overview of the transition from sor to sora

TRANSCRIPT

Overview of the transition from SOR to SORA

Mikkel Larsen

Managing Director, Group Tax and Accounting PolicyDBS Bank

2

IBOR background materials prepared with the support of Yura Mahindroo, IBOR lead, PwC Singapore

Where we are today…

December 2021 date not delayed

(<350 working days)

Industry priority is COVID-19, but this is not going

away

Increasing regulator focus on interim milestones pre-

December 2021

3

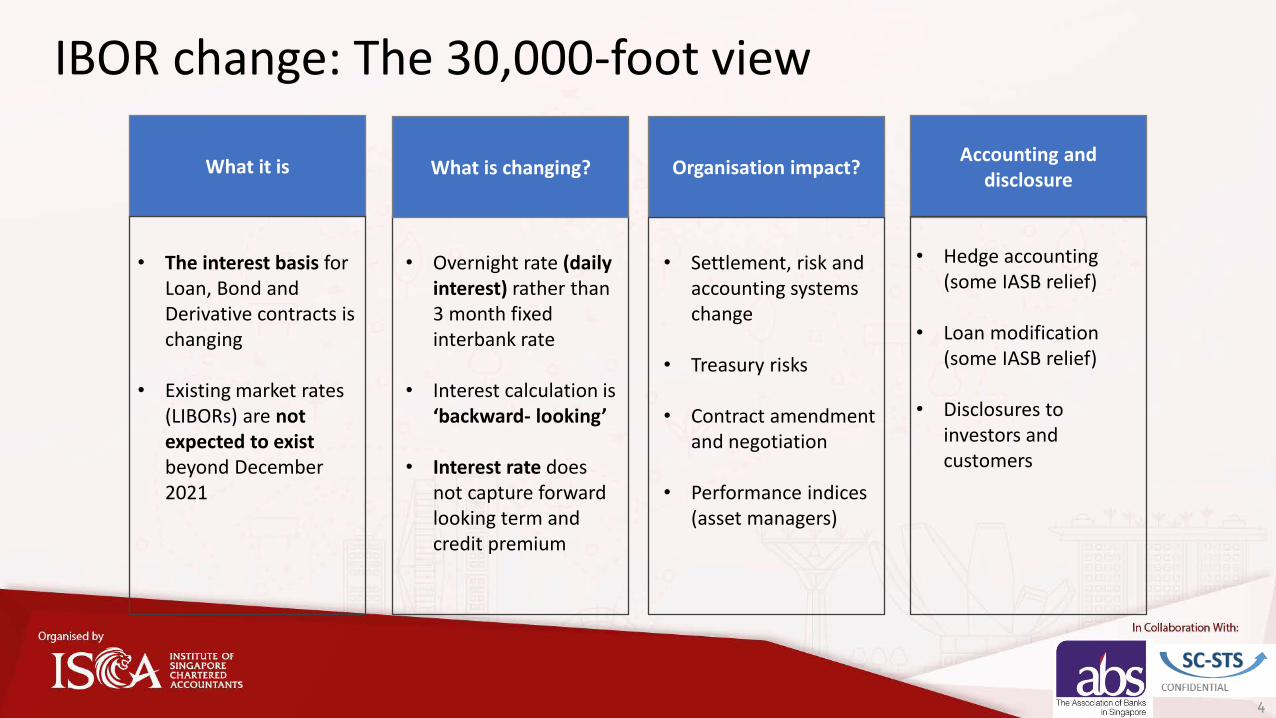

What it is

• The interest basis for Loan, Bond and Derivative contracts is changing

• Existing market rates (LIBORs) are not expected to exist beyond December 2021

• Overnight rate (daily interest) rather than 3 month fixed interbank rate

• Interest calculation is ‘backward- looking’

• Interest rate does not capture forward looking term and credit premium

Organisation impact?

• Settlement, risk and accounting systems change

• Treasury risks

• Contract amendment and negotiation

• Performance indices (asset managers)

Accounting and disclosure

• Hedge accounting (some IASB relief)

• Loan modification (some IASB relief)

• Disclosures to investors and customers

What is changing?

4

IBOR change: The 30,000-foot view

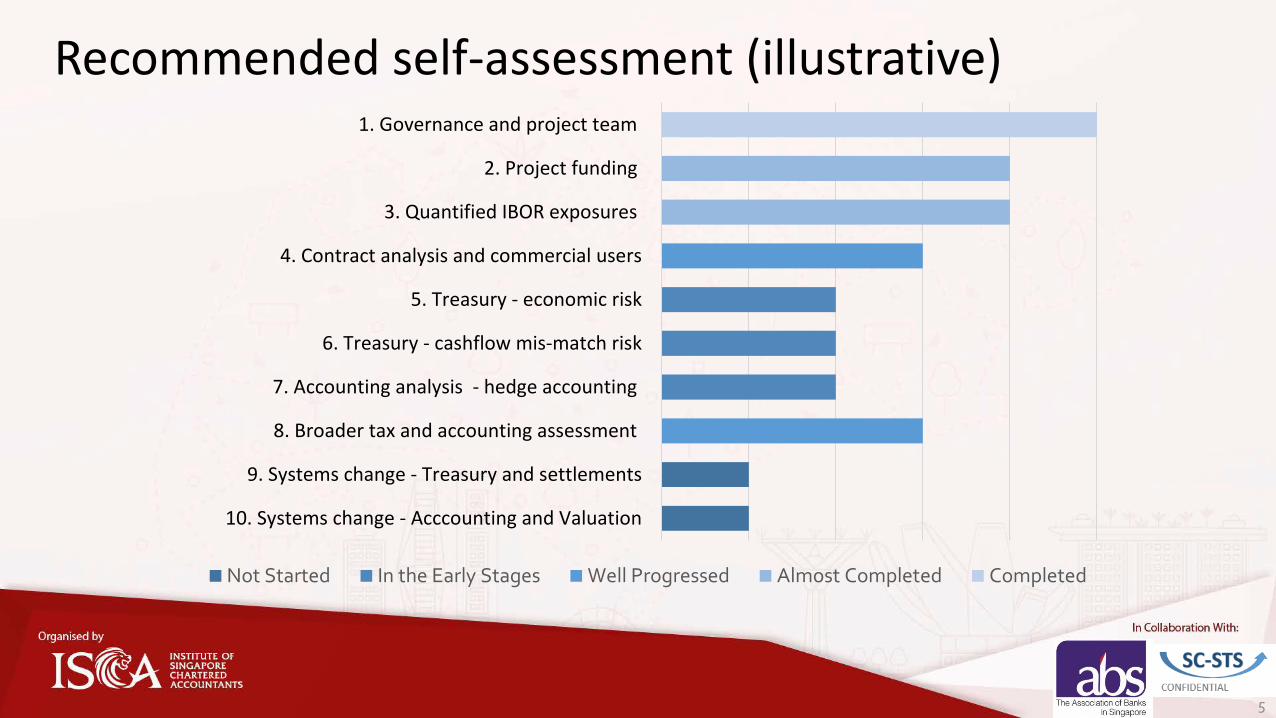

1. Governance and project team

2. Project funding

3. Quantified IBOR exposures

4. Contract analysis and commercial users

5. Treasury - economic risk

6. Treasury - cashflow mis-match risk

7. Accounting analysis - hedge accounting

8. Broader tax and accounting assessment

9. Systems change - Treasury and settlements

10. Systems change - Acccounting and Valuation

Not Started In the Early Stages Well Progressed Almost Completed Completed

5

Recommended self-assessment (illustrative)

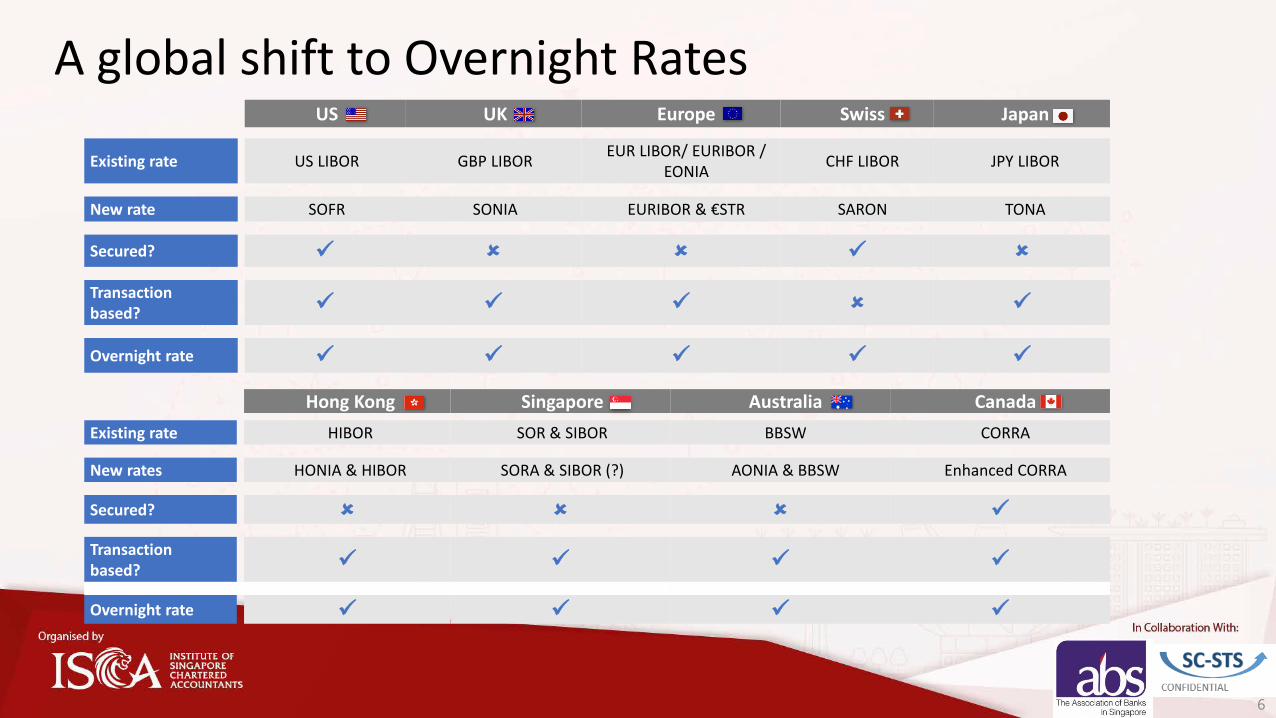

A global shift to Overnight RatesUS UK Europe Swiss Japan

Existing rate US LIBOR GBP LIBOREUR LIBOR/ EURIBOR /

EONIACHF LIBOR JPY LIBOR

New rate SOFR SONIA EURIBOR & €STR SARON TONA

Secured? ✓ ✓

Transaction based? ✓ ✓ ✓ ✓

Overnight rate ✓ ✓ ✓ ✓ ✓

Hong Kong Singapore Australia Canada

Existing rate HIBOR SOR & SIBOR BBSW CORRA

New rates HONIA & HIBOR SORA & SIBOR (?) AONIA & BBSW Enhanced CORRA

Secured? ✓

Transaction based? ✓ ✓ ✓ ✓

Overnight rate ✓ ✓ ✓ ✓

6

7

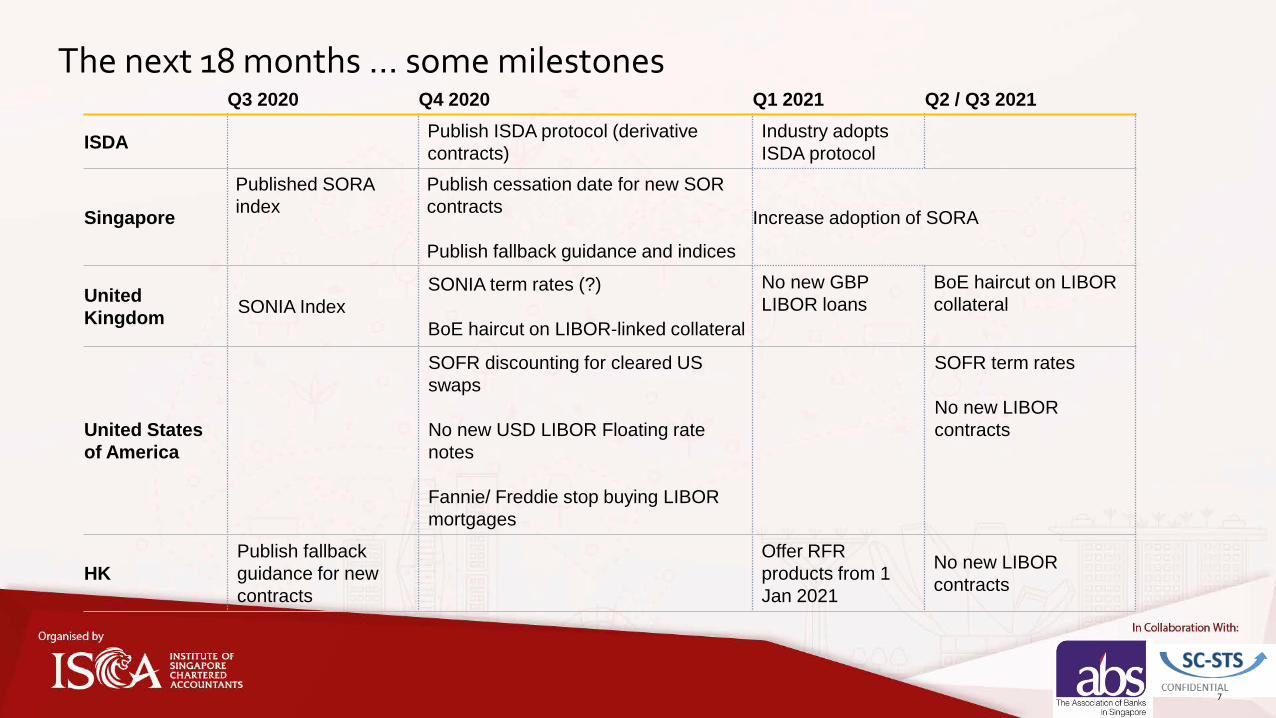

The next 18 months … some milestones Q3 2020 Q4 2020 Q1 2021 Q2 / Q3 2021

ISDAPublish ISDA protocol (derivative

contracts)

Industry adopts

ISDA protocol

Singapore

Published SORA

index

Publish cessation date for new SOR

contracts

Publish fallback guidance and indices

Increase adoption of SORA

United

KingdomSONIA Index

SONIA term rates (?)

BoE haircut on LIBOR-linked collateral

No new GBP

LIBOR loans

BoE haircut on LIBOR

collateral

United States

of America

SOFR discounting for cleared US

swaps

No new USD LIBOR Floating rate

notes

Fannie/ Freddie stop buying LIBOR

mortgages

SOFR term rates

No new LIBOR

contracts

HK

Publish fallback

guidance for new

contracts

Offer RFR

products from 1

Jan 2021

No new LIBOR

contracts

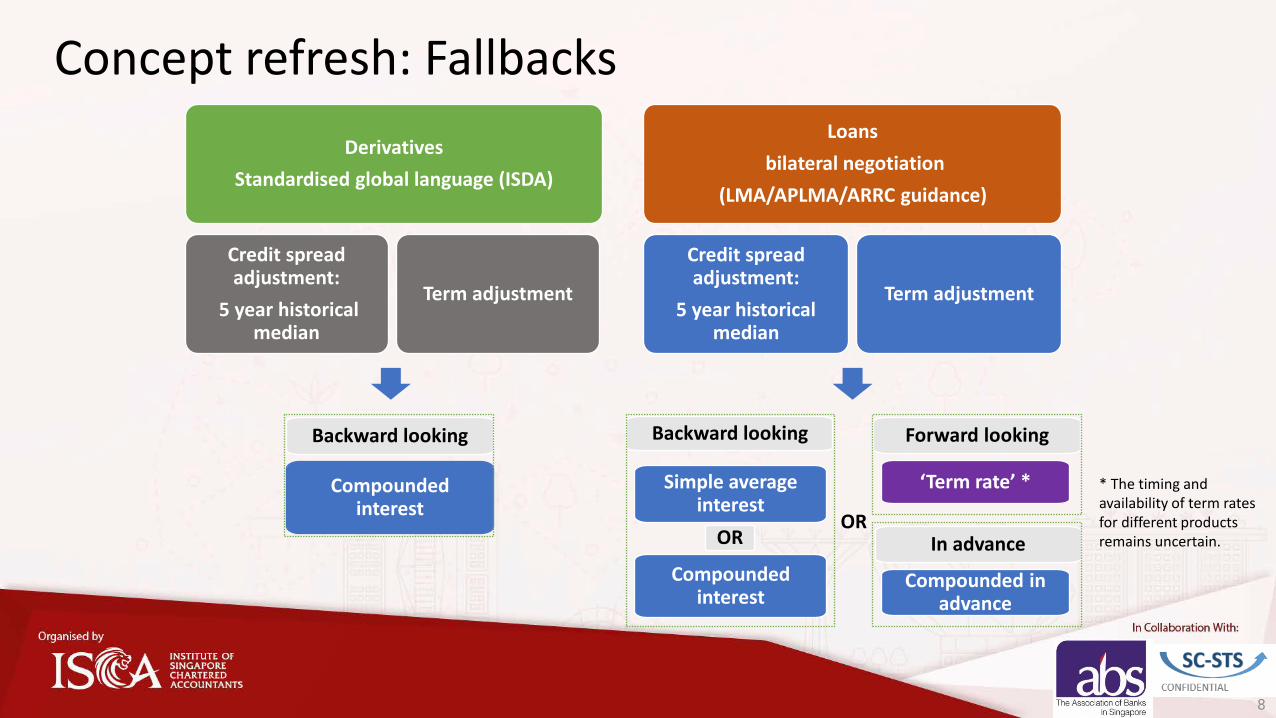

Concept refresh: Fallbacks

* The timing and availability of term rates for different products remains uncertain.

8

Derivatives

Standardised global language (ISDA)

Credit spread adjustment:

5 year historical median

Term adjustment

Loans

bilateral negotiation

(LMA/APLMA/ARRC guidance)

Credit spread adjustment:

5 year historical median

Term adjustment

Compounded interest

Backward looking

Simple average interest

Compounded interest

Backward looking

OR

‘Term rate’ *

Compounded in advance

Forward looking

ORIn advance

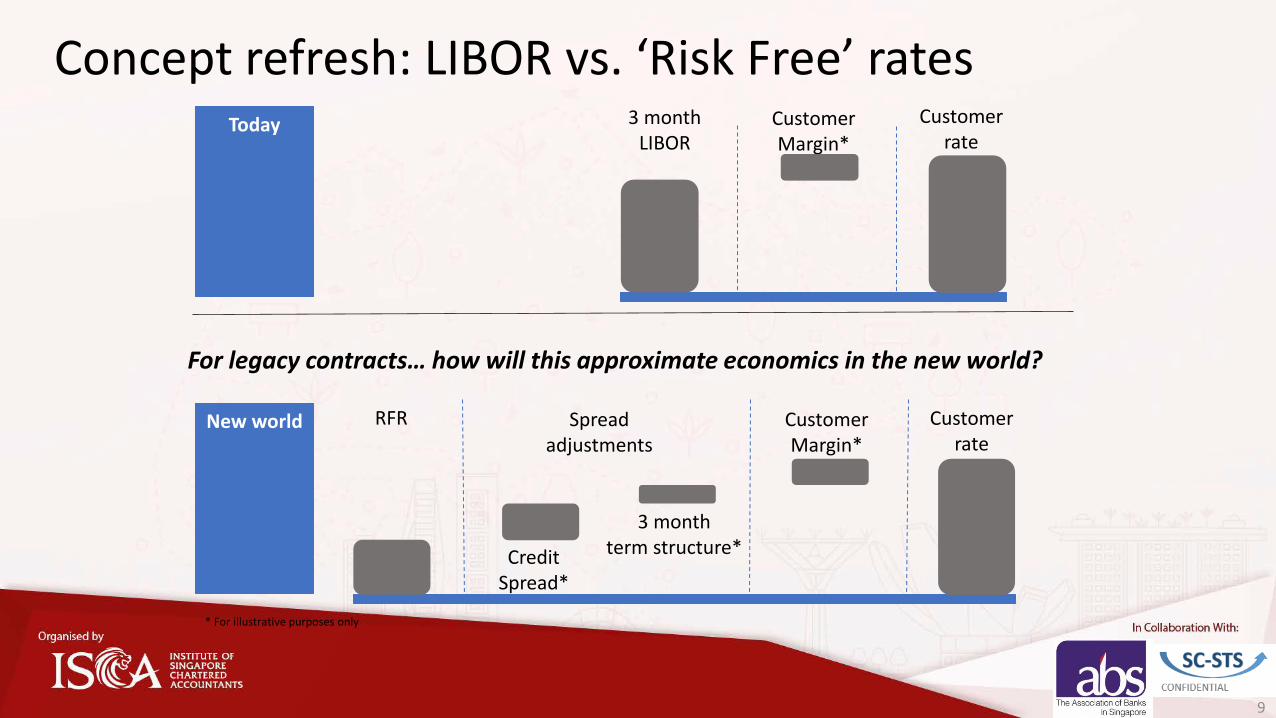

Concept refresh: LIBOR vs. ‘Risk Free’ rates

* For illustrative purposes only

RFR Spread adjustments

Customer Margin*

Credit Spread*

3 month term structure*

Customer rate

New world

Today 3 month LIBOR

Customer Margin*

Customer rate

For legacy contracts… how will this approximate economics in the new world?

9

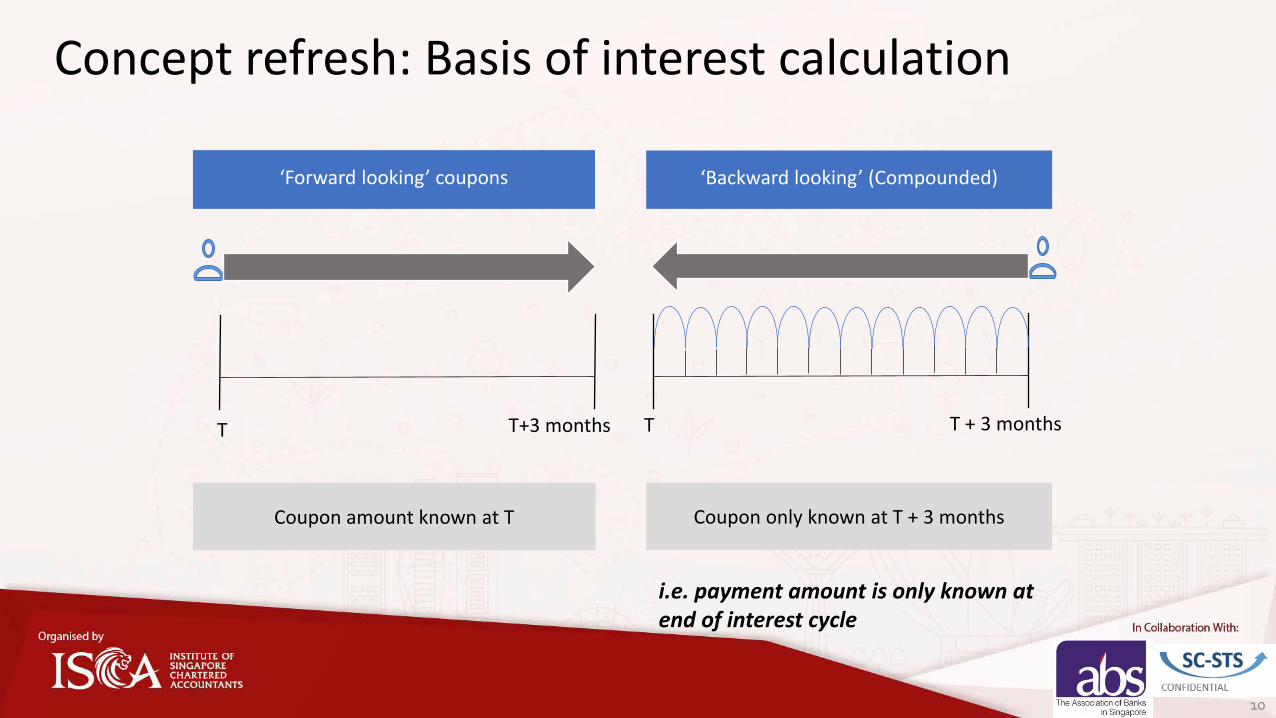

Concept refresh: Basis of interest calculation

i.e. payment amount is only known at end of interest cycle

T+3 monthsT T + 3 months T

Coupon only known at T + 3 months

‘Forward looking’ coupons ‘Backward looking’ (Compounded)

Coupon amount known at T

10

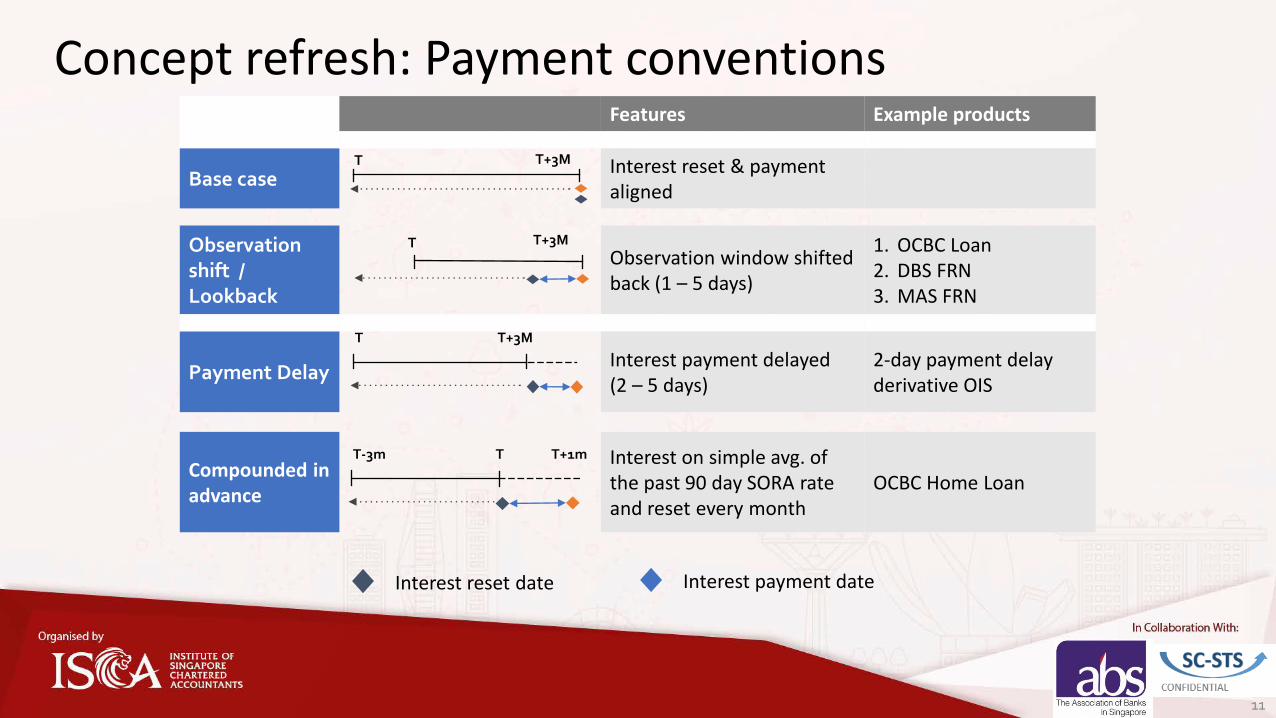

Concept refresh: Payment conventions Features Example products

Base case Interest reset & payment aligned

Observation shift / Lookback

Observation window shifted back (1 – 5 days)

1. OCBC Loan2. DBS FRN3. MAS FRN

Payment DelayInterest payment delayed(2 – 5 days)

2-day payment delay derivative OIS

Compounded in advance

Interest on simple avg. of the past 90 day SORA rate and reset every month

OCBC Home Loan

T+3MT

T+3MT

Interest reset date Interest payment date

TT-3m T+1m

T+3MT

11

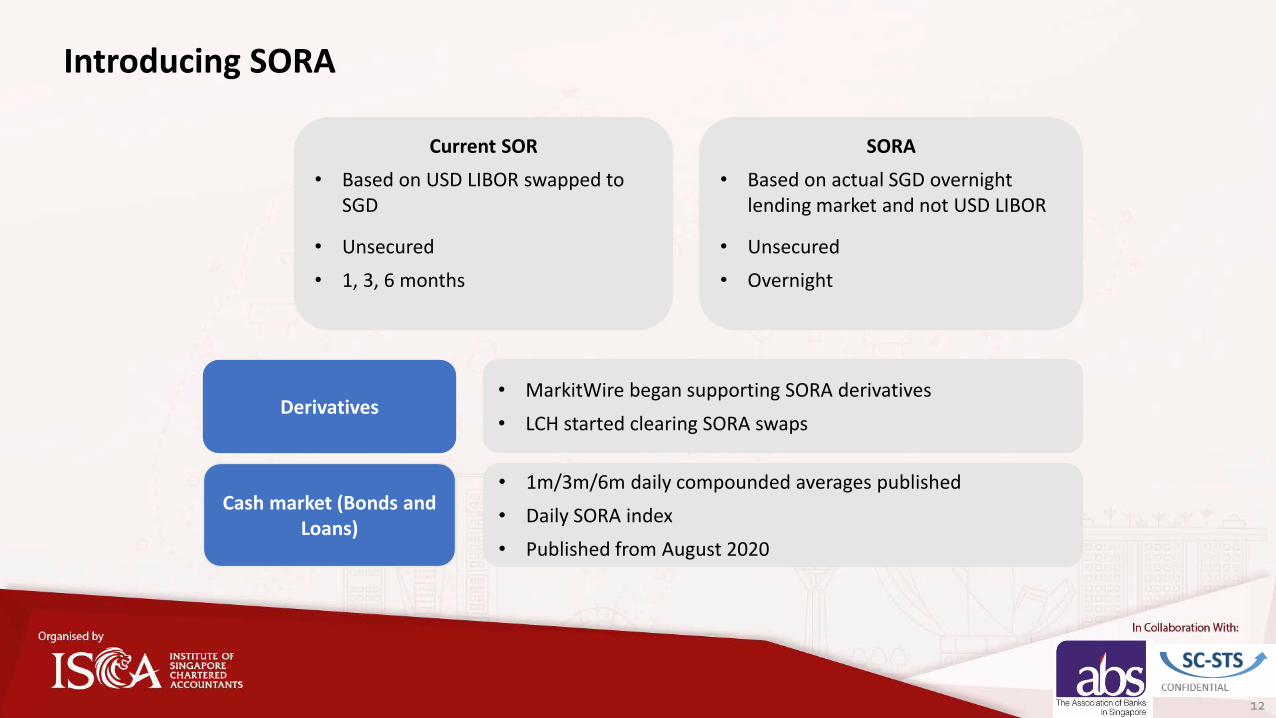

Current SOR

• Based on USD LIBOR swapped to SGD

• Unsecured

• 1, 3, 6 months

SORA

• Based on actual SGD overnight lending market and not USD LIBOR

• Unsecured

• Overnight

Derivatives

Cash market (Bonds and Loans)

• MarkitWire began supporting SORA derivatives

• LCH started clearing SORA swaps

• 1m/3m/6m daily compounded averages published

• Daily SORA index

• Published from August 2020

12

Introducing SORA

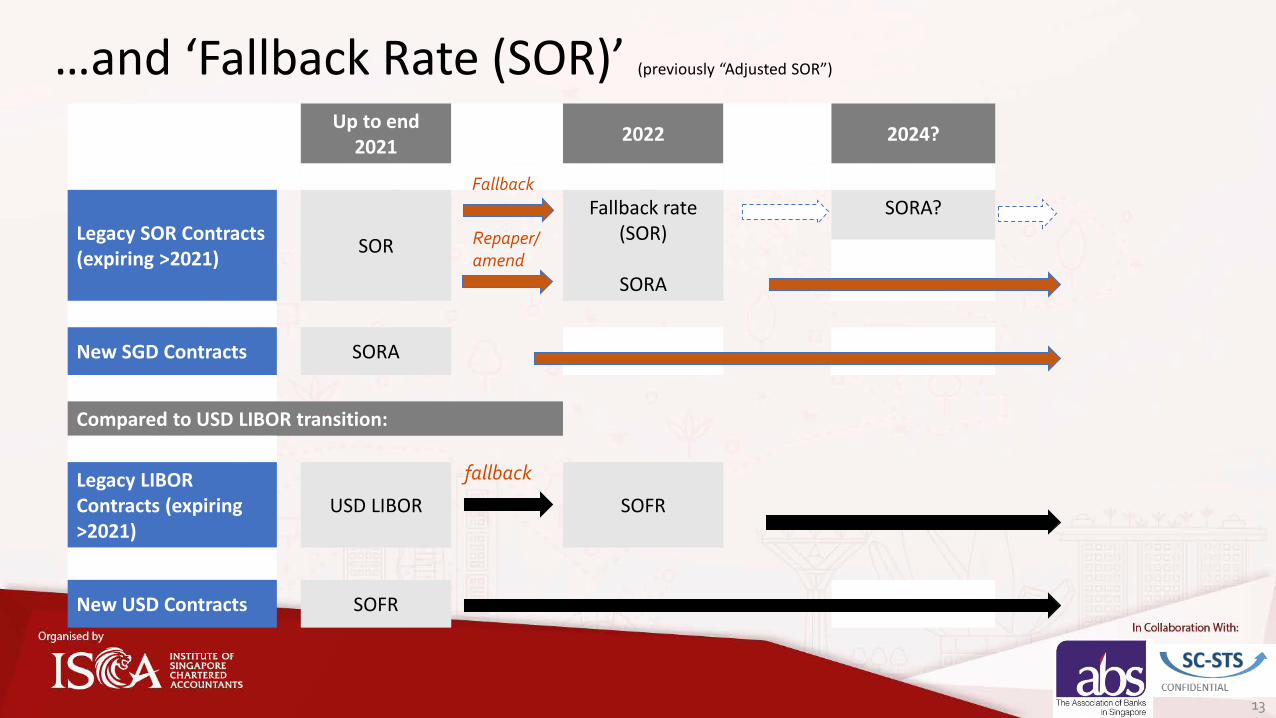

…and ‘Fallback Rate (SOR)’ (previously “Adjusted SOR”)

Up to end 2021

2022 2024?

Legacy SOR Contracts (expiring >2021)

SOR

Fallback rate (SOR)

SORA

SORA?

New SGD Contracts SORA

Compared to USD LIBOR transition:

Legacy LIBOR Contracts (expiring >2021)

USD LIBOR SOFR

New USD Contracts SOFR

Fallback

fallback

13

Repaper/ amend

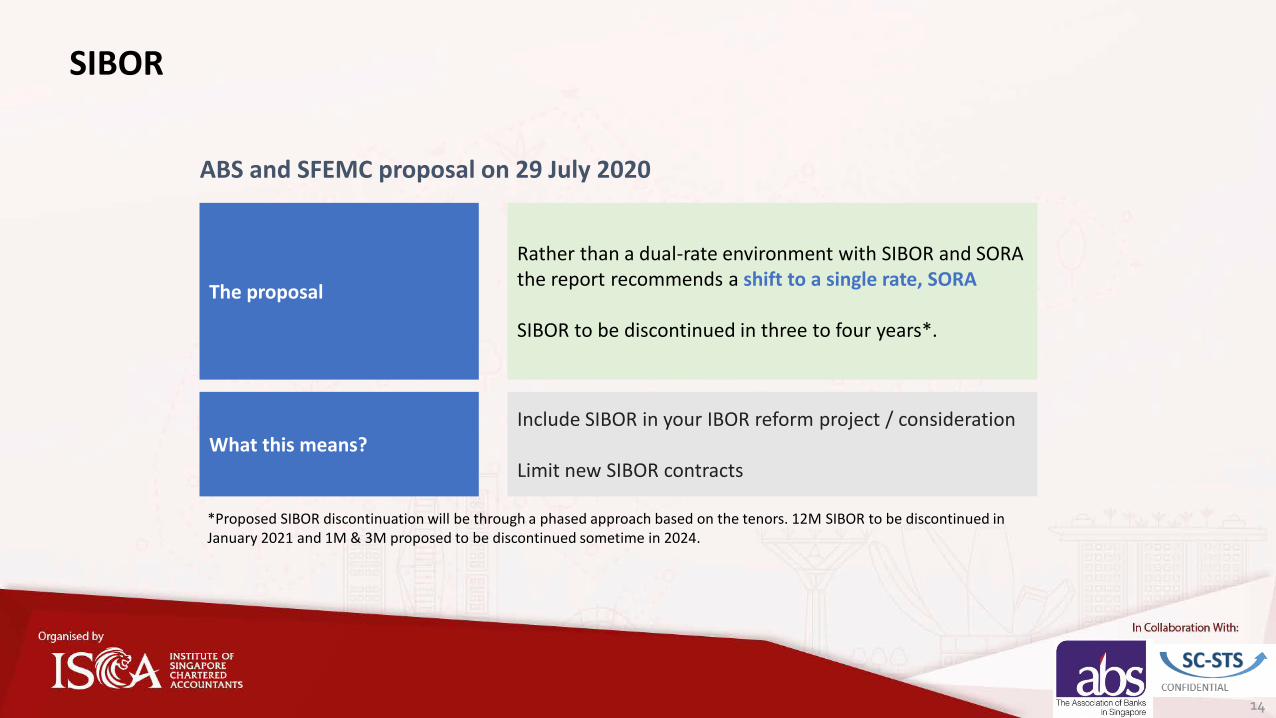

ABS and SFEMC proposal on 29 July 2020

The proposal

Rather than a dual-rate environment with SIBOR and SORA the report recommends a shift to a single rate, SORA

SIBOR to be discontinued in three to four years*.

What this means?Include SIBOR in your IBOR reform project / consideration

Limit new SIBOR contracts

*Proposed SIBOR discontinuation will be through a phased approach based on the tenors. 12M SIBOR to be discontinued in January 2021 and 1M & 3M proposed to be discontinued sometime in 2024.

14

SIBOR

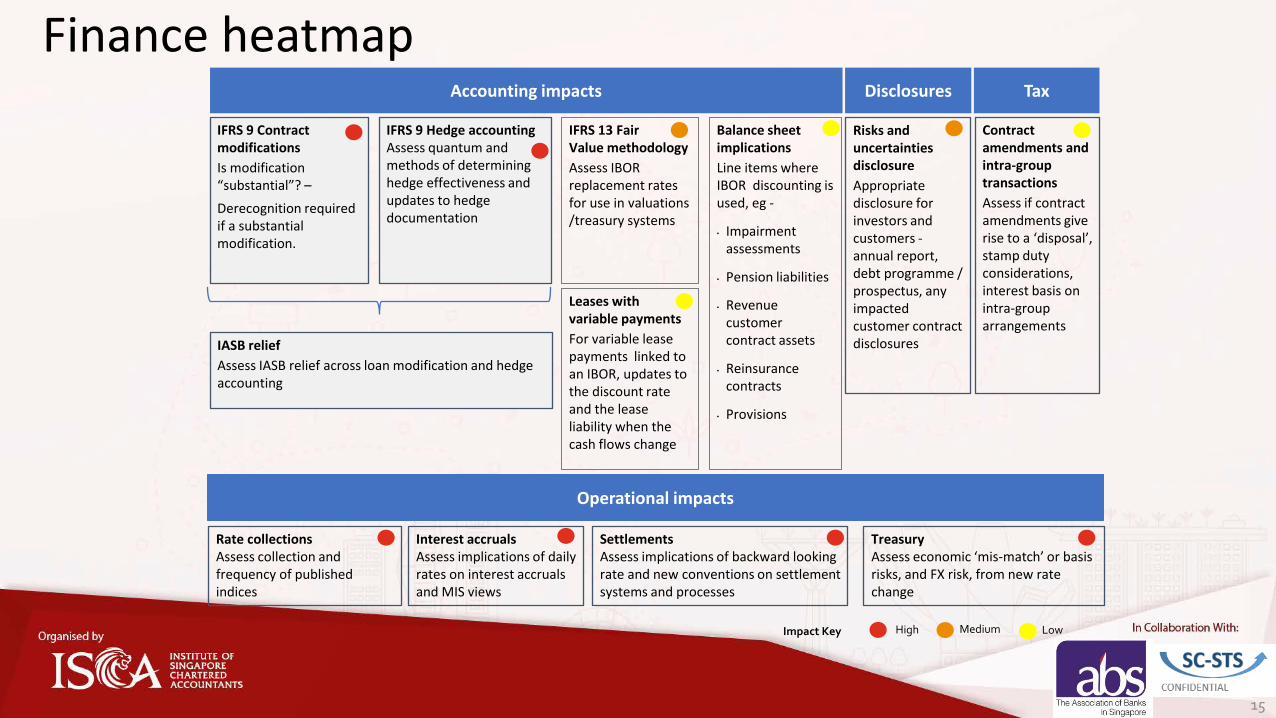

Finance heatmap

Operational impacts

Interest accrualsAssess implications of daily rates on interest accruals and MIS views

Rate collectionsAssess collection and frequency of published indices

Settlements Assess implications of backward looking rate and new conventions on settlement systems and processes

Treasury Assess economic ‘mis-match’ or basis risks, and FX risk, from new rate change

15

Accounting impacts Tax Disclosures

Balance sheet implications

Line items where IBOR discounting is used, eg -

• Impairmentassessments

• Pension liabilities

• Revenue customer contract assets

• Reinsurance contracts

• Provisions

Contract amendments and intra-group transactions

Assess if contract amendments give rise to a ‘disposal’, stamp duty considerations, interest basis on intra-group arrangements

Risks and uncertainties disclosure

Appropriate disclosure for investors and customers -annual report, debt programme / prospectus, any impacted customer contract disclosures

Leases with variable payments

For variable lease payments linked to an IBOR, updates to the discount rate and the lease liability when the cash flows change

IFRS 13 FairValue methodology

Assess IBOR replacement rates for use in valuations /treasury systems

IFRS 9 Contract modifications

Is modification “substantial”? –

Derecognition required if a substantial modification.

IASB relief

Assess IASB relief across loan modification and hedge accounting

IFRS 9 Hedge accountingAssess quantum and methods of determining hedge effectiveness and updates to hedge documentation

Impact Key High Medium Low

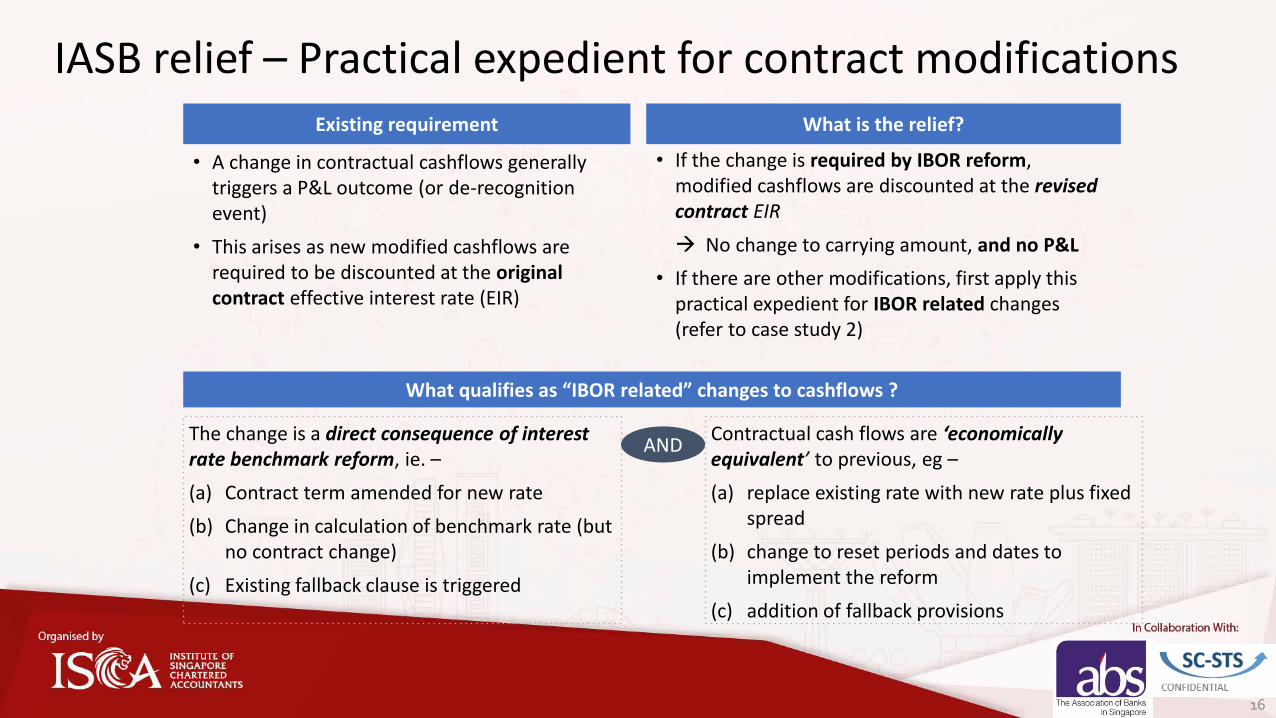

IASB relief – Practical expedient for contract modifications

16

• A change in contractual cashflows generally triggers a P&L outcome (or de-recognition event)

• This arises as new modified cashflows are required to be discounted at the original contract effective interest rate (EIR)

Existing requirement What is the relief?

• If the change is required by IBOR reform, modified cashflows are discounted at the revised contract EIR

→ No change to carrying amount, and no P&L

• If there are other modifications, first apply this practical expedient for IBOR related changes (refer to case study 2)

What qualifies as “IBOR related” changes to cashflows ?

The change is a direct consequence of interest rate benchmark reform, ie. –

(a) Contract term amended for new rate

(b) Change in calculation of benchmark rate (but no contract change)

(c) Existing fallback clause is triggered

Contractual cash flows are ‘economically equivalent’ to previous, eg –

(a) replace existing rate with new rate plus fixed spread

(b) change to reset periods and dates to implement the reform

(c) addition of fallback provisions

AND

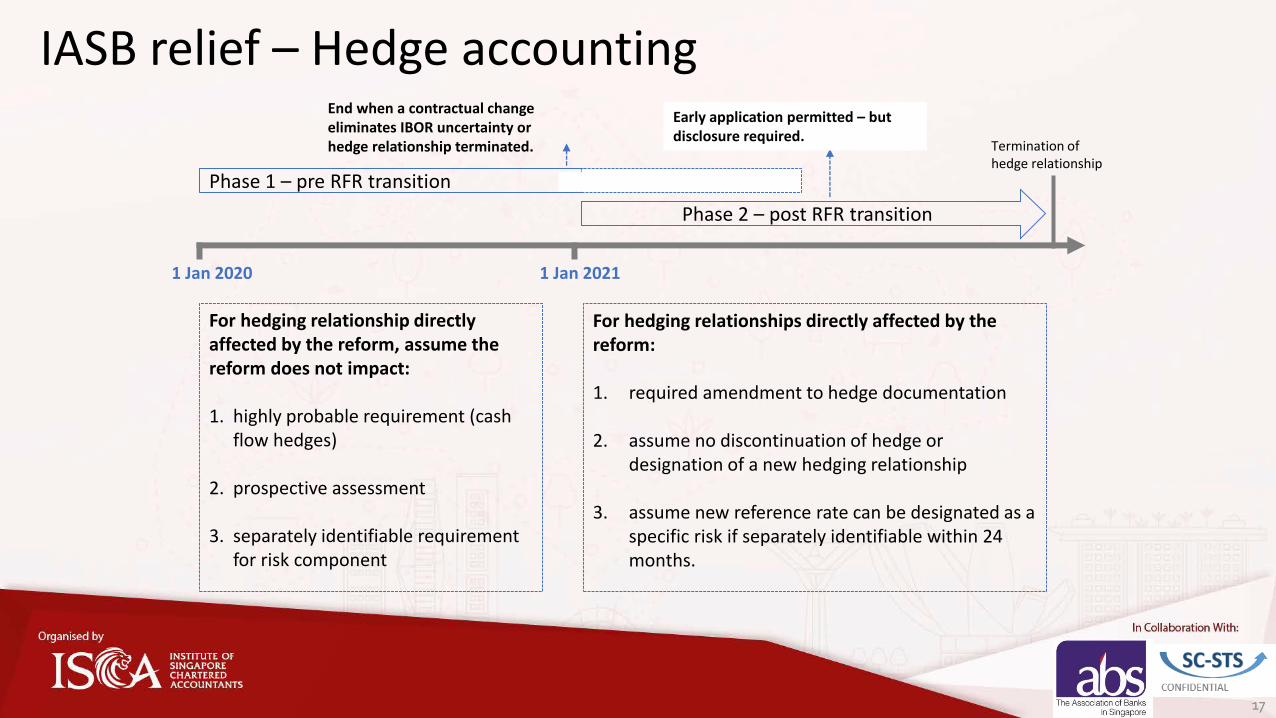

IASB relief – Hedge accounting

Phase 1 – pre RFR transition

For hedging relationship directly affected by the reform, assume the reform does not impact:

1. highly probable requirement (cash flow hedges)

2. prospective assessment

3. separately identifiable requirement for risk component

1 Jan 2020

End when a contractual change eliminates IBOR uncertainty or hedge relationship terminated. Termination of

hedge relationship

For hedging relationships directly affected by the reform:

1. required amendment to hedge documentation

2. assume no discontinuation of hedge or designation of a new hedging relationship

3. assume new reference rate can be designated as a specific risk if separately identifiable within 24 months.

1 Jan 2021

Phase 2 – post RFR transition

Early application permitted – but disclosure required.

17

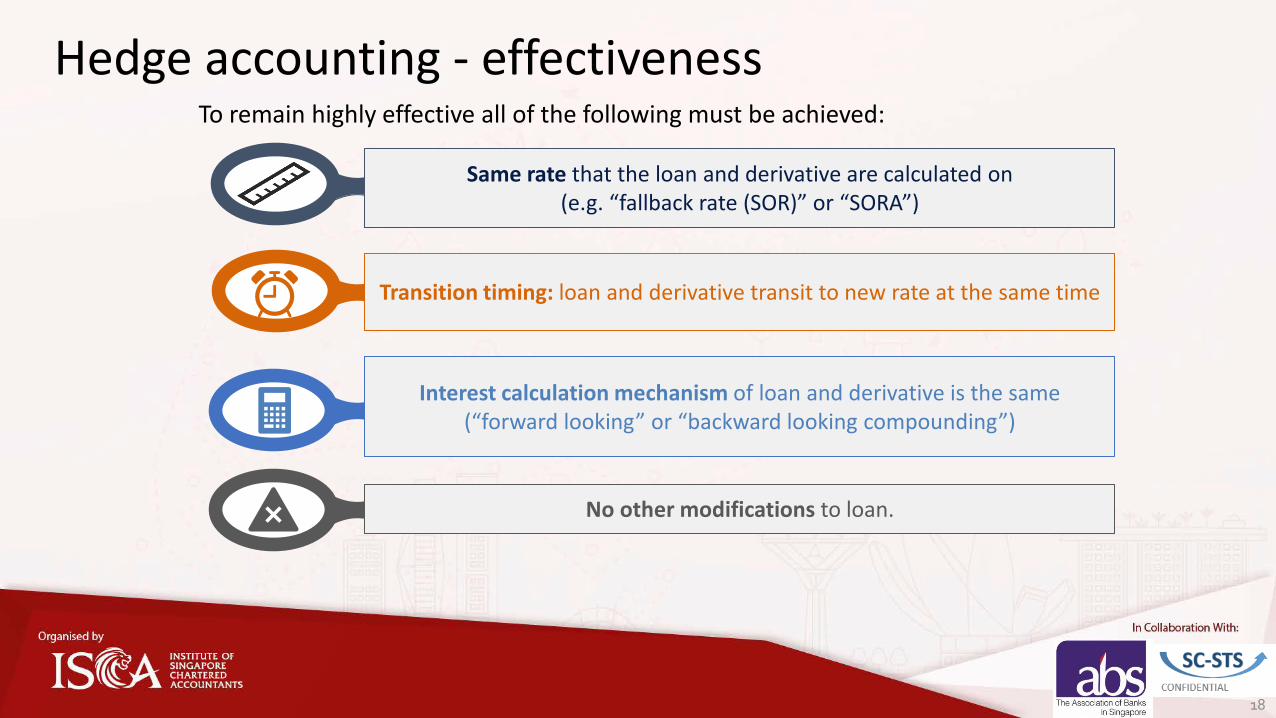

Hedge accounting - effectivenessTo remain highly effective all of the following must be achieved:

Same rate that the loan and derivative are calculated on (e.g. “fallback rate (SOR)” or “SORA”)

Interest calculation mechanism of loan and derivative is the same (“forward looking” or “backward looking compounding”)

18

Transition timing: loan and derivative transit to new rate at the same time

No other modifications to loan.

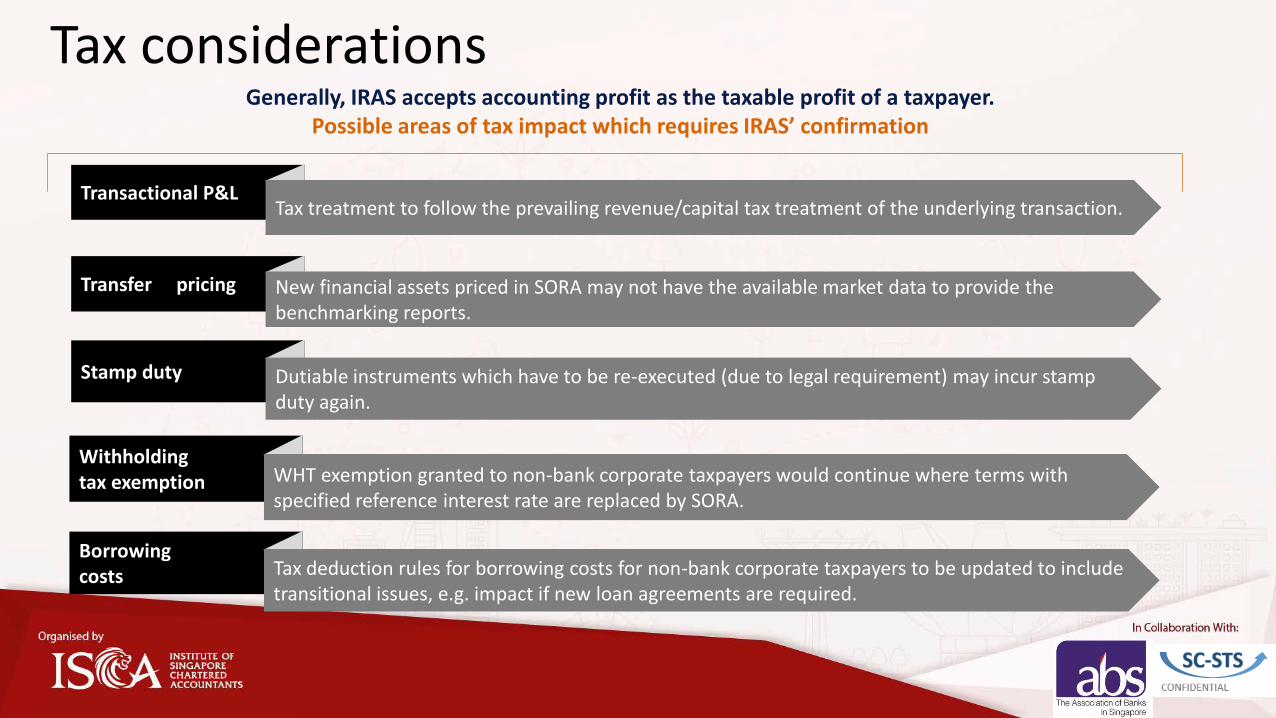

Tax considerationsGenerally, IRAS accepts accounting profit as the taxable profit of a taxpayer.

Possible areas of tax impact which requires IRAS’ confirmation

Transfer pricing New financial assets priced in SORA may not have the available market data to provide the benchmarking reports.

Transactional P<ax treatment to follow the prevailing revenue/capital tax treatment of the underlying transaction.

Stamp duty Dutiable instruments which have to be re-executed (due to legal requirement) may incur stamp duty again.

Withholding tax exemption WHT exemption granted to non-bank corporate taxpayers would continue where terms with

specified reference interest rate are replaced by SORA.

Borrowing costs Tax deduction rules for borrowing costs for non-bank corporate taxpayers to be updated to include

transitional issues, e.g. impact if new loan agreements are required.