not clear where its annual dividend (£85m in

200919) is spent. This is income generated on the back of licence fee investment, as

the Trust acknowledged in its recent report on the BBC’s commercial operations,

which concluded: “We recognise the significant return for licence fee payers delivered

by BBC Worldwide on those assets which have been paid for from the licence fee.”20

BBC Worldwide expenditure

10) As a point of clarity, the BBC Trust should make public BBC spending on

content/distribution as a proportion of total group expenditure (or preferably income).

This would include BBC Worldwide expenditure (£799m in 200921). It is not justifiable

to argue that BBC Worldwide expenditure represents the cost of generating a

dividend and programme investment for the BBC and therefore should be excluded.

The dividend returned to the BBC represents only part of BBC Worldwide’s remit, as

set by the Trust. The 2009 review of BBC commercial operations by the Trust

strengthened BBC Worldwide’s focus on building an international brand for the BBC

and the UK creative industries, and on pursuing the Public Purpose of bringing the

UK to the rest of the world. This is not to say that such activity does not contribute to

the dividends returned to the BBC, but neither is it the only purpose or even

necessarily the most effective means of generating a dividend on BBC assets (which

might, for example, be best achieved by selling a BBC programme directly to a US

network, rather than broadcasting it on BBC America).

19 BBC Worldwide accounts

20 BBC Commercial Review, introduction to final report, BBC Trust 2009

21 BBC accounts

BBC strategy review

16

A clear strategy on imports

11) The BBC is proposing to cut its annual spend on imports of £100m by 20%, but has

not explained how it has reached this figure. We suggest that the majority of the

BBC’s spending on imports is on high profile, sought-after dramas and Hollywood

films. In acquiring US drama Harper’s Island last year, for example, the BBC outbid

Channel 4. In contrast, foreign films and drama such as The Wire or the original

Swedish-language Wallander have public service value but are relatively low cost.

We note also that imports achieved a very low rating in the BBC’s consumer research

for this review.22

12) In our view, given the current financial pressure on broadcasters in the commercial

sector, the BBC should only buy imports where there is a clear public service

rationale and where the BBC does not have to compete against the market to acquire

such content. To ensure this it should only buy overseas series after their first season

has aired in their domestic market, such as occurred with the BBC’s acquisition of

The Wire.

13) The BBC has historically said that it could not collude with other broadcasters to

distort the market, but a blanket policy of not acquiring series until their second

season would not constitute any such distortion. Indeed, there is a likelihood that the

BBC is currently driving up prices by entering into the market for imports in direct

competition with other UK broadcasters, raising concerns that the licence fee may be

distorting the market.

14) The BBC should seek to reduce spending on imports further. At the very least,

however, the BBC Trust should require BBC management to provide clear details as

to why it has set its proposed reduction in imports at just 20%. The Trust should also

seek to benchmark what the BBC spends on imports with comparable acquisitions by

UK broadcasters in the commercial sector, just as it requires BBC Worldwide to

benchmark programme prices for BBC in-house content against the wider market. In

addition, the BBC should compare and make public the cost per hour of its

originations compared to its acquisitions, in order to establish value for money. We

note that Channel 4 has been subject to similar scrutiny: analysis of the cost of

imports compared to original commissions was an integral part of LEK Consulting’s

financial review of Channel 4 for Ofcom.23

22 BBC Strategy Review, BBC Trust, March 2010, page 20

23 Financial Review of Channel 4, LEK Consulting for Ofcom

BBC strategy review

17

Summary of proposals regarding clarity

• We would welcome clarification of the time frame for achieving the target for

spending 90% on content/distribution.

• As part of a commitment to invest in content, the BBC should guarantee a level of

spending on first-run originations, as opposed to repeats and imports.

• The BBC should adopt a definition of content that is consistent with that of Ofcom

(and thereby with the rest of the industry). The BBC should also provide more

details as to what will constitute distribution spending.

• To provide clarity and security for the content sector, the BBC should break down

planned spending on content by television, radio and online.

• The BBC’s target of 90% should be measured against income.

• The BBC should make public the total cost of in-house and external commissions

on a per hour basis, as well as by service.

• The BBC should clarify whether dividends paid to the BBC by BBC Worldwide will

be included in its calculation of spending towards its proposed 90% target for

investment in content/distribution.

• The BBC Trust should make public BBC spending on content/distribution as a

proportion of total group expenditure (or preferably income). This would include

BBC Worldwide expenditure.

• The BBC should only buy imports where there is a clear public service rationale

and where the BBC does not have to compete against the market to acquire such

content. To ensure this it should only buy overseas series after their first season

has aired in their domestic market.

• The BBC Trust should require BBC Management to explain why it has set its

proposed reduction in imports at just 20%, and look to reduce spending on imports

further where appropriate.

BBC strategy review

18

• The Trust should benchmark what the BBC spends on imports with comparable

acquisitions by UK broadcasters in the commercial sector, and against BBC

originations.

Section 3: Putting quality first in commissioning

"[W]hat the WOCC has done is raise the

creative bar. Ultimately the real winners are the

audience”

Jana Bennett, BBC Vision, 2010

1) Pact broadly welcomes the BBC’s proposed commitment to high quality, UK-made

public service content as part of its strategy review. Yet, while the BBC rightly

considers the level of its investment in UK content, and in which genres it invests, the

strategy paper does not review how the BBC commissions – whether it is genuinely

commissioning the very best ideas, no matter where they come from, and whether it

is doing so on an efficient basis. This is crucial to delivering both creative quality and

value for money for the licence fee payer.

2) For several years, the BBC failed to demonstrably commission on a meritocratic

basis. The BBC’s vertical integration (ownership of both broadcast and in-house

production) skewed commissioning towards in-house production departments. This

was because the BBC needed to justify and manage its in-house production capacity,

and maintained a commissioning structure aligned to in-house production. As a

result, the BBC regularly failed to meet or exceed the statutory independent quota,

which requires that “not less than” 25% of qualifying television programmes be

commissioned from independent producers.24 As BBC director general Mark

Thompson told the House of Lords Select Committee during the last Charter review,

the 25% independent quota was regarded as ceiling, not a floor.25

3) In a purely commercial environment this might have been acceptable, even

desirable, but the undue marginalisation of external suppliers is not in the interests of

the licence fee payer, as it dampens creative competition, potentially restricts the

range and quality of ideas, and raises concerns over value for money from in-house

24 Communications Act 2003, 277 (1)

25 House of Lords Select Committee on the BBC Charter Review, First Report, Section 254

BBC strategy review

19

suppliers. As Mr Thompson also noted to the Lords Select Committee: "It is in the

interests of the licence payer that investment should go to the best ideas and the best

talent."26

The WOCC’s success in affecting “a real shift in culture”

4) In recent years, the introduction of the Window of Creative Competition (WOCC) has

been arguably the biggest shift in how the BBC approaches commissioning. As 25%

of qualifying commissioning, the WOCC represents in total around £200m in

commissioning by value. In its first full year (2007/08), external suppliers (including

non qualifying independents) achieved their biggest share ever of BBC commissions,

winning three quarters of the WOCC and 43% of qualifying BBC hours overall. In

year two (2008/09) – the latest available – the external supply sector maintained this

overall level.

5) In initial assessments, the new system was judged to be successfully encouraging

the BBC to commission the best ideas regardless of whether they came from external

or in-house producers. The first biennial review of the WOCC, carried out by the BBC

Trust in July 2008, found on the whole that the WOCC had done much to encourage

a meritocracy in commissioning. A report by PricewaterhouseCoopers (PWC) for the

Trust stated that:

“In general the procedures and structures in place suggest that ideas from

independents and in-house commissioners are treated equally. Commissioners have

clear incentives to pick the best ideas, no matter where they came from. In general

we detected no obvious bias towards accepting in-house ideas over independent

ones or vice-versa.”

6) The Trust’s final report endorsed PWC’s overall finding, stating that the new system

had started to affect a real change in BBC commissioning:

“The introduction of the WOCC and the associated structural and staffing changes

has been a significant step for the BBC and the evidence from this first biennial

review suggests that a real shift in culture is being achieved.”

26 Mark Thompson oral evidence to House of Lords Select Committee on the BBC Charter Review, First

Report, Section 255

BBC strategy review

20

7) We note that PWC’s report found that, although adapting to the new system may not

have been easy, the WOCC had improved performance amongst in-house producers

by exposing them to increased competition. PWC noted increased performance and

a new focus on efficiency at in-house production departments:

“The introduction of the WOCC has been a spur to in-house producers...We noted in

our interviews that in-house producers were focusing not only on innovation and

quality, but also on costs and overheads. These are encouraging signs.”27

8) Commenting on the second year of the WOCC, Jana Bennett, Director, BBC Vision,

said: "[W]hat the WOCC has done is raise the creative bar. Ultimately the real

winners are the audience – who benefit from the increase in creativity and quality that

this drives. You only have to look at the range and distinctiveness of our output over

the last year from both in-house and independents to see evidence of this heightened

creativity."28

The flawed case for the in-house guarantee

9) Although the WOCC has led to increased creative competition within 25% of

qualifying BBC commissions, by far the biggest proportion of BBC commissions is

now guaranteed to in-house production, which has a 50% guarantee for qualifying

commissions and, in addition to this, provides all BBC news. It is important to bear in

mind that the in-house guarantee, put in place at the same time as the WOCC,

effectively caps potential commissions from external suppliers at 50% (the total of the

independent quota and WOCC combined). Previously, although independents won

little more than the minimum 25% quota in practice, they could in theory have won

100% of BBC commissions.

10) In the five years since the WOCC was designed (it was launched in the last Charter

but conceived prior to that), the external supply sector has grown in scale

significantly, with annual turnover increasing by 40%.29 Over the same period,

commissioning of UK content by commercial broadcasters has declined. Competition

amongst external suppliers for commissions from the BBC, the only stable source of

investment for UK programming over this period, has therefore intensified. This

raises the risk of the in-house guarantee distorting commissioning decisions in favour

27 The Operation of the Window of Creative Competition (WOCC): First Biennial Review, BBC Trust, page

11 28 BBC press release, Monday 10 May 2010, “BBC WOCC continues to stimulate creative competition

between in-house production and the independent sector in 2008/09” 29 Pact Census

BBC strategy review

21

of in-house production departments by placing an artificial restraint on

commissioners’ ability to commission from external suppliers – thereby potentially

restricting commissioners’ ability to commission the best ideas regardless of where

they come from.

11) In 2004/05, when the levels of the in-house guarantee and the WOCC were planned,

the BBC’s position, as set out in the Tipping Point Analysis carried out as part of the

BBC’s Content Supply Review in 2004/05, was:

• Only BBC in-house production could guarantee a pipeline of content, particularly in

core PSB genres and programming from the devolved nations and regions.

• Only BBC in-house could deliver its high level of training.

• BBC in-house needed a guaranteed critical mass of 50% (plus news) to ensure

economies of scale, manage costs, retain talent and guarantee a flow of strong

ideas.

• BBC in-house was vital to supply the BBC with the IP rights it needed for

innovative new services in the digital era.

• BBC in-house internalised profit margins and recycled the resulting investment into

programmes.

12) If such arguments were ever well founded, the significant developments in the

market over the last five years at the very least raise serious questions over the in-

house guarantee. We examine each of the justifications for the in-house guarantee

below, then look at concerns that growth in the external supply sector has led to the

risk of the in-house guarantee now distorting commissioning by placing an artificial

restraint on commissioners.

“Only BBC in-house production could guarantee a pipeline of content”

13) BBC in-house clearly does not have a monopoly on PSB programming. The

independent sector consists of hundreds of companies, based across the UK,

offering a variety of view points and specialisms. Many of the BBC’s most acclaimed

productions, in a rich mix of genres, come from the independent sector, including Life

On Mars, Britain From Above, Question Time, Who Do You Think You Are?,

Himalaya With Michael Palin, and Wallace & Gromit. The independent sector has

successfully supplied publisher-broadcaster Channel 4 with a distinctive mix of

innovative content, and regularly dominates awards for content made for a wide

variety of broadcasters, feature film, and online. At the last television Bafta awards,

BBC strategy review

22

external producers won 17 out of 20 awards. Slumdog Millionaire, produced by

Celador for Film4, won eight Academy Awards last year, while Pact members won

two out of three international digital Emmys, the digital industry’s equivalent to the

Oscars.

14) In the run up to launching the in-house guarantee/WOCC, the BBC commissioned

the Work Foundation to analyse the creative role of in-house production.30 The report

identified two approaches to fostering creative excellence in programming: an

environment of competition for commissions, as created within the WOCC; and the

relative stability of in-house, where programme-makers could take risks and develop

ideas over a period of years without the pressure of a commercial environment.

15) Pact accepts that different talent responds to different environments, and a longer

term approach is important for some genres or programmes. Yet we reject the

assertion that maintaining an in-house guarantee is the only way, or even the best

way, to achieve this. Many independent producers have well established track

records in producing high quality current affairs content and documentaries, such as

Wall To Wall, Mentorn, Lion, and Darlow Smithson. Many of these belong to large

commercial groups with shareholders, but nevertheless are acutely conscious that

their reputation is vital to winning future commissions (and thereby generating future

revenues). In fact, the scale of such groups can mean they are less reliant on the

success of a single programme idea, as their revenue streams will be based on a

portfolio of commissions across multiple programmes, genres, and broadcasters.

16) Another BBC-funded report, From the Cottage to the City: the Evolution of the

Independent Production Sector, argued that larger independent producers are not

interested in making public service programming. Larger companies will of course

seek to work in genres where margins are potentially higher, but to suggest that this

necessarily excludes public service genres is a simplification not borne out by market

reality. For example, the last tendering process for Question Time saw an array of

larger independent companies compete against each other in what is a core public

service genre. The list of 15 bidders included such “super indies” as Lion TV (part of

the All3Media Group), Cheetah TV (Endemol), Ten Alps, Mentorn (Tinopolis), and

Tiger Aspect (IMG), along with smaller companies.

17) The key to the competition around Question Time is that the commission covered

three years. Companies are able to develop their businesses strategically around

such a commission, investing in talent and creating related content such as

documentaries. In this context, current affairs can be a perfectly viable business

30 The Tipping Point: How Much Is Broadcast Creativity At Risk?, The Work Foundation for the BBC

BBC strategy review

23

opportunity for a larger company. Indeed, preparing a proposal as part of the

tendering process for Question Time cost a significant sum, particularly as part of the

final shortlist. Companies were willing to invest risk capital in an effort to win this

tender.

18) Although it may have been commissioned under the independent quota rather than

the WOCC, Question Time also illustrates the creative benefits of opening up

commissioning to a wider range of suppliers. To win the commission companies had

to compete with each other creatively, as well as financially, to deliver the most

innovative and compelling proposal. George Entwistle, the BBC's then head of

current affairs, said of the tendering process for Question Time:

“It was a very tough and rigorous selection process. All four shortlisted companies

came up with strong proposals both for the linear programme and for developing

multi-platform offerings.”31

19) If the BBC is concerned that larger suppliers are not keen to compete for public

service commissions, the BBC should consider longer term contracts and tenders

across different genres. The external supply sector has evolved and it is far

preferable for the BBC to evolve with it rather than use a rigid approach that

dampens competition to provide the best content for the licence fee payer.

20) We note that S4C recently awarded longer term contracts in another core public

service genre, children’s. S4C this month announced that it had awarded two

independents contracts worth more than £7m to produce children’s content over the

next three years.

21) A key factor in ensuring a flow of public service content – and one that historically

has been all but ignored in the BBC’s justification for the in-house guarantee - is that

BBC commissioners should be the most important element in the process of bringing

an idea to the screen, not in-house producers. The BBC should ensure

commissioners are empowered with a clear remit, coupled with a flexible approach

towards the types of contracts they award. Independents will seek to offer a

commissioner what the commissioner wants. Winning commissions is the life blood

of independents – everything else in the business model of an independent company

flows from the initial commission.

“An in-house guarantee ensures Out of London programming”

31 George Entwistle, the BBC's then head of current affairs, on the tendering process for Question Time,

MediaGuardian, March 8 2007

BBC strategy review

24

22) The BBC’s original justification for the 50% guarantee argued that in-house

production is vital to ensuring a sufficient flow of Out of London programming. Yet

there is evidence that the external supply sector outside London has spare capacity.

From a high in 2006, network hours produced by Out of London independents

dropped by 17% in 2007, the latest available year.32 This appears to be mostly due to

declines in Out of London commissioning by ITV. We note that Out of London

producers can excel in public service genres – 81% of commissions from

independent production companies in Scotland are in factual, for example.33

23) We also note that the WOCC is open to external companies that do not qualify as

independents, such as STV in Scotland.

24) In addition, commissioning from Out of London external suppliers delivers benefits

that cannot be achieved through in-house. Companies that secure BBC commissions

are able to build their expertise and infrastructure, helping them win commissions

from other broadcasters. Channel 4 has, for example, publicly called on the BBC to

commission more from external producers in the developed nations and regions in

order to help build the supply base so it can raise its own Out of London

commissioning from 30% to 35%.

“BBC in-house is vital to delivering high quality training”

25) The BBC’s annual investment in training of around £40m from the licence fee is

valuable and can and should be safeguarded regardless of the scale of in-house

production at the BBC. We see no reason why this investment could not be spent on

training initiatives delivered through the external supply sector rather than in-house.

Indeed, this is already the case for some BBC training, and exclusively the case for

Channel 4’s production training programmes, such as its research schemes (which

are match-funded by companies in the independent sector). Indeed, it is possible that

developing and running such training in closer partnership with the external supply

sector could make BBC training more relevant to the wider market.

26) The BBC-commissioned Tipping Point report also argues that companies in the

external supply sector need to recruit former BBC staff as they supposedly do not

have the skills themselves to make high quality public service content. It might just as

32 Pact’s latest Production Trend Report (November 2008) found that total network hours commissioned

from independent companies in 2006 amounted to 3,811, but fell to 3,152 in 2007. 33 Survey of Television Production Scotland 2006, Ekos for Scottish Enterprise and the Scottish

Broadcasting Commission, January 2008, page 12

BBC strategy review

25

well be argued, however, that such recruitment practices are testimony to the BBC’s

tendency to commission from “familiar faces”, a practice which the WOCC was aimed

at changing.

“BBC in-house is necessary to managing costs”

27) In-house production clearly does not guarantee that costs will be contained. We note

the recent reports by the Public Affairs Committee and the National Audit Office

concerning costs associated with BBC in-house’s production of sports and music

events, along with BBC overspending on major buildings. The Culture Select

Committee has also recently criticised BBC in-house for talent payments.

28) At the time of the last Charter, the BBC argued that any advantage in external

suppliers being more cost efficient was offset by the need to factor in profit margins

for commissions in the external supply sector. At the time of the Charter profit

margins in the independent sector had indeed experienced an initial surge following

the introduction of the Terms of Trade in 2004. As the sector has grown, however,

profit margins have remained flat, or declined amongst some companies, as shown

below. Figure 3: Independent sector profitability, aggregated and by turnover band

7.0%

8.4%

9.3%

8.0%

8.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2004 (2005 Census)

2006 (2007 Census)

2007(2007/2008

Census)

2008(2010 Census -

restated)

2009 (2010 Census -

restated)

%

Source: Oliver & Ohlbaum analysis, PACT census

2.2%

5.5%

3.6%

5.4%

4.9%

9.9%

(1.2%)

3.7%

6.1%

3.3%

5.6%

11.0%

-2%

0%

2%

4%

6%

8%

10%

12%

less than £1m 1-5m 5-10m 10-25m 25-70m 70m+

%

2008

2009

BBC strategy review

26

29) Arguments in favour of high levels of BBC in-house production in order to internalise

profits are misguided, as the UK television content sector has built its global success

on being incentivised to and effective at selling IP rights in order to raise investment

that can be re-invested back into UK programme budgets, reducing the price to the

broadcaster, as we will detail later.

30) Reports commissioned by the BBC during the Charter review raised concerns that it

would increasingly be at the mercy of larger independents when negotiating terms.

We reject this is in principle: for the most part the UK networks are sufficiently

differentiated in their mood, demographic focus and genre mix to avoid head to head

competition for individual programmes. The limited competition between buyers

combined with any specific project’s dependency on the initial commission for

financing gives leading commissioners such as the BBC significant power.

31) Although the independent sector has grown substantially in the five years since the

Charter, this has not translated into market power. For this to have occurred, we

would expect to see one or both of two factors occurring:

• The share of independent commissions from the five main networks, as opposed

to commissions won from digital channels, would have had to decrease

significantly; and/or

• The share of commissions from one broadcaster won by any individual company

would have had to have increased substantially.

BBC strategy review

27

32) Analysis of market power in the content supply sector commissioned by Pact from

O&O indicates that, five years into the Charter, the five main PSB networks and their

spin-off channels still account for over 90% of commissioning, as illustrated below.

Figure 4: Share of originations spend by networks, spin offs and thematics, 2005-2007*

84% 85% 84%

11% 10% 11%

4% 5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007

% OF TOTAL ORIGINATIONS SPEND

*Excludes regional spend; includes news and sport spend **Includes GMTV and excludes S4CSource: Oliver & Ohlbaum Analysis

33) Nor is there any evidence that any single independent producer has achieved

sufficient market share to exert significant influence in the negotiating process. In

contrast to continued buyer power in the commissioning market, only one external

supplier to the main network channels accounted for more than 20% of their

commissioned output (excluding sport and news) in 2008 (for Channel 4) – a

situation that has remained largely unchanged over the last three years despite

independent sector consolidation, as shown overleaf.

BBC strategy review

28

Figure 5: Top three independent suppliers by broadcaster, 2008*

8% 5% 4%

27%

19%3% 5%4%

14%

4%

3% 2%2%

6%

3%23%19%

28%

42%

65%

62%

61%

57%

6%

2%7%

4%

11%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

BBC1 BBC2 ITV C4 FIVE

% OF ALL ORIGINATED OUTPUT HOURS

*Excludes news and sportSource: Oliver & Ohlbaum, Attentional, BARB

34) O&O’s analysis found that primary commission prices paid by broadcasters across

the sector were largely flat in nominal terms.34 Furthermore, a significant sign that

broadcasters still enjoy significant bargaining leverage can be seen by their ability to

push through primary price reductions over the last 12 months, as shown by O&O’s

Policy Survey of independent producers for Pact. The figure overleaf shows the

extent of this reduction over the last 12 months.

34 The Economics of UK content supply, May 2009, O&O for Pact

BBC strategy review

29

Figure 6: Response to Q: How have primary prices per hour changed in 2009/10 compared with 2008/09?

1%

0%

0%

0%

0%

3%

2%

1%

30%

34%

35%

56%

35%

28%

36%

20%

34%

35%

27%

23%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

% of all respondents who have received a UK commission

Increase of 10% Increase of 5% No change Decrease of 5% Decrease of 10%

Source: Oliver & Ohlbaum analysis, PACT policy survey Q15

WEIGHTED AVERAGE

DECREASE/INCREASE

2009/10: (4.4)%

2008/09: (4.8)%

2008/09: (3.2)%08/09

09/10

08/09

09/10

RETURNING

STRANDS

NEW

STRANDS

2009/10: (5.1)%

+20%

+6%

35) Instead of the growth of the production sector over the least five years leading to

price inflation for the BBC, the opposite seems to have occurred, with increasingly-

well capitalised companies in the external supply sector able to take on risk by part

funding production themselves, so offering broadcasters price flexibility. Independent

producers are investing a total contribution of £190m directly into the upfront creation

of UK programming35 – more than the comparable figure from BBC Worldwide.

36) We also note analysis by PKF for the DCMS during the last licence fee settlement

process which suggested that, far from increasing prices for the BBC, the emergence

of larger companies in the independent sector might generate cost efficiencies that,

in a competitive market for commissions, could be passed onto the BBC, and

ultimately to the licence fee payer in terms of value for money. PKF stated that:

“Taken together this may offer the opportunity to reduce costs.”36

35 Pact Census

36 Review of the BBC Value for Money and Efficiency Programmes, PKF for DCMS, April 2006, page 20

BBC strategy review

30

37) PKF’s conclusions challenged BBC Management’s argument that independent

commissions were more expensive, questioning whether examples put forward by

Management were like for like. PKF concluded that prices at other broadcasters

indicated that independents could produce programming at relatively low costs:

“[W]hat the data for broadcasters B and C suggest is that it may be possible to

commission relatively low cost independently produced programmes for most

genres.”37

“Only in-house can provide the BBC with the necessary rights”

38) In terms of the BBC’s strategic need for rights in order to launch innovative new

services, Pact and the BBC have been able to promptly negotiate an agreement

under the Terms of Trade that allows the BBC to retain the rights it needs in such

cases. On the iPlayer, for example, the BBC was able to secure on-demand rights to

independent productions at no additional upfront cost.

39) Nor is it the case that not having 100% of IP rights when commissioning

independents has led to any increased cost for the BBC. As we have noted above,

independents use their IP rights to raise investment to help fund programme

production, with the result that broadcasters including the BBC have been able to pay

only for those rights they require. The Digital Britain review concluded that costs per

hour to broadcasters of commissioning had dropped by 25% as a result.38

40) The question of rights does, however, raise the question of what the BBC should be

expected to deliver to the licence fee payer – this applies equally to programmes

made in-house and externally. In the digital era, funding for creating UK content has

inevitably become more fragmented, with producers (in-house and external) seeking

investment from a variety of sources to raise the production budget, a process which

will often involve selling off rights. The result is that the licence fee payer is no longer

paying 100% of the production costs – this creates value for money in enabling the

BBC to secure programming at a lower price, but raises difficulties if the BBC is

expected to make that content available across all potential outlets in the digital era.

The licence fee payer cannot as a rule expect all rights if the BBC is not meeting

100% of production costs. This does not mean that the BBC should not be universally

available via certain key services – it may just not be available via every service.

37 Review of the BBC Value for Money and Efficiency Programmes, PKF for DCMS, April 2006, page 76

38 Digital Britain, final report

BBC strategy review

31

“In-house production protects future supply of content”

41) We have already outlined our views and analysis as to why we consider that BBC in-

house does not have a monopoly on creating high quality public service content, or

value for money. The BBC’s argument that it requires a critical mass of 50% in-house

production in order to retain talent and an efficient infrastructure is in our view

unfounded - and sets the in-house guarantee at an arbitrary level. BBC in-house is by

far the UK’s largest television content producer. BBC in-house production accounts

for approximately 34% of all original commissions in the UK, with its nearest

competitor, ITV Studios, on 12%. The BBC is therefore arguing that it needs to

maintain a guaranteed level of production that is significantly more than twice the

scale of its nearest rival, as show below.

Figure 7: Estimated share of total UK first-run TV commissioning spend by producer*, 2007

34%

12%

4% 4%3% 3% 3% 3%

2% 1% 1% 1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Percent

Source: OFCOM Communications Report, ITV, Oliver & Ohlbaum Analysis

*Fremantle data not available

BBC strategy review

32

Risks associated with the in-house guarantee

42) In addition to the case for an in-house guarantee being in our view fundamentally

flawed, there is also evidence that the current in-house guarantee carries certain

significant risks, potentially:

• Distorting commissioning by preventing BBC commissioners from commissioning

the best ideas regardless of their origin.

• Distorting competition between external and in-house producers by enabling in-

house to cover fixed costs through the guarantee and win commissions through

the WOCC on a marginal cost only basis, driving down prices for independent

commissions on an undue basis.

• Restricting the growth and economic spillover benefits of the UK creative content

sector by guaranteeing the single largest share of commissioning investment to in-

house, despite a lack of analysis of the economic benefits of commissioning in-

house, compared to externally.

• Risking reducing audience choice through the continued incentive created by

vertical integration of restricting the availability of content on third-party services in

order to protect existing BBC services.

43) We deal with these issues in more detail below.

The risk of distorting commissioning

44) In certain genres, BBC spending with external suppliers is already approaching or

exceeding 50%, suggesting the in-house guarantee is placing an artificial constraint

on external commissions and preventing commissioners from commissioning the

best ideas regardless of their source.39

39 The statutory level of the in-house guarantee – set at 50% in the Charter Agreement – applies only in

aggregate, averaged across all genres, leaving the BBC free to set levels of external and internal commissions in each genre. External suppliers win around three quarters of commissions in the WOCC, but over 50% in many individual genres. This is counter balanced by the BBC setting a relatively high guarantee for in-house in other genres, ensuring that the overall 50% in-house guarantee is achieved.

BBC strategy review

33

45) This is the situation that PWC warned against in its initial report on the in-house

guarantee/WOCC for the BBC Trust. PWC expressed concerns about the in-house

guarantee eventually distorting commissioning decisions as the independent sector

grew, stating: “At some point in the future the continued growth in independent

production may be capped by the in-house guarantee set at the individual genre and

sub-genre level. There is a risk that changes to the in-house guarantee at these

levels may not be consistent with the principle of ideas being commissioned on merit,

whatever the source.”40

46) In the five years since the WOCC was conceived, the market has changed

dramatically in two relevant ways. Firstly, the capacity of the external supply sector

has grown substantially, due to growth spurred by the Terms of Trade that resulted

from the 2003 Communications Act and, since 2007, increased commissioning from

the BBC under the WOCC. Sector turnover has grown by 40% since 2004, as shown

below.

Figure 8: Independent producer revenues by TV and non-TV activities, 2004 to 2009

1,492

1,753 1,894

2,016 1,999

105

199

242 175 225

1,597

1,952

2,136 2,190 2,223

-

500

1,000

1,500

2,000

2,500

2004 (2005 Census)

2006 (2007 Census)

2007(2007/2008 Census)

2008(2010 Census - restated)

2009 (2010 Census - restated)

£m

Source: Oliver & Ohlbaum analysis, PACT census

NON TV-REVENUE

TV REVENUE

28.8%

12.7%

CAGR

2004 - 07 2008- 09

15.7% 1.5%

51.8%

(0.8%)

REVISED METHODOLOGY

40 BBC Window of Creative Competition, Report for the BBC Trust, July 2008, PWC, page 2

BBC strategy review

34

47) Secondly, commissioning of UK content from broadcasters in the commercial sector

has fallen, due to fragmenting advertising revenues and an advertising downturn. As

we have noted, annual commissioning of new UK content is expected to have

dropped by £250m since 2007.41

48) These factors have led to a situation where there is increased capacity on the supply

side, but shrinking demand. As a result, competition has increased for BBC

commissions, a relatively stable and sizable source of commissions in an otherwise

decreasing market. In older children’s content, for example, the BBC has become an

almost monopoly buyer, and external suppliers have won markedly high levels of

children’s commissions under the WOCC, at times exceeding 50% of overall BBC

commissions.

49) There is now in Pact’s view a risk that the in-house guarantee is distorting

commissioning decisions by placing an artificial limit on the amount of external

content commissioned by the BBC. Were this to be the case, the BBC would not

necessarily be commissioning the best ideas on a meritocratic basis across its entire

output.

50) The issue of whether the BBC is genuinely commissioning the best ideas is in

addition to concerns that maintaining an in-house guarantee distorts competition

between the BBC in-house and individual external suppliers. The 50% guarantee

enables BBC in-house to cover fixed costs from the guarantee and charge for

commissions won under the WOCC on a marginal cost only basis, forcing down

prices for commissions from the independent sector on an undue basis.

Risk to UK creativity

51) In recent years, core investment in UK content by UK public service broadcasters

has been coupled with the emergence of entrepreneurial independent production

businesses of some scale. As we have illustrated, independent production sector

turnover has increased by 40% since 2004, as we have noted. This growth has been

founded on investment in the form of the primary licence fee from broadcasters, but

increasingly independents have leveraged this initial investment to generate further

sales. Such secondary sales, for example from exports, now account for around a

third of sector turnover.42 Export growth has created a virtuous circle, enabling

41 O&O for Pact

42 Pact Census

BBC strategy review

35

independents to raise investment from international sales for the creation of UK

content. As we have outlined, independents now raise around £190m in investment

for UK television programming through a variety of means.43

52) As we have mentioned, the BBC has helped foster this growth, and Deloitte’s report

for the BBC as part of this review confirms the substantial positive impact that BBC

investment through commissioning has had on the independent sector. In

considering the case for an in-house guarantee the BBC should look at whether

commissioning in-house delivers the same spillover benefits as commissioning from

external suppliers. We note that the Deloitte report detailed at length the BBC’s

positive impact on the wider economy through its investment in the independent

sector and corresponding spillover benefits, but made no reference to in-house

production (other than the preface) and its comparative spillover benefits.

53) For example, as we have mentioned, commissioning from Out of London external

suppliers delivers benefits that cannot be achieved through in-house. Companies that

secure BBC commissions are able to build their expertise and infrastructure, helping

them win commissions from other broadcasters. Channel 4 has, for example, publicly

called on the BBC to commission more from external producers in the devolved

nations and regions in order to help build the supply base so it can raise its own Out

of London commissioning from 30% to 35%.

Danger of reducing audience choice

54) Analysis commissioned by Pact from Oliver & Ohlbaum last year indicated that the

risks inherent to vertical integration - where corporate groups combine broadcast and

production – are likely to become more pronounced in the digital era. As

broadcasters face increasing competition for audiences through digital television and

the growth in on-demand delivery, the incentive increases to slow, stop or, perhaps,

skew the nature of competition they might face on these new platforms through either

commissioning in-house (and therefore owning all rights) or any control of the

secondary and ancillary rights to their commissioned programming.

55) It is worth noting that the BBC, despite its public service remit and launch of new

services such as then iPlayer, still requires that it retain exclusive use of on-demand

rights for multiple years on popular shows (through holdbacks on returning series)

43 Ibid

BBC strategy review

36

when commissioning from independent producers, preventing third-party services

from making that content available even alongside BBC services.

56) Furthermore, broadcasters with significant in-house production activities such as the

BBC have an added incentive to squeeze independent producer Terms of Trade

and/or divert key programming to their own in–house activities in order to both

weaken the independent sector as a whole (and its appeal to top off screen and on

screen talent) and to secure key secondary and ancillary rights to all programming –

in-house and independent – to slow down competition on new platforms.

57) While commercial broadcasters will see rights control as a way of retaining influence

over new platform and revenue models, the BBC will see it as a way of guaranteeing

reach in a more fragmented environment, even though this may entail restricting the

availability of content on alternative services.

Summary of proposals for ensuring meritocratic commissioning

• The BBC Trust and Management should review whether current commissioning

structures are optimal on a strategic basis, with a view to removing the in-house

guarantee or setting it an appropriate level as soon as possible.

• As part of this review, and in light of significant market developments, BBC

Management should demonstrate publicly why the in-house guarantee should be

maintained and at what level, in order to show that BBC commissioning is

delivering value for money in and commissioning the highest quality programmes

on their merits across all of its output.

Section 4: the BBC’s impact online

1) The BBC’s proposed cut of 25% to online spending is in Pact’s view misguided. A

spending cut alone does not deliver the BBC’s stated goals of efficiency or a tighter

remit. Instead, it is likely to damage the BBC’s fulfilment of its Public Purpose under

the Charter of fostering creativity, in terms of the BBC’s investment in the nascent

digital production sector.

2) In Pact’s view the best ways to achieve the BBC’s goals are through a clear and well

enforced remit for online, and, in terms of efficiency in commissioning, greater

transparency and competition.

3) Indeed, it is a key concern for Pact that the Trust and Management address

longstanding problems in online commissioning, which has for several years treated

the 25% quota for external suppliers as a ceiling rather than a floor, as occurred in

television prior to the WOCC. We urge the BBC to ensure meritocratic commissioning

in online, both as a way of delivering value for money for the licence fee payer and

ensuring that the best content is provided to the public. In addition, opening up

commissioning would be expected to help stimulate growth in the external supply

sector, potentially offsetting the negative impact on the sector from the 25% cut.

Ensuring meritocratic commissioning online

“Healthy and fair competition and a diverse supply base

encourage excellence as well as improved value for

money. Using external suppliers also provides positive

externalities for a healthy and vibrant UK production

sector.”

BBC Management, 2007

4) As the Trust is aware, the Graf review called for an online quota for external

commissioning that stimulated genuine creative diversity in content. Graf stated that:

“A higher level of contribution from external suppliers will promote the diversity,

plurality and quality of content offered by BBC Online, and will help drive innovation

BBC strategy review

38

and creativity, much as it has done in the TV sector.” 44 In their response, the BBC

Governors confirmed the BBC’s commitment to “the development of the wider new

media production sector.”

5) The new service licence for bbc.co.uk confirms the BBC’s role in stimulating the

digital production sector, requiring BBC online to “make an important contribution

to”45 the BBC’s Public Purpose under the Charter of stimulating UK culture and

creativity. We note, however, that the BBC Trust’s service licence review concluded

that bbc.co.uk was under performing in this area compared to delivery on other

Public Purposes. The Trust stated that: “bbc.co.uk’s contribution to the culture and

creativity purpose is weaker than its contribution to the other purposes.”46

6) This is a missed opportunity. Clearly the BBC must be mindful not to have a negative

market impact, but equally it has perhaps unrivalled potential to encourage growth,

innovation and creativity in the UK’s new media sector. As a source of investment in

online content, the BBC is second only to government and local authorities. bbc.co.uk

is the UK’s biggest content-based website,47 while the BBC is the only UK company

amongst the top 20 new media players in the UK, providing “a vital foothold for UK

content on the internet.”48

7) A key way of unlocking this potential is through a genuinely meritocratic and

competitive commissioning policy, open equally to in-house and external suppliers. A

meritocratic commissioning process delivers two benefits: