p. 0 united nations capital development fund panel discussion on regulation of microfinance...

TRANSCRIPT

p. 1

United Nations Capital Development Fund

Panel Discussion on Regulation of Microfinance

Initiatives Supporting the Development of Regulatory Frameworks for Microfinance

Financing for Development Office, UNDESA

New York City

10 April 2007

p. 2

UNCDF: Investing in the LDCs.

UN Advisors Group on Inclusive Financial Sectors.

Brief Survey of Initiatives Supporting Regulatory Frameworks for Microfinance.

UNCDF.

GTZ.

USAID.

ADB.

Microfinance Networks.

Microfinance Consensus Guidelines: Guiding Principles on Regulation and Supervision.

Financial Access Initiative.

Presentation Overview

p. 3

UNCDF makes investments in the Least Developed Countries (LDCs):

Currently working in 28 Least Developed Countries.

- Total population: approximately 625 million.

- Average GDP: approximately US$ 317 per person per year.

Current investment portfolio about $125 million.

Our Mission: Reduce poverty in these countries and help them achieve the Millennium Development Goals (MDGs).

Our Method: Investing in human and institutional capacity at the local and national levels and funding and supporting Local Development Programmes and Microfinance Institutions (MFIs).

Our Approach: Long-term outlook seeking local and national capital formation and human development.

Our Capital: Flexible, high risk and innovative.

UNCDF: Investing in the LDCs

p. 4

UNCDF Methodology

1. Conduct Financial Sector Assessment.

Gather data on access to financial services to establish a baseline and measure results.

Evaluate legal, regulatory, and policy frameworks, and financial services infrastructure requirements.

Evaluate human and institutional capacity and constraints.

2. Develop Nationally Owned Policy, Strategy and Action Plan.

Legal, regulatory, and policy environments.

Financial Service Providers (FSPs) required to provide products and services and to strengthen financial sector.

Financial services infrastructure requirements.

FSP investment requirements.

Coordinating, implementing, and monitoring requirements.

UNCDF’s Sector Development Approach for building inclusive financial sectors:

p. 5

UNCDF Methodology

3. Execute National Action Plan.

Establish Investment Committees.

Composed of government representatives, development partners and other financial industry participants.

Solicits investment proposals for broad range of MFIs, FSPs and other industry participants.

Review process is competitive and transparent.

Make investments in microfinance institutions (MFIs), FSPs, financial services infrastructure providers, and other industry participants.

Investments may be grants, loans, or equity.

Human and institutional strengthening and capacity building emphasized.

… continued

p. 6

UNCDF also hosts the Secretariat of the UN Advisors Group on Inclusive Financial Sectors.

Established in June 2006 for a term of 2 years.

Seeks to increase global access of poor and low income households and micro and small enterprises to a broad range of financial products and services on a sustainable basis.

Consists of 25 representatives from the UN, World Bank, IMF, CGAP, African Development Bank, Central Bank of West Africa, Government Savings Bank of Thailand, World Council of Credit Unions, Accion International, Goldman Sachs, ABN-Amro, Deutsche Bank, Visa International, among other institutions.

Significant opportunity to raise global public awareness regarding financial inclusion and to place inclusive finance on the global development agenda.

UN Advisors Group on Inclusive Financial Sectors

p. 7

UN Advisors Group on Inclusive Financial Sectors and Regulation.

Of the four Working Groups established, one is focused exclusively on the issues of Regulation and Supervision.

Institutions represented in the Regulation & Supervision Working Group include: CGAP (Chair), IMF, World Bank, UN DESA, Central Bank of West African Banks (BCEAO), Visa International, Aga Khan Agency for Microfinance, Central Bank of Malaysia, World Council of Credit Unions, Foreign Ministry of Affairs of Luxembourg, and World Savings Bank Institute.

The Regulation and Supervision Working Group is currently preparing to conduct a Regional Conference on Regulation to be held in early 2008.

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 8

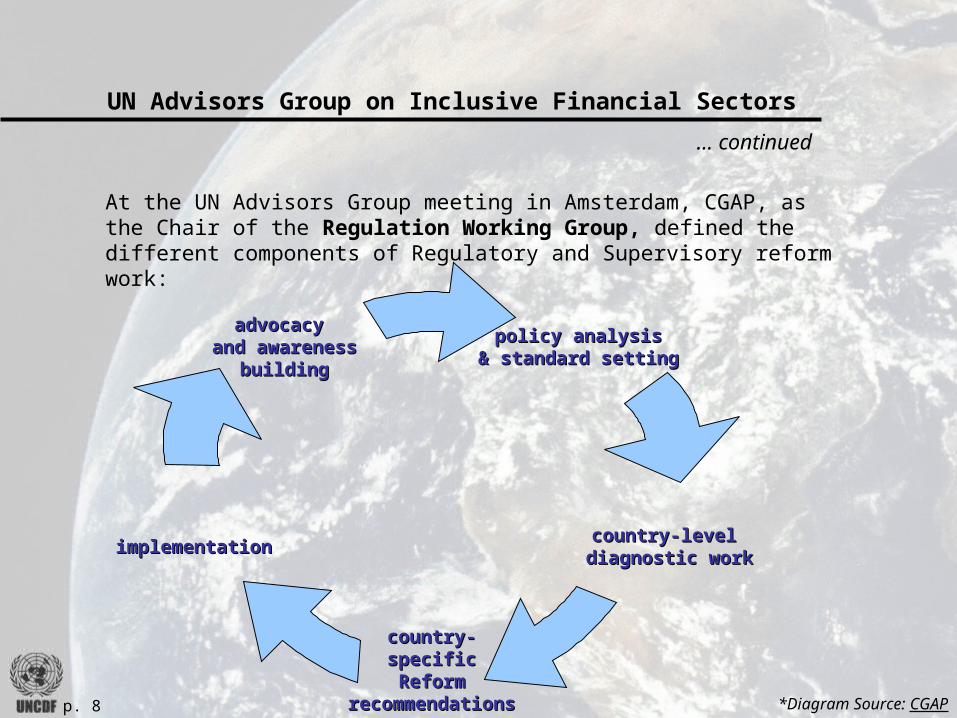

At the UN Advisors Group meeting in Amsterdam, CGAP, as the Chair of the Regulation Working Group, defined the different components of Regulatory and Supervisory reform work:

policy analysispolicy analysis& standard setting& standard setting

country-level country-level diagnostic workdiagnostic workimplementationimplementation

country-country-specificspecificReformReform

recommendationsrecommendations

advocacy advocacy and awarenessand awareness

buildingbuilding

*Diagram Source: CGAP

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 9

The Regulation Working Group also noted that there are multiple actors involved in one or more of these components.

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 10

The major conclusions of the Regulation Working Group were:

This is a very crowded space with multiple actors and institutions.

Donor coordination is a huge challenge.

.to avoid undercutting each other ־

.to avoid inconsistent advice ־

All actors need to think carefully about their comparative advantage.

.specialized expertise is needed but in short supply ־

practitioners have vital role to play, but not always seen as ־neutral.

different actors have different influence on decisions makers ־(varies by country).

*Source: CGAP

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 11

Within this context, the Regulation Working Group concluded that its overall objectives should be to:

Raise public awareness about the importance of inclusive finance among policymakers, central bankers, and government officials.

Advocate for appropriate regulatory and supervisory policies that encourage and support inclusive financial sectors.

Identify new areas where further discussions are needed with governments, regulators and supervisors.

Focus on particular regulatory and supervisory risks which potentially constrain access to financial services and products.

Recently provided input to "Five Key Messages for Four Key Audiences“: statements of best practices for expanding access to finance for the poor targeted at regulators, governments, development partners and the private sector.

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 12

The Key Messages to Regulators include:

Financial inclusion should be a major objective of financial regulation. The role of regulators is to establish environments that allow a diverse range of institutions to provide a wide variety of financial products and services.

Regulators must be flexible in their approach; they must mitigate risks, without limiting access to financial services.

Regulators must assure appropriate supervision of both financial service providers and their supporting industries, such as telecommunications.

Regulators must exercise caution that anti-money laundering and related regulations do not block access to financial transfers that are critical for poor people.

Broad-based access to financial services requires an enabling regulatory environment for telecommunications and technology infrastructure.

… continued

UN Advisors Group on Inclusive Financial Sectors

p. 13

Brief Survey of Initiatives Supporting Regulatory Frameworks for Microfinance.

p. 14

UNCDF:

UNCDF’s microfinance sector development approach is built upon the premise that microfinance institutions and other financial service providers (FSPs) serving the poor should over time become an integrated part of the formal financial sector.

Sector development programmes are designed to identify and respond to new opportunities, and address constraints that keep a financial sector exclusive.

One component of the sector development approach is the evaluation of a country’s legal, regulatory and policy frameworks, as well as financial services infrastructure requirements.

Since early 2003, sector assessments have been carried out in Nepal, Sierra Leone, Senegal, Madagascar, Democratic Republic of Congo, Malawi, Angola, and Liberia.

… continued

Country-level Diagnostic Work

p. 15

UNCDF:

Nepal Country Case Study

A 2006 financial sector assessment of Nepal conducted by UNCDF showed no immediate regulatory constraints to building an inclusive financial sector.

But Nepal’s Central Bank requested guidance on regulating the growing microfinance sector. Thus within the context of a $30 million programme to build an inclusive financial sector in Nepal, capacity building of the regulator is an integral component.

Assistance will be provided to help the government develop an appropriate policy/strategy and to the Central Bank to develop criteria for determining which institutions should be licensed and regulated and which institutions might only have a reduced reporting requirement.

This project will be launched in 2007 and co-funded by UNCDF, UNDP and the World Bank.

… continued

Country-level Diagnostic Work

p. 16

UNCDF:

Liberia Country Case Study

One of the findings of a 2004 financial sector assessment was that the present legal and regulatory environment creates several constraints for the development of the microfinance sector:

Low ceiling on interest rates (18% effective) made it unlikely that any commercial bank would enter the lending side of the microfinance market.

High reserve requirements of 50% and 18% for LD$ and USD$ discouraged domestic resource (savings) mobilization.

Unclear guidance on the percentage of portfolios permissible for cash collateral was being provided by Liberia’s Central Bank.

Since the financial sector assessment was conducted, the government has taken positive steps towards liberalizing the financial sector.

… continued

Country-level Diagnostic Work

p. 17

UNCDF:

Microfinance Regulation and Supervision Project In the West African Monetary Union (BCEAO)

The Central Bank of West African States (BCEAO) is the common central bank for 8 countries (Benin, Burkina Faso, Côte d’Ivoire, Guinea Bissau, Mali, Niger, Senegal, and Togo).

The $2.3 million project is being financed by a consortium of donors including UNCDF, CGAP, and SIDA. Project goals include:

Improving the regulatory framework to strengthen MFI governance and management and refine the region’s approach to supervision.

Strengthening the effectiveness of supervision, including licensing new entrants, supervising ongoing operations, and imposing sanctions.

Improving understanding of the financial sector, institutional risks, and overall performance of MFIs in the region.

… continued

Country-level Diagnostic Work

p. 18

GTZ:

GTZ supports microfinance operations in more than 40 countries, combining technical assistance to MFIs with financial sector reform that affects the institutional environment of MFIs.

GTZ advises central banks and banking supervisory agencies, and (in some countries) the ministries responsible for supervising MFIs.

Some of these projects include:

Uganda: Financial Systems Development Project - developed and implemented a regulatory and supervisory framework for MFIs.

Honduras: Financial Sector Development Project - assisted supervisory authorities in tailoring regulation and supervision to MFIs.

Kyrgyzstan: Strengthening and Development of Rural Financial Market - developed a legal framework for the co-operative sector.

Country-level Diagnostic Work

*Source: GTZ website

… continued

p. 19

USAID:

A variety of USAID projects have supported regulatory reform for microfinance.

These projects are usually in conjunction with implementing partners such as Development Alternatives International (DAI) or IRIS.

Some of the countries in which USAID has helped to support projects regarding microfinance regulatory reform are: Armenia, Bolivia, Ecuador, Georgia, Jordan, Malawi, Mexico, Nepal, Nigeria, Philippines, and Zambia.

Country-level Diagnostic Work

*Source: USAID website

… continued

p. 20

Asian Development Bank (ADB):

Provides assistance in the form of loans and technical assistance to member developing countries.

Some of ADB’s microfinance regulatory/supervisory activities include:

Uzbekistan: Financial Services for the Poor Project – aims to develop an enabling policy, legal and regulatory supervisory framework for savings and credit unions.

Azerbaijan: Microfinance Sector Development Project – seeks to develop microfinance regulations and collateral framework.

Laos PDR, Mongolia, Nepal, and Sri Lanka: Rural Finance Sector Development Programme - supports the creation of an enabling policy for a regulatory and supervisory framework for rural microfinance.

Published 2000 study “The Role of Central Banks in Microfinance in Asia and the Pacific” that examined the role and operations of central banks in microfinance development in Bangladesh, China, India, Indonesia, Kyrgyz Republic, Nepal, Pakistan, Papua New Guinea, Philippines, Sri Lanka, Vanuatu, and Vietnam.

Country-level Diagnostic Work

*Source: ADB website

… continued

p. 21

Microfinance Networks

Microfinance Centre for Central & Eastern Europe and the New Independent States (MFC):

International, grass-root network of 90 MFIs from the region.

Along with other Regulation initiatives, it conducts an annual "Policy Forum on Microfinance Law and Regulation“.

The main purposes of the annual Policy Forum are to benchmark the progress of the countries in which initiatives to create favorable environment for microfinance are taking place or that took place during the previous year and to increase the awareness of policy makers from countries not yet selected for MFC Initiatives.

*Source: MFC website

Advocacy and Awareness Building

p. 22

Microfinance Consensus Guidelines: Guiding Principles on Regulationand Supervision.

Published by CGAP.

Captures a broad consensus on best practices in regulation and supervision of microfinance. The guidelines summarize these principles for government regulators and others engaged in moving microfinance into the formal financial sector.

Some major principles that have been agreed include:

Problems that do not require the government to oversee and judge the financial soundness of regulated institutions should not be dealt with through prudential regulation.

In some countries, legal changes are needed to make it clear that NGOs and other private bodies may conduct a lending-only business without having to be prudentially licensed and regulated.

Depending on practical costs and benefits, prudential regulation in some cases may not be necessary for MFIs that take cash collateral.

Policy Analysis & Standard Setting

*Source: CGAP

p. 23

Financial Access Initiative

A joint project of Yale University, Harvard University, New York University, and Innovations for Poverty Action (IPA).

Formed in 2006 as a research consortium focused on improving access to financial services for the world’s poor through research on innovation, regulation, and financial policy.

Of the three main activities that will be conducted, one focuses on policy around regulation.

Aims to describe policy options for central bankers and regulators in a high-level but accessible format.

Focus will be on recent experiences across countries, regulatory constraints, and possibilities.

Outputs will be independent, rigorous guides for regulatory policy with an emphasis on direct effects and trade-offs of policy choices.

… continued

Policy Analysis & Standard Setting

p. 24

United Nations Capital Development Fund

Panel Discussion on Regulation of Microfinance

Initiatives Supporting the Development of Regulatory Frameworks for Microfinance

Financing for Development Office, UN DESA

New York City

10 April 2007