oxy permian tour - occidental petroleum investordaymarch2… · 4 • 2.5 million net acres in the...

TRANSCRIPT

Oxy Permian TourDriving Value in the PermianMarch 10, 2017

2

Forward-Looking StatementsPortions of this presentation contain forward-looking statements and involve risks and uncertainties that could materially affect expected results of operations, liquidity, cash flows and business prospects. Actual results may differ from anticipated results, sometimes materially, and reported results should not be considered an indication of future performance. Factors that could cause results to differ include, but are not limited to: global commodity pricing fluctuations; supply and demand considerations for Occidental's products; higher-than-expected costs; the regulatory approval environment; reorganization or restructuring of Occidental's operations, not successfully completing, or any material delay of, field developments, expansion projects, capital expenditures, efficiency projects, acquisitions or dispositions; uncertainties about the estimated quantities of oil and natural gas reserves; lower-than-expected production from development projects or acquisitions; exploration risks; general economic slowdowns domestically or internationally; political conditions and events; liability under environmental regulations including remedial actions; litigation; disruption or interruption of production or manufacturing or facility damage due to accidents, chemical releases, labor unrest, weather, natural disasters, cyber attacks or insurgent activity; failure of risk management; changes in law or regulations; or changes in tax rates. Words such as “estimate,” “project,” “predict,” “will,” “would,” “should,” “could,” “may,” “might,” “anticipate,” “plan,” “intend,” “believe,” “expect,” “aim,” “goal,” “target,” “objective,” “likely” or similar expressions that convey the prospective nature of events or outcomes generally indicate forward-looking statements. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Occidental does not undertake any obligation to update any forward looking statements, as a result of new information, future events or otherwise. Material risks that may affect Occidental’s results of operations and financial position appear in Part I, Item 1A “Risk Factors” of the 2016 Form 10-K.

Use of non-GAAP Financial InformationThis presentation includes non-GAAP financial measures. You can find the reconciliations to comparable GAAP financial measures on the“Investors” section of our website.

Cautionary Statements

3

$9.8

$1.3

$6.4

$1.0

$0

$2

$4

$6

$8

$10

Resources EOR

Wel

l Cos

t ($

MM

)

2014 2016

2016 Performance Exceeded Expectations

• Overall Permian CAGR 10%

> Base management

> Well productivity improvement

• Improved F&D 25%

> Increasing EURs

> Focused development synergies

• Reduced operating expense 27%

> Water management

> Reducing well failures

• Improved well costs by 33%

> Oxy Drilling Dynamics

> Integrated section development

Program F&D Cost*

Operating Expense Drilling & Completion

Production

222

269

0

50

100

150

200

250

300

2014 2016

mbo

e/d

Total Permian

$13

$21

$8

$17

$0

$5

$10

$15

$20

$25

Resources EOR$

/boe

2014 2016

$12

$9

$0

$2

$4

$6

$8

$10

$12

$14

2014 2016

$/b

oe

Total Permian

*Includes improved recovery, extensions, and discoveries related to capital program, no revisions or acquisitions

4

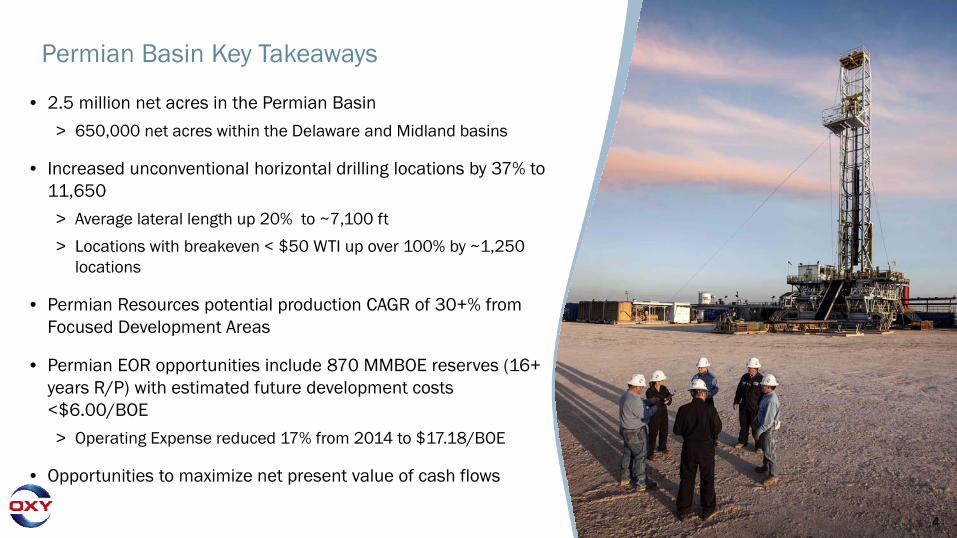

• 2.5 million net acres in the Permian Basin

> 650,000 net acres within the Delaware and Midland basins

• Increased unconventional horizontal drilling locations by 37% to 11,650

> Average lateral length up 20% to ~7,100 ft

> Locations with breakeven < $50 WTI up over 100% by ~1,250 locations

• Permian Resources potential production CAGR of 30+% from Focused Development Areas

• Permian EOR opportunities include 870 MMBOE reserves (16+years R/P) with estimated future development costs <$6.00/BOE

> Operating Expense reduced 17% from 2014 to $17.18/BOE

• Opportunities to maximize net present value of cash flows

Permian Basin Key Takeaways

5

-

50

100

150

200

250

300

350

400

OXY

CVX

PXD

APA

CXO

XOM

XEC

EOG

DVN EC

AEG

NFA

NG

COP PE LPI

APC

KM

ISH

ERID

ANSH

ELL

RSP

PSI

NO

CHEM BH

PW

PXPE

RM

RES

.EN

DEA

VOR

QEP

MTD

RSM NB

LLI

NN

CPE

LGCY EP

EAR

EXSS

UM

YH

ESS

CWEI

REN

CRZO

PER

MIA

N B

ASIN

NET

MB

OEP

D O

PER

ATED

PR

OD

UCT

ION

**

Liquids Gas

Oxy Permian

5

• Largest operated position in the Permian

• Exceptional subsurface characterization

• Proven value based development approach

• Improving through unique technology advancements

• 68% 4Q16 oil production

• Resources – Unconventional Areas 1.4 5,150 124 • Enhanced Oil Recovery Areas 1.1 19,310 145

Oxy Permian Total 2.5MM 24,460 269

Net Operated 2016 NetAcres Wells* ProductionOxy Permian Business Overview

*Gross Oxy operated wells including producers and injectors, and idle wells.**Source: Wood Mackenzie 2016 production, 3/2/17, company NWI% production rates, operators shown represent ~85% of Permian Basin daily production

Permian Basin Industry Production

6

The Permian Drives Oxy’s Value Proposition

DevelopmentCost

Opex G&A ProductionTaxes

Cash Costs

$16 - $19/BOE

Note: Estimated future project costs.

Improving top tier margins with recent operational and technical breakthroughs.

$6 - $12/BOE

DevelopmentCost

Opex G&A ProductionTaxes

Cash Costs

$6 - $10/BOE

$18 - $25/BOE

Permian EOR provides stable, free cash flow with minimal base decline.

~11,650 Undeveloped Drilling Locations ~2B Bbls Identified Undeveloped Resource

Permian Resources Permian EOR

7

Shaping Competitive AdvantageFull Cycle Value

• Unmatched acreage + infrastructure

• Resources – Dynamic Development

• EOR – Reservoir Management

• Subsurface excellence

• People, innovation & entrepreneurial culture

Reservoir Management

Operational Efficiency & Speed

Subsurface Technical Excellence

Field Development Planning + Execution

Enhanced Recovery

8

Permian Resources• Acreage and Inventory Update

• Problems Solved

• Problem Solving Now

9

Permian Resources

Significant acreage& growth potential in all development areas

~650,000 net acres within the Delaware and Midland Basin boundaries

~300,000 net acres associated with 11,650 wells in unconventional development inventory

• NM Delaware Basin 290,000

• TX Delaware Basin 150,000

• Midland Basin 210,000

Total ~650,000

NetAcres*Resources Basin Development Areas

• Central Basin Platform 215,000

• New Mexico NW Shelf 150,000

• Emerging Unconventional 50,000

• Continuing Evaluation 335,000

Total ~750,000

NetAcres*

Other Resources Unconventional Areas

• Resources – Unconventional Areas 1.4• Enhanced Oil Recovery Areas 1.1

Oxy Permian Total 2.5MM

NetAcres*Business Area Acreage

*Includes surface and minerals

NM Delaware Basin

TX Delaware Basin

Midland Basin

Central BasinPlatform

Permian Resources Acreage Permian EOR Acreage

New Mexico NW Shelf

10

Diversified Portfolio Provides High-Return and Significant Flexibility

Asset Portfolio Role Upside Potential

Southeast New Mexico

High return, low capital intensity for near-term growth and cash recycle

Acreage improvement for longer laterals and facilities optimization for multi-bench bench development

Greater Barilla Draw

High return, deep inventory of drill locations, complete infrastructure position

Continued full cycle cost improvement through operational and subsurface synergies from large acreage position

North New Mexico High confidence step-out development areas, replenishment source for high quality inventory

Acreage improvement for longer laterals and development scale. Appraise and delineate additional benches

East Midland Basin

De-risked multi-bench play with mature infrastructure for flexibleshort-cycle growth

Continued acreage improvement to create synergies of large development area

West Midland Basin

Long-term growth potential on large contiguous acreage position with significant flexibility

Technology applications and OBO intelligence to lower project breakeven price

Central BasinPlatform

Conventional low-decline development for long-term growth

Apply unconventional operationalcapabilities and EOR expertise to maximize recovery

North New Mexico

Greater Sand Dunes

East Midland Basin

Central Basin Platform

West Midland Basin

Greater Barilla Draw

2017 – 2019 Focused Resource Development Areas

Permian Resources Acreage Permian EOR Acreage

11

Improved Permian Resources Horizontal Inventory from 4Q2015

• Added 1,250 locations BE < $50

• Added 3,150 total locations

• Increased average length from 5,950’ to 7,100’

• Traded 10,000 net acres to enable longer lateral and consolidated facilities

• 14 years of inventory <$50 breakeven at a 10 rig development pace

0

2,000

4,000

6,000

8,000

10,000

12,000

BE <$50 BE<$60 BE <$70 AdditionalInventory

Total

~5,300

2015 Locations8,500

~11,650~11,650

~2,500

~4,100

2016 Added3,150

Texas Delaware

Basin

Midland Basin

New Mexico Delaware

Basin

Increased Total Horizontal Drilling Locations ~37%

*Breakeven values based on NPV10.

Locations within 300,000 of 650,000 net acres in Basin Development Areas

12*Wells where Oxy is a non-op working interest partner which provides access to all technical data.

New Mexico Acreage is Being De-Risked by the Industry

GOBBLER 5 B2PM STATE COM 1HMEWBOURNEBONE SPRINGLateral Length: 3,98630-day IP: 2,336 BOE/d (80% Oil)

1 5

IRRITABLE 22 STATE COM – 2HDEVONBONE SPRINGLateral Length: 4,17530-day IP: 1,401 BOE/d (74% Oil)

KLEIN 33 FEDERAL COME – 5HCIMAREXBONE SPRINGLateral Length: 6,74130-day IP: 3,351 BOE/d (69% Oil)

NOOSE FEDERAL COM – 9HCONCHOYESOLateral Length: 4,18030-day IP: 848 BOE/d (86% Oil)

STOVE PIPE FEDERAL COM – 2H*CONCHOBONE SPRINGLateral Length: 6,74530-day IP: 2,258 BOE/d (83% Oil)

GEM 36 STATE COM – 1H*EOGBONE SPRINGLateral Length: 4,47130-day IP: 2,314 BOE/d (58% Oil)

THRISTLE UNIT – 30HDEVONBONE SPRINGLateral Length: 9,39330-day IP: 2,199 BOE/d (85% Oil)

2

3

4

6

7

8

1

2

3

45

BLUE JAY FEDERAL 1-HCONCHOBONE SPRINGLateral Length: 4,15830-day IP: 2,258 BOE/d (82% Oil)

6

7

8

Greater Sand Dunes

Permian Resources Acreage Permian EOR Acreage

Source: IHS Enerdeq

13

Permian Resources 2017 Focused Development

• Contiguous Acreage

• Multi-bench

• Capable Infrastructure

• Valuable Growth Greater Barilla Draw – 5,000+ Locations

Greater Sand Dunes – 2,000+ Locations

Permian Resources Acreage Permian EOR Acreage

NM Delaware Basin

TX Delaware Basin

Midland Basin

Central BasinPlatform

New Mexico NW Shelf

14

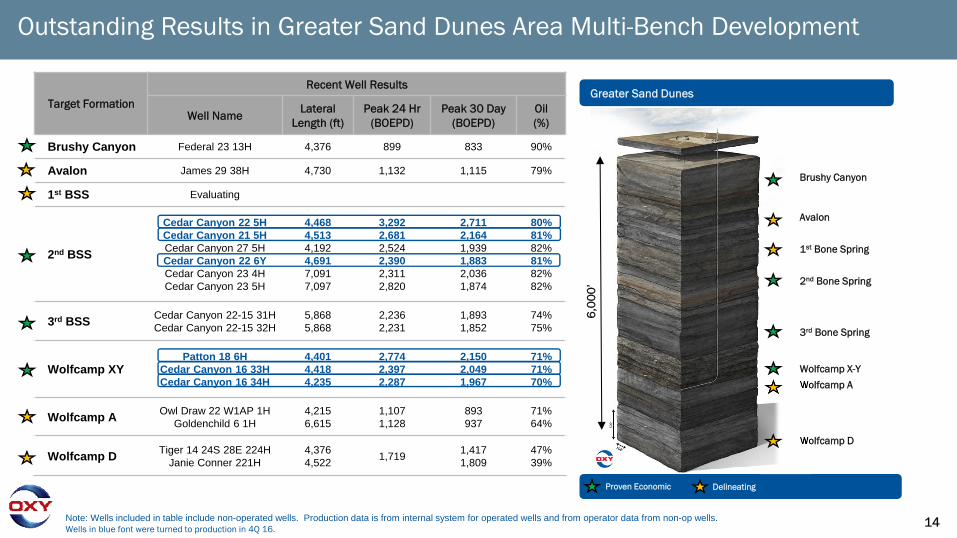

Target Formation

Recent Well Results

Well NameLateral

Length (ft)Peak 24 Hr

(BOEPD)Peak 30 Day

(BOEPD)Oil (%)

Brushy Canyon Federal 23 13H 4,376 899 833 90%

Avalon James 29 38H 4,730 1,132 1,115 79%

1st BSS Evaluating

2nd BSS

Cedar Canyon 22 5HCedar Canyon 21 5HCedar Canyon 27 5HCedar Canyon 22 6YCedar Canyon 23 4HCedar Canyon 23 5H

4,4684,5134,1924,6917,0917,097

3,2922,6812,5242,3902,3112,820

2,7112,1641,9391,8832,0361,874

80%81%82%81%82%82%

3rd BSS Cedar Canyon 22-15 31HCedar Canyon 22-15 32H

5,8685,868

2,2362,231

1,8931,852

74%75%

Wolfcamp XYPatton 18 6H

Cedar Canyon 16 33HCedar Canyon 16 34H

4,4014,4184,235

2,7742,3972,287

2,1502,0491,967

71%71%70%

Wolfcamp A Owl Draw 22 W1AP 1HGoldenchild 6 1H

4,2156,615

1,1071,128

893937

71%64%

Wolfcamp D Tiger 14 24S 28E 224HJanie Conner 221H

4,3764,522 1,719 1,417

1,80947%39%

Note: Wells included in table include non-operated wells. Production data is from internal system for operated wells and from operator data from non-op wells.Wells in blue font were turned to production in 4Q 16.

Barilla Draw Type LogGreater Sand Dunes

Proven Economic Delineating

Outstanding Results in Greater Sand Dunes Area Multi-Bench Development

Brushy Canyon

Avalon

1st Bone Spring

2nd Bone Spring

3rd Bone Spring

Wolfcamp X-Y

Wolfcamp A

Wolfcamp D

6,0

00’

15

Target Formation

Recent Well Results

Well NameLateral

Length (ft)Peak 24 Hr

(BOEPD)Peak 30 Day

(BOEPD)Oil (%)

Avalon Evaluating

1st Bone Spring Evaluating

2nd Bone Spring Roan State 24 #51HAardvark State 6 2H

4,5144,947

9931,254

762821

83%87%

3rd Bone Spring Big George 180 SW 3H 7,576 759 571 57%

Wolfcamp A

Buzzard State Unit #16HPeck State 258 #6H

Buzzard State Unit #15HLenox 2 #5H

Eagle State 28 #13H

7,7004,2127,5984,7214,250

2,0502,2442,0192,4251,958

1,8221,7911,7641,5061,505

74%82%73%71%69%

Wolfcamp DFOppenheimer 188 1H

Nyala Unit 9B #3HOppenheimer 188 2H

Teller 186 1H

4,5006,5754,7764,681

2,4511,5351,5471,707

1,9071,2471,3401,263

82%83%82%81%

Wolfcamp B

Manhattan 183W 1HDaytona Unit 1B 2H

Black Bear State 11 NE #3H

Iron Mike 40 SE 2H

7,0446,9476,935

7,376

1,9541,8971,215

1,703

NA15441,124

1,416

73%79%85%

76%

Wolfcamp C Lemur 24 1H 4,251 1,125 937 81%

Note: Wells included in table include non-operated wells. Production data is from internal system for operated wells and from operator data for non-op wells. Well highlighted in blue is most recent well put online by Oxy from newly acquired acquisition area.

Barilla Draw Type LogGreater Barilla Draw – Drilled 228 Wells Across 8 Benches

Proven Economic Delineating

Improving Results in Greater Barilla Draw Area Multi-Bench Development

Avalon

1st Bone Spring

2nd Bone Spring

3rd Bone Spring

Wolfcamp A

Wolfcamp DF

Wolfcamp C

4,5

00’

Wolfcamp B

16

0

2

4

6

8

10

12

14

16

18

-

50

100

150

200

250

300

2017 2018 2019

Growth Potential of 30+% from Focused Development Areas

• Top-tier well performance

• Deep inventory for range of activity

• Infrastructure to support growth

• Core development areas drive capital efficient growth

• 2017 Capital of $1.0 to $1.4 Bn

Prod

uctio

n (m

boed

)

Multi-Year Permian Resources Growth Potential

Rig

Cou

nt

20% CAGR

30% CAGR

Base rig count* Upside rig count*

6

8

9

*Includes estimated net non-operated rigs

9

1415

17

Permian Resources• Acreage and Inventory Update

• Problems Solved

• Problem Solving Now

18

2014 2017E

2014 2017E

DevelopmentCost

Operating Cost

$7 - $9

Infrastructure

DevelopmentPlanning

SurveillanceBase Management

SubsurfaceCharacterization Stimulation

Design

CustomizedTechnology

Permian Resources Development Costs Per BOE

Permian Resources Operating Costs Per BOE

Problems Solved in the Permian – Adding It All Up

• Cost structure dramatically driven lower since 2014

• Value Drivers:

> Subsurface Characterization

> Stimulation Design

> Customized Technology

> Development Planning

> Infrastructure

> Oxy Drilling Dynamics

> Integrated Planning

> Base Management

DevelopmentPlanning

Infrastructure

$6 - $12

Planning19

Subsurface Characterization Adds Value• Problem: Subsurface uncertainties &

unknowns to predict resource potential

> Sweet spots

> Frac barriers

> Landing zones

• Solutions: Customized subsurface characterization & expertise

> Seismic integration

> Data acquisition

> Models

• Maximize and capture resource potential

Schematic Representation of 2nd Bone Spring Sand Well Placement

2nd Bone Spring Net Sand Thickness and Middle Carbonate Outline

Seismic Interpretation of Middle Carbonate Inside 2nd Bone Spring Sand

A

A A’

Landing + Stimulation + Spacing Optimization

A A’

A’Middle Carb. Outline

Planning20

Subsurface Characterization Adds Value• Problem: Subsurface discontinuity

differentiates stimulation impacts

> Oil left behind

> Frac interference

> Landing zones

• Solutions: Customized subsurface stimulation modeling

> Calibrated stimulation design

> Maximized stimulated rock volume

> Technical type curves

• Maximize economic recovery

Customized Stimulation Design and Landing Selection

2nd Bone Landing and Frac OptimizationA A’

Scenario A B C D

Results21

2nd Bone Spring Optimization ResultsCustomized Technical Excellence Adds Value

0

50

100

150

200

250

300

0 30 60 90 120 150 180

Cum

ulat

ive

MB

OE

4,5

00

ftLa

tera

ls

Days Online

4Q 2016 Wells 1H 2016

Old Design -2014

3Q 2016

2nd Bone Spring Improvements

~150% 6 month cumulative production improvement from old design

• 150% Improved productivity

• Best Bone Spring wells in Eddy Co, NM

• Results continue to improve

1,479

1,227

400

800

1,200

1,600

BO

D

Average normalized 30-day oil peak rate2016 Bone Spring wells, Eddy Co., New Mexico

Peers2016

OXY2016

OXY4Q16

Play Leading Bone Spring Oil Results

Source: IHS Enerdeq and Oxy Internal. Peers listed alphabetically: Bopco, CVX, Cimarex, CXO, DVN, EOG, Mewbourne, WPX. Data normalized to 5,000 ft equivalent.

Planning22

Technology Staircase - Setting The Bar HigherCustomized Technical Excellence Adds Value

Integrated Subsurface Analysis

Stim Design

Drilling Dynamics

+10K Laterals

Single Location Sequenced Laterals –SL2

Play-Leading Wells

Other custom solutions:

• Drilling wellbore design

• Facilities

• Flowback process

• Artificial lift

• Operating maintenance

Planning23

4

4

1

1 1

11

2 22

22

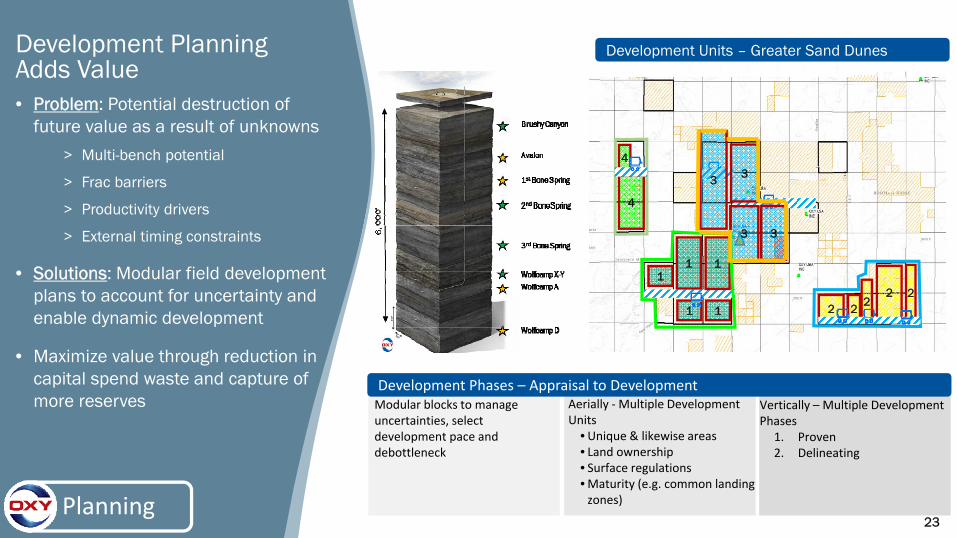

Development Units – Greater Sand DunesDevelopment Planning Adds Value• Problem: Potential destruction of

future value as a result of unknowns

> Multi-bench potential

> Frac barriers

> Productivity drivers

> External timing constraints

• Solutions: Modular field development plans to account for uncertainty and enable dynamic development

• Maximize value through reduction in capital spend waste and capture of more reserves

Development Phases – Appraisal to DevelopmentModular blocks to manage uncertainties, select development pace and debottleneck

Aerially ‐Multiple Development Units

•Unique & likewise areas• Land ownership• Surface regulations•Maturity (e.g. common landing zones)

Vertically – Multiple Development Phases

1. Proven2. Delineating

3

3 3

3

Execution24*BHA = bottom hole assembly

Oxy Drilling Dynamics Adds Value• Problem: Inefficient use of rig

energy resulting in slow and higher cost drilling

> Downhole tool failures

> Wellbore quality

• Solutions: Oxy Drilling Dynamics

> Proprietary Oxy MSE equation

> Reduced drilling days

> Fewer tool failures

> Precision landing

• Maximize value through better time to market and precision landing

Step Changing Performance

Identify Understand Engineer Implement

Bit Vibration

Increase BHA* St i ffness

Pump Pressure

Alternative Dr i l l P ipe

Directional Control

Weight Transfer

Redesign Bi t

Re-Engineer BHA*

Weight on Bit

Rat

e of

Pen

etra

tion

(ft/

hr)

31

22

1612

30%

28%

25%

Drilling Days 7,500’ Lateral(Rig Release to Rig Release)

Real Time Monitoring from Anywhere

Execution25

0

20

40

60

80

100

120

140

Jan Mar May Jul Sep Nov Jan Mar Sep Nov Jan Jul Sep Nov

2014 2015 2016

Expected 2017 range with normalized rig-to-frac ratio

Rig Release to Well Online

Day

s• Implementation resulted in 5,000

production days above the baseline plan.

Integrated Planning Adds Value• Problem: Delay in production and

cash flows due to complex operations and planning

> Multiple unaligned schedules

• Solutions: Implemented Integrated Master Schedule

> Optimized sequence of events reducing “flat time”

• Maximize Value through better time to market and securing pricing and supply of services

• 2017 additions to process

> Increased granularity of well prep, clean-out, and pre-spud activities

> Focus on efficient resources utilization

Execution26

Surveillance and Base Management Adds Value

• Oxy operates 24,460 wells in the Permian Basin

• Company operated production of 235 MboepdNet (EOR and Unconventional)

• Long-term operability is critical

> Well design

> Drilling quality wells

> Artificial lift optimization

> Mechanical integrity

• Oxy finds significant value upside in base optimization

• Oxy can operate large base at low opex

> Offset fixed costs of high well count with operational expertise

-

2.0

4.0

6.0

8.0

10.0

1Q 16 2Q 16 3Q 16 4Q 16

Cum

ulat

ive

Net

MB

OEP

D

2016 Permian Resources Base Optimization

Total Operated Wells

OXY 1 2 3 4 5 6 7 8 9 10 11 12 13

Major and Large Cap Peers

Permian Pure-Play PeersPeers (alphabetical) include: APA, COP, CPR, CVX, CXO, EOG, FANG, LPI, MPI, MTD, PE, RSP, XOM. Source : IHS Enerdeq

27

2014 2017E

2014 2017E

DevelopmentCost

Operating Cost

$7 - $9

Infrastructure

DevelopmentPlanning

SurveillanceBase Management

SubsurfaceCharacterization Stimulation

Design

CustomizedTechnology

Permian Resources Development Costs Per BOE

Permian Resources Operating Costs Per BOE

Problems Solved in the Permian – Adding It All Up

• Cost structure dramatically driven lower since 2014

• Value Drivers:

> Subsurface Characterization

> Stimulation Design

> Customized Technology

> Development Planning

> Infrastructure

> Oxy Drilling Dynamics

> Integrated Planning

> Base Management

DevelopmentPlanning

Infrastructure

$6 - $12

28

Permian Resources• Acreage and Inventory Update

• Problems Solved

• Problem Solving Now

29

0

2,000

4,000

6,000

8,000

10,000

12,000

BE <$50 BE<$60 BE <$70 AdditionalInventory

Total

~5,300

2015 Locations8,500

~11,650~11,650

~2,500

~4,100

2016 Added3,150

Texas Delaware

Basin

Midland Basin

New Mexico Delaware

Basin

Lower Breakeven Cost Through Innovative Problem Solving

*Breakeven values based on NPV10Locations within 300,000 of 650,000 net acres in Basin Development Areas

SS Characterization +Dev. Plans + Technology

Innovation expected to offset cost inflation and move more locations to lower breakevens

30

• Single Location Sequenced Laterals - SL2> Single vertical well bore producing from multiple zones

> Reduce section development cost

> Initial studies and development began mid-2015 with pilot currently underway

> Potential cost impact per well of $0.5 - $1.0 mm

• Subsurface characterization update with data analytics> Identify production drivers

> High-grade inventory and improve field development plans

• Oxy Drilling Dynamics update with analytics > Better wells faster

• Logistics Hubs> Integrated partnerships with service contractors

> Protect margins

Solving Permian Problems NowSL2

Appendix

32

Key Messages

33

Overriding Goal is to Maximize Total Shareholder Return

We believe this can be achieved through a combination of:

• Consistent, annual dividend growth

• Value growth through oil and gas development that meets the following targets:

• Above cost-of-capital returns (ROE and ROCE)

> Return Targets*− Domestic – 15+%− International – 20+%

• Target growth rates of 5% to 8% average per year over the long-term

• Maintaining a strong balance sheet

33*Assumes moderate product prices

Key Message and Strategy

34

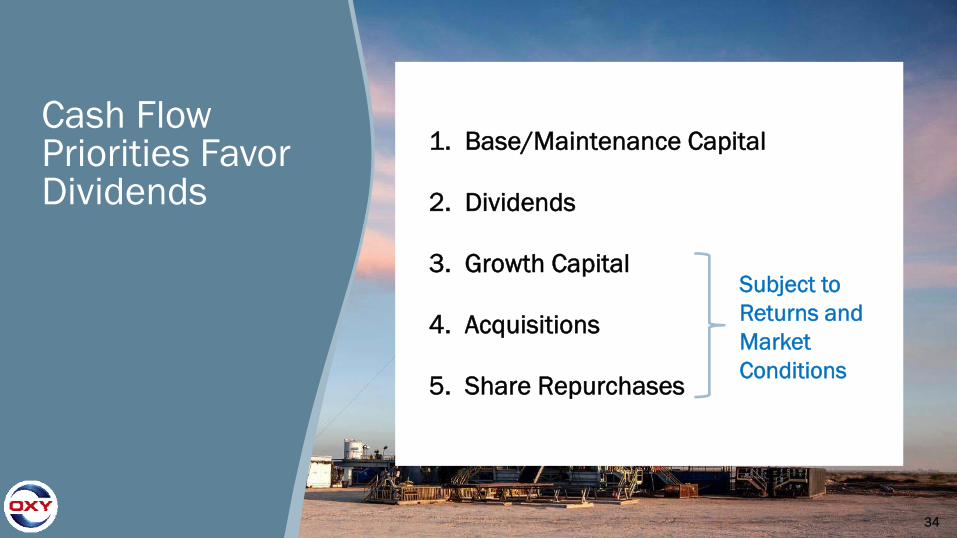

1. Base/Maintenance Capital

2. Dividends

3. Growth Capital

4. Acquisitions

5. Share Repurchases

Subject to Returns and Market Conditions

Cash Flow Priorities Favor Dividends

35

Production GrowthFY 2016

Total Company All-Sources F&D

Permian Resources Production Growth FY

2016

Total Company Reserve Replacement

Ratio

Permian Resources Reserve Replacement

Ratio

7%

290%

189% $9.65

13%$9.00

Permian Resources Program F&D

22%Permian Resources Well

Costs Reduction

25%Permian Resources

Operating Costs Reduction

2016 Highlights

Low-cost Production Growth Exceeds Target

Capital Program Under $3 billion Target

Strong Balance Sheet and Ample Liquidity

Permian Basin Acquisitions Adds Development Flexibility and Cost Synergies

36

Oil and Gas Core Areas

• Leading position in the Permian

• Permian Resources is a growth driver

United States

Latin America• Highest margin operations in Colombia

• Opportunities for moderate growth with partners

Middle East Region• Focus areas – Oman, Qatar, and UAE

• Opportunities for growth with partner countries

Focused Businesses

OxyChem

High FCF, moderate growth business

Midstream

Integratedinfrastructure and marketing business to maximize realizations

37

Oxy Operating adds over $600mm of expected future NPV10

to the Greater Barilla Draw Area

Increased working interest from 26% to 100%

Increased working interest from 26% to 63%

• Increased acreage position to 100,000 net acres & 5,000+ horizontal locations

• Capability to deploy 3 rigs in 2017 and 5+ rigs in 2018+ on acquisition acreage

• Scale allows for operational and subsurface synergies

• Operatorship adds immediate value

– Lower well costs

– Better productivity

– Operating capability

• Unconstrained high value growth capability

*Note: Assumes 5-6 wells per zone per section and future upside potential with downspacing**Note: NPV10 calculation assumes a modest 3 rig pace with $500K/well cost improvement, $0.50 / boe opex improvement and 10% well productivity improvement from the prior operator.

Q4 Acquisition Highlights

Growing the Greater Barilla Draw Area

38

Operating Highlights

39

Production Growth Exceeded Guidance

* Ongoing operations; excludes Piceance, Iraq and Bahrain production volumes* Ongoing operations; excludes Piceance, Iraq and Bahrain production volumes

Total Company Production*

(MBOED)

565

602

2015 2016

~7% Growth Y/Y

110

124

2015 2016

Permian Resources Production

(MBOED)

~13% Growth Y/Y

40

• Internal performance metric to focus on operational efficiency, especially in consideration of the sharp decline in commodity prices

• Significant portion of management and employees incentive compensation is directly aligned with this performance metric

• Focuses on efficiency, improved margins, and free cash flow generation

• Designed to help manage reduction in overall spending while rewarding production growth

Total Spend per BOE = Capital Spending* + G&A + All Operating Costs

Global Oil & Gas Sales Volumes

$40.00

2014 2015 2016

$28.37

~$62.00

2016 Accomplishments - Total Spend per BOE Achieved Target

*Excludes cost of acquisitions

41

2016 Reserve Additions Through Reservoir Performance

~505 MMBOE Reserve Additions prior to price revisionsTotal

Company Reserve

Replacement 2016

189% All In

150% Organic

YE 2015Reserves

Production* Additions Acquisitions& Sales

YE 2016Reserves

2,200 (231)

3462,40691

~77% Proved

Developed

~74% Liquids

All reserves are in Mmboe. *2016 production includes Bahrain and Iraq.

42

• Improved productivity and lower well costs in Permian Resources drive improved profitability

• Pre-tax margins > 50% at $50 / bbl oil prices

Improved Margins in Permian Resources Attracting Investment

DevelopmentCost

Opex G&A ProductionTaxes

Cash Costs

$16 - $19 / boe

Permian Resources Cost Structure

43

• Design and efficiency to secure well costs

• Improving well costs despite increasing stimulation designs> Total Permian Resources reduced cost / 1,000 ft of lateral by 30% from

2015 to $1.07 MM

Lower Well Costs Are Sustainable Through Design and Performance Gains

Oxy New Mexico 2nd Bone Spring Well Cost Improvement

1Q15 Design Performance Market Current Design AdditionalPerformance

Market 2017Target

$8.5+$0.5 -$1.9

-$0.5 $6.6 $0.0 -$0.9+$0.2 $5.9• 1,100 lbs/ft sand

• 16 frac stages• 75,000 bbl Hybrid

• 1,700 lbs/ft sand• 19 frac stages• 165,000 bbl SW

Note: Well cost analysis based on New Mexico 2nd Bone Spring 4,500 type well. Costs include drilling, completion, hookup, initial flow-back, artificial lift, and capitalized overhead.

2017 Focus Areas

• Reduction of drilling non productive time through focused development

• Improve execution of new stimulation designs

• Flowback management

• Produced water utilization for frac

44

Proven Leader in Maximizing Recovery Across the Permian

0

500

1,000

1,500

2,000

Future Development Cost <$6Future Development Cost <$10Additional Unconventional Inventory TotalAdditional Conventional Inventory

Total Identified Barrels

<$10 <$6

Permian EOR Net Resource Potential

MM

BO

E

CO2 Floods

TZ/ROZ*Water Floods +

Other Infill Drilling

Opportunities

High-gradable Inventory

*Note: TZ/ROZ – Transition Zone and Residual Oil Zone

Permian EOR

Significant inventory in 10-year plan

Geographically diverse

100 active CO2 + water floods covering multiple horizons

2 BBOE of identified net resource potential

870 net MMBOE at < $6.00 Future Development Cost

Future Development Cost ($/BOE)

Permian EOR Acreage

Delaware Basin

Midland Basin

Central BasinPlatform

45

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Gro

ss B

OPD

South Hobbs Unit Production and CO2 Flood Forecast

SOUTH HOBBS TARGETS 5 per. Mov. Avg. (SOUTH HOBBS)

Waterflood

Phase 1 CO2Flood

Reservoir Management

$0

$5

$10

$15

$20

$25

2014 2015 2016

$/B

OE

0

100

200

300

400

500

600

2016 TargetCapex

2016 ActualCapex

$M

M

Opex Reduction Capital Efficiency

Downhole Maintenance InjectantSurface, Energy and Other Facilities and Well Work Drilling

12% Reduction Y/Y17% Reduction 2014-2016

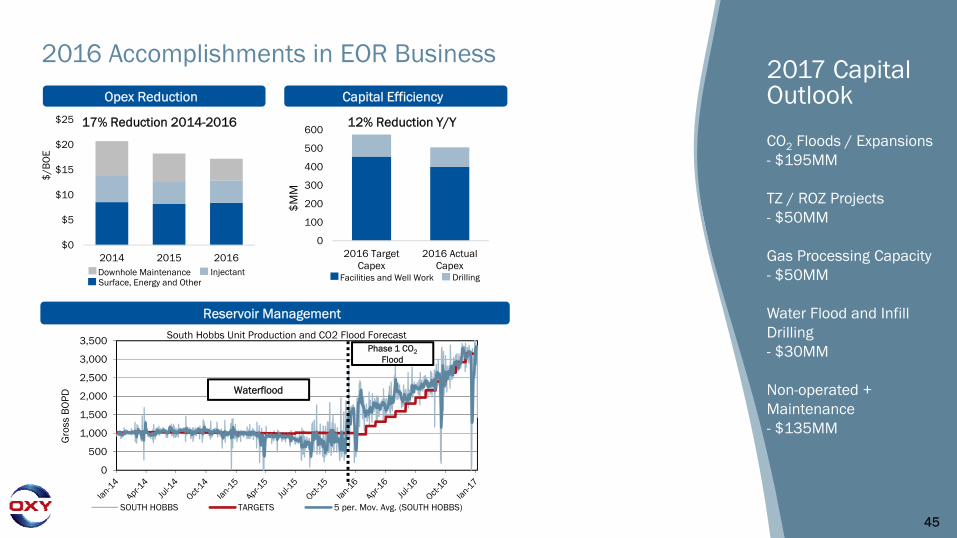

2016 Accomplishments in EOR Business2017 Capital Outlook

CO2 Floods / Expansions - $195MM

TZ / ROZ Projects - $50MM

Gas Processing Capacity - $50MM

Water Flood and Infill Drilling - $30MM

Non-operated + Maintenance - $135MM

46

Corpus Christi

Nederland

Mid‐Valley240 kb/d

McCamey

Crane

Midland

Houston

Wink

ColoradoCity

Ho‐Ho Pipeline

Oxy owned

Oxy is a major shipper

Cushing

HOFTCO Terminal

Ingleside Terminal

• Ample takeaway capacity to reach multiple markets and to drive improved price realizations

• Blending capabilities allow for optimization

Access to Multiple Markets Through Midstream Investments

Execution47

Produced Water FacilityWater Injection

Lea County

Eddy County

Oil Pipeline

2016+ Development Area11 Centralized Tank Batteries4 Disposal Wells2 Compressor Stations2 Frac Ponds

2017+ Development Area34 Centralized Tank Batteries15 Disposal Wells2 Compressor Stations2 Frac Ponds

2016 Highlights 2017 Highlights

• Oil Pipeline with expansion capability

– 30+ mi of pipeline– 90+ Mbopd capacity

• Produced Water Re-cycling Facility

– 36,000 bwpd treatment

• Frac Water Storage– 2 MMbw storage capacity

Infrastructure Adds Value – Greater Sand Dunes

• Integrated SWD System– 100+ mi. of pipeline– 90+ Mbwpd injection capacity

• Gas Compression add– 50+ MMcfpd

• Gas Processing Connections– 4 x 3rd party gas processing

connections in area

48

Shipments from Ingleside export facility

2017 Impact

• Free cash flow expected to improve $150 -$200+ MM due to better marketing economics and ramp up of Ingleside oil storage and export facility

• Ample takeaway capacity and new outlet for Permian oil production

Business Segments

• Gas Plants: Natural gas and CO2gathering, compression and processing systems to control upstream costs

• Pipelines - Domestic: Take-away capacity via common carrier oil pipeline and storage systems, including Centurion pipeline, CO2 source fields and pipeline systems

• Pipelines - Foreign: Stable free cash flow from Dolphin natural gas pipeline

• Power Generation: Lower cost electricity through power and steam generating facilities

• Marketing & Trading: market production at highest realizations; includes Ingleside export facility

Midstream: Improving Cash Flows and Market Access

49

• Ingleside Ethylene Cracker commercial operation in Q1 2017> All systems turned over for commissioning

• 50/50 JV with Mexichem in Corpus Christi, TX> $1.5 Billion for a 1.2 Billion lb/yr cracker, pipeline to

Markham, TX and storage

> 20-year supply agreement with Mexichem

• OxyChem capital spend will continue to decline in 2017> Capital spend for cracker will be reduced from $160 mm in

2016 to $35 mm in 2017

> Growth business spending in 2017 will also include capital for an expansion to a plant in Geismar, LA to produce climate-friendly refrigerants (4CPe)0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016 2017

Maintenance Other Capital Spending New Business Spending

Ingleside Ethylene Cracker – September 2016

$m

mChemicals Free Cash Flow to Significantly Increase

50

Spot Domestic Caustic Soda Price** Low end of price range as reported by IHS

• Caustic soda prices reversed their multi-yeartrend of steady decline in mid-2016

• Global caustic soda demand forecasted to outstrip capacity increases again in 2017

> European mercury technology conversion/closure deadline December 2017

• Higher energy prices will erode some of the impact of higher caustic soda prices

$200

$250

$300

$350

$400

$450

Olin35%

OxyChem24%

Westlake18%

Rest of Industry

23%

North American Chlor-Alkali Capacity Share

• Major industry consolidation iscomplete after several years of M&A activity

• Protracted poor financial performance in the industry is improving market discipline

Basic Chemical Market Dynamics Are Shifting

51

~79% Proved

Developed

~74% Liquids

• Improved Reservoir Surveillance

• Infill and shallow drilling

programs

• 2016 Total Spend per Barrel

reduced by 24%

• Next Generation Drilling Platforms

> Sustainable savings

> No lift barge needed

> Local Construction

> Flexibility of installation

115

120

125

130

135

140

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct

-16

Nov

-16

Dec

-16

Oman - Mukhaizna Gross Production (Mbopd)

ISND

Oman

Qatar

Oman Mukhaizna

Record Monthly Production

Qatar

Well Cost reduced by 30%

52

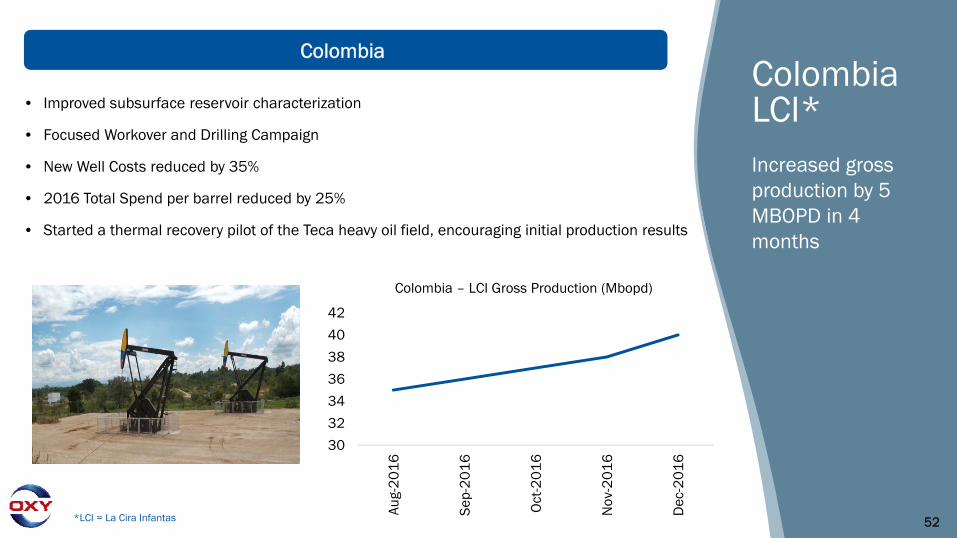

~79% Proved

Developed

~74% Liquids

• Improved subsurface reservoir characterization

• Focused Workover and Drilling Campaign

• New Well Costs reduced by 35%

• 2016 Total Spend per barrel reduced by 25%

• Started a thermal recovery pilot of the Teca heavy oil field, encouraging initial production results

30

32

34

36

38

40

42

Aug-

20

16

Sep-

20

16

Oct

-20

16

Nov

-20

16

Dec

-20

16

Colombia – LCI Gross Production (Mbopd)

*LCI = La Cira Infantas

ColombiaColombia LCI*Increased gross production by 5 MBOPD in 4 months

5353

Al Hosn Gas

• Optimized plant to deliver more capacity

• Completed operational trials

• Minimal capital was required

Al Hosn Gas

Increased Plant Capacity to 110%

2017 production expected to be >70 MBOED net

54

2017 Outlook

55

• Domestic> Increased Permian Resources drilling in SE New

Mexico and Greater Barilla Draw> Short cycle development allows for flexibility to

respond to oil price volatility

• International> Spending levels in Middle East will be flat

• Chemicals > Includes project for manufacturing next-generation,

climate-friendly refrigerants; expected completion by YE 2017

• Midstream> Crude gathering system and intermediate

transportation to support SE New Mexico growth

2017 Capital Plan Will Deliver 4% to 7% Production Growth

$3.0 $3.6

Flexible Capital Program ($ in billions)

International Exploration & Other

Midstream Chemicals

Permian EOR Permian Resources

56

2017 vs 2016FCF Improvement

International O&G ~$400 MMMidstream $150 - $200 MMChemicals ~$400 MMTotal $950 - $1,000 MM

• Improved market conditions, project start-ups and lower capital should increase free cash flow generation in 2017

Free Cash Flow Improvement

57

• Improved product prices> Annualized cash flow changes ~$100 million for a ~$1.00 / barrel change in oil prices

> Annualized cash flow changes ~$45 million for a ~$0.50 / Mmbtu change in natural gas prices

• Improved chemicals performance> Annualized cash flow changes ~$30 million for a ~$10 / ton change in caustic soda prices

> Start-up of ethylene cracker

• Additional sources of liquidity in 2017 - 2018 of ~$2 billion including:> Anticipated tax refund of ~$700 million in 1H17

> Monetization of non-strategic corporate assets

> Portfolio management & optimization

Cash Flow Improvements Expected in 2017

58

Oil & Gas Segment • FY 2017E Total Production

> 625,000 – 645,000 BOED

> Permian Resources production of 140,000 – 150,000 BOED

• 1Q17E Production

> Total production of 590,000 – 595,000 BOED

> Permian EOR production flat

> Permian Resources production of 127,000 – 132,000 BOED

> International production impacted by ~15,000 BOED for turnarounds, PSCs and quota compliance

Production Costs – FY 2017E

• Domestic Oil & Gas: ~$13.00 / BOE

Exploration Expense

• ~$25 mm in 1Q17E

DD&A – FY 2017E

• Oil & Gas: ~$15.00 / BOE• Chemicals and Midstream: $685 mm

Midstream

• ($60) – ($70) mm pre-tax loss in 1Q17E

Chemical Segment

• ~$150 mm pre-tax income in 1Q17E

Corporate

• FY 2017E Domestic tax rate: 36% • FY 2017E Int'l tax rate: 55%• Interest expense of $80 mm in 1Q17E

1Q17 and FY 2017 Guidance Summary

59

• Total production grew 13% year-over-year to 124 MBOED

• Increased activity in 4Q 2016> 16 wells online in 4Q16 vs. 9 in 3Q16> Added 7 top tier performing wells in Greater Sand Dunes

• 1Q17 program: increase in activity expected in 1Q17> 2 rigs added in January 2017> 6 operated rigs drilling primarily development wells> Expect to drill 26 wells and put online 21 wells in 1Q17

• 2017 program: expect 117 wells online> Program will be focused in Greater Sand Dunes and

Greater Barilla Draw, with 2-3 rigs in each on average

Permian Resources Results and Guidance

43 71 77

75

110 124 127- 132

140 - 150

2014 2015 2016 1Q17 2017E

Production (MBOED)

Oil NGL Gas

E