overview - eurasiagroup.net · top risks 2019 eurasia group | 3 bad seeds the geopolitical dangers...

TRANSCRIPT

IAN BREMMER, PresidentCLIFF KUPCHAN, Chairman

12345678910

* -

Bad seedsUS-ChinaCyber gloves offEuropean populismThe US at homeInnovation winterCoalition of the unwilling MexicoUkraineNigeriaBrexitRed herrings

eurasia group | 2 Top Risks 2019

Overview

IAN BREMMER, PresidentCLIFF KUPCHAN, Chairman

The geopolitical environment is the most dangerous it’s been in decades ... and at a moment when the global economy is faring well. Markets are increasingly volatile but resilient, taking hits but mostly bouncing back. What’s wrong with this picture?

Nothing … yet. Geopolitical cycles are slow-moving. It takes a long time to build a geopolitical or-der; governments change course through the workings of complex institutions, coalition politics, election cycles, and checks and balances. Multilateral institutions take decades to build, and they gain momentum slowly. Norms and values need to develop, to become accepted, and to shape institutions and societies over time. Once in place, they’re sticky. And so, barring bad luck (read: a sudden unforeseen crisis), it takes years, even decades to knock down a geopolitical order. That process of erosion is underway around the world today.

Sure, 2019 could turn out to be the year the world falls apart. Tail risks created by bad actors in�icting damage that then create an escalatory cycle are higher than they’ve been at any point since we launched Eurasia Group in 1998. A Russian cyberattack gets out of control. Iran and Saudi Arabia (or Israel) trigger a Middle East war. The Chinese and Americans get into a trade war that causes a deep recession, they blame one another, and retaliation spills into the kinetic space. There are other risks of similar scale. But for now, all of these remain low-likelihood events.

More likely, and despite increasingly worrisome headlines, 2019 is poised to be a reasonably good year. Even, dare we say it, not a particularly politically risky year. But we’re setting ourselves up for trouble down the road. Big trouble. And that’s our top risk.

eurasia group | 3 Top Risks 2019

Bad seeds

The geopolitical dangers taking shape around the world will bear fruit in the years to come. This is the greatest impact of the G-Zero: The world’s decision-makers are so consumed with addressing (or failing to address) the daily crises that arise from a world without leadership that they’re allowing a broad array of future risks to germinate, with serious consequences for our collective midterm future.

Consider the trajectories of all the current geopolitical dynamics that matter. Start with the big ones. The strength of political institutions in the US and other ad-vanced industrial economies. The transatlantic relationship. US-China. The state of the EU. NATO. The G20. The G7. The WTO. Russia and the Kremlin. Russia and its neighbors. Regional power politics in the Middle East. Or in Asia, for that matter.

Every single one of these is trending negatively. Every single one. And most in a way that hasn’t been in evidence since World War II. Indeed, the overwhelming majority of geopolitical developments that matter, the wide array of issues that we follow at Eurasia Group—more than 90% of them—are now headed in the wrong direction.

The overwhelming majority of geopolitical dynamics that matter are now headed in the wrong direction

eurasia group | 4 Top Risks 2019

These relationships and institutions won’t collapse tomorrow, but the risks plaguing them are landmines. That’s especially important because they’re all piec-es of the international architecture, some of them foundational. Eventually, people are going to get hurt. Think climate change, but in the geopolitical sphere.

Let’s take a closer look at several of these bad seeds.

a – US political institutions

It’s not urgent. President Donald Trump has been notably constrained by US institutions—the judiciary slapping limits on his immigration policies, bureau-crats slow-rolling regulatory changes, and Congress focused on incremental approaches to change rather than passing legislation that generates sudden, dra-matic upheaval. Not to mention preventing Trump from taking any measures to impede special counsel Robert Mueller’s investigation. Indeed, a�er two years of the Trump administration, the most important do-mestic takeaways are how resilient US political institu-tions have proven and how e�ectively they’ve limited Trump’s intended actions.

But damage is being done to the legitimacy of demo-cratic institutions in the world’s largest economy. The list of examples is long. Trump publicly contradicts high-con�dence estimates of US intelligence agencies. He claims choices made by lead actors at the Justice Department and the FBI are politically motivated. He insists the judiciary is biased against him and that journalists are enemies of the people.

An overwhelming majority of Americans don’t trust Congress. The political parties have grown further apart, and the political center has disappeared—near-ly half of all Democrats and Republicans now report they “hate” the other side. Social media has further undermined people’s trust in what’s true, and there’s no clear message from government on how large in-formation technology companies should be regulated.

Meanwhile, Trump has weaponized the divisions between his supporters and those who oppose him, transforming governing institutions into political battlegrounds, weakening the long-term functionality of a representative democracy, and persuading a larg-er percentage of citizens that the system is “rigged” against them. If Trump is defeated in 2020, the trend will slow. But American liberal democracy and accom-panying values aren’t what they were. No one can put humpty dumpty back together again.

b – Europe

It’s not urgent. The ongoing Brexit debacle has made clear that nobody bene�ts from an exit. That, in turn, has forced euroskeptic parties like the National Rally (France’s rebranded National Front) and the League (Italy’s former Northern League; why do these far-right parties keep changing their names?) to shi� gears.

But nearly every current trend in Europe weakens the broader European convergence project. Obviously, without the Brits, Europe isn’t what it was. With Chan-cellor Angela Merkel in succession mode, neither is Germany. With President Emmanuel Macron at 23%

eurasia group | 5 Top Risks 2019

approval, facing a state of national emergency and his domestic and European-integrationist reforms a dead letter, there’s a limit to what can be expected from France. Now consider the governments—in Italy and much of eastern Europe—controlled by those who want to assert more national sovereignty to claw back power from Brussels. Add a more divided European parliament a�er May elections (please see Top Risk #4), and Europe is headed toward (at best) a more fragmented future or (at worst) a long, slow unwind.

Presuming no immediate unforeseen emergencies, European governments can handle shocks more easily when there’s decent economic growth and money to spend. But when belts must be tightened, �ghts be-come crises. The reason many in the UK voted to leave the EU is that they recognized it wasn’t �t for purpose over the long term. On that count, they look to be right.

c – The system of global alliances

It’s not urgent. The US remains a critical ally for most of the world’s developed nations. And it isn’t going home this year.

But US alliances everywhere are weakening. Trump has said it’s not America’s job to police the world and other nations must pay for their own security. Trump’s views on trade are decidedly unilateral. And the US has stepped well back from promoting common val-ues; indeed, it’s hard for the US to agree what Ameri-can values are. On all three fronts, the Trump admin-istration sees alliances as corsets that restrict the US’s

ability to pursue its interests. That means alliances are eroding and will continue to do so. Transatlantic relations are in the roughest shape given challenges on both sides of the Atlantic; in particular, US-Ger-man and US-French relations are deteriorating. That undercuts NATO and the broader international order. Trump’s skeptical view of alliances could well spread next to bases and activity in the Middle East.

Asia is least a�ected. Both Trump and the political es-tablishment remain committed to the region, in large part because of China’s rise. The US-Japan alliance remains strong. But even here, watch South Korea, where Trump would prefer to reduce the US military presence, while continuing to create uncertainty on trade. Trump’s doubts about alliances create opportu-nities for Chinese leader Xi Jinping, Russian President Vladimir Putin, populists in Europe, and others happy to exploit frustration with Washington. This trend will slow if Trump fails to win a second term as president, but the move toward a more modest conception of American power and a weaker set of alliances began well before Trump arrived.

d – Populism/nationalism

It’s not urgent. Aggrieved and disenfranchised popula-tions remain minorities in most developed countries, with less ability to force change than the elites in power. The political “swamp” resists being drained, and most governments continue to allocate resources much as they have over the past several decades.

eurasia group | 6 Top Risks 2019

But these trends are becoming more toxic, especially given the growing disintermediation of labor from capital. The “fourth industrial revolution” is appropri-ately named for its bene�ciaries—it promises more growth and more e«ciency. But for those whose jobs are lost to automation and don’t have the education and training to �nd new employment that demands new skill sets, it’s a post-industrial revolution. They’ll end up part of an expanding group who believe their political systems can’t meet their needs.

These polarizing trends now being politically exploit-ed across the advanced industrial world and in pock-ets of wealthier emerging markets are likely to inten-sify and spread over the coming decade, weakening governments and delegitimizing political leaders as a consequence. Along with the US-China con�ict, this is the risk that will be most frighteningly intensi�ed by the next global economic downturn. We don’t want a repeat of the 1930s.

***

There are others we could add to this list. Xi’s success in consolidating so much power in China is a “bad seed” because it makes decision-making in (what will soon be) the world’s largest economy less predictable and a smooth future leadership transition much more challenging. The �ght among regional powers for dom-inance in the Middle East is set to pose a much larger challenge over time, especially given the reduced value of their oil exports for the global economy. Decentral-ization of control over dangerous technologies—partic-ularly malware, drones, and biological weaponry—is another. Add the continued inadequate and poorly co-ordinated political response to climate change. Those are far more bad seeds than we’ve ever seen geopoliti-cally. We’re not looking forward to the harvest.

eurasia group | 7 Top Risks 2019

US-China

The truce that Trump and Xi struck at the G20 meeting in Buenos Aires last month put a temporary halt to the path of tari� escalation the US and China had embarked on. Yet we remain concerned about the world’s most important bilateral relationship. We’re not confident the trade and economic disagreements will be resolved anytime soon. And something more fundamental has broken in the relationship between Washington and Beijing that can’t be put back together, regardless of what happens to their economic ties.

On trade, it remains to be seen whether last month’s truce can be turned into a longer-term peace. We’re skeptical. The o«cial timeline for negotiations is short (though Trump is likely to extend it). The issue to be resolved is the fundamental nature of China’s economic system—something Beijing is unlikely to compromise on. That makes a comprehensive deal hard to reach, an e�ort to “paper over” dif-ferences hard to sustain.

Further, a deal on tari�s wouldn’t end economic friction between the US and Chi-na. US economic grievances are bipartisan and therefore harder to resolve regard-less of next steps. US and Chinese supply chains and technology cooperation will continue to fragment even if tari� threats recede.

At issue is the fundamental nature of China’s economic system—something it is unlikely to compromise on

eurasia group | 8 Top Risks 2019

The Trump administration is determined to force US companies to reduce their reliance on inputs from China and to limit the transfer of intellectual property, particularly in high-tech sectors and those related to national security. The US will continue to use non-tar-i� barriers as a key tool in this push, including invest-ment restrictions, export controls, �nancial sanctions, and criminal indictments. China will reciprocate with its own non-tari� measures—from its cybersecurity laws to antitrust decisions. Moves on both sides will disrupt �rms and broader industries, increasing costs and decreasing collaboration.

Perhaps more importantly, even if the US and China can resolve their trade tensions, and even if they can keep the economic competition civil, the limited trust that underpins the US-China relationship appears to be gone.

Beijing and Washington have always viewed one another with suspicion. But until a few months ago, both shared a common understanding that it was in both their interests to at least try to keep their relationship as amicable as possible for as long as

possible. That’s changed, especially in Washington. The US political establishment believes engagement with Beijing is no longer working, and it’s embracing an openly confrontational approach. Beijing is less ready to take the gloves o�—partly because it feels China is not ready to challenge the US—but rising nationalist sentiment makes it unlikely that Beijing will ignore US provocations. Structural competition and dangers will shape the relationship—in the tech-nology, economic, and security arenas. Tensions will grow regardless of what happens on the trade issues currently making headlines.

This new competition means areas of discord will be-come more escalatory in 2019. Neither side wants a di-rect military confrontation, but there is a greater chance that an accident—such as a collision in the South China Sea—becomes a full-blown foreign-policy crisis. The two countries in the past have successfully navigated several such near-crises, including the collision between a US spy plane and a Chinese �ghter in 2001. Doing so again would be much harder in today’s climate.

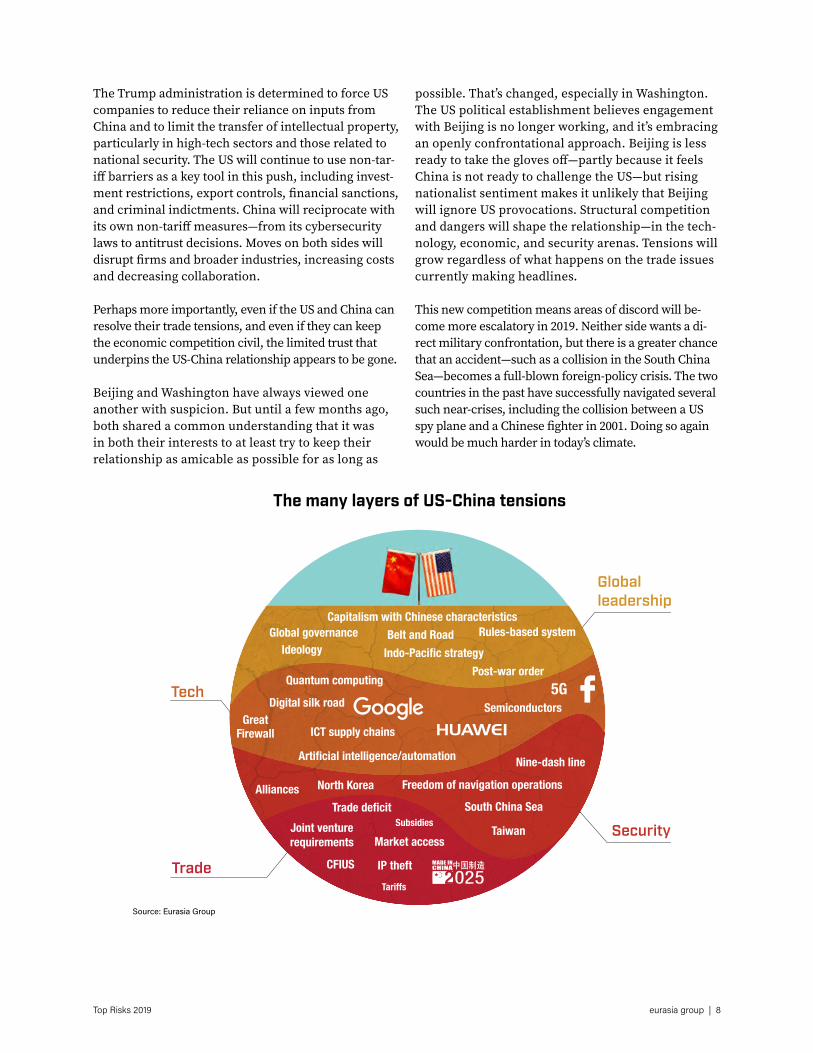

The many layers of US-China tensions

Source: Eurasia Group

Trade

Global leadership

Security

Tech

Joint venturerequirements Market access

CFIUS

Tariffs

Trade deficit

IP theft

Subsidies

Rules-based systemBelt and RoadCapitalism with Chinese characteristics

IdeologyGlobal governance

Post-war orderIndo-Pacific strategy

5G

GreatFirewall

Quantum computing

Artificial intelligence/automation

Semiconductors

ICT supply chains

Digital silk road

Nine-dash line

Taiwan

North Korea Freedom of navigation operationsAlliancesSouth China Sea

eurasia group | 9 Top Risks 2019

Cyber gloves offThis year marks a decade since the US and Israel destroyed portions of Iran’s covert nuclear weapons program using a computer worm known as Stuxnet, ushering in the modern era of cyber conflict. Ten years on, hackers have grown more sophisticated, societies have become heavily dependent on digital services, and e�orts to agree on basic rules of the road for cyber conflict have gone nowhere. It’s a mess.

Cyber deterrence is hard. The source of an attack and lines between state and non-state actors are blurred in cyberspace. That makes it di«cult to be sure whom to retali-ate against, and attackers know that. Also, there is still a lack of clear red lines in many areas, meaning attackers can o�en get away with their misdeeds if they avoid clear no-gos (such as critical infrastructure). Finally, cyber weapons become obsolete fast, and access to targets comes and goes. It’s tempting to use a capability when you can, making the idea of Cold War-style peaceful stockpiling of weaponry less likely.

For the first time, the US will attempt to establish deterrence by projecting its cyber power in more assertive ways

GOTHIC PANDA REAPERFANCY BEAR

eurasia group | 10 Top Risks 2019

So, if cyber deterrence has never come close to actual-ly working, what’s new?

This year is a turning point. For the �rst time, the US will be undertaking a serious e�ort to establish real deterrence by projecting its cyber power in much more assertive ways. Not only will this show of strength fail to create an e�ective system of global deterrence, but it could back�re.

The US is changing its tone—and the doctrine of ac-tion and reaction—to become far more aggressive in the cyber world than it’s been in the past. A�er taking a cautious approach while former president Barack Obama was in o«ce, the US is now leaning heavily to-ward greater o�ensive action in cyberspace, including by freeing the Department of Defense’s Cyber Com-mand to unleash preemptive strikes. It’s even con-sidering giving private-sector actors leeway to “hack back” when attacked.

In an ideal world, this show of teeth would lead for-eign actors to keep their arsenals in check and create a new security equilibrium in which perceptions of US cyber dominance would discourage attacks. That’s not going to work—for two reasons.

First, like traditional deterrence, cyber deterrence works best against states. But many of the world’s most

destructive cyber actors are non-state actors who have less to lose from taking their chances on o�ense. We’re particularly worried that the stolen National Security Agency tools that powered the 2017 NotPetya attacks are being updated for current so�ware systems and have been incorporated into sophisticated cyber operations. Non-state actors’ temptation to use them against critical infrastructure or corporate networks before systems are upgraded will increase in 2019.

Second, even governments won’t back down in reaction to Trump’s assertive cyber policy. In the US-Russia rivalry, it’s unclear which nation controls escalation dominance—the ability of one side to dominate a conflict as it grows more serious—and whether classic deterrence would work. For weaker states such as Iran or North Korea, there’s also an asymmetry of power in the use of cyber weapons that makes them too tempting not to use. Several of the world’s most aggressive cyber powers have little to lose in the event of retaliation, given their low level of connectedness (think North Korea). And for China, the stakes are too high to allow the US sole use of a weapon that works. All of this leads to a scary prospect: The Trump administration thinks it’s strengthening deterrence (and therefore peace) by deploying its arsenal, but the odds are greater that this show of force leads nations to “see and raise” the US’s bet.

UBER 57 million

GOOGLE+ 500K

FACEBOOK 3 million

Source: CFR, Eurasia Group

MARRIOTT 500 million

FEDEX BONGO 119K

UNDER ARMOUR150 million

BRITISH AIRWAYS 380K

TICKETMASTER UK 400K

DIXON CARPHONE 10 million

Major recent data breachesNumber of users a�ected

eurasia group | 11 Top Risks 2019

European populismWhen Macron beat Marine Le Pen in France’s 2017 presidential election, some argued that the populist tide that had swept Europe since the onset of the Greek debt crisis in 2009 could be receding. We were skeptical of that interpretation, and 2019 will show that populists and protest movements are stronger than ever.

The EU will hold parliamentary elections in May, and euroskeptics of the le� and right will win more seats than ever before. The previous election, in 2014, took place shortly a�er the Eurozone crisis, when countries were still going from bailout to bailout. Now, the o«cial message is that Europe is stronger. But the coming victories for parties from outside the European mainstream will be harder to square with a positive story.

The decline of some of the main parties that sit in the European Parliament’s three mainstream blocs opens an opportunity for right-wing euroskeptics to become an imposing force in the parliament—perhaps the second-largest group. Together with populists on the far le�, they won’t reach a majority but will �nd it easier to block initiatives when the smaller majority of pro-Europeans can’t agree. Then, the four populist member-state governments—Italy, Austria, Poland, and Hungary—will all want to make sure they are appropriately represented by a commissioner of their ideological ilk, bringing euroskeptics closer to the commission’s real deci-sion-making power. In short, this year euroskeptics will hold more in�uence than

Right-wing populists have the opportunity to become an imposing force in the European Parliament

eurasia group | 12 Top Risks 2019

ever before in parliament, the commission, and—by virtue of their control of some governments—the European Council.

This unprecedented in�uence will undermine Europe’s ability to function. The presence of euroskeptics within the ranks of the European Commission will undermine that body’s cohesiveness and its ability to manage the EU’s day-to-day a�airs, as well as the clarity of its mes-sage among the European public, investors, and the wider world. The historically collegial institution will become a battleground. Then, with populists in the parliament and the council as well, it will be harder to build consensus on key policy issues, including mi-

gration, trade, and the rule of law. Also, internal dis-agreements will disrupt the EU’s ability to quickly react to crises. If Italy were to face an economic meltdown, or if Europe were hit with a shock from its eastern or southern borders, the presence of populists in Brussels would hamper the EU’s ability to come to the rescue.

The current commission led by President Jean-Claude Juncker believed it represented the EU’s last chance to repair its compact with voters. The new body that will be formed later in 2019 will be in crisis before it even gets to work. This year will be the one when populists gain real power on Europe’s largest stage, eroding the EU from within.

Projected makeup 2019*

Populists will gain seats in European Parliament

63%79%

European Parliament since 2014

PopulistsPro-Europeans

28%72%

37%

*Calculated with reallocated seat numbers following the UK’s departureSource: pollofpolls.eu, Eurasia Group

eurasia group | 13 Top Risks 2019

The US at homeThis will be a chaotic year for US domestic politics. While the odds of Trump being impeached and removed from o�ice remain low, political volatility will be exceptionally high.

With a Democratic majority in the House of Representatives, the president faces adversarial congressional oversight for the �rst time. Democrats will use their control of House committees and subpoena power to force the release of Trump’s tax returns, investigate his �nancial dealings and those of his family, and dig into con�ict-of-interest allegations at several cabinet agencies.

Trump will return �re, further straining relations between the executive, on the one hand, and the courts, Congress, and media on the other. The president’s November spat with Chief Justice John Roberts over “Obama judges” foreshad-ows a �re�ght between Trump and the courts. He’ll launch full-throated attacks on Democratic committee chairs. US institutions—especially the courts—are too strong for the president to e�ectively muscle, but that won’t always be so clear at times this year, as he looks for ways to go a�er those who threaten him, his busi-ness, and his family. In addition, a defensive Trump will try to shi� focus abroad. He’s averse to military intervention, so a “wag-the-dog” type war isn’t likely. But rhetorical and twitter fury are, and markets will be rattled accordingly.

US institutions are too strong for the president to effectively muscle, but that won’t be so clear at times this year

eurasia group | 14 Top Risks 2019

There’s a real risk that articles of impeachment will move forward. Both investigatory routes—congres-sional oversight and Mueller’s probe—could lead to Trump’s impeachment by the Democratic Party-con-trolled House. Articles advanced by the House Judicia-ry Committee would likely include multiple instances of obstruction of justice, violations of the emoluments clause, and potentially, evidence of collusion with Russia during the 2016 election.

Even if Trump is impeached by the House, it’s implau-sible the Senate would convict him with the necessary two-thirds supermajority, particularly since Republi-cans added to their majority in the 2018 midterms. In addition, when articles of impeachment were dra�ed in the past (against former presidents Richard Nixon and Bill Clinton), markets proved resilient. That said, there are reasons to be concerned.

Though Trump’s removal from o«ce is hard to imag-ine, a constitutional crisis that arises following legal action against his businesses or that place his family in jeopardy is not impossible. Trump’s response to such a threat would be to hit back at those who threat-en core interests. He’s been constrained by his advis-

ers from similar actions in the past, but that restraint will be sorely tested if members of his family become targets. We believe the Supreme Court would meet any resulting challenge to the separation of powers, but that’s not guaranteed.

Also, though they’ve been limited in the past, market e�ects from the impeachment process are di«cult to predict. There’s a “Trump bounce” in the US mar-ket that is supporting stock prices; investors would grow jittery at even the possibility of this president’s political demise. And if the news came during a pro-nounced slowdown in the US economy, we could be looking at many months of market instability. Any impeachment process would grind the policy process to a halt, diminishing the already slim chances of Congress making progress on infrastructure spending or immigration reform.

There’s a �nal tail risk. The US could face a renewed bout of street violence like that which plagued many of the nation’s cities during the 1960s and 1970s. American society is already deeply polarized, and the political vitriol and institutional con�ict that’s likely to occur this year could boil over.

What is haunting Trump?

Source: Eurasia Group

TAX RETURNS

THE WALL

IMPEACHMENT

THE MEDIA

MONEYLAUNDERING

REELECTION

DEEP STATEWITCH HUNT

TRUMPTOWERS

TRADE WAR

eurasia group | 15 Top Risks 2019

Innovation winter

A “global tech cold war” was Top Risk #3 last year. Over the course of 2018, technology competition grew extremely political. This is the year investors and markets will start paying the price. We’re heading for a global innovation winter—a politically driven reduction in the financial and human capital available to drive the next generation of emerging technologies. The shortfall will have important consequences.

Three political drivers are behind this global technological mayhem: Security con-cerns are leading states to reduce their exposure to foreign suppliers in areas criti-cal to national security; privacy concerns are leading governments to more tightly regulate how their citizens’ data can be used; and economic concerns are leading countries to put up barriers to protect their emerging tech champions against es-tablished market leaders from abroad.

The most immediate source of trouble is the US-China relationship. Tensions will inhibit synergies, to put it mildly, between US and Chinese policies that have been key to developing advanced technologies. Tari�s are already forcing US �rms to shi� portions of their supply chains out of China—to Southeast Asia, Latin Amer-ica, and in some cases back to the US. The decoupling will accelerate as political and �nancial pressures drive more US production, including potentially complex �nal assembly, to politically safer markets.

Products become more expensive if you can’t source from the most cost-effective suppliers

eurasia group | 16 Top Risks 2019

The countries are parting ways. Equally important, US e�orts to increase scrutiny of Chinese STEM stu-dents and workers, and to limit or reject their US visa terms and applications, will reduce the �ow of cre-ative talent into the US. Likewise, it will limit the �ow back to China of engineers and entrepreneurs with US experience. This trend will disrupt the innovation talent pipeline, with unforeseen ripple e�ects in key technology sectors.

The problem goes beyond US-China relations. The EU and Japan are likely to follow the US in imposing new restrictions. Then there’s the “tech-lash”: Digital regulation is mushrooming around the world as gov-ernments—facing a public backlash over privacy and concerned about foreign in�uence operations waged over social media—slap taxes on Big Tech and restrict the �ow of sensitive information across borders. Brazil, India, and even California have all adopted or are considering legislation that draws on, or in some cases goes beyond, Europe’s tough data protection rules. Data localization is already �rmly entrenched in Russia and China, though for di�erent reasons. Heavy regulation impairs collaboration and innovation.

This US-China technology divorce will create specif-ic problems for companies and markets, which will drain capital from the sector. As US-China tensions persist, �rms will have to spend money to relocate assembly lines and warehouses to countries that don’t

have the same base of highly skilled labor and �nely tuned logistics that have been built up in China over decades. And this is all happening as countries around the world speed toward the rollout of next-generation 5G data networks, a project that will take more than a decade and be one of the most expensive technol-ogy buildouts ever. But a major push by the US and like-minded countries to exclude Chinese 5G equip-ment-makers from their next-generation networks means the process will be more expensive and take longer than it might have. The Chinese government, meanwhile, will require that major Belt and Road investment recipients use Chinese 5G suppliers to the exclusion of others. 5G starts rolling out next year; the political �ght will start now.

More broadly, products become more expensive if you can’t source from the most cost-e�ective suppliers; pro�ts shrink if you can’t sell users’ data to advertis-ers; costs increase if you can’t transfer data across bor-ders and you have to hire more content moderators and lawyers; and dynamism su�ers if you can’t hire the best people because of the name of the country on their passports.

Markets may recognize these trends in isolation, but they’re underestimating how they will come together to cast a pall over global innovation—and call into question lo�y tech industry share prices—in 2019.

Touch-screen controller: Broadcom US

Accelerometer: Bosch Sensortech Germany

Chips for 3G/4G/LTE networking: Qualcomm US

Battery: Sunwoda Electronic China

Wi-Fi chip: Murata US

Battery: Samsung South KoreaLCD screen: Sharp Japan

LCD screen: LG South Korea

Glass screen: Corning US

Audio chips: Cirrus Logic US

Camera: Sony Japan

Touch ID: Xintec TaiwanTouch ID: TSMC

Camera: Qualcomm US

iPhone is poster boy for the tech globalization now under threat

Compass: AKM Semiconductor Japan

Gyroscope: STMicroelectronics SwitzerlandFlash memory: Toshiba Japan

Flash memory: Samsung South Korea

A-series processor: TSMC Taiwan

Source: Eurasia Group

eurasia group | 17 Top Risks 2019

Coalition of the unwilling

The US once led a Washington consensus, a collection of countries committed to a US-led global order and the institutions it was built upon. This order has been eroding for a couple of decades now, a trend that became more obvious with the 2016 election of Trump, whose “America First” campaign message proclaimed his view that the US should no longer play a leadership role. Many of Trump’s critics call this strategy “America Alone.”

But a�er two years, Trump has collected some international fellow-travelers—a coalition of world leaders unwilling to uphold the global liberal order, with some even bent on bringing it down. These leaders form a motley crew, but they have important things in common with Trump. Some are authentic nationalists who used a playbook similar to Trump’s to win an election—for example, Italy’s Matteo Salvini and Brazil’s Jair Bolsonaro. (Depending on what happens to Theresa May, her successor as UK prime minister might belong in this group.) Others have their

These are all leaders who challenge institutions and the consensus they represent ... their ranks are growing

eurasia group | 18 Top Risks 2019

own grievances against the existing global order and �nd a tactical embrace of Trump useful: Russia’s Pu-tin, Turkey’s Recep Erdogan, and even North Korea’s Kim Jong-un.

Finally, a couple �nd US support important enough to their own survival that they must ally with Trump, whatever their personal instincts: Saudi Arabia’s Mo-hammed bin Salman and Israel’s Bibi Netanyahu.

These are all leaders who challenge institutions and the consensus they represent. The group includes international spoilers and revisionists, and their ranks are growing.

Call them the “coalition of the unwilling,” because they won’t form an actual alliance—nationalists don’t salute a common �ag. But for Trump’s impact on foreign policy, which is signi�cantly greater than on

domestic policy, this group of fellow malcontents can act as a force multiplier. That poses a number of risks.

In the aggregate, this coalition will speed the erosion of the international system. Putin and Salvini have be-come more mainstream, and greater acceptance boosts their revisionist goals. All these men are unpredictable, which makes geopolitics and investing riskier. Moham-med bin Salman isolated Qatar, disrupted relations with Canada, and—in the opinion of US intelligence—or-dered the killing of a prominent critic. All were bolts from the blue. Putin’s penchant for the unexpected is also well-documented. And members of this “coalition” all have outsized egos. That means that the need to feed the political base—not the greater good—will play out-sized roles in their decision-making.

Cumulatively, these leaders will have an increasingly disruptive e�ect on the international order.

The motley crew

Source: Eurasia Group

eurasia group | 19 Top Risks 2019

Mexico

Domestic risk factors loom large. The country’s new president, Andres Manuel Lopez Obrador, begins his term with a degree of power and control over the political system not seen in Mexico since the early 1990s. His Morena party has comfortable majorities in both houses of congress, and together with allies, it could reform the constitution at will.

This was always going to be a complicated presidency for markets, and recent actions by the new president have con�rmed our expectations, which leaned more bearish than consensus. Lopez Obrador believes that many of Mexico’s problems today are a function of the structural reforms implemented since the 1980s. These include an opening of the economy, orthodox macroeconomic policies, privatiza-tions, and deregulation. For Lopez Obrador, making Mexico great again is to take it back to the 1960s and 1970s.

During his �rst year, Lopez Obrador will focus on launching his ambitious social and infrastructure programs, at the expense of Mexico’s �scal position. Though he has vowed to be �scally prudent, he’s unlikely to �nd the resources to �nance his proj-ects. He will prioritize this spending anyway, because he sees it as critical to solving many of the country’s problems—including poverty, security, and immigration.

For Lopez Obrador, making Mexico great again means to take it back to the 1960s and 1970s

eurasia group | 20 Top Risks 2019

The operating environment for �rms in the energy sector will become more challenging. Lopez Obra-dor has historically opposed the energy opening and private investment, particularly in the upstream seg-ment, and has nominated a team with highly national-istic views. While a full reversal of the energy reform is unlikely, policy will become more restrictive, and there will be an e�ort to boost the role of state-owned companies. All of this will have a negative impact on production and further worsen the �scal picture.

More generally, policy will become less predictable, more interventionist, and of lower quality—with neg-ative e�ects for markets. Lopez Obrador will central-ize decision-making in his own hands, and the roles of secretaries and advisers will be limited. As was clear with the cancellation of the Mexico City airport project, he will make decisions based on his person-al beliefs and preferences, with moderate advisers having limited in�uence. Lopez Obrador’s Morena

party will also be a source of continual demands and initiatives that will make life di«cult for investors. If the US-Mexico-Canada Agreement isn’t rati�ed by the US Congress (though we expect it will be), risks will be even higher.

Finally, security will be one of the new president’s main challenges, and he lacks a clear strategy to deal with this worsening problem. He will probably con-tinue to rely on the military, coupled with reforms such as amnesty for some drug-related o�enses and the legalization of certain drugs. But that’s unlikely to improve an increasingly dire situation; 2018 was the most violent year on record, and 2019 could easily break that standard yet again.

Until now, Mexico had been in a di�erent political and economic cycle than the rest of Latin America, and in a lower category of political risk. This year, it will look more like its southern neighbors.

4.5

5.0

5.5

6.0

6.5

DecemberNovemberOctoberSeptemberAugustJulyJune2018

Lopez Obrador driving volatility10-year Mexican vs US yield spread

New composition of congress

3 Dec Airport bonds buyback tenderannounced

1 Dec Lopez Orbrador’sinaugration

17 AugLopez Obrador

announcesdetails on

airportconsultation

1 JulLopez Obrador

wins election

25 OctDecision to cancel

airport project announced

24 NovProposal to eliminateprivate pension funds

8 NovInterventionist bankingcommissions initiative

introduced in congress

Morena PESPT MCPRDPVEM PRIPAN Other

Morena and allies (65%)

Morena and allies (59%)

Source: Congress, Bloomberg, Eurasia Group

LOWER HOUSE

SENATE

eurasia group | 21 Top Risks 2019

Ukraine

Contrary to common perception, Putin isn’t always on the lookout for the next country to invade, and he isn’t aiming to start a new war in 2019.

But then there’s Ukraine. November’s clash in the Kerch Strait was a taste of coming tensions. Putin continues to see Ukraine as vital to Russia’s sphere of influence. Their shared historic, political, and cultural links have undergirded Russia’s actions since long before the 2013-2014 Maidan revolution. Putin believes that Russia should have a decisive say in Ukraine’s future.

Against that backdrop, 2019 will be an important year in Ukraine. Presidential elections will take place in March, and parliamentary elections in the fall. Russian interference, to support or undermine particular candidates, is a certainty. There’s not much chance of a pro-Russia president or parliament. But the Kremlin will want to weaken candidates it deems a threat and ensure that advocates for Russian political and business interests have momentum.

There are tense and festering issues between Russia and Ukraine, and they’ll be enmeshed in election dynamics and become more problematic in 2019. Neither government will back down from its position on access to the Sea of Azov and Kerch Strait; additional incidents are likely this year. The status of the separatist

Putin believes Russia should have a decisive say in Ukraine’s future

eurasia group | 22 Top Risks 2019

territories will remain unresolved, and sporadic vi-olence will continue. A major spike in �ghting is un-likely, as that would lead to tougher sanctions against Russia. But given all the dry wood, serious �are-ups are possible.

And there’s the growing split between the Ortho-dox churches in Russia and Ukraine. The Eastern Orthodox church leadership will formally grant the Ukrainian church independence from the patriarch in Moscow in January. There will be disputes over church property and divisions among communities. Related violence is a possibility.

Additional US and EU sanctions are likely over per-ceived Russian interference in the Ukrainian elections and further tensions in the Sea of Azov. The moves will probably entail designating additional Russian individ-

uals and entities for sanctions. If �ghting �ares in and around the separatist territories, severe measures are likely—probably not sovereign debt sanctions, but big-name oligarchs and their businesses would be at risk.

Finally, Ukrainian domestic policy will be in play this year. The presidential and parliamentary elections are likely to yield a reformist, pro-West government, but one that is weak in the eyes of voters, who are distrust-ful of the political class and upset over continued �ght-ing and slow reforms. Martial law ended right before New Year’s and is probably done. Absent a clear and present threat, any attempt to bring it back that delays the March presidential election would touch o� a politi-cal crisis. The IMF program will move forward, helping Ukraine meet its external debt obligations, but reforms will stall at the height of the election campaigns. Ukraine should muddle through, but it won’t be pretty.

Kerch Strait incident raises tensions in Ukraine

Source: Liveuamap

Areas under Russian control

Port

R U S S I A

U K R A I N E

KERCHSTRAIT

AZOV SEA

BERDYANSK

MARIUPOL

eurasia group | 23 Top Risks 2019

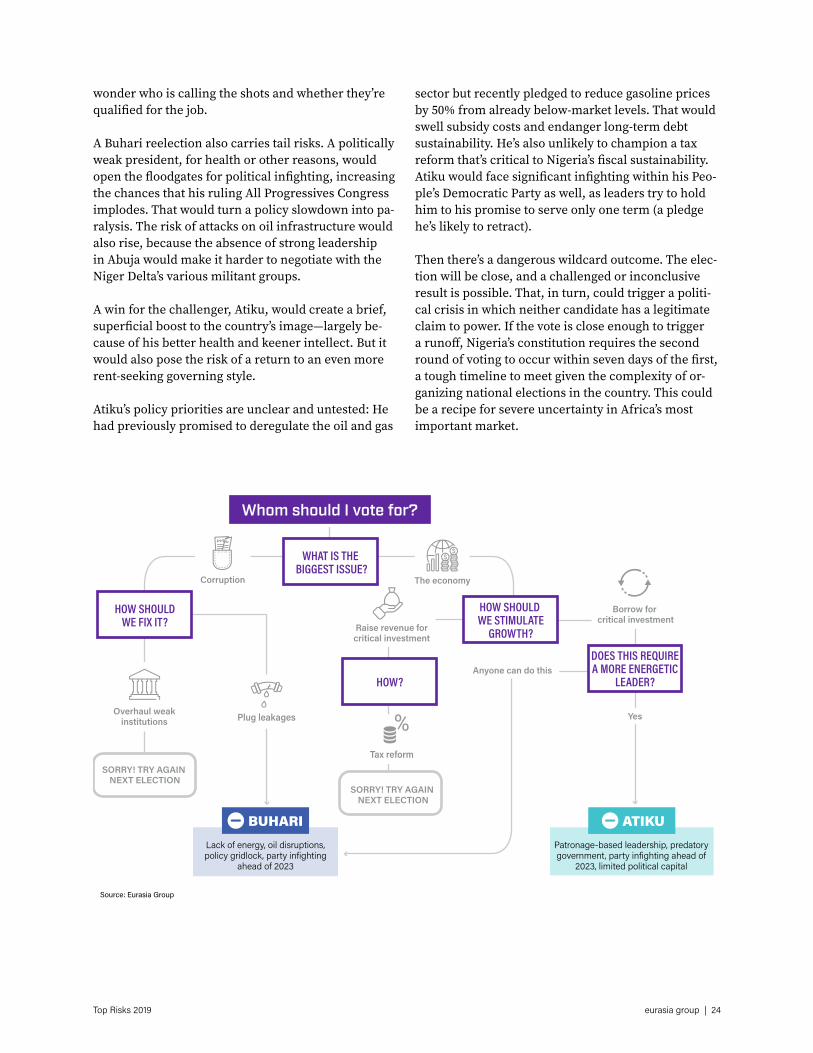

Nigeria

The country faces its most fiercely contested election since the transition to democracy in 1999. One candidate is the incumbent, Muhammadu Buhari. He is an elderly, infirm leader who lacks the energy, creativity, or political savvy to move the needle on Nigeria’s most intractable problems. His opponent is Atiku Abubakar, another gerontocrat who would focus on enriching himself and his cronies, avoiding the di�icult and politically unpopular tasks necessary for reform.

Buhari is the frontrunner. A second term for him would mean the country at best muddles through the next four years, with little progress on critical policy pri-orities like tax reform or a restructuring of the energy sector. Buhari would be a lame duck from day one, with powerbrokers in his own party quickly shi�ing their focus to the next electoral cycle in 2023. And if Buhari’s health problems continue or worsen, the situation will get worse. The president’s continual medical leaves abroad impaired governance his �rst term. A repetition would again remove him from decision-making and the public eye for months at a time, leaving investors to

The election will be close, and a challenged or inconclusive result is possible

eurasia group | 24 Top Risks 2019

wonder who is calling the shots and whether they’re quali�ed for the job.

A Buhari reelection also carries tail risks. A politically weak president, for health or other reasons, would open the �oodgates for political in�ghting, increasing the chances that his ruling All Progressives Congress implodes. That would turn a policy slowdown into pa-ralysis. The risk of attacks on oil infrastructure would also rise, because the absence of strong leadership in Abuja would make it harder to negotiate with the Niger Delta’s various militant groups.

A win for the challenger, Atiku, would create a brief, super�cial boost to the country’s image—largely be-cause of his better health and keener intellect. But it would also pose the risk of a return to an even more rent-seeking governing style.

Atiku’s policy priorities are unclear and untested: He had previously promised to deregulate the oil and gas

sector but recently pledged to reduce gasoline prices by 50% from already below-market levels. That would swell subsidy costs and endanger long-term debt sustainability. He’s also unlikely to champion a tax reform that’s critical to Nigeria’s �scal sustainability. Atiku would face signi�cant in�ghting within his Peo-ple’s Democratic Party as well, as leaders try to hold him to his promise to serve only one term (a pledge he’s likely to retract).

Then there’s a dangerous wildcard outcome. The elec-tion will be close, and a challenged or inconclusive result is possible. That, in turn, could trigger a politi-cal crisis in which neither candidate has a legitimate claim to power. If the vote is close enough to trigger a runo�, Nigeria’s constitution requires the second round of voting to occur within seven days of the �rst, a tough timeline to meet given the complexity of or-ganizing national elections in the country. This could be a recipe for severe uncertainty in Africa’s most important market.

Whom should I vote for?

Source: Eurasia Group

Raise revenue forcritical investment

Borrow for critical investment

Yes

Anyone can do thisHOW?

SORRY! TRY AGAIN NEXT ELECTION

SORRY! TRY AGAIN NEXT ELECTION

WHAT IS THE BIGGEST ISSUE?

HOW SHOULDWE FIX IT?

DOES THIS REQUIREA MORE ENERGETIC

LEADER?

Corruption The economy

Plug leakages

Tax reform

Overhaul weakinstitutions

HOW SHOULD WE STIMULATE

GROWTH?

ATIKUPatronage-based leadership, predatory government, party infighting ahead of

2023, limited political capital

BUHARILack of energy, oil disruptions, policy gridlock, party infighting

ahead of 2023

eurasia group | 25 Top Risks 2019

Brexit

Why the asterisk? Because three years after the vote, almost any Brexit outcome remains possible. The botched leadership challenge protected the prime minister’s rule over the Conservative Party for now but, without her lawmakers’ support, she has almost no chance of passing her unpopular withdrawal agreement. That promises a very messy 2019.

May’s plan to secure a more palatable version of the Northern Irish backstop is doomed to fail. The EU can o�er reassurances that it also hopes to conclude a free-trade agreement in time to prevent the backstop from kicking in. But it will never so�en the mechanism itself, which Ireland regards as its insurance policy.

The prime minister may also think time is on her side. By having delayed the House of Commons vote to January, she hopes a greater number of lawmakers will decide there is no alternative to her deal. But we now know that 117 Conservative members of parliament were willing to risk a chaotic leadership race rather than accept May’s proposal—which she will barely be able to amend. It is highly unlikely that the deal the UK and EU negotiating teams have been working on for almost two years will ever be rati�ed.

There are alternatives, but all of them are painful and time-consuming. Some in the Conservative Party are becoming interested in a “Norway Plus” option, which would see the UK pick an already existing close relationship with the EU’s single market and complement it with a customs union. May could just about manage to justify this arrangement on the grounds that it would be more likely to command a majority thanks to the support of some Labour members of parliament, while also delivering on the mandate from the 2016 referendum to leave the EU.

The obvious counterargument is that this would rule out most if not all of the supposed bene�ts of leaving the EU in the �rst place: regaining regulatory �exibility, having the freedom to strike independent free-trade deals, and—crucially—putting a halt to the free movement of continental labor across the UK’s borders.

That’s where the argument that the UK should just cancel Brexit and stay in the EU resurfaces.

Could May pull o� a referendum? Some ministers think this would be her best way of surviving, but she has also ruled it out more vigorously than any other course of action. The Labour opposi-tion is hedging, hinting at the possibility but still insisting it must come a�er an unlikely general election, which could only be triggered if some Conservative lawmakers vote against their own government and in essence kick themselves out of o«ce.

Brexit promises to keep the UK distracted in 2019. But will there actually be a Brexit? And if so, what �avor? Your guess is as good as the prime minister’s.

eurasia group | 26 Top Risks 2019

Red herrings

A return to dictatorship in Brazil

The election of far-right politician Bolsonaro marked the �rst presidential defeat of the le�ist Workers’ Party (PT) in twenty years and brought a (retired) army o«-cer to power for the �rst time since the 1964-1985 era of military rule. But despite Bolsonaro’s defense of authoritarian practices and his �ery rhetoric against oppo-nents, this is not the end of Brazil’s young democracy.

The new president will not have popular support to aggressively centralize power. He had the highest rejection rate of any elected president in recent history, he’ll have to focus on a laundry list of demands from voters, and he’s far from con-trolling congress—a requirement for amending the constitution.

Brazilian institutions are more decentralized and robust than they were �ve de-cades ago, and they look particularly strong when compared to those of other emerging-market countries. The Supreme Court has entrenched independence; state courts and prosecutors enjoy autonomy; individual governors control police forces; and the media operates freely without strong government oversight. Brazil is not Venezuela or even Turkey.

And, perhaps most importantly, there is no support within the armed forces for taking power. This isn’t the 1960s, there is no “Communist threat,” and most mili-tary o«cers know that running the country would be more hassle than it’s worth.

eurasia group | 27 Top Risks 2019

Saudi Arabia

Mohammed bin Salman is not the most popular man in the world these days, but 2019 will be a better year for him, and for Saudi Arabia, than many would like to believe. International pressure on the young crown prince will not end his bid to become king; he re-mains �rmly in line to take power from his father. The killing of Jamal Khashoggi will convince King Salman to rein in his son and once again include senior mem-bers of the family in the decision-making process, but this will act as a stabilizing factor for the country, not a direct threat to his rule.

Washington and Riyadh will work to contain tensions in their relationship, as each needs the other for the protection of strategic interests. The Trump admin-istration won’t go a�er the crown prince. Regionally, Iran and Saudi Arabia will spar, but each will try to avoid any intensi�cation of their rivalry as both focus on growing domestic concerns. Saudi Arabia will con-tinue to deescalate its war in Yemen and ease tensions with Qatar to placate its Western partners.

Vision 2030 and the domestic reform agenda will face setbacks, as international investors remain reluctant to re-engage too quickly with the Saudi leadership. Domestic spending will increase to ensure that do-mestic pressures on the regime remain under control. However, deep pockets will help the kingdom manage these challenges in 2019.

Iran

Iran is a serious trouble spot in 2019. Faced with severe US sanctions, the economy will contract, in-�ation will rise, and the unemployment rate will in-crease. But the US campaign against Iran is unlikely to trigger a major crisis this year. The nuclear issue will remain on the back burner.

Iran will probably remain in the nuclear deal—and abide by its restrictions—to preserve economic ties with Europe and oil sales to Asia, hoping to run out

the clock on the Trump administration. Even if the country does leave the deal, it will not drastically ramp up its nuclear program. It may tinker with new centrifuges or marginally increase its stockpile of low enriched uranium. But it will be cautious to avoid provoking US or Israeli military strikes. Iran will show resolve by pursuing a tough policy in the region, but pragmatism will limit its aggressiveness.

Most signi�cantly, regime change is not coming to Iran anytime soon. Most Iranians see the regime as legitimate, if deeply �awed. The government is well practiced at sanctions evasion. And the security forces are a �rm backstop to any protest movement that gets out of hand.

Russia-China relations

As Beijing and Moscow face new challenges in their respective relationships with the US, speculation has grown about the prospect for a formal China-Russia alliance. Such a partnership remains unlikely.

True, collaboration between Moscow and Beijing has increased dramatically in recent years. Politically, both countries have an incentive to join forces on pushing back against the US leadership. Economically, each makes an attractive partner for the other: energy for China and external funding for Russia. Russia has emerged as the biggest recipient of China’s Silk Road Fund, and last year China participated in Russia’s large military exercises for the �rst time.

But that’s where the love stops. Deep cultural suspi-cion persists between the two sides. China has little incentive to boost a declining Russian economy. Rus-sia has no desire to become Beijing’s raw materials junior partner. The two share a desire to reshape the global order, but Beijing’s approach is far more incre-mental and collaborative than Moscow’s brash revi-sionism. And while the two countries’ militaries work together, their geopolitical outlooks remain divergent, and they could clash down the road over competing areas of interest, particularly in Central Asia.

This material was produced by Eurasia Group for use by the recipient. This is intended as general background research and is not intended to constitute advice on any particular commercial investment, trade matter, or issue and should not be relied upon for such purposes. It is not to be made available to any person other than the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic or otherwise, without the prior consent of Eurasia Group. Photo credit: Reuters

© 2019 Eurasia Group, 149 Fifth Avenue, 15th Floor, New York, NY 10010

Brasília London New York San Francisco São Paulo Singapore Tokyo Washington D.C.

It’s been 21 years since we started Eurasia Group, and we’ve been through more than our share of global changes together. Taking a moment to look back, we remind ourselves of our modest beginnings, personally and as an organization, and of how much of a privilege it is to have your support.

Thank you for being a part of our community. We appreciate it and wish you only the best for 2019.

—Ian and Cliff