p e r f o r m a n c e r e p o r t first quarter ended 30 june 2011€¦ · ·...

TRANSCRIPT

WP

PL

P E R F O R M A N C E R E P O R T

First Quarter Ended30 June 2011

Celebrating 25 years 1986-2011

Garments

END T

O EN

D SO

LUTIO

NS A

CROSS T

HE V

ALU

E CH

AIN

To be the world's best integrated textile solutions enterprise with leadership position across products and markets, exce e d i n g c u s to m e r & s t a ke h o l d e r ex p e c t a t i o n s . The barometer of our success would be reflected by our ROCE

WE WILL:

ØMaximize people development initiatives

ØOptimize use of all resources

ØBecome a process driven organization

ØExceed compliance and global quality standards

ØActively explore potential market & products

ØOffer innovative, customized and value added services to our customers

ØBe a knowledge leader & an innovator in our businesses

ØBe an ethical, transparent and responsible global organization

Alok Mission

Alok Vision

Celebrating 25 Years 1986-2011

"Alok is an 'end-to-end' provider of Integrated Textile Solutions, with five core divisions: Cotton Yarn, Apparel Fabric, Home Textiles, Garments and Polyester Yarn

Alok's State of the Art Integrated Textile Facilities

Spinning

Processing

Knitting

Quilting Schiffli Embroidery

Madep-ups

Multi Head Embroidery

Weaving

Yarn Dyeing

Printing

Processing

1TM Integrated Textile Solutions

PERFORMANCE HIGHLIGHTS

BUSINESS HIGHLIGHTS: FOR THE QUARTER ENDED 30 JUNE 2011

Sales at Rs. 1,644.89 crore

An increase of 49.68% over quarter ended 30 June 2010 (Rs. 1,098.97 crore)

Exports at Rs. 602.19 crore

Compared to Rs. 435.85 crore during Q1 2010-11: a growth of 38.16%

EBIDTA at Rs. 452.92 crore

Growth of 38.57% over corresponding quarter in 2010-11 (Rs. 326.85 crore)

PAT at Rs. 57.77 crore

An increase of 24.21% over Q1 2010-11 (Rs.46.51 crore)

2 Celebrating 25 Years 1986-2011

(Rs. Crore)

PARTICULARS 1ST QUARTER ENDED YEAR ENDED30.06.2011 [3 months]

(Provisional)

30.06.2010 [3 months]

(Provisional)

31.03.2011 [12 months]

(Audited)

1. Net Sales / Income from operations 1,644.89 1,098.97 6,388.442. Other Income 0.70 0.05 6.423. Total Income 1,645.59 1,099.02 6,394.864. Total Expenditure 1,192.67 772.17 4,638.91a] (Increase) / Decrease in Stock in trade and work in

progress(284.66) (104.34) (216.23)

b] Consumption of raw material 1,090.69 617.36 3,567.36c] Employee Cost 54.96 41.60 199.75d] Other Expenditure 331.68 217.55 1,087.63 Profit Before Interest & Depreciation 452.92 326.85 1,756.355. Depreciation 164.97 99.32 518.796. Interest 200.44 157.08 654.377. Profit from ordinary activities Before Tax 87.51 70.45 583.198. Provision for Tax – Current 17.50 14.37 120.40 – MAT Credit 0.00 0.00 (42.25) – Deferred 12.24 9.57 100.68 Net Profit from ordinary activities after Tax 57.77 46.51 404.379. Extra ordinary items (Net of tax) 0.00 0.00 0.00

10. Net Profit for the period 57.77 46.51 404.3711. Paid up Equity Share Capital

(Face Value Rs.10/- per equity Shares)787.79 787.79 787.79

12. Reserve excluding revaluation reserves (as per Balance Sheet of previous accounting year)

2,309.79 1,928.40 2,309.79

13. Earnings Per Share (Rs.) Basic 0.73 0.59 5.13 Diluted 0.73 0.59 5.13

14. Aggregate of public share holdings -Number of Shares 55,64,08,006 56,44,21,927 56,44,21,927 -Percentage of Shareholding 70.63% 71.65% 71.65%

15. Promoter & Promoter Group Shareholding a) Pledged/Encumbered - Number of Shares 13,64,27,640 20,22,42,838 15,24,27,640

- Percentage of Shares (as a % of the total shareholding of promoter and promoter group)

58.96% 90.54% 68.24%

- Percentage of Shares (as a % of the total share capital of the Company)

17.32% 25.67% 19.35%

b) Non- encumbered - Number of Shares 9,49,48,711 2,11,33,513 7,09,48,711 - Percentage of Shares (as a % of the total

shareholding of promoter and promoter group 41.04% 9.46% 31.76%

- Percentage of Shares (as a % of the total share capital of the Company)

12.05% 2.68% 9.00%

UNAUDITED FINANCIAL RESULTS FOR THE QUARTER ENDED 30 JUNE 2011

3TM Integrated Textile Solutions

NOTES:

1. The above results have been reviewed by the Audit Committee and taken on record by the Board of Directors of the Company at their meeting held on 29 July 2011. The same are subject to Limited Review by the statutory auditors of the Company.

2. Total Income has increased by 49.73% over the corresponding quarter of the previous year to reach Rs. 1,645.59 crore. Domestic sales increased by 57.24% over Q4, 2009-10 to reach Rs.1,042.70 crore, while export sales was Rs.602.19 crore – an increase of 38.16%

3. The Board of Directors of the company have considered and approved the proposal for amalgamation of Grabal Alok Impex Limited (GAIL) into the company as per the terms and conditions mentioned in the Scheme of Amalgamation placed before the Board, subject to necessary approvals from the statutory and regulatory authorities. The swap ratio as determined by M/s Ernst & Young Pvt Ltd., independent valuer and the fairness report provided by M/s Fortune Financials Services (India) Ltd. and as approved by the Board is 1 (One) fully paid equity share of Rs. 10/ – each of the company to be issued and allotted for every 1 (One) fully paid equity share of Rs. 10/ – each held in GAIL.

4. The company has contracted the following deals relating to real estate held by its wholly owned subsidiary:

i. TwocommercialfloorsoutofTwentyfloorsinTower‘B’ofPeninsulaBusinessPark,LowerParelhavebeen leased out to a leading FMCG MNC;

ii. OneflooroutofEightfloorsinAshfordCentre,LowerParelhavebeensoldtoareputeddomesticNBFC;

iii. Seventy Three Acres of land at Silvassa have been agreed to be sold to six different parties.

5. TheBoardconsideredandrecommendedequitydividendof2.5%i.e.Rs.0.25perequityshareforthefinancialyear ending March 31, 2011, subject to the approval of the members at the Annual General Meeting, which has beenfixedforThursdaythe29September2011.

6. No. of investor complaints at the beginning of the quarter were NIL, received during the quarter were 16, disposed off during the quarter were 16 and lying unsolved at the end of the quarter were NIL.

7. The entire operations of the Company relate to only one segment viz., textiles. The risk and returns are generally perceived by the management to be the same for all units and thus treated as one segment.

8. Thefiguresofpreviousquarter/periodhavebeenreclassified/regroupedwherevernecessarytocorrespondwith those of the current quarter/period.

By order of the Board

For ALOK INDUSTRIES LIMITED

Sd/-

DILIP B. JIWRAJKA

Managing Director

Place: Mumbai

Date: 29 July 2011

UNAUDITED FINANCIAL RESULTS FOR THE QUARTER ENDED 30 JUNE 2011

4 Celebrating 25 Years 1986-2011

• RightsIssueofFCDs of Rs. 51 crores.

• Turnoversurpasses Rs. 550 crores

• Expansionofweaving and wider width processing capacities under TUFS of Rs.225 crores

• Turnoverof Rs. 350 crores• RightsIssue

of Rs. 14.98 crores

• TurnoverofRs.100 crores

• IPOofRs.4.50 crores

• Incorporation

• Collaborationwith Grabher, Austria to form Grabal Alok Impex Ltd. for manufacture of embroidery

• Privateplacement of Rs. 15 crores to Century Direct Fund (Mauritius)

1986 1993 1995 1996 1997 1998 2000 2001 2002

MAJOR MILESTONES OF LAST 25 YEARS

5TM Integrated Textile Solutions

• TurnoverRs.6388 crores, export Rs. 2217 Crores.

• IMC-Ramakrishna Bajaj Award for manufacturing.

• Expansionofpolyester from 600 tons/day to 1400 tons/day

• RecognisedStarTrading House

• TurnoverRs.4311crores, export Rs. 1500 crores

• QIPRs.425crores• Addedterrytoweltoits

home textile range

• RightsIssueRs.450 crores

• Completedintegration of polyester by continuous polymerization capacity of 600 tpa.

• EmbarkedonphaseIV of expansion project aggregating to Rs. 1180 crores

• RaisedECBequivalent to USD 90 mn

• AcquirestakeinUKretail store twenty one

• CompletedPhaseI & II expansion drive

• FCCBissueofUSD 70 mn.

• FCCBissueofUSD 35 mn.

• “ExportTradingHouse” Status awarded.

• Forayintohometextiles.

• TurnoversurpassesRs.1000crores (Exports exceeded Rs.100 crores)

• MezzanineFinanceTransactionof Rs.101 crores with CLSA group

• InitiatedPhaseI&IIofRs.1175crores

• ISO9001:2000certificationobtained• Forayintodomesticretailingunderthename“H&A”

• EmbarkedonPhaseIIIofexpansionprojectaggregating to Rs. 1100 crores

• AcquisitionofMiletaInternational(60%stake), a company based in Czech Republic

• Contractedtoacquirepremiumpropertiesadmeasuring about 7,00,000sq. feet. In Lower Parel

• Turnover-Rs.1800croreswithexports-Rs.640 crores

2003 2004 2005 2006 2007 2008 2009 2010 2011

6 Celebrating 25 Years 1986-2011

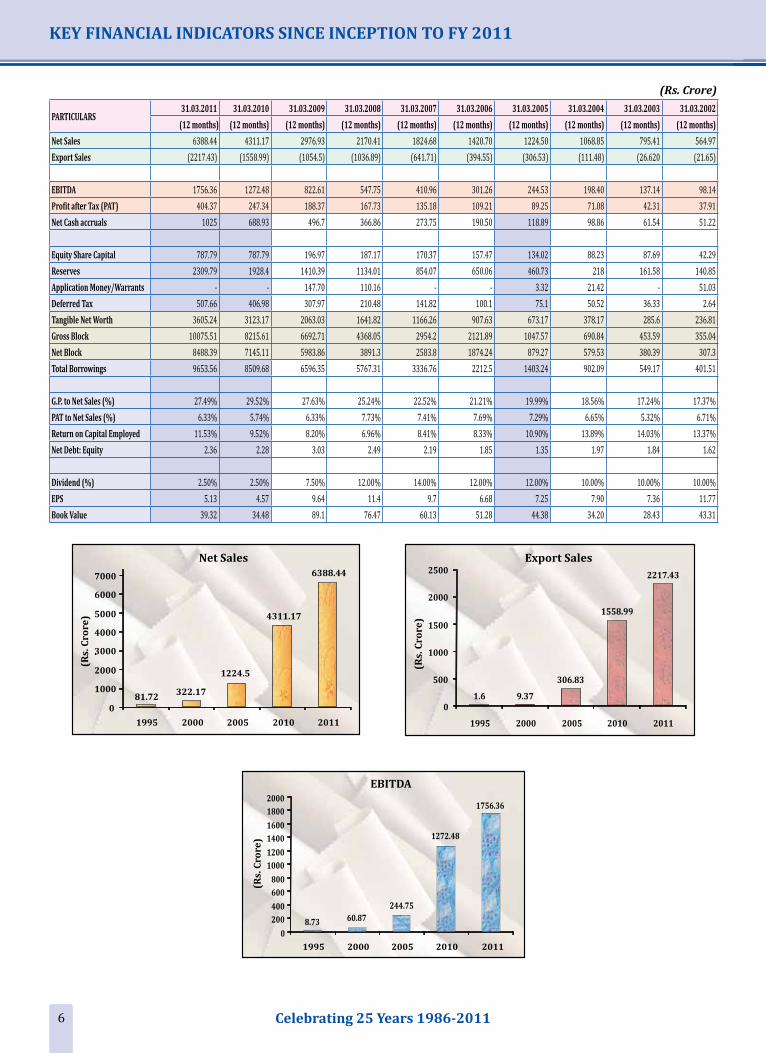

KEY FINANCIAL INDICATORS SINCE INCEPTION TO FY 2011

(Rs. Crore)

PARTICULARS31.03.2011 31.03.2010 31.03.2009 31.03.2008 31.03.2007 31.03.2006 31.03.2005 31.03.2004 31.03.2003 31.03.2002

(12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (12 months)

Net Sales 6388.44 4311.17 2976.93 2170.41 1824.68 1420.70 1224.50 1068.85 795.41 564.97Export Sales (2217.43) (1558.99) (1054.5) (1036.89) (641.71) (394.55) (306.53) (111.48) (26.620 (21.65)

EBITDA 1756.36 1272.48 822.61 547.75 410.96 301.26 244.53 198.40 137.14 98.14Profit after Tax (PAT) 404.37 247.34 188.37 167.73 135.18 109.21 89.25 71.08 42.31 37.91Net Cash accruals 1025 688.93 496.7 366.86 273.75 190.50 118.89 98.86 61.54 51.22

Equity Share Capital 787.79 787.79 196.97 187.17 170.37 157.47 134.02 88.23 87.69 42.29Reserves 2309.79 1928.4 1410.39 1134.01 854.07 650.06 460.73 218 161.58 140.85Application Money/Warrants - - 147.70 110.16 - - 3.32 21.42 - 51.03Deferred Tax 507.66 406.98 307.97 210.48 141.82 100.1 75.1 50.52 36.33 2.64Tangible Net Worth 3605.24 3123.17 2063.03 1641.82 1166.26 907.63 673.17 378.17 285.6 236.81Gross Block 10075.51 8215.61 6692.71 4368.05 2954.2 2121.89 1047.57 690.84 453.59 355.04Net Block 8488.39 7145.11 5983.86 3891.3 2583.8 1874.24 879.27 579.53 380.39 307.3Total Borrowings 9653.56 8509.68 6596.35 5767.31 3336.76 2212.5 1403.24 902.09 549.17 401.51

G.P. to Net Sales (%) 27.49% 29.52% 27.63% 25.24% 22.52% 21.21% 19.99% 18.56% 17.24% 17.37%PAT to Net Sales (%) 6.33% 5.74% 6.33% 7.73% 7.41% 7.69% 7.29% 6.65% 5.32% 6.71%Return on Capital Employed 11.53% 9.52% 8.20% 6.96% 8.41% 8.33% 10.90% 13.89% 14.03% 13.37%Net Debt: Equity 2.36 2.28 3.03 2.49 2.19 1.85 1.35 1.97 1.84 1.62

Dividend (%) 2.50% 2.50% 7.50% 12.00% 14.00% 12.00% 12.00% 10.00% 10.00% 10.00%EPS 5.13 4.57 9.64 11.4 9.7 6.68 7.25 7.90 7.36 11.77Book Value 39.32 34.48 89.1 76.47 60.13 51.28 44.38 34.20 28.43 43.31

7TM Integrated Textile Solutions

(Rs. Crore)

31.03.2001 31.03.2000 31.03.1999 31.03.1998 31.03.1997 1.03.1996 31.03.1995 31.03.1994 31.12.1992 31.03.1992 31.03.1991 31.03.1990 31.03.1989 30.10.1987

(12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (12 months) (15 months) (9 months) (12 months) (12 months) (12 months) (17 months) (12 months)

443.29 322.17 238.18 196.71 167.97 120.55 81.72 55.84 26.43 16.53 15.88 8.92 0.38 0.04(18.74) (9.37) (6.1) (3.17) (2.77) (0.1) (1.6) (2.87) (0.18) - - - - -

76.21 60.86 44.7 26.94 17.96 14.25 8.73 3.52 1.45 1 0.5 0.21 0.01 -29.47 21.38 14.96 10.22 6.23 6.02 4.88 1.92 0.8 0.53 0.11 (0.11) (0.03) -37.76 26.27 16.4 10.80 7.86 8.21 6.14 1.04 0.94 0.67 0.24 0.02 - -

28.35 27.82 23.64 11.62 9.71 3.74 3.75 3.49 0.73 0.25 0.25 0.25 0.25 -103.13 75.04 46.2 28.14 23.22 13.1 7.78 3.6 0.99 0.49 - (0.12) (0.03) -

29.48 13.95 1.35 1.13 - 7.24 - - 0.81 - 0.14 0.14 0.14 0.03- - - - - - - - - - - - - -

160.96 116.81 71.19 40.89 32.93 24.08 11.53 7.09 2.53 0.74 0.38 0.27 0.37 0.03227.89 144.94 130.08 105.25 62.23 45.24 24.84 7.98 3.76 2.15 - 1.42 1.39 0.03195.82 123.99 116.75 98.15 54.79 35.35 21.83 8.07 3.41 1.74 1.22 1.28 1.36 0.03285.16 209.32 183.68 145.88 73.47 47.28 33.34 11.92 2.51 2.29 1.89 1.167 1.13 -

17.19% 17.07% 15.98% 13.70% 10.69% 11.82% 10.56% 6.30% 5.49% 6.04% 3.15% 2.35% 2.63% 2.29%6.65% 6.00% 5.35% 5.20% 3.71% 4.99% 5.97% 3.43% 3.03% 3.21% 6.93% -1.23% -7.89% 0.75%

14.61% 15.59% 14.97% 12.70% 14.44% 16.23% 19.46% 18.52% 28.77% 33.00% 21.95% 14.57% 0.67% -1.65 1.58 2.44 3.46 2.14 1.89 2.85 1.36 0.85 2.93 4.53 4.10 3.09 -

10.00% 10.00% 20.00% 20.00% 20.00% 20..00% 20.00% 20.00% 15.00% 10.00% - - - -10.39 8.91 8.98 8.8 16.25 16.10 13.01 5.50 10.96 21.20 4.40 (4.40) (1.20) -46.38 36.97 29.54 34.22 33.91 64.39 30.75 20.32 34.66 29.60 15.40 10.96 14.57 840.29

8 Celebrating 25 Years 1986-2011

The`H&A’chainofstoresopenedanadditional20shopsduringthequarter;takingthetotalnumberto311 (including shop-in-shop); target is to have about 500 stores operational by March 2012. In Annual Survey, Franchise India has ranked H&A as one of the top 100 franchising opportunities in India for 2011

`StoreTwentyOne’,theUKretailchainofvalue-formatstorescontinuedtodoreasonablywellduringthequarter.GrabalAlok(UK)Ltd,theCompanythatoperatesthesestorescontinuedtogeneratepositiveEBIDTA of £ 0.71 mn. The sales for Q1 2011-12 was at £ 31.47 mn as compared to £ 30.84 mn in the corresponding quarter of the previous period. As of today, there is a total of 219 stores

The Board of Directors of the company have considered and approved the proposal for amalgamation of Grabal Alok Impex Limited (GAIL) into the company as per the terms and conditions mentioned in the Scheme of Amalgamation placed before the Board, subject to necessary approvals from the statutory and regulatory authorities. The swap ratio as determined by M/s Ernst & Young Pvt. Ltd., independent valuer and the fairness report provided by M/s Fortune Financials Services (India) Ltd. and as approved by the Board is 1 (One) fully paid equity share of Rs. 10/ – each of the company to be issued and allotted for every 1 (One) fully paid equity share of Rs. 10/ – each held in GAIL.

CreditAnalysisandResearchLtd(CARE)hasmaintained‘CAREA+’ratingfortheCompany’slongtermfacilities,whileratingfortheCompany’sshorttermcommercialpaper/MIBORlinkedshorttermNCDshavebeenupgradedandassigned‘CAREA1+’rating

The company has contracted the following deals relating to real estate held by its wholly owned subsidiary:

• Twocommercial floorsoutofTwentyfloors inTower ‘B’ofPeninsulaBusinessPark,LowerParelhave been leased out to a leading FMCG MNC;

• OneflooroutofEightfloorsinAshfordCentre,LowerParelhavebeensoldtoareputeddomesticNBFC;

• SeventyThreeAcresoflandatSilvassahavebeenagreedtobesoldtosixdifferentparties

The Company has intensified efforts to sell / lease its prime commercial properties at Lower Parel,Mumbai (held bywholly owned subsidiaries) and is confident ofmaking significant progress in thisdirection by the year end

KEY DEVELOPMENTS IN THE QUARTER

9TM Integrated Textile Solutions

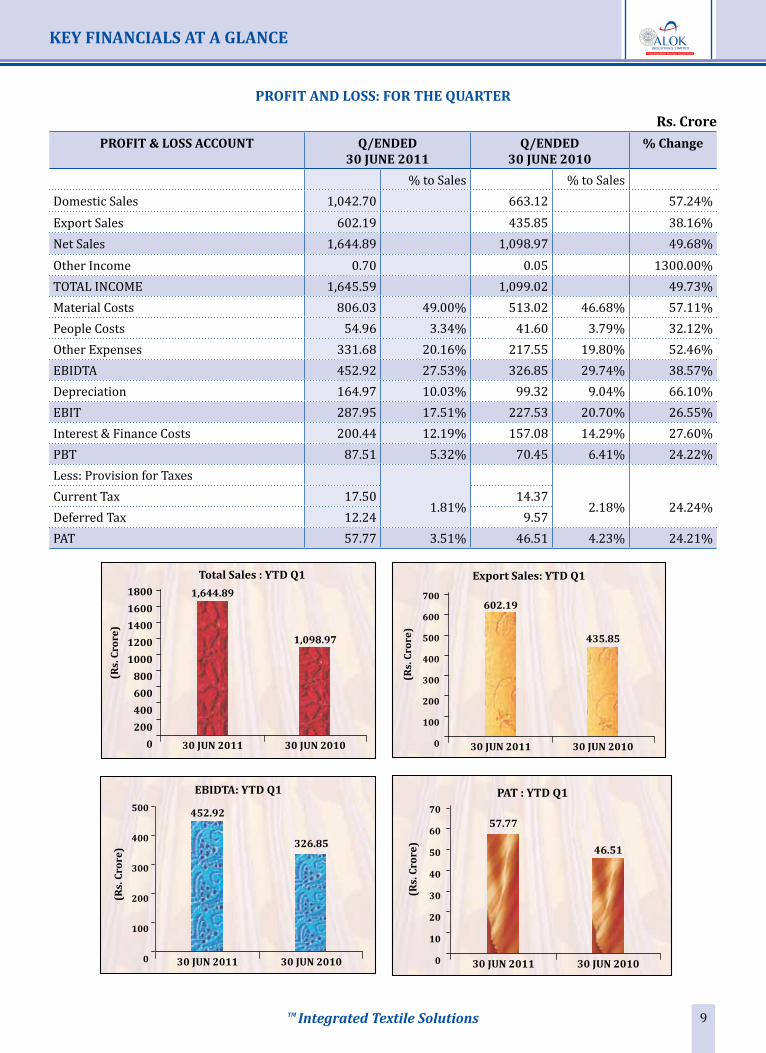

PROFIT AND LOSS: FOR THE QUARTER

Rs. CrorePROFIT & LOSS ACCOUNT Q/ENDED

30 JUNE 2011Q/ENDED

30 JUNE 2010% Change

% to Sales % to SalesDomestic Sales 1,042.70 663.12 57.24%Export Sales 602.19 435.85 38.16%Net Sales 1,644.89 1,098.97 49.68%Other Income 0.70 0.05 1300.00%TOTAL INCOME 1,645.59 1,099.02 49.73%Material Costs 806.03 49.00% 513.02 46.68% 57.11%People Costs 54.96 3.34% 41.60 3.79% 32.12%Other Expenses 331.68 20.16% 217.55 19.80% 52.46%EBIDTA 452.92 27.53% 326.85 29.74% 38.57%Depreciation 164.97 10.03% 99.32 9.04% 66.10%EBIT 287.95 17.51% 227.53 20.70% 26.55%Interest & Finance Costs 200.44 12.19% 157.08 14.29% 27.60%PBT 87.51 5.32% 70.45 6.41% 24.22%Less: Provision for Taxes

1.81%

2.18%

24.24%Current Tax 17.50 14.37Deferred Tax 12.24 9.57PAT 57.77 3.51% 46.51 4.23% 24.21%

KEY FINANCIALS AT A GLANCE

10 Celebrating 25 Years 1986-2011

DIVISIONAL PERFORMANCE : FOR THE QUARTER

Rs. Crore

PARTICULARS 3 M YTD ENDED 30 JUN 2011 3M YTD ENDED 30 JUN 2010

CHANGELO

CAL

EXP

OR

T

TO

TAL

% T

O

TO

TAL

SALE

S

LOCA

L

EXP

OR

T

TO

TAL

% T

O

TO

TAL

SALE

S

COTTON YARN 28.95 14.15 43.10 2.62% 19.07 30.53 49.60 4.51% (13.10%)

APPAREL FABRIC

WOVEN 488.97 116.84 605.81 36.82% 397.02 41.73 438.75 39.92% 38.08%

KNITTING 36.09 38.22 74.31 4.52% 23.28 21.59 44.87 4.08% 65.61%

525.06 155.06 680.12 41.34% 420.30 63.32 483.62 44.00% 40.63%

HOME TEXTILES 3.77 231.59 235.36 14.31% 11.50 170.16 181.66 16.53% 29.56%

GARMENTS 3.17 39.53 42.70 2.60% 1.81 29.37 31.18 2.84% 36.95%

POLYESTER YARN 481.75 161.86 643.61 39.13% 210.44 142.47 352.91 32.12% 82.37%

TOTAL 1,042.70 602.19 1,644.89 100.00% 663.12 435.85 1,098.97 100.00% 49.68%

DIVISIONAL PERFORMANCE: RELATIVE SHARE IN TOTAL SALES

Q1 JUNE 2011 Q1 JUNE 2010

DIVISIONAL PERFORMANCE

11TM Integrated Textile Solutions

SUMMARY PROFIT & LOSS ACCOUNT: FOR THE QUARTER Rs. Crore

PARTICULARS 3M ENDED 30 JUN 2011

3M ENDED30 JUN 2010

NET SALES 1,644.89 1,098.97

EBIDTA 452.92 326.85

DEPRECIATION 164.97 99.32

MISC. EXP. W/OFF 0.00 0.00

PBIT 287.95 227.53

INTEREST 200.44 157.08

PBT 87.51 70.45

PAT 57.77 46.51

CASH PROFIT 222.74 145.83

OPERATING NET CASH ACCRUALS 222.74 145.83

SUMMARY BALANCE SHEET

Rs. Crore

PARTICULARS AS ON 30 JUN 2011

AS ON 31 MAR 2011

(Audited)

TANGIBLE NET WORTH 3,150.84 3,097.58

TOTAL LONG TERM BORROWINGS 7,505.00 7,129.67

TOTAL SHORT TERM BORROWINGS 2,394.08 2,523.89

TOTAL BORROWINGS 9,899.07 9,653.56

DEFERRED TAX LIABILITY 494.20 507.66

TOTAL LIABILITIES 13,544.11 13,258.80

NET FIXED ASSETS 8,689.36 8,488.39

TOTAL INVESTMENTS 187.53 167.20

Foreign Currency Translation Monetary A/c 0.00 (0.22)

CURRENT ASSETS 5,551.57 5,579.46

CURRENT LIABILITIES 884.35 976.03

NET CURRENT ASSETS 4,667.22 4,603.43

TOTAL ASSETS 13,544.11 13,258.80

FINANCIAL POSITION

12 Celebrating 25 Years 1986-2011

CASH FLOW

Rs. Crore

PARTICULARS Q1 Annual

2011-12(Provisional)

2010-11(Audited)

NET CASH GENERATED FROM OPERATING ACTIVITIES (38.68) 1,135.50

NET CASH USED IN INVESTING ACTIVITIES (486.09) (1195.66)

NET CASH GENERATED FROM FINANCING ACTIVITIES (43.05) 369.37

NET FLOW (567.81) 309.22

CASH AND CASH EQUIVALENTS

AT THE BEGINNING OF THE PERIOD 1,099.37 587.97

AT THE END OF THE PERIOD 531.56 897.19

NET INCREASE IN CASH AND CASH EQUIVALENTS (567.81) 309.22

KEY RATIOS

PARTICULARS 30-JUN-11 (3 Months)

(Provisional)

2010-11 (12 Months)

(Audited)

2009-10(12 Months)

(Audited)Profitability Ratios

EBITDA (%) 27.53% 27.49% 29.52%ProfitBeforeTaxMargin(%) 5.32% 9.13% 8.69%ProfitAfterTaxMargin(%) 3.51% 6.33% 5.74%Return on Net worth (%) 6.34% 11.22% 7.92%Return on Capital Employed (%) 10.33% 11.53% 9.52%Balance Sheet Ratios

Net Debt (Long Term) – Equity including Deferred Tax Liability 1.88 1.66 1.62Net Total Debt – Equity including Deferred Tax Liability 2.53 2.36 2.28Net Total Debt / EBITDA 5.09 4.85 5.59Current Ratio 1.69 1.59 1.83Coverage Ratios

PBDIT/Interest 2.26 2.68 2.38Debtors Turnover – Days 89 98 93Inventory Turnover – Days 136 114 125

FINANCIAL POSITION

13TM Integrated Textile Solutions

SHARE CAPITAL AND TANGIBLE NET WORTH

Rs. Crore

PARTICULARS

AS ON

30 JUN 2011 31 MAR 2011(Audited)

EQUITY CAPITAL 787.79 787.79

SECURITIES PREMIUM RESERVE 880.39 880.39

GENERAL RESERVE 274.98 274.98

P&L ACCOUNT 888.32 921.60

OTHERS 319.36 232.82

TANGIBLE NET WORTH 3,150.84 3,097.58

LOANS: LONG AND SHORT TERM

Rs. Crore

PARTICULARS AS ON

30 JUN 2011 31 MAR 2011(Audited)

SECURED LOANS 7,398.24 6,967.45

UNSECURED LOANS 106.75 162.22

TOTAL LONG TERM BORROWINGS (A) 7,505.00 7,129.67

SECURED LOANS 1,072.30 1,092.71

UNSECURED LOANS 205.24 264.95

WORKINGCAPITALBORROWINGS 1,116.54 1,166.23

TOTAL SHORT TERM BORROWINGS (B) 2,394.08 2,523.89

TOTAL BORROWINGS (A+B) 9,899.07 9,653.56

LESS:CASH&BANKBALANCES (669.06) (1,141.21)

NET BORROWINGS 9,230.01 8,512.35

FINANCIAL POSITION

14 Celebrating 25 Years 1986-2011

FIXED ASSETSRs. Crore

PARTICULARS

AS ON30 JUN 2011 31 MAR 2011

(Audited)

FIXED ASSETS 9,297.49 9,014.31CAPITALWORKINPROGRESS 1,149.33 1,061.20GROSS FIXED ASSETS 10,446.82 10,075.51LESS: DEPRECIATION (1,757.46) (1,587.12)NET FIXED ASSETS 8,689.36 8,488.39

NET CURRENT ASSETS

Rs. Crore

PARTICULARSAS ON

30 JUN 2011 31 MAR 2011(Audited)

INVENTORIES 2,483.76 1,995.61DEBTORS 1,630.70 1,708.67CASH&BANKBALANCES 669.06 1,141.21LOANS & ADVANCES 768.05 733.97TOTAL CURRENT ASSETS 5,551.57 5,579.46SUNDRY CREDITORS 795.18 844.27OTHER CURRENT LIABILITIES 66.26 68.97PROVISIONS 22.91 62.79TOTAL CURRENT LIABILITIES 884.35 976.03NET CURRENT ASSETS 4,667.22 4,603.43

CAPACITIES

Divisions Units Current Capacities Capacities under Implementation

Capacities Post Expansions

SPINNING Tons 69,040 10,960 80,000(Spindles) ( 3,43,840) (68,000) (4,11,840)

HOME TEXTILESProcessing mn mtrs 82.5 22.5 105Weaving mn mtrs 68 24 92Terry Towels Tons 6,700 6,700 13,400APPAREL FABRICProcessing Woven mn mtrs 105 21 126Weaving mn mtrs 93 17 110Knits Tons 18,200 6,800 25,000GARMENTS mn pcs 22 - 22POLYESTERDTY Tons 1,14,000 56,000 1,70,000FDY Tons 65,700 - 65,700POY & Chips Tons 3,00,000 2,00,000 5,00,000

FINANCIAL ANALYSIS

15TM Integrated Textile Solutions

SHARE PRICE AND VOLUMES

Month BSE (In Rs. per share) NSE (In Rs. Per share)

High Low Volume High Low Volume

Apr-11 28 22 10,04,62,800 27.9 21.8 35,73,98,800

May-11 27.8 23.75 5,13,09,300 27.8 23.75 20,61,21,600

Jun-11 28.5 22.85 5,12,69,100 28.5 22.8 22,14,77,800

SHARE PERFORMANCE VIS-A-VIS STOCK MARKET INDICES

Note: Share prices and indices indexed to 100 as on 1 April 2011

EQUITY INFORMATION

Equity as on 30 JUN 2011 78.78 crore

BSE NSE

Closing Price as on 30 JUN 2011 25.20 25.15

3-Month High Low High: 28.50 High: 28.50

Low: 22.00 Low: 21.80

Market Capitalisation as on 30 JUN 2011 (Rs) 1,985.26 crore

SHAREHOLDING PATTERN

SHAREHOLDER ENTITIES CURRENT QUARTER PREVIOUS QUARTER

Promoters 29.37% 28.35%

Banks, Mutual Funds And FIs 11.69% 13.41%

FIIs, NRIs And OCB 20.68% 23.12%

Other Corporate Bodies and Public 38.26% 35.12%

Total 100.00% 100.00%

• 58.96%ofthepromoters’holdinghavebeenpledgedwithFIIs,MFsandotherlendersaspartofloanconditions. This represents a sum total of 13,64,27,640 equity shares

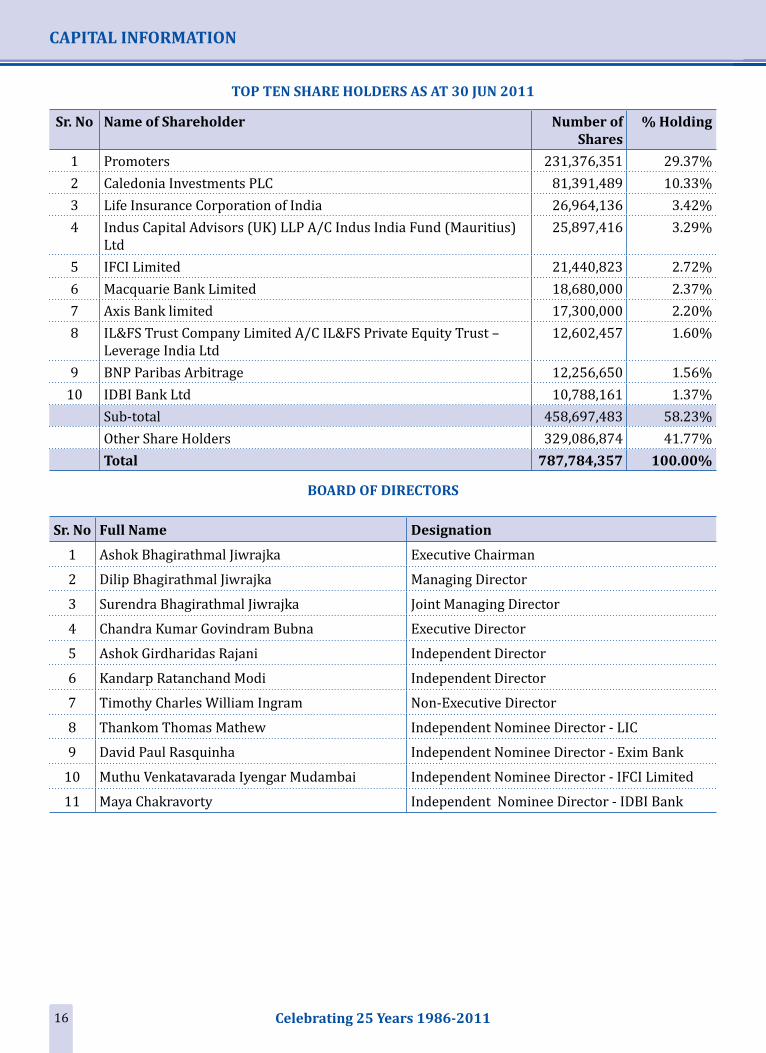

CAPITAL INFORMATION

16 Celebrating 25 Years 1986-2011

TOP TEN SHARE HOLDERS AS AT 30 JUN 2011

Sr. No Name of Shareholder Number of Shares

% Holding

1 Promoters 231,376,351 29.37%2 Caledonia Investments PLC 81,391,489 10.33%3 Life Insurance Corporation of India 26,964,136 3.42%4 IndusCapitalAdvisors(UK)LLPA/CIndusIndiaFund(Mauritius)

Ltd25,897,416 3.29%

5 IFCI Limited 21,440,823 2.72%6 Macquarie Bank Limited 18,680,000 2.37%7 Axis Bank limited 17,300,000 2.20%8 IL&FS Trust Company Limited A/C IL&FS Private Equity Trust –

Leverage India Ltd12,602,457 1.60%

9 BNP Paribas Arbitrage 12,256,650 1.56%10 IDBI Bank Ltd 10,788,161 1.37%

Sub-total 458,697,483 58.23%Other Share Holders 329,086,874 41.77%Total 787,784,357 100.00%

CAPITAL INFORMATION

BOARD OF DIRECTORS

Sr. No Full Name Designation

1 Ashok Bhagirathmal Jiwrajka Executive Chairman

2 Dilip Bhagirathmal Jiwrajka Managing Director

3 Surendra Bhagirathmal Jiwrajka Joint Managing Director

4 ChandraKumarGovindramBubna Executive Director

5 Ashok Girdharidas Rajani Independent Director

6 KandarpRatanchandModi Independent Director

7 Timothy Charles William Ingram Non-Executive Director

8 Thankom Thomas Mathew Independent Nominee Director - LIC

9 David Paul Rasquinha Independent Nominee Director - Exim Bank

10 Muthu Venkatavarada Iyengar Mudambai Independent Nominee Director - IFCI Limited

11 Maya Chakravorty Independent Nominee Director - IDBI Bank

17TM Integrated Textile Solutions

THE GLOBAL ECONOMY

Activity is slowing down temporarily, and downside risks have increased again. The global expansion remains unbalanced. Growth in many advanced economies is still weak, considering the depth of the recession. In addition, the mild slowdown observed in the second quarter of 2011 is not reassuring. Growth in most emerging and developing economies continues to be strong. Overall, the global economy expanded atanannualizedrateof4.3%inthefirstquarter,andforecasts for 2011–12 are broadly unchanged, with offsetting changes across various economies. However, greater-than-anticipated weakness in U.S. activity and renewedfinancialvolatilityfromconcernsaboutthedepthoffiscalchallengesintheeuroareaperipherypose greater downside risks. Risks also draw from persistent fiscal and financial sector imbalances inmany advanced economies, while signs of overheating are becoming increasingly apparent in many emerging and developing economies. Strong adjustments—credible and balanced fiscal consolidation andfinancialsectorrepairandreforminmanyadvancedeconomies, and prompter macroeconomic policy tightening and demand rebalancing in many emerging and developing economies—are critical for securing growth and job creation over the medium term.

INDIA

• On the domestic front, a revised and rebased IIP suggests that earlier signals of a growth deceleration in H2, FY12 were exaggerated. Data for April-May 2011 suggests that some moderation might be under way,reflectinginpartalaggedresponsetothemonetarytighteningthathasbeeneffectedsinceOctober2009

• The softening of commodity prices over the past three months did not translate into a decline in either headlinewholesalepriceindex(WPI)inflationornon-foodmanufacturinginflation

• GDP growth forecast retained at 8% for FY12

• WPIinflationforMarch2012isrevisedupwardfrom6%to7%,onbackofa)anyshortfallinrainfalloritspatterncouldposesignificantriskstofoodinflation,b)crudeoilpricesinthenearfutureisuncertain,c)IftheGovernmentraisesadministeredfuelprices,theinflationimplicationsarestraightforward.IftheGovernmentabsorbsthisinthefiscalaccounts,theresultantexpansionaryimpactwilladdtoinflationpressures.

ECONOMIC OVERVIEW

18 Celebrating 25 Years 1986-2011

THE TEXTILE INDUSTRY

Global Textile and Apparel Trade

• The imports of textile and apparel products by US increased from US$ 81 bn in 2009 to US$ 93 bn in 2010, growing by 15%. The imports have recovered from the economic slump in 2008-09 and growing further.

• EU imports of Textile and Apparel has increased in 2010 by 6.6% from US$ 215 bn in 2009 to US$ 229 bn in 2010. Growth has been slower than US imports primarily due to the prevailing economic downturn in major EU countries

• Therisingpricesofcotton,resultinginsubsequentdifficultyinremaining competitive in the global apparel market, has been one of the major trends of 2010. While the prices have shown a downward trend recently, the volatility in prices has become an even bigger concerns

• The unprecedented growth in cotton prices and the scarcity in its supply have started changing global equations in the textile and apparel market. There is increasing stress on substitutes and volume demand for polyester has started to increase rapidly.

Indian Textile Update

Indian Domestic Textile and Apparel Market Growth

India’s domestic textile and apparel market continued to grow in2010 on the back of ever increasing consumer demand. Domestic textile and apparel market is estimated to be US$ 52 bn in 2010 and expected to grow further to reach US$ 140 bn by 2020.

Indian Textile and Apparel Industry Export GrowthAlong with the growth of global trade, India has emerged as one of the strongest textile and apparel production hubs in the past years. India’sexportshavegrownataCAGRof11%inlast25yearstoreachUS$25bnin2010.Further,India’sexportsareexpectedtogrow@12% to reach US$ 80 bn by 2020.

Sources: Technopak, Ministry of Textiles (Govt of India)

Source: UN Comtrade, Ministry of Textiles

INDUSTRY OVERVIEW

19TM Integrated Textile Solutions

Alok Industries Limited

Q1 FY12 Net Sales up by 49.68% to Rs. 1,644.89 crore PAT up by 24.21% to Rs. 57.77 crore

Editors Synopsis

For the Quarter ended June 30, 2011:

• Net Sales up by 49.68% at Rs. 1,644.89 crore• EBIDTA increased by 38.57% at Rs. 452.92 crore• PAT up by 24.21% at Rs. 57.77 crore

Mumbai, 29 July, 2011:

Alok Industries Limited, one of the leading integrated textile companies in India, today reported net sales of Rs. 1,644.89 crore for the quarter ended June 30, 2011, as compared to Rs. 1,098.97 crore in the corresponding periodofthelastfiscal,registeringagrowthof49.68%.

Export sales for the quarter ended June 30, 2011 stood at Rs. 602.19 crore, as against Rs. 435.85 crore in the sameperiodofthelastfiscal,registeringagrowthof38.16%.

DuringtheJune’11quarterthecompany’snetprofitstoodatRs.57.77crore,higherby24.21%,ascomparedtoRs.46.51crorepostedinthesamequarteroflastfiscalyear.

The EBIDTA for the quarter was at Rs. 452.92 crores as against Rs. 326.85 crores in the corresponding quarter oflastfiscalyear,registeredagrowthof38.57%.

Earning per share (EPS) for June quarter stood at Rs. 0.73.

Dividend for Financial Year 2010-2011

Thecompany’sboard,inameetingheldtoday,hasrecommendedadividendof2.5%,orRs.0.25pershare,ontheequitysharesofRs10eachforthefinancialyear2010–11.

Merger of Grabal Alok Impex Ltd with the company

The Board of Directors of the company have considered and approved the proposal for amalgamation of Grabal Alok Impex Limited (GAIL) into the company as per the terms and conditions mentioned in the Scheme of Amalgamation placed before the Board, subject to necessary approvals from the statutory and regulatory authorities.

The swap ratio as determined by M/s Ernst & Young Pvt Ltd., independent valuer and the fairness report provided by M/s Fortune Financials Services (India) Ltd. and as approved by the Board is 1 (One) fully paid equity share of Rs. 10/ – each of the company to be issued and allotted for every 1 (One) fully paid equity share of Rs. 10/ – each held in GAIL.

GrabalAlokispromotedbyAlokIndustriesLimitedintechnicalandfinancialcollaborationwithGrabalAlbertGrabher Gesellschaft m.b.H & Co., of Austria. The company is a manufacturer of all kinds of embroidered products having wide application in home textiles, apparel fabrics and garments.

25th AGM to be held on Thursday, September 29, 2011

TheboardhasalsofixedThursday,September29,2011asthedateforholdingthecompany’sTwentyFifthAnnualGeneralMeeting.ThemeetingwillbeheldattheregisteredofficeofthecompanyatSilvassaat12.00Noon

Management Comment

Commenting on the results, Mr. Dilip Jiwrajka, Managing Director, Alok Industries Limited,said,“Ourbusiness performance was quite encouraging in Q1 FY 2012 and we were able to achieve satisfactory growth. We are glad to see the continued demand for our products, the widening of the business across product

PRESS RELEASE

20 Celebrating 25 Years 1986-2011

segments and geographies. We look forward to encash our real estate investments in subsidiaries, optimize ourexpandedcapacitiesandreducecost,whichwouldbenefitallstakeholders.”

OntheschemeofamalgamationofGrabalAlokImpexLimitedwiththecompany,hesaid,“Thiscorporateaction should bring about operational and financial synergies besides enabling focused managementattentionthroughasingleunifiedTextileenterprise.”

About Alok Industries Limited:

(BSE Code: 521070) (NSE Code: ALOKTEXT) (Reuters Code: ALOK.BO) (Bloomberg Code: ALOK@IN)

Established in 1986, Alok Industries Ltd. is amongst the fastest growing vertically integrated textiles solutions provider in India.Adiversifiedmanufacturerofworld-classhometextiles,apparel fabrics,garmentsandpolyester yarns, Alok has capacities of 82.50 mn meters of sheeting fabric and 6700 tons of terry towels for its home textiles business, 105.00 mn meters of apparel width woven fabrics, 18200 tons per annum of knitted fabrics and 22 million pieces per annum of garments.

With the commencement of spinning of cotton yarn (58,500 tons per annum), Alok has achieved complete integration. The company also has a strong presence in the polyester segment with a capacity of 1,14,000 tons per annum of polyester textured yarn supplemented by 2,00,000 tons per annum of POY. The company has a blue chip international customer base comprising of world renowned retailers, importers and brands.

For More Information Please Contact:Mr.SunilO.KhandelwalChief Financial OfficerAlok Industries LtdTel: 022-2499 6241Email: [email protected]

Mr.SiddharthKumar/Mr.AnkurParikhAdfactors PR, MumbaiCell : 9833933447/9820092291siddharth.kumar@adfactorspr.comankur.parikhadfactorspr.com

PRESS RELEASE

Garments

END T

O EN

D SO

LUTIO

NS A

CROSS T

HE V

ALU

E CH

AIN

To be the world's best integrated textile solutions enterprise with leadership position across products and markets, exce e d i n g c u s to m e r & s t a ke h o l d e r ex p e c t a t i o n s . The barometer of our success would be reflected by our ROCE

WE WILL:

ØMaximize people development initiatives

ØOptimize use of all resources

ØBecome a process driven organization

ØExceed compliance and global quality standards

ØActively explore potential market & products

ØOffer innovative, customized and value added services to our customers

ØBe a knowledge leader & an innovator in our businesses

ØBe an ethical, transparent and responsible global organization

Alok Mission

Alok Vision

Celebrating 25 Years 1986-2011

"Alok is an 'end-to-end' provider of Integrated Textile Solutions, with five core divisions: Cotton Yarn, Apparel Fabric, Home Textiles, Garments and Polyester Yarn

Alok's State of the Art Integrated Textile Facilities

Spinning

Processing

Knitting

Quilting Schiffli Embroidery

Madep-ups

Multi Head Embroidery

Weaving

Yarn Dyeing

Printing

Processing

WP

PL

P E R F O R M A N C E R E P O R T

First Quarter Ended30 June 2011

Celebrating 25 years 1986-2011